36

Presentation to the National Assembly Portfolio Committee on Trade and Industry Public Hearings on the National Credit Amendment Bill 30 January 2018 Mr. Hennie Ferreira CEO

Presentation to the National Assembly Portfolio Committee on Trade and Industry

Public Hearings on the National Credit Amendment Bill30 January 2018

Mr. Hennie FerreiraCEO

Our Purpose Today

LEGISLATED DEBT INTERVENTIONS: A BALANCED APPROACH TO THE RIGHTS OF

CONSUMERS AND CREDIT PROVIDERS

LEGAL & RESPONSIBLE

MICRO FINANCIERS

CONSUMER RIGHTS

Micro financiers are distinct self sustaining small businesses, who fulfil a unique role the South African credit ecosystem

Micro financiers are legal and responsible lenders providing affordable short term and unsecured loans to South African in need of financial inclusion

Enabling Financial Inclusion to meet real, basic needs

Recognition and provision of existing measures

Evidence based, practical and pragmatic recommendations for legislating

5 Key Themes and Messages

1

2

3

45

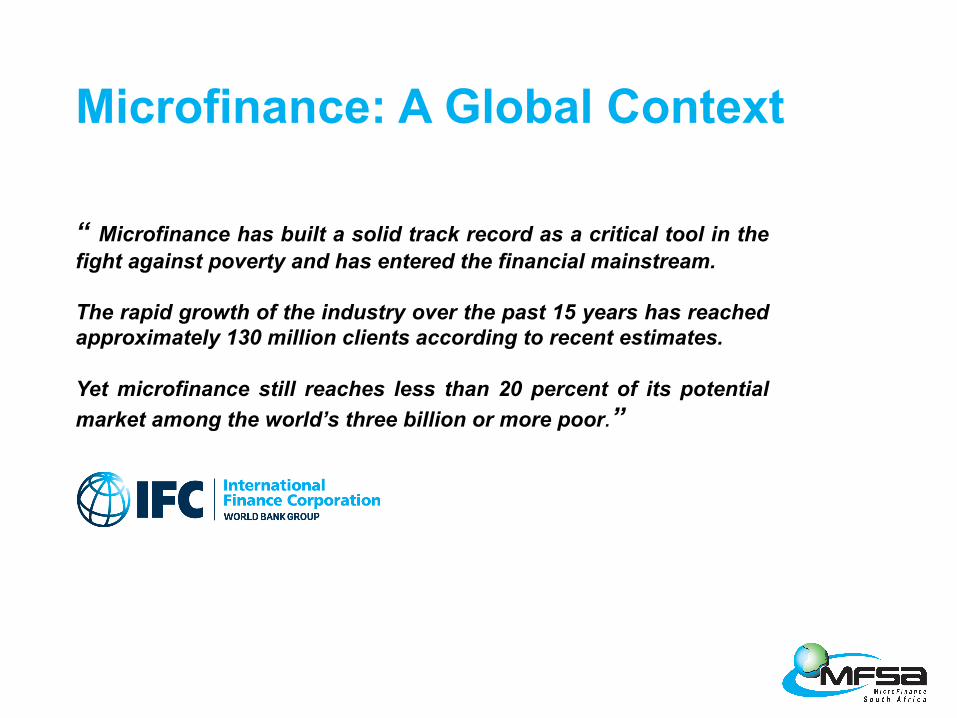

Microfinance: A Global Context

“ Microfinance has built a solid track record as a critical tool in thefight against poverty and has entered the financial mainstream.

The rapid growth of the industry over the past 15 years has reachedapproximately 130 million clients according to recent estimates.

Yet microfinance still reaches less than 20 percent of its potentialmarket among the world’s three billion or more poor.”

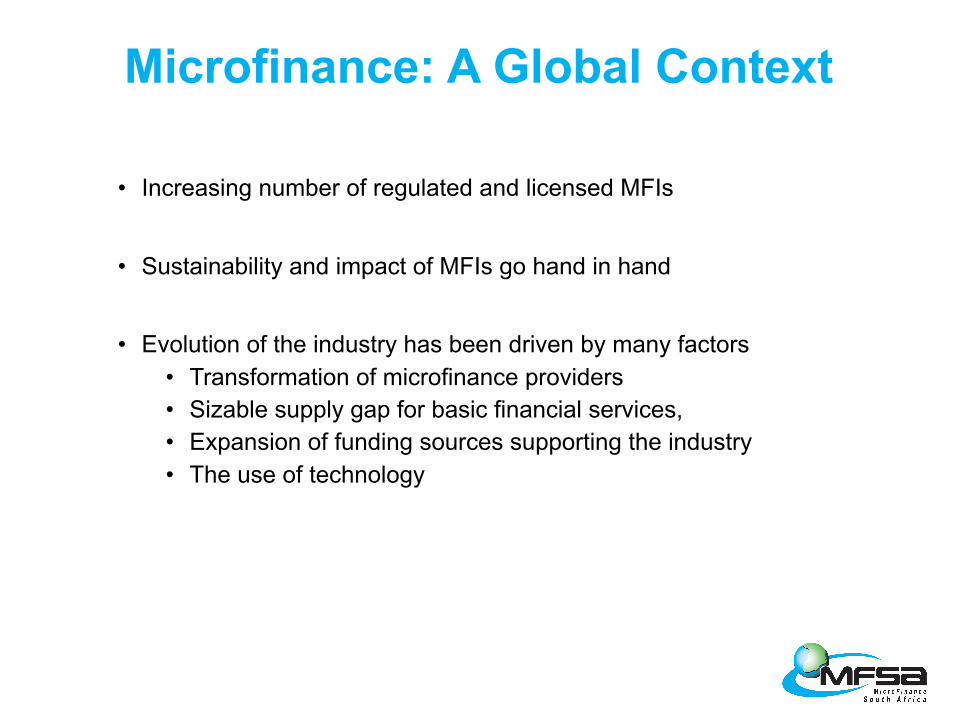

Microfinance: A Global Context

• Increasing number of regulated and licensed MFIs

• Sustainability and impact of MFIs go hand in hand

• Evolution of the industry has been driven by many factors• Transformation of microfinance providers• Sizable supply gap for basic financial services,• Expansion of funding sources supporting the industry• The use of technology

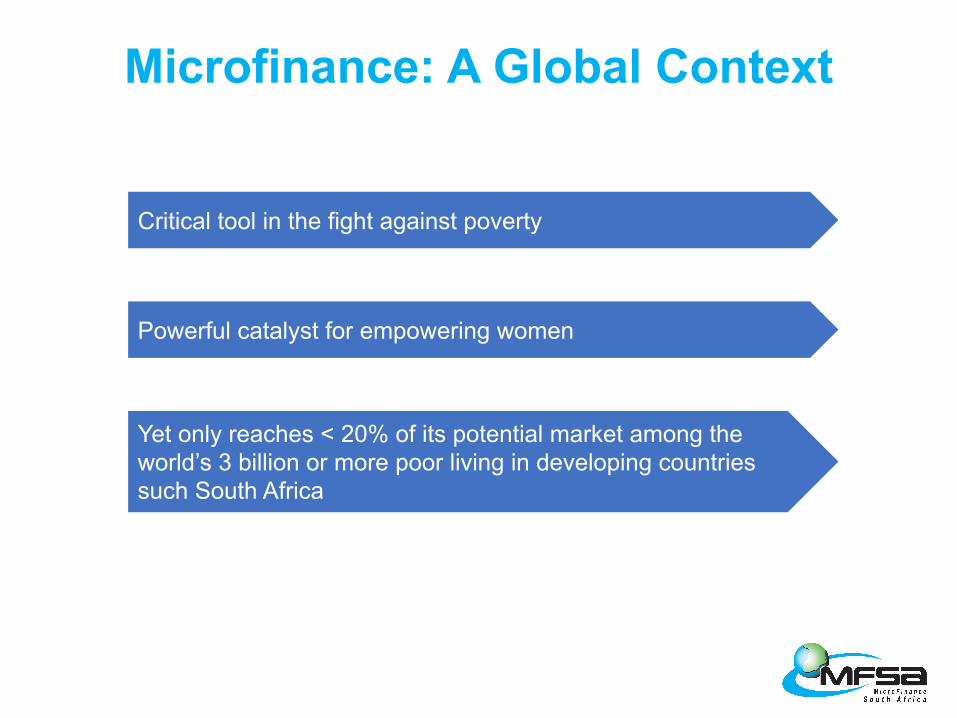

Microfinance: A Global Context

Yet only reaches < 20% of its potential market among the world’s 3 billion or more poor living in developing countries such South Africa

Critical tool in the fight against poverty

Powerful catalyst for empowering women

Microfinance: South African Context

In developing countries such as South Africa, Microfinance achieves the following:who have little or no access to formal financial services.

• Access to financial services for poor people - powerful instrument for reducing poverty

• Enabling poor people to build assets, increase incomes, and reduce their vulnerability to economic stress.

• Enabling savings, loans, and money transfers, enabling poor families to:• invest in enterprises• Access better nutrition,• Improve their living conditions• Cater for the health and education of their children.

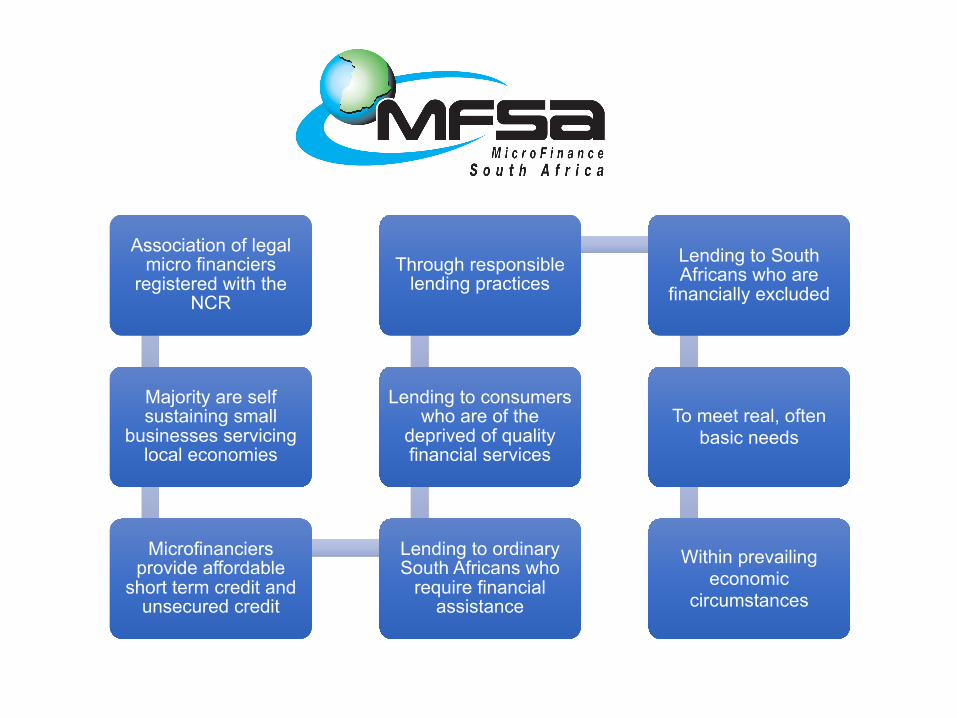

Association of legal micro financiers

registered with the NCR

Majority are self sustaining small

businesses servicing local economies

Microfinanciers provide affordable

short term credit and unsecured credit

Lending to ordinary South Africans who

require financial assistance

Lending to consumers who are of the

deprived of quality financial services

Through responsible lending practices

Lending to South Africans who are

financially excluded

To meet real, often basic needs

Within prevailing economic

circumstances

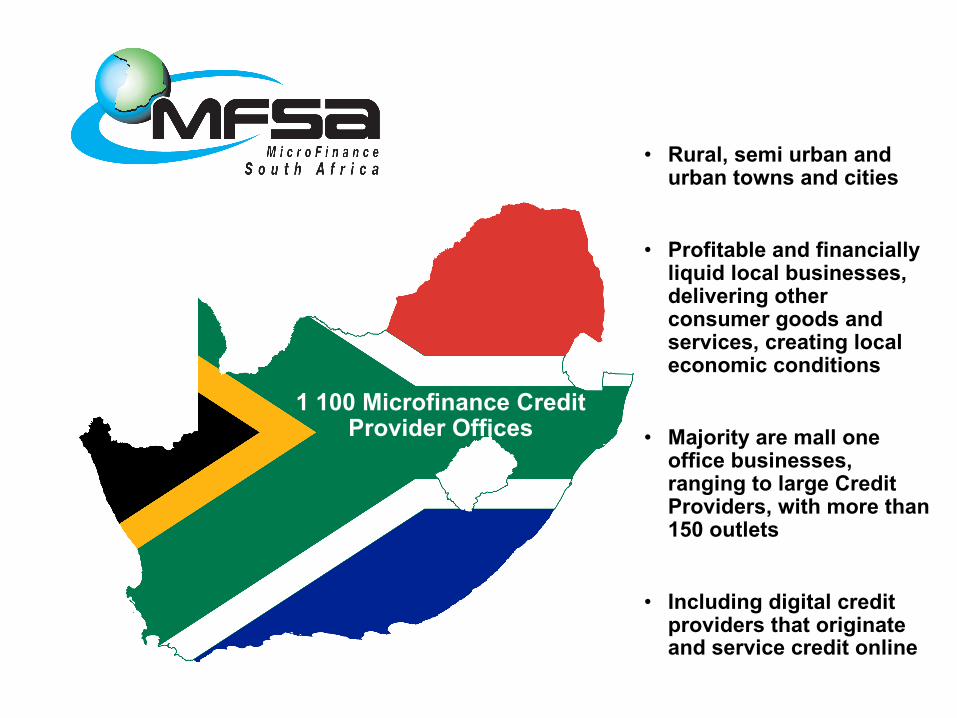

1 100 Microfinance CreditProvider Offices

• Rural, semi urban and urban towns and cities

• Profitable and financially liquid local businesses, delivering other consumer goods and services, creating local economic conditions

• Majority are mall one office businesses, ranging to large Credit Providers, with more than 150 outlets

• Including digital credit providers that originate and service credit online

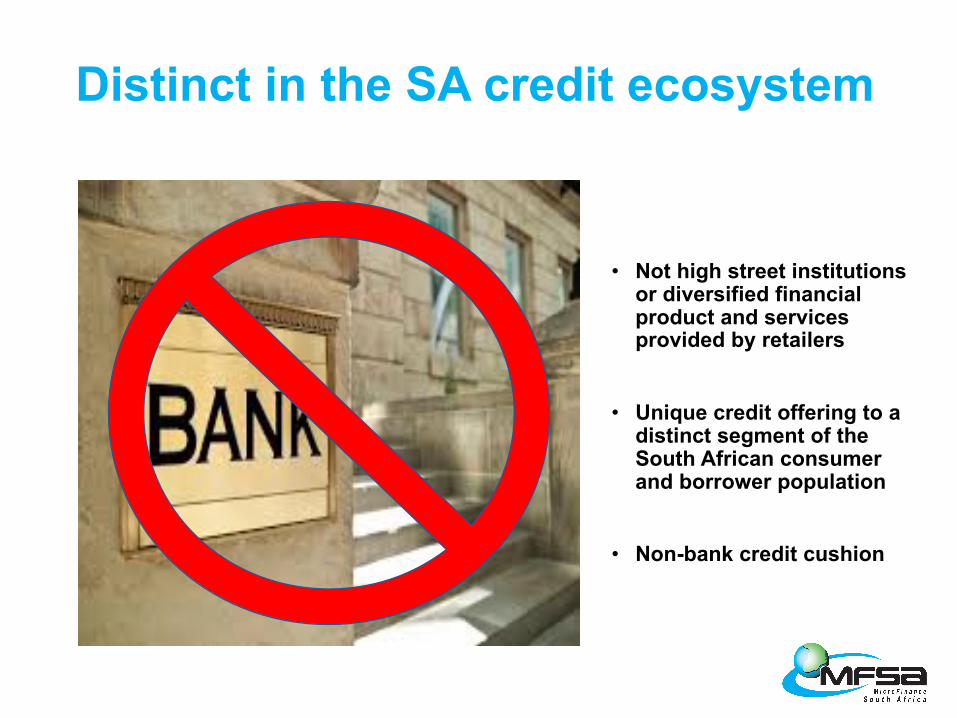

Distinct in the SA credit ecosystem

• Not high street institutions or diversified financial product and services provided by retailers

• Unique credit offering to a distinct segment of the South African consumer and borrower population

• Non-bank credit cushion

• Do not take or hold depositors money.• MFIs assume the full risk

Thus, any legislative proposals cannot define and impose regulation, which assumes and treats all credit providers as banks.

Distinct in the SA credit ecosystem

Legal microfinanciers registered with the

National Credit Regulator

Subscribe to an Industry Code of Conduct which ensures and facilitates professional, legal and

ethical conduct

There has never been a charge against a MFSA member for abusing the

National Payment System

We are responsible credit providers

MFSA Members are Misunderstood• Illegal underground rogue

lenders, ’mashonisas’ and loan sharks DO EXIST

• NOT MFSA members

• We do not engage in instants loans with punitive consumer practices detrimental to financial and socio economic welling of consumers afflicted by poverty and unemployment

• NCR should play a more active role including enforcement of the National Credit Act.

We need to guard against legislated debt interventions which will further drive consumers out of the credit market and into the

underground market.

Serving Needy SA Consumers

• Low income citizens most deprived of quality financial services –

• Short Term Unsecured lending products

• Up to 6 months - Maximum Average of R8 000

• Practically and simplistically achieving financial inclusion

Responsible Credit forReal-Life Needs

✓ Typically for purposes which normal commercial banks would not offer

✓ Take into account personal and financial position of consumers

✓ Recognising that such credit may be used for basic necessities§ school and related fees§ groceries, public transport costs, § servicing secured debt obligations

✓ Consumers awareness of applicable T&Cs

✓ Consumers cognisant of not defaulting on repayments as this may limit or cease their ability to obtain short-term credit in future

Existing debt intervention measures

• Many debt relief interventions are already in place

• Legislated debt relief may build on and strengthen these

• E.g. debt counselling and alternative dispute resolution

• Recognition should be afforded to credit providers which already apply debt intervention on a case-by-case and ongoing basis. E.g.

§ Ongoing Consumer Education§ Applying the National Credit Act Including the Affordability Regulations§ Mediation and engagement with consumers who cannot afford to make payments

Existing debt intervention measures

Legislative recognition and provisions should also be afforded to ….

• Role of the Credit Ombud • Affordability Regulations • Consumer education and awareness • Informal Debt Mediation• Debt Counselling• Changes to prescription of Debt• Administration orders• Sequestration• Legal Debt Collection

5 Principles on Debt Intervention1. Sustainable credit ecosystem benefiting society in totality, including financially challenged

consumers

2. Implies recognition for the distinct role of legitimate and responsible microfinanciers fulfilling a specific role in the credit ecosystem and address a need, which commercial and retail banks cannot and will not fulfill.

3. Therefore while both banks and microfinanciers are all registered and legal credit providers, MFSA members cannot be regulated in the same manner as banks, specifically in areas such as:

• Interest rates and fees• Credit life insurance • Implementation of imposed debt relief

4. Consumers who land in a debt predicament through legitimate and authentic reasons, can be assisted, through a process, and reach a negotiated and fair solution.

5. A fair process considers the consequence to the total eco-system and has an intention to facilitate sustainable lending and borrowing practices and behaviors.

Methodology to estimate the impact of draft legislative proposals:• Sample of the credit active consumer base, prior to 24 November 2017.

• Application confined to consumers with a valid SA Identity Number.

• Applying the definition of ‘Debt Intervention’ according to the following criteria:• Unsecured debt/short term credit totalling (Less than or Equal to R50 000)• Predicted Income (Less than or Equal to R7 500)• No Legal action status codes• No Debt Counselling

• Rural / Urban categorisation

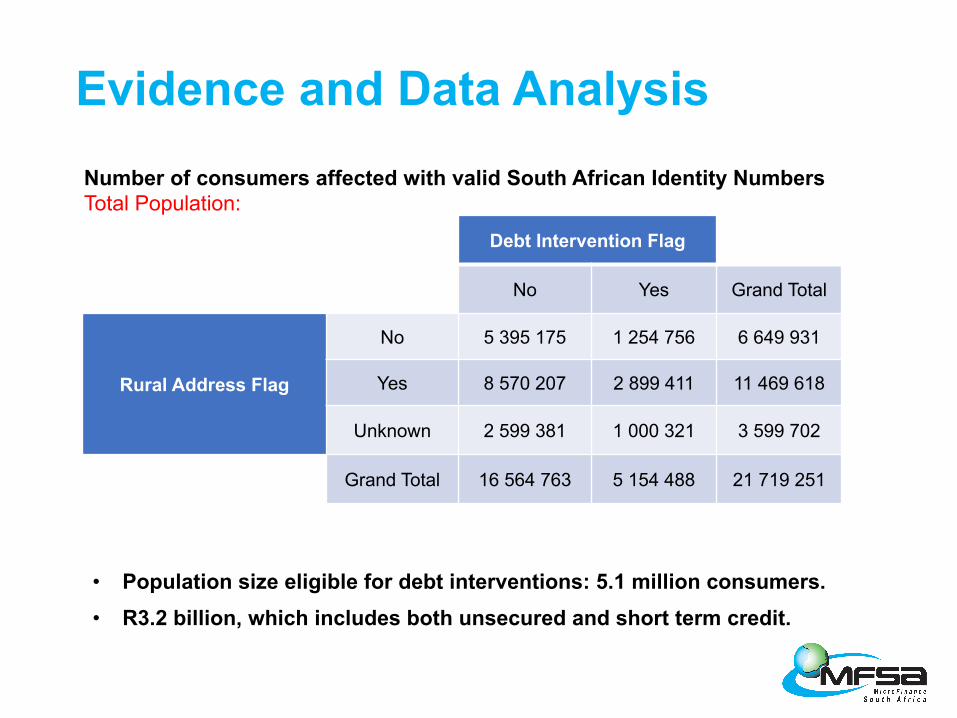

Evidence and Data Analysis

• Population size eligible for debt interventions: 5.1 million consumers.• R3.2 billion, which includes both unsecured and short term credit.

Debt Intervention Flag

No Yes Grand Total

Rural Address Flag

No 5 395 175 1 254 756 6 649 931

Yes 8 570 207 2 899 411 11 469 618

Unknown 2 599 381 1 000 321 3 599 702

Grand Total 16 564 763 5 154 488 21 719 251

Number of consumers affected with valid South African Identity NumbersTotal Population:

Evidence and Data Analysis

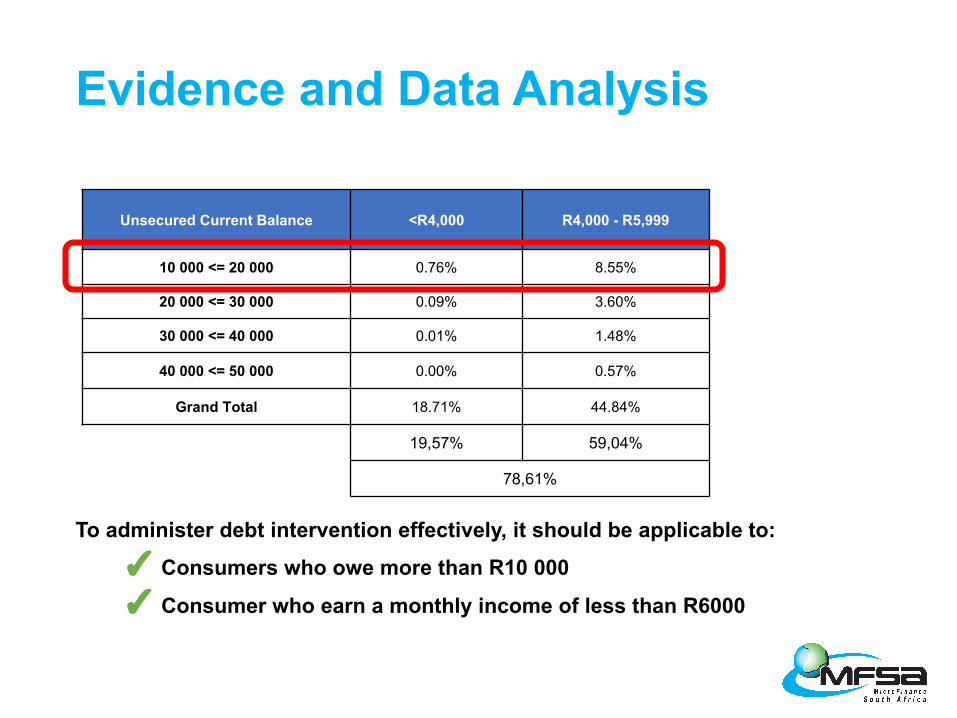

Evidence and Data Analysis

Unsecured Current Balance <R4,000 R4,000 - R5,999

10 000 <= 20 000 0.76% 8.55%

20 000 <= 30 000 0.09% 3.60%

30 000 <= 40 000 0.01% 1.48%

40 000 <= 50 000 0.00% 0.57%

Grand Total 18.71% 44.84%

19,57% 59,04%

78,61%

To administer debt intervention effectively, it should be applicable to: ✓ Consumers who owe more than R10 000✓ Consumer who earn a monthly income of less than R6000

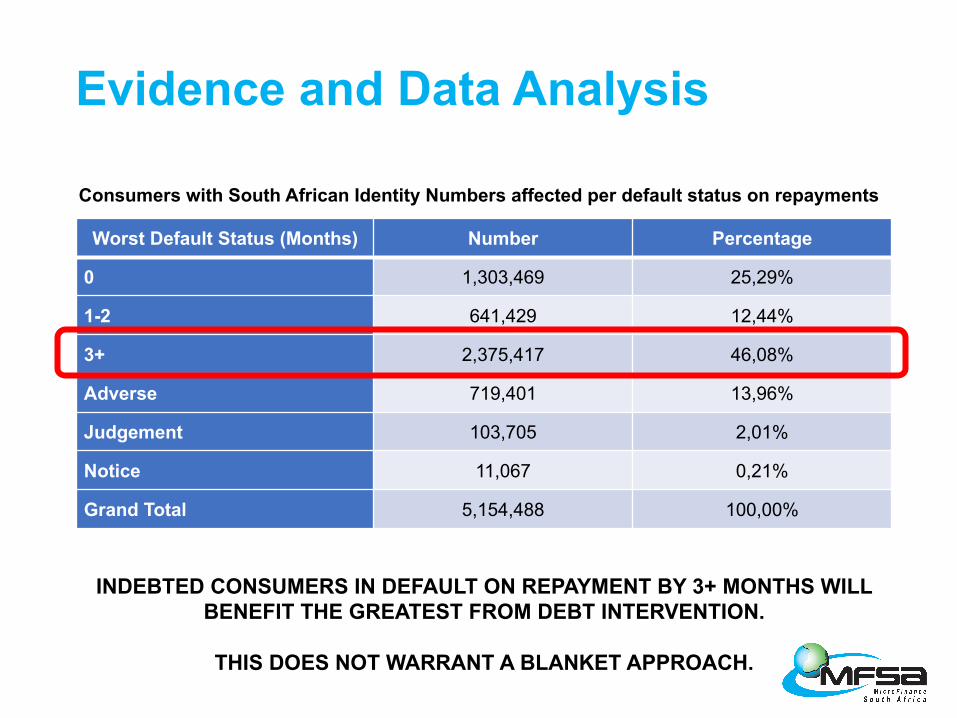

Consumers with South African Identity Numbers affected per default status on repayments

Worst Default Status (Months) Number Percentage

0 1,303,469 25,29%

1-2 641,429 12,44%

3+ 2,375,417 46,08%

Adverse 719,401 13,96%

Judgement 103,705 2,01%

Notice 11,067 0,21%

Grand Total 5,154,488 100,00%

Evidence and Data Analysis

INDEBTED CONSUMERS IN DEFAULT ON REPAYMENT BY 3+ MONTHS WILL BENEFIT THE GREATEST FROM DEBT INTERVENTION.

THIS DOES NOT WARRANT A BLANKET APPROACH.

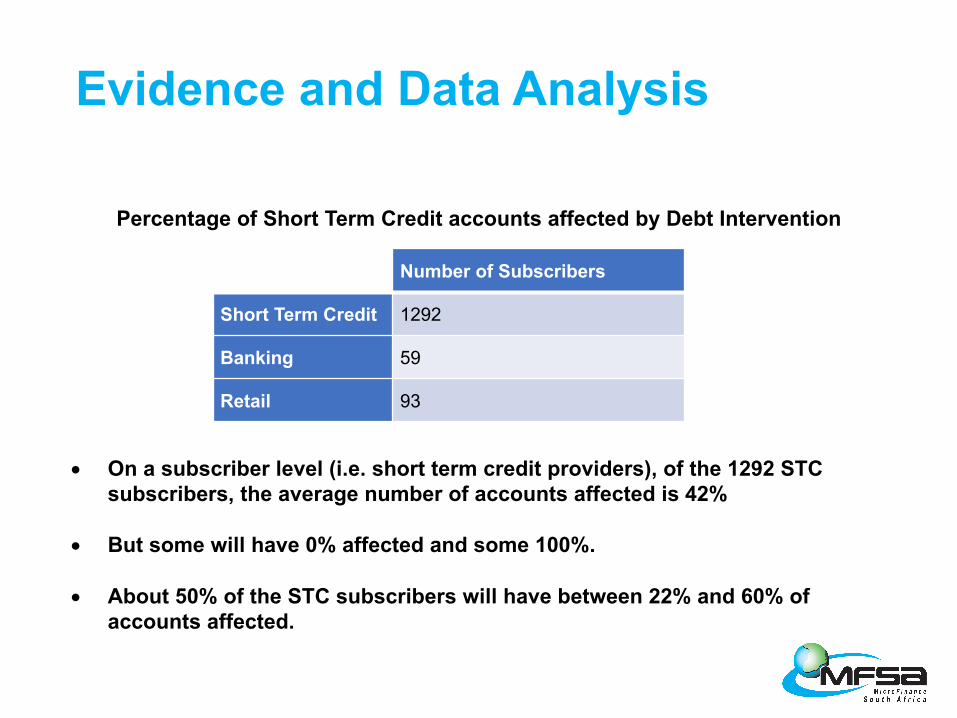

Percentage of Short Term Credit accounts affected by Debt Intervention

Number of Subscribers

Short Term Credit 1292

Banking 59

Retail 93

• On a subscriber level (i.e. short term credit providers), of the 1292 STC subscribers, the average number of accounts affected is 42%

• But some will have 0% affected and some 100%.

• About 50% of the STC subscribers will have between 22% and 60% of accounts affected.

Evidence and Data Analysis

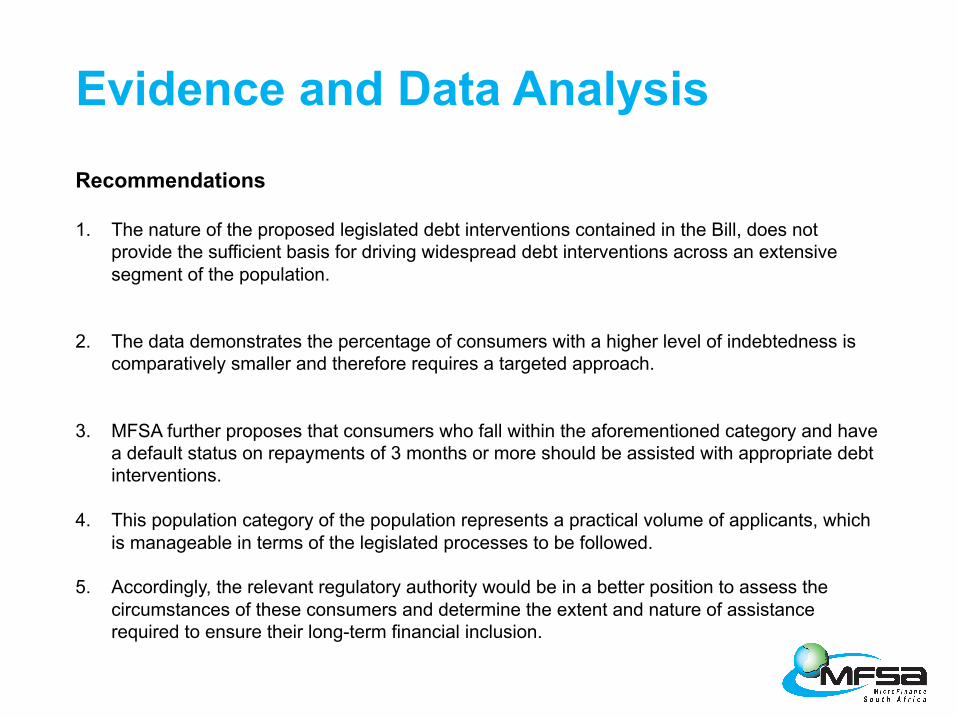

Recommendations

1. The nature of the proposed legislated debt interventions contained in the Bill, does not provide the sufficient basis for driving widespread debt interventions across an extensive segment of the population.

2. The data demonstrates the percentage of consumers with a higher level of indebtedness is comparatively smaller and therefore requires a targeted approach.

3. MFSA further proposes that consumers who fall within the aforementioned category and have a default status on repayments of 3 months or more should be assisted with appropriate debt interventions.

4. This population category of the population represents a practical volume of applicants, which is manageable in terms of the legislated processes to be followed.

5. Accordingly, the relevant regulatory authority would be in a better position to assess the circumstances of these consumers and determine the extent and nature of assistance required to ensure their long-term financial inclusion.

Evidence and Data Analysis

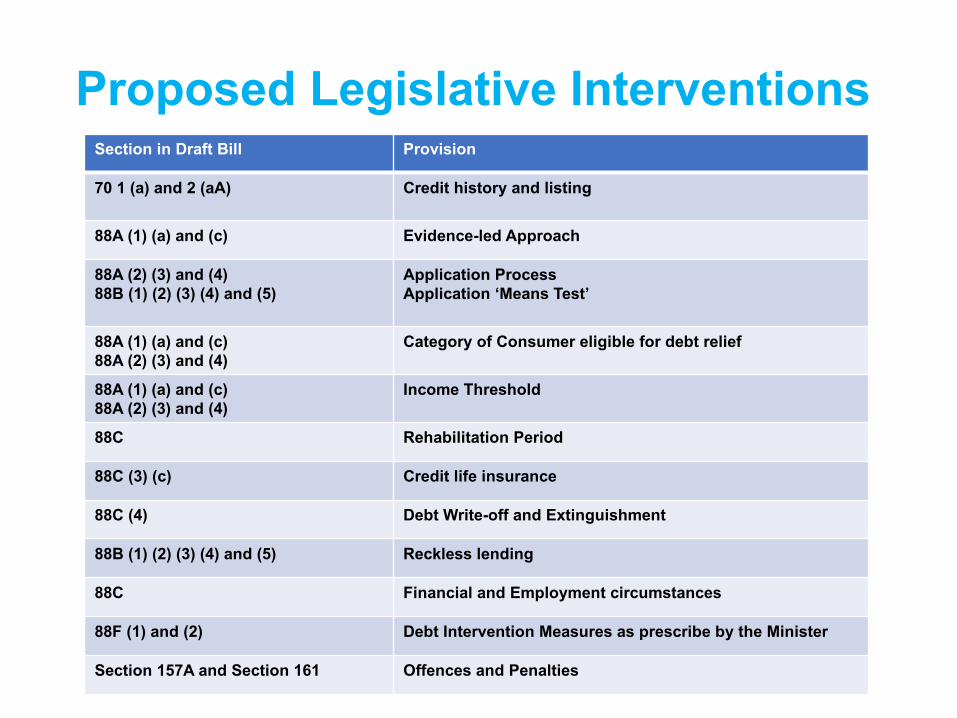

Proposed Legislative InterventionsSection in Draft Bill Provision

70 1 (a) and 2 (aA) Credit history and listing

88A (1) (a) and (c) Evidence-led Approach

88A (2) (3) and (4)88B (1) (2) (3) (4) and (5)

Application Process Application ‘Means Test’

88A (1) (a) and (c)88A (2) (3) and (4)

Category of Consumer eligible for debt relief

88A (1) (a) and (c)88A (2) (3) and (4)

Income Threshold

88C Rehabilitation Period

88C (3) (c) Credit life insurance

88C (4) Debt Write-off and Extinguishment

88B (1) (2) (3) (4) and (5) Reckless lending

88C Financial and Employment circumstances

88F (1) and (2) Debt Intervention Measures as prescribe by the Minister

Section 157A and Section 161 Offences and Penalties

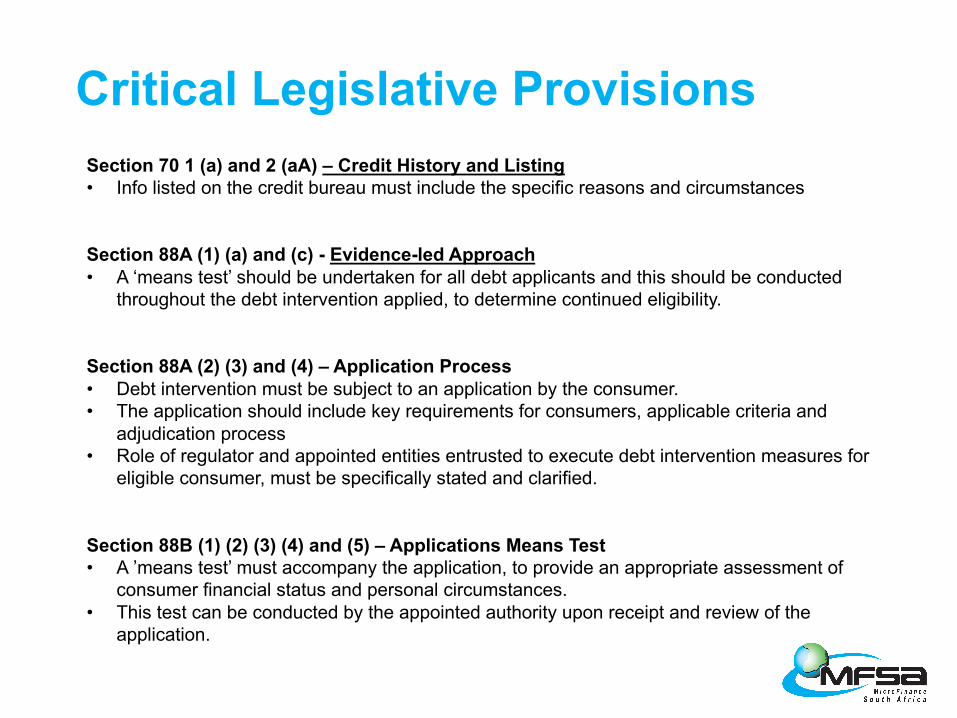

Section 70 1 (a) and 2 (aA) – Credit History and Listing• Info listed on the credit bureau must include the specific reasons and circumstances

Section 88A (1) (a) and (c) - Evidence-led Approach• A ‘means test’ should be undertaken for all debt applicants and this should be conducted

throughout the debt intervention applied, to determine continued eligibility.

Section 88A (2) (3) and (4) – Application Process• Debt intervention must be subject to an application by the consumer.• The application should include key requirements for consumers, applicable criteria and

adjudication process• Role of regulator and appointed entities entrusted to execute debt intervention measures for

eligible consumer, must be specifically stated and clarified.

Section 88B (1) (2) (3) (4) and (5) – Applications Means Test• A ’means test’ must accompany the application, to provide an appropriate assessment of

consumer financial status and personal circumstances.• This test can be conducted by the appointed authority upon receipt and review of the

application.

Critical Legislative Provisions

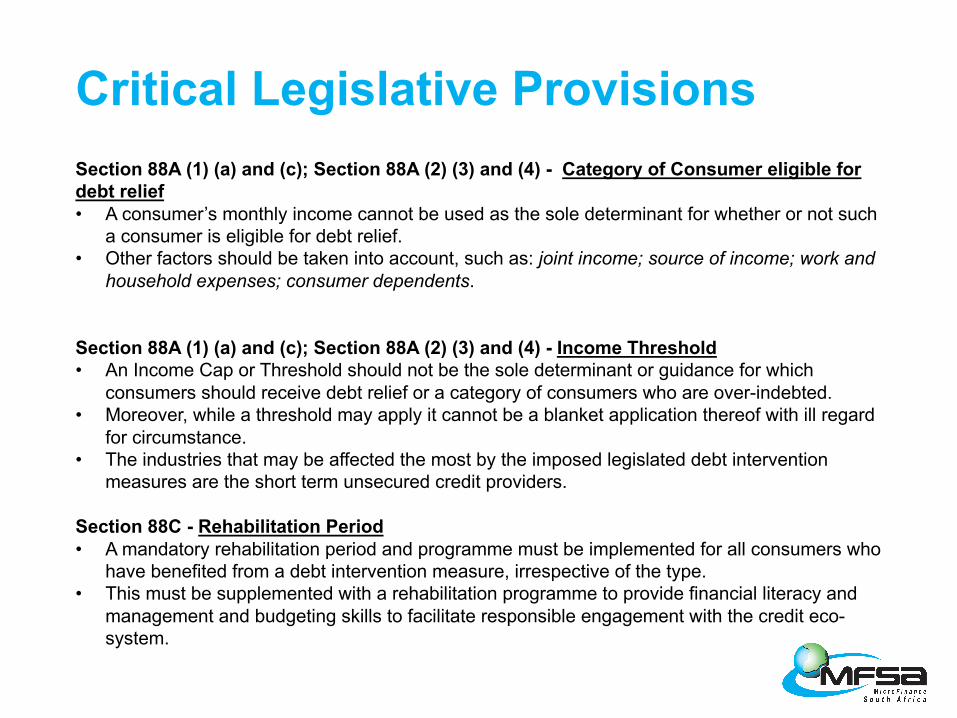

Section 88A (1) (a) and (c); Section 88A (2) (3) and (4) - Category of Consumer eligible for debt relief• A consumer’s monthly income cannot be used as the sole determinant for whether or not such

a consumer is eligible for debt relief.• Other factors should be taken into account, such as: joint income; source of income; work and

household expenses; consumer dependents.

Section 88A (1) (a) and (c); Section 88A (2) (3) and (4) - Income Threshold• An Income Cap or Threshold should not be the sole determinant or guidance for which

consumers should receive debt relief or a category of consumers who are over-indebted.• Moreover, while a threshold may apply it cannot be a blanket application thereof with ill regard

for circumstance.• The industries that may be affected the most by the imposed legislated debt intervention

measures are the short term unsecured credit providers.

Section 88C - Rehabilitation Period• A mandatory rehabilitation period and programme must be implemented for all consumers who

have benefited from a debt intervention measure, irrespective of the type.• This must be supplemented with a rehabilitation programme to provide financial literacy and

management and budgeting skills to facilitate responsible engagement with the credit eco-system.

Critical Legislative Provisions

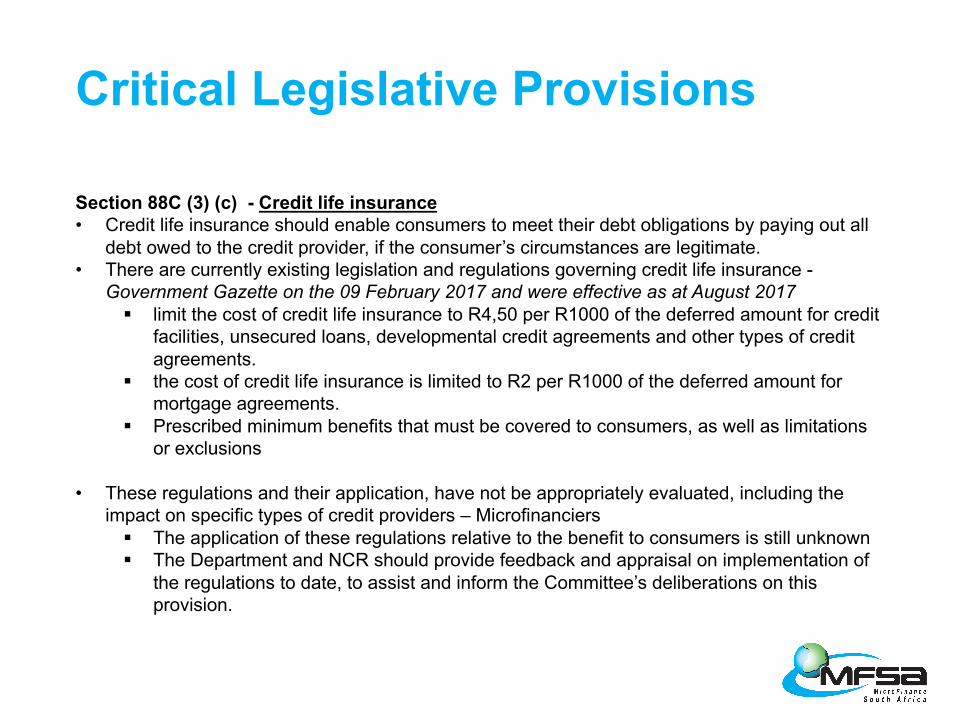

Section 88C (3) (c) - Credit life insurance• Credit life insurance should enable consumers to meet their debt obligations by paying out all

debt owed to the credit provider, if the consumer’s circumstances are legitimate.• There are currently existing legislation and regulations governing credit life insurance -

Government Gazette on the 09 February 2017 and were effective as at August 2017§ limit the cost of credit life insurance to R4,50 per R1000 of the deferred amount for credit

facilities, unsecured loans, developmental credit agreements and other types of credit agreements.

§ the cost of credit life insurance is limited to R2 per R1000 of the deferred amount for mortgage agreements.

§ Prescribed minimum benefits that must be covered to consumers, as well as limitations or exclusions

• These regulations and their application, have not be appropriately evaluated, including the impact on specific types of credit providers – Microfinanciers§ The application of these regulations relative to the benefit to consumers is still unknown§ The Department and NCR should provide feedback and appraisal on implementation of

the regulations to date, to assist and inform the Committee’s deliberations on this provision.

Critical Legislative Provisions

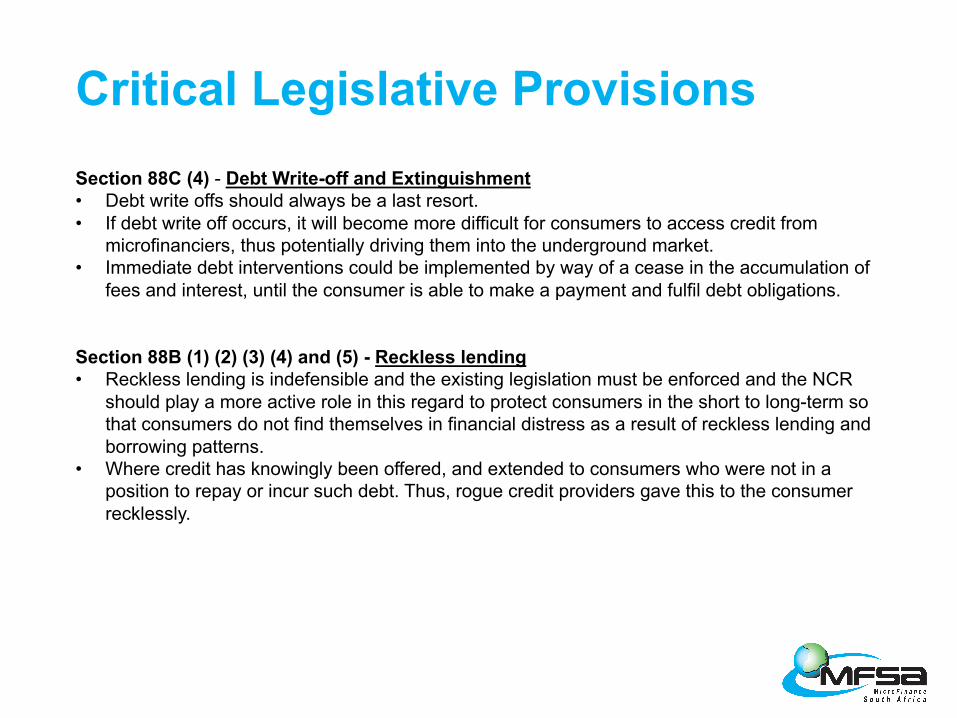

Section 88C (4) - Debt Write-off and Extinguishment• Debt write offs should always be a last resort.• If debt write off occurs, it will become more difficult for consumers to access credit from

microfinanciers, thus potentially driving them into the underground market.• Immediate debt interventions could be implemented by way of a cease in the accumulation of

fees and interest, until the consumer is able to make a payment and fulfil debt obligations.

Section 88B (1) (2) (3) (4) and (5) - Reckless lending• Reckless lending is indefensible and the existing legislation must be enforced and the NCR

should play a more active role in this regard to protect consumers in the short to long-term so that consumers do not find themselves in financial distress as a result of reckless lending and borrowing patterns.

• Where credit has knowingly been offered, and extended to consumers who were not in a position to repay or incur such debt. Thus, rogue credit providers gave this to the consumer recklessly.

Critical Legislative Provisions

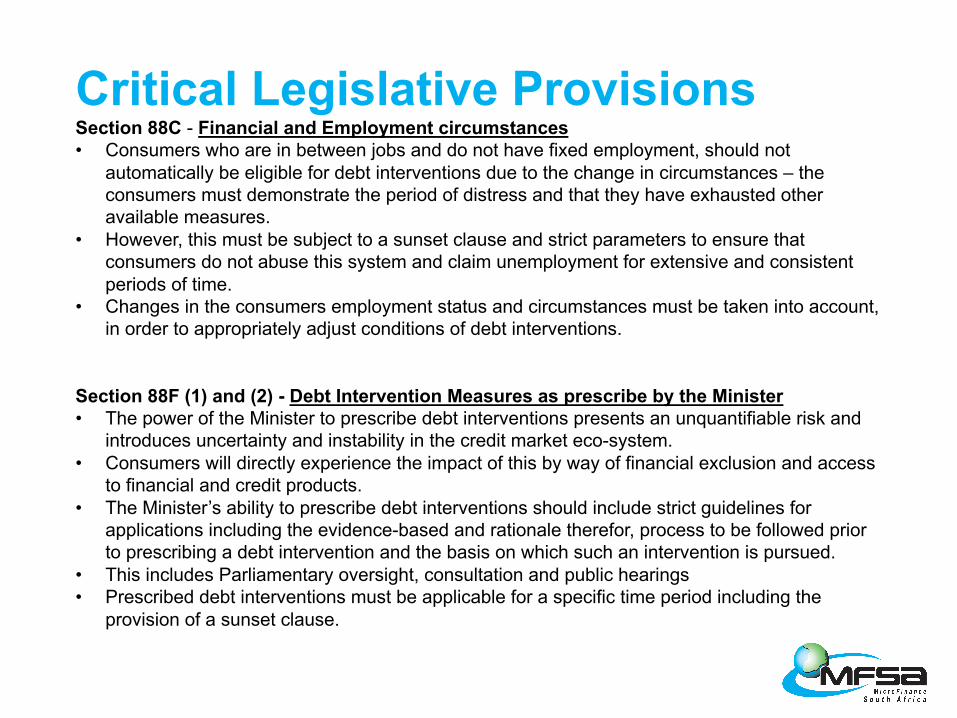

Section 88C - Financial and Employment circumstances• Consumers who are in between jobs and do not have fixed employment, should not

automatically be eligible for debt interventions due to the change in circumstances – the consumers must demonstrate the period of distress and that they have exhausted other available measures.

• However, this must be subject to a sunset clause and strict parameters to ensure that consumers do not abuse this system and claim unemployment for extensive and consistent periods of time.

• Changes in the consumers employment status and circumstances must be taken into account, in order to appropriately adjust conditions of debt interventions.

Section 88F (1) and (2) - Debt Intervention Measures as prescribe by the Minister • The power of the Minister to prescribe debt interventions presents an unquantifiable risk and

introduces uncertainty and instability in the credit market eco-system. • Consumers will directly experience the impact of this by way of financial exclusion and access

to financial and credit products.• The Minister’s ability to prescribe debt interventions should include strict guidelines for

applications including the evidence-based and rationale therefor, process to be followed prior to prescribing a debt intervention and the basis on which such an intervention is pursued.

• This includes Parliamentary oversight, consultation and public hearings• Prescribed debt interventions must be applicable for a specific time period including the

provision of a sunset clause.

Critical Legislative Provisions

Section 157A and Section 161 - Offences and Penalties

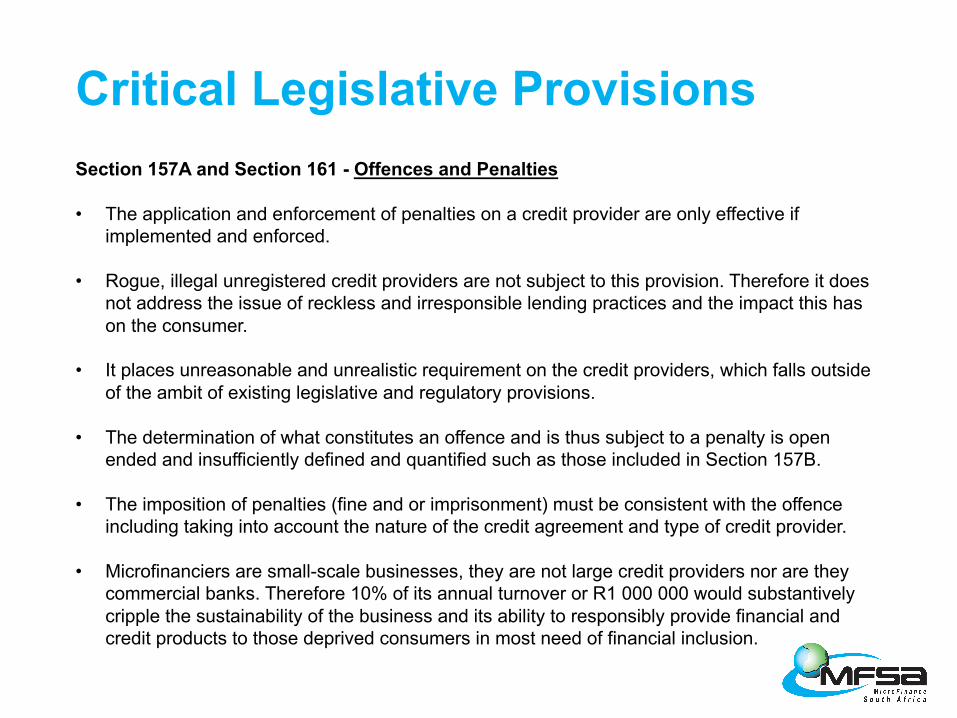

• The application and enforcement of penalties on a credit provider are only effective if implemented and enforced.

• Rogue, illegal unregistered credit providers are not subject to this provision. Therefore it does not address the issue of reckless and irresponsible lending practices and the impact this has on the consumer.

• It places unreasonable and unrealistic requirement on the credit providers, which falls outside of the ambit of existing legislative and regulatory provisions.

• The determination of what constitutes an offence and is thus subject to a penalty is open ended and insufficiently defined and quantified such as those included in Section 157B.

• The imposition of penalties (fine and or imprisonment) must be consistent with the offence including taking into account the nature of the credit agreement and type of credit provider.

• Microfinanciers are small-scale businesses, they are not large credit providers nor are they commercial banks. Therefore 10% of its annual turnover or R1 000 000 would substantively cripple the sustainability of the business and its ability to responsibly provide financial and credit products to those deprived consumers in most need of financial inclusion.

Critical Legislative Provisions

1. Moral Hazards

2. Removal of adverse credit information

3. Variable inflation for various LSMs

4. Legitimate consumer circumstances

5. Financial Exclusion and Stimulating the illegal Credit Market

Unintended Consequences

1. Moral Hazards• Consumer education and awareness is key during debt intervention, to

ensure reciprocal obligations for consumers and credit providers.• A rehabilitation program should be non-negotiable – ideally funded by the

State as a long-term benefitting all consumers

2. Removal of adverse credit information• Positive stepping stone, but has cultivated an expected norm for repetition,

resulting in bad borrower practices and undermining consumer’s legal obligation to service their debt incurred.

• Practically, it resulted in credit providers adopting a risk averse and an even more cautious approach to lending inadvertently penalizes those consumers who did not ‘benefit’ from such a ‘once-off’ regulatory remedy.

Unintended Consequences

3. Variable inflation for various LSMs• For lower LSMs, credit is more expensive and credit providers become more

risk averse.• Consequently loans may be extended to a specific category of people who

will pay the price and premium.

4. Legitimate consumer circumstances• Consumers should only be eligible for debt interventions on the basis of

authentic and legitimate circumstances and reasons.• This is to guard against the assumption that because it is offered, all

consumers should be eligible to attain the benefit.

5. Financial Exclusion and Stimulating the illegal Credit Market• Microfinanciers may be forced to exit the market if legislation favours debt

interventions without appropriate discretion and legitimate circumstances• Consumers then have 2 choices – financial exclusion, or resort to

underground and illegal rogue credit providers who prey on vulnerable consumers.

Unintended Consequences

1. Solutions to address over indebtedness• Affordable for short term consumers• Equitable and fair in respect of requirements of all credit providers• Merits based system in the interest of all consumers• Consideration must be given to individual circumstances• Regulator must be suitably comfortable and confident to execute its role• Built on consumer education and awareness

2. A holistic approach to address consumer interests in the credit ecosystem• Timely opportunity to comprehensively review the National Credit Act

3. Legal, registered are responsible microfinanciers are a distinct component of the SA credit ecosystem and require to be legislated for appropriately.

4. Any legislation for debt relief, not accompanied by lessons for responsible lending and borrowing for both consumers and credit providers, inculcates bad practices.

5. It is vitally important that any legislative interventions recognise that borrowing and lending are part of economic stimulus and that the role of lending in the market is to promote and support growth and development, for both consumers and the economy.

Conclusion