37

Indonesia’s Largest, Fastest Growing, World Class Hospital Group PT Siloam International Hospitals Tbk

Indonesia’s Largest, Fastest Growing,

World Class Hospital Group

PT Siloam International Hospitals Tbk

Disclaimer

This presentation has been prepared by PT Siloam International Hospitals, Tbk (SILO ) and is circulated for the purpose of general

information only. It is not intended for any specific person or purpose and does not constitute a recommendation regarding the securities

of SILO. No warranty ( expressed or implied ) is made to the accuracy or completeness of the information. All opinions and estimations

included in this report constitute our judgment as of this date and are subject to change without prior notice. SILO disclaims any

responsibility or liability whatsoever arising which may be brought against or suffered by any person as a result of reliance upon the

whole or any part of the contents of this presentation and neither SILO nor any of its affiliated companies and their respective

employees and agents accept liability for any errors, omission, negligent or otherwise, in this presentation and any inaccuracy herein or

omission here from which might otherwise arise.

Forward – Looking Statements

The information communicated in this presentation contains certain statements that are or may be forward looking. These statements

typically contain words such as “will”, “expects” and “anticipates” and words of similar import. By their nature, forward looking statements

involve a number of risks and uncertainties that could cause actual events or results to differ materially from those described in this

presentation. Factors that could cause actual results to differ include, but are not limited to, economic, social, and political conditions in

Indonesia ; the state of the property industry in Indonesia; prevailing market conditions; increases in regulatory burdens in Indonesia,

including environmental regulation and compliance cost; fluctuations in foreign currency exchange rates; interest rate trends, cost of

capital and capital availability; the anticipated demand and selling prices for SILO developments and related capital expenditures and

investments; the cost of construction; availability of real estate property; competition from other companies and venues; shifts in

customer demands; changes in operation expenses, including employee wages, benefits, and training, governmental and public policy

changes; SILO’s ability to be and remain competitive; SILO’s financial condition, business strategy as well as the plans and objectives of

SILO’s management for future operations; generation of future receivables; and environmental compliance and remediation. Should one

or more of these uncertainties or risks, among others, materialize, actual results may vary materially from those estimated, anticipated

or projected. Specifically, but without limitation, capital costs could increase, projects could be delayed and anticipated improvements in

production, capacity or performance might not be fully realized. Although SILO believes that the expectations of its management as

reflected by such forward –looking statements are reasonable based on information currently available to us, no assurances can be

given that such expectations will prove to have been correct. You should not unduly rely on such statements. In any event, these

statements speak only as of the date hereof, and SILO undertakes no obligation to update or revise any of them, whether as a result of

new information, future events or otherwise.

Contents

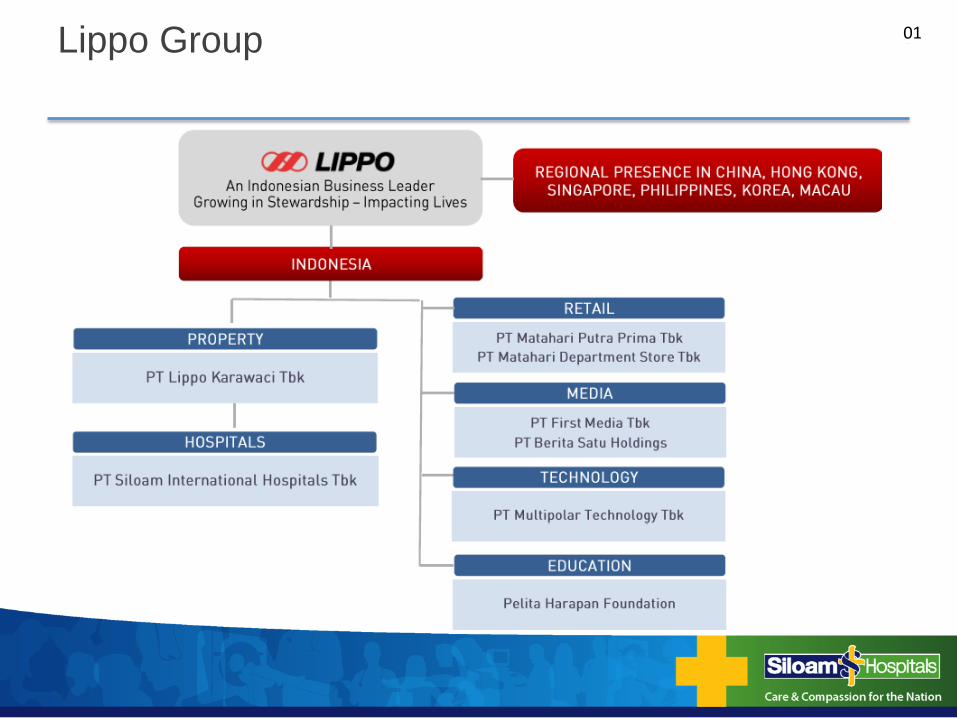

Lippo Group 01

Where We Are In Lippo Karawaci 02

Highly Experienced & Professional Management 03

The Vision 04

Nationwide Hospitals Network & Market Catchment 05

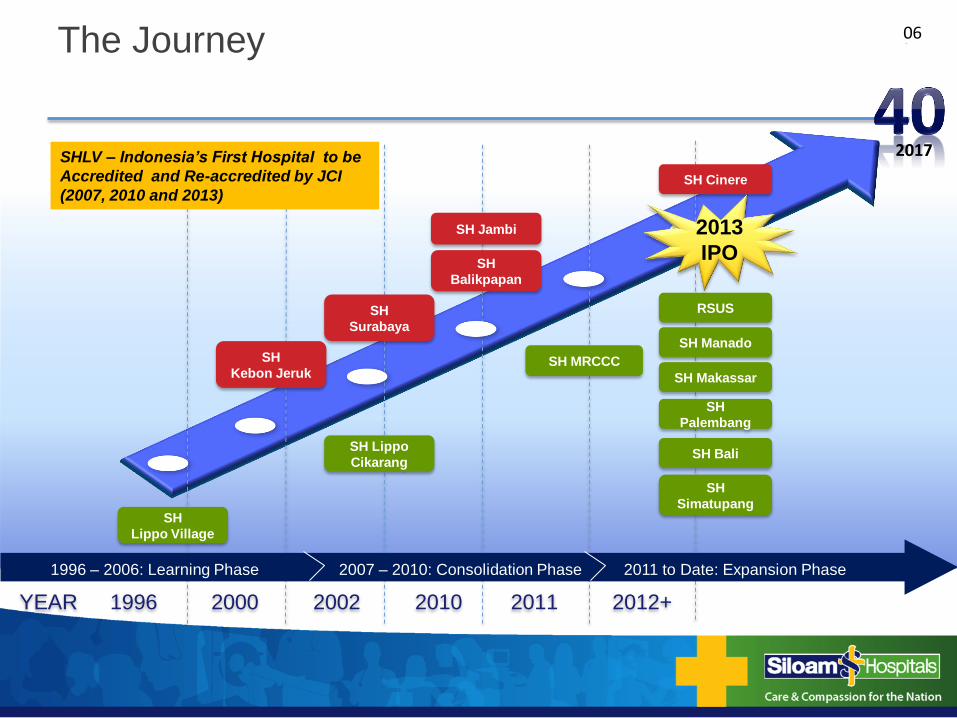

The Journey 06

The Landscape 07 - 09

The Strategy & Business Model 10 - 12

Premier Private Hospital Group 13 - 15

Operational & Financial Performance 16 - 25

Management Focus 26

Appendices 27 - 33

4

Lippo Group 01

5

Where We Are In Lippo Karawaci 02

6

Highly Experienced & Professional Management

Board of

Directors

dr. Gershu Paul

President Director dr. Grace Frelita

Director, Global

Quality Development

Romeo Lledo

Director, Accounting

and Finance

Prof. George Mathew

President, MRIN, UPH

& UPHMS*

dr. Anang Prayudi

Director, Strategy and

Development

S.Budisuharto

Director, Network and

Marketing

Development Group

Board of

Commisioners

Ketut Budi Wijaya

President

Commissioner

Theo L. Sambuaga

Commissioner

Agus Benjamin

Commissioner

Ir. Jonathan L. Parapak

Independent

Commissioner

Farid Harianto

Independent

Commissioner

Prof. Dr. H. Muladi, S.H

Independent

Commissioner

03

*) Universitas Pelita Harapan Medical Science Group

7

Reach

Scale

International Quality

The Vision

Affordable and Accessible Healthcare

to all socio economic segments

Godly

Compassion

5 Year Vision… • Beds

3,000 to 10,000

• Patients per annum

1.5 million to 15 million

• Hospitals

14 to 40 hospitals

11 to over 25 cities

04

8

Nationwide Hospitals Network & Market

Catchment

05

1 Siloam Hospitals Lippo Village

2 Siloam Hospitals Kebon Jeruk

3 Siloam Hospitals Surabaya

4 Siloam Hospitals Cikarang

5 Siloam Hospitals Jambi

6 Siloam Hospitals Balikpapan

7 MRCCC

8 RSUS (Siloam General Hospital)

9 Siloam Hospitals Manado

10 Siloam Hospitals Makassar

11 Siloam Sriwijaya

12 Siloam Hospitals Cinere

13 Siloam Hospitals Bali

14 Siloam Hospitals Simatupang

Sumatra Population :

50.6 mio

Kalimantan Population :

13.8 mio

Java Population :

136.6 mio

Sulawesi Population :

17.4 mio

Papua Population :

3.6 mio

Bali Population :

3.9 mio

Nusa Tenggara Population :

9.2 mio

Maluku Population :

2.6 mio

Greater Jakarta Population :

28 mio

Jakarta Population :

10 mio Opening in 2015 – 2017

Operating hospitals Opening in 2H 2013-2014

18 -20 hospitals

6-8 hospitals

Current

Direct Target Market

Population – 33 Million

19 hospitals currently in various

stages of development

9

The Journey

YEAR 1996 2000 2002 2010 2011 2012+

SH MRCCC

SH Lippo

Cikarang

SH

Lippo Village

SH

Kebon Jeruk

SH

Balikpapan

SH Jambi

SH

Surabaya

1996 – 2006: Learning Phase 2007 – 2010: Consolidation Phase 2011 to Date: Expansion Phase

RSUS

SH Manado

SH Makassar

SH

Palembang

SH Bali

SHLV – Indonesia’s First Hospital to be

Accredited and Re-accredited by JCI

(2007, 2010 and 2013) SH Cinere

SH

Simatupang

06

2017

2013

IPO

10

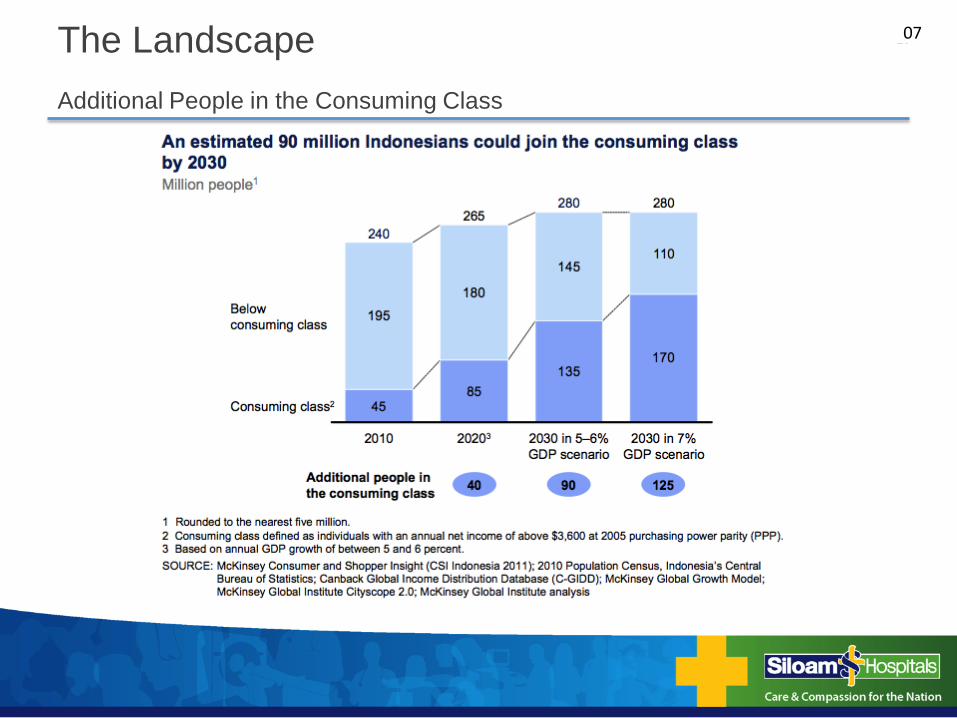

Additional People in the Consuming Class

The Landscape 07

11

Demography Profile

The Landscape

58% Coverage

Communicable Diseases

13%

Cardiovascular Diseases

31% Cancer

18%

Other Chronic Diseases

28%

Injuries 10%

Communicable Diseases

28%

Cardiovascular Diseases

30%

Cancer 13%

Other Chronic Diseases

20%

Injuries 9%

2008 2030

Relatively Young Population is Expected to Sustain in the Future

Changing Disease Pattern Morbidity Per Capita Healthcare Expenditure

2012 2018

USD 109 USD 237 Doubles in 6 years

Succeeding 20 Years

40%

Source: United Nations, Department of Economic and Social Affairs, Population Division (2011), Frost & Sullivan Estimates, Ministry of Health.

10.3 10.8 10.5 10.5 10.6 10.8 10.5 9.7 8.8 7.6 6.3 4.8 3.5 2.9 2.3 3.9

10.7 11.3 10.9 10.8 10.8 10.8 10.3 9.5 8.7 7.6 6.3 4.8 3.3 2.4 1.8 2.7

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

2012 Indonesian Population (mm) by Age and Gender

Female Male

• Life expectancy at birth is 68 years

• 50% of the population under 30 years

• Consistent population band for next 30 years

08

12

70,655 doctors v. Global: Shortage of 267,000 doctors(1)

v. OECD: Shortage of 718,086 doctors(1)

0.30 0.31

0.74

1.26

1.48

1.77

2.31

2.79

0.00

0.50

1.00

1.50

2.00

2.50

3.00

TH Indo India MY China SG US UK

0.97 1.02

1.63

2.01

2.16

2.84 2.84 2.95

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Indo India MY TH SG UK US China

Severely Underserved Healthcare Markets

The Landscape

238,373 beds v. Global: Shortage of 229,491 beds (1) v. OECD: Shortage of 977,189 beds (1)

Doctors /1,000 population

OECD Average = 4.93

Beds /1,000 population

Note: (1) Calculated based on global average beds and doctors per 1,000 population ratios. (2) Latest available data for Thailand as of 2009. Source: Respective countries’ ministries of health, WHO, OECD.

OECD Average = 3.14

• Indonesia’s bed to population ratio way below global average

• Ample opportunity for private healthcare operators to fill the supply gap

• Doctor to population ratio also way below global average

• Ability to attract and retain doctors and specialists is a critical success factor for hospitals

Lack of Beds…

and Qualified Doctors…

(2) (2)

Global Average = 3.0

Global Average = 1.4

09

13

4 Pillar Foundation

The Strategy & Business Model

Siloam Hospitals’ four pillar foundation has been key to the success of our existing hospitals

and will serve as the basis for replicating this success at our expansion hospitals…

1

Emergency

Excellence in

Emergency Services

500-911

2

Technology

3

Telemedicine

4

Doctors

State-of-the-Art

Medical Equipment

and Systems

Digital Telemedicine

“Hub and Spoke”

Siloam Doctor

Partnership and

Development

Program

4 Pillar Foundation

10

14

Clinical Service Delivery

The Strategy & Business Model

• Primary clinics for corporate clients

• Public-Private-Partnership (PPP) model - Siloam Puskesmas (Public Health

Clinic)

• RSUS – First general hospital using public sector model

– Additional demand from patients under governmental insurance and social

schemes

– Gateway to Indonesia’s “Universal Healthcare Coverage” and Government

Health Insurance Programs

• Specialist access for

primary healthcare

demand

• Public-Private-

Partnership

• High standard and

accessible medical

care through focus

on clinical

governance and

affordable price

points

• Access to

Centres of

Excellence

through hub and

spoke system

and Tele-

medicine

3

2

1

Siloam’s

Integrated Healthcare

Delivery Model

Primary

Secondary

Tertiary

Research and Education • Integrated platform with UPHMS and other partnerships

• Medical students training at RSUS, SHLV, and SHKJ

• Integrated Centres of Excellence: Neuroscience, Cardiology, Cancer, Orthopedic, Urology,

Fertility

• Hub and Spoke strategy and extensive coverage of specialised services via Digital Tele-Medicine

• Pioneering investments in Indonesia’s healthcare sector

– Comprehensive Cancer Centre opened in 2011

– Indonesia’s first Gamma Knife installed in 2012

• Best in class and highly accessible healthcare services platform

through:

– Rapid expansion of hospital network across Indonesia

– Attracting and retaining the best doctors with strong focus on

doctors’ welfare (SDPDP)

– Equip hospitals with State-of-the-Art facilities such as 128 slice

CT Scan and 1.5T MRI

One-stop continuum of care at primary, secondary, tertiary and quaternary levels

Quaternary

11

15

UPHMS (UPH Medical Sciences)

The Strategy & Business Model

Centre of Excellence and

Global Reputation

• Alignment – across

teaching and service

delivery

• Affiliate with agencies

such as

ACORN/NUS/SGH/UOM

• Leading edge research

• Best practice Models

• Remote Access Diagnosis (RAD)

and Remote Access Clinical

Management (RACM)

• Telemedicine

• Centres of Clinical Excellence/

Accreditation

• Teaching Hospital paradigm

• Future workforce

• Systems based curriculum

converged with PBL

• Best practice replication

• Clinical placement

• Foundation for Innovation

• Overseas training –

Singapore/Australia/USA/China

UPHMS (UPH Medical Sciences)

·

Education Research

Clinical

12

16

Our Hospitals (Mature and Developing)

Premier Private Hospital Group

TANGERANG (West of Jakarta)

SILOAM HOSPITALS LIPPO VILLAGE

WEST JAKARTA

SILOAM HOSPITALS KEBON JERUK

EAST JAVA

SILOAM HOSPITALS SURABAYA

BEKASI (East of Jakarta)

SILOAM HOSPITALS CIKARANG

JCIA 322 Bed Capacity

228 GP and Specialists

455 Nurses

Centre of Excellence : Neurosience &

Heart Centre

279 Bed Capacity

213 GP and Specialists

325 Nurses

Centre of Excellence : Urology &

Orthopaedic

182 Bed Capacity

80 GP and Specialists

272 Nurses

Centre of Excellence : Fertility Centre

110 Bed Capacity

134 GP and Specialists

158 Nurses

Centre of Excellence : Occupational Health

EAST SUMATERA

SOUTH JAKARTA

SILOAM HOSPITALS JAMBI

MRCCC SILOAM SEMANGGI

331 Bed Capacity

155 GP and Specialists

255 Nurses

Centre of Excellence : Cancer Centre

106 Bed Capacity

57 GP and Specialists

135 Nurses

EAST KALIMANTAN

SILOAM HOSPITALS BALIKPAPAN

228 Bed Capacity

80 GP and Specialists

186 Nurses

83% Ownership

79.6% Ownership

13

17

SOUTH JAKARTA

SILOAM HOSPITALS TB SIMATUPANG

269 Bed Capacity

70 GP and Specialists

41 Nurses

Centre of Excellence : Emergency,

cardiology, oncology &

neuroscience

New Hospitals in 2012 to 2013

Premier Private Hospital Group

TANGERANG (West of Jakarta)

SILOAM GENERAL HOSPITAL (RSUS)

733 Bed Capacity

20 GP and Specialists

143 Nurses

NORTH SULAWESI

SILOAM HOSPITALS MANADO

231 Bed Capacity

76 GP and Specialists

188 Nurses

Centre of Excellence : Emergency

SOUTH SULAWESI

SILOAM HOSPITALS MAKASSAR

360 Bed Capacity

77 GP and Specialists

140Nurses

Centre of Excellence : Cardiology &

Emergency

BALI

SILOAM HOSPITALS BALI

281 Bed Capacity

82 GP and Specialists

133 Nurses

Centre of Excellence : Emergency,

medical tourism, orthopaedics &

cardiology

DEPOK (South of Jakarta)

SILOAM HOSPITALS CINERE

21 Bed Capacity

11 GP and Specialists

51 Nurses

Centre of Excellence: Cardiology

SOUTH SUMATERA

SILOAM HOSPITALS PALEMBANG

347 Bed Capacity

86 GP and Specialists

168 Nurses

14

18

Hospitals under Construction

Premier Private Hospital Group

NORTH SUMATERA

SILOAM HOSPITALS MEDAN

EAST NUSA TENGGARA

SILOAM HOSPITALS KUPANG

WEST JAVA

SILOAM HOSPITALS BANDUNG

CENTRAL JAVA

SILOAM HOSPITALS SEMARANG

EAST JAVA

SILOAM HOSPITALS SURABAYA

EXTENSION

There are currently 19 sites under

various stages of development

15

Operational & Financial

Performance For The 9 Months Ended September 30, 2013

Completed a successful initial public offering of Siloam International Hospitals

- Listed on September 12, 2013

- Priced at Rp 9,000 per share

- Raised total proceeds of IDR 1,405 bn

Siloam Hospitals Bali (SHDP), opened on January 1, 2013, turned EBITDAR

positive on the 6th month

Siloam Hospitals TB Simatupang (SHTB) opened on July 1, 2013 and is

performing to plan

Strong momentum in operations as developing hospitals increase their

contribution to revenue and EBITDAR, and new hospitals turn EBITDAR positive

Slight drag on 3Q 2013 primarily due to:

- Slight decrease in patient visits due to fasting month

- Delay in commissioning Medan and Kupang and the resulting staff cost

due to timing

Q3 2013 Highlights 17

21

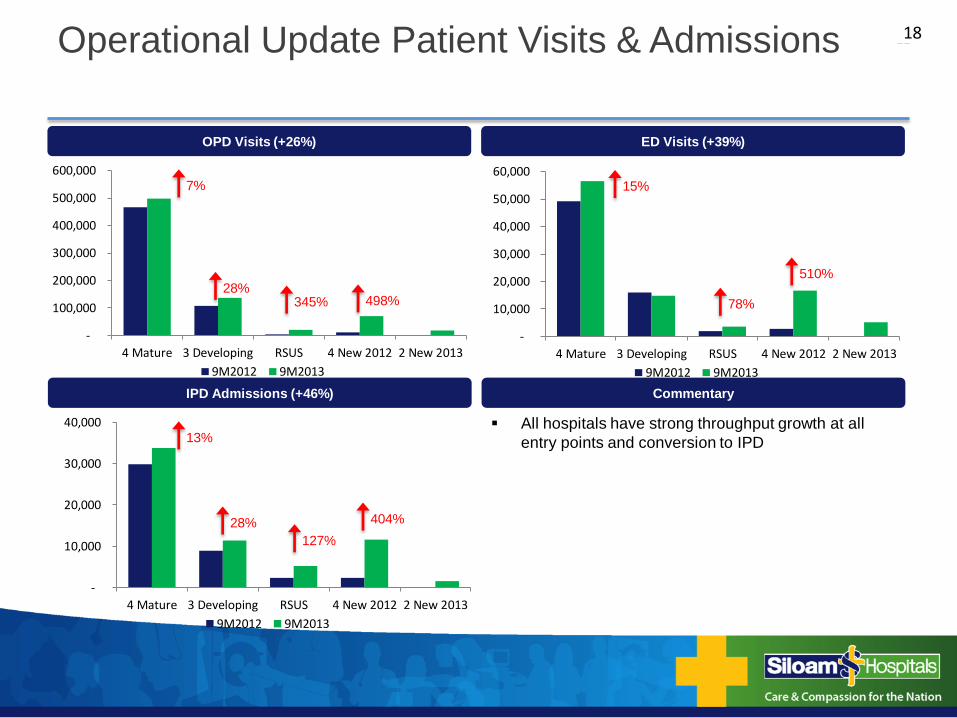

4 Mature 3 Developing RSUS 4 New 2012 2 New 2013

-

100,000

200,000

300,000

400,000

500,000

600,000

9M2012 9M2013

ED Visits (+39%) OPD Visits (+26%)

7%

28% 345% 498%

4 Mature 3 Developing RSUS 4 New 2012 2 New 2013

-

10,000

20,000

30,000

40,000

50,000

60,000

9M2012 9M2013

15%

78%

510%

4 Mature 3 Developing RSUS 4 New 2012 2 New 2013

-

10,000

20,000

30,000

40,000

9M2012 9M2013

13%

28%

127%

404%

Commentary IPD Admissions (+46%)

Operational Update Patient Visits & Admissions

All hospitals have strong throughput growth at all

entry points and conversion to IPD

18

22

Siloam is the clear leader and fastest growing private hospital group in Indonesia serving all segments of the population

Strong Financial Performance

737 890

1,030

1,259

1,788 1,830

2008 2009 2010 2011 2012 9M2013

102 114

140 155

221

201

2008 2009 2010 2011 2012 9M2013

Total Revenue EBITDA ( In Rp Bn ) ( In Rp Bn )

+21%

+16%

+22%

+42%

+12%

+23%

+10%

+43%

19

Notes: *) Audited figures for 9 months ended September 30, 2013 **) EBITDA refers to income before depreciation, provisions for post-employment benefits, allowance for impairment in value, corporate income taxes and other expense and/or income (consisting primarily of financing income and others-net).

*

*

23

Gross Operating Revenue 1,829.8 1,263.2 44.9%

Service Charge 493.4 367.9 34.1%

Net Operating Revenue 1,336.4 895.4 49.3%

Material Cost 594.3 419.8 41.6%

Gross Margin 742.1 475.5 56.0%

Operating Expenses 483.2 284.3 70.0%

EBITDAR 258.8 191.2 35.3%

% to GOR 14.1% 15.1%

Rent 24.5 11.9 105.1%

HO Expenses 33.1 22.9 44.4%

EBITDA 201.3 156.4 28.7%

% to GOR 11.0% 12.4%

9M2012 ∆%Description 9M2013

Q3 Results

Revenue & EBITDA Analyses 20

New Hospitals 2013

- SHDP, opened on January 1, 2013, performing as planned. Hit positive EBITDAR on the 6 th month.

- SHTB, opened on July 1, 2013, performing within plan.

New Hospitals 2012

- SHMK and SHPL are generating EBITDAR of 10% to GOR in Q3, exceeding expectations.

Commentary

(i) In IDR Bn

Notes: (i) Represents rental expenses for the land and buldings, Siloam is leasing from FREIT, PT Lippo Karawaci Tbk and other party. PT Lippo Karawaci started charging rent for

the land and buildings of 9 hospitals on May 1, 2013. (see note 34 of the audited financial statement as of and for the periods ended September 30, 2012 and 2013) (ii) EBITDA refers to income before depreciation, provisions for post-employment benefits, allowance for impairment in value, corporate income taxes and other expense

and/or income (consisting primarily of financing income and others-net).

(i)

(ii)

24

76%

61%

20%

21%

13%

9M2012 9M2013

4 Mature 3 Developing RSUS 4 New 2012 2 New 2013

EBITDAR Contribution and Growth by Classification Revenue Contribution and Growth by Classification

Commentary

(Rp bn) (Rp bn)

+ 16.6% + 50.3%

+ 452.6% + 304.4%

93% 88%

8%

12%

4%

9M2012 9M2013

4 Mature 3 Developing RSUS 4 New 2012 2 New 2013

+ 28.2% + 91.6.0%

+ 8,390.0% + 52.8%

Significant Growth in GOR (44.9%) and EBITDAR (35.3%).

Developing and new hospitals category will continue to grow over 50% as these hospitals ramp-up their operations

to mature level.

Mature hospitals will continue to have annual growth ranging from 15% to 20%.

Q3 Results

Revenue & EBITDAR Growth

Note: EBITDAR refers to income before rent, HO expenses, depreciation, provisions for post-employment benefits, allowance for impairment in value, corporate income taxes and other expense and/or income (consisting primarily of financing income and others-net).

21

25

Revenue Contribution 9M2013

Commentary

(Rp bn) SHLC, 6% SHBP, 5%

SHMK, 4%

SHMN, 4%

SHPL, 3%

SHJB, 3%

SHDP, 3%

RSUS, 2% SHCN, 2%

SHTB, 0%

SHLV, 27%

SHKJ, 18%

MRCCC, 13%

SHSB, 10%

EBITDAR Contribution 9M2013

(Rp bn) SHLC, 7% SHBP, 5%

SHMK, 3%

SHMN, -1% SHPL, 1% SHJB, 0%

SHDP, -1% RSUS, -2% SHCN, 0% SHTB, -1%

SHLV, 45%

SHKJ, 21%

MRCCC, 6%

SHSB, 15%

Q3 Results

Revenue & EBITDAR Contribution by Hospital

Currently, the 4 mature hospitals (SHLV, SHKJ, SHSB and SHLC) contribute 61% and 88% to the consolidated

Revenue and EBITDAR of SIH, respectively.

As the hospitals ramp-up their operations to mature level, their contribution to total revenue and EBITDAR will

significantly change going forward.

22

Note: EBITDAR refers to income before rent, HO expenses, depreciation, provisions for post-employment benefits, allowance for impairment in value, corporate income taxes and other expense and/or income (consisting primarily of financing income and others-net).

26

Assets 12M2012 Assets 9M2013

Commentary

(Rp bn) (Rp bn)

Property and Equipment,

1,198 Cash & Cash Equivalent,

978

A/R, 253

Inventories, 80

Others, 170

Property and Equipment,

865

Cash & Cash Equivalent,

169

A/R, 187

Inventories, 75

Others, 290

Rp 2,680 Billion Rp 1,586 Billion

As of September 30, 2013 and December 31, 2012

Balance Sheet - Assets

Increase in cash and cash equivalent from Rp 169bn to Rp 978bn (5.8x) was primarily due to the proceeds of the

IPO in September 2013.

Increase in property and equipment from Rp 865bn in 2012 to Rp 1,198bn in 2013 was primarily due to the

investments in new hospitals in October 2012 to September 2013.

23

27

Liabilities + Equity 12M2012 Liabilities + Equity 9M2013

Commentary

(Rp bn) (Rp bn) Current Liabilities,

388

Non Current Liabilities,

700

Equity, 1,593

Rp 2,680 Billion

Non Current Liabilities,

1,074

Current Liabilities,

268

Equity, 245

Rp 1,586 Billion

As of September 30, 2013 and December 31, 2012

Balance Sheet – Liabilities + Equity

Increase in equity from 12M2012 to 9M2013 was primarily due to the IPO offering in September 2013 and

accumulated net profit of the period ended.

Decrease in non-current liabilities was due to the partial payment to parent company from the proceeds of the IPO.

24

Q4 has historically been the strongest performing quarter and we expect a similar

trend this year

All hospitals continue to perform within plan, and SHTB is expected to hit

EBITDAR positive by early 2014

Construction of Medan and Kupang hospitals is underway and are expected to

open and commence operations early 2014

Drivers for Q4 2013 and Looking Ahead to 2014 25

29

i. Dynamic plug and play hospital models to respond to market needs as well

as market changes.

ii. Execute a clear strategy to drive business focus and stewardship

accountabilities.

iii. Focus on partnering with doctors and clinical staff to help us on our journey

iv. Achieve seamless service by optimizing our people, process and

technology capacity and capability.

v. Customize marketing and promotion to maximize use of our service capacity

and capability and achieve our vision.

vi. Fulfill the demand side through Public Private Partnership (PPP).

vii. Drive economies of scale in healthcare through Managed Care schemes.

viii. Continue building Clinical Excellence in Indonesia.

Management Focus 26

Appendices

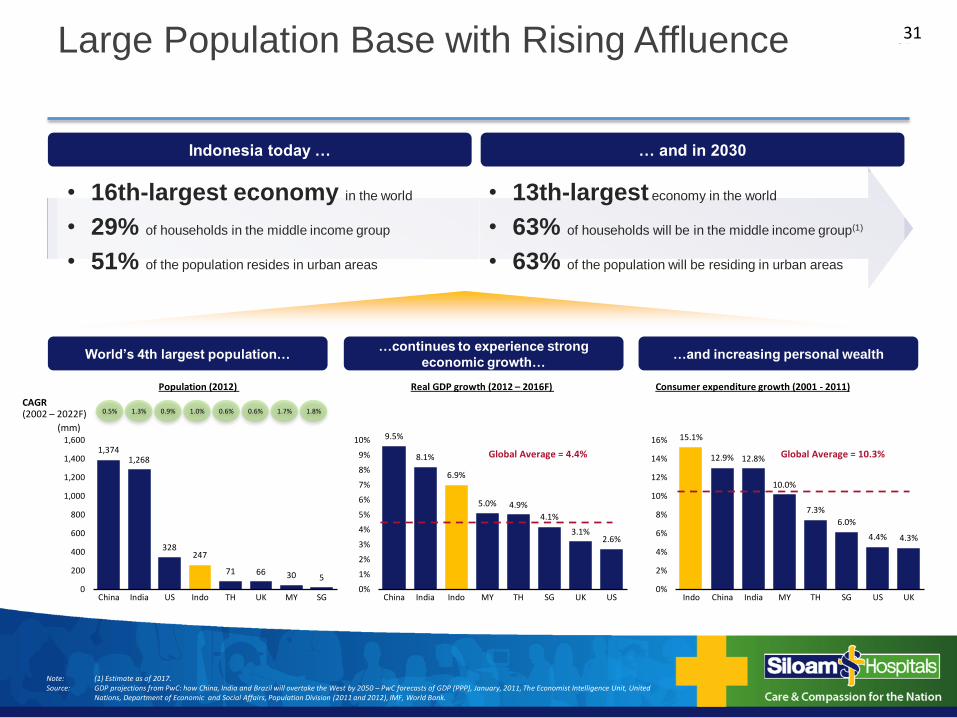

31

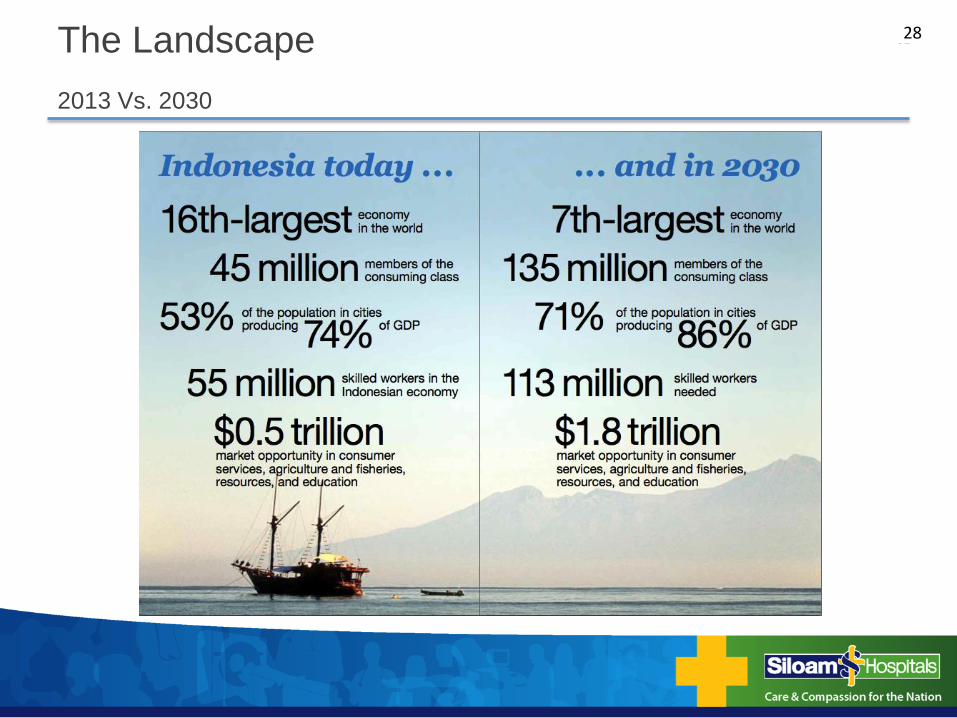

2013 Vs. 2030

The Landscape 28

32

Impressive Performance over the Past Decade

The Landscape 29

33

Population and Urbanization

The Landscape

A large population base with emerging middles class and rising affluence

Large and

Growing

Population

Base…

Experiencing

Rapid

Urbanization

Resulting in

Increasing

Spending

Expenditure

…

30

34

9.5%

8.1%

6.9%

5.0% 4.9%

4.1%

3.1% 2.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

China India Indo MY TH SG UK US

15.1%

12.9% 12.8%

10.0%

7.3%

6.0%

4.4% 4.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Indo China India MY TH SG US UK

Large Population Base with Rising Affluence

(mm)

Consumer expenditure growth (2001 - 2011) Real GDP growth (2012 – 2016F)

0.5% 1.3% 0.9% 1.0% 0.6% 0.6% 1.7% CAGR (2002 – 2022F)

Population (2012)

Note: (1) Estimate as of 2017. Source: GDP projections from PwC: how China, India and Brazil will overtake the West by 2050 – PwC forecasts of GDP (PPP), January, 2011, The Economist Intelligence Unit, United

Nations, Department of Economic and Social Affairs, Population Division (2011 and 2012), IMF, World Bank.

• 16th-largest economy in the world

• 29% of households in the middle income group

• 51% of the population resides in urban areas

• 13th-largest economy in the world

• 63% of households will be in the middle income group(1)

• 63% of the population will be residing in urban areas

Global Average = 4.4% Global Average = 10.3%

Indonesia today … … and in 2030

World’s 4th largest population… …continues to experience strong

economic growth… …and increasing personal wealth

1.8%

1,374 1,268

328 247

71 66 30 5

0

200

400

600

800

1,000

1,200

1,400

1,600

China India US Indo TH UK MY SG

31

35

63% Coverage

Healthcare Reforms and Universal Insurance

Coverage to Add Further Demand

Source: Center for Health Financing and Health Security (Insurance) (PPJK, MOH), WHO, Frost & Sullivan estimates

Indonesia healthcare reform program highlights

Government implementation of healthcare reform

platform to provide universal coverage

Insurance schemes established to enhance healthcare

accessibility:

Jamkesmas: public health insurance scheme that

serves the “poor” and “near poor”, forming the key

building block of universal coverage

JPK Jamsostek: life insurance scheme that has

health as an optional feature

Askes: health insurance for civil servants

Existing insurance schemes permit enrollees to seek

treatment in private hospitals

Government funds effectively channeled through

these schemes to the private sector

Private hospitals required to dedicate percentage of

beds to lower-income individuals

Healthcare coverage

2012 = 148 Million 2019 Target = 263 Million

100% Coverage

Total Healthcare Expenditure

Flow of public funding to private healthcare providers creates tremendous growth opporutnities for the private sector

2012 – 2018 CAGR: 16.8%

checked

2012 = 3.1% of GDP 2018F = 4.4% of GDP

US$59 Bn US$27 Bn

32

36

Excellence Asian Hospital Management

Awards (AHMA) 2011

Human Resources Development Category

Frost and Sullivan Healthcare

Services Provider of The Year

2010 & 2012

Ministry of Woman Empowerment Award

as The Best Mom and Child Hospital in

The Province

Awarded to Siloam Hospitals Lippo Village

Ministry of Health Hospital Management Award

2011 - The Best Accredited Hospital

Awarded to Siloam Hospitals Lippo Village

ISO 9001:2008 Certification for the

Management Hospitals Activity

Awarded to Siloam Hospitals Lippo

Cikarang (2011-2014)

AstraZeneca Infection

Management Award (Azima

Award) as the 1st winner

Siloam Hospitals Surabaya

Indonesia’s Most Admired Company

(IMAC) award as “The Best Building and

Managing Corporate Image” in Hospital

Category (2011, 2012 & 2013)

Indonesia Sustainable Awards 2012

Industry Champion Healthcare

Awards 33

37

Investor Relation

e-mail : [email protected]

Address:

Siloam Hospital Lippo Village 5th floor – Head Office

Jalan Siloam No.6

Lippo Village

Tangerang 15811

Indonesia

Telp : +62 21 25668000

Fax : +62 21 5460075

Website : www.siloamhospitals.com