46

Public Contracting Institute: FCPA Presentation September 28, 2016

Public Contracting Institute:FCPA Presentation

September 28, 2016

PwC

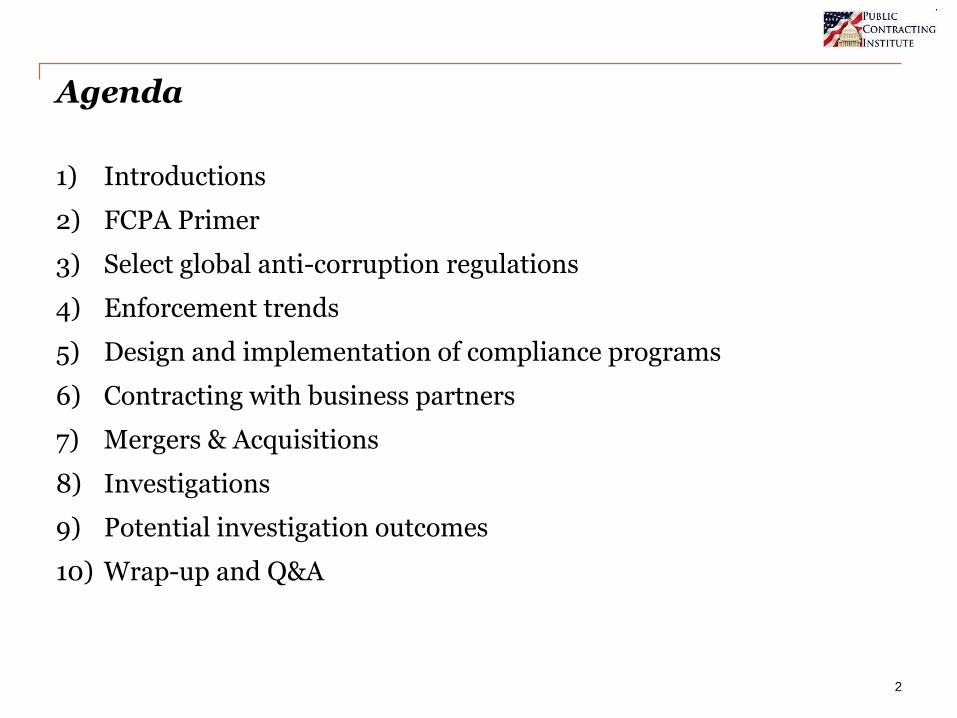

Agenda

1) Introductions

2) FCPA Primer

3) Select global anti-corruption regulations

4) Enforcement trends

5) Design and implementation of compliance programs

6) Contracting with business partners

7) Mergers & Acquisitions

8) Investigations

9) Potential investigation outcomes

10) Wrap-up and Q&A

2

PwC

Introductions

3

PwC

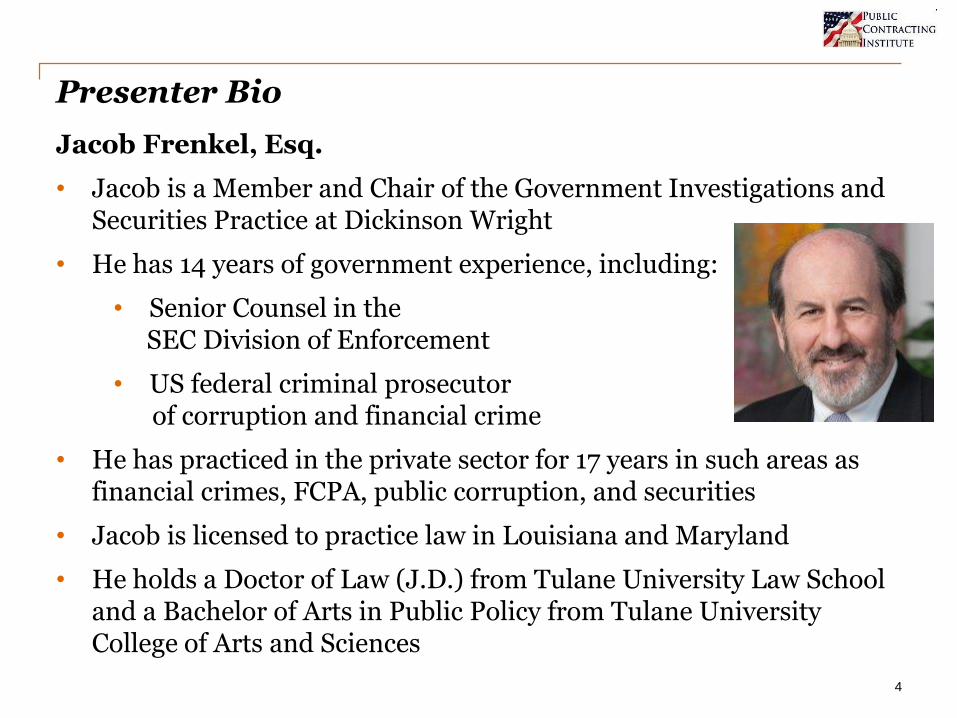

Presenter Bio

Jacob Frenkel, Esq.

• Jacob is a Member and Chair of the Government Investigations and Securities Practice at Dickinson Wright

• He has 14 years of government experience, including:

• Senior Counsel in the SEC Division of Enforcement

• US federal criminal prosecutor of corruption and financial crime

• He has practiced in the private sector for 17 years in such areas as financial crimes, FCPA, public corruption, and securities

• Jacob is licensed to practice law in Louisiana and Maryland

• He holds a Doctor of Law (J.D.) from Tulane University Law School and a Bachelor of Arts in Public Policy from Tulane University College of Arts and Sciences

4

PwC

Presenter Bio

James Gargas, MAcc, CPA, CFE, CFF

• James is the Senior Director in PwC’s Forensics Practice in Washington, D.C.

• He has 11 years of specialized anti-corruption experience, including:

• Cross-border corruption investigations;

• Anti-corruption compliance auditing;

• Compliance program build, implementation,

testing and refinement; and

• Investment-setting due diligence.

• James is a Certified Public Accountant (CPA), licensed in Ohio, Virginia and the District of Columbia. He is also a Certified Fraud Examiner and is Certified in Financial Forensics by the American Institute of Certified Public Accountants.

5

PwC

Polling Question #1

Question: What is your current role?

Answer Choices:

1) Legal

2) Compliance

3) Internal Audit

4) Procurement

5) Sales/Marketing

6) Accounting/Finance

7) Human Resources

6

PwC

Polling Question #2

Question: Is the facilitation payments exception within the

FCPA similar to most other anti-corruption statutes and the

OECD guidance?

Answer Choices:

1) Yes

2) No

3) I don’t know!

7

PwC

FCPA Primer

8

PwC

FCPA Primer

• FCPA enacted in 1977 to address bribery of foreign officials

• Violations:

◦ pays, offers to pay, or authorizes;

◦ the payment of money or anything of value;

◦ to a foreign official, foreign political party, candidate for political office, or official of a public international organization;

◦ to secure an improper business advantage

• Books and records provisions

◦ Make and keep books and records, which, in reasonable detail, accurately and fairly reflect the disposition of assets

• Internal controls

◦ Devise and maintain a system of internal controls to provide reasonable assurance that transactions are recorded appropriately

9

PwC

Select Global Anti-Corruption Regulations

10

PwC

Select global anti-corruption regulations

11

US FCPA and

China Anti-Corruption

Law (Criminal Code)

(1977)

False Claims Act (Amended

1986)

US Federal Sentencing Guidelines

(1991)

Inter –American Convention

Against Corruption (1996)

US FCPA (Amended

1998)

OECD Anti-Bribery

Convention (1997)

1980’s 1990’s 2000’s

US Travel Act(1961)

Sarbanes-Oxley Act

(2002)

PwC

Select global anti-corruption regulations

12

U.N. Convention

Against Corruption

(2005)

UK Bribery Act and Dodd-

Frank Act (2010)

Issuance of US FCPA Guidance

(2012)

Canadian CFPOA

(Amended 2013)

Issuance of UK Bribery Act

Guidance, and

China Anti-Corruption

Law Amended

(2011)

Brazil Clean Companies

Act(2013)

2000’s 2010’s

Indian Lokpal Bill

(2014)

Federal Law Against

Corruption in Public

Procurement (2012)

PwC

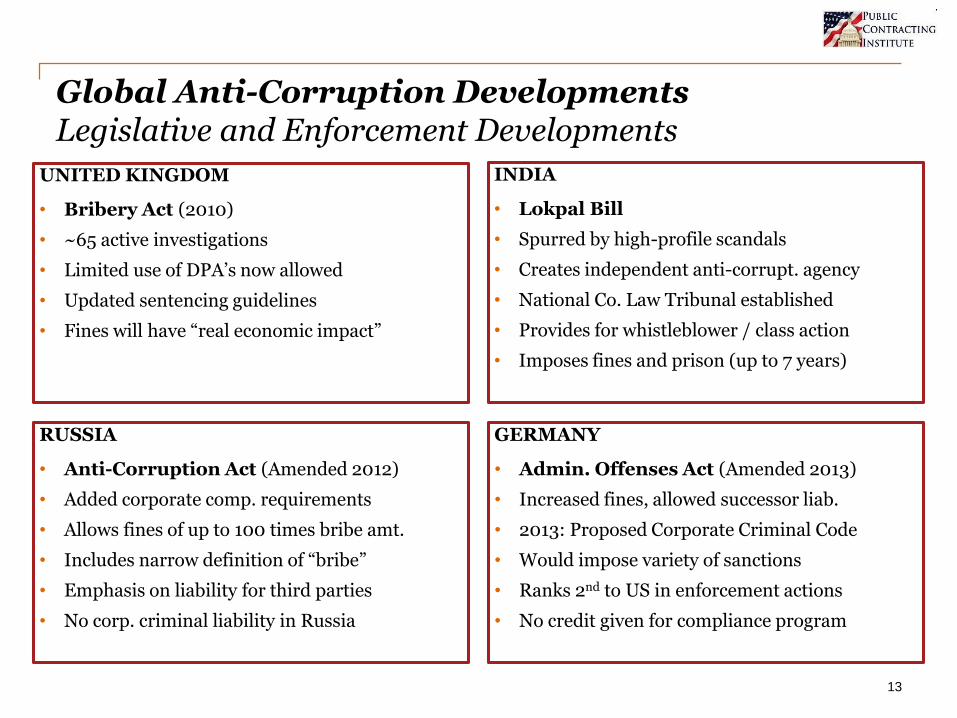

Global Anti-Corruption DevelopmentsLegislative and Enforcement Developments

GERMANY

• Admin. Offenses Act (Amended 2013)

• Increased fines, allowed successor liab.

• 2013: Proposed Corporate Criminal Code

• Would impose variety of sanctions

• Ranks 2nd to US in enforcement actions

• No credit given for compliance program

13

RUSSIA

• Anti-Corruption Act (Amended 2012)

• Added corporate comp. requirements

• Allows fines of up to 100 times bribe amt.

• Includes narrow definition of “bribe”

• Emphasis on liability for third parties

• No corp. criminal liability in Russia

INDIA

• Lokpal Bill

• Spurred by high-profile scandals

• Creates independent anti-corrupt. agency

• National Co. Law Tribunal established

• Provides for whistleblower / class action

• Imposes fines and prison (up to 7 years)

UNITED KINGDOM

• Bribery Act (2010)

• ~65 active investigations

• Limited use of DPA’s now allowed

• Updated sentencing guidelines

• Fines will have “real economic impact”

PwC

Global Anti-Corruption DevelopmentsLegislative and Enforcement Developments

BRAZIL

• Clean Companies Act (Aug. 2013)

• Civil statute, applicable only to entities

• Coexists with existing anti-bribery leg.

• Receiving training from US DOJ

• No exception for facilitation payments

• Credit given for compliance programs

14

CHINA

• Laws cover commercial and gov’t bribes

• Recent crackdown on domestic bribery

• Gov’t investigated 30K+ cases over 5 yrs

• New rules include background checks

• $1,500 is min. for bribe to be criminal

• Penalties include life in prison or death

CANADA

• CFPOA (Amended 2013)

• Received strong criticism from OECD

• Amendment imposed stricter rules

• Recent fine of USD 10.5M

• Recently convicted first individual

• No exception for facilitation payments

COLOMBIA

• Anti-Corruption Act (2011)

• OECD Anti-Bribery Convention in 2013

• New Presidential anti-corruption office

• Institutional reforms in progress

• CPI: Fallen from 59th to 94th in 10 years

• Inadequate regulatory mechanisms

PwC

Enforcement Trends

15

PwC

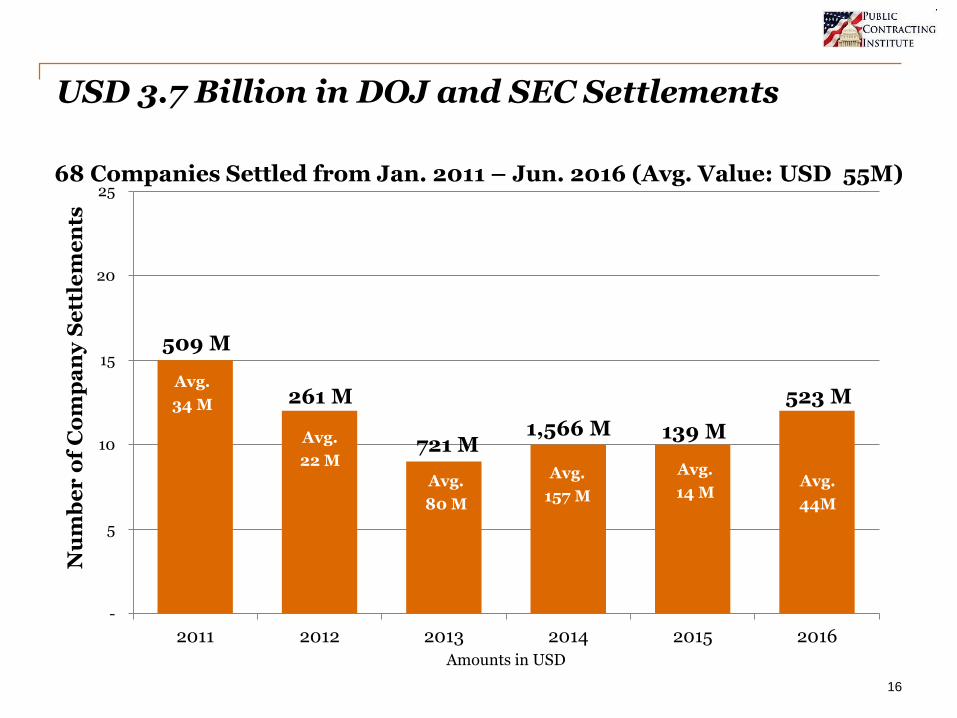

USD 3.7 Billion in DOJ and SEC Settlements

-

5

10

15

20

25

2011 2012 2013 2014 2015 2016

Nu

mb

er

of

Co

mp

an

y S

ett

lem

en

ts

Amounts in USD

721 M1,566 M

509 M

261 MAvg.

34 M

Avg.

80 M

Avg.

22 M

Avg.

80 M

Avg.

157 M

68 Companies Settled from Jan. 2011 – Jun. 2016 (Avg. Value: USD 55M)

139 M

Avg.

44M

16

523 M

Avg.

14 M

PwC

Current US Regulatory & FCPA TrendsIndividual SEC and DOJ Indictments Jan. 2011 – Jun. 2016

C-Suite (26)

• Vice President - 12• CEOs - 8• CFOs - 4• President - 2

Management (13)

• Director - 10• Controller - 2• Manager - 1

Employee (10)

• Other - 5• Employee - 3• Sales - 2

Third Party (1)

• Agent - 1

Board Member (2)

• Board Member - 2

17

PwC

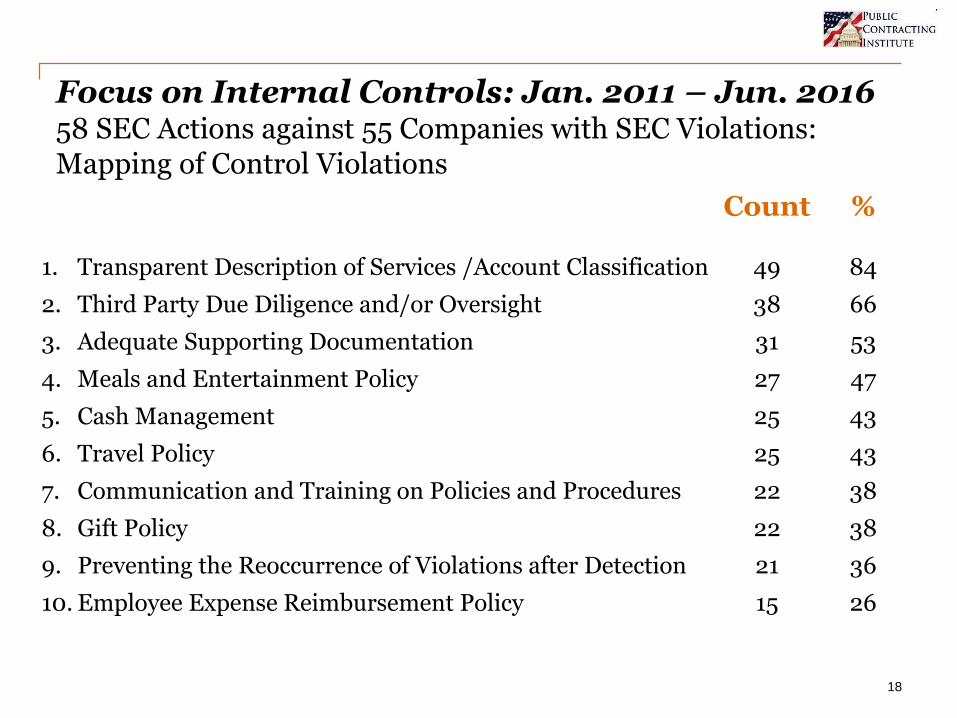

Count %

1. Transparent Description of Services /Account Classification 49 84

2. Third Party Due Diligence and/or Oversight 38 66

3. Adequate Supporting Documentation 31 53

4. Meals and Entertainment Policy 27 47

5. Cash Management 25 43

6. Travel Policy 25 43

7. Communication and Training on Policies and Procedures 22 38

8. Gift Policy 22 38

9. Preventing the Reoccurrence of Violations after Detection 21 36

10. Employee Expense Reimbursement Policy 15 26

Focus on Internal Controls: Jan. 2011 – Jun. 201658 SEC Actions against 55 Companies with SEC Violations: Mapping of Control Violations

18

PwC

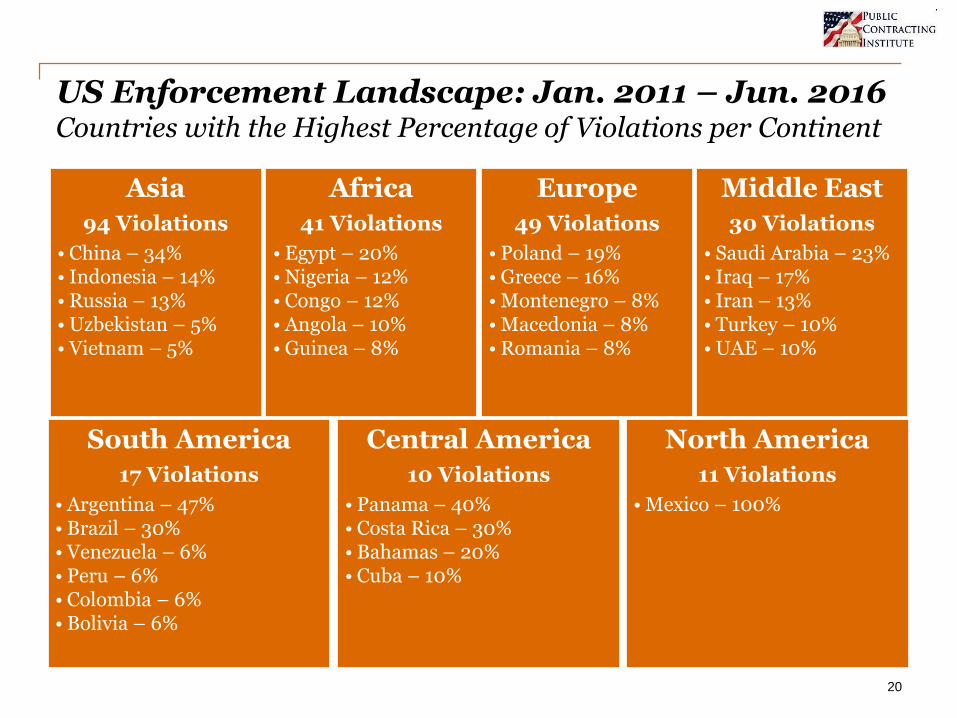

US Enforcement Landscape: Jan. 2011 – Jun. 201668 Companies and the Locations of their Violations

North America

11

Central America

10

South America

17

Asia

94

Africa

41

Europe

49

Middle East

30

19

PwC

Asia

94 Violations

• China – 34%• Indonesia – 14%• Russia – 13%• Uzbekistan – 5%• Vietnam – 5%

Africa

41 Violations

• Egypt – 20%• Nigeria – 12%• Congo – 12%• Angola – 10%• Guinea – 8%

Europe

49 Violations

• Poland – 19%• Greece – 16%• Montenegro – 8%• Macedonia – 8%• Romania – 8%

Middle East

30 Violations

• Saudi Arabia – 23%• Iraq – 17%• Iran – 13%• Turkey – 10%• UAE – 10%

South America

17 Violations

• Argentina – 47%• Brazil – 30%• Venezuela – 6%• Peru – 6%• Colombia – 6%• Bolivia – 6%

Central America

10 Violations

• Panama – 40%• Costa Rica – 30%• Bahamas – 20%• Cuba – 10%

North America

11 Violations

• Mexico – 100%

US Enforcement Landscape: Jan. 2011 – Jun. 2016Countries with the Highest Percentage of Violations per Continent

20

PwC

Recent Enforcement Trends and Hot Topics

• Increase in both Department of Justice (DOJ) and Securities and Exchange Commission (SEC) Settlements:

• Increasing company settlements in Q1 2016 compared to 2015.

• Fines and penalties in Q1 2016 represent a 259% increase from the total fines and penalties for the full year of 2015.

• Life Sciences industry is present in four of the eight settlements of Q1 2016, while the majority of the fines and penalties involved the Telecommunications industry.

• 50% of settlements of Q1 2016 include allegations of improper payments in China.

• Coordination of regulators globally:

• Continued coordination among SEC, DOJ and law enforcement and regulatory authorities in other countries (e.g., Brazil, Poland, UK).

21

PwC

IndustryCompany

Count Total

US Penalties

Aerospace & Defense 5 $37 M

Agriculture 1 $54 M

Chemicals 1 $384 M

Conglomerate 1 $50 M

Consumer Goods 7 $171 M

Energy 5 $709 M

Engineering & Construction

5 $276 M

Which Companies have violated the FCPA?

IndustryCompany

Count

Total US

Penalties

Entertainment/ Media 1 $9 M

Financial Services 3 $44 M

Industrial Products 8 $871 M

Life Sciences 16 $390 M

Technology 9 $219 M

Telecommunications 4 $504 M

Jan. 2011 – Jun. 2016

22

PwC

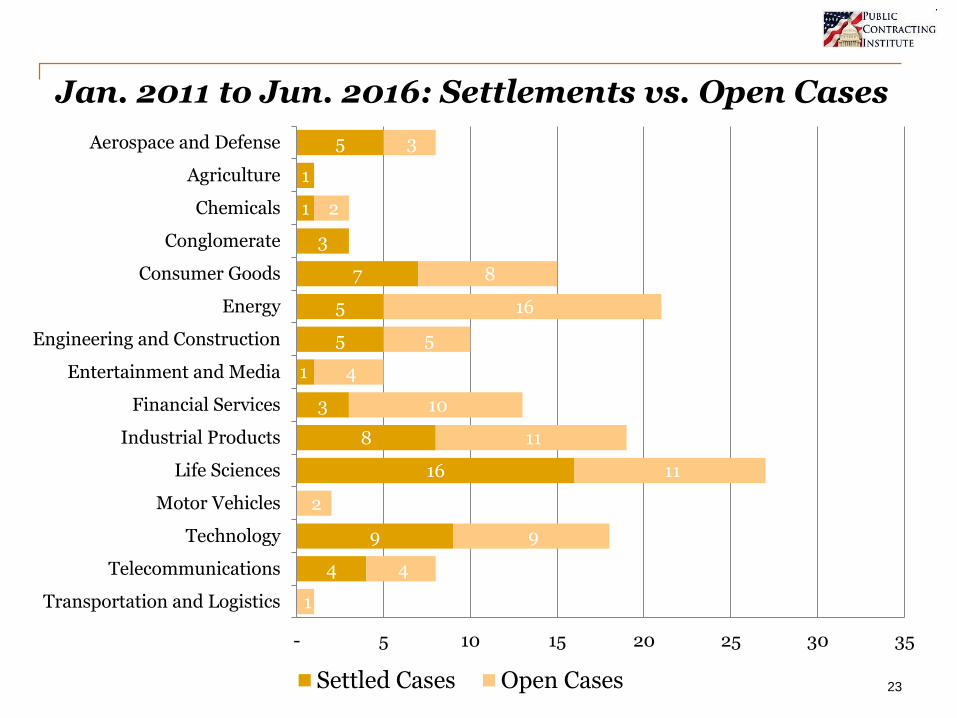

Jan. 2011 to Jun. 2016: Settlements vs. Open Cases

4

9

1

16

8

3

5

5

7

3

1

1

5

1

4

9

2

11

11

10

4

5

16

8

2

3

- 5 10 15 20 25 30 35

Transportation and Logistics

Telecommunications

Technology

Motor Vehicles

Life Sciences

Industrial Products

Financial Services

Entertainment and Media

Engineering and Construction

Energy

Consumer Goods

Conglomerate

Chemicals

Agriculture

Aerospace and Defense

Settled Cases Open Cases 23

PwC

Polling Question #3

Question: What region of the world has had the highest

number of corruption violations by US companies since 2011?

Answer Choices:

1) Europe

2) Africa

3) Asia

4) South America

24

PwC

Design and Implementation of Compliance Programs

25

PwC

Design and Implementation of Compliance ProgramsSentencing guidelines used as a starting point

• Seven Elements set forth in the Federal Sentencing Guidelines:

- Standards and Procedures

- Assign Compliance Responsibility

- Diligence in Delegation of Authority

- Communicate Effectively/Training

- Monitor & Audit

- Disciplinary & Incentive Mechanisms

- Respond Appropriately

26

PwC

Design and Implementation of Compliance ProgramsCompliance responsibility

• Direct and Regular Access to the Board

• Participates in Training Programs

• Credible with the Businesses

• Credible with the Regulators

• Sufficient Resources

• Credible with Auditors and Counsel

27

PwC

Contracting with Business Partners

28

PwC

Contracting with Business Partners

Representations and warranties to consider to mitigate corruption risk:

• Pledge not to engage in bribery of any kind;

• Promise to follow anti-corruption laws;

• Implement (or verify existence of) an anti-corruption compliance program;

• Inform partner if the business partner comes under any kind of investigation;

• Covenants encompassing all payments made by the business partner (e.g. no cash payments, no payments to tax havens without legitimate business purpose);

• Agreement to report all political contributions;

• No close relationships with foreign officials (e.g. foreign officials who own or are employees of the third party) and obligation to update if change;

• Guidance on invoicing and regular provision of documents (e.g. receipts for disbursements to government entities);

• Maintain adequate books and records for a minimum period of time (e.g. at least 7 years)

29

PwC

Mergers & Acquisitions (M&A)

30

PwC

Why conduct anti-corruption/FCPA due diligence?

• FCPA due diligence is now a clear regulatory expectation (e.g. US, UK, and more)

• Mitigate the risk of FCPA successor liability

• Mitigate the risk of penalties/fines

• Mitigate remediation costs

• Make any purchase price adjustments that may be required with respect to tainted revenue streams

• Get a “jump start” on implementing acquirer’s compliance program

31

PwC

Regulatory Expectations

DOJ and SEC encourage companies engaging in mergers & acquisitions to:

• Conduct thorough risk-based FCPA and anti-corruption due diligence on potential new business acquisitions

• Apply their code of conduct, compliance policies, and FCPA and other anti-corruption procedures as quickly as practicable to new acquisitions

• Train all levels of employees, and business partners and agents when appropriate, of merged or acquired companies on FCPA and other anti-corruption laws, the company’s code of conduct and compliance policies and procedures

• Conduct an FCPA-specific audit of all newly acquired or merged businesses as quickly as practicable

In some instances, the DOJ and SEC have declined to take action against companies that voluntarily disclosed and remediated conduct and cooperated with DOJ and SEC in the merger and acquisition context.

32

Source: A Resource Guide to the U.S. Foreign Corrupt Practices Act

PwC

Regulatory ExpectationsRecent FCPA deferred prosecution agreement

• The company should ensure that its target’s policies and procedures regarding anti-corruption laws and regulations apply as quickly as is practicable, but in any event no less than one year post-closing, to newly acquired businesses, and promptly:

• Train directors, officers, employees, agents, consultants, representatives, distributors, joint venture partners, and relevant employees thereof, who present corruption risk to the company, on the anti-corruption laws and regulations and the company’s related policies and procedures;

• Conduct an FCPA-specific audit of all newly acquired businesses within 18 months of acquisition

33

PwC

Polling Question #4

Question: Which of the following is NOT one of the reasons why

anti-corruption due diligence should be performed as part of a

merger or acquisition?

Answer Choices:

1) Mitigate the risk of fines/penalties

2) Jump start on implementing acquirer’s compliance program

3) Minimize the cost of SEC filing costs

4) FCPA due diligence is a regulatory requirement

34

PwC

Investigations

35

PwC

FCPA investigationsSource/Cause

• Disgruntled (or Entrepreneurial, in light of new Dodd-Frank Whistleblower Bounty Program) Employee/Whistleblower

• Competitor

• Internal/External Auditor

• SEC/DOJ

• Due Diligence (M&A)

36

PwC

FCPA investigations (continued)Main reasons to investigate

• Minimize possibility of intense government investigation, government sanctions and punitive damages

• Increase likelihood of favorable settlement

• Compliance with Sarbanes-Oxley has raised the stakes for non-compliance with the FCPA

- Section 302 – requires CEOs and CFOs to personally sign off on the accuracy of financial statements

- Section 404 – requires top executives to certify adequacy of internal controls over financial reporting

• Meet stakeholder expectations/potentially minimize litigation

37

PwC

FCPA investigations (continued)Benefits of external investigator

• FCPA, accounting, and investigative experience

• Credibility with regulators

• Expedited global coverage

• Impartial

• Independent

• Relieves internal time and resource constraints

38

PwC

FCPA investigations (continued)Typical red flags – Where to look

Overall Risk- Business Conditions

• High Risk Countries

Treasury

• Cash Payments

• Re-directed payments

• “Off the books” bank accounts or funds

Local Business Practices

• Compliance Sensitive Expenses

- Donations

- Political & Social Contributions

- Gifts

- Travel and Entertainment

Other Third Parties

• Processing Agents (e.g., Customs agents, Freight Forwarding agents)

• Consultants (e.g., tax consultants)

Payroll

• Non-employees paid through payroll (e.g., third parties)

Sales

• Use of commercial third parties

• Unusual Compensation Agreements

• Free products or services

39

PwC

FCPA investigations (continued)Potential work streams and procedures

• Interviews of Employees (and third parties)

• Analysis of Financial Data

• Analysis of E-mails

• Analysis of Third Party Contracts and Payments

• Reporting

40

PwC

FCPA investigations (continued)Decision to voluntarily disclose

Why to Disclose?

• Minimize Punishment

• Avoid Criminal Charges

• Limit Civil Charges

• Reduce Litigation Risk

• Deal with Violators Proactively

Why Not to Disclose?

• Allegation not yet Substantiated

• Trigger Government Investigation

• Negative Publicity

• Waiver of Privilege

41

PwC

Polling Question #5

Question: Which of the following would be considered a

compliance sensitive account that should be selected for further

review as part of an FCPA investigation?

Answer Choices:

1) Travel and Entertainment

2) Property, Plant and Equipment

3) Salaries Expense

4) Interest Income

42

PwC

Potential Investigation Outcomes

43

PwC

Potential Investigation Outcomes

• Fines

• Penalties

• Disgorgement

• Debarment

• Deferred Prosecution Agreement

• Non-Prosecution Agreement

• Cease & Desist Order

• Compliance Monitor

44

PwC

Presenter Information

Jacob Frenkel - Member, Dickinson Wright

(202) 466-5953

James Gargas – Senior Director, PwC Forensics

(202) 412-2352

45

PwC

Thank You!Any Questions?

46