Page 1

1

Public Policy on Modern Governance And Public Policy on Modern Governance And Transparency To Improve Investment Transparency To Improve Investment

Environment In EgyptEnvironment In Egypt

Presented By

Eng. Ahmed El-SayedGAFI ; Consultant & Head of promotion Affairs

OECD Global Forum On International Investment

17-19 Nov. 2003

Page 2

2

Public Policy on Modern Governance & Transparency For Investment

FDI Inflows (World / MENA Countries/Egypt)

Egypt Overview ( Role of government in achieving transparency )

a) Demographic Data.

b) Political & Economic Indicators.

c) Trade & Markets.

d) General Authority for Investment and Free Zones

One stop Shop.

Disputes Settlements.

Laws Amendments .

e) Development of promotion role to be proactive for Targeting

quality FDI.

Cooperation with International organizations (MIGA/FIAS/UNCTAD/ OECD).

Page 3

3

World FDI Inflow

Page 4

4

FDI Inflow In The World 2002

In Billion US $

Source : World Investment Report United Nation 2003

254

482

686

1079

824

652

0

200

400

600

800

1000

1200

1400

1991

-199

6

1997

1998

1999

2000

2001

2002

1392

41%

21%

Page 5

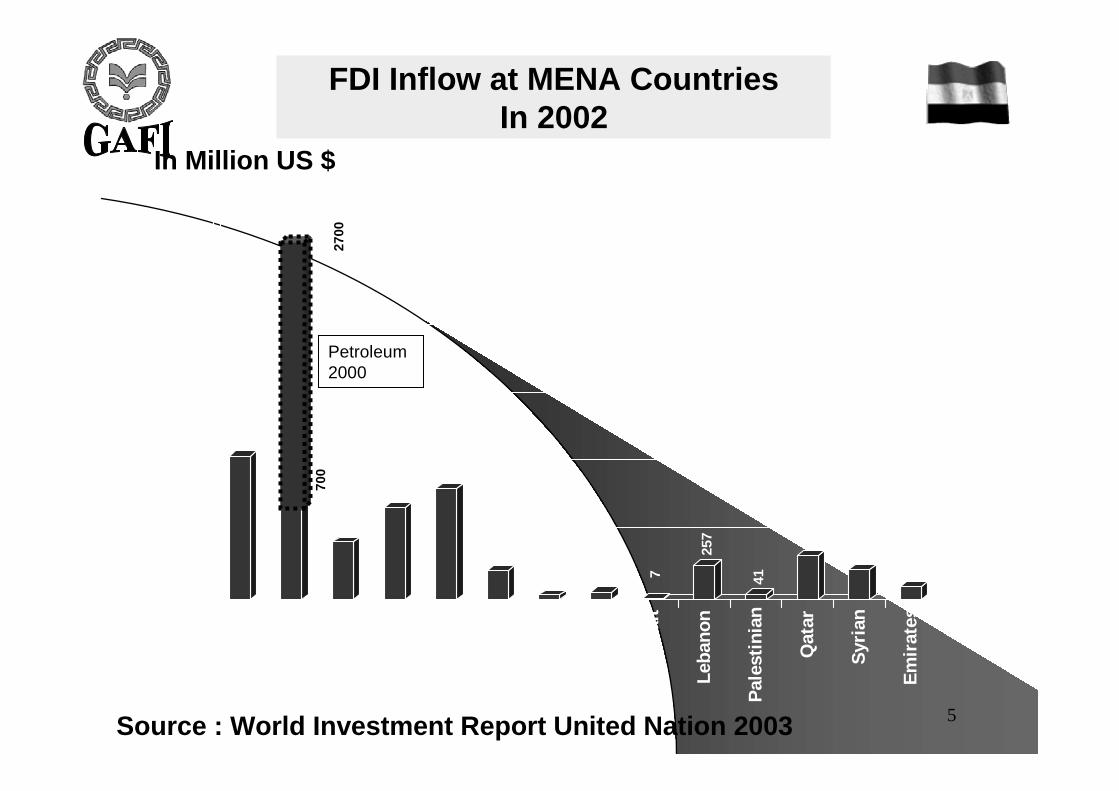

5

FDI Inflow at MENA CountriesIn 2002

1065

428

681 82

1

218

37 56

7

257

41

326

225

95

0

500

1000

1500

2000

2500

3000

Alg

eria

Egy

pt

Mor

occo

Sud

an

Tuni

sia

Bah

rain

Iran

Jord

an

Kuw

ait

Leba

non

Pal

esti

nian

Qat

ar

Syr

ian

Em

irat

es

In Million US $

Source : World Investment Report United Nation 2003

700

Petroleum 2000

2700

Page 6

6

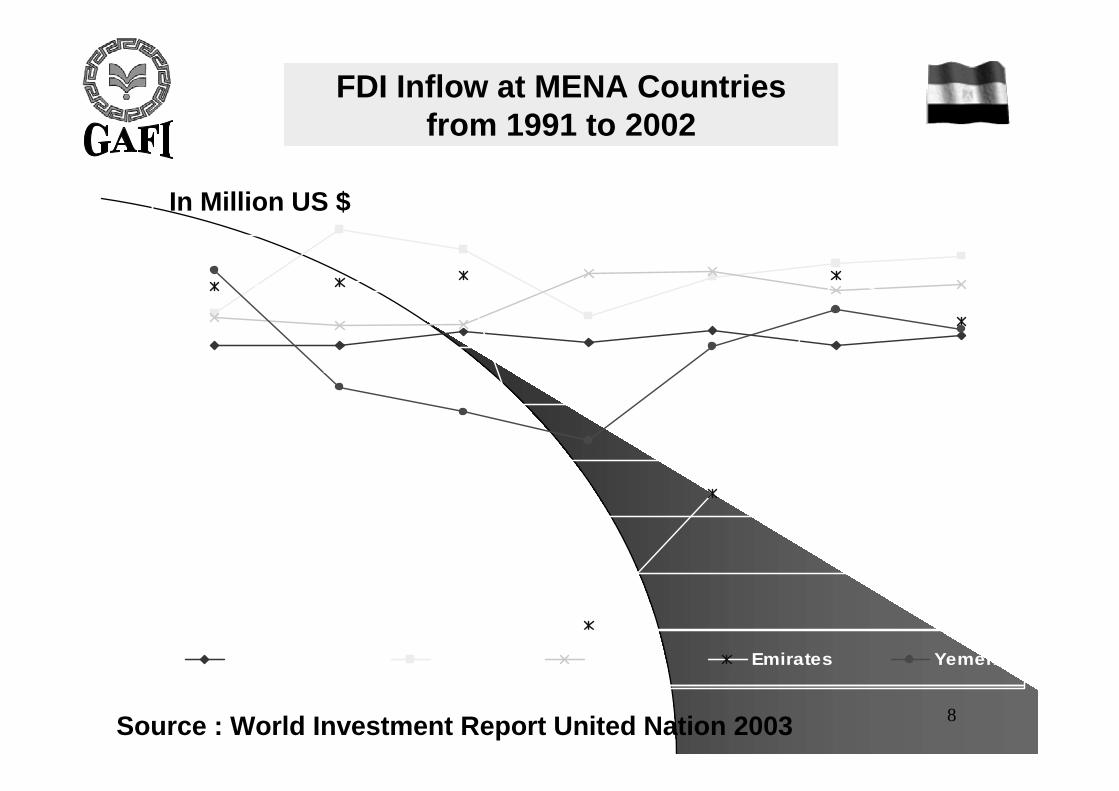

FDI Inflow at MENA Countriesfrom 1991 to 2002

-500

0

500

1000

1500

2000

2500

3000

1991-1996 1997 1998 1999 2000 2001 2002

Algeria Egypt Libyan Morocco Sudan Tunisia

In Million US $

Source : World Investment Report United Nation 2003

Page 7

7

FDI Inflow at MENA Countriesfrom 1991 to 2002

-200

0

200

400

600

800

1000

1991-1996 1997 1998 1999 2000 2001 2002

Bahrain Iran Jordan Kuwait Lebanon

In Million US $

Source : World Investment Report United Nation 2003

Page 8

8

FDI Inflow at MENA Countriesfrom 1991 to 2002

-1200

-1000

-800

-600

-400

-200

0

200

400

600

1991-1996 1997 1998 1999 2000 2001 2002

Palestinian Qatar Syrian Emirates Yemen

In Million US $

Source : World Investment Report United Nation 2003

Page 9

9

Factors Affecting FDI InflowFactors Affecting FDI InflowPolitical & Economic Stability

Market access .

Cost of doing business .

Utilities ( water , Electricity , Gas , Telecommunication , ………..).

Other Resources.

Availability of world class infrastructure.

Availability of well trained , productive & low cost work force.

Transparency.

Availability of information.

Sustainable investment laws .

Investor awareness and participation in regulatory changes.

Regular meeting between investors and policy markers.

Investor facilitation startup “ from red tape to red carpet “ and reducing of administrative burdens .

Page 10

10

Role Of Egyptian Government In Achieving

Transparency

Page 11

11

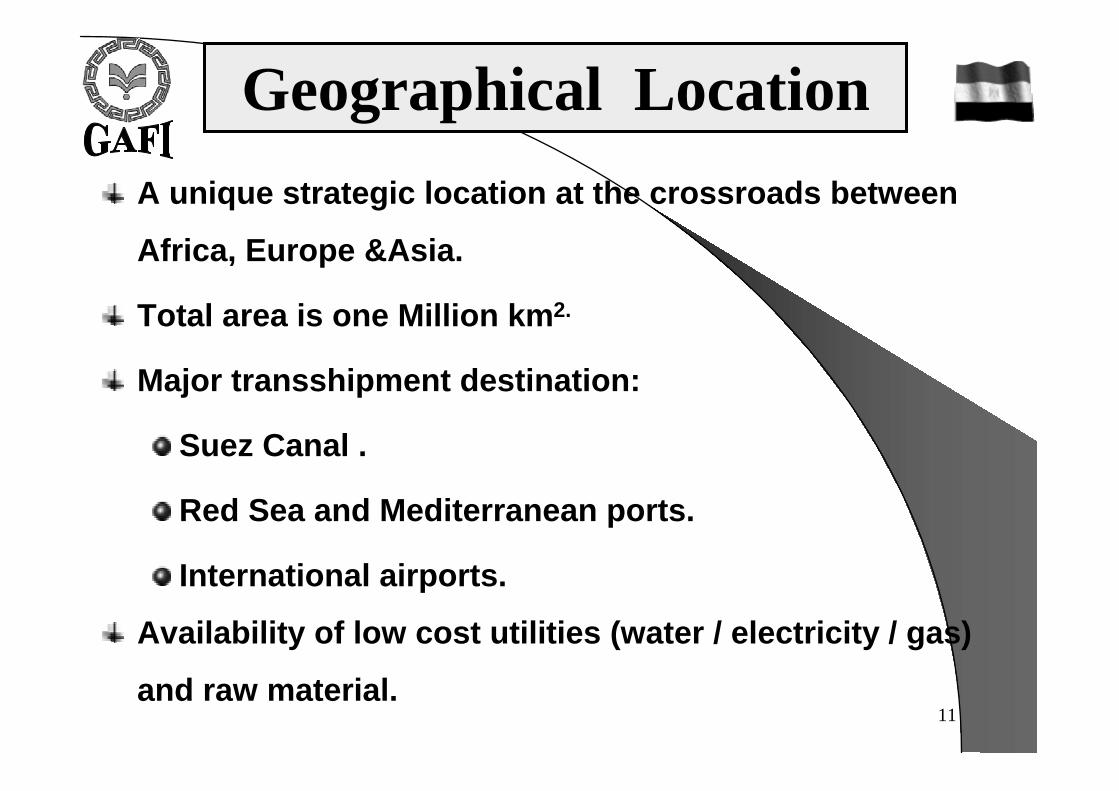

A unique strategic location at the crossroads between

Africa, Europe &Asia.

Total area is one Million km2.

Major transshipment destination:

Suez Canal .

Red Sea and Mediterranean ports.

International airports.

Availability of low cost utilities (water / electricity / gas)

and raw material.

Geographical Location

Page 12

12

Population 71.2 millions.

Population growth rate 2.1% ( 2001/ 2002).

Sustainable growth rates , 3.2% of GDP on Sustainable growth rates , 3.2% of GDP on

averageaverage..

EgyptEgypt’’s inflation has consistently declined to s inflation has consistently declined to

reach 2.4 %.reach 2.4 %.

Total foreign debt is $ 28.7 billion.Total foreign debt is $ 28.7 billion.

Demographic Data

Page 13

13

9.4

7.3

6.2

3.8 3.8

2.82.4 2.4

0

1

2

3

4

5

6

7

8

9

10

1995 1996 1997 1998 1999 2000 2001 2002

Inflation Rate in Egypt (%)

1995 - 2002

Political & Economic IndicatorsPolitical & Economic Indicators

1.92.5

3.94.7 4.9

5.35.7

6.3

3.63.2

0

1

2

3

4

5

6

7

8

9

10

%

1991/92 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99 2000/01 2001/02

Real GDP Growth Rate %

Source : Ministry of foreign Trade

Page 14

14

Political & Economic IndicatorsPolitical & Economic Indicators

Since January 29,2003 Egypt adopted Since January 29,2003 Egypt adopted

a a ““Free Float FX SystemFree Float FX System””..

Rates are to be determined by banks Rates are to be determined by banks

(55 banks).(55 banks).

Foreign Exchange SystemForeign Exchange System

Source : Central Bank Of Egypt

Page 15

15

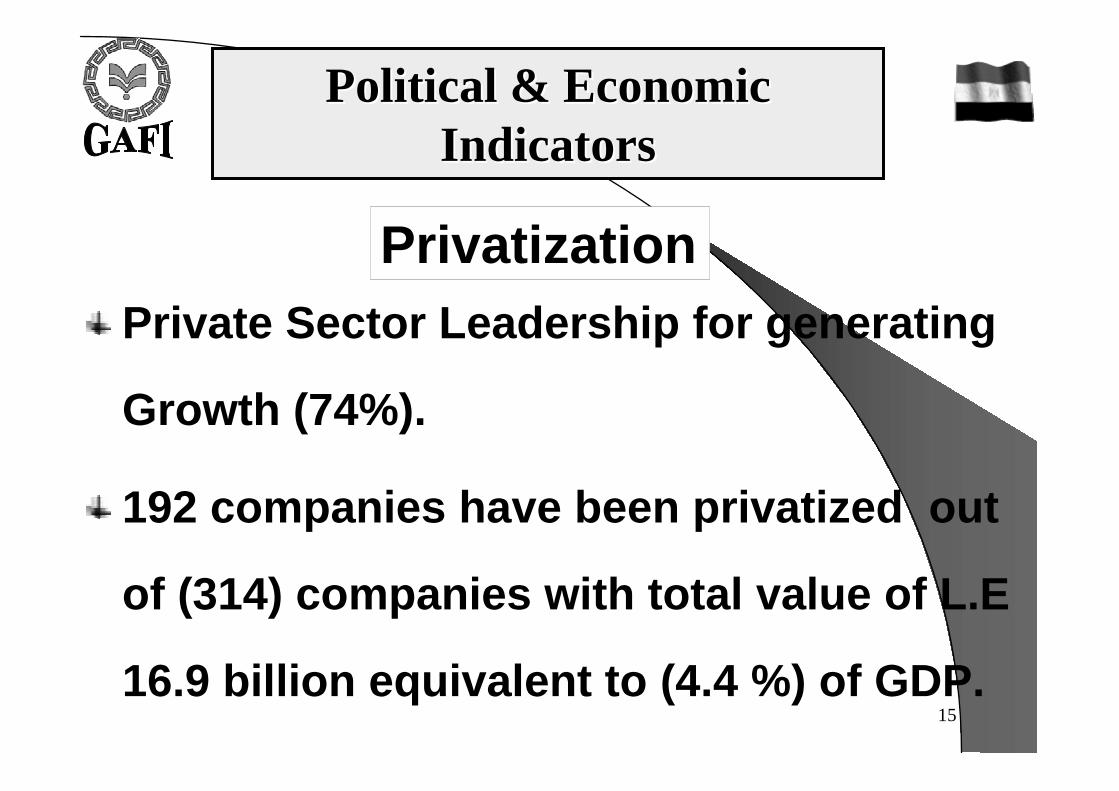

Private Sector Leadership for generating

Growth (74%).

192 companies have been privatized out

of (314) companies with total value of L.E

16.9 billion equivalent to (4.4 %) of GDP.

Political & Economic Political & Economic IndicatorsIndicators

Privatization

Page 16

16

Political & Economic IndicatorsPolitical & Economic Indicators

664

1215

2791

3396

2361

2785

2476

1126

920

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1994/95 1995/96 1996/97 1997/98 1998/99 1999/01 2000/01 2001/02 2002

Privatization Proceeds (L.E. Millions)1994- End June, 2002

Page 17

17

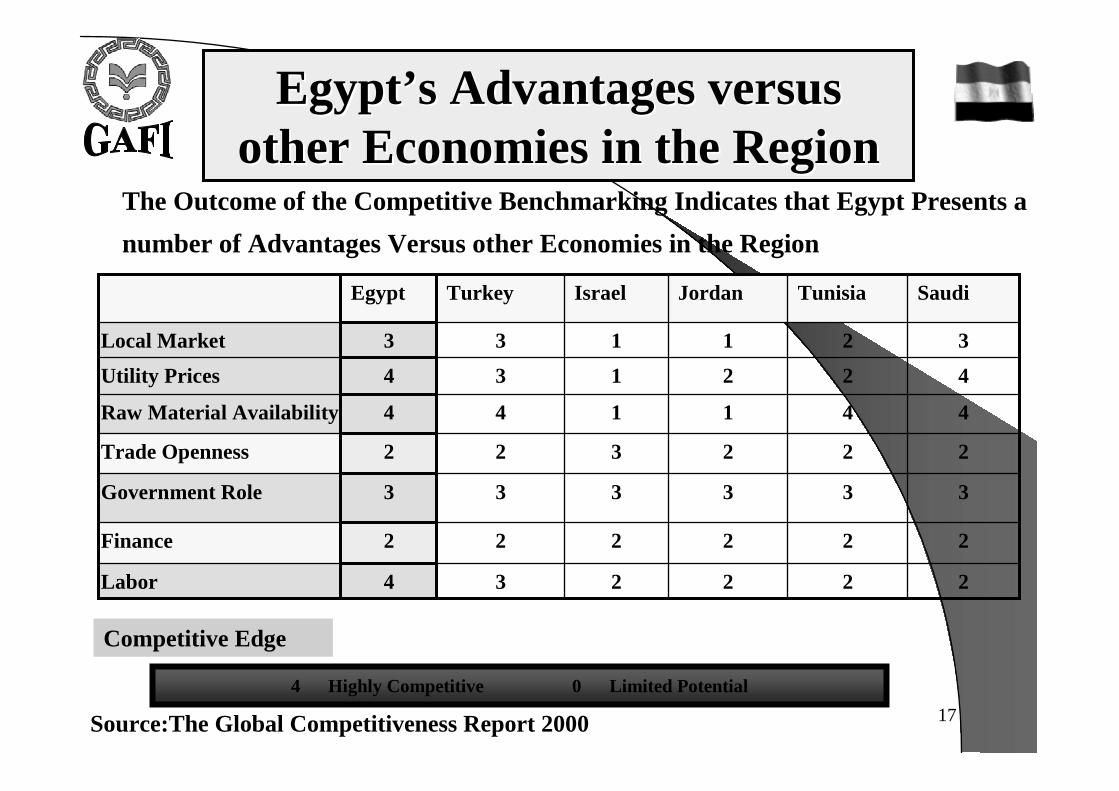

EgyptEgypt’’s Advantages versus s Advantages versus other Economies in the Regionother Economies in the Region

222234Labor

222222Finance

333333Government Role

222322Trade Openness

441144Raw Material Availability

422134Utility Prices

321133Local Market

SaudiTunisiaJordanIsraelTurkeyEgypt

4 Highly Competitive 0 Limited Potential

Competitive Edge

The Outcome of the Competitive Benchmarking Indicates that Egypt Presents a

number of Advantages Versus other Economies in the Region

Source:The Global Competitiveness Report 2000

Page 18

18

Government Economic Policy Government Economic Policy Independence RatingIndependence Rating

2.1

2.7

2.7

3

3.1

3.1

3.2

3.3

3.4

3.8

4.3

4.4

5.5

0 1 2 3 4 5 6

R u ssia

Isra e l

In d o n e sia

P h ilip p in e

In d ia

T u rke y

G re e c e

Ita ly

T h a ila n d

M a la ysia

E g yp t

Jo rd a n

S in g a p o re

Source: The Global Competitiveness ReportAverage Score ,From 0 to 6 Highest rank

90.4%

84.6%

57.6%

14.0%

9.0%

8.1%

6.6%

5.3%

4.7%

4.4%

2.4%

2.1%

0% 20% 40% 60% 80% 100%

R u ssia

T u rke y

In d o n e sia

In d ia

P h ilip p in e s

T h a ila n d

Isa re l

M a la ysia

G re e c e

Jo rd a n

E g yp t

Ita ly

S in g a p o re

Inflation PercentagesInflation Percentages

The Egyptian Government’s Economic Policies Are Well Perceived And Executed, As Evidenced By The Relatively Low Inflation Among Selected Economies

Page 19

19

Work force is 20 Million.

Number of universities is 18.

Ranking 17th worldwide in number of yearly graduates

270,000 high school graduates year 2002 .

248,451 colleague graduates year 2001.

Man PowerA country of 71.2 million people

Page 20

20

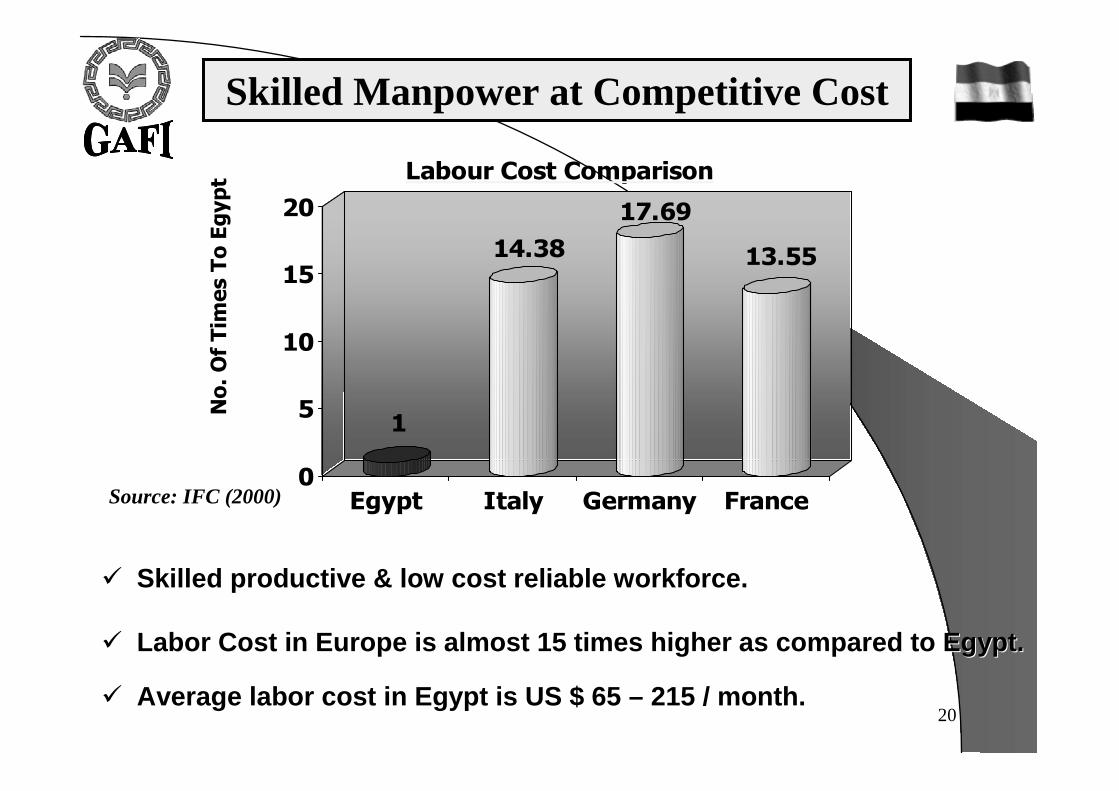

Skilled Manpower at Competitive Cost

Skilled productive & low cost reliable workforce.Skilled productive & low cost reliable workforce.

Labor Cost in Europe is almost 15 times higher as compared to EgLabor Cost in Europe is almost 15 times higher as compared to Egypt.ypt.

Average labor cost in Egypt is US $ 65 Average labor cost in Egypt is US $ 65 –– 215 / month.215 / month.

1

14.3817.69

13.55

0

5

10

15

20

Egypt Italy Germany France

Labour Cost Comparison

No.

Of

Tim

es T

o Eg

ypt

Source: IFC (2000)

Page 21

21

Trade AgreementsTrade Agreements

Egypt

World Trade Organization (WTO) Europe – Mediterranean

Partnership

Other Agreements

Greater Arab Free Trade Area (GAFTA)

Common Market forEastern and southern

Africa (COMESA)

Inhabitants 380 Million

Inhabitants 300 MillionInhabitants 728 Million

Trade & MarketsTrade & Markets

Local market 71.2 million consumer & Regional market 1.4 billionLocal market 71.2 million consumer & Regional market 1.4 billion consumer .consumer .

Page 22

22

General Authority for Investment and Free

Zones (GAFI) Sole governmental agency

responsible for investment affairs.

Private sector oriented organization.

Headed by board of directors formed by

members from governmental agencies and

private sector equally.

Reports directly to the Prime Minister.

Who we are ?Who we are ?

Page 23

23

GAFI’s Role

Encompasses delegates from different governmental agencies

dealing with investors.

Comprises Following Divisions.

A) The Advisory UnitFocuses on investor facilitation, business support service.

Respond to investor’s inquiries.

Optimize and streamline incorporation procedures.

Investment Facilitation Services offered to investor before, during &

after incorporation, such as :Providing needed data and information to investors.

Providing Utilities & Land prices.

Assist investors to select proper Locations for their projects.

Supply investors with Investment opportunities.

One Stop Shop

Page 24

24

B) The Current awareness unit:

Receiving documents related to the legal incorporations of

companies.

Act on behalf of investors to obtain company license .

Electronic registration of companies.

Registration approvals & licensing of companies.

Issue & Renew of Work Permits for foreigners.

Airport entry permits for company representatives.

GAFI’s Role

One Stop Shop

Page 25

25

A permanent ministerial committee for investment affairs has been

formed, presided by the deputy Prime Minister, competent

ministries and GAFI Chairman, so as to solve investment disputes

amicably outside court channels.

A minor permanent committee is also formed with Ministry of

finance to study and take action to solve Taxes & Custom problems

; ministerial committee will take the lead for unsolved cases.

Out of (274) case discuss during (15 ministerial meetings), (217)

have been solves and (14 ) decree became as general rule.

C) Disputes Settlements

GAFI’s RoleOne Stop Shop

Page 26

26

Setting laws and decrees , so as to improve investment environment

Outcome from investment disputes solved by Ministerial committee is used to amend laws.

Discussions of regulatory changes with investors in done before issuance of laws

New laws have been issued during 2002-2003 as follows :-

Intellectual property law

Mortgage Law

Banking Law

Labor law

Amendments of Laws

GAFI advice the government for investment regulatory changes in order to :

Antimony laundry Law

Export Development Law

Special Economic zones

law

Page 27

27

Other New Laws will be issued soon, which are

Custom Law

Tax Law

Addition of New chapter in investment law

to acquire GAFI’s decisions the power of the

law and to be final and binding for all

governmental agencies

Amendments of Laws

Page 28

28

GAFI’s role in proactive Investment Targeting

Prioritizing potential sectors for development.

Defining Egypt’s sector competitive location

Analyses potential markets, trade flow and FDI

flow affecting such sectors.

Performing assessment studies; SWOT analysis,

Bench Marking, competitiveness for sectors and

regions targeted for development, in order to issue

vision strategies& policies

Page 29

29

GAFI’s role in proactive Investment Targeting

Compile the output of such studies in a proactive

promotion plan.

Formation of Joints desk with foreign Embassies

at Egypt to solve any problems facing foreign

investors, As well as, coordinating for business

affairs, Visits, Forums, according to agreed up

annual plans

Page 30

30

MIGA – FIAS - UNCTAD - OECD Future Cooperation Program

with Egypt

Page 31

31

Development and implementation :

Investment Promotion Strategy

promotional materials

Information & CRM systems program

Sector Targeting Program

Market Intelligence Program

National & International Public Relations and Communications

Campaign

Cooperation with international organization MIGA, FIAS, UNCTAD &

OECD

MIGA Program

Page 32

32

International Country Branding Campaign

Policy Advocacy Program

Investor Facilitation & Servicing Program

Investor Aftercare Program

General Monitoring and Evaluation Program

Human Resources and Staffing Program

Monitoring and Project Supervision Program

Cooperation with international organization MIGA, FIAS, UNCTAD &

OECD

MIGA Program

Page 33

33

FIAS ProgramInvestment & Business environment improvement program

Diagnostic review of the Direct Investment & Business Environment

in Egypt

Administrative Barriers to Investment

Assistance Program for the Implementation of the finding of the

Administrative Barriers to Investment

Competition Policy Environment for FDI

Promoting the Development of Companies in selected sectors

through FDI spillovers

Cooperation with international organization MIGA, FIAS, UNCTAD &

OECD

Page 34

34

Cooperation with international organization MIGA, FIAS, UNCTAD &

OECD

UNCTAD Review of the Investment Environment

Both studies were to be published internationally

OECD Review of the Investment Environment

Page 35

35

General Authority For General Authority For Investment and Free ZonesInvestment and Free Zones

30, 30, SheriefSherief St. Down Town, CairoSt. Down Town, Cairo

Tel: 3938759 Tel: 3938759 –– Fax :3933799Fax :3933799

Email : Email : [email protected] @maktoob.com

Web Site : Web Site : www.gafinetwww.gafinet.org.org