27

| Date post: | 02-Jan-2016 |

| Category: |

Documents |

| Upload: | zeph-flowers |

| View: | 16 times |

| Download: | 0 times |

204-052-dp

PurposePurpose

• To survey the economic literature regarding North American (NA) integration in the agri-food sector– To summarize the lessons learned so far

– To identify knowledge gaps and suggest areas for future research

• Structure of presentation

304-052-dp

How useful are trade statistics as indicators of integration?How useful are trade statistics as indicators of integration?

• Generally provide good insights– Detailed information on volume, value, and commodity composition

of trade over time

– Lacks the precision of price-based studies

• Quality of data has improved but is still not superior– Unnerving differences between US and Mexican statistics

– Similar differences existed between US and Canadian statistics prior to initiation of joint data collection in 1990

404-052-dp

Continental agri-food trade has grown tremendously over CUSTA/NAFTA period

Billions of U.S. Dollars

0

2

4

6

8

10

12

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

U.S. Exports to Canada

Canadian Exports to U.S.

US Exports to Mexico

Mexican Exports to U.S.

Canadian Exports to Mexico

Mexican Exports to Canada

504-052-dp

Agricultural exports to the rest of the world have experienced modest growth over the same period

Billions of U.S. Dollars

0

10

20

30

40

50

60

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

U.S. Exports to ROW

Mexican Exports to ROW

Canadian Exports to ROW

Intra-NAFTA trade

604-052-dp

Canada and the US have become more dependent on their NAFTA partners, Mexico more diversified

Percent of total exports

46

20

88

66

29

85

0

10

20

30

40

50

60

70

80

90

100

Canada U.S. Mexico

1991-1993

2000-2002

North American Share of Agriculture and Agri-Food Exports

704-052-dp

Mexico’s main agricultural exports to the US reflect Mexico’s comparative advantages

Annual avg., millions USD

4

322

923

145

749

1949

879

0

500

1000

1500

2000

2500

Fruits Vegetables Beer

1991-1993

2000-2002

804-052-dp

Similarly, the main US agricultural exports to Mexico are indicative of the comparative advantages of US agriculture

Annual avg., millions USD

4

219

896

231

744

1932

786

0

500

1000

1500

2000

2500

Beef and beef varietymeats

Grains and feeds Fruits and vegetables

1991-1993

2000-2002

904-052-dp

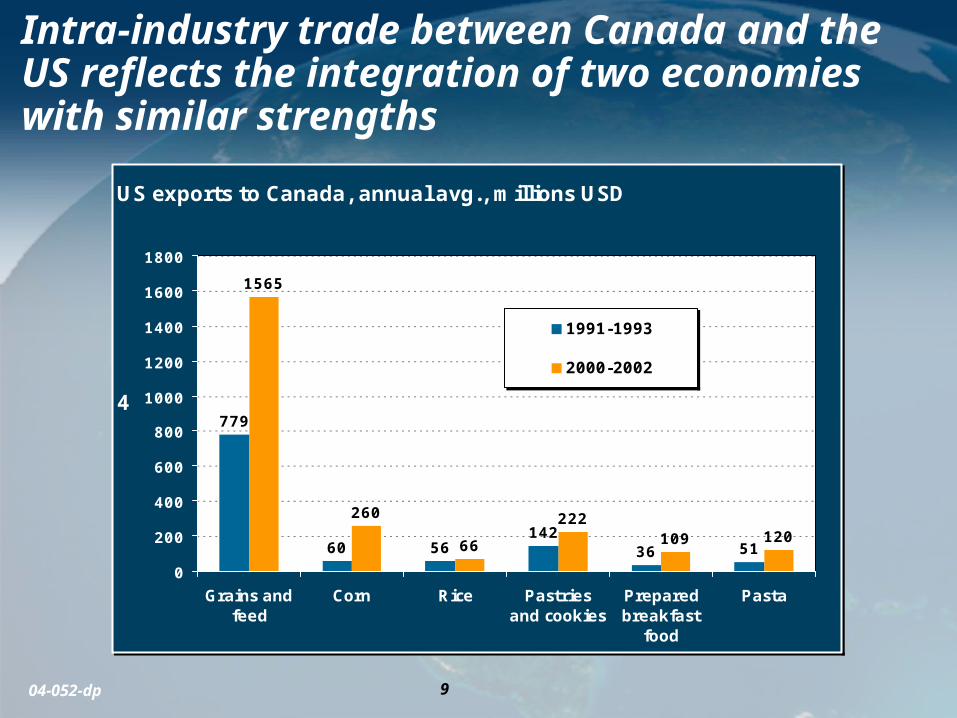

Intra-industry trade between Canada and the US reflects the integration of two economies with similar strengths

US exports to Canada, annual avg., millions USD

4779

60 56142

36 51

1565

260

66

222109 120

0

200

400

600

800

1000

1200

1400

1600

1800

Grains andfeed

Corn Rice Pastriesand cookies

Preparedbreakfast

food

Pasta

1991-1993

2000-2002

1004-052-dp

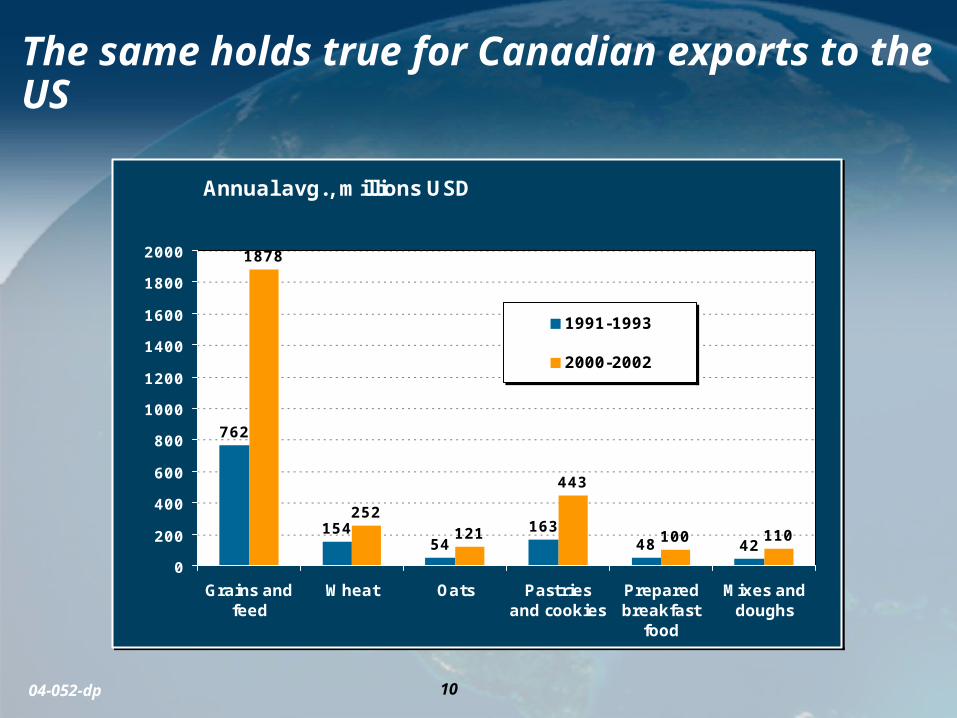

The same holds true for Canadian exports to the US

Annual avg., millions USD

4

762

15454

16348 42

1878

252121

443

100 110

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Grains andfeed

Wheat Oats Pastriesand cookies

Preparedbreakfast

food

Mixes anddoughs

1991-1993

2000-2002

1104-052-dp

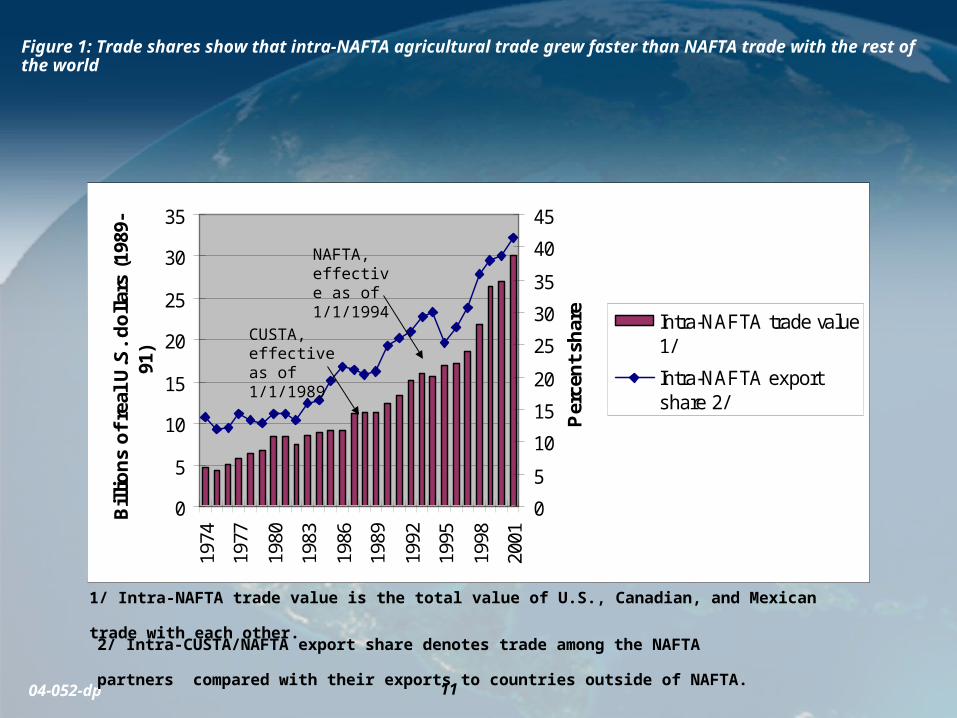

Figure 1: Trade shares show that intra-NAFTA agricultural trade grew faster than NAFTA trade with the rest of the world

0

5

10

15

20

25

30

3519

74

1977

1980

1983

1986

1989

1992

1995

1998

2001

Bil

lio

ns

of

real

U.S

. d

oll

ars

(198

9-91

)

0

5

10

15

20

25

30

35

40

45

Per

cen

t sh

are

Intra-NAFTA trade value1/

Intra-NAFTA exportshare 2/

NAFTA, effective as of 1/1/1994

CUSTA, effective as of 1/1/1989

2/ Intra-CUSTA/NAFTA export share denotes trade among the NAFTA partners compared

with their exports to countries outside of NAFTA.

1/ Intra-NAFTA trade value is the total value of U.S., Canadian, and Mexican trade with each other.

1204-052-dp

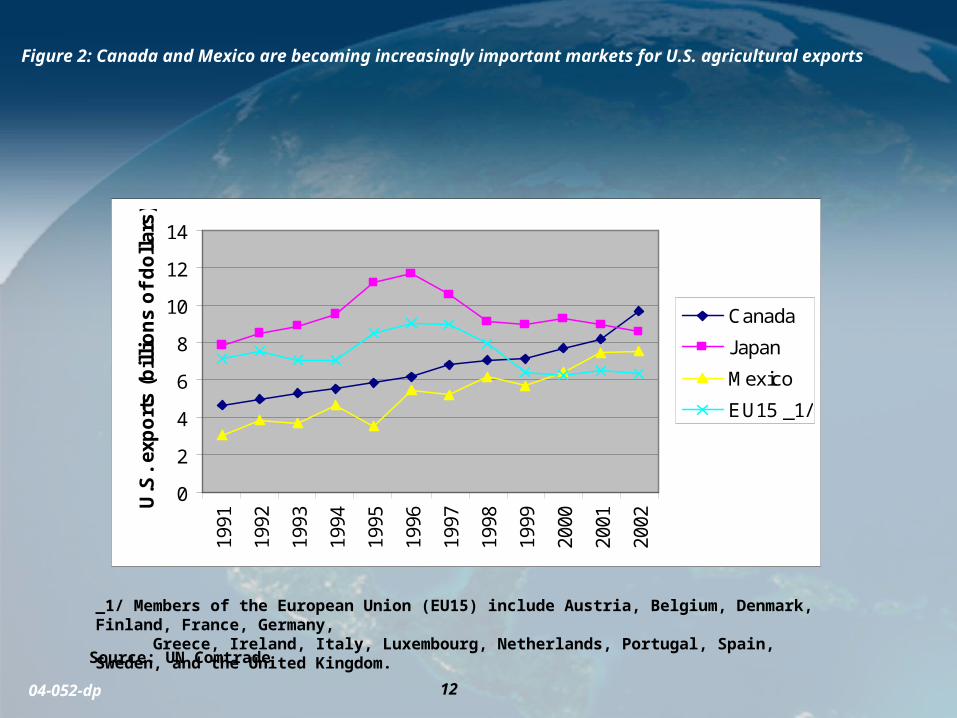

Figure 2: Canada and Mexico are becoming increasingly important markets for U.S. agricultural exports

_1/ Members of the European Union (EU15) include Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain, Sweden, and the United Kingdom.

Source: UN Comtrade

0

2

4

6

8

10

12

1419

91

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

U.S

. ex

po

rts

(bil

lio

ns

of

do

llar

s)

Canada

Japan

Mexico

EU15 _1/

1304-052-dp

Figure 3: The United States is also a very important agricultural market for exporters in Canada and Mexico

Source: UN Comtrade

0102030405060708090

1001991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Part

ner

exp

ort

desti

nati

on

sh

are

s

Mexico

Canada

1404-052-dp

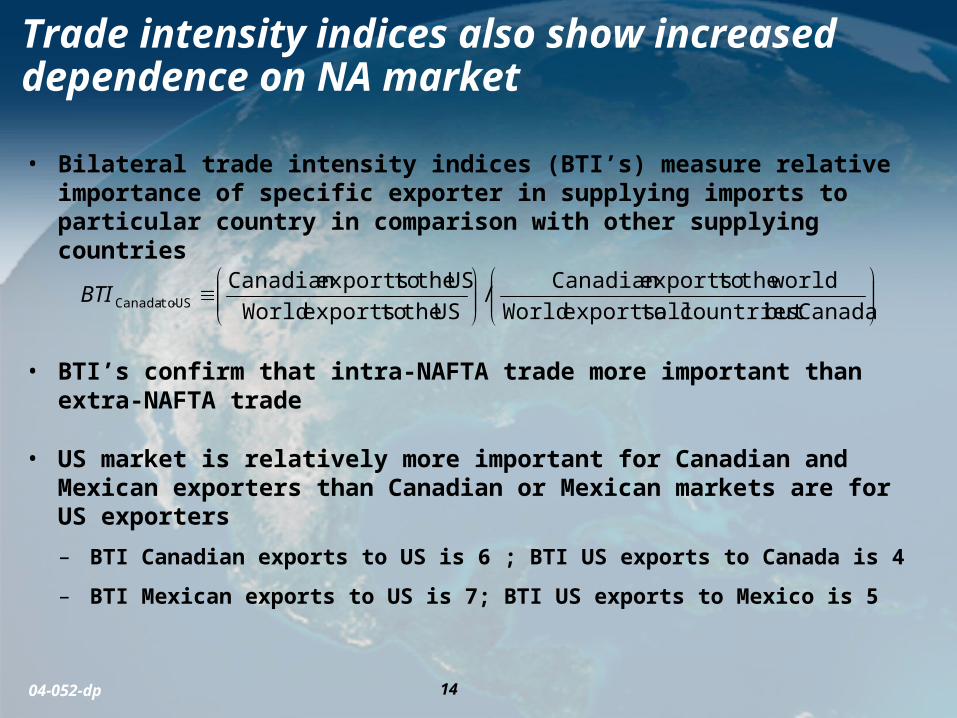

Trade intensity indices also show increased dependence on NA market

• Bilateral trade intensity indices (BTI’s) measure relative importance of specific exporter in supplying imports to particular country in comparison with other supplying countries

• BTI’s confirm that intra-NAFTA trade more important than extra-NAFTA trade

• US market is relatively more important for Canadian and Mexican exporters than Canadian or Mexican markets are for US exporters

– BTI Canadian exports to US is 6 ; BTI US exports to Canada is 4

– BTI Mexican exports to US is 7; BTI US exports to Mexico is 5

Canadabut countries all toexports World

world the toexportsCanadian /

US the toexports World

US the toexportsCanadian US-to-CanadaBTI

1504-052-dp

Composition of NA agri-food trade is changing

• Importance of bulk commodities declining

• Canada and U.S. trading more high-value processed products and intermediate goods

• Mexican exports now dominated by fresh produce and horticultural products, Mexican breweries also major force

• Intra-industry trade growing – particularly between Canada and US

– Sign that production processes cut across border

• Evidence of increasing trade complementarities since CUSTA/NAFTA

– Trade increasingly reflects comparative advantage

1604-052-dp

The trade criterion can be misleading

• Trade flows affected by many factors

• Discriminating monopolists segment markets to maximize profits

• Entrepreneurs may be indifferent as to with whom they trade

• Arbitrage may not be profitable due to transportation and marketing costs

1704-052-dp

Theoretical yardstick: Price-based view of

market integration

• Consistency with LOP, Dornbusch, Rogoff

• Nationality not important, Goldberg & Knetter

• A matter of degree, Fackler & Goodwin

• S.R. & L.R. dynamics of price adjustments, Fackler & Goodwin

• “Market connectedness,” McNew

• Rationale absence of arbitrage, Barrett

• Price variability, Hufbauer, Bradford & Lawrence

• “thickness” of product availability, Knetter & Slaughter

1804-052-dp

Laymen’s definitions

• Removal of barriers to commercial exchange, Robertson • No arbitrage rents, Harvey

• Market integration exists when product flows between countries are on the same terms and conditions as within countries, Knutson & Ochoa

• An integrated market consists of two or more economically interdependent but spatially separated markets in which there are no barriers that distort trade and investment activities across borders

1904-052-dp

Law of One Price holds for Canada-US agri-food trade

• Econometric studies quantifying the degree of integration in commodity markets

• Prices in Canada/U.S. beef and pork markets highly correlated, supply-managed sectors less so

• Policy changes have increased price co-integration

– Prices in Canada/U.S. wheat and barley markets more co-integrated following repeal of WGTA, NAFTA

• Asymmetrical price effects

– Price shocks originating in the U.S. have greater impact on Canadian prices than vice-versa

• Law of One Price less useful in US-Mexico context

– Incomplete exchange-rate pass through, high and variable Mexican inflation rate

2004-052-dp

Trade agreements not the only factors contributing to integration

• Geographical location & cultural heritage

• Technology: Advances in transportation, storage, and electronic communication

• Macroeconomic factors

– Level of development

– Exchange rates

• National policy goals• Market orientation of domestic policy key to capturing

benefits from trade agreements

– Trade agreements• Regional: CUSTA and NAFTA on market access,

investment• Multilateral: WTO’s URAA on export subsidies, domestic

support

2104-052-dp

Foreign direct investment is an important element of integration

• FDI in NA has grown tremendously since CUSTA/NAFTA

• Processed food demand in Canada, US, Mexico met more through FDI than trade

• Sales of US affiliates 2.5 times larger than exports of processed food to Canada or Mexico

Billions of U.S. Dollars

0

5

10

15

20

25

30

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Sales by U.S.-owned affiliates

Imports from Canada and Mexico

Exports to Canada and Mexico

2204-052-dp

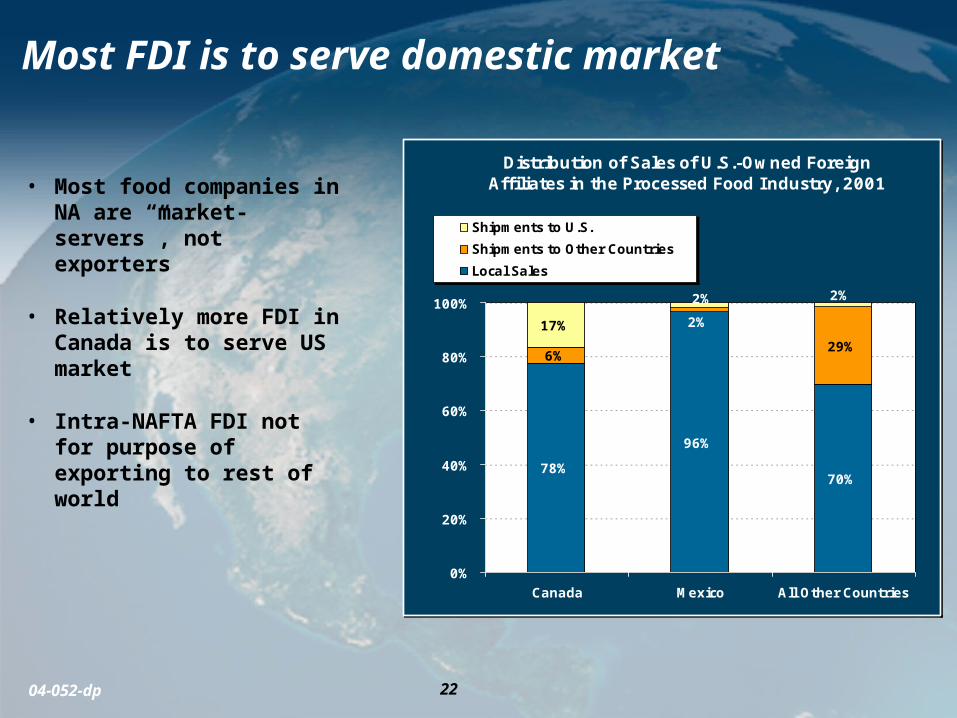

Most FDI is to serve domestic market

• Most food companies in NA are “market-servers”, not exporters

• Relatively more FDI in Canada is to serve US market

• Intra-NAFTA FDI not for purpose of exporting to rest of world

Distribution of Sales of U.S.-Owned Foreign Affiliates in the Processed Food Industry, 2001

70%

96%

78%

6%29%

2%17%

2% 2%

0%

20%

40%

60%

80%

100%

Canada Mexico All Other Countries

Shipments to U.S.

Shipments to Other Countries

Local Sales

2304-052-dp

Food firms display preference for majority ownership

• Desire for control over brand, technology, and market development drives ownership decisions

• Typical steps to market entry– Export to test market potential

– Strategic alliance with domestic firm

– Foreign direct investment through mergers and acquisitions

• International joint ventures offer advantages– Anti-trust policy, access to distribution networks

– Soft drink and brewing industries built solidly on international licensing

– Cross-border contracting in production agriculture

2404-052-dp

Big fish from Canada and Mexico now swim in bigger pond

• Large firms in Canada and Mexico expand to take advantage of continental market

– McCain (Canadian) operates 8 food processing facilities in US, one in Mexico

– Weston Foods (Canadian) has large and growing share of US bakery products market, ¾ total corporate sales in US market

– Gruma (Mexican) is largest producer of corn flour and tortillas in US, ½ total corporate sales in US market

2504-052-dp

Link between integration and performance deserves more attention

• More questions than answers

• Trade theory suggests gains from:– Specialization/comparative advantage

– Economies of scale

– Increased competition

– Knowledge spillovers

• Benefits should be greatest in Mexico– Lower capital/labour ratio, low labour productivity

– Higher agricultural tariffs

– Greater access to US market

2604-052-dp

Economic research needed to further policy discussions

– Extent of price integration• No studies of price co-movements in Mexico-US

agri-food markets & many US-Canada commodity markets remain unexamined

– Measurement of border transaction costs• As tariffs come down, impact of non-tariff

barriers ever more important• Useful in the design of regulations and standards

– Effect of integration on competition• Relationship between increasing trade &

investment and market power exercised by food companies

• Input into design and enforcement of competition policy

2704-052-dp

Economic research needed to further policy discussions

– Effect of integration on productivity• Identify and quantify economic gains arising

from trade and investment

• Useful in trade communications

– Distribution of gains from integration• Many sub-sectors/regions are better-off, but

some worse-off

• Input into design of policies to ease adjustment

– Other topics?