36

Public TeliaSonera International Carrier Daniel Sjoberg, Reykjavik, August 25th Bringing knowledge, quality and stability to the communications industry

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | cleopatra-bond |

| View: | 215 times |

| Download: | 0 times |

Public

TeliaSonera International CarrierDaniel Sjoberg, Reykjavik, August 25th

Bringing knowledge, quality and stability to the communications industry

Public

“Outlining requirements for new network services and examining how the optical core can be cost effectively upgraded to support them"

Daniel SjobergHead of Technology

TeliaSonera International Carrier

3

?

4

Requirements

More Capacity & Cheaper

How the optical core can be cost effectively upgraded?

Lower Price from Vendors

5

Outline

• Current drivers for international Capacity

• Future Requirements

• Cost Drivers For International Carriers– Comparison between IP and DWDM

• Conclusions

6

TeliaSonera International Carrier

Target

To be one of the top three profitable carriers in the wholesale

segment in Europe.

Business scope

Focus on offering wholesale capacity and IP services to network and

service providers over the wholly-owned European and the trans-Atlantic

networks. TeliaSonera IC will also run its own IP network and maintain

and operate its peering points and relationships in Europe and in the US.

The international voice business will at the same time be focused to

international interconnect agreements and bilateral routes.

Public

Current drivers for international Capacity

8

TSIC Infrastructure

• X ducts

• 96 Fiber pares

• One fiber pare lit and used for

– DWDM

– IP

– SDH

– Voice

• IP & Voice is “buying” wavelengths at Market price

• Voice is buying IP and SDH at Market price

• This enable us to create Business Case for all PoP’s and services

DWDM

SDHIP

VOICE

9

TSIC Business Logic

Consumers Corporate

Service Providers

TSIC

For TSIC to understand future service requirements, we need to understand end customer markets.

10

General Business Comments

• IP has higher Margin per MBPS then SDH & DWDM

• SDH & DWDM gets Profitable with Volume alone

• IP price should be “lower” per MBPS then long haul SDH & DWDM price

• IP gets Profitable with Volume and tight Cost control

43%

22%

35%

Fixed Cost

Variable Cost

Depriciation

89%

6% 5%

Fixed Cost

Variable Cost

Depriciation

IP DWDM

11

Drivers For International Capacity• IP

– Main driver for International Capacity either through IP Transit or building own Backbones for IP

• Fixed Voice– Most Voice Network already in place. Might be incentive to replace

bilateral with cheaper leased lines

• Private Line & VPN– Legacy VPN network might upgrade but highest growth will be in IP

VPN.

– In Markets with cheap capacity SDH will still be alternative to VPN’S

• Mobile– Little demand today for International Capacity, will change with

increasing data usage

– Consolidation and price pressure might drive need

12

Drivers for International Capacity

Capacity

Time

Best Effort IP

IP VPNMobileFixed Voice

Private Line & VPN

13

Wholesale Buying behavior

• IP

– Still same old IP Transit

– Bundle solutions with MPLS

• SDH

– In Western Europe mainly smaller ISP

– Still growing in Eastern Europe

– Price and Growth decrease due to Ethernet

• DWDM

– Buying Circuits not Networks

– Still volume growth but also price erosion

Public

New Requirements & Future Network Services

15

“People tend to overestimate what can be done in one year

and underestimate what can be done in five or ten years.”

16

What will drive new requirements?

• Broadband– Peer to Peer dominating

– Today not quality minded

• Media– Using legacy systems

– Will migrate but are very quality minded

• VPN– Traffic growing due to change is behavior that might be enable

through cheap capacity

• Mobile– Still for closed Networks

– Internet vs Mobile Networks, the next big battle

17

Capacity pricing

• Cost Broadband Service

• 70 % of the cost are fixed including last mile & Equipment

• 30% is traffic related

• This will drive pricing down for International Capacity

• Gives opportunity for new International services

Fixed Cost(Last Mile

&Dslam)

IP Traffic

Margin

30 %

70 %

18

Capacity Alternatives

SDH/SONET

DWDM/WDM

EthernetCA

RR

IER

S By far the dominating solution

Few large customer, mainly carriers

Flexible Solution for Corporate customers, Service Providers and………. Carriers

ATM

IPSE

RV

ICE

P

RO

VID

ER

S

Ethernet

Might over time be replaced by new technology

Service platform for the future

Flexible Solution for Corporate customers

19

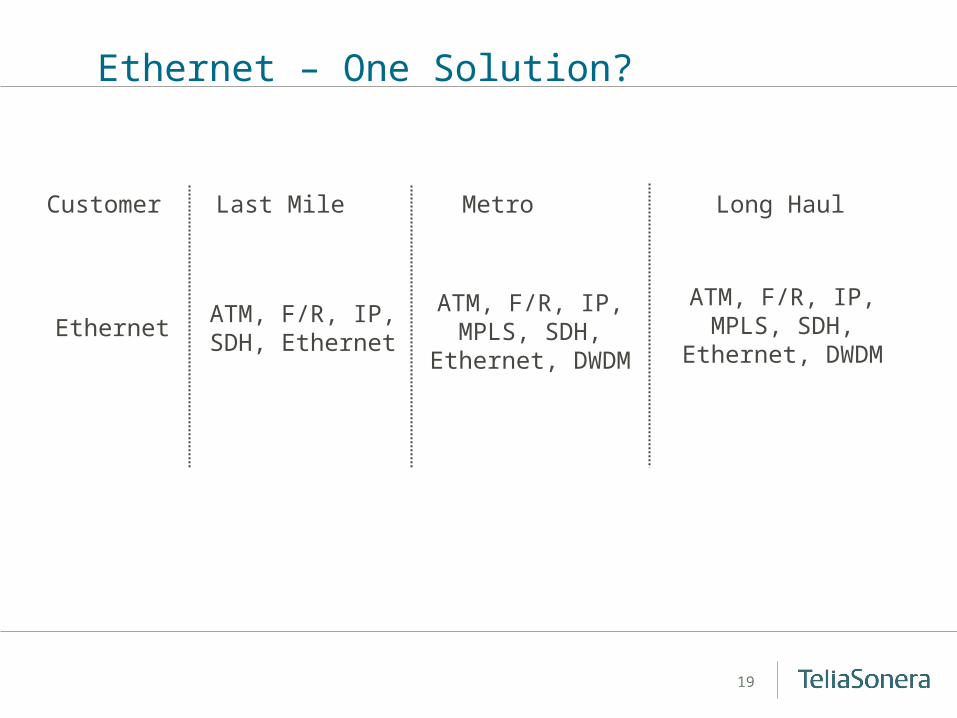

Ethernet – One Solution?

EthernetATM, F/R, IP, SDH,

Ethernet

ATM, F/R, IP, MPLS, SDH,

Ethernet, DWDM

Customer Last Mile Metro Long Haul

ATM, F/R, IP, MPLS, SDH,

Ethernet, DWDM

20

When Technology shift?

Road to IP VPN

Private Networks

Public Networks

X.25ISDN

PrivateLines

Public Internet

F/R and ATM

IP VPN

PSTN

Ovum 2001

Lessons on Migration

New service have only triggered large scale migration when two conditions are met New service must offer substantial cost savings for existing applications Match or exceed the quality and reliability

21

Traffic Mix TeliaNet 1997 - 2002

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1997 1998 1999 2000 2001 2002

Europe

US

Sweden

22

Transatlantic Traffic Pattern

OLD

NEW

23

Investing at the right time

• 60 – 80 % of Cost for IP is OPEX

• Of those more then 50% fixed

• 20 – 40 % % is depreciation

• Depreciation cost goes up

– with 20 % if customer is delayed with 6 month

– with 50 % if the delay is 12 month

• For IP investment timing is everything to maintain Product profitability

24

Future IP Concept – IP like Voice?

Global Routes

Glo

bal R

ou

tes

Global Routes

Glo

bal

Ro

ute

s European Routes

Customer Routes

BroadbandRoutes

US PeersRoutes

Back Up ConnectServer Colocation

IP Transit IP Connect

How will this impact the optical Network planning?

25

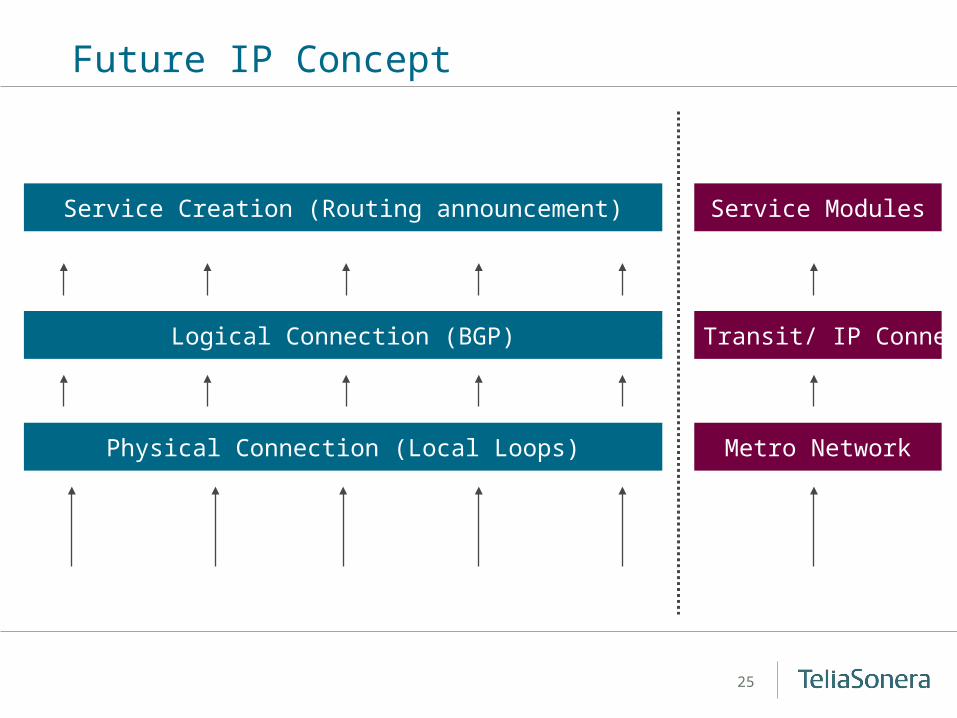

Future IP Concept

Physical Connection (Local Loops)

Logical Connection (BGP)

Service Creation (Routing announcement) Service Modules

IP Transit/ IP Connect

Metro Network

26

Next coming Years

• SDH Customer will migrate towards DWDM and Ethernet bringing requirements from current SDH service

• 40 G will make sense on certain stretches for IP Backbones

• 10 G Ethernet will be used as Backbone links

• Not likely that routers will use GMPLS to provision capacity

• GMPLS will be use to improve OPEX

27

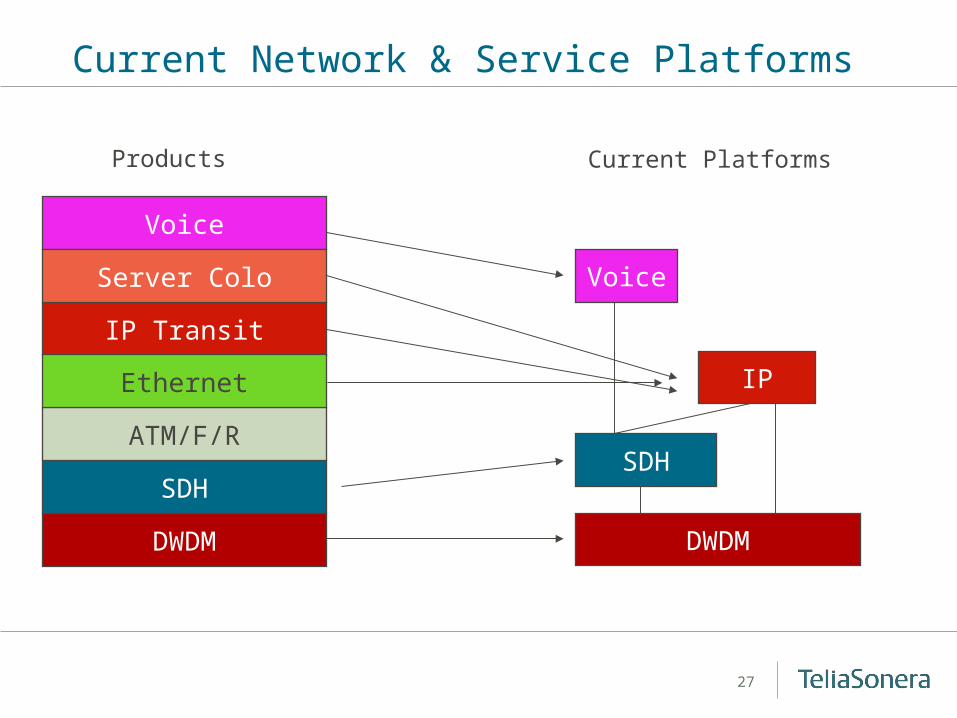

Current Network & Service Platforms

IP Transit

SDH

DWDM

Voice

ATM/F/R

Ethernet

Products Current Platforms

IP

SDH

DWDM

VoiceServer Colo

28

Capacity Grooming?

UNITEUNITEUNITEUNITEUNITEDXC 4/4

2.5 G622 Mbps155 mbps XtremeXtreme

DWDM

10 G

Use DXC 4/4- muxing, - grooming, - protection / restoration - and fast provisioning

Connecting 10 G directly to DWDM equipment because of no grooming possibilities

29

Current Network & Service Platforms

IP Transit

SDH

DWDM

Voice

ATM/F/R

Ethernet

Products New Platforms

IP

SDH/DWDM

VoiceServer Colo

Will this save money for Carriers?

10 G Ethernet?GMPLS ?

Public

Network Cost

31

TS IC Cost Allocation Project

• TSIC initiated Cost allocation project late 2002

• Purpose was to allocated all company cost onto Product Platform

• Based on allocation create Long Term P&L based on growth Scenarios

• Used it as base for Network & Product Strategy

32

Cost for upgrading

Time

Cost

?

• Current operation, investing based on customer, will short term be effective on Corporate Cash Flow• Change in technology might long term give lower production cost• Very difficult to say what to recommend

33

DWDM Cost

34

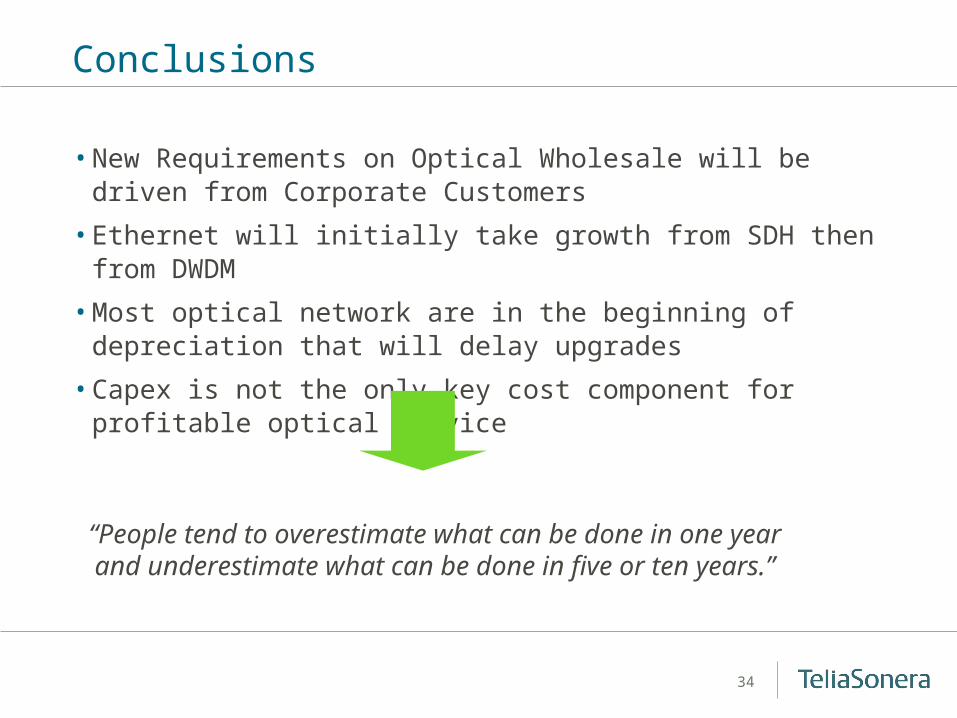

Conclusions

• New Requirements on Optical Wholesale will be driven from Corporate Customers

• Ethernet will initially take growth from SDH then from DWDM

• Most optical network are in the beginning of depreciation that will delay upgrades

• Capex is not the only key cost component for profitable optical service

“People tend to overestimate what can be done in one yearand underestimate what can be done in five or ten years.”

Public

The Nordic and Baltic telecommunications leader