20

Purchasers’ Path to Promoting Higher Value in Health Care Peter V. Lee Pacific Business Group on Health Citizens’ Health Care Working Group – Salt Lake City, Utah July 22, 2005

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | allan-dawson |

| View: | 220 times |

| Download: | 0 times |

Purchasers’ Path to Promoting Higher Value in Health Care

Peter V. LeePacific Business Group on Health

Citizens’ Health Care Working Group – Salt Lake City, UtahJuly 22, 2005

2

Pacific Business Group on Health: Mission and Priorities

Quality Measurement and Improvement

Value PurchasingConsumer Engagement

Mission: To improve the quality and availability of health care while moderating costs.

3

Pacific Business Group on Health Members

4

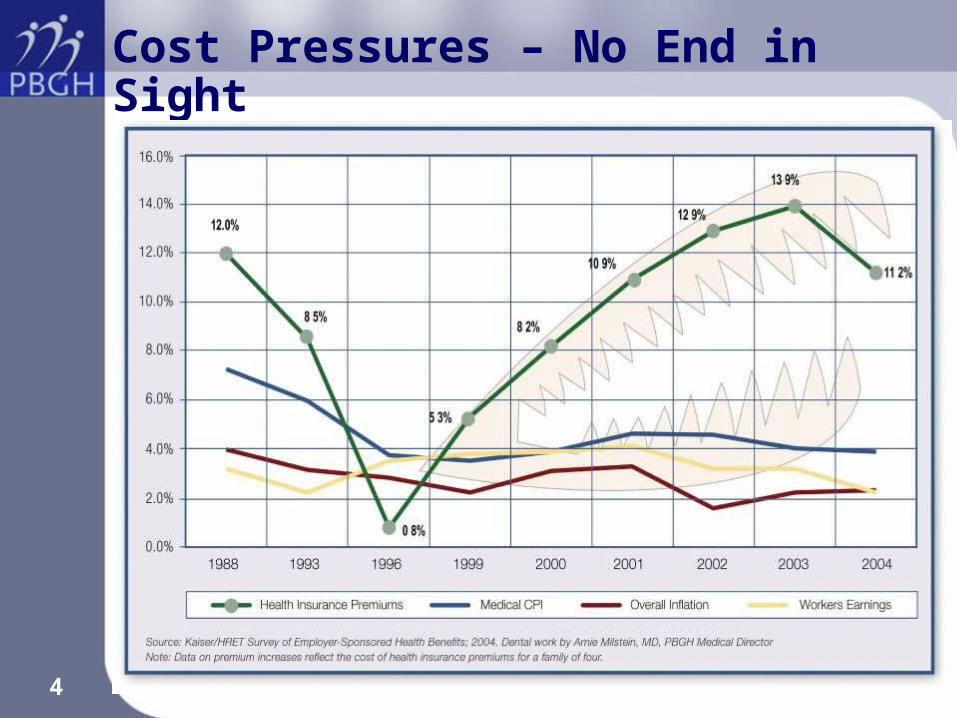

Cost Pressures – No End in Sight

5

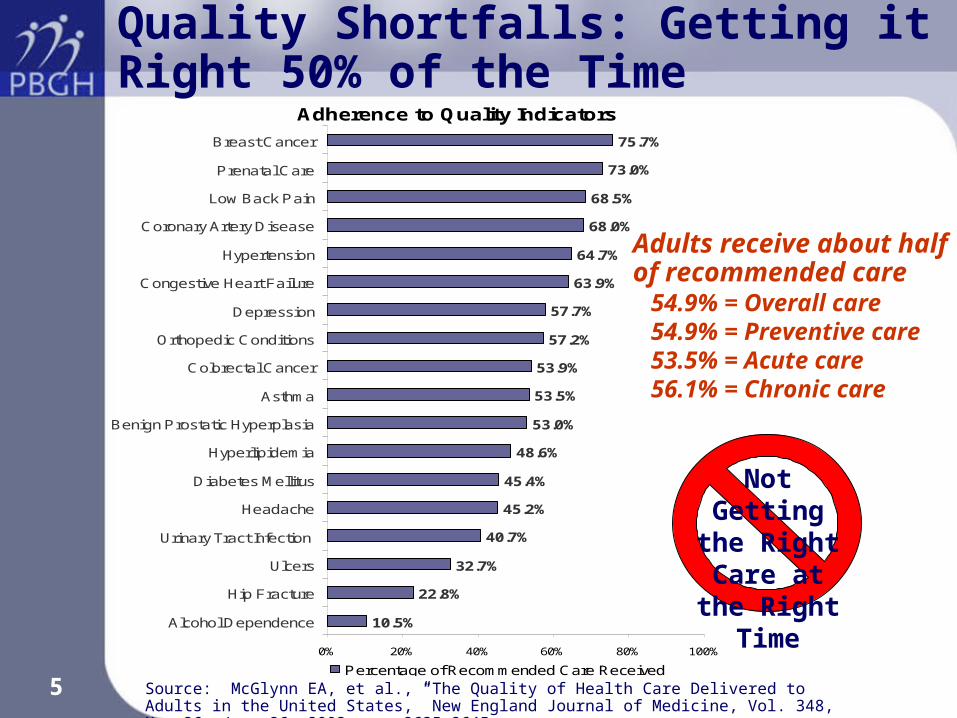

Adherence to Quality Indicators

10.5%

22.8%

32.7%

40.7%

45.2%

45.4%

48.6%

53.0%

53.5%

53.9%

57.2%

57.7%

63.9%

64.7%

68.0%

68.5%

73.0%

75.7%

0% 20% 40% 60% 80% 100%

Alcohol Dependence

Hip Fracture

Ulcers

Urinary Tract Infection

Headache

Diabetes Mellitus

Hyperlipidemia

Benign Prostatic Hyperplasia

Asthma

Colorectal Cancer

Orthopedic Conditions

Depression

Congestive Heart Failure

Hypertension

Coronary Artery Disease

Low Back Pain

Prenatal Care

Breast Cancer

Percentage of Recommended Care Received

Quality Shortfalls: Getting it Right 50% of the Time

Adults receive about half of recommended care

54.9% = Overall care 54.9% = Preventive care 53.5% = Acute care56.1% = Chronic care

Not Getting the Right

Care at the Right Time

Source: McGlynn EA, et al., “The Quality of Health Care Delivered to Adults in the United States,” New England Journal of Medicine, Vol. 348, No. 26, June 26, 2003, pp. 2635-2645

6

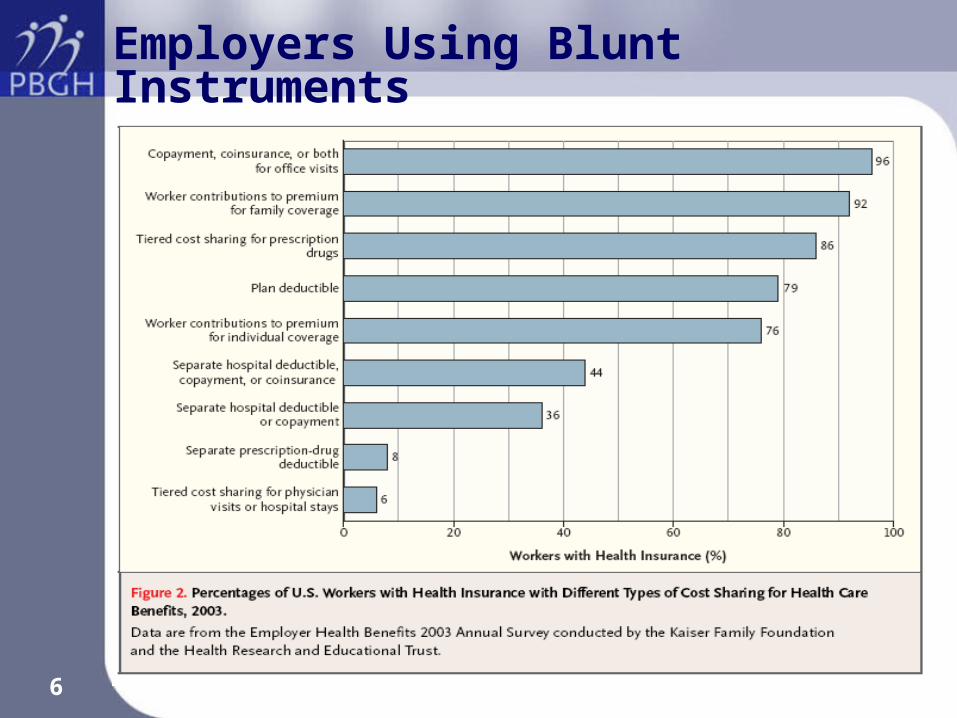

Employers Using Blunt Instruments

7

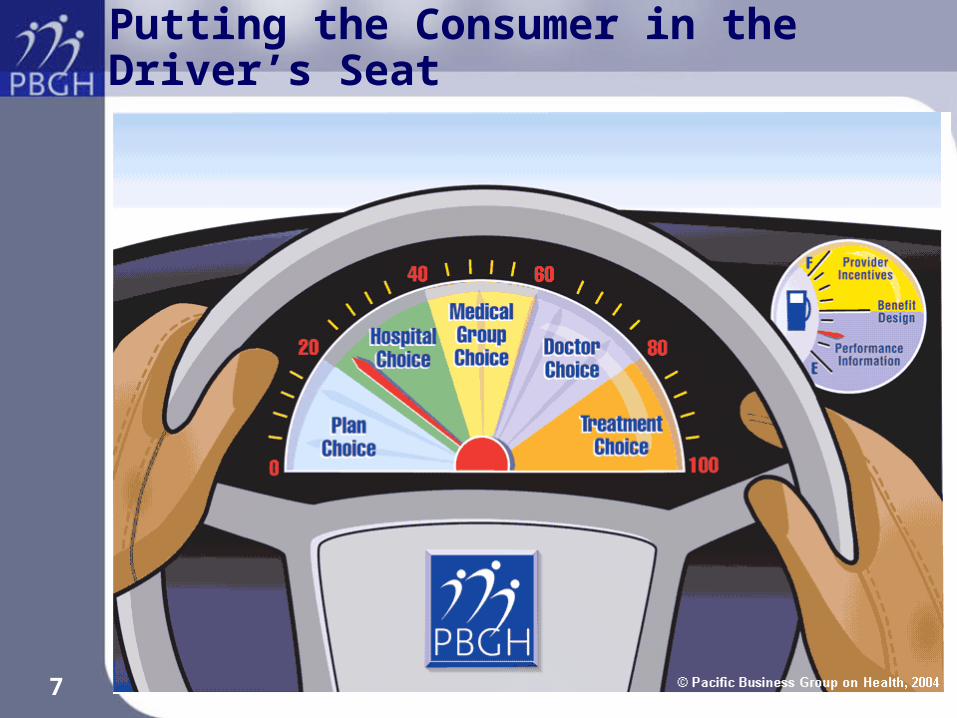

Putting the Consumer in the Driver’s Seat

8

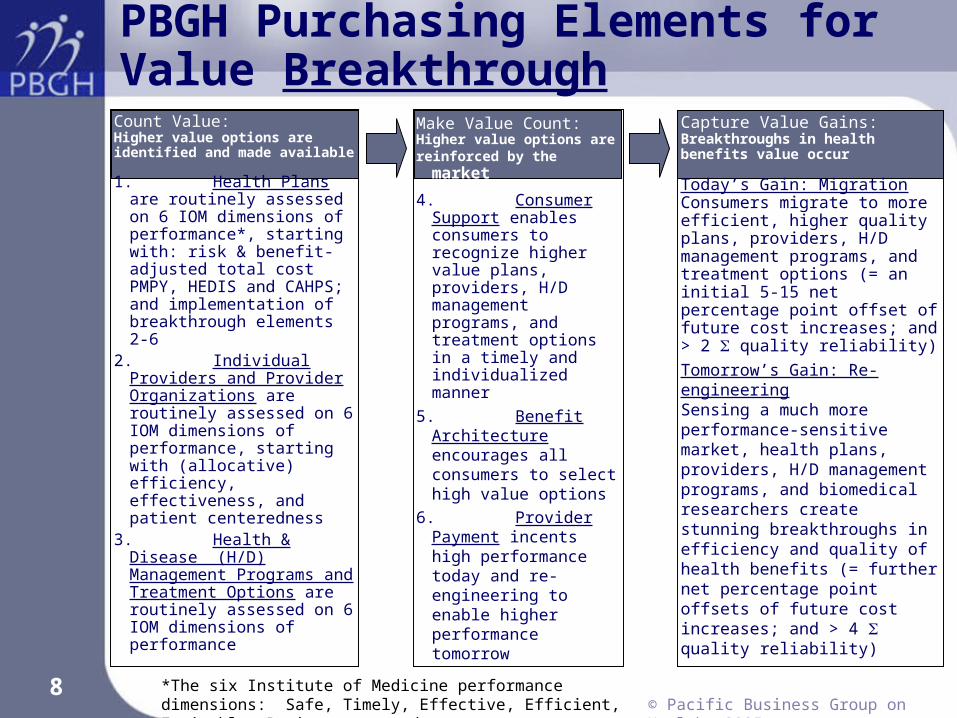

PBGH Purchasing Elements for Value Breakthrough

*The six Institute of Medicine performance dimensions: Safe, Timely, Effective, Efficient, Equitable, Patient-centered © Pacific Business Group on Health,

2005

Count Value:Higher value options areidentified and made available

1. Health Plans are routinely assessed on 6 IOM dimensions of performance*, starting with: risk & benefit-adjusted total cost PMPY, HEDIS and CAHPS; and implementation of breakthrough elements 2-6

2. Individual Providers and Provider Organizations are routinely assessed on 6 IOM dimensions of performance, starting with (allocative) efficiency, effectiveness, and patient centeredness

3. Health & Disease (H/D) Management Programs and Treatment Options are routinely assessed on 6 IOM dimensions of performance

Make Value Count:Higher value options arereinforced by the market

4. Consumer Support enables consumers to recognize higher value plans, providers, H/D management programs, and treatment options in a timely and individualized manner

5. Benefit Architecture encourages all consumers to select high value options

6. Provider Payment incents high performance today and re-engineering to enable higher performance tomorrow

Capture Value Gains:Breakthroughs in health benefits value occur

Today’s Gain: MigrationConsumers migrate to more efficient, higher quality plans, providers, H/D management programs, and treatment options (= an initial 5-15 net percentage point offset of future cost increases; and > 2 quality reliability)

Tomorrow’s Gain: Re-engineeringSensing a much more performance-sensitive market, health plans, providers, H/D management programs, and biomedical researchers create stunning breakthroughs in efficiency and quality of health benefits (= further net percentage point offsets of future cost increases; and > 4 quality reliability)

9

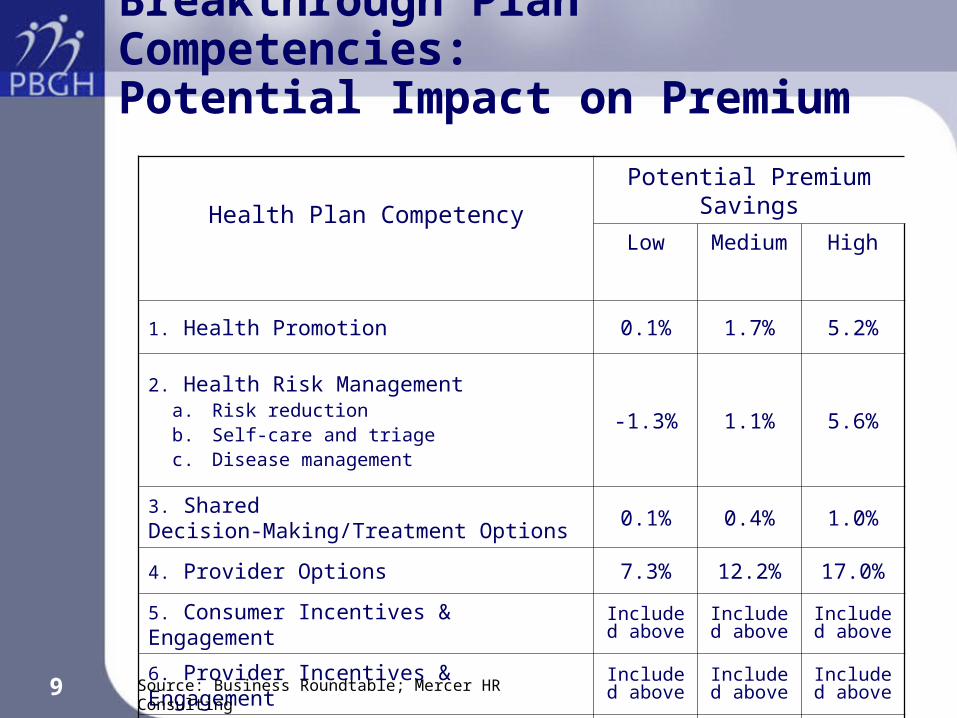

Breakthrough Plan Competencies: Potential Impact on Premium

Health Plan Competency

Potential Premium Savings

Low Medium High

1. Health Promotion 0.1% 1.7% 5.2%

2. Health Risk Managementa. Risk reductionb. Self-care and triagec. Disease management

-1.3% 1.1% 5.6%

3. Shared Decision-Making/Treatment Options 0.1% 0.4% 1.0%

4. Provider Options 7.3% 12.2% 17.0%

5. Consumer Incentives & EngagementIncluded above

Included above

Included above

6. Provider Incentives & EngagementIncluded above

Included above

Included above

TOTAL PREMIUM VALUE 6.2% 15.4% 28.8%

Source: Business Roundtable; Mercer HR Consulting

10 Adapted from Regence Blue Shield© Pacific Business Group on Health, 2005

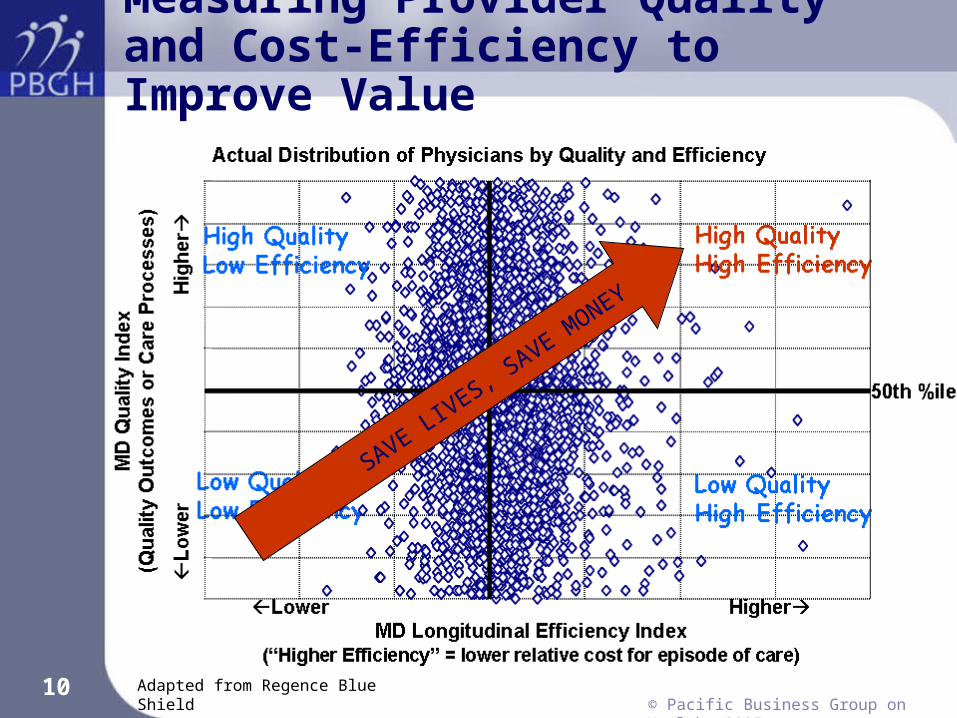

SAVE LIVES, S

AVE MONEY

Measuring Provider Quality and Cost-Efficiency to Improve Value

11

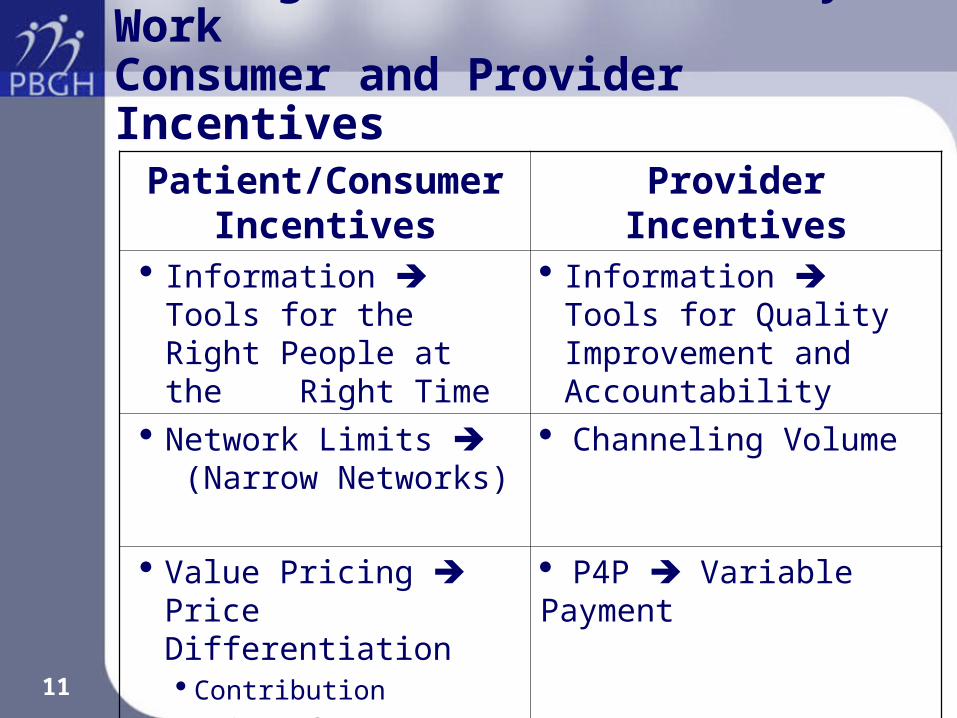

Putting Information & Money to WorkConsumer and Provider Incentives

Patient/Consumer Incentives

Provider Incentives

Information Tools for the Right People at the Right Time

Information Tools for Quality Improvement and Accountability

Network Limits (Narrow Networks)

Channeling Volume

Value Pricing Price Differentiation Contribution Point of Care

P4P Variable Payment

12

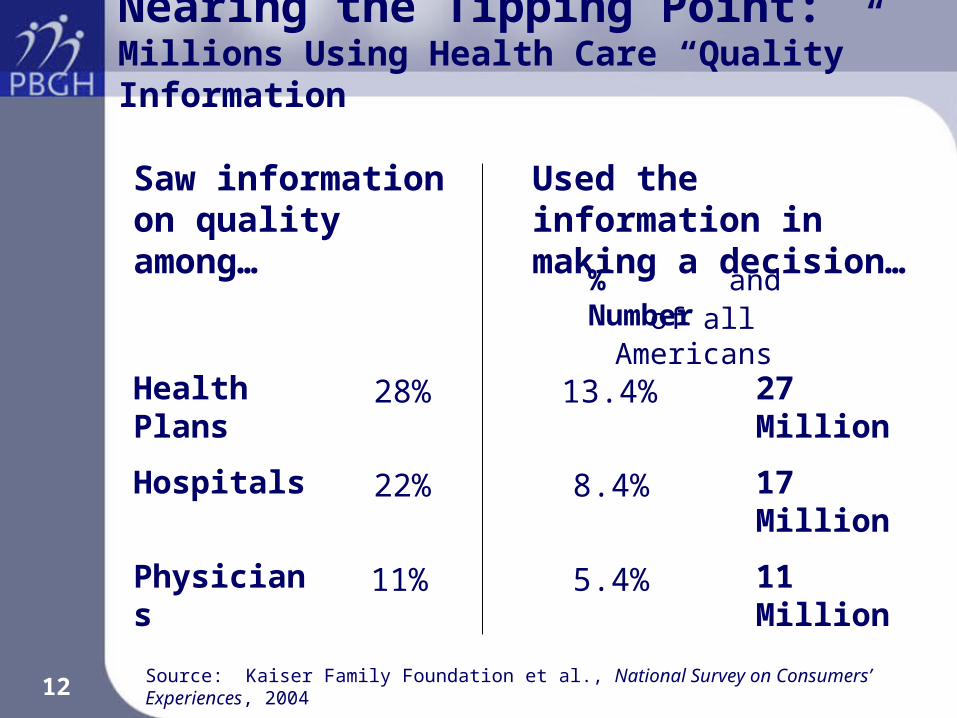

Nearing the Tipping Point:Millions Using Health Care “Quality” Information

Saw information on quality among…

Used the information in making a decision…

Physicians 11% 5.4% 11 Million

Hospitals 22% 8.4% 17 Million

Health Plans 28% 13.4% 27 Million

Source: Kaiser Family Foundation et al., National Survey on Consumers’ Experiences, 2004

of all Americans% and Number

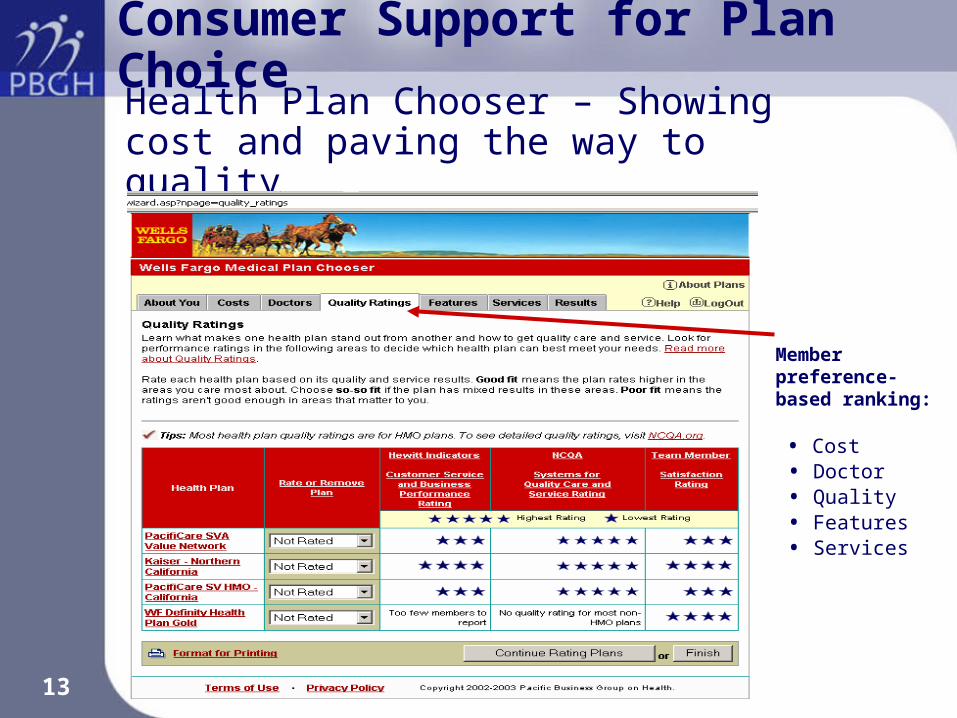

13

Health Plan Chooser – Showing cost and paving the way to quality

Consumer Support for Plan Choice

Member preference-based ranking:

• Cost • Doctor • Quality • Features • Services

CONFIDENTIAL14

Salary Level

<$40K $40-$80K & retirees

$80-$120K $120K plus

Health Net Monthly $$

$36 $86 $141 $187

% of Pay 1.3% 1.8% 1.8% 1.5%

Blue Cross Monthly $$

$172 $215 $274 $320

% of Pay 6.3% 4.5% 3.4% 2.6%

Source: University of California 2004

Supporting Equity:UC Employee’s Family Plan Cost

Consumer Incentives for Plan Choice

15

Hospital Choice Tools • Hospital quality linked to treatment choice information • Network, cost and quality information linked to tiered benefit design

Member preference-based ranking:

• Volume • Mortality • Complications • Length of Stay • Leapfrog • Cost • Patient Experience

Consumer Support for Hospital Choice

16

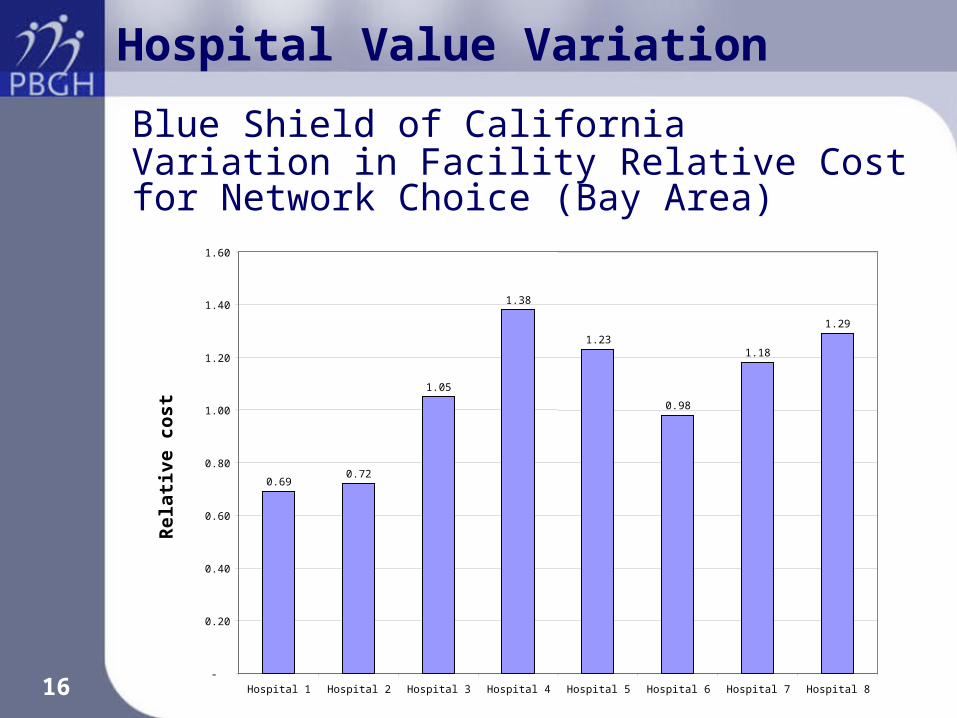

Rel

ati

ve

co

st

0.690.72

1.05

1.38

1.23

0.98

1.18

1.29

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Hospital 1 Hospital 2 Hospital 3 Hospital 4 Hospital 5 Hospital 6 Hospital 7 Hospital 8

Blue Shield of California Variation in Facility Relative Cost for Network Choice (Bay Area)

Hospital Value Variation

17

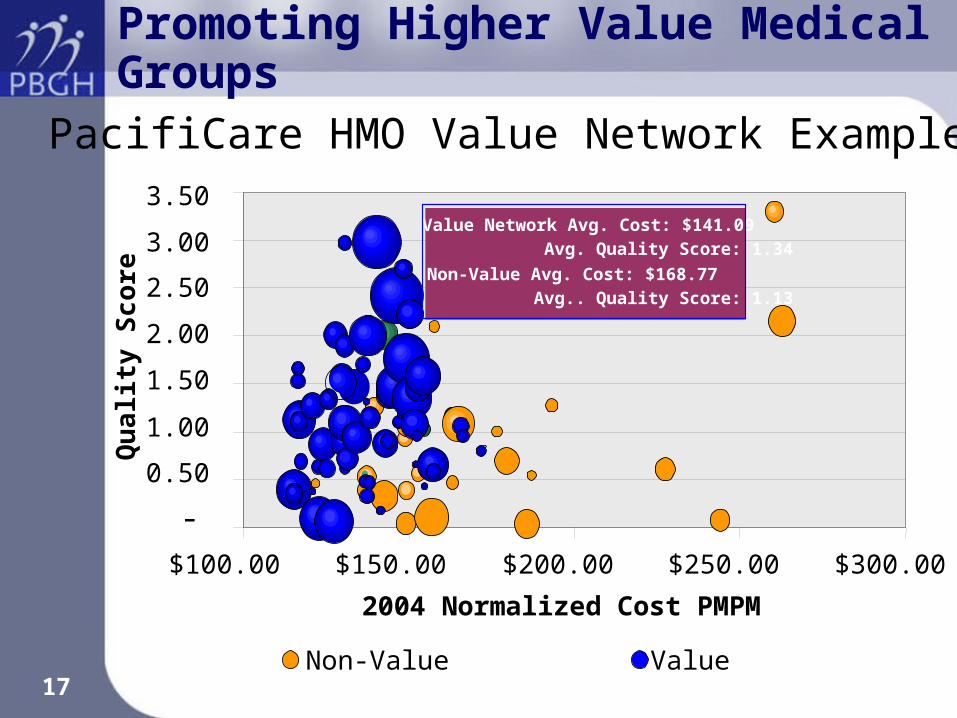

PacifiCare HMO Value Network Example

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

$100.00 $150.00 $200.00 $250.00 $300.00

2004 Normalized Cost PMPM

Qu

alit

y S

core

Non-Value Value

Value Network Avg. Cost: $141.09 Avg. Quality Score: 1.34

Non-Value Avg. Cost: $168.77 Avg.. Quality Score: 1.13

Promoting Higher Value Medical Groups

18

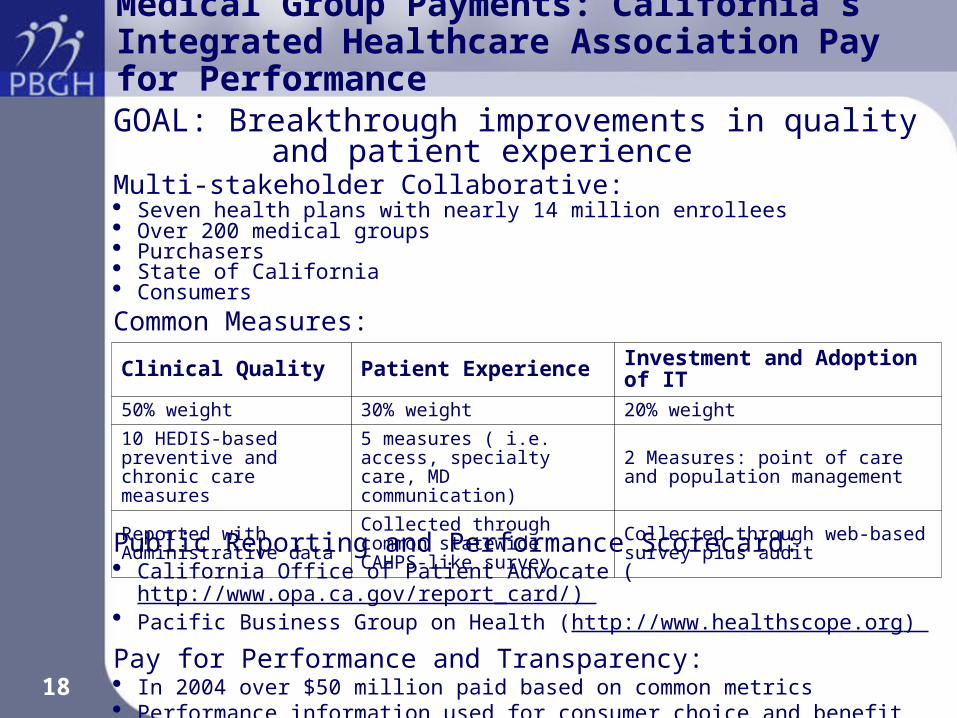

Medical Group Payments: California’s Integrated Healthcare Association Pay for Performance

GOAL: Breakthrough improvements in quality and patient experience

Multi-stakeholder Collaborative: Seven health plans with nearly 14 million enrollees Over 200 medical groups Purchasers State of California Consumers

Common Measures:Clinical Quality Patient Experience Investment and Adoption of IT50% weight 30% weight 20% weight

10 HEDIS-based preventive and chronic care measures

5 measures ( i.e. access, specialty care, MD communication)

2 Measures: point of care and population management

Reported with Administrative data

Collected through common statewide CAHPS-like survey

Collected through web-based survey plus audit

Public Reporting and Performance Scorecard: California Office of Patient Advocate (http://www.opa.ca.gov/report_card/) Pacific Business Group on Health (http://www.healthscope.org)

Pay for Performance and Transparency: In 2004 over $50 million paid based on common metrics Performance information used for consumer choice and benefit design

19

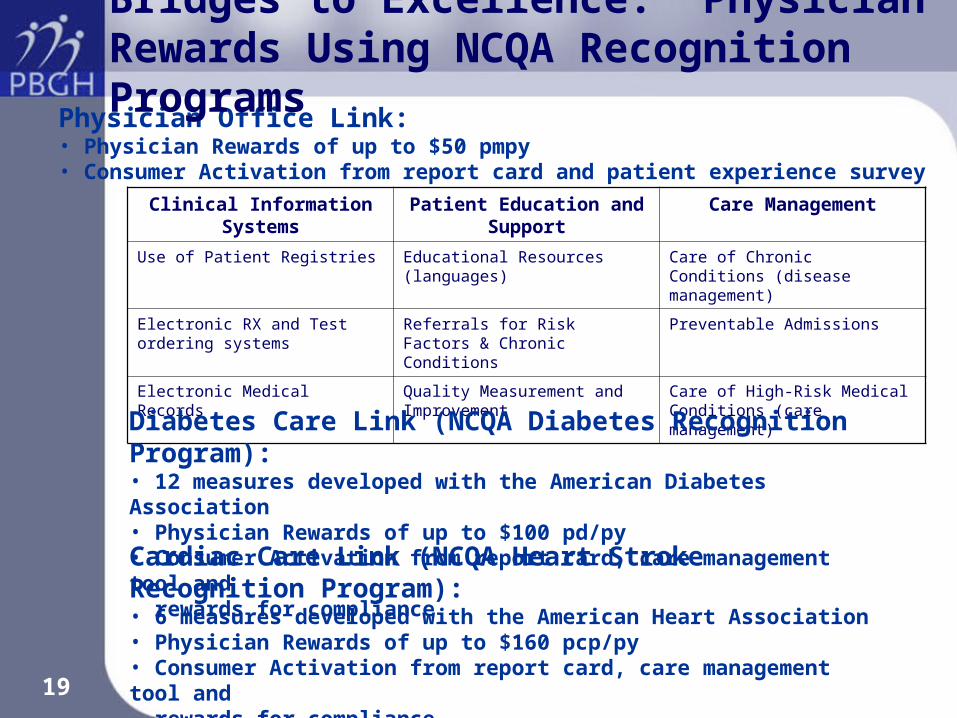

Clinical Information Systems

Patient Education and Support

Care Management

Use of Patient Registries Educational Resources (languages)

Care of Chronic Conditions (disease management)

Electronic RX and Test ordering systems

Referrals for Risk Factors & Chronic Conditions

Preventable Admissions

Electronic Medical Records Quality Measurement and Improvement

Care of High-Risk Medical Conditions (care management)

Physician Office Link: • Physician Rewards of up to $50 pmpy• Consumer Activation from report card and patient experience survey

Bridges to Excellence: Physician Rewards Using NCQA Recognition Programs

Diabetes Care Link (NCQA Diabetes Recognition Program):• 12 measures developed with the American Diabetes Association• Physician Rewards of up to $100 pd/py• Consumer Activation from report card, care management tool and rewards for compliance

Cardiac Care Link (NCQA Heart Stroke Recognition Program):• 6 measures developed with the American Heart Association• Physician Rewards of up to $160 pcp/py• Consumer Activation from report card, care management tool and rewards for compliance

20

PBGH & Where to Get More Information

To Learn More…

www.pbgh.org — an overview of PBGH programs and initiatives

www.HealthScope.org — consumer Web site with health plan and provider quality measurements

www.PacAdvantage.org — small group purchasing pool

http://chooser.pacadvantage.org — sample site to assist enrollees in plan selection

To subscribe to the PBGH E-Letter, go to www.pbgh.org/news/eletters