PT Pertamina (Persero) Jln. Medan Merdeka Timur No.1A Jakarta 10110 Telp (62-21) 381 5111 Fax (62-21) 384 6865 http://www.pertamina.com Investing in Sustainable Biofuel PT PERTAMINA (PERSERO) CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of Pertamina is strictly prohibited Yenni Andayani Gas and New Renewable Energy Director 20 th August 2015

Transcript

PT Pertamina (Persero)

Jln. Medan Merdeka Timur No.1A Jakarta 10110

Telp (62-21) 381 5111 Fax (62-21) 384 6865

http://www.pertamina.com

Investing in Sustainable Biofuel

PT PERTAMINA (PERSERO)

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of Pertamina is strictly prohibited

Yenni Andayani

Gas and New Renewable Energy Director

20th August 2015

PERTAMINA | 1

Agenda

• Background

• Pertamina Future Strategic Developments in Biofuel

- Co Processing

- Integrated Stand Alone Refinery

• Conclusions

PERTAMINA |

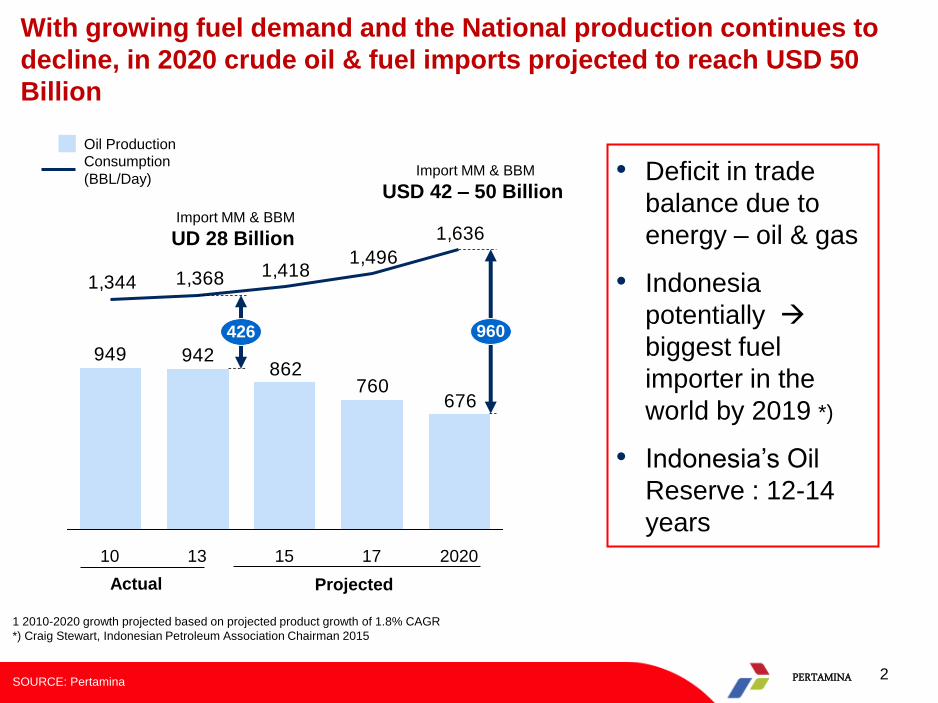

676760

862942949

1,636

1,4961,4181,3681,344

426 960

2020 17 15 13 10

Consumption

(BBL/Day)

Oil Production

Actual Projected

With growing fuel demand and the National production continues to

decline, in 2020 crude oil & fuel imports projected to reach USD 50

Billion

SOURCE: Pertamina

Import MM & BBM

UD 28 Billion

Import MM & BBM

USD 42 – 50 Billion • Deficit in trade

balance due to

energy – oil & gas

• Indonesia

potentially

biggest fuel

importer in the

world by 2019 *)

• Indonesia’s Oil

Reserve : 12-14

years

2

1 2010-2020 growth projected based on projected product growth of 1.8% CAGR

*) Craig Stewart, Indonesian Petroleum Association Chairman 2015

PERTAMINA |

As of November 2014 : Indonesia is the Largest importer of Gasoline

& top 5 importer of Gas oil

Largest importer of

Gasoline in the world :

INDONESIA

MEXICO

UNITED KINGDOM

355,000

340,000

150,000

Barrel/Day

INDONESIA 290,000

Gas oil Volume import

Barrel/Day

3

PERTAMINA | 4

Vision To be a world class national oil energy

company

Mission To carry out integrated core business in oil, gas,

& renewable based on strong commercial

principles

Value Clean; Competitive; Confident; Customer Focus;

Commercial; Capable

Pertamina as State-owned enterprises have seen the growing importance of

renewable energy and it is reflected through changes in our vision and mission

PERTAMINA | 5

Government has aggressively set new biofuels policy, which require

biofuel players to blend up to 20% in 2016

New MEMR Regulation

No. 12 year 2015

Old blending mandate

New blending mandate

Biodiesel (PSO&NPSO) Bioethanol

Fuel Current 2015 2016 2025

20%

2%

25%

20%

10%

1%

10%

1%

Biodiesel Bioethanol

Fuel 2008 2010 Current 2015 2016 2025

10%

10%

20%

15%

5%

5%

7.5%

-%

1%

1%

2.5%

3%

Doubled by 2016

2% 5 %

BioAvtur (BioJet)

Being an SOE, Pertamina will

comply to the aggressive

mandate, as long as it is

economically viable

PERTAMINA | 6

Agenda

• Background

• Pertamina Future Strategic Developments in Biofuel

- Co Processing

- Integrated Stand Alone Refinery

• Conclusions

PERTAMINA | 7

Bioethanol,

FAME/Biodiesel

• GREEN DIESEL

• BIO AVTUR

• 2nd Generation BIO ETHANOL

As well as Algae based

Biofuel (3G)

2025

Establish domestic

production with proven

1G technologies and

available feedstocks

Develop advanced 1.5G

(Green Diesel) leveraging

same feedstock or improved

ones

Grow 2G platform

(if technology develops)

and/or further roll out 1.5G

technology Wave 1

Wave 2

Wave 3

2018

PERTAMINA’s Aspiration in 2025 : 13,9 Million KL from Biofuels

Improved biodiesel1 characteristics

Why 2nd G ?

Biodiesel 1st Generation

(FAME) will hit a

blending wall at 20% due

to technical issues.

2nd Generation of

Biofuel can act as a drop

in fuel, with no max

limitation.

PERTAMINA | 8

To cover National Mandate,

Indonesia need more than

100 Bioethanol Refineries cap.

76,000KL/year in upcoming 10

years

To cover National Mandate,

Indonesia need more than

10 Green Diesel Refineries cap.

10,000 bbl/day in upcoming 10

years

3.2

6.5

2025 2020 2014 2015 2018

3.3

3.3

3.3

3.3 2.8 2.7

0.4

3.3

6.4 4.7

0.4

3.6

8.7

0.4 Other Partnership opportunity

Green Diesel partnership with Pertamina

1 G Transesterification/FAME

Unfortunately, there is still a huge gap between national supply and demand

of Biofuel until 2025, large investment opportunity in biofuels projects and

Pertamina is open for Co-partnership

1

2025

958

76 30

2,380

76 30

2,486

10,472

76 30

10,578

2020

178

2018 2015

391

30 361 852

2014

178 Other Partnership opportunity

1G Yeast Bioethanol

Bioethanol partnership with Pertamina

Bio/Green Diesel Demand & Opportunities

Bioethanol Demand & Opportunities

(Mio KL)

(thousand KL)

As an initial

step,

partnership are

open for

1 Green Diesel

Refinery,

1 Bioethanol

refinery and

1 Bioavtur

refinery. (marked

as green color)

PERTAMINA | 9

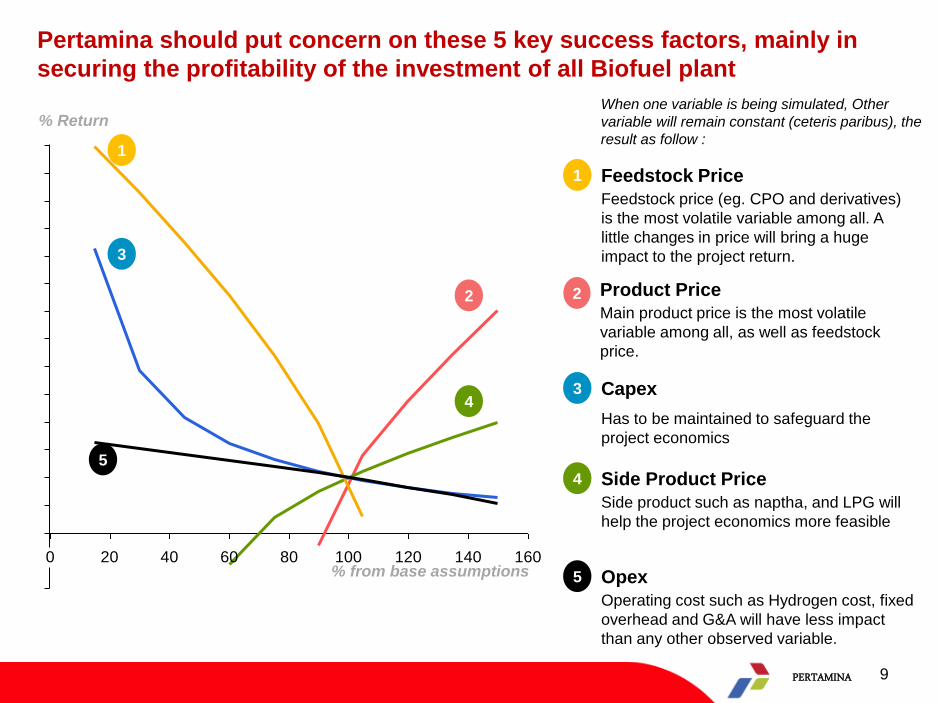

0 20 40 60 80 100 120 140 160% from base assumptions

1

4

2

4 Side Product Price

Side product such as naptha, and LPG will

help the project economics more feasible

3 Capex

Has to be maintained to safeguard the

project economics

When one variable is being simulated, Other

variable will remain constant (ceteris paribus), the

result as follow :

Pertamina should put concern on these 5 key success factors, mainly in

securing the profitability of the investment of all Biofuel plant

3

1 Feedstock Price

Feedstock price (eg. CPO and derivatives)

is the most volatile variable among all. A

little changes in price will bring a huge

impact to the project return.

Product Price

Main product price is the most volatile

variable among all, as well as feedstock

price.

2

% Return

5 Opex

Operating cost such as Hydrogen cost, fixed

overhead and G&A will have less impact

than any other observed variable.

5

PERTAMINA | 10

Typical Joint Development scheme with partners :

Integrated Business Concept will be the Key Success Factor in this

business. Scheme ex. is for Green Diesel Project

At the 1st step into the business, our target is to build an integrated JV company, with 90,000Ha

CPO plantation to support our 10,000 bbl/day greendiesel/BHD refinery that will produce EURO

5-equal Diesel Product

CPO

Plantation

(Upstream)

Green Diesel

Refinery

(Downstream)

Greendiesel CPO

And

Derivatives

Integrated JV Company

Market

• ‘Biofuel project will be feasible and sustainable an integrated business model

from upstream to downstream’

• Pertamina is not an expert on plantation, thus we are inviting plantation company

to become one of our strategic partner in developing and end to end biofuel

business scheme

PERTAMINA | 11

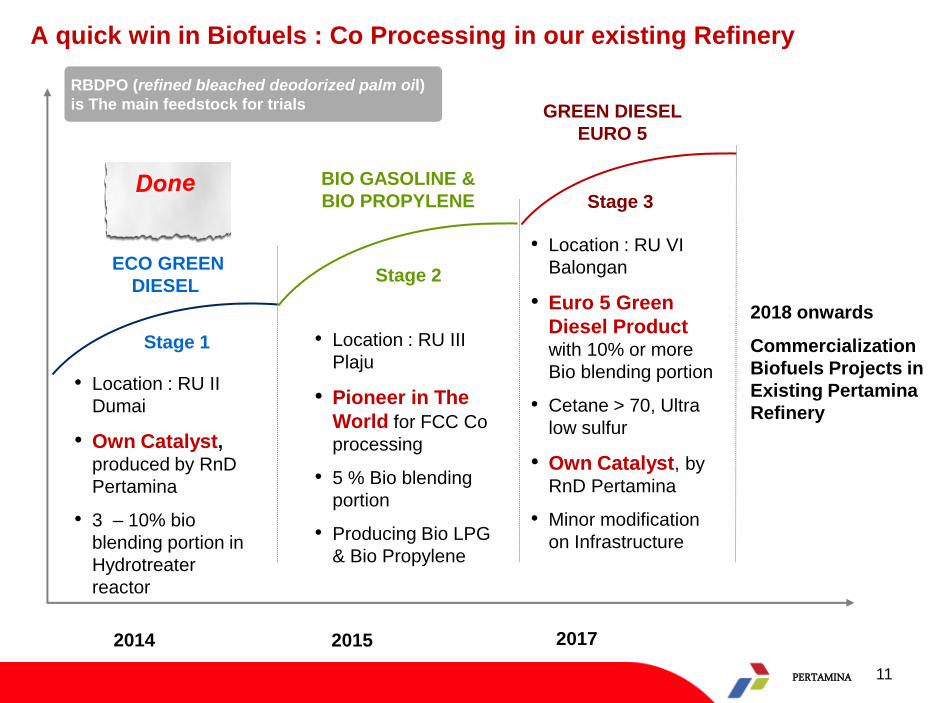

ECO GREEN

DIESEL

BIO GASOLINE &

BIO PROPYLENE

Stage 1

Stage 2

Stage 3

2015

GREEN DIESEL

EURO 5

• Location : RU II

Dumai

• Own Catalyst, produced by RnD

Pertamina

• 3 – 10% bio

blending portion in

Hydrotreater

reactor

• Location : RU III

Plaju

• Pioneer in The

World for FCC Co

processing

• 5 % Bio blending

portion

• Producing Bio LPG

& Bio Propylene

• Location : RU VI

Balongan

• Euro 5 Green

Diesel Product with 10% or more

Bio blending portion

• Cetane > 70, Ultra

low sulfur

• Own Catalyst, by

RnD Pertamina

• Minor modification

on Infrastructure

2017 2014

A quick win in Biofuels : Co Processing in our existing Refinery

RBDPO (refined bleached deodorized palm oil)

is The main feedstock for trials

2018 onwards

Commercialization

Biofuels Projects in

Existing Pertamina

Refinery

PERTAMINA | 12

Agenda

• Background

• Pertamina Future Strategic Developments in Biofuel

- Co Processing

- Integrated Stand Alone Refinery

• Conclusions

PERTAMINA |

▪ Indonesia will face an energy challenge in the future, Biofuel will play a

very strategic role.

▪ PERTAMINA consistently supports government’s biofuel mandate and

will target 15 % of sales will be from biofuels in 2025

▪ PERTAMINA is committed to develop 2nd Generation biofuels with

integrated project approach

▪ Partners in Plantation and Process Licensor plays an important role in

2nd generation Biofuels projects

▪ Total investment required for all 3 Biofuel projects is 1.8 bio USD (incl.

Upstream investment). Projects coverage is up to 5% of total demand

▪ Pertamina still holds majority market shares in National fuel demand.

Partnering with Pertamina will be a strategic decision for investor.