Page 1

Public Sector Audit Committee: Assessment of Finance Function

The information contained in this guidance paper is provided for discussion purposes. As such, it is intended to provide the reader and the entity with general information of interest and not to address the circumstances of any particular individual or entity.

The information should not be regarded as professional or legal advice or the official opinion of any of the individual organisations represented on the steering committee of the Public Sector Audit Committee Forum (PSACF).

Although the PSACF takes all reasonable steps to ensure the quality and accuracy of the information, no action should be taken on the strength of the information without obtaining professional advice. The PSACF and the sponsors shall not be liable for any damage, loss or liability of any nature incurred directly or indirectly by whomever and resulting from any cause in connection with the information contained herein.

Page 2

2

Content

1. Purpose of the paper . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 2. WhyshouldtheAuditCommitteeassessthefinancefunction? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 3. WhenshouldtheAuditCommitteeassessthefinancefunction? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 4. HowshouldtheAuditCommitteeassessthefinancefunction? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 5. WhatshouldtheAuditCommitteedoifitisnotsatisfiedwiththecompetenceofthefinancefunction? . . . . . . . . . . . . . 3

Annexure A–Assessmenttemplate/Guidelinestoconsider . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Annexure B–LocalGovernmentlegislation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Annexure C–NationalandProvincialGovernmentlegislation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1. Purpose of the paper

ThepurposeofthispaperistoprovidePublicSectorAuditCommitteeswithguidanceonassessingthefinancefunction.

2.WhyshouldtheAuditCommitteeassessthefinancefunction?

Themanagementoffinanceiscriticalinthepublicsector,aspublicsectorentitiesarefundedbypublicfundstobeusedforaspecificmandate. Infact,themainpurposeofboththePFMA(PublicFinanceManagementAct)andMFMA(MunicipalFinanceManagementAct)istoregulatefinancialmanagementwithinpublicsectorentities.Inthepublicsector,thefinancefunctioniscriticalasanassuranceprovidertotheAuditCommitteeontheeffectivenessoffinancialreporting,aswellasitslinktoservicedeliveryasdisplayedinperformanceinformation.

Thefinancialmanagementofapublicsectorentityistypicallyexecutedbythefollowingmembersofmanagement1:theChiefFinancialOfficer(CFO),FinanceManagers,AccountingOfficersoranyotherseniorfinancialofficials.BoththePFMAandtheMFMAemphasisetheimportantroleoftheCFOinensuringtheproperfinancialmanagementofthepublicsectorentity.(RefertoAppendixBandCforextractsoftherelevantlegislationinthisregard.)

TheAuditCommitteeassessmentofthefinancefunctionisnotaspecificrequirementofthePFMAorMFMA.However,sincethedutiesoftheAuditCommitteelargelyincludeoversightoverthefinancialaffairsofthepublicsectorentity,itisimplied that Audit Committees should satisfy themselvesofthecompetenceoftheindividualsinvolvedinthefinancefunctioninordertoplacerelianceontheinformationobtainedfromthem.

Asamatterofbestpractice,publicsectorentitiesshouldalsoapplyKingIII,whichrecommendsinChapter3,Principle3that:“Theauditcommitteeshouldsatisfyitselfoftheexpertise,resourcesandexperienceofthecompany’sfinancefunction.Everyyear,theauditcommitteeshouldconsiderandsatisfyitselfoftheappropriatenessoftheexpertiseandadequacyofresourcesofthefinancefunctionandexperienceoftheseniormembersofmanagementresponsibleforthefinancialfunction…”

Inaddition to this, theRegulations to theMFMAimposeminimumcompetency levels forAccountingOfficers,ChiefFinancialOfficers, seniormanagers,otherfinancialofficersaswellassupplychainmanagementofficials.ThishasanimpliedlinktotheAuditCommitteeperforminganassessmentandsatisfyingitselfastothecompetenceofthefinancefunction,aspartofitsMFMAcompliance.(RefertoAnnexureBforextractsoftherelevantlegislation.)

TheAuditCommitteeshouldincludebriefcommentaryontheeffectivenessofthefinancefunctioninitsAuditCommitteeReport,whichisincludedintheAnnualReport.

1seealsoPSACFpaperon“TherelationshipbetweenthepublicsectorAuditCommitteeandManagement”

For Local Government, in terms of the MFMA, an Audit Committee must advise on matters relating to, amongst others, accounting policies, theadequacy,reliabilityandaccuracyoffinancialreporting,aswell asreviewtheannualfinancialstatementstoprovidewithanauthoritativeand credible view of the financial position of the municipality ormunicipal entity.

For National and Provincial Government, in terms of the Treasury Regulations to the PFMA, the Audit Committee must, amongst others, reviewtheadequacy,reliabilityandaccuracyofthefinancialinformationprovided to management and other users of such information.

Page 3

3

3.WhenshouldtheAuditCommitteeassessthefinancefunction?

Followingeachfinancialyear-end,theAuditCommitteeshouldperformanin-depthassessmentofthefinancefunction,asdescribedbelow.

Additionalassessmentscouldbeperformedinbetweenthese,asandwhentheAuditCommitteeconsidersitnecessary.Thismayinclude,forexample,wheretherehasbeenasignificantchangeinthestaffingwithinthefinancefunctionorwherethepublicsectorentity2isgoingthroughaspecificfinancialcrisis.

4.HowshouldtheAuditCommitteeassessthefinancefunction?

ThisassessmentcouldbeperformedviaquestionnairesbeingcompletedbyeachAuditCommitteemember,thesignificantresultsofwhichshouldbesummarisedanddiscussedatthefollowingAuditCommitteemeeting.

AnexampleofaquestionnaireisprovidedinAnnexureAtothispaper.Thisexampleisnotintendedasdefinitive,andshouldratherbeusedasaguidelineofthetypesofaspectstoconsider.Itshouldbetailoredaccordinglytomeettheneedsofeachspecificpublicsectorentity.

Alternatively,shouldthepre-completionofaquestionnairenotbefeasible,anin-depthdiscussioncouldtakeplaceatanAuditCommitteemeeting,coveringsimilarpointstowhatwouldhavebeencoveredinthequestionnaire.

Havingassessedthefinancefunctionandarrivedatitsconclusion,theAuditCommitteeshouldusethisoutcometoinfluenceitsopinionontheeffectivenessoffinancialreportingandfinancialcontrols.Thisshouldbecorroboratedbytheworkandopinionoftheinternalauditfunction.

5.WhatshouldtheAuditCommitteedoifitisnotsatisfiedwiththecompetenceofthefinancefunction?

Following this assessment, should theAuditCommittee feel that thefinance function isnot competent toeffectively fulfill itsduties, theAuditCommittee should:

• Identifytherootcauseoftheproblemi.e.recruitmentshortfall/controlenvironment/organisationalculture;• Informtheaccountingofficerand/oraccountingauthority;• Recommendtraining/coachingfortherelevantmembersofthefinancefunctioninordertobringthemuptothestandardrequired;• Ensurethatthefindingsarefedintotherelevantindividuals’performanceappraisalprocess,tobeactionedandimprovedupon.

2Inthispaper,“publicsectorentities”shouldbereadtoincludecompanies(forstate-ownedcompaniesandmunicipalentities),othernationalandprovincialentitiesandmunicipalities.

Page 4

4

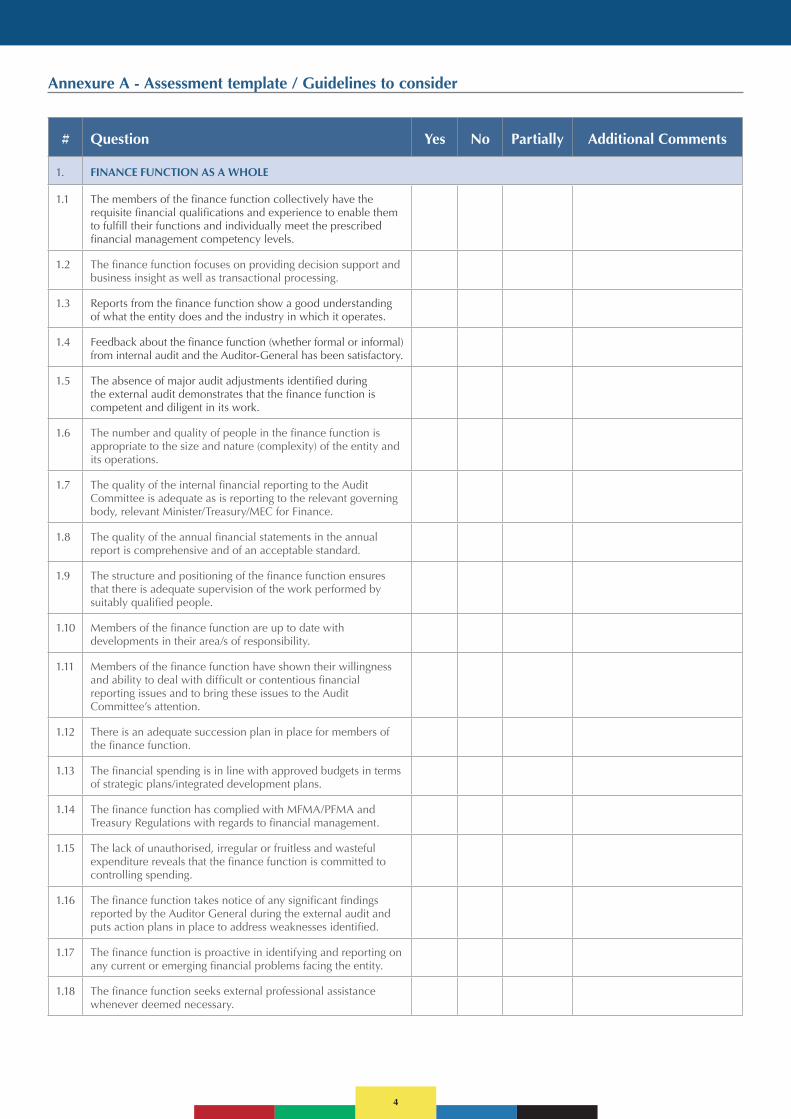

Annexure A - Assessment template / Guidelines to consider

# Question Yes No Partially Additional Comments

1. FINANCE FUNCTION AS A WHOLE

1.1 Themembersofthefinancefunctioncollectivelyhavetherequisitefinancialqualificationsandexperiencetoenablethemtofulfilltheirfunctionsandindividuallymeettheprescribedfinancialmanagementcompetencylevels.

1.2 Thefinancefunctionfocusesonprovidingdecisionsupportandbusinessinsightaswellastransactionalprocessing.

1.3 Reportsfromthefinancefunctionshowagoodunderstandingofwhattheentitydoesandtheindustryinwhichitoperates.

1.4 Feedbackaboutthefinancefunction(whetherformalorinformal)frominternalauditandtheAuditor-Generalhasbeensatisfactory.

1.5 Theabsenceofmajorauditadjustmentsidentifiedduringtheexternalauditdemonstratesthatthefinancefunctioniscompetentanddiligentinitswork.

1.6 Thenumberandqualityofpeopleinthefinancefunctionisappropriatetothesizeandnature(complexity)oftheentityanditsoperations.

1.7 ThequalityoftheinternalfinancialreportingtotheAuditCommitteeisadequateasisreportingtotherelevantgoverningbody,relevantMinister/Treasury/MECforFinance.

1.8 Thequalityoftheannualfinancialstatementsintheannualreportiscomprehensiveandofanacceptablestandard.

1.9 Thestructureandpositioningofthefinancefunctionensuresthatthereisadequatesupervisionoftheworkperformedbysuitablyqualifiedpeople.

1.10 Membersofthefinancefunctionareuptodatewithdevelopmentsintheirarea/sofresponsibility.

1.11 MembersofthefinancefunctionhaveshowntheirwillingnessandabilitytodealwithdifficultorcontentiousfinancialreportingissuesandtobringtheseissuestotheAuditCommittee’sattention.

1.12 Thereisanadequatesuccessionplaninplaceformembersofthefinancefunction.

1.13 Thefinancialspendingisinlinewithapprovedbudgetsintermsofstrategicplans/integrateddevelopmentplans.

1.14 ThefinancefunctionhascompliedwithMFMA/PFMAandTreasuryRegulationswithregardstofinancialmanagement.

1.15 Thelackofunauthorised,irregularorfruitlessandwastefulexpenditurerevealsthatthefinancefunctioniscommittedtocontrollingspending.

1.16 ThefinancefunctiontakesnoticeofanysignificantfindingsreportedbytheAuditorGeneralduringtheexternalauditandputsactionplansinplacetoaddressweaknessesidentified.

1.17 Thefinancefunctionisproactiveinidentifyingandreportingonanycurrentoremergingfinancialproblemsfacingtheentity.

1.18 Thefinancefunctionseeksexternalprofessionalassistancewheneverdeemednecessary.

Page 5

5

# Question Yes No Partially Additional Comments

2. CFO

2.1 TheCFOhasagoodworkingrelationshipwithmembersoftheAuditCommittee/EXCO/relevantgoverningbody.

2.2 TheCFOprovidesleadershiptotheentirefinancefunction:

•Demonstratingadherencetoentityvalues;•Providingstrategicinsight,and•Coachingsubordinatesasappropriate.

2.3 TheCFOhasadequateknowledge,technicalcompetenceandexperiencetoenablehim/hertofulfilltherole.

2.4 TheCFOaddressesproblemsandidentifiesandimplementsappropriatesolutionsquickly.

2.5 TheCFOviewsthebusinessissuesthroughanowner’slensandownstheresults.

2.6 TheCFOdrivesthediscussionofcriticalissuesbeyondtheprescribedregulatoryrequirements.

2.7 TheCFOhasagoodunderstandingofthebusinessand itsoperations.

2.8 TheCFO’spreparationforAuditCommitteemeetingsisgood.

2.9 TheCFOissufficientlyavailableforconsultationoutsideofAuditCommitteemeetings.

2.10 TheCFOadequatelybriefsthechairmanoftheAuditCommitteeonsignificantfindingsordevelopmentspriortoAuditCommitteemeetings.

2.11 TheCFOhasagoodworkingrelationshipwiththeCEO.

2.12 TheCFOunderstandstheneedsandexpectationsoftheAudit Committee.

2.13 TheCFOisproactiveinraisingissueswiththeAuditCommittee.

2.14 TheCFOparticipatesasasignificantcontributortotheCombinedAssuranceFramework.

2.15 TheCFOisuptodatewithfinancialandindustrydevelopments.

2.16 TheCFOfulfilshis/herlegislatedduties.

2.17 TheCFOensurestheprofessionaldevelopmentandtrainingofhis/hersupportstaff.

2.18 TheCFOhasdocumentedallthematerialpolicies,processesandprocedureswithinthefinancefunction.

3Inthispaper,thetermrelevantgoverningbodyshouldbereadtoincludeBoard,AccountingAuthorityorCouncilasapplicabletotherelevantpublicsectorentity.

Page 6

6

Annexure B – Local Government legislation

Relevant extracts from MFMA:

81.Roleofchieffinancialofficer

(1)Thechieffinancialofficerofamunicipality— (a)isadministrativelyinchargeofthebudgetandtreasuryoffice; (b)mustadvisetheaccountingofficerontheexerciseofpowersanddutiesassignedtotheaccountingofficerintermsofthisAct; (c)mustassisttheaccountingofficerintheadministrationofthemunicipality’sbankaccountsandinthepreparationandimplementationofthe municipality’sbudget; (d)mustadviseseniormanagersandotherseniorofficialsintheexerciseofpowersanddutiesassignedtothemintermsofsection78ordelegated tothemintermsofsection79;and (e)mustperformsuchbudgeting,accounting,analysis,financialreporting,cashmanagement,debtmanagement,supplychainmanagement, financialmanagement,reviewandotherdutiesasmayintermsofsection79bedelegatedbytheaccountingofficertothechieffinancialofficer.

(2)Thechieffinancialofficerofamunicipalityisaccountabletotheaccountingofficerfortheperformanceofthedutiesreferredtoinsubsection(1).

82. Delegations

(1)Thechieffinancialofficerofamunicipalitymaysub-delegateanyofthedutiesreferredtoinsection81(1)(b),(d)and(e)— (a)toanofficialinthebudgetandtreasuryoffice; (b)totheholderofaspecificpostinthatoffice;or (c)withtheconcurrenceoftheaccountingofficer,to— (i)anyotherofficialofthemunicipality;or (ii)anypersoncontractedbythemunicipalityfortheworkoftheoffice.

(2)Ifthechieffinancialofficersub-delegatesanydutiesintermsofsubsection(1)toapersonwhoisnotanemployeeofthemunicipality,thechief financialofficermustbesatisfiedthateffectivesystemsandproceduresareinplacetoensurecontrolandaccountability.

(3)Asub-delegationintermsofsubsection(1)— (a)mustbeinwriting; (b)issubjecttosuchlimitationsorconditionsasthechieffinancialofficermayimpose;and (c)doesnotdivestthechieffinancialofficeroftheresponsibilityconcerningthedelegatedduty.

(4)Thechieffinancialofficermayconfirm,varyorrevokeanydecisiontakeninconsequenceofasub-delegationintermsofsubsection(1),butno suchvariationorrevocationofadecisionmaydetractfromanyrightsthatmayhaveaccruedasaresultofthedecision.

83.Competencylevelsofprofessionalfinancialofficials

(1)Theaccountingofficer, seniormanagers, thechieffinancialofficerandotherfinancialofficialsofamunicipalitymustmeet theprescribed financialmanagementcompetencylevels.

(2)Amunicipalitymustforthepurposesofsubsection(1)provideresourcesoropportunitiesforthetrainingofofficialsreferredtointhatsubsection tomeettheprescribedcompetencylevels.

(3)TheNationalTreasuryoraprovincialtreasurymayassistmunicipalitiesinthetrainingofofficialsreferredtoinsubsection(1).

Theabovementionedminimumcompetencylevelsareprescribedinregulation493totheMFMA.ThefullRegulationcanbeviewedonthislink:http://mfma.treasury.gov.za/MFMA/Regulations%20and%20Gazettes/Municipal%20Regulations%20and%20Guidelines%20on%20Minimum%20Competency%20Levels%20-%20Gazette%20No%2029967,%2015%20June%202007/Municipal%20Regulations%20on%20Minimum%20Competency%20Levels%20-%20Gazette%20No%2029967.pdf

Page 7

7

Annexure C – National and Provincial Government legislation

Relevant extracts from PFMA Treasury Regulations:

2.1Chieffinancialofficer

2.1.1 Unlessdirectedotherwisebytherelevanttreasury,eachinstitutionmusthaveachieffinancialofficerservingontheseniormanagementteam.

2.1.2Thechieffinancialofficerisdirectlyaccountabletotheaccountingofficer.

2.1.3Withoutlimitingtherightoftheaccountingofficertoassignspecificresponsibilities,thegeneralresponsibilityofthechieffinancialofficer istoassisttheaccountingofficerindischargingthedutiesprescribedinPart2ofChapter5ofthePFMAandtheannualDivisionofRevenue Act(DORA).Thesedutiesrelatetotheeffectivefinancialmanagementoftheinstitutionincludingtheexerciseofsoundbudgetingand budgetarycontrolpractices;theoperationofinternalcontrolsandthetimelyproductionoffinancialreports.

FurtherspecificinformationontheroleanddutiesoftheChiefFinancialOfficerandtheAccountingOfficer,refertothePFMA(http://www.treasury.gov.za/legislation/pfma/), DORA (http://www.treasury.gov.za/legislation/acts/2013/Division%20of%20Revenue%20Act,%202013%20(Act%20No.% 202%20of%202013).pdf ) aswellastheTreasuryRegulationstoPFMA(http://www.treasury.gov.za/legislation/pfma/regulations/gazette_27388.pdf)

Page 8

Institute of Directors in Southern AfricaPSACF Secretariat

NationalOffice-Johannesburg|POBox908,Parklands2121|Johannesburg,SouthAfrica

144KatherineStreet,Sandown,Sandton2196

Tel:0114309900|Fax:0114447907|Email:[email protected] |Web:www.IoDSA.co.za