14

0 www.bayan.com.sg 2018 Guidance

0 www.bayan.com.sg

2018 Guidance

1

Executive Summary

The Group continues to aggressively expand its production and sales

volumes on the back of the successful expansion achieved in 2017. We

anticipate that prices will remain good and the Group will perform strongly

Total production and sales is Budgeted to be in the range of 25 to 28 million

MT.

ASP anticipated to be in the range of US$ 48-52 / MT based on the

benchmark reference price (NEWCASTLE) being on average US$ 85 / MT for the year

Cash costs anticipated to be in the range of US$ 28-32/MT (include COGS,

Royalties, and SGA) Capex is Budgeted to be in the range of US$ 80 to 120 million

www.bayan.com.sg

Overburden Removal Volume (OB)

Overburden Removal

(million BCM)

(million BCM)

Note : 2017D figures are unaudited figures 2

www.bayan.com.sg

FY18 Overburden Removal volume is budgeted to increase principally due to the increased production at Tabang.

159

96

41 33

84

100 - 120

2013 2014 2015 2016 2017D 2018B

Quarterly Overburden Removal

2017D 2018B

Gunungbayan Pratamacoal - Block II 2 3 to 7

Perkasa Inakakerta 8 5 to 8

Teguh Sinar Abadi/ Firman Ketaun Perkasa 40 35 to 39

Tabang Concessions 24 46 to 51

Wahana Baratama Mining 10 11 to 15

Total 84 100 to 120

(in million BCM)OB

23 - 28 23- 28 28 - 33 26 - 31

1Q18B 2Q18B 3Q18B 4Q18B

Coal Production

Coal Production

(million MT)

(million MT)

Note : 2017D figures are unaudited figures 3

www.bayan.com.sg

FY18 Production Volume is anticipated to increase primarily due to the increase in production at Tabang despite a slight increase in overall weighted average stripping ratio combined with coal extraction reaching commercial levels at GBP

Quarterly Coal Production

6 - 7 6 - 7 6 - 7 6 - 7

1Q18B 2Q18B 3Q18B 4Q18B

2017D 2018

Gunungbayan Pratamacoal - Block II - 0.4 to 0.6

Perkasa Inakakerta 1 0.9 to 1.2

Teguh Sinar Abadi/Firman Ketaun Perkasa 3 2.7 to 3.0

Tabang Concessions 16 19.0 to 22.0

Wahana Baratama Mining 1 1.0 to 1.2

Total 21 24 to 28

Coal Production(in million MT)

14

10 11

10

21

24 – 28

2013 2014 2015 2016 2017D 2018

Weighted Average Strip Ratio (SR)

Weighted Average Strip Ratio

Note : 2017D figures are unaudited figures 4

www.bayan.com.sg

FY18 Weighted Average Strip Ratio is budgeted to increase slightly, primarily due to higher stripping ratios at Tabang and WBM, caused by the continuation of Wahana into the Snake Pit and slightly higher at Tabang due to increasing each of the mining areas closer to their Life-Of-Mine stripping ratios

11.6 10.0

3.8 3.4 4.0 4.0 – 4.5

2013 2014 2015 2016 2017D 2018B

4.1 - 4.3 3.9 - 4.1 4.5 - 4.7 4.5 - 4.7

1Q18B 2Q18B 3Q18B 4Q18B

2017D 2018

Gunungbayan Pratamacoal - Block II - 12.0 to 14.0

Perkasa Inakakerta 7.2 7.6 to 7.8

Teguh Sinar Abadi/ Firman Ketaun Perkasa 13.6 13.2 to 13.7

Tabang Concessions 1.5 2.2 to 2.4

Wahana Baratama Mining 8.9 13.4 to 13.8

Total 4.0 4.0 to 4.5

Weighted Average SR (:1)Weighted Average SR

Quarterly Weighted Average SR

Cash Costs

(US$ / MT)

Average Cash Costs per MT(*) Sing Gas Oil Price(*)

(US$ / liter)

FY18 Average Cash Costs is anticipated to be in the region of US$ 28 to 32/ MT

5

www.bayan.com.sg

*(1) Average cash costs include barging, royalty, and SGA (2) 2017D figures were unaudited figures

71 65

43

30 29 28 to 32

2013 2014 2015 2016 2017D 2018

0.9 0.8

0.5 0.3

0.4 0.5 -0.6

2013 2014 2015 2016 2017 2018B

* Published by ANZ Singapore, including PBBKB and VAT

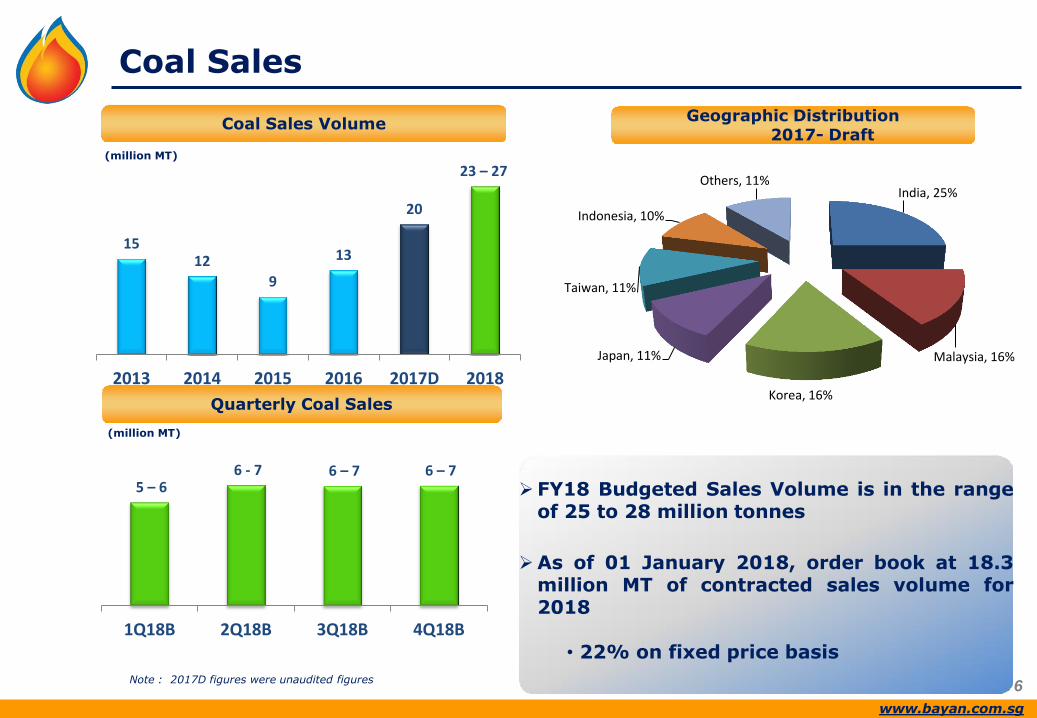

Coal Sales

Coal Sales Volume

(million MT)

FY18 Budgeted Sales Volume is in the range

of 25 to 28 million tonnes

As of 01 January 2018, order book at 18.3

million MT of contracted sales volume for 2018

• 22% on fixed price basis

(million MT)

Quarterly Coal Sales

Geographic Distribution 2017- Draft

Note : 2017D figures were unaudited figures 6

www.bayan.com.sg

Japan

15 12

9

13

20

23 – 27

2013 2014 2015 2016 2017D 2018

5 – 6 6 - 7 6 – 7 6 – 7

1Q18B 2Q18B 3Q18B 4Q18B

India, 25%

Malaysia, 16%

Korea, 16%

Japan, 11%

Taiwan, 11%

Indonesia, 10%

Others, 11%

Average Selling Price (ASP)

Average Selling Price(*)

7

www.bayan.com.sg

FY18 ASP is anticipated to be in the region of US$ 48 to 52/ MT; Based on the benchmark reference price (NEWCASTLE) being on average US$ 85.0/ MT in 2018

* (1) ASP includes coal and non-coal s

(2) 2017D figures were unaudited figures

(US$ / MT)

78 69

52 43 52 48 – 52

1.00

11.00

21.00

31.00

41.00

51.00

61.00

71.00

81.00

91.00

2013 2014 2015 2016 2017D 2018B

4,200

6,300 CV GAR

Committed and Contracted Sales

Note : 01 January 2018

As at 01 January 2018 committed and contracted sales were 18.3 million MT with an average CV of 4,604 GAR kcal/kg

2018 Fixed Price element with

an average CV of 4,461 GAR kcal/kg

2018 Floating Price element with an average CV of 4,644 GAR kcal/kg

Additional sales will be made as progressive production targets are met throughout the year

8

www.bayan.com.sg

22%

78%

18.3 million MT

Fixed Price Floating Price

2018

Capital Expenditure

(US$ million)

2018 CAPEX

9

www.bayan.com.sg

Major capital projects undertaken

include:

• Initial spend on new Haul Road

to Mahakam and Port Facilities

•BCT Upgrade

•Site Dump 4 and 3rd Barge

Loader at Senyiur

•ROM Pad 2 crushing and silo

facilities

•Asphalting and Upgrade of

existing 69KM Senyiur Coal Haul

Road

80.0-120.0

Buildings & Infrastructure

Equipment and Machinery

Office Equipment Transportation Equipment

Tabang

Pakar

Mamahak

Appendix

10

www.bayan.com.sg

PT Perkasa Inakakerta PIK

PT Teguh Sinarabadi TSA

PT Firman Ketaun Perkasa FKP

PT Wahana Baratama Mining WBM

PT Fajar Sakti Prima FSP

PT Bara Tabang BT

PT Brian Anjat Sentosa BAS

PT Tanur Jaya TJ

PT Silau Kencana SK

PT Orkida Makmur OM

PT Tiwa Abadi TA

PT Sumber Api SA

PT Dermaga Energi DE

PT Bara Sejati BS

PT Apira Utama AU

PT Cahaya Alam CA

PT Mamahak Coal Mining MCM

PT Bara Karsa Lestari BKL

PT Mahakam Energi Lestari MEL

PT Mahakam Bara Energi MBE

PT Graha Panca Karsa GPK

Appendix

11

www.bayan.com.sg

Kangaroo Resources Limited KRL

PT Dermaga Perkasapratama DPP

PT Indonesia Pratama IP

PT Muji Lines Muji

PT Bayan Energy BE

PT Metalindo Prosestama MP

PT Sumber Aset Utama SAU

PT Bara Karsa Lestari BKL

PT Karsa Optima Jaya KOJ

Disclaimer

12

www.bayan.com.sg

This presentation contains forward-looking statements based on assumptions and forecasts made by PT. Bayan Resources Tbk management. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. These statements are based on current plans, estimates and projections, and speak only as of the date they are made. We undertake no obligation to update any of them in light of new information or future events.

These forward-looking statements involve inherent risks and are subject to a number of uncertainties, including trends in demand and prices for coal generally and for our products in particular, the success of our mining activities, both alone and with our partners, the changes in coal industry regulation, the availability of funds for planned expansion efforts, as well as other factors. We caution you that these and a number of other known and unknown risks, uncertainties and other factors could cause actual future results or outcomes to differ materially from those expressed in any forward-looking statement.

Thank You

For more information, please contact :

www.bayan.com.sg