Public Finance and Public Policy: Responsibilities and Limitations of Government Arye L. Hillman Cambridge University Press, 2009 Second edition Presentation notes, chapter 4 PUBLIC FINANCE FOR PUBLIC GOODS

Transcript

Public Finance and Public Policy: Responsibilities and Limitations of Government

Arye L. Hillman

Cambridge University Press, 2009

Second edition

Presentation notes, chapter 4

PUBLIC FINANCE FOR PUBLIC GOODS

Hillman, 2009: Public finance for public goods

2

Societies cannot rely on voluntary payments for prisoners-dilemma public goods and governments are called upon to levy taxes to finance public goods.

o We cannot rely on the Tiebout mechanism to reveal information about preferences because people with different preferences reside in the same jurisdiction

o We cannot rely on the Clarke tax

o Governments do not know subjective benefits ∑MB that

public goods provide to the people in a population

o Asymmetric information remains

Hillman, 2009: Public finance for public goods

3

We set aside political and bureaucratic principal-agent problems We hope that governments have been successful in using cost-benefit analysis to approximate efficient public spending

We shall not now ask normative questions about the desirable structure of taxation The question is positive: What are the consequences of using public finance to provide public goods?

Hillman, 2009: Public finance for public goods

4

The advantage of government:

Governments can resolve the free-rider problem by making payment for public goods compulsory through taxes

Hillman, 2009: Public finance for public goods

5

4.1 TAXATION

A. Efficient tax-financed public spending

The excess burden of taxation arises for both direct and indirect taxes:

A direct tax is paid when income is earned

An indirect tax is paid when income is spent

Hillman, 2009: Public finance for public goods

6

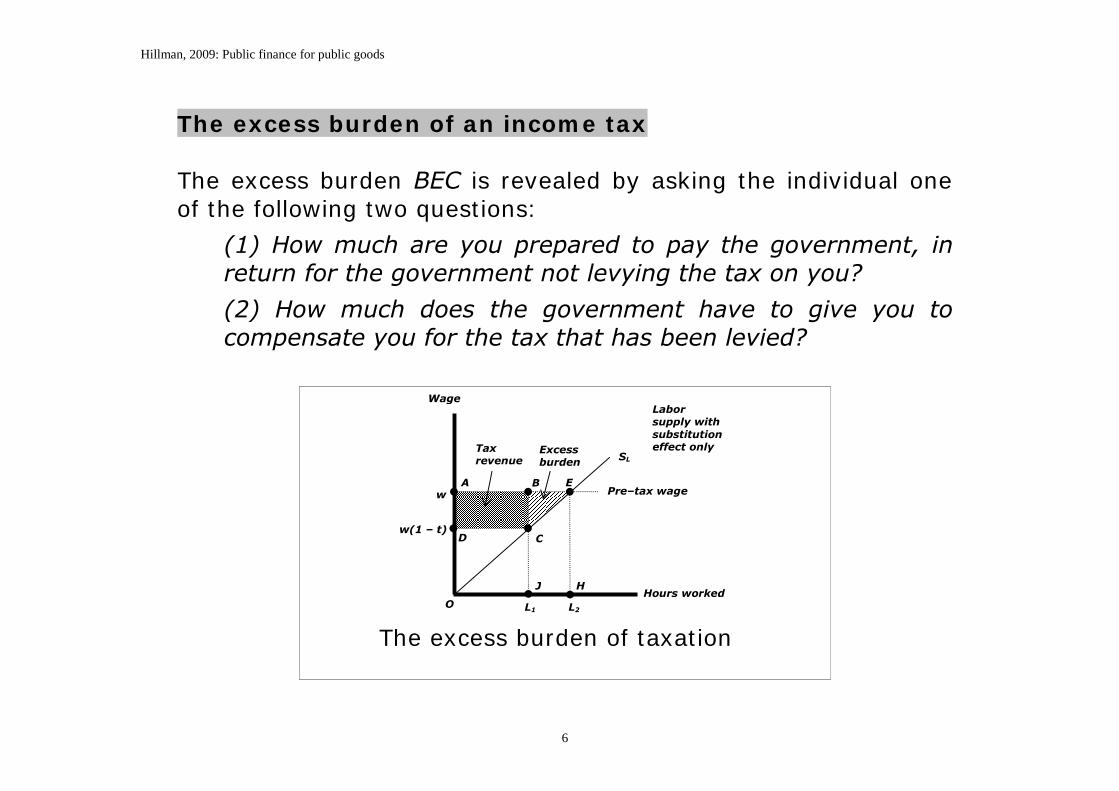

The excess burden of an income tax The excess burden BEC is revealed by asking the individual one of the following two questions:

(1) How much are you prepared to pay the government, in return for the government not levying the tax on you?

(2) How much does the government have to give you to compensate you for the tax that has been levied?

The excess burden of taxation

Hours worked O L1

J H

L2

Wage

w(1 – t)

A

D

E B

C

SL

w

Tax revenue

Excess burden

Pre–tax wage

Labor supply with substitution effect only

Hillman, 2009: Public finance for public goods

7

When there is only a substitution effect, and no income effect, the answer to the questions is the same: area BEC

The tax has imposed a greater cost than the money paid in taxes

No sum of money equal to the excess burden of taxation changes hands. The excess burden of taxation is invisible.

When the supply-of-labor function SL is linear, the area BEC is a triangle and the excess burden of taxation is

212 SLw L t

Measurement of the excess burden of taxation requires knowing the elasticity of labor supply SL

Hillman, 2009: Public finance for public goods

8

The elasticity of labor supply The previous figure showed a special case where SL = 1 The elasticity of labor supply can be constant or variable, depending on the form of the labor supply function.

A labor-supply function with an increasing elasticity of labor supply

Labor supply with substitution effect only

Wage

Hours worked O

SL

1

2

Hillman, 2009: Public finance for public goods

9

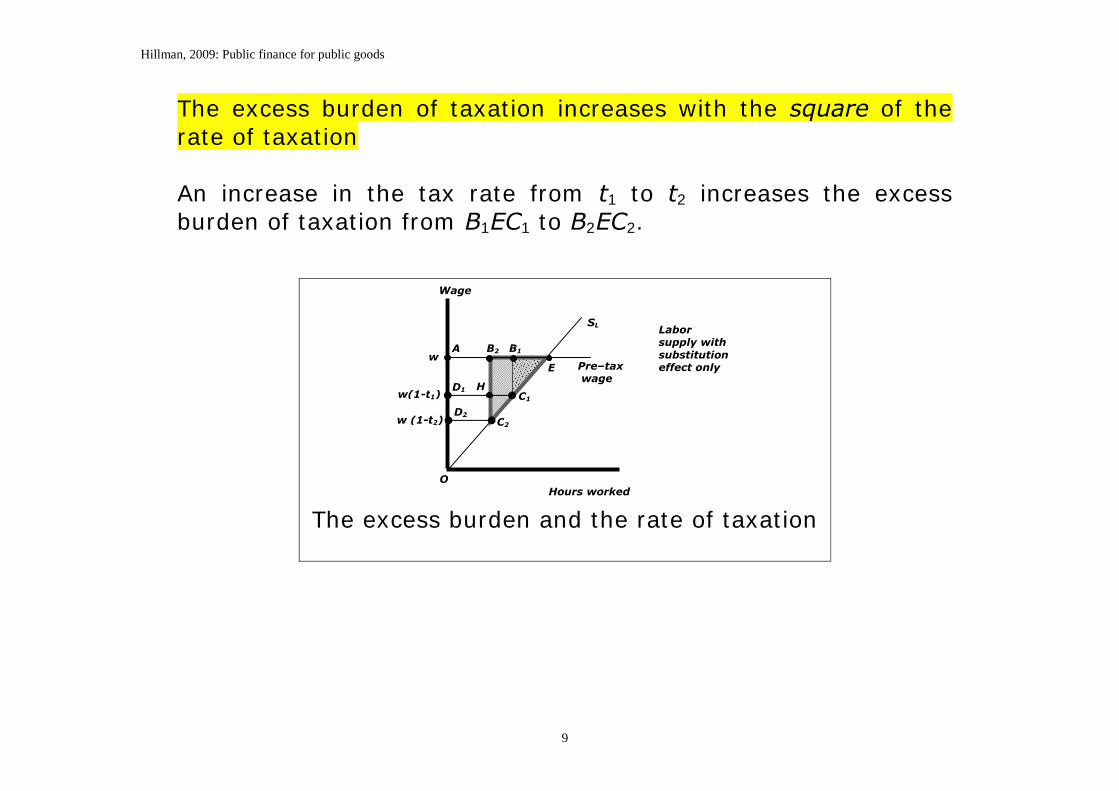

The excess burden of taxation increases with the square of the rate of taxation An increase in the tax rate from t1 to t2 increases the excess burden of taxation from B1EC1 to B2EC2.

The excess burden and the rate of taxation

Labor supply with substitution effect only

D1

D2

H

Hours worked

Wage

E

B1 B2

C1

C2

O

SL

w

w(1-t1)

w (1-t2)

Pre–tax wage

A

Hillman, 2009: Public finance for public goods

10

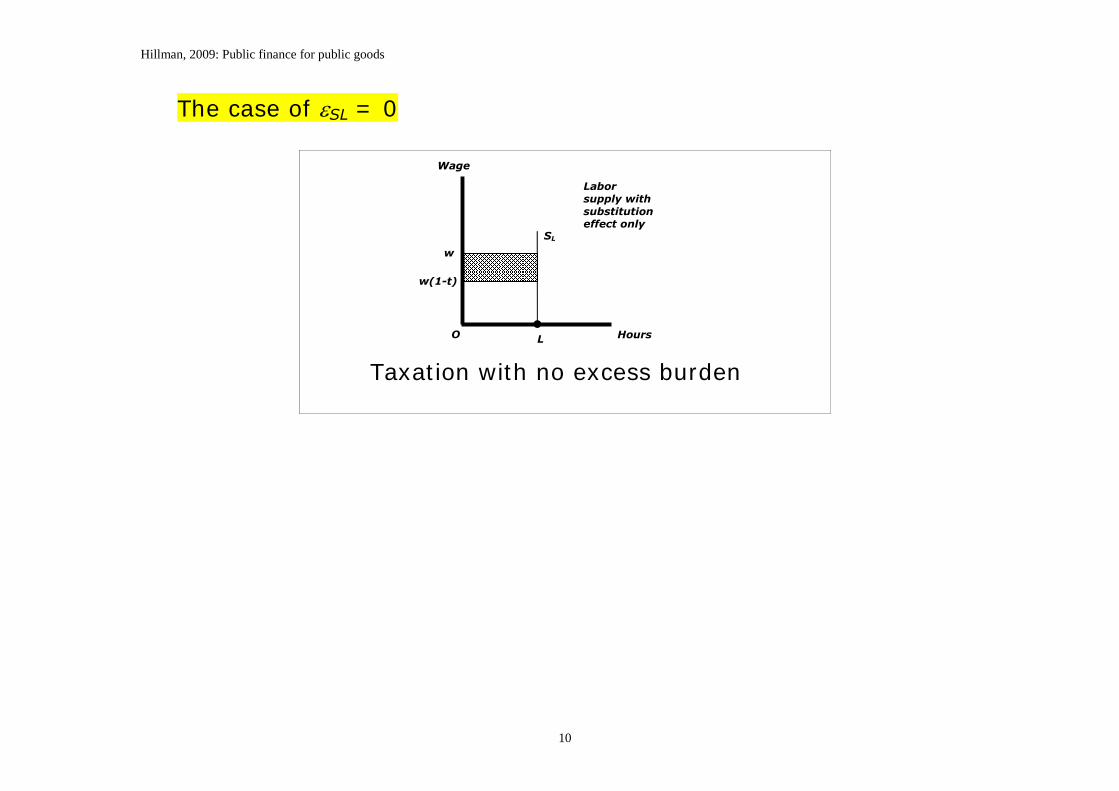

The case of SL = 0

Taxation with no excess burden

Labor supply with substitution effect only

Wage

Hours L O

SL w

w(1-t)

Hillman, 2009: Public finance for public goods

11

Intrusion into other markets

The excess burden of taxation arises because payment for public goods is not taking place in the market for public goods There would be no excess burden if public goods were voluntarily financed in markets for public goods: payment would then be taking place in the same market in which the goods are supplied.

Hillman, 2009: Public finance for public goods

12

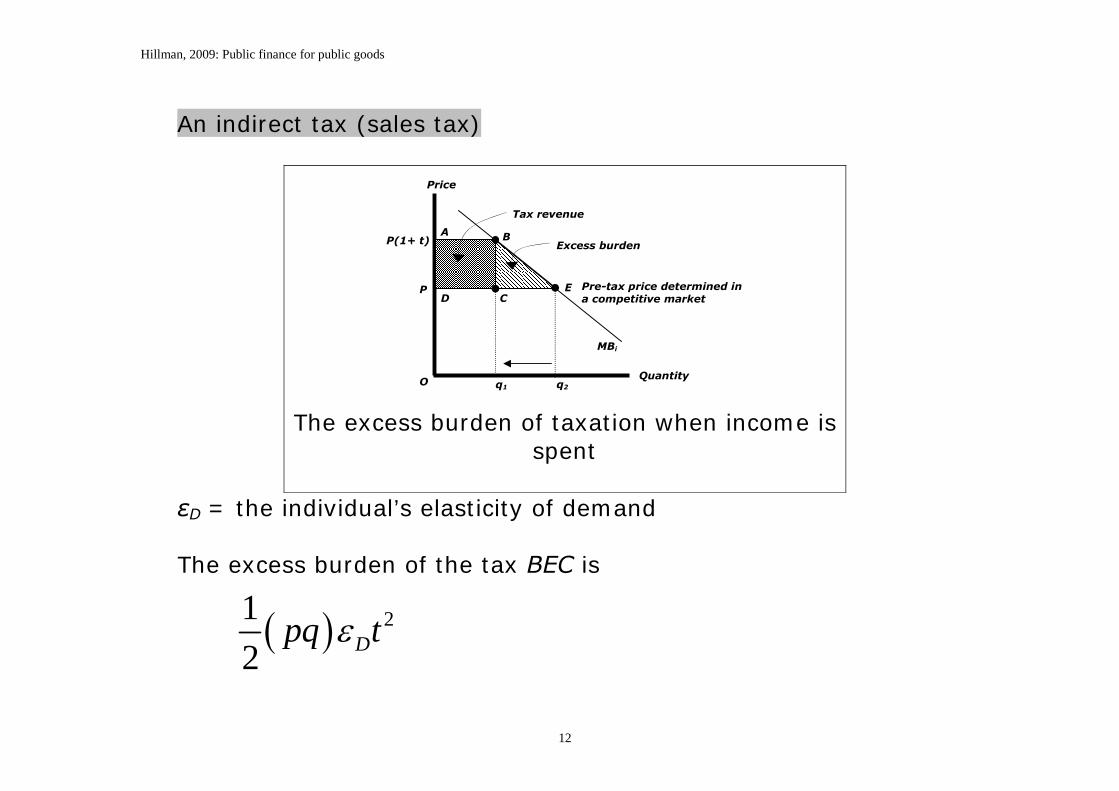

An indirect tax (sales tax)

The excess burden of taxation when income is spent

εD = the individual’s elasticity of demand The excess burden of the tax BEC is

212 Dpq t

D C P

A P(1+ t)

q1 q2

MBi

E

B

Quantity O

Price

Pre-tax price determined in a competitive market

Tax revenue

Excess burden

Hillman, 2009: Public finance for public goods

13

Substitution effects and the excess burden of taxation

In the labor market, the individual is a seller (or supplier of labor services) and the substitution response to a tax is expressed through the supply elasticity In the case of a sales tax, the individual is the buyer and the substitution response is expressed through the demand elasticity

Hillman, 2009: Public finance for public goods

14

A value-added tax A value-added tax is an indirect tax, like a sales tax The tax base

o For a sales tax, the value of goods sold (and therefore bought)

o For a value-added tax, value-added at different stages of production

The virtue of the value-added tax compared to a sales tax:

o The value-added tax does not depend on the structure of ownership of productive activities

o A value-added tax makes income tax evasion difficult International trade: the value-added tax can be levied on imports so that foreign intermediate goods have no advantage over domestic output and can be rebated for exports

Hillman, 2009: Public finance for public goods

15

Use of the value-added tax o A value-added tax is the common indirect tax outside of the

U.S. o In the U.S. individual state governments levy sales taxes: a

value-added tax would require a complex administrative tracking procedures

o Similar problems arise if governments in a union such as the European Union levy their own value-added taxes

Hillman, 2009: Public finance for public goods

16

An excise tax

o Excise taxes are higher than general rates for sales and value-added taxes

o The taxes are usually levied on goods for which demand is

perceived to be quite inelastic, such as alcohol and tobacco

o The low demand elasticities suggest goods that are habit-forming or addictive

o The low elasticities give rise to low substitution effects and so

there are low excess burdens of taxation

Hillman, 2009: Public finance for public goods

17

Other costs of taxation The excess burden is accompanied by other costs of taxation Compliance costs Administrative costs Emotional costs of taxation

Rent seeking

The administrative costs associated with taxation reflect rent-seeking behavior – or behavior intended to change or prevent change to distribution

We proceed by focusing on the excess burden of taxation How does the excess burden of taxation affect efficient publicly-financed public spending?

Hillman, 2009: Public finance for public goods

18

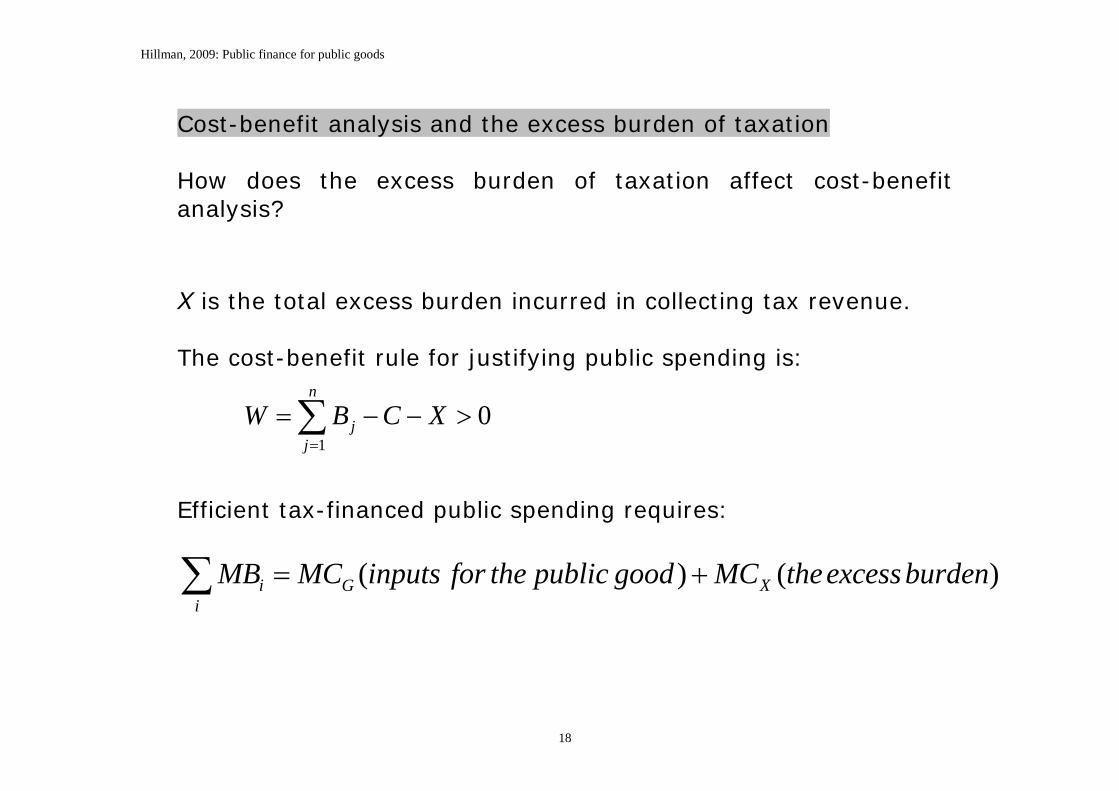

Cost-benefit analysis and the excess burden of taxation How does the excess burden of taxation affect cost-benefit analysis?

X is the total excess burden incurred in collecting tax revenue. The cost-benefit rule for justifying public spending is:

1

0n

jj

W B C X

Efficient tax-financed public spending requires:

( ) ( )i G Xi

MB MC inputs for the public good MC theexcessburden

Hillman, 2009: Public finance for public goods

19

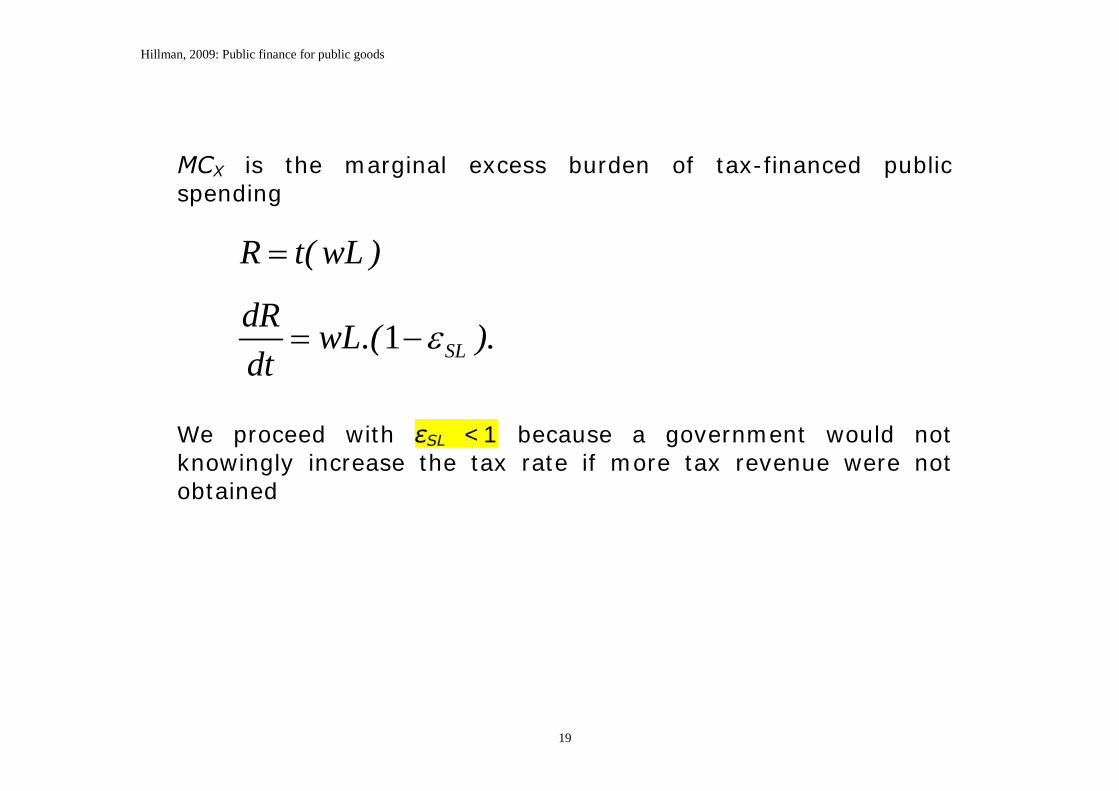

MCX is the marginal excess burden of tax-financed public spending

R t( wL )

1 SLdR wL.( ).dt

We proceed with εSL <1 because a government would not knowingly increase the tax rate if more tax revenue were not obtained

Hillman, 2009: Public finance for public goods

20

View εSL as constant

1 . .2 SLX R t

The average excess burden per dollar of tax revenue is

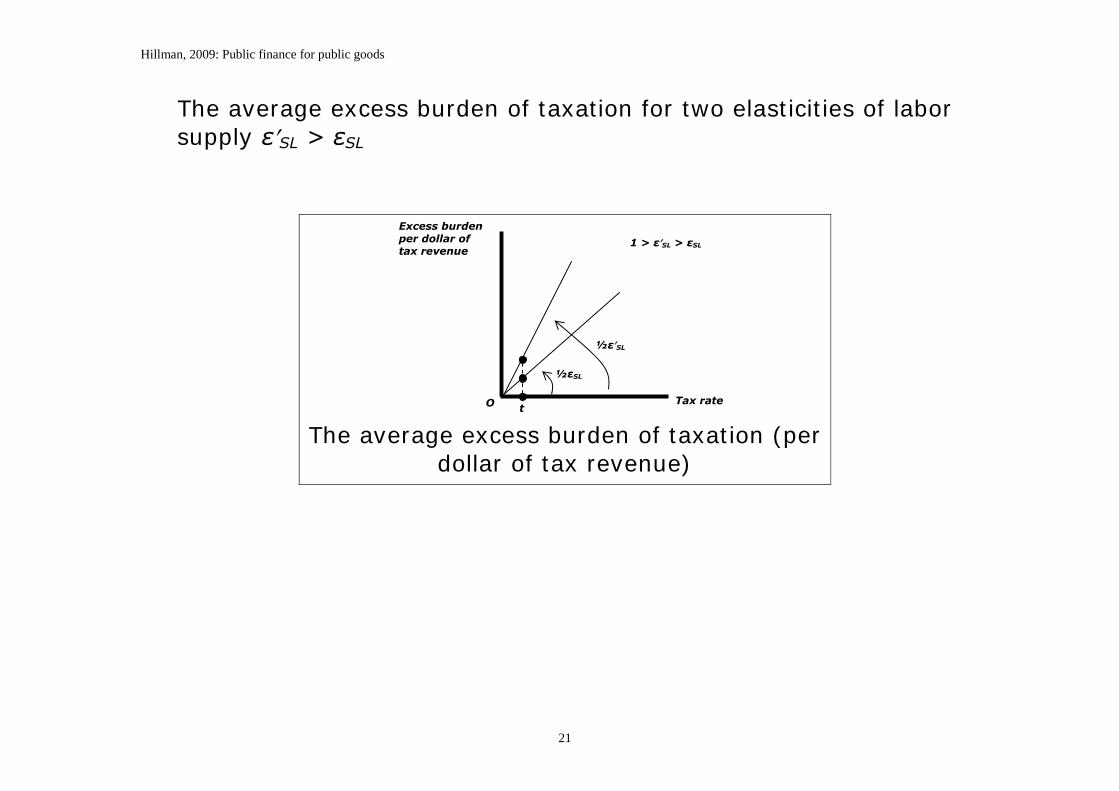

12 SL

X tR

For any rate of taxation t, the average excess burden increases with the labor-supply elasticity εSL

Hillman, 2009: Public finance for public goods

21

The average excess burden of taxation for two elasticities of labor supply εSL > εSL

The average excess burden of taxation (per dollar of tax revenue)

Tax rate

Excess burden per dollar of tax revenue

O

½εSL

½εSL

1 > εSL > εSL

t

Hillman, 2009: Public finance for public goods

22

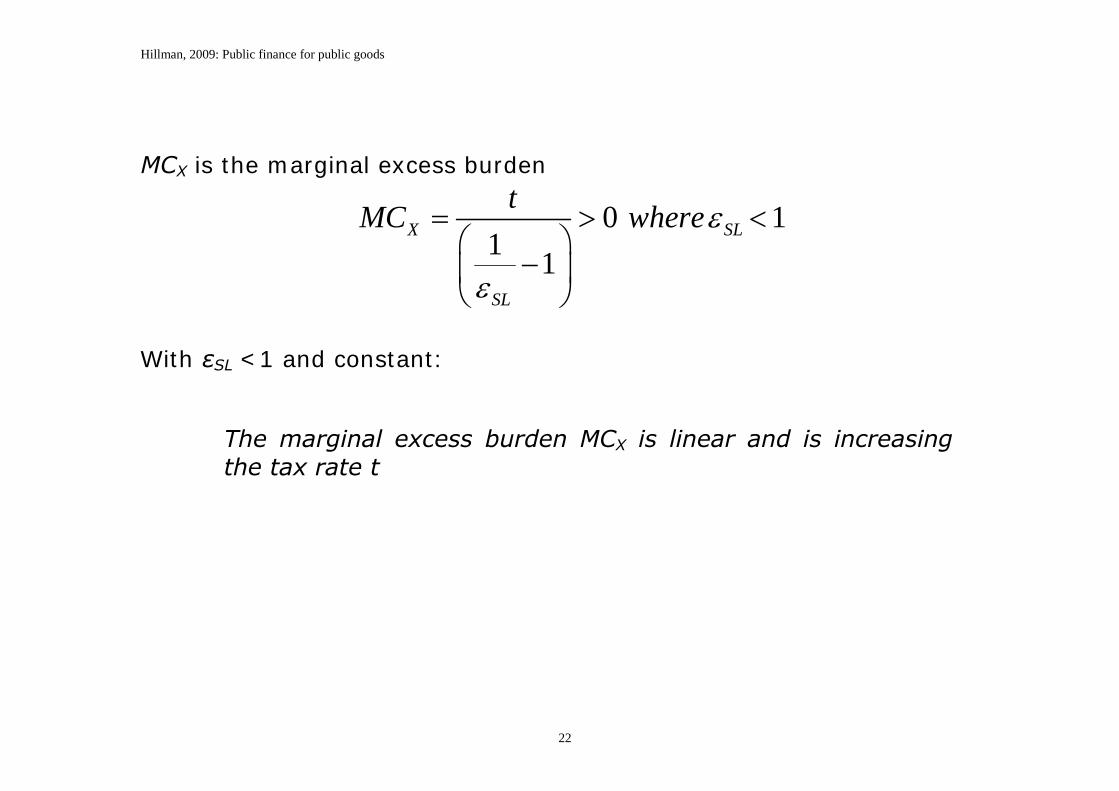

MCX is the marginal excess burden

0 11 1

X SL

SL

tMC where

With εSL <1 and constant:

The marginal excess burden MCX is linear and is increasing the tax rate t

Hillman, 2009: Public finance for public goods

23

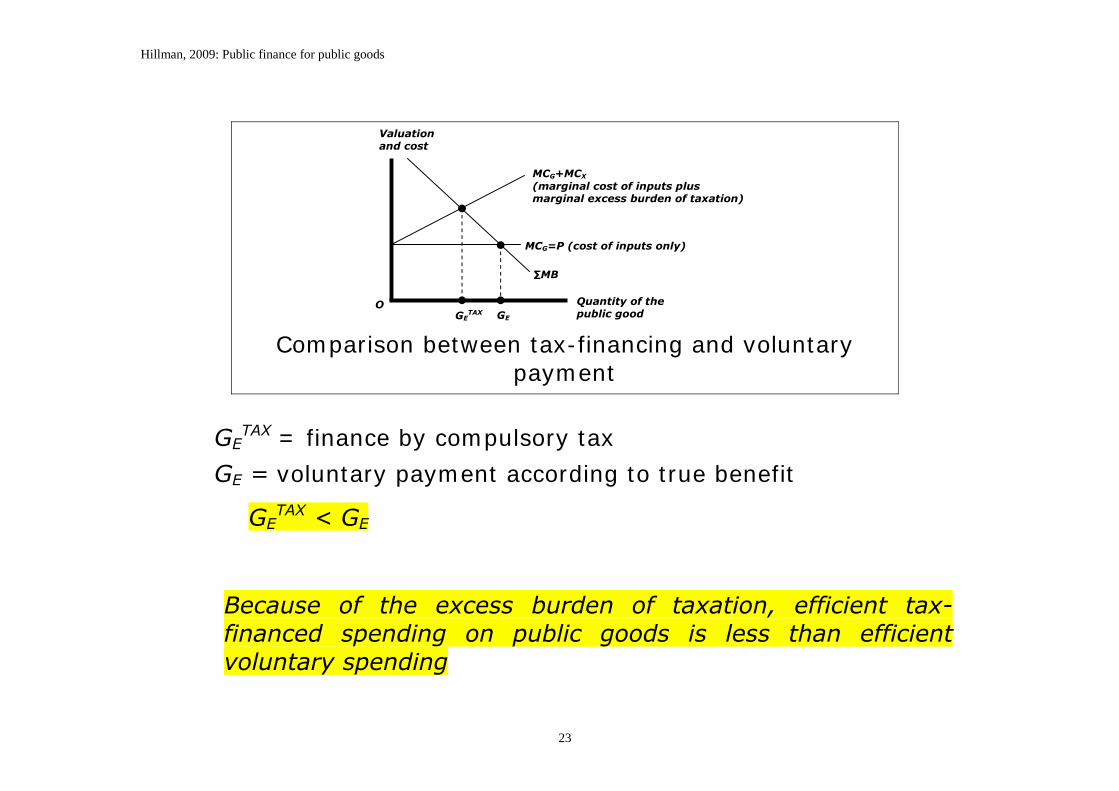

Comparison between tax-financing and voluntary payment

GE

TAX = finance by compulsory tax

GE = voluntary payment according to true benefit

GETAX < GE

Because of the excess burden of taxation, efficient tax-financed spending on public goods is less than efficient voluntary spending

GETAX GE

Quantity of the public good

MCG=P (cost of inputs only)

MCG+MCX (marginal cost of inputs plus marginal excess burden of taxation)

∑MB

O

Valuation and cost

Hillman, 2009: Public finance for public goods

24

Accountability and transparency of public spending

Accountability and transparency require the government budget to include the excess burden of the taxes that finance public spending

Hillman, 2009: Public finance for public goods

25

Are taxes available that have no excess burden? A tax with no substitution response is called a lump-sum tax Taxation of goods with no substitution effects

A life-preserving medication has completely inelastic demand A tax on essential goods or services is politically unwise

Addiction and taxes Addiction ensures the tax base The excess burdens of the taxes are low

Hillman, 2009: Public finance for public goods

26

Tiebout locational choice and taxes

The Tiebout locational choice mechanism is an application of the benefit principle of taxation

There would be no excess burden if the taxes paid to governments through voluntary locational choice were analogues of voluntarily paid market prices

Local public goods are in general not financed according to the benefit principle but through property, income, and sales taxes that have excess burdens

Often the principal tax for financing local public goods is a property tax on improved land: this is a tax on adding to the value of a property through further investment

The substitution response to the tax is that investment is undertaken elsewhere in other lower-tax jurisdictions

Substitution responses also occur through allowances in the tax code for depreciation

Hillman, 2009: Public finance for public goods

27

Taxes on unimproved value of land and Henry George Taxes on the unimproved value of land have no excess burden Land is trapped within a tax jurisdiction with no substitution

response that allows “escape” from the tax

Henry George (1839 - 1897) proposed that there should be only a single tax levied on the tax base of the unimproved value of land

George did not make his case on efficiency grounds due to the absence of an excess burden

His case was based on social justice He observed that people who owned land benefited when economic growth increased the value of land, yet landowners had done nothing productive to merit the increase in their wealth

Hillman, 2009: Public finance for public goods

28

A poll tax A poll tax is a payment for the right to vote If all citizens choose to exercise their right to vote, poll taxes are lump-sum taxes Poll taxes impose a cost of voting By determining who votes, a poll tax can affect political decisions about public finance and public policy

Hillman, 2009: Public finance for public goods

29

A personal head tax A personal head-tax is a lump-sum tax with no substitution effect

The head-tax can depend on nothing other an individual’s existence and identity

The head-tax cannot depend on any attribute or behavior that a person can change – income, purchases, wealth, number of dependents, or marital status, personal ability (which people can hide)

There is scope for unfairness because different people can arbitrarily be assigned different taxes

The only escape from a head tax is to leave the jurisdiction of the government levying the tax

Head taxes would not be politically popular

In civil societies, taxes are levied on the market-determined value of a person’s income or the market-determined value of property and not according to people’s inalterable identities

Hillman, 2009: Public finance for public goods

30

The unavailability of taxes with no excess burden Other than taxes on unimproved value of property, taxes without an excess burden are not feasible, or not ethically or politically desirable

Taxes without an excess burden are generally not used

Hillman, 2009: Public finance for public goods

31

Measurement of the excess burden of taxation

Invisibility of the excess burden of taxation makes measurement difficult: the excess burden cannot simply be observed and directly measured Surveys are unlikely to yield reliable information Estimation from aggregate market data Two types of problems (1) There are taxes with no tax revenue

The excess burden (which is invisible in the first place) may be invisible in a market that no longer exists.

(2) Taxes in one market result in excess burdens in other markets.

The excess burden of a tax in the market where the tax is levied understates the excess burden of taxation because of responses in other markets.

Hillman, 2009: Public finance for public goods

32

A tax with an excess burden

and no revenue

The change in the

excess burden in market 2 when the tax changes in market

1

E2

O

C1

B1

E1

Excess burden

Quantity of good 2

Price of good 2

Supply good 2

Demand for good 2 BEFORE the tax on good 1

Demand for good 2 AFTER the tax on good 1

B2

C2

Hours worked

O

Wage

B E

SL

w

Excess burden

Pre–tax wage

L1

Hillman, 2009: Public finance for public goods

33

Measuring the excess burden in labor markets The value of the labor-supply elasticity depends on Possibilities for marginal adjustments to labor supply The decision whether to work for a living (when hours worked

are not flexible, the choice is between having and not having a job)

Payments provided by governments to people who do not work

Obligations outside the labor market

Hillman, 2009: Public finance for public goods

34

Diversity in empirical estimates of the excess burden Example: In the United States, estimates of the marginal excess burden of taxation have ranged from 7 cents to 39 cents. Tracing effects through other markets suggests higher values. Why is there diversity in estimates? Difficulties of accurately measuring something that is invisible tracing through effects in the different markets in an economy taking into account both adjustments in hours worked and the

decision whether or not to have a job accounting for the effect of income received from the

government when not working Scope for discretion and assumptions

Flexibility in assumptions can result in estimates that are influenced by predisposition regarding size of government

Hillman, 2009: Public finance for public goods

35

Evidence on the excess burden from social experiments Under communism, people were asked (or compelled to) behave as if their personal elasticity of labor supply were zero

The principle was

People should contribute according to their ability and not according to personal reward.

The natural experiment persisted over decades and over generations The social experiment resulted in significant excess burdens “We pretend to work and they pretend to pay us”

Hillman, 2009: Public finance for public goods

36

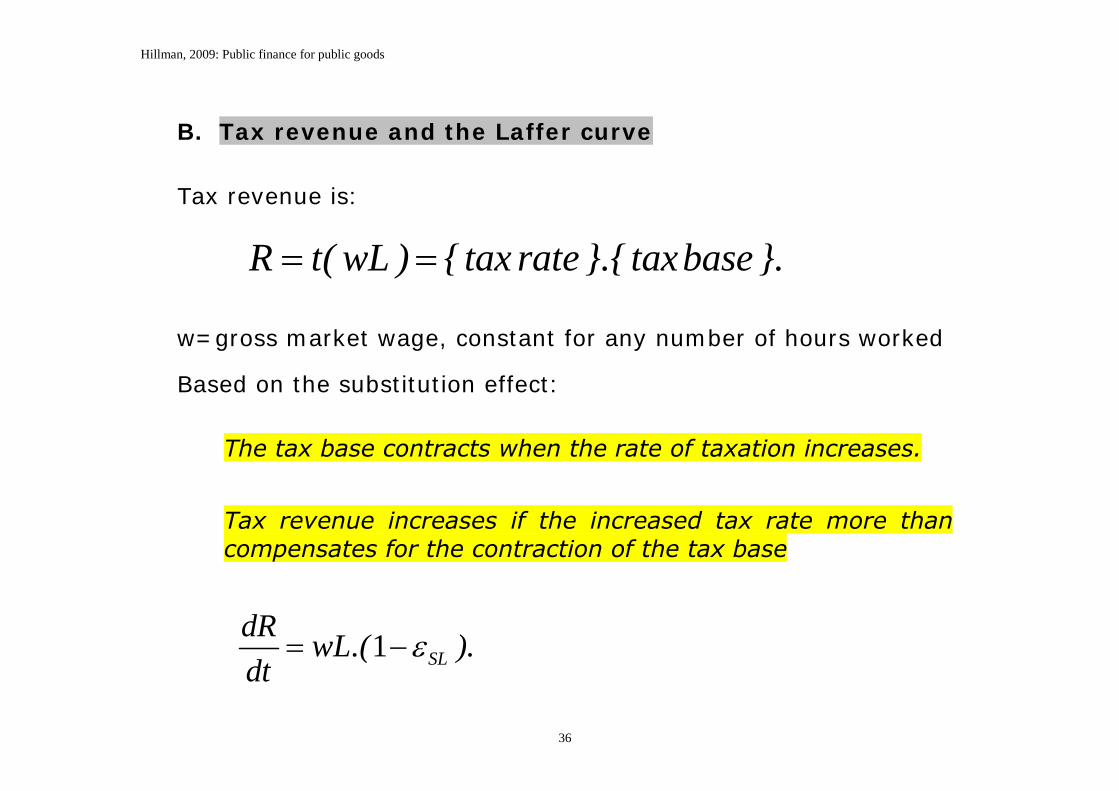

B. Tax revenue and the Laffer curve

Tax revenue is:

R t( wL ) { tax rate }.{ taxbase }.

w=gross market wage, constant for any number of hours worked

Based on the substitution effect:

The tax base contracts when the rate of taxation increases.

Tax revenue increases if the increased tax rate more than compensates for the contraction of the tax base

1 SLdR wL.( ).dt

Hillman, 2009: Public finance for public goods

37

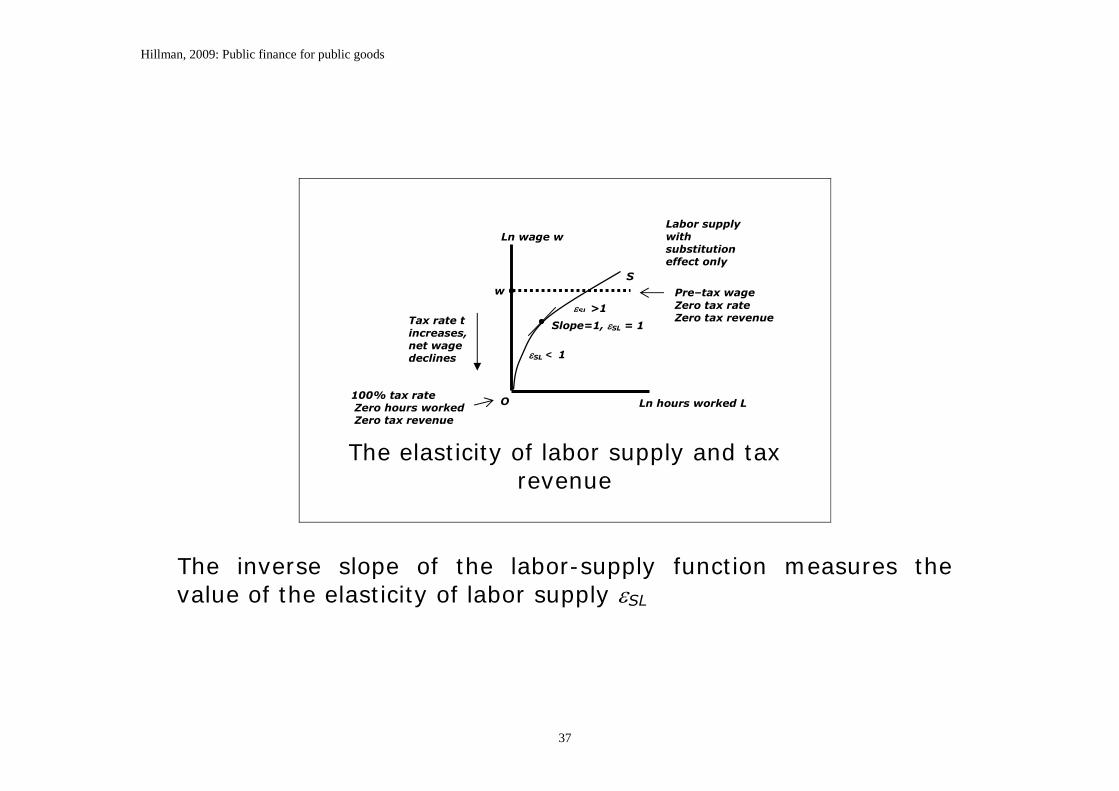

The elasticity of labor supply and tax revenue

The inverse slope of the labor-supply function measures the value of the elasticity of labor supply SL

O

Tax rate t increases, net wage declines SL < 1

Ln hours worked L

Ln wage w

SL >1

S w

Slope=1, SL = 1

Labor supply with substitution effect only

100% tax rate Zero hours worked Zero tax revenue

Pre–tax wage Zero tax rate Zero tax revenue

Hillman, 2009: Public finance for public goods

38

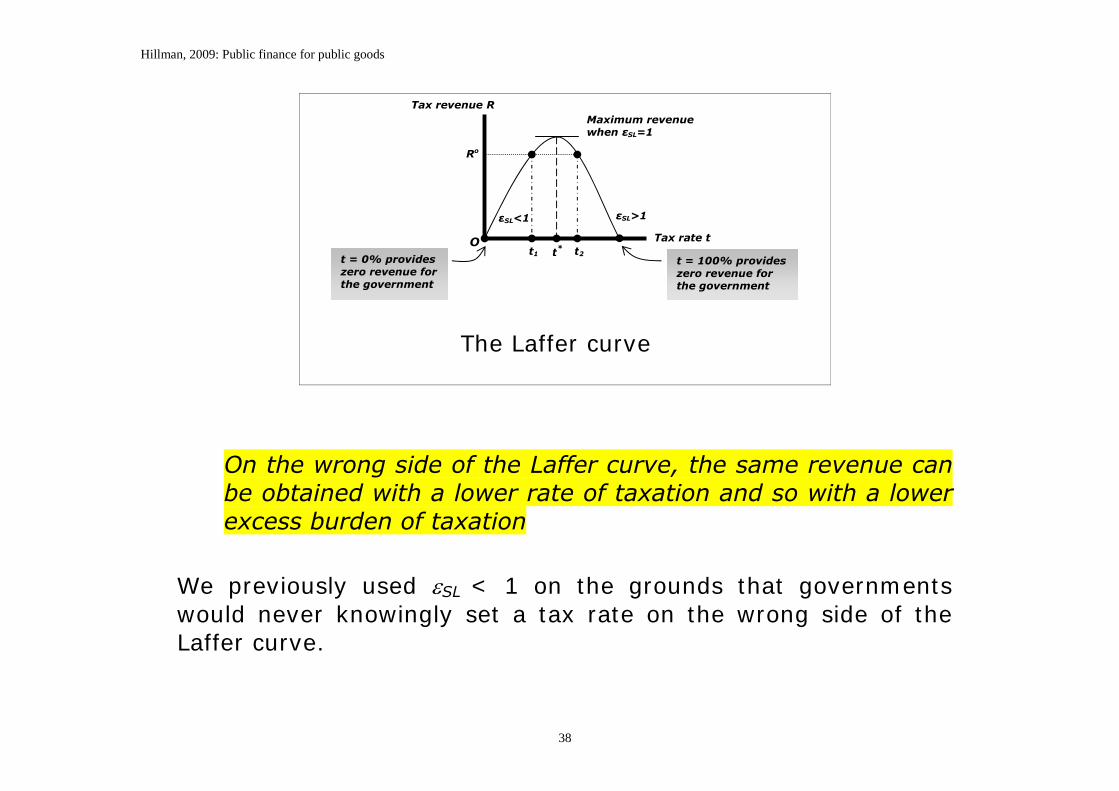

The Laffer curve

On the wrong side of the Laffer curve, the same revenue can be obtained with a lower rate of taxation and so with a lower excess burden of taxation

We previously used SL < 1 on the grounds that governments would never knowingly set a tax rate on the wrong side of the Laffer curve.

Ro

Maximum revenue when εSL=1

t = 0% provides zero revenue for the government

εSL>1 εSL<1

t*

Tax revenue R

Tax rate t t2

t = 100% provides zero revenue for the government

O t1

Hillman, 2009: Public finance for public goods

39

Individual behavior and the aggregate Laffer curve

The aggregate Laffer curve reveals the tax rate that maximizes total tax revenue Individuals have their own personal labor-supply functions and labor-supply elasticities Values of the tax rate that drive individuals onto the wrong side of their personal Laffer curve differ for different people Tax rates that are sufficiently high drive some people onto the wrong side of their personal Laffer curves.

Hillman, 2009: Public finance for public goods

40

Investment and the Laffer curve There is a Laffer curve for taxation of capital

Taxes on returns from investment result in substitution effects: investment declines or capital moves elsewhere to other tax jurisdictions When capital leaves a tax jurisdiction, the marginal product of labor declines and the tax base for labor income contracts There is negative reinforcement on tax revenue: a tax on one factor of production reduces the tax base of the other factor

Hillman, 2009: Public finance for public goods

41

Tax evasion the Laffer curve

o Another reason for the Laffer curve is tax evasion where tax rates become too high

The political sensitivity of the Laffer curve

o Location on the Laffer curve is revealed empirically by changing the rate of taxation and observing the revenue response

o The Laffer curve is politically sensitive for people who prefer

high government spending because of the possibility that decreasing tax rates can increase government revenue

o Political sensitivity is compounded by the distinction between

the short and long-run Laffer curve

Hillman, 2009: Public finance for public goods

42

A leviathan government and the Laffer curve

o A leviathan government seeks the maximum point of the Laffer curve

o Information about the Laffer curve is not always precise

o A leviathan government is prone to straying onto the wrong

side of the Laffer curve

Hillman, 2009: Public finance for public goods

43

C. Who pays a tax?

Normative principles of just taxation are:

o Horizontal equity requires that people who are identical in income and other attributes face the same tax obligations.

o Vertical equity requires that people who are not identical in income and other attributes face tax liabilities that are just in accounting for the sources of individual differences.

Principles according to which taxes can be levied:

o The benefit principle of taxation: people who benefit from public spending should pay the taxes that finance the spending

o Ability-to-pay principle of taxation: people who can most afford to pay should pay taxes, without regard for personal benefit obtained from the taxes paid.

Hillman, 2009: Public finance for public goods

44

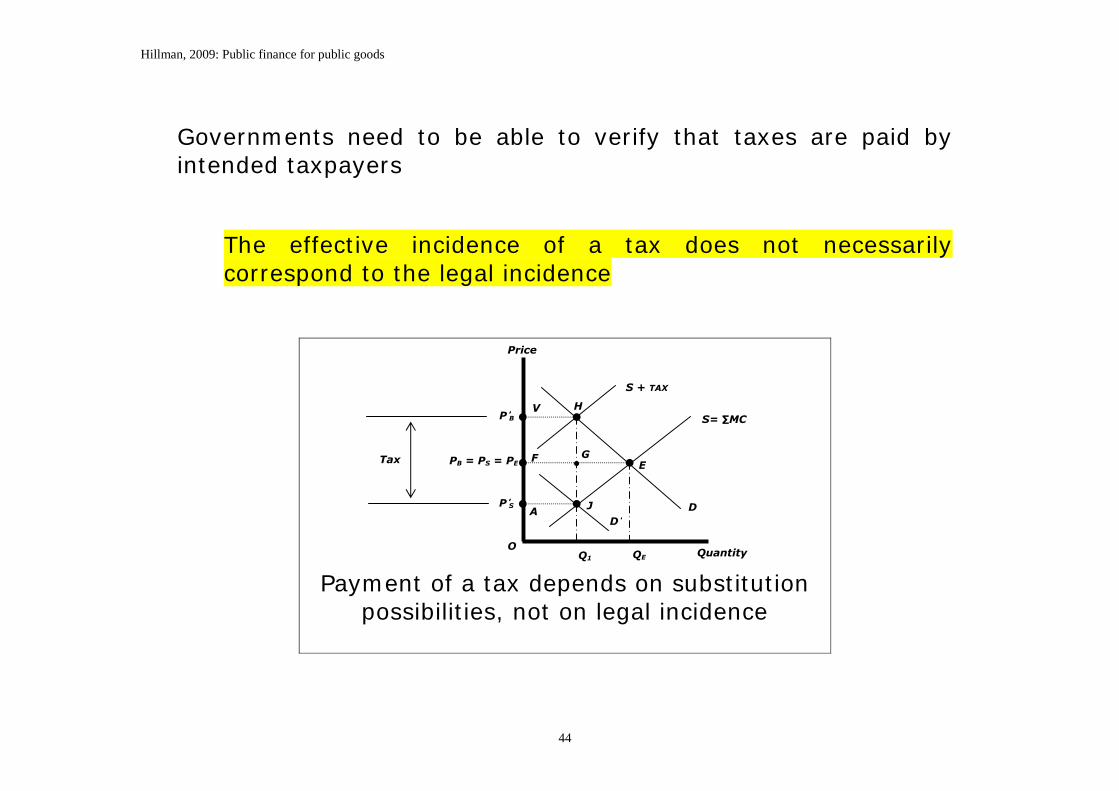

Governments need to be able to verify that taxes are paid by intended taxpayers

The effective incidence of a tax does not necessarily correspond to the legal incidence

Payment of a tax depends on substitution possibilities, not on legal incidence

P’S

PB = PS = PE

P’B

F

A J D’

O Q1 QE

V

G

H

E

S + TAX

S= ∑MC

Quantity

D

Price

Tax

Hillman, 2009: Public finance for public goods

45

The sharing of the excess burden Demand and supply elasticities determine

Effective tax incidence (who pay a tax) The sharing of the excess burden

Hillman, 2009: Public finance for public goods

46

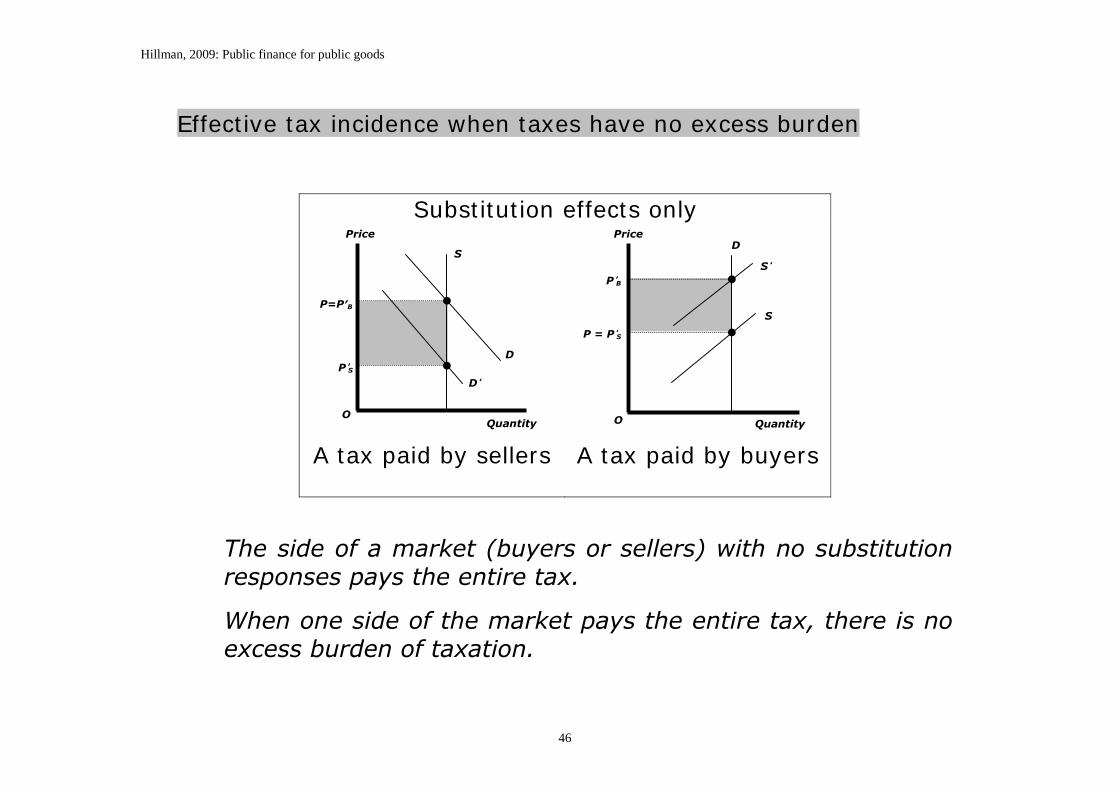

Effective tax incidence when taxes have no excess burden

Substitution effects only

A tax paid by sellers

A tax paid by buyers

The side of a market (buyers or sellers) with no substitution responses pays the entire tax.

When one side of the market pays the entire tax, there is no excess burden of taxation.

P’S

P=P′B

D’

O

D

S

Quantity

Price D

O Quantity

S’

S

P = P’S

P’B

Price

Hillman, 2009: Public finance for public goods

47

Political pronouncements and taxation

Substitution effects determine who pays a tax and the sharing of the excess burden of taxation

Public policy pronouncements that imply effective tax incidence is determined by legal tax incidence indicate

Misinformation (the political decision maker does not know economic principles), or

Disinformation (the political decision maker hopes that others do not know economic principles)

L1 O

Demand for labor

LE

wE wB

wS

Tax

Hours worked

Supply of labor

Wage

Hillman, 2009: Public finance for public goods

48

Fiscal illusion and tax incidence

Fiscal illusion occurs when taxpayers are not aware they are paying taxes

The excess burden of taxation and fiscal illusion

o When there is fiscal illusion, people do not know that they are paying taxes but the excess burden of taxation is present

o The substitution response is a response to change in a relative price and not a response to the reason for the change

Political decisions o Political benefit from effective tax incidence requires

asymmetric information about who pays a tax o Because of fiscal illusion, political decision makers may prefer

indirect taxes

Fiscal illusion arises with bond financing (to be considered presently)

Hillman, 2009: Public finance for public goods

49

Economy-wide effects on who pays taxes Economy-wide (or general-equilibrium effects) of taxes affect how the excess burden is shared and who pays a tax Examples

o Factor prices and incomes o A sales tax on toothbrushes and incomes of dentists

To know who in the final analysis pays a tax and who bears the excess burden of taxation, governments need to be able to trace the effect of the tax throughout all markets.

Hillman, 2009: Public finance for public goods

50

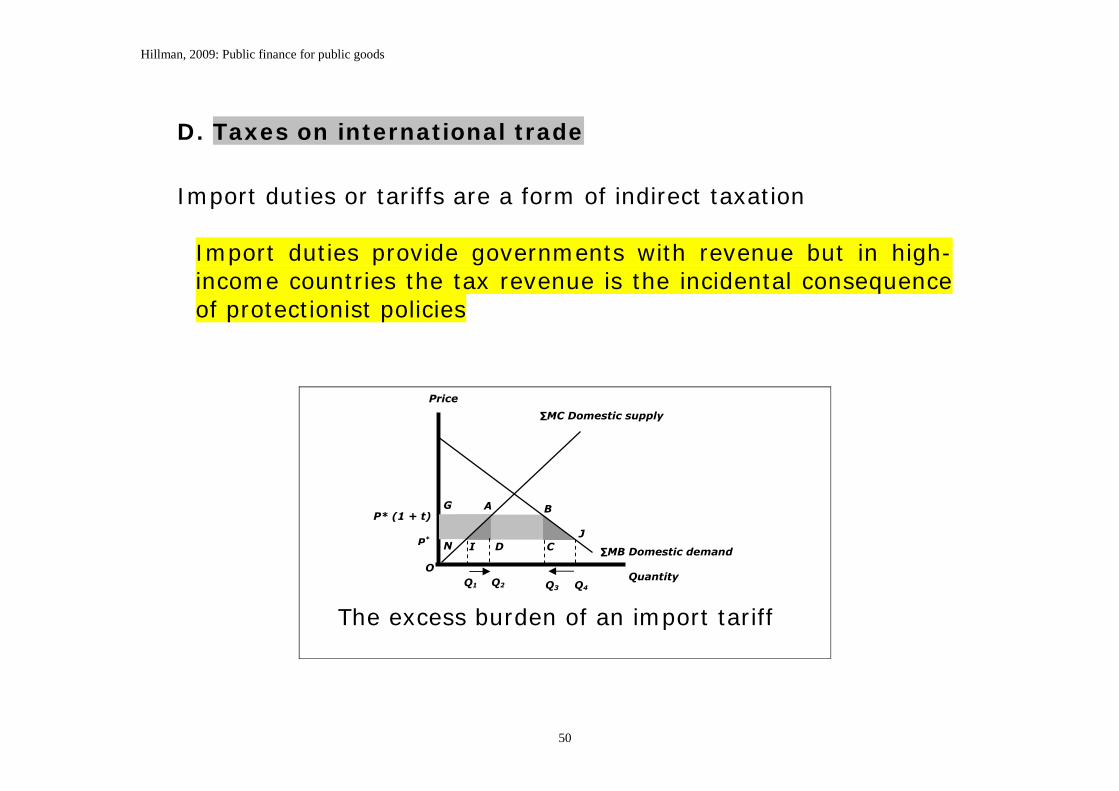

D. Taxes on international trade

Import duties or tariffs are a form of indirect taxation

Import duties provide governments with revenue but in high-income countries the tax revenue is the incidental consequence of protectionist policies

The excess burden of an import tariff

J I

G A

∑MC Domestic supply

P* (1 + t)

N D C

B

∑MB Domestic demand

O

Price

Quantity

P*

Q1 Q2 Q4 Q3

Hillman, 2009: Public finance for public goods

51

A sales tax and a tariff

A sales tax provides the same tax revenue as an import tariff with a lower rate of taxation and a lower excess burden of taxation.

Costs of collection of revenue Costs of collecting revenue from taxes on imports are low compared to a sales tax

Hillman, 2009: Public finance for public goods

52

Where tax administration allows domestic taxes to be collected, the purpose of a tax on imports cannot be to provide tax revenue – since a sales tax is a better revenue instrument.

The purpose of a tax on imports is not revenue but to provide protectionist rents to domestic industry interests.

Hillman, 2009: Public finance for public goods

53

Why use an import tariff? If the objective is government revenue, a sales tax is preferable to an import tariff If the objective is protection, a subsidy to domestic producers provides the same rents to domestic producers as an import tax but with a smaller efficiency loss.

Why would governments choose to use import tariffs as means of providing protectionist rents to a domestic industry?

o Visibility in the government budget opens production

subsidies to scrutiny and debate. o An import tax provides protectionist rents that do not appear

in the government budget o Buyers provide the rents directly to the domestic industry,

through the higher domestic price directly paid to domestic producers

Hillman, 2009: Public finance for public goods

54

Import quotas The choice between tariffs and import quotas For a competitive domestic industry, the two policy instruments are equivalent – except for who obtains revenue

The quota creates rents for private individuals at the expense of government revenue.

The private profits from being assigned quota rents set in place a rent-seeking contest

Why would a government forego tariff revenue to create private rents through an import quota?

Hillman, 2009: Public finance for public goods

55

4.2 TAX EVASION AND THE SHADOW ECONOMY

A. Tax evasion as free riding

Tax evasion is illegal free riding in contributions to public goods.

o Tax evasion and tax incidence

o Public policy The expected penalty for being found to have evaded taxes is:

{probability of detection}.{penalty if detected}.

o Why do people evade taxes?

o Tax evasion and social norms

o Risk-averse behavior

Hillman, 2009: Public finance for public goods

56

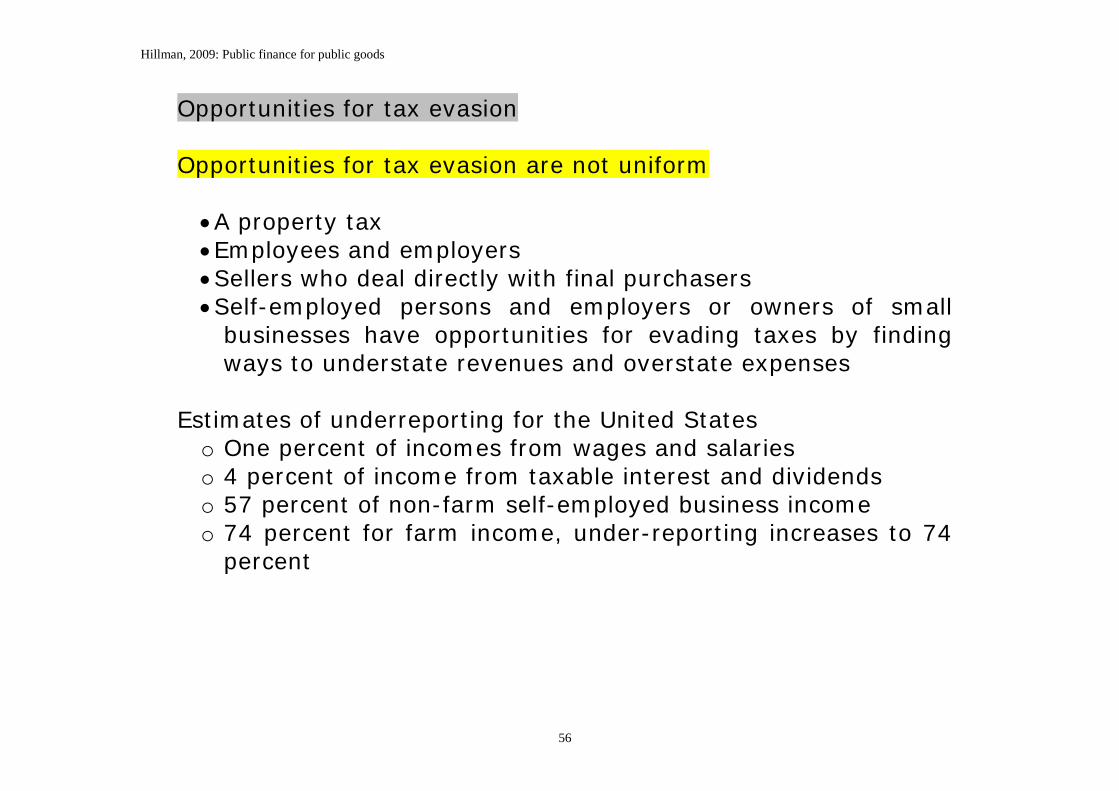

Opportunities for tax evasion Opportunities for tax evasion are not uniform A property tax Employees and employers Sellers who deal directly with final purchasers Self-employed persons and employers or owners of small

businesses have opportunities for evading taxes by finding ways to understate revenues and overstate expenses

Estimates of underreporting for the United States

o One percent of incomes from wages and salaries o 4 percent of income from taxable interest and dividends o 57 percent of non-farm self-employed business income o 74 percent for farm income, under-reporting increases to 74

percent

Hillman, 2009: Public finance for public goods

57

Tax evasion and exchanges of services

Indirect taxes (sales taxes, excise taxes, and import tariffs) - complicity of corrupt cooperating customs inspectors.

Multinational firms and transfer prices

Illegal immigrants

Tax avoidance and tax evasion

There is injustice when some people can engage in tax avoidance and others only in tax evasion

Tax evasion does not incur the expenses of tax avoidance but is illegal and subject to penalties and stigma if detected.

Hillman, 2009: Public finance for public goods

58

Unequal opportunities to evade taxes are a source of social injustice because of arbitrary sharing of the tax burden and of the excess burden of taxation

Hillman, 2009: Public finance for public goods

59

B. The behavior of the tax authorities

How do the tax authorities behave toward taxpayers?

Presumptive taxation

Corruption in low-income countries

Hillman, 2009: Public finance for public goods

60

C. The shadow economy

In the shadow economy, incomes are entirely outside of the domain of taxation Tax evasion takes place in the shadow economy but also in the official economy.

Welfare fraud o People employed in the shadow economy declare themselves

to be officially unemployed and receive unemployment benefits or welfare payments

o They fraudulently take money from the government (i.e., from taxpayers) while at the same time evading taxes on their incomes in the shadow economy.

Hillman, 2009: Public finance for public goods

61

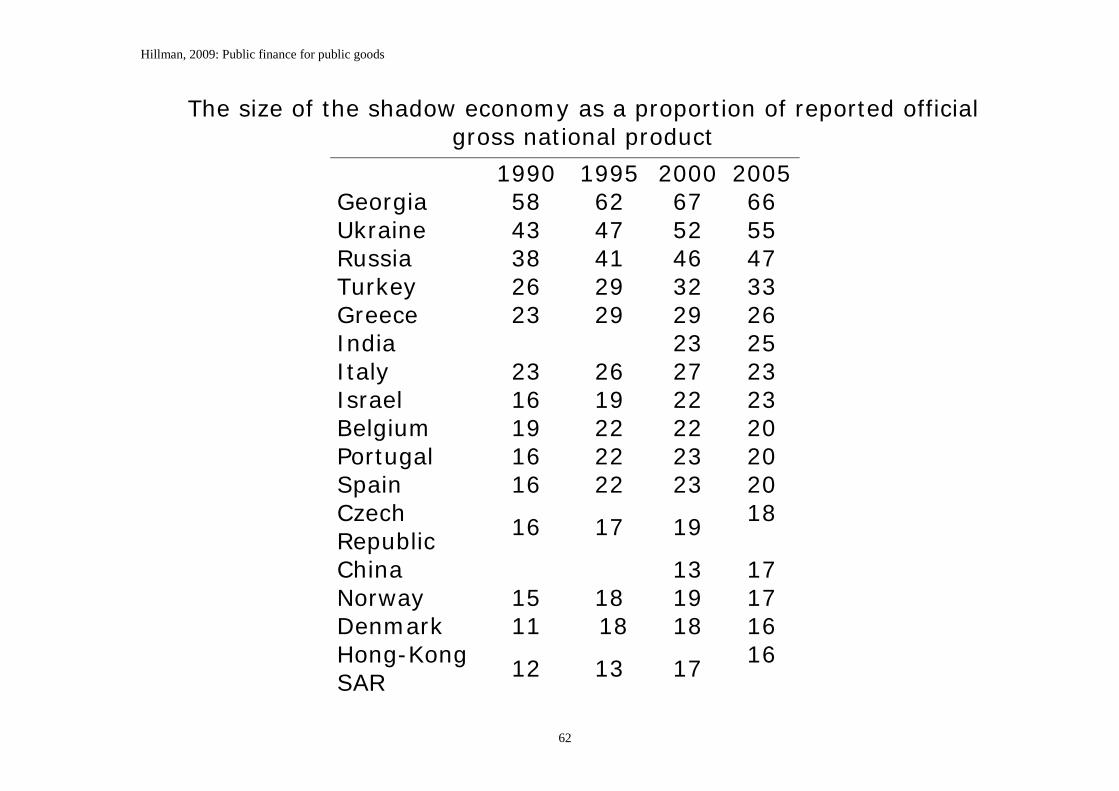

The size of the shadow economy The size of the shadow economy cannot be directly observed and therefore has to be inferred or estimated Researchers look for observed variables that are correlated with the size of the shadow economy – or that are correlated with the true size of national income including the shadow economy Money supply Extent of cash payments Use of electricity Differences between total income and total spending Differences between population size and people employed

indicated by official statistics. More complex approaches: A variety of indicators and causes are used to estimate the size of the shadow economy as an unknown variable

Hillman, 2009: Public finance for public goods

62

The size of the shadow economy as a proportion of reported official gross national product

Source: Schneider (2005, 2007). Numbers are rounded up.

Corruption and the shadow economy

Hillman, 2009: Public finance for public goods

64

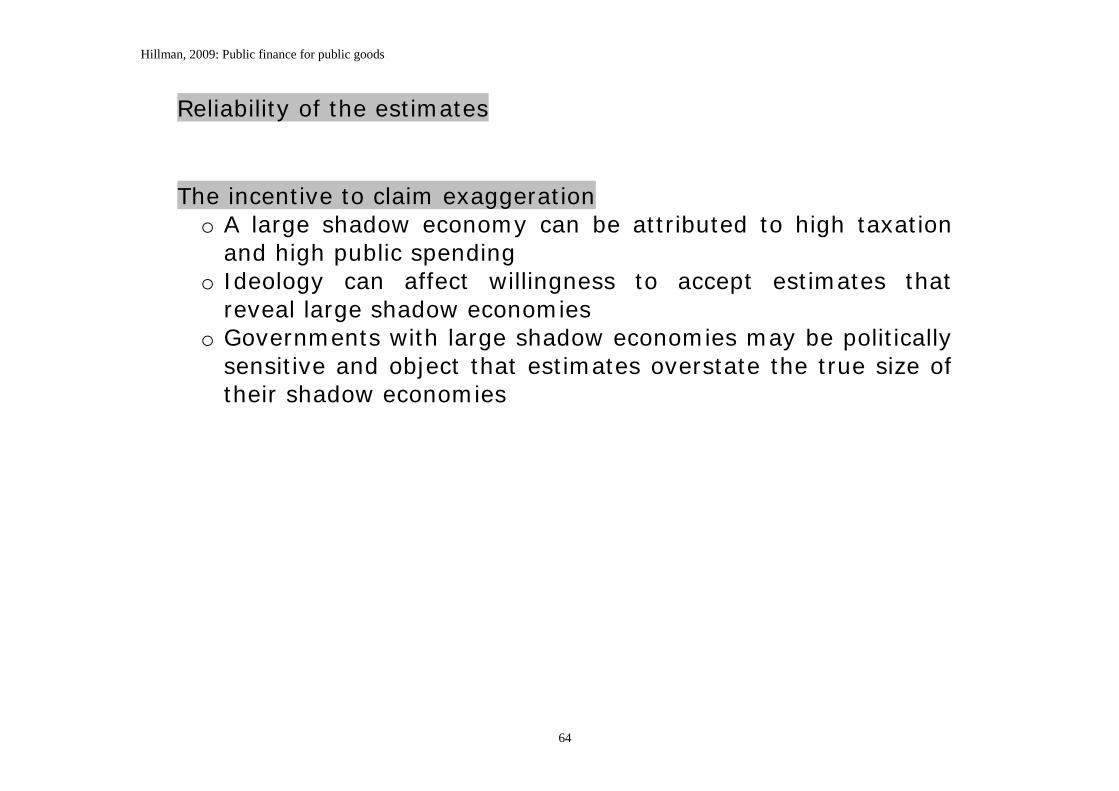

Reliability of the estimates

The incentive to claim exaggeration o A large shadow economy can be attributed to high taxation

and high public spending o Ideology can affect willingness to accept estimates that

reveal large shadow economies o Governments with large shadow economies may be politically

sensitive and object that estimates overstate the true size of their shadow economies

Hillman, 2009: Public finance for public goods

65

D. Inefficiency and illegality in a shadow economy

Injustice There is injustice when unequal opportunities for tax evasion result in discriminatory tax burdens Honesty is penalized: Activity in the shadow economy provides a cost advantage for producers who do not pay taxes

Inefficiency in the shadow economy The excess burden of taxation is reduced However, tax evasion is a source of inefficiency

o Limited scope for personal success o No recourse to courts for enforcement of contracts and to

settle disputes o The shadow economy invites corruption

Hillman, 2009: Public finance for public goods

66

Conspicuous consumption and visible spending

Money laundering

The Laffer curve and tax evasion

Hillman, 2009: Public finance for public goods

67

4.3 GOVERNMENT BORROWING

Bond financing of public spending is deferred taxation, including a deferred excess burden of taxation

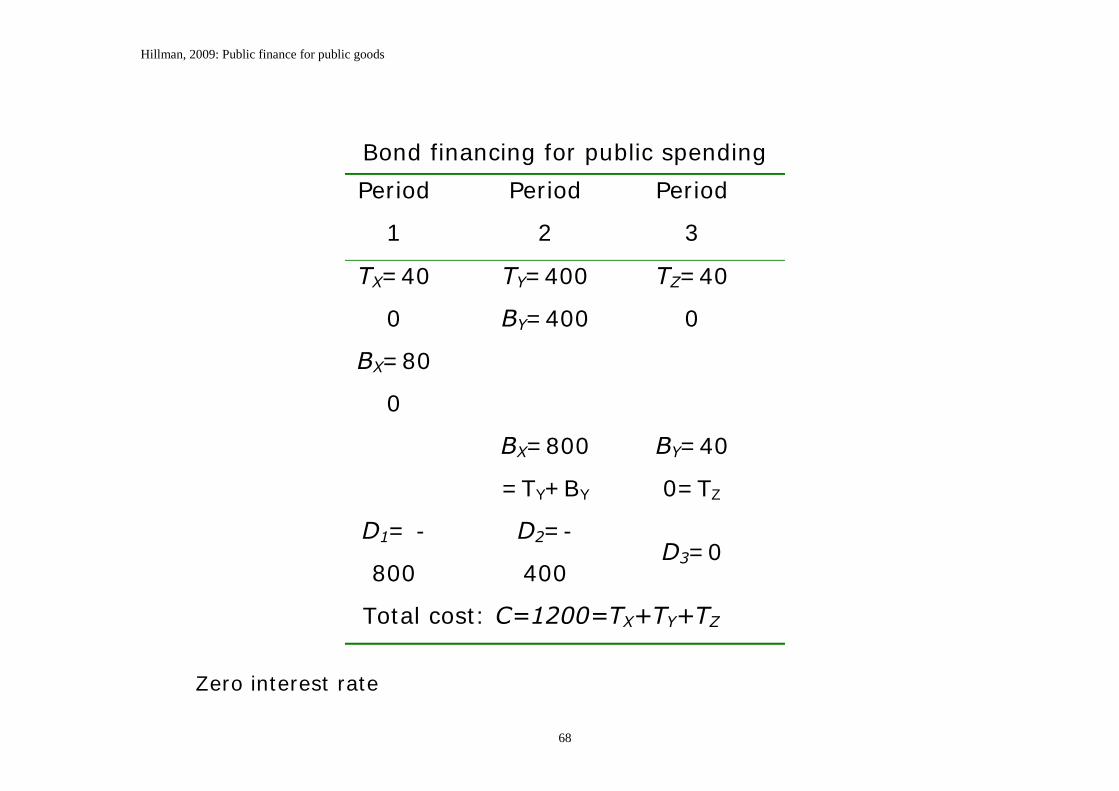

A. Bond financing and the benefit principle of taxation

The normative rule based on the benefit principle of taxation is:

Current taxes should be used to finance current benefits from public spending

Bond financing should be used to match future benefits with future tax payments.

Hillman, 2009: Public finance for public goods

68

Bond financing for public spending

Period

1

Period

2

Period

3

TX=40

0

BX=80

0

TY=400

BY=400

TZ=40

0

BX=800

=TY+BY

BY=40

0=TZ

D1= -

800

D2=-

400 D3=0

Total cost: C=1200=TX+TY+TZ

Zero interest rate

Hillman, 2009: Public finance for public goods

69

Default on government bonds

o Generation Z could gain by reneging and refusing to transfer its share of the cost of the project to generation Y.

o The public project would continue to provide benefits o The project was completed in period 1 and the only change if

a government reneges on honoring bond redemption obligations is in intergenerational income distribution.

Sale of government bonds to foreigners

o Bonds can be sold to foreigners o The taxes to repay the bonds (and to pay interest on the

bonds) continue to levied on the different generations of domestic taxpayers

Hillman, 2009: Public finance for public goods

70

B. Intergenerational tax sharing

Bond financing can be manipulated to redistribute income among different generations

Ricardian equivalence

When the taxes of different people repay the bond, the choice between taxes and bond financing has distributional effects

Whether taxes or bond financing is used does not matter for an individual, if the same individual pays the taxes that finance interest and repayment of the government loan

Intergenerational altruism makes taxation and bond financing equivalent

When governments tax gifts or bequests, the intergenerational altruism that restores Ricardian equivalence is taxed

Hillman, 2009: Public finance for public goods

71

Future taxpayers Is present bond-financed public spending consistent with the preferences of future taxpayers? Asymmetric information: Only a future generation knows its own preferences for public spending

In practice, present generations have no choice but to make decisions on behalf of future generations Example of defense

o Defense spending provides a public good for the immediately threatened generation

o Future generations also benefit o It therefore seems reasonable that future generations should

pay part of the cost of ending the threat, through future taxes of bond financing

Hillman, 2009: Public finance for public goods

72

C. Fiscal illusion in bond financing

Do taxpayers know that bond financing implies future taxes? If so, do taxpayers accurately perceive the values of their

future tax liabilities due to bond financing? The compensating transfers required for Ricardian equivalence require positive answers to both questions Asymmetric information because of fiscal illusion

A political principal-agent problem allows government spending to exceed the spending that informed tax payers would want

Hillman, 2009: Public finance for public goods

73

D. Constitutional restraint on government borrowing

We have identified reasons why bond financing can be socially undesirable

o A government might favor contemporary taxpayers through bond financing

o If there is fiscal illusion, present taxpayers will find

themselves with higher tax payments (and excess burdens) in the future than they would have agreed to

A legal constitutional restraint can limit financing through government borrowing to benefits that each future generation receives from past public investment

Hillman, 2009: Public finance for public goods

74

A budgetary surplus We have been considering a government that requires revenue to finance spending Surplus revenue can be used: (1) to reduce present taxes (benefits present taxpayers) (2) to repay past government borrowing by buying back

previously issued government bonds (benefits future taxpayers)

(3) in ways that benefit particular groups rather than to take advantage of the surplus to reduce present or future taxes

The decision about how to use a government budget surplus is distributional and political

Constitutional restraint can also apply to government policies when there are budgetary surpluses

Hillman, 2009: Public finance for public goods

75

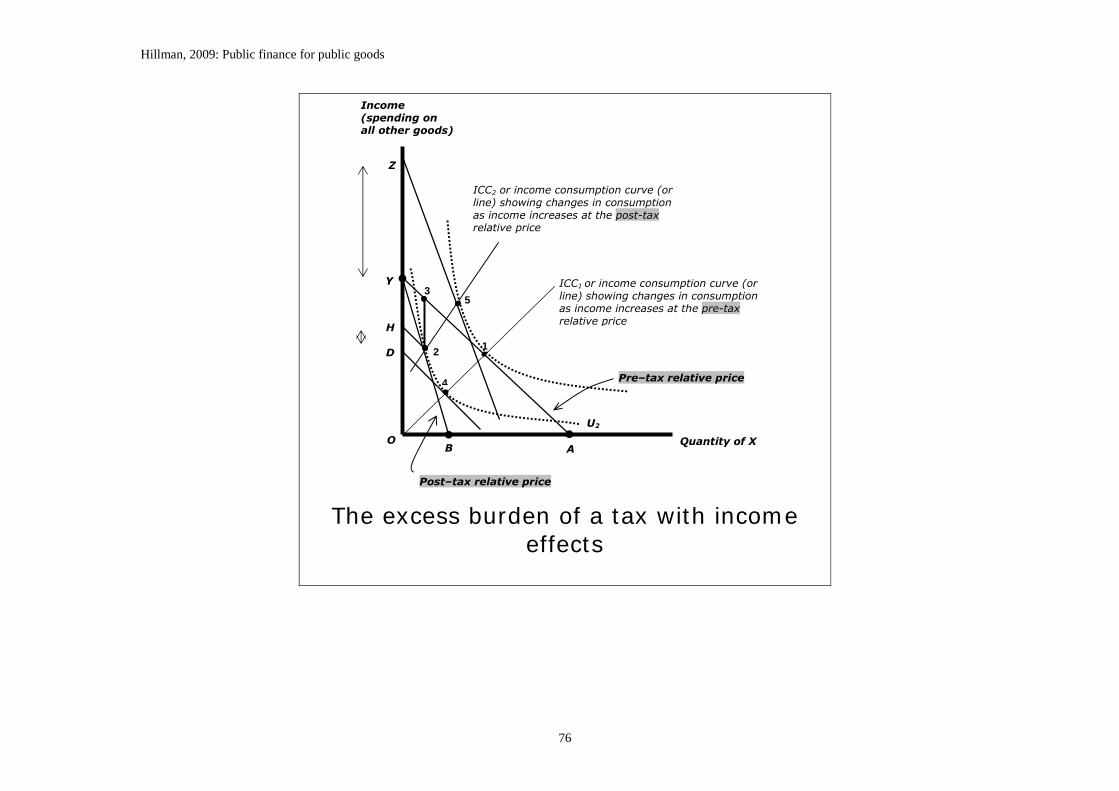

SUPPLEMENT

The excess burden with substitution and income effects

The analysis of the excess burden of taxation has been based on the substitution effects alone Taxes also have an income effect

The excess burden as payment to avoid a tax and compensation for a tax differ because of the income effect

Hillman, 2009: Public finance for public goods

76

The excess burden of a tax with income effects

1

5

H

D 2

3

4

A O

B

Y

Z

U2

Pre–tax relative price

ICC1 or income consumption curve (or line) showing changes in consumption as income increases at the pre-tax relative price

Quantity of X

ICC2 or income consumption curve (or line) showing changes in consumption as income increases at the post-tax relative price