51

Prudential Independent Governance Committee’s Report 2018 Enter

Prudential Independent Governance Committee’s Report 2018

Enter

Contents

One page summary for Members 3

Chair report for activities during 2017 111. Introduction 112. Charges 123. Investments 244. Service Levels 305. Communication and Engagement 316. Our 2018 Plans 32

Appendices 33Appendix 1 – What is the IGC set up to do? 33Appendix 2 – Who are the IGC Members? 33Appendix 3 – Summary of the Schemes, Members and Funds under IGC Review 39Appendix 4 – IGC’s Definition of Value for Money (VfM) 40

Shows or hides information

Navigates on the same page

Indicates an interactive function

Navigates to the previous or following page

This document is interactive allowing you to navigate through it and control the information that you want to view. Look out for the following icons:

You can navigate to sections from this Contents page and return to it using the link at the top of each page.

33

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

What we are still working onWe are working on ways to make it easier for you to check on the progress of your pensions saving and to check that you are on track for the retirement you want. To be frank, there is still much to do and we will continue to work with Prudential, your Employer and the Industry. There is no quick fix.

We want to simplify things for you, communicate in a straightforward way, and to encourage you to be more comfortable with your retirement plans.

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement

Click on each segment for more information

44

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Annual Management ChargesAll member borne charges are less than or equal to reference points, and the most frequent charge applied on our default strategy is less than 0.5%.

55

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Investment Performance – ActualGrowth Funds achieve CPI + 3%pa over every period measured.

66

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Investment Performance – vs BenchmarksA mixed set of performance results with around half of Prudential’s investment options outperforming their benchmark.

77

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Investment Strategy DesignDefault Fund Glide Paths are being brought in line with Pension Freedoms. Work is due to complete August 2018.

88

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Transaction CostsAcross all of the IGC funds around 92% have transactions costs (as defined by the proxy measure) of less than 0.20%, which is approximately the same as last year.

99

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Service LevelsAll service levels met barring the speed at which calls are answered.

1010

One page summary for Members

In 2015 the Financial Conduct Authority set up the Independent Governance Committee (IGC) to ensure you get value for money from your pension.

Improvements during 2017In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year.

• Charges have been lowered for everyone

• Investment performance has been strong across almost all funds. Prudential’s flagship default fund, the Dynamic Growth Fund IV, gave returns of 4% more than our long term objective.

• All funds will be changed to allow for Pension Freedoms by August 2018.

IGC’s VfM Framework and Scores for 2017

Key conclusionsOverall, we are very satisfied with the level of charges, very satisfied with investment strategy design and the level of investment performance over 1, 3 and 5 years. Overall service levels are fine.

The major factor in how much pension you can take out, is how much you put in. The value for money from Prudential is now much better than it was three years ago.

Any questions?If you want to know more, please read my report or contact me at [email protected]

Lawrence Churchill CBE Chairman, Independent Governance Committee

Contents | Summary

Investment Performance

Investment Performance vs Benchmark

Investment Strategy Design

AnnualManagement

Charges

TransactionCosts

Service Levels

Communication and

Engagement Communication and EngagementWe do not currently have a consistent scorecard for the various components involved here, so we have made an intuitive assessment for 2017.

1111

Chair report for activities during 2017

Contents | Report of the Chair

1. Introduction

The main report summarises our activity during the year (from literally thousands of pages of reports). Where I don’t mention anything, you have no need to worry! This year to improve clarity I’ve colour coded the IGC’s Value for money Framework on the traditional Red, Amber, Green traffic lighting system (see Appendix 4 for details).

In order to reduce the amount you have to read, I have moved to Appendices

• the purpose of the IGC

• who the IGC members are

• a summary of the Schemes, Members and Funds under IGC review

• IGC’s definition of Value for Money and scoring framework

• Jargon explained.

• Schedule of IGC meetings and principal agenda items

Lawrence Churchill CBE, Independent Chair

In this, my third annual report, I am pleased to report excellent progress on the programme of improvements we set out last year…

1212

2. Charges

2.1 Progress during the year

We have ensured Prudential is not charging more than IGC thinks is justified (see appendix 4).

At the end of 2017, we have now eliminated all complications to the way charges were taken, and we have confirmed that all categories of member, no matter how small their pension pot, are not being charged more than our reference points (see Appendix 4).

About 4% of members choose to invest in funds which charge more than our reference points but we are closing any funds we think are not providing sufficient extra return to justify the extra costs.

Progress is shown in the interactive timeline on the following page. Click through the dates to view actions, implementation dates and commentary.

Michael Payne, Prudential Appointed Member

All complex charging structures now eliminated.96% of members and assets are in funds charging at or below the IGC’s reference points, and the rest also pass our VfM test.

Contents | Report of the Chair

Customer ‘personas’

To demonstrate the impact that some of these changes may have had on our customers, we have developed a set of ‘personas’ which are representative of the populations affected.

These can be accessed on the same timeline by clicking on the persona icon.

2.2 Annual Management Charges for Default Funds

Prudential operates variable charging based on commercial considerations. No-one is paying more than the IGC reference points for any default fund, but there is considerable variability in charges paid. The charge most commonly paid for Prudential’s flagship Default Fund is less than 0.5% so gets an excellent Dark Green rating.

1313

ActionInitial charges eliminated

CommentaryAs outlined in 2016/17 Chair Statement

Implementation date(s)March 16 – June 16

Contents | Report of the Chair

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1414

Contents | Report of the Chair

Implementation date(s)

Sarah, 45

Potential fund prior to these changes:Potential fund after these changes:Increase in potential fund value of:

Sarah’s pension value after 20 years, cashed in at 65:

In March 2017, we brought charges for our ‘Workplace Leavers’ in line.

£43,100

£47,100

£4,600 (or 10.7%)

Sarah has built up a number of pensions with different employers and finds it hard to keep an eye on them all. We wanted to make sure that the savings she had with Prudential weren’t being chipped away by charges, especially as Sarah is not making any payments in. These lower charges will mean that Sarah will now potentially have more money to put towards an income in later life.

Pension: Group Personal Pension

Sarah stopped making payments into this pension when she changed employer

Current pension savings: £22,000

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1515

ActionIndividual Pensions that were formerly in a contract-based workplace pension: ‘IP Workplace Leavers’

CommentaryIt’s taken a long time to identify all individual pension members who were previously members of a workplace scheme. We found 110,000 policies, and successively brought their charges in line.

Around 25,000 customers benefitted from these changes.

Implementation date(s)Removal of commission charges completed March 17

Removal of initial charges completed July 17

Contents | Report of the Chair

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1616

Contents | Report of the Chair

Implementation date(s)

Michael, 50

With policy fees:

Without policy fees:

Increase in fund value of:

Michael’s pension value after 15 years, cashed in at 65

We removed Michael’s policy fees in May 2017

£40,400

£40,800

£400 (or 1%)

Michael plans not to touch this workplace pension until age 65, he has savings and another work pension elsewhere so is thinking about combining these savings together when he retires. Now Michael’s policy fees have been removed, he has more opportunity to maximise the potential of this pension.

Pension: Group Personal Pension

Michael does not make any payments

Current pension savings: £22,000

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1717

ActionMonthly admin fees eliminated

CommentaryDue to be eliminated by July 17, removed two months ahead of schedule.

Implementation date(s)May 17

Contents | Report of the Chair

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1818

Contents | Report of the Chair

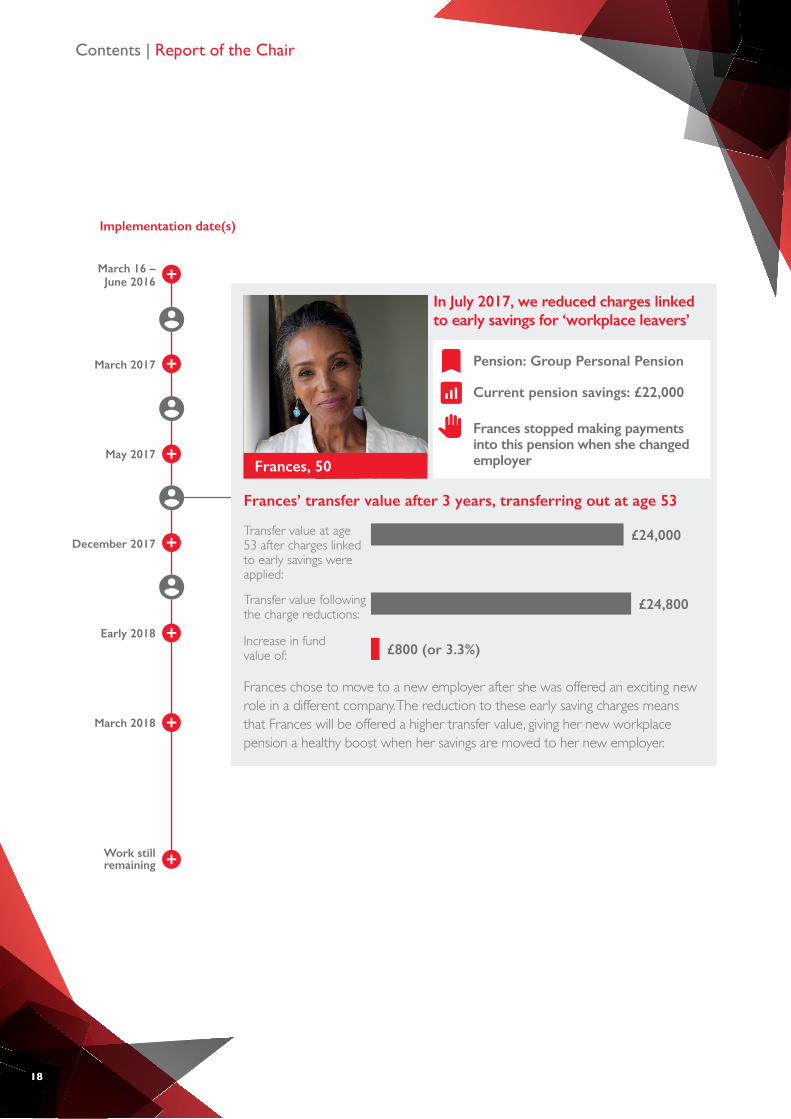

Implementation date(s)

Frances, 50

Transfer value at age 53 after charges linked to early savings were applied:

Transfer value following the charge reductions:

Increase in fund value of:

Frances’ transfer value after 3 years, transferring out at age 53

In July 2017, we reduced charges linked to early savings for ‘workplace leavers’

£24,000

£24,800

£800 (or 3.3%)

Frances chose to move to a new employer after she was offered an exciting new role in a different company. The reduction to these early saving charges means that Frances will be offered a higher transfer value, giving her new workplace pension a healthy boost when her savings are moved to her new employer.

Pension: Group Personal Pension

Frances stopped making payments into this pension when she changed employer

Current pension savings: £22,000

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

1919

Contents | Report of the Chair

ActionHigher charging fund closures

CommentaryI reported last year that there were 32 higher charging funds, 3 of which were on the Watch List and a further 2 failing to meet our Value for Money performance criteria.

In 2017 we identified a further two funds failing our Value for Money test when our workplace leavers population was further analysed. This brought the total number of funds we felt needed to be addressed to 34.

Prudential closed four of these funds in December 2017; a progamme is in place to close a further 4 in March, 4 in May and one further fund will be closed in August 2018. These 13 closing (or closed) funds contain around 14,500 members and over £100m invested – representing 6.5%of the membership and 1.8% of funds invested.

With 13 of the 34 funds addressed, this left 21 still under review.

Prudential’s policy is to allow individual funds to charge more than IGC’s reference point provided they pass the Value for Money test, but their ambition is not to charge individual members more than the reference point (when considering the charges across all the investments a policy may be utilising).

Implementation date(s)Closed 13/12/17

• Prudential Newton Global Equity Fund

• Prudential BlackRock Ascent US Equity Fund

• Prudential BlackRock Ascent Japanese Equity Fund

• Pru Axa Rosenberg Global Equity Alpha

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

2020

Contents | Report of the Chair

Implementation date(s)

Anisha, 45

In her original investment: In her lower charging investment: Increase in fund value of:

Anisha’s pension value after 20 years, cashed in at 65:

In December 2017, Anisha’s money was moved into a similar fund with a lower management charge

£124,000

£127,000

£3000 (or 2.4%)

As part of our programme to reduce the number of higher charging funds within Prudential’s range, Anisha’s money was moved into a similar fund with lower charges. This is because we felt that her higher charging option was not providing Anisha with value for money. Assuming both her original investment and new investment perform in a similar way, Anisha may now see a greater increase in the value of her savings over time.

Pension: Group Personal Pension

Anisha pays around £200 each month into her workplace pension savings

Current pension savings: £10,300

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

2121

Contents | Report of the Chair

ActionApproved for closure early 2018

CommentaryAn additional ten funds were approved for closure in December where it was identified that the fund charges were too high to be appropriate for members.

These 10 funds contain a further 1,364 policies.

Implementation date(s)Timescales are still being scoped but Prudential aims to close all of these funds by September 2018.

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

2222

Contents | Report of the Chair

ActionHigher charging fund closures

CommentaryI reported last year that there were 32 higher charging funds, 3 of which were on the Watch List and a further 2 failing to meet our Value for Money performance criteria.

In 2017 we identified a further two funds failing our Value for Money test when our workplace leavers population was further analysed. This brought the total number of funds we felt needed to be addressed to 34.

Prudential closed four of these funds in December 2017; a progamme is in place to close a further 4 in March, 4 in May and one further fund will be closed in August 2018. These 13 closing (or closed) funds contain around 14,500 members and over £100m invested – representing 6.5%of the membership and 1.8% of funds invested.

With 13 of the 34 funds addressed, this left 21 still under review.

Prudential’s policy is to allow individual funds to charge more than IGC’s reference point provided they pass the Value for Money test, but their ambition is not to charge individual members more than the reference point (when considering the charges across all the investments a policy may be utilising).

Implementation date(s)Closing 17/03/18

• Prudential M&G Managed Growth Fund

• Prudential Invesco Perpetual Managed Growth Fund

• Prudential M&G Global Leaders Fund

• Prudential Newton Global Equity Fund

We are due to close four more funds in May and one in August 2018.

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

2323

Contents | Report of the Chair

CommentaryWe have identified those policies investing through higher charging funds, and after the closure programme concludes in the first half of 2018, we estimate there will be around 170 members with £1.2m invested in the 11 remaining higher charging funds; this represents less than 1% of policies and funds under management.

It is important to note that these funds are performing well so that there is no Value for Money concern; however we challenge Prudential to find ways of lowering the charges to below our reference points.

Implementation date(s)Further work will be initiated Q1 2018 to look at the ways in which Pru can reduce charges for these customers.

Implementation date(s)

March 16 – June 2016

May 2017

December 2017

Early 2018

March 2017

March 2018

Work still remaining

2424

3. Investments

3.1 Performance

2017 was another good year for pension investment. Prudential’s own default fund, Prudential Dynamic Growth IV, delivered returns in excess of our long term target in absolute terms. In relative terms, compared to similar funds in the market, performance beat the ABI benchmark. External appraisal of Prudential’s default fund strategy by Redington revealed that there were no areas of concern for the IGC to pursue.

Gross Performance of Prudential’s Dynamic Growth IV Fund

Some Employers choose their own Default funds and in 2017 we increased our scrutiny of the largest Employer pension schemes measured by membership and assets under management and looked at the top 20. All defaults performed in excess of our Consumer Price Index + 3% target with the exception of one investment. This fund has been a poor performer for some time and as part of Prudential’s default fund review we are discussing options to address this.

Should you wish to review the performance of your investments, Prudential’s Corporate Pension Fund Factsheets can be found here.

John Nestor, Independent Member

2017 has seen strong performance from Prudential’s investments and continued work to improve what’s on offer.We have begun to simplify the fund range available to our customers and all default strategies are due to be compatible with Pension Freedoms by August 2018. We will also continue to focus on transaction charges as the FCA’s new methodology comes into effect.

Contents | Report of the Chair

Feb 15 Jul Oct Feb 16 Jun Oct Feb 17 Jun Oct Feb 18

35.0%

25.0%

15.0%

5.0%

-5.0%

-15.0%

Pru Dynamic Growth IV Pn S3 (GR) in GBXABI Mixed Investment 40-85% Shares (GR) in GBX

2525

3.2 Investment Strategy Design;

Contents | Report of the Chair

86% of members were previously put offside by Pensions Freedoms, now:

Consistency with New Pension Freedoms

now, by August 2018

I reported last year that a large number of strategies were not yet consistent with Pensions Freedoms introduced by the Government in 2015, and that some smaller schemes did not have sufficient asset diversification in their strategies. This was a widespread problem affecting 86% of all members and nearly 1,350 schemes.

We have a programme in full swing to remedy this. Two of the three administration platforms were completed in February and October 2017, putting right 1065 schemes. Most members are in the third platform and this has been split into 15 tranches. All Employers have been informed, and the transition to the new defaults has been completed for 99 schemes covering 13,100 members and £363m assets.

Risk weightings clearly communicated Prudential’s Dynamic Growth Funds clearly communicate the percentage allocated to riskier growth assets.

Risk/Return trade offs close to the Efficient Frontier During the year, we have received reports from Prudential’s Portfolio Management Group on Strategic Asset Allocation and independent external reports from Natixis and Redington. These reports helped IGC to identify the strengths of the approach and to monitor progress on some minor recommendations revealed by the analysis.

Environmental, Social and Governance factors Long term risk to returns can be affected by sustainability factors. In addition many investors prefer to invest with ‘ESG’ factors in mind. The Law Commission made recommendations to expand the remit of the IGC to include reporting on the Prudential’s policies in this area and the FCA is still considering its response.

In January 2017, we received a presentation from M&G, Prudential’s fund management arm who confirmed that ESG considerations were integrated into their investment approach, that they support both the UK Corporate Governance and Stewardship Codes and are signatories of the United Nations’ Principles for Responsible Investment. They implement these principles through a Responsible Investment Management Committee.

2626

What are the most material ESG issues M&G’s Responsible Investment Management Committee consider?

M&G also enlist the services of leading providers of ESG-focused information and analysis (such as MSCI ESG Research and ISS-Ethix). Together with other sources of ESG information such as company reporting, broker research and media reports, this analysis helps M&G to better understand the ESG risks and opportunities facing existing and potential investors.

Environmental Social Governance

• Toxic Emissions• Water usage• Resource scarcity• Waste and pollution• Carbon/GHG• Climate Change• Energy efficiency

• Health and Safety• Working Conditions• Supply chains• Customer satisfaction• Community relations• Stakeholder management• ‘Social license to operate’• Product quality

• Shareholder rights• Board independence• Dividend policy• Remuneration and incentives• Audit and internal control• Cybersecurity• Diversity• Bribery and corruption

Contents | Report of the Chair

2727

In 2016, Prudential established a cross-functional working group to undertake a Group-wide review to identify the ESG issues that are most material for Prudential. This included identifying ESG trends, risks and opportunities directly applicable to Prudential, and wider ESG issues reported on by other providers.

Prudential continually monitor the changing environment in which we operate to ensure that those ESG issues that are important to our stakeholders are captured and managed on an ongoing basis.

If you would like to learn more about Prudential’s approach towards its Corporate Responsibility, or would like to review its ESG report in more detail, please visit the Prudential website.

We will continue to review Prudential’s approach towards Environmental, Social and Governance factors in 2018.

Stakeholder group How does Prudential engage with these stakeholders?

Areas of interested raised by these stakeholders

in 2016/17.

Customers Contact centres, online servicing, face-to-face advice, annual statements, surveys

Retirement income choices, service delivery (including service delays), UK pensions freedom reform

Investors Half and full-year results, Annual report, annual general meeting, investor briefings

Customer satisfaction, product suitability, diversity, employee training and retention, remuneration, succession planning, responsible investment, financial strength and performance, risk management

Employees (including contractors, potential recruits and trade unions)

Surveys, town hall meetings, away days, team meetings, appraisals, intranets, training programmes.

Diversity and inclusion, employee relations

Governments (including central banks, stock exchanges and global policy bodies)

Meetings, input to policy papers, sector-wide analysis, partnering and/or speaking at public and private events, data input

Responsible business, role in financial stability, customer fairness and engagement, sector regulation, responsible investment

Regulators Senior management meetings, discussions on key policy proposals, annual meeting of the Regulatory College of Supervisors, continuous working-level engagement

Governance, conduct risk, cyber security, customer protections, solvency II, G-SII and international capital standards

Civil Society Meetings, data sharing, sector benchmarks

Inclusion, education, disaster relief, climate change support and funding

Media Media releases, meetings and calls, monitoring of media output

Financial performance, business strength, leadership, remuneration, low-carbon economy

Suppliers Assessments, contract negotiations, review meetings

Data protection, anti-bribery and corruption, environment (waste management), human rights, Modern Slavery Act

Contents | Report of the Chair

2828

3.3 Governance of the Watch List;

IGC has continued to press hard on the governance of the much improved watch list process. The direction of our challenge has been to have the customers’ interests considered as a priority and to speed up action on non-performing funds. We are making progress and will continue to challenge.

3.4 Simplicity

129 funds to choose from – completely unnecessary…

Members have been able to invest in 129 different funds. We regard this number as far too high for Workplace Pensions, and see little sign of customer demand or need for many. For example, 71 funds have fewer than 500 members investing and 72 funds have less than £5m invested by workplace pension members. In addition, a number of funds seem to be doing pretty much the same thing.

We believe there is an opportunity for Prudential to simplify its fund range and reduce its costs by reducing the range of funds offered.

As set out above, 23 funds will have closed in the last 18 months, simplifying Prudential’s proposition and delivering better Value for Money for members. But 106 funds still remain. We are challenging Prudential to make much more progress in 2018.

3.5 With Profits With £1.2bn of funds under the IGC remit being invested in With Profits, we undertook further research into the charges for guarantees and smoothing. This showed that the charges were less than could be supported theoretically. Importantly, we also confirmed that if the charges for guarantees were excluded, all the with-profits funds were charging 1% or less for investment, in line with our reference point for unit-linked funds. There are consequently no concerns about the Value for Money members are receiving.

Performance of the With Profits fund exceeded both the ABI’s indices for equivalent unit-linked funds and our Value for Money reference point of CPI +3%, over both one, three and five years.

With Profits Gross investment Returns

Contents | Report of the Chair

WPSF (gross Return)

16%

2011 2012 2013 2014

Year

Year

on

Year

incr

ease

(%

)

2015 2016 2017

14%

12%

10%

8%

6%

4%

2%

0%

2929

3.6 Transaction costs

We welcome the finalisation of FCA rules for measuring transaction costs published in September 2017. The rules come into force from January 2018, so we measured transaction costs once again using the method we developed last year. The results are broadly similar, with some differences for individual funds explained by increases or reductions in turnover and less activity in the Property Fund.

We analysed about 85% of the unit linked funds and found that just over 60% of funds under management had transaction costs of less than 0.1%, earning a Dark Green rating. There was a small increase in transaction costs for Prudential’s flagship default fund to 0.09%. At the other end of the scale, two funds covering 1% of funds under management charged more than 0.4%, receiving an Amber rating.

We have started to collect data to support the new FCA approach and will be in a position to analyse the data in the summer. Once the figures on the new basis have been available for a while, we will be recommending that these costs are appropriately communicated to Employers and members. We expect that this will focus attention on any costs which are not essential (but for example support a particular trading strategy).

Contents | Report of the Chair

3030

4. Service Levels

We continue to monitor the quality of service you receive and place emphasis on Prudential’s performance against key areas, your feedback (in the form of complaints and net promoter survey scores) and the commentary we received from Service Management.

We monitor service levels across seven areas every quarter. The time to answer the phone has fallen short of target consistently with the other six areas being above target. Benchmarking with six other leading companies revealed that call wait times for Prudential were in fact lower than average, indicating that the targets set might be demanding a higher standard than other companies. During industrial action at Prudential’s outsourcer, Capita, the number of customers hanging up almost breached the target.

Performance of Individual Service Areas:

In addition we receive an audited report to ensure that all premiums are allocated to investments speedily, or, in the rare case of a delay, that customers’ interests are fully protected. We also review the number of complaints, including the number referred to the Financial Ombudsman. We regard these additional areas as performing satisfactorily.

For New Business’, ‘Claims’ and ‘Customer Servicing’, Prudential’s targets reflect the proportion of cases they believe should be concluded within five working days.

Some of these targets have a lower threshold set, this is to reflect that some tasks encompassed under this measure will take longer than five days to complete

Jennifer Owens, Prudential Appointed Member

Service levels continue to be satisfactory throughout 2017. All areas aside from the speed at which calls are answered scored green against their targets. We will continue to monitor Prudential’s performance throughout 2018 and gather more information from ongoing benchmarking with other providers.

Contents | Report of the Chair

Area Achieved Targets

New Business 95% 83%

Claims 78% 59%

Customer Servicing 92% 66%

Lost Call Rate 4% 4.5%Calls answered within 20 seconds 65% 80%

Quality Auditing 97% 95%

Call Quality Auditing 97% 95%

3131

5. Communication and Engagement

I will report on our activities in 2017 in two parts – what we are learning from our customers and external research, and how Prudential is responding.

5.1 How we are learning

We are understanding customer needs better by

• supporting the Pension Policy Institute’s three reports on Engagement

• adopting the Net Promoter system to find out what customers think

• conducting further research into customers’ needs and values with two other providers to develop deeper insights from last year’s research

• launching a group research programme into how we can use Employers to increase member engagement

• benchmarking different aspects of service/default funds with seven other providers

• conducting seminars with large employers on barriers to engagement

• holding seminars with employers of all sizes to communicate research findings and identify next steps

• continuing to discuss IGC work and findings with management committees of employers pension schemes.

5.2 How we are responding

We are working with Prudential and external communications experts to

• improve the language and tone of our written communications

• get feedback on the much shorter Annual Benefit Statement

• create a dedicated team for Workplace Pensions to make information less complex and more relevant

• re-connect with customers who have moved house and not told us

• develop both digital and traditional communications for different audiences.

5.3 What have we learned?

Research findings are consistently pointing in the same direction

• make it easier for those who want to engage by removing barriers (jargon as well as easy access)

• make it easier to connect with one’s later life, and stress the importance of early action

• identify the times when the customer is interested, and communicate then

• inform customers of the level of State pension in the UK and the consequent importance of private saving to enable a comfortable retirement.

Lesley Alexander, Independent Member

Employers are keen for more help from PrudentialPrudential’s IGC will be continuing their work exploring our customer’s needs by sponsoring research and further exploring and piloting actions with Employers to improve levels of engagement.

Contents | Report of the Chair

3232

Contents | Report of the Chair

Fundamentally, this is about changing social attitudes and empowering individuals (with support from their Employer and Pension Provider) to take appropriate savings decisions at the right time. There is no quick fix. Encouragingly, those individuals involved in last year’s research did take some action as a result of their involvement.

Although there is still much to do, we believe Prudential is on the right track. An external consultancy reported a customer feedback score of 2.2 out of 5 for a letter. Having re-crafted the letter on the new principles, the score rose to 4.8

6. Our 2018 Plans

Charges

Report on transaction costs using the FCA methodology and challenge any areas which raise questions on Value for Money

Consider setting a Reference Point as part of our Value for Money assessment above which we believe there may be Value for Money concerns

Communicate to Employers and Members the additional transaction costs they are incurring to deliver fund performance

Investments

Monitor completion of the transition of default funds to be compatible with Pension Freedoms (by August)

Challenge Prudential to reduce the number of funds available to Workplace Pension Members.

Begin research into potential improvements to glide path design acknowledging customers’ desire for flexibility on when they will start drawing their pension.

Communication and Engagement

Continue to sponsor research and to pilot actions with Employers to improve levels of engagement

Explore what Prudential can do to provide information and guidance to members to help align savings habits and desired retirement lifestyle (acknowledging that Prudential only has incomplete information about a customers’ wealth).

Service levels

Monitor the transition of outsourced services from Capita to TCS.

Other

Challenge Prudential to extend the IGC remit to cover Personal Pensions and AVCs, and “in retirement” products, so that we can ensure Value for Money is being provided.

We will follow the progress of the recently announced demerger and monitor that the potential to improve customer value is realised.

3333

Appendices

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

John Nestor, Independent Member

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

3434

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

John Nestor, Independent Member

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

Lawrence has devoted his life to making financial services work for everyone.

As well as being CEO of three insurance groups, Lawrence chaired the Raising Standards Quality Mark Scheme for the Associate of British Insurers, and was a board member of the Personal Investment Authority and of the Financial Ombudsman Service. Totally independent, the ombudsman deals with complaints against financial firms.

To protect pensions where their employer goes bust, Lawrence set up the Pension Protection Fund for the UK Government.

He is also a former board member of the Board for Actuarial Standards – setting technical and communications standards for actuaries.

More recently, Lawrence set up NEST for the UK Government. This gives people on modest incomes a pension provider designed specifically for them.

He currently chairs the Financial Services Compensation Scheme. This organisation gives us protection if financial firms go bust. Lawrence is also Senior Independent Director at the global health insurer, Bupa, and Chairman of the Pensions Policy Institute.

3535

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

Managing director of the employee communications company, Ferrier Pearce. Lesley is a fellow and council member of the Pensions Management Institute.

Lesley is also chair of the UK Sustainable Investment and Finance Association and is the former CEO of the HSBC Bank Pension Trust (UK) Ltd.

She has unique experience and insight into the practical application of behavioural economics to employee retirement savings.

Lesley takes a passionate interest in how clearly we tell you what is going on and explain things.

John Nestor, Independent Member

3636

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

John brings considerable expertise in investment strategy and asset management. John is a Client Director of Capital Cranfield Pensions Trustees Limited.

He was managing director of both UBS Global Asset Management and Citigroup Asset Management.

John is chair of trustees for Marylebone Cricket Club (MCC) Pension Scheme and a trustee of the RAC Staff Pension Scheme.

John is an expert on how well, and how reliably, your pension pot should grow.

John Nestor, Independent Member

3737

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

Michael is a qualified actuary with around 20 years of post-qualification experience, and around 30 years of experience of working in life assurance and pensions.

Michael is currently the Regulatory and Legacy Portfolio Actuarial and Operations Director at M&G Prudential, where he has Actuarial and Operational accountability across a number of regulatory and legacy related areas.

Over his 12 years at M&G Prudential, Michael has held a number of senior actuarial and finance roles, most recently being accountable for all of financial reporting across UK and Europe, in his role as Director of Finance Reporting.

Before joining M&G Prudential, Michael spent a number of years working at Scottish Widows now part of Lloyds Banking Group, Scottish Friendly, and Scottish Amicable, in a variety of senior positions.

John Nestor, Independent Member

3838

Contents | Appendices

Appendix 1 – What is the IGC set up to do?

The IGC’s overriding objective is to independently review the Value for Money of contract based defined contribution (“DC”) workplace pension schemes.

The IGC has met as a Committee for formal meetings on six occasions during 2017. A number of informal meetings have taken place, and individual members have met with staff, other IGC Chairs, subject matter experts and Prudential’s regulators (FCA) outside of formal meetings.

Appendix 2 – Who are the IGC Members?

The IGC is properly constituted with three independent members and two members from Prudential, whose biographies indicating their qualifications for the role can be seen later in the Appendix.

External members are recruited via open competition run by the Chair and existing external members. Internal members are suggested by Prudential and interviewed by the external members. Internal members have their contracts of employment altered so that they act solely in the customers’ interest in IGC discussions.

Lawrence Churchill CBE, Independent Chairman

Lesley Alexander, Independent Member

Michael Payne, Prudential Appointed Member

Jennifer Owens, Prudential Appointed Member

Jennifer joined M&G Prudential as General Counsel in August 2017 and was previously General Counsel and Company Secretary at Towergate Insurance.

Prior to that, she held General Counsel roles within investment bank and fund manager Execution Noble and held senior legal and compliance roles at GE Capital, after her time in private practice at Herbert Smith.

John Nestor, Independent Member

3939

Contents | Appendices

Appendix 3 – Summary of the Schemes, Members and Funds under IGC Review

Taking into account both workplace pension members, and personal pension holders who were previously members of workplace schemes (referred to in this report as ‘IP Workplace Leavers’), there are a total 220,000 customers with 273,000 policies within Prudential’s workplace pension schemes forming part of the IGC’s ongoing scope.

As I mentioned last year, we had problems identifying those members who were once in workplace schemes but who now hold personal pensions policies. We have completed our investigation and found 71,000 members holding 110,000 policies with £1.8bn of assets. This is broadly a 50% increase in the population under IGC scrutiny.

Throughout 2017 we continued to see a small decrease in member and employer plan numbers, this is largely due to natural attrition as Prudential’s strategy for workplace pensions is to preserve and enhance value in its existing business, alongside the selective acquisition of new business.

The number of actively paying members remained consistent and assets under management increased, now totaling £5.75bn (£1.2bn of which is invested in Prudential’s With-Profits fund).

We asked Prudential to provide more in depth analysis of their customer base. Some of the results, taking into account customer age and the current value of retirement savings, are provided below:

Current pension pot value (£k) by age bands

This kind of analysis compliments the information we receive from other sources such as Net Promoter Scores, research studies and employer seminars. All of this helps to create a more complete picture for the IGC who are then better able to anticipate customer needs. It is our intention to use this information to help improve engagement which remains one of our top priorities in 2018.

50k

Age<30

Age30-34

Age35-39

Age40-44

Age45-49

Age50-54

Age55-59

Age 65+

Age 60-64

Volu

me

of C

usto

mer

s 40k

30k

20k

10k

0

■ 7. £250k+

■ 6. £150k–£250k

■ 5. £100k–£150k

■ 4. £50k–£100k

■ 3. £20k–£50k

■ 2. £10k – £20k

■ 1. £0 – £10k

4040

Contents | Appendices

Appendix 4 – IGC’s Definition of Value for Money (VfM)

The IGC’s approach to VfM takes account of a range of factors, including charges, performance, service and communications. However, these have been weighted to reflect our view that what ultimately matters is the outcome for members.

On the basis that good financial outcomes that lead to higher retirement income are the most important, we prioritise investment returns and charges as being the most important elements of VfM. We then look at a number of secondary service quality features, placing particular emphasis on the swift and accurate processing of contributions, the level of performance in dealing with complaints, and the quality of communications. We anticipate more work on the quality of communications in the years ahead.

With regard to the primary financial components of VfM, it is important to note that

a) for investment returns, we have given priority to actual outcomes as well as looking at forecast returns for an appropriate risk exposure in the design of default investment strategies. We have used an externally benchmarked reference point for fund performance of CPI +3%pa (after charges) over a sustained period. If fund performance has been delivered at this level or above, we believe that VfM concerns do not arise in relation to investment returns or charges. We measure performance over 1, 3 and 5 years, where the fund has been in existence for that long.

b) For charges, we have continued to use the following reference points to identify where Value for Money concerns might arise:

• O. 75% pa for charges in schemes used for auto-enrolment (or the equivalent limits set by DWP for schemes with combination charges)

• 1.00% pa for unit-linked schemes not used for auto-enrolment (thus maintaining consistency with the IPB reference point)

• 1.25% pa for with-profits investments where the benefits of smoothing and guarantees bring extra value to members. We review both the cost of the investment and the cost of these guarantees separately, scrutinizing the value offered by both. Our reference point represents the combined cost of both elements.

During 2017, we reviewed with-profits in more detail to test that the benefits of smoothing and guarantees brought extra value to Members above and beyond their costs.

4141

Contents | Appendices

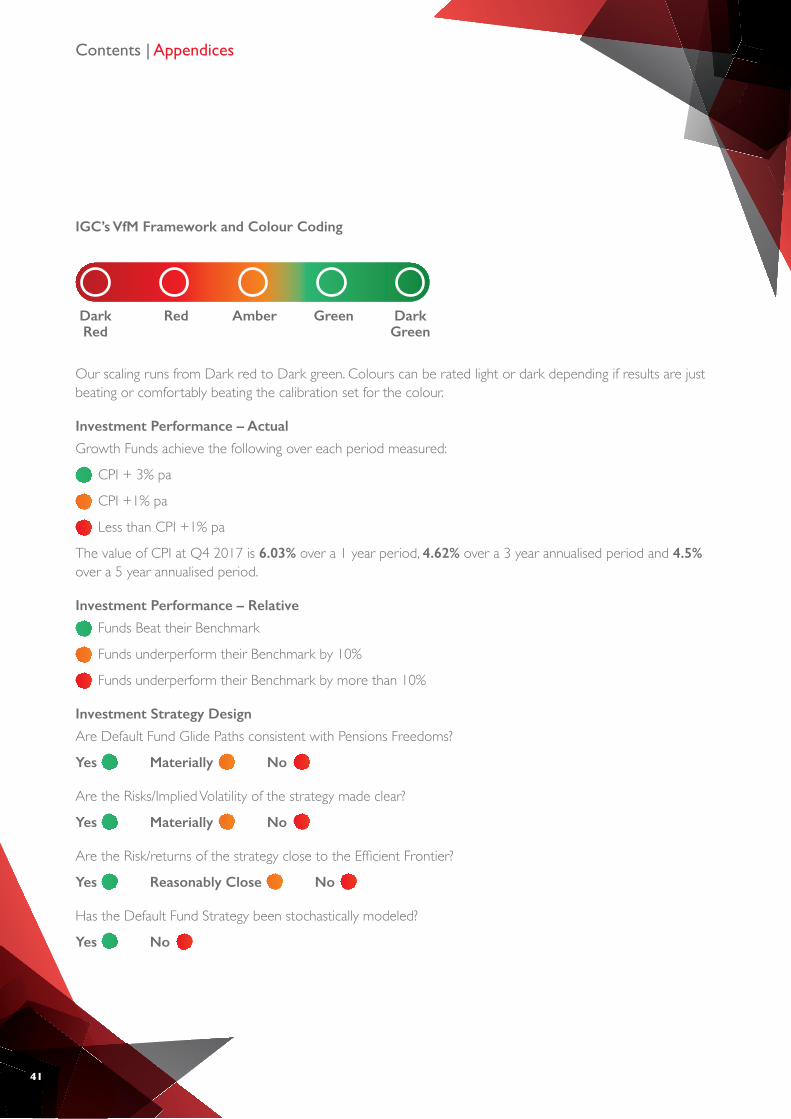

IGC’s VfM Framework and Colour Coding

Our scaling runs from Dark red to Dark green. Colours can be rated light or dark depending if results are just beating or comfortably beating the calibration set for the colour.

Investment Performance – Actual

Growth Funds achieve the following over each period measured:

CPI + 3% pa

CPI +1% pa

Less than CPI +1% pa

The value of CPI at Q4 2017 is 6.03% over a 1 year period, 4.62% over a 3 year annualised period and 4.5% over a 5 year annualised period.

Investment Performance – Relative

Funds Beat their Benchmark

Funds underperform their Benchmark by 10%

Funds underperform their Benchmark by more than 10%

Investment Strategy Design

Are Default Fund Glide Paths consistent with Pensions Freedoms?

Yes Materially No

Are the Risks/Implied Volatility of the strategy made clear?

Yes Materially No

Are the Risk/returns of the strategy close to the Efficient Frontier?

Yes Reasonably Close No

Has the Default Fund Strategy been stochastically modeled?

Yes No

Dark Green

Dark Red

Red Amber Green

4242

Contents | Appendices

IGC’s VfM Framework and Colour Coding

Our scaling runs from Dark red to Dark green. Colours can be rated light or dark depending if results are just beating or comfortably beating the calibration set for the colour.

Annual Management Charges

Most frequent charge applied less than 0.5%

All member borne charges less than or equal to reference points

Between 0% and 5% FUM above reference point

More than 5% of funds under management are above reference point

Transaction Costs (to be refined when FCA model is implemented)

(NOTE: The FCA quoted 0.5% as the average level of transaction Costs in their Market Study)

Default fund less than 0.2% 80% of Funds under management incur costs of less than 0.2%

80% of Funds under management incur costs between 0.2 – 0.5%

More than 20% of Funds under Management incur costs of more than 0.5%

Service Levels

All service levels met

Between 50% – 100% of Service levels met

More than half Service levels not met

Communication and Engagement

We do not currently have a consistent scorecard for the various components. We have made an intuitive assessment for 2017.

Dark Green

Dark Red

Red Amber Green

4343

Contents | Appendix

Appendix 5 Jargon explained

AMC – Annual Management Charge: the charge made over the year by fund managers and product providers to cover the expenses associated with running the investment fund and administering the pension plan. Although expressed as an annual percentage figure, the charge is usually taken from the fund daily.

COBS – Code of Business Sourcebook (in other words, the FCA’s rule book).

CPI – The Consumer Prices Index: CPI is the official measure of inflation of consumer prices of the United Kingdom.

Efficient Frontier – A combination of assets (i.e. a portfolio) is referred to as efficient if it has the best possible expected level of return for its level of risk.

FCA – The Financial Conduct Authority.

Guarantees – An investment guarantee is a special provision that is designed to protect investors from incurring overall losses.

IGC – Independent Governance Committee.

IPB – The Independent Project Board was set up by the OFT to oversee the audit of workplace pensions.

Pensions Freedoms – In April 2015 tax rules were changed to allow individuals in defined contribution pensions (also known as money purchase pensions) to choose whether they use their pension to provide a lump sum, a series of lump sums, a guaranteed income for life or to place their money in a drawdown plan.

Prudential – “Prudential” is a trading name of The Prudential Assurance Company Limited, the provider of the workplace pensions.

Smoothing – The use of accounting techniques to level out fluctuations in investment returns from one period to the next (aiming to ‘smooth’ the peaks and troughs of market movements).

VfM – Value for Money, see section 4 for more information.

Watch List – Funds are added to this watch list if they are under performing or if there are additional causes for concern (e.g. significant unexpected changes in the market). These funds are then monitored closely and reviewed on a regular basis.

Net Promoter System – Feedback from customers which separates Advocates from Detractors

Reference Point – a level of charge for a fund above which IGC believes Value for Money concerns might arise.

4444

Contents | Appendices

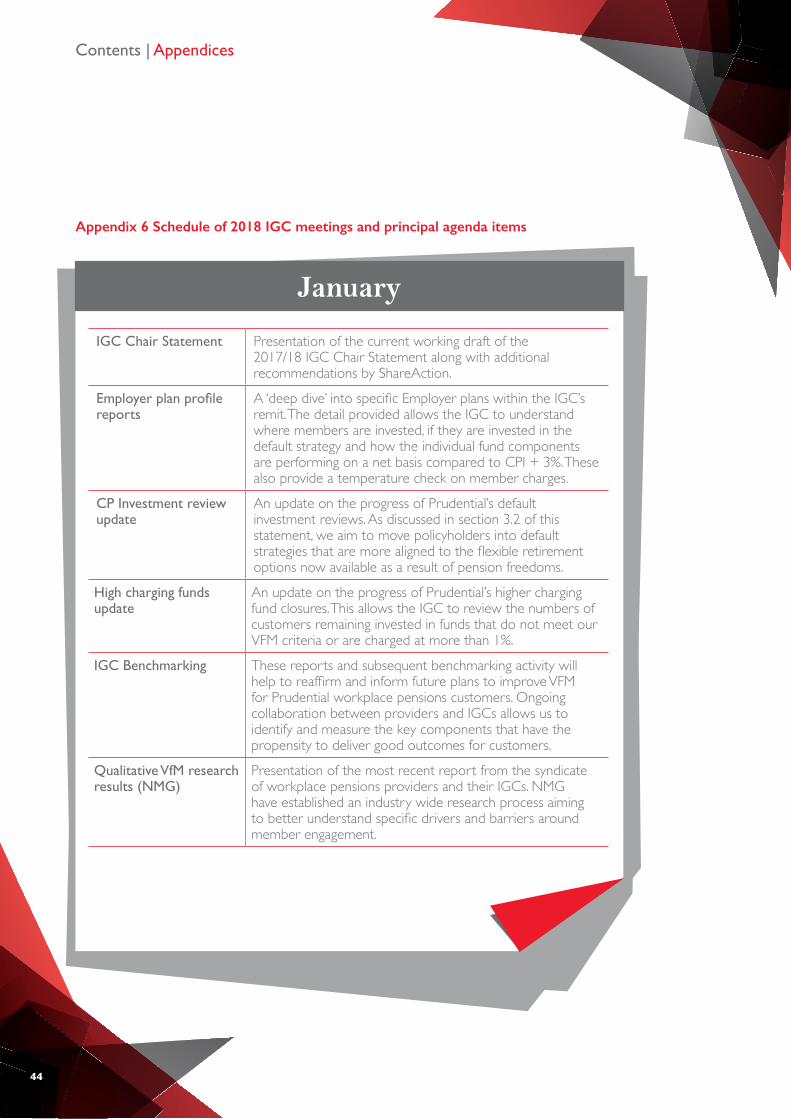

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

January

IGC Chair Statement Presentation of the current working draft of the 2017/18 IGC Chair Statement along with additional recommendations by ShareAction.

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

CP Investment review update

An update on the progress of Prudential’s default investment reviews. As discussed in section 3.2 of this statement, we aim to move policyholders into default strategies that are more aligned to the flexible retirement options now available as a result of pension freedoms.

High charging funds update

An update on the progress of Prudential’s higher charging fund closures. This allows the IGC to review the numbers of customers remaining invested in funds that do not meet our VFM criteria or are charged at more than 1%.

IGC Benchmarking These reports and subsequent benchmarking activity will help to reaffirm and inform future plans to improve VFM for Prudential workplace pensions customers. Ongoing collaboration between providers and IGCs allows us to identify and measure the key components that have the propensity to deliver good outcomes for customers.

Qualitative VfM research results (NMG)

Presentation of the most recent report from the syndicate of workplace pensions providers and their IGCs. NMG have established an industry wide research process aiming to better understand specific drivers and barriers around member engagement.

4545

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

March

Annual prospective charge cap attestation

Annual review of the charges members have applied to their plans.

Quarterly Service Scorecard report

These scorecards give the IGC appropriate oversight of the quality of administration, servicing, complaint and breach handling for the employer plans that fall under their remit.

Quarterly Investment Performance update

The member specific performance information provides an improved understanding to the IGC of the investment returns experienced by members of workplace pensions relative to our benchmark of CPI + 3% over the longer term.

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

Publication of IGC Chair Statement

A final update to present the finished statement to the IGC and its members. Publication of this statement fully completes the statutory requirement for the IGC to produce an annual report in 2018.

CP Investment Review update

An update on the progress of Prudential’s default investment reviews. As discussed in section 3.2 of this statement, we aim to move policyholders into default strategies that are more aligned to the flexible retirement options now available as a result of pension freedoms.

Environmental, Social and Governance Update

A presentation to the IGC by M&G, Prudential’s fund management arm. The insight provided will allow the committee to assess M&G’s ESG policies and how they are applied to the funds they manage on behalf of Prudential’s corporate pension customers

4646

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

May

Quarterly Service Scorecard report

These scorecards give the IGC appropriate oversight of the quality of administration, servicing, complaint and breach handling for the employer plans that fall under their remit.

Quarterly Investment Performance update

The member specific performance information provides an improved understanding to the IGC of the investment returns experienced by members of workplace pensions relative to our benchmark of CPI + 3% over the longer term.

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

CP Investment Review update

An update on the progress of Prudential’s default investment reviews. As discussed in section 3.2 of this statement, we aim to move policyholders into default strategies that are more aligned to the flexible retirement options now available as a result of pension freedoms.

IGC Chair Statement comparisons

In addition to direct member and employer feedback, the IGC will complete an overall comparison review of other Providers 2017/18 Chair Statements. The comparisons and collective feedback will then be used to further improve and generate ideas for future reports.

4747

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

July

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

CP Investment Review update

An update on the progress of Prudential’s default investment reviews. As discussed in section 3.2 of this statement, we aim to move policyholders into default strategies that are more aligned to the flexible retirement options now available as a result of pension freedoms.

Transaction Cost Reporting

This work will provide more transparency on costs and charges experienced by workplace pension members. It will allow the Committee to undertake fuller assessment of ongoing value for money for members of workplace pension schemes.

4848

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

September

Quarterly Service Scorecard report

These scorecards give the IGC appropriate oversight of the quality of administration, servicing, complaint and breach handling for the employer plans that fall under their remit.

Quarterly Investment Performance update

The member specific performance information provides an improved understanding to the IGC of the investment returns experienced by members of workplace pensions relative to our benchmark of CPI + 3% over the longer term.

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

IGC Effectiveness Review

Completed on an annual basis, the review will consider the overall effectiveness of the Committee and make recommendations for its future operation, as appropriate.

Options for 2018/19 Chair Statement

This will sets out a proposed implementation plan and timeline for producing and finalising the 2018/19 IGC Chair Statement. The IGC will primarily discuss suggestions of content to be included and potential presentation options available

4949

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

November

Quarterly Service Scorecard report

These scorecards give the IGC appropriate oversight of the quality of administration, servicing, complaint and breach handling for the employer plans that fall under their remit.

Quarterly Investment Performance update

The member specific performance information provides an improved understanding to the IGC of the investment returns experienced by members of workplace pensions relative to our benchmark of CPI + 3% over the longer term.

Employer plan profile reports

A ‘deep dive’ into specific Employer plans within the IGC’s remit. The detail provided allows the IGC to understand where members are invested, if they are invested in the default strategy and how the individual fund components are performing on a net basis compared to CPI + 3%. These also provide a temperature check on member charges.

IGC Effectiveness Review

Completed on an annual basis, the review will consider the overall effectiveness of the Committee and make recommendations for its future operation, as appropriate.

Progression of 2018/19 Chair Statement

An update on the progression of the Chair Statement against the proposed timeline.

5050

Contents | Appendices

Appendix 6 Schedule of 2018 IGC meetings and principal agenda items

Additional items due to be scheduled into the 2018 agenda:

Environmental, Social and Governance Update

A further update on this topic to outline the updated Group-wide review into ESG issues that are most material for Prudential and it’s customers. This included identifying ESG trends, risks and opportunities directly applicable to Prudential, and wider ESG issues reported on by other providers.

Annual With Profits Performance and Charges

The members of the IGC will receive a presentation on the performance of Prudential’s With Profits fund. This will include data regarding the charges, investment returns and benefits of with-profits investments, and will enable the IGC to confirm whether the with-profits investments available to members of DCWP schemes under Prudential insurance contracts deliver value-for-money.

IGC Benchmarking Results and continued work (phase 2 implementation)

These reports and subsequent benchmarking activity will help to reaffirm and inform future plans to improve VFM for Prudential workplace pensions customers. Ongoing collaboration between providers and IGCs allows us to identify and measure the key components that have the propensity to deliver good outcomes for customers.

PRU

AG

5076

_A 0

4/20

18