HIGHLIGHTS A vast majority of the Latin America population still does not have access to mobile broadband services (mobile broadband penetration of the population will stand at 4% at the end of 2011). On the fixed broadband front, we project an 8% penetration of the population by the end of 2011. Recognizing the need for national level policy and guidance for the telecom sector, many governments in Latin America have developed comprehensive broadband plans with ambitious goals and targets to ensure that a significant percentage of the population has or will gain access in the next 5-10 years. National broadband plans are welcomed politically, and they help prove that a country values the development of a knowledge society with citizens who are increasingly digitally literate. There is no “one size fits all” approach available, and Pyramid Research sees various models adopted by countries in Latin America. Clear plans with multiple layers of resource support are most likely to succeed in LA. NBPs can mobilize the private sector and stimulate new areas of economic productivity. Public-private partnerships can be a successful, mutually beneficial

model to deliver NBP goals and objectives.

Vol. 3, No. 9, December 2011

Pyramid Research

Latin America Telecom Insider

National Broadband Plans Show a Diversity of Methods but a Unity of Purpose

TABLE OF CONTENTS

INTRODUCTION 2

NATIONAL BROADBAND PLANS IN THE LATIN AMERICAN CONTEXT 3

A. Clear plans with multiple layers of resource support are most likely to succeed in LA 4 B. NBPs can mobilize the private sector and stimulate new areas of economic productivity 9 C. Public-private partnerships can be a successful, mutually beneficial model to deliver NBP goals and objectives 11

MARKET DETAIL 13 CASE STUDY: Colombia sets ambitious goals to increase access to broadband Internet 13 CASE STUDY: Chile demonstrates its commitment to UAS by setting clear objectives and seeking assistance from the private sector 14 CASE STUDY: Brazil aims to reach universal access to broadband Internet with a minimum of 1Mbps at R$35 per month 15

Introduction National broadband plans (NBPs) have become synonymous with a country’s commitment to expansion and development. ICTs are considered a highway to socioeconomic development. Lack of access to broadband capacity is one impediment that must be addressed with the appropriate resources to support the progress that can come with successful broadband introduction and adoption. Recognizing the need for national level policy and guidance for the sector, many governments in Latin America (LA) have developed comprehensive broadband plans with ambitious goals and targets to ensure that a significant percentage of the population has or will gain access in the next 5-10 years. Argentina, Brazil, Chile, Colombia, the Dominican Republic, Paraguay and Peru (see Exhibit 3) have all articulated plans that are generally overseen by government ministries and/or the regulatory authorities in each country. One of the most important benefits of broadband access is an increase in economic development and productivity. For example, a 2009 World Bank report revealed that there is a positive correlation between broadband service penetration and increases in economic development. The GSMA released a study in September 2011 that stated that “the deployment of the 700MHz spectrum for Mobile Broadband across Latin America also delivers significant social and economic benefits. This includes an additional US$3.1 billion in GDP growth, 5,540 more jobs and US$2.6 billion further tax revenue than would be created through broadcasting services.” In addition to these studies, there have been numerous anecdotes and case studies relating the ways that broadband access has transformed lives in LA for the better. NBPs are drivers for development and mobilize resources from the public and private sectors for investment and expansion of broadband services. NBPs also provide guidance and align all stakeholders’ objectives with national level goals. The provision of broadband service does not only impact the telecommunications industry; the agriculture, education and health sectors all can be boosted by connectivity. The multipurpose use of broadband service therefore requires input from organizations across all sectors to bolster the likelihood of NBP success. National broadband plans are catalysts to development and help facilitate the cooperation of human, business and technological resources for the purpose of building a strong broadband presence in a nation. Pyramid Research believes that operators have a vested interest in influencing and supporting NBPs because the dividends generated from a country’s digital development have the potential to contribute to increased service adoption and consequently operators’ revenue. Becoming a part of national broadband discussions in Latin America and offering support is a forward-looking strategy that helps create a win-win situation for all involved. In this Insider, we will examine national broadband plans that have debuted in select countries in Latin America and highlight key themes that are vital to success. This examination will include examples of accomplishments that have been made through the help of having a clearly defined NBP in place. Next, we will provide project investments that the private sector has made to support NBPs, with special attention given to areas previously deemed to lack commercial potential. An analysis of the suitability of public-private partnerships (PPPs) to realize NBP objectives will follow. The report will conclude with case studies of more detailed national broadband plans from Brazil, Colombia and Chile, along with recommendations of best practices for NBP development.

National broadband plans in the Latin American context In the past decade, on average, new technology has debuted in Latin America about two years after it debuts in the US. For example, 3G was introduced in 2004, just two years after it was made available in the US. The telecom sector in Latin America, especially the mobile segment, has grown drastically in the past decade. Despite our projection that LA will swell from a 99% mobile subscription penetration in 2010 to 108% at the end of 2011, a vast majority of the population still does not have access to mobile broadband services (mobile broadband penetration of the population will stand at 4% at the end of 2011). On the fixed broadband front, we project an 8% penetration of the population by the end of 2011. Looking forward, Pyramid Research expects 3G and 4G networks to quickly displace 2G networks in the region and to account for 73% of subscriptions by 2016 (see Exhibit 1).

Exhibit 1: Evolution of subscriptions by technology, Latin America, 2008-2016

Source: Pyramid Research Mobile Forecast, Latin America

We predict that the availability of 3G, and eventually LTE, will drive demand for mobile broadband by expanding the ways in which mobile services, especially connectivity, can be leveraged by increasingly sophisticated consumers. The maturation of ICTs in the telecom sector has caused most Latin American governments to consider how they can respond to the growing need for firm courses of action to help ensure universal access to broadband services. For example, in November 2011, Brazilian Minister of Communications Paulo Bernardo proposed developing a broadband network that would connect the whole of South America, with the intent of driving down Internet and mobile services costs. Before broadband subscription numbers can rise, interested stakeholders must work together to address challenges that can stifle access. One of the biggest hurdles to achieving universal broadband access in the region is geography. Latin America is home to a range of landscapes ― from rugged mountains to tropical rainforests in large areas of several countries ― where it is difficult to build a solid fixed-line infrastructure. Accessing broadband service once it is available is then dependent upon affordability. The GDP per capita in many LA countries is below US$15,000 (see Exhibit 2), and significant percentages of the population live in remote and rural areas, often considered commercially non-viable to large operators. Given these market and economic realities, operators in Latin America must prioritize the development of competitive pricing schemes in order to help ensure high levels of broadband adoption while

making a return on their investment. Still another consideration to make is the availability and affordability of hardware and devices to access broadband services.

Exhibit 2: GDP per capita, select countries, Latin America, 2011E

Source: Pyramid Research, September 2011 Mobile Data Forecast, Latin America

In light of the present lack of broadband ubiquity, the creation of national broadband plans can offer governments and the private sector in Latin America a road map to guide and facilitate infrastructure deployment while addressing the myriad challenges with targeted projects and programs (e.g., to increase ICT literacy, to provide shared access to the Internet, to provide ICT training and capacity to SMEs). Furthermore, assessing and measuring the achievement of goals established by NBPs is made easier when stakeholders know the expectations for their roles and are engaged in the process. Early involvement in NBP formulations or updates is imperative for operators and all stakeholders who seek to benefit once broadband service matures in the region.

A. Clear plans with multiple layers of resource support are most likely to succeed in LA In September 2011, the International Telecommunications Union (ITU) released a report on national broadband plans that described these plans as a type of social contract. With this framework in mind, NBPs can be said to bind the public sector, private sector and civil society together in a way that encourages each party to work for the best interests of the whole; the gains that one group makes can generally benefit the others. Several countries in the region have developed and issued detailed plans in order to establish a clear path to broadband accessibility and affordability for all. NBPs are welcomed politically, and they help prove that a country values the development of a knowledge society with citizens who are increasingly digitally literate. There is no “one size fits all” approach available, and Pyramid Research sees various models adopted by countries in Latin America (see Exhibit 3).

Exhibit 3: Brief overview of national broadband plans, select countries, Latin America

Country National broadband plans

Argentina

“Argentina Conectada” is Argentina’s national telecoms plan that debuted in October 2010. By 2015, the plan aims to expand broadband and digital TV service throughout the country. One of the top strategic objectives of the plan is to promote digital inclusion. Most of the nearly $2bn that has been allocated for implementing this plan will be used to purchase laptops to be used in homes and telecommunications equipment that will help make broadband service or access to a connection a reality for at least 10m households by the end of the project period.

Brazil

The “Programa Nacional de Banda Larga” (National Broadband Plan) was announced by the government in May 2010 and established a number of key objectives: promote digital inclusion, improve service quality and contribute to economic development. With a goal to connect 72% of Brazil’s households to broadband by 2014, the plan outlines the government’s program to invest in and mobilize private investment in broadband infrastructure, as well as several regulatory measures to increase competition, make additional spectrum available, and promote infrastructure sharing, among other measures. The government established the Digital Inclusion Secretariat in the Ministry of Communications and made clear that reaching the targets set by the NBP are a priority for Brazil’s socioeconomic development. The plan will cost approximately $7.5bn.

Colombia

Colombia announced its national broadband plan, “Vive Digital,” in October 2010. Under this plan, the Ministry for Information and Communication Technologies has named four aspects that it hopes to address in order to support technological advancement and the construction of a digital ecosystem in the country: infrastructure, services, applications and users. These goals will be achieved by bolstering and proliferating PPPs, eliminating regulatory and tax barriers, promoting the demand for ICTs, and government use of ICTs to demonstrate their utility to the populace. By 2014 the government hopes to increase Internet connections to 8.8m (about four times the number of subscriptions today). Specifically, it aims to have 50% of households and 50% of SMEs in Colombia with Internet connections and to triple the number of cities with high-speed Internet connections to 700. A National Digital Council has been created to oversee the achievement of these goals, which include a total investment of $2.8bn from the Ministry of ICTs and other ministries that have a vested interest and are engaged in the success of the plan.

Chile

The “Digital Strategy 2007-2012” was launched in Chile under the presidency of Michelle Bachelet. The plan was developed primarily through a participatory process that sought out views and opinions from a cross-section of society and includes attention to increasing broadband access. The plan aims to provide broadband service for an additional 2.3m people in Chile, including 90% of people located in rural areas. Broadband will be used to develop ICT skills for entrepreneurs for businesses of all sizes, augment existing e-government services, and reducing the student/computer ratio while using broadband access to facilitate management of schools. The Chilean government has pledged at least $100m to support this initiative, with $70m of the funds coming from Chile’s Telecoms Development Fund.

In November 2011 the Paraguayan government announced that it would be investing $150m a year in the implementation of its National Telecommunications Plan (PNT). The focus of its plan is to increase access to broadband for its citizens. The projects will primarily be managed by Paraguay’s telecommunications regulator, Comisión Nacional de Telecomunicaciones (Conatel). The government wishes to deploy 1,000km of fiber-optic cable each year to reach 50% of homes by 2015. The PNT’s other ambitious goals include increasing mobile penetration to 100% and fixed lines from 6.1% to 10%. The target for broadband penetration is to grow from 13% to 50% in three years. While only 76 municipalities in Paraguay are covered by broadband service, the government aims to have 200 municipalities covered by 2015. One source of funding already dedicated to helping achieve these goals is the country’s Universal Service Fund. Another is through private investment, which Paraguay plans to encourage through the use of subsidies.

Dominican Republic

Currently in development with input from the National Commission for an Information and Knowledge Society of the Dominican Republic, the “e-Dominicana” national broadband strategy document for the year 2015 is being crafted as an update to the guide laid out in the 2007-2010 plan. Under the old plan, seven axes were identified as areas of potential broadband impact: access and connectivity, education, culture and information, e-government, industry productivity, a legal framework permitting and promoting ICT usage, and the civil society. Accordingly, future broadband-related investments will be prioritized in these areas. INDOTEL, under the “Red Dominicana de Banda Ancha para el Desarollo,” is estimated to have invested about $461,000 in a high-speed connectivity network projects at six universities in the country between 2009 and 2011. Another project to support technology in education, including the provision of computers with Internet access for educational resources, will receive about $742,000 from INDOTEL during the same time period. Overall, for the 2009-2011 Biennial Development Plan, INDOTEL will invest more than $30m to fund 14 initiatives for broadband-related development, around $4m of which is earmarked for rural broadband connectivity development, an initiative that INDOTEL considers a priority.

Peru

The provision of universal access is the main theme of the “National Broadband Plan for Peru,” which is largely guided and implemented by FITEL, the telecommunications investment fund, funded by taxes on telecom revenue. The goal is to promote socioeconomic development in Peru, especially in rural areas. By 2010 FITEL had invested around $114m in rural connectivity projects, and nearly 15,000 towns benefited from the support. For the next few years, FITEL will invest more than $16m in areas across Peru, with the aim of providing additional public telephone service and broadband Internet. The Peruvian government also signed an agreement with Telefónica in 2009 to have the MNO help with nationwide broadband deployment for around 1.7m residential customers.

Sources: Pyramid Research, governments in Latin America

When reviewing these NBPs, we see that there are some recurring elements:

the plans are generally five years in length,

a ministry or other government entity is charged with shepherding the actions under the plan,

significant funding toward broadband infrastructure and development is pledged by the government and/or through contributions by the private sector, and

specific and measurable goals to be achieved are delineated.

All of these elements have a similar level of importance in terms of their efficacy to form a plan that will make an impact on bridging the digital divide. Furthermore, these elements leverage aspects of what are considered to be best practices in national broadband plan formation (see Exhibit 4).

Exhibit 4: National broadband plan decision tree

Source: International Telecommunications Union, 2011

Some of the countries in Latin America, which are currently in their second or third five-year cycle, have so far demonstrated that adhering to a formula that makes use of a customized combination of the components named above can yield tangible results (see Exhibit 5).

Exhibit 5: National broadband plan accomplishments, select countries, Latin America

National broadband plans: Some accomplishments

Argentina

The government invested about $7m to lay 500km of fiber optics in the La Rioja province to connect 17k households to Wi-Fi Internet services. Citizens pay about $9 a month for the service.

Compared with 2010, Internet access in homes rose by 31.7% and grew by 37.5% for organizations, according to the National Institute of Statistics and Census.

From 2005 to 2010 the number of online shoppers in Argentina doubled to just over 5m people, partially a result of broadband service provision.

In the summer of 2011 the government in Argentina offered a tender to provide nearly 5k schools and 700 public libraries with broadband Internet access.

Chile

According to government statements, as of March 2011, Chile spends the equivalent of $400m a year on ICTs.

Peru

Between 1998 and 2009, 515 “cabinas publicas” were built for providing citizens access to the Internet.

As of spring 2009 there were 13 government-level and 42 ministry-level projects related to e-government development being designed, planned, ongoing or completed in Peru. A notable project is One Laptop Per Child, due to be completed in 2011.

Dominican Republic

An agreement to create a national digital archive in 2010 for $122k.

As of September 2011, in partnership with World Vision, 35 telecenters have been created.

Since 2006, at least 1,528 people have benefited from taking courses in five computer training centers opened by INDOTEL and la Federación Internacional de Asociaciones de Ayuda Social Ecológica y Cultural (FIADASEC).

As of September 2011, 63 Wi-Fi connections that offer free Internet access to the public have been installed in places around the country.

Connectivity centers installed in 20 prisons.

Colombia

The first phase of a broadband development project guided by Compartel and completed in 2010 provided connectivity for 4,857 educational institutions and 121 health centers. A second phase of the plan to be completed year-end 2011 will benefit 363 libraries.

As part of the Digital Literacy project, Compartel has opened 1,669 community telecenters, which offer seven courses that help the public develop ICT skills.

Uruguay

One of the leaders in Latin America in broadband development activity, Uruguay now has over 25% of its citizens connected to broadband services.

In 2007 the government launched the Ceibal Plan, an initiative to bring broadband connectivity to schools throughout the country and laptops to every child in conjunction with the One Laptop Per Child initiative. The aim of the plan is to increase social inclusion and to integrate ICTs into the educational experience.

Under the Ceibal Plan, as of December 2010, nearly 337k users have been reached, a figure that represented 10% of the population for that year. Three out of four schools also have an Internet connection.

Sources: Pyramid Research, governments in Latin America

It is critical to note the importance of the early involvement by the beneficiary communities in the planning process. It is not sufficient to bring broadband to a region if the population and businesses, especially micro and SMEs, in those areas do not know how to make the most of ICT access. By providing ICT capacity and training at local telecenters or working in conjunction with universities and other education institutions to integrate ICT awareness and skills delivery into the curriculum, governments and operators can help strengthen the level of adoption experienced. Education and training can boost the productivity and skill level of the human resources in a country, help a government remain competitive by its ability to attract business development with a better skilled workforce, and enable operators to develop a more solid foundation for a broadband consumer market. Whatever approach is selected, stakeholders must consider the challenge of delivering universal broadband access as one that can benefit not just the telecommunications sector, but the entire development of the country.

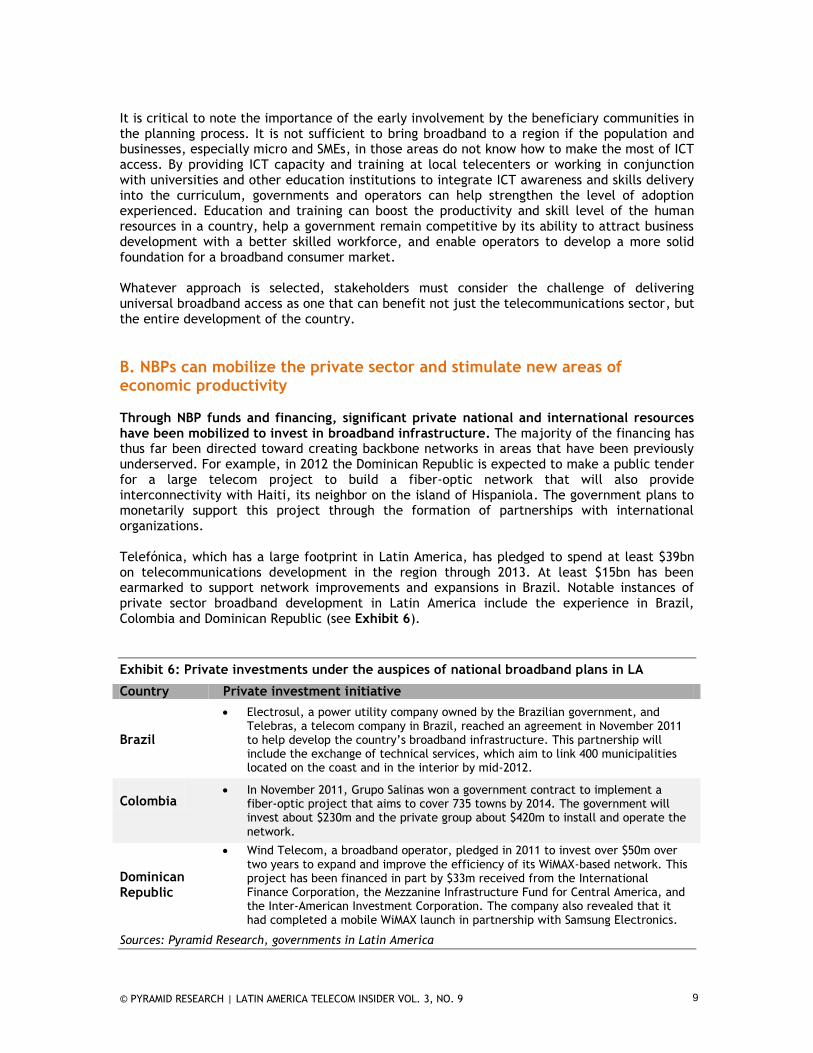

B. NBPs can mobilize the private sector and stimulate new areas of economic productivity Through NBP funds and financing, significant private national and international resources have been mobilized to invest in broadband infrastructure. The majority of the financing has thus far been directed toward creating backbone networks in areas that have been previously underserved. For example, in 2012 the Dominican Republic is expected to make a public tender for a large telecom project to build a fiber-optic network that will also provide interconnectivity with Haiti, its neighbor on the island of Hispaniola. The government plans to monetarily support this project through the formation of partnerships with international organizations. Telefónica, which has a large footprint in Latin America, has pledged to spend at least $39bn on telecommunications development in the region through 2013. At least $15bn has been earmarked to support network improvements and expansions in Brazil. Notable instances of private sector broadband development in Latin America include the experience in Brazil, Colombia and Dominican Republic (see Exhibit 6).

Exhibit 6: Private investments under the auspices of national broadband plans in LA

Country Private investment initiative

Brazil

Electrosul, a power utility company owned by the Brazilian government, and Telebras, a telecom company in Brazil, reached an agreement in November 2011 to help develop the country’s broadband infrastructure. This partnership will include the exchange of technical services, which aim to link 400 municipalities located on the coast and in the interior by mid-2012.

Colombia

In November 2011, Grupo Salinas won a government contract to implement a fiber-optic project that aims to cover 735 towns by 2014. The government will invest about $230m and the private group about $420m to install and operate the network.

Dominican Republic

Wind Telecom, a broadband operator, pledged in 2011 to invest over $50m over two years to expand and improve the efficiency of its WiMAX-based network. This project has been financed in part by $33m received from the International Finance Corporation, the Mezzanine Infrastructure Fund for Central America, and the Inter-American Investment Corporation. The company also revealed that it had completed a mobile WiMAX launch in partnership with Samsung Electronics.

Sources: Pyramid Research, governments in Latin America

When a government seeks private involvement and investments for broadband development, it undoubtedly looks to all potential sources that would be a good fit, regardless of whether this source is internal or external to its borders. The decision to invite foreigners to contribute to the development of a country can be a contentious issue among some segments of the population, so when this is done governments must take care to crystallize the benefits of outside involvement for the purposes of broadband deployment and capacity building. This strategy can serve multiple purposes: highlighting broadband-related impact in a country for its citizens, fortifying any existing monitoring and evaluation mechanisms for broadband activity and helping government officials to document success stories that can then be used to attract further investment across all industries. Another benefit of this invigorated mobilization is that, in addition to business and innovation-related services, areas that were previously deemed non-commercial are receiving more attention and financial support than ever before through the work of national broadband plans. Education, health, content development and even government services are sectors that are gaining both directly and indirectly from NBP development initiatives. Governments that have integrated these sectors as priorities in their digital development agendas have given a much-needed boost to areas that traditionally lag in this region. As discussed in the case study on the Colombia plan (see Case Studies), the government of Colombia has established an office of the Chief Information Officer (CIO) of Colombia, which will oversee ICT development through e-government services as well as ICT-based services provided across sectors and ministries. In addition, we have seen a number of partnerships with industry players to increase the use of ICT across sectors. For example, there have been partnerships established with Nokia to augment the presence of ICTs, especially broadband connectivity, in schools. Gilat, a connectivity solutions provider, announced in September 2011 that it had signed an agreement with an unnamed government in Latin America to provide 1,800+ SkyEdge 2 VSATs to bring broadband connections to thousands of schools over the next three years. Throughout Latin America, Telefónica has championed the Proniño program, which has promoted socioeducational development by providing grants to poor families in order to send nearly 212,000 children back to school. The company has also promoted the use of ICTs in education by offering teacher training programs and a Web portal called EducaRed to facilitate the use of ICTs in classrooms. Telefónica is also touching the healthcare industry in the region. Currently, they are piloting a phone-based medical advice program so that people without good access to medical personnel can have their questions answered without the hassle of traveling. In Chile, Movistar announced that it would be launching e-health and education-related applications so that the company’s service delivery to customers could become more sophisticated and targeted to their needs. Google established administrative headquarters in Belo Horizante, Brazil, after its affiliate Orkut (a social network) was widely adopted by Brazilians. This localized value-added service helps promote the development and exchange of content specific to the country. E-government services are also becoming quite a popular way to improve the delivery of social services, voter registration and, most importantly, providing access to information previously unobtainable unless someone visited a government office. A common result of this broadband activity in non-commercial areas in the region are narratives about time savings, increased access to services and increased productivity, which further corroborates World Bank economist Qiang’s argument and findings on the contribution of broadband technology to economic development.

C. Public-private partnerships can be a successful, mutually beneficial model to deliver NBP goals and objectives The Inter-American Development Bank (IDB) released a report on the Union of South American Nations (UNASUR) in November 2011 that positioned broadband as the key to development in the region, and stressed that the use of public-private partnerships (PPPs) was necessary to make gains. An equally important concern raised by the IDB is the need to maintain cooperation between governments in Latin America because this has the potential to create more attractive investment packages by aggregating resources for private investors in the region. When governments in Latin America require support to drive broadband development forward, the formation of PPPs represents an opportunity for telecommunications companies to collaborate in a mutually beneficial manner. Earlier we discussed some of the challenges to broadband adoption, namely access, affordability and hardware availability. Often privately held telecommunications companies and affiliated service providers possess the expertise and finances that governments in LA need to help address these issues. Governments can in turn offer exclusive tenders and tax incentives for broadband service delivery, encourage operators with subsidies to expand service to areas of low or non-existing broadband penetration, and lower or eliminate tariffs on broadband-ready hardware importation. PPPs can help create a market climate for broadband that cultivates uptake, which can in turn benefit both parties: Governments gain a connected citizenry and opportunities to use broadband for development purposes, while operators develop new or stronger markets for their products and services. PPPs can be a viable way for an operator to more deeply embed itself into an emerging telecommunications market. This form of partnership will likely contribute to the operator’s revenue generation opportunity. To date, public-private partnerships have been arranged or sought out by a number of governments in Latin America with the objective of achieving universal broadband access for the nation. The finance minister of Peru announced in November 2011 that Peru would spend $1bn on public-private projects in the country by 2012, with a broadband project prioritized for completion by the end of 2011. Peru currently has two additional broadband projects awaiting funding from private investors. To mobilize funding from the private sector, the Peruvian government employs ProInversion, its private investment promotion agency. Venezuela has a similar body called Conapri, which is charged with attracting private interest for its telecommunications market. The use of a promoter to help stimulate the formation of PPPs is an innovative solution that other governments should consider if tapping into private resources is difficult to manage. PPPs not only mobilize financial resources needed to invest in the countries’ infrastructure, but they also provide a platform for stakeholders to collaborate on projects that will have an impact in the development of the sector and the economic development of the country in general. Some additional PPP activity in Latin America includes examples from Chile, Colombia and Brazil (see Exhibit 7).

Exhibit 7: Select public-private partnerships for broadband development in Latin America

Country Partners Area of collaboration

Chile

The Ministry of Digital Development, the Ministry of Economy, the Chilean Association of Information Technology Companies (ACTI), Movistar and the International Data Corporation

The creation of a Digital Development Index (DDI). This index intends to measure ICT evolution and adoption, specifically for both home consumers and businesses, and in the fields of government and education. This will help the Chilean government identify gaps in ICT adoption, including broadband service access. Eventually this index will be introduced into other countries in the LA region.

Colombia The Ministry of Communications, Cisco, Intel, Microsoft, Google, Avantel and Polyvision

The Last Mile Initiative is a large PPP that incubates telecom connectivity in underserved and rural areas.

Brazil The Brazilian government, Oi and Telefónica

In June 2011, Brazilian telecom companies Oi and Telefónica both signed on to support the National Broadband Plan, and each operator has agreed to offer broadband services that are more economical to customers in the country.

Sources: Pyramid Research, governments in Latin America

As governments and operators explore developing (additional) ways that public-private partnerships can help them realize broadband-related goals, each stakeholder should consider innovative actions that will produce long-term impact of advantage to all.

CASE STUDY: Colombia sets ambitious goals to increase access to broadband Internet

The government of Colombia launched its national broadband plan, “Vive Digital,” in October 2010. Based on a clear framework aiming to build a strong digital ecosystem in the country by 2014 (see Exhibit 8), the plan makes both supply (infrastructure) and demand (services, applications and users) considerations to achieve its goals. By focusing on these key action areas in coordination with all interested parties in the government and the sector, the government expects to achieve a number of ambitious targets for Colombia, including the following:

Increase the number of households connected to the Internet from 27% to 50%

Increase the number of SMEs connected to the Internet from 7% to 50%

Increase the number of municipal areas with access to fiber networks from 200 to 700

Increase the number of Internet connections (fixed and mobile) from 2.2m to 8.8m (about four times the number of subscriptions today)

Continue to increase the deployment of telecenters in the country

Connect 94% of all schools to the Internet and provide ICT training to 80% of all teachers

Increase access to banking by facilitating the use of mobile finance to 50% of users

These goals will be achieved by promoting PPPs as a means to increase investment in the country’s infrastructure, especially in rural areas, by eliminating regulatory and tax barriers (including those on equipment), by promoting and stimulating the demand for ICTs, and by increasing government use of ICTs to demonstrate their utility to the population as a whole. In fact, the government of Colombia has established an office of the country’s Chief Information Officer (CIO), charged with mobilizing the use of broadband technology.

The plan’s coordinators organized and benefited from the concerted participation of ministries across all sectors of the economy, which were engaged in the planning process and have aligned their projects and initiatives with the national plan. The Ministry of Communications currently oversees 35 projects deemed critical or with high impact to the development of the ecosystem, including the recent project to award a significant financial investment to the development of the nation’s fiber network. Projects are funded through the ICT Fund (i.e., the country’s universal access fund supported with contributions of 5% of operators’ revenues), as well as the other ministries’ own budgets for ICT initiatives. Colombia’s Vive Digital reflects several of the key factors in the development of successful national policy plans:

A concrete set of achievable goals and targets,

The commitment by the government for specific investments and regulatory action to facilitate and promote development of the sector’s infrastructure,

The coordinated effort, commitment and dedication by all involved at the national level, and

The implementation of a transparent process for decision making and ongoing assessment to revise and update the plan with public input and experience.

With positive results so far, Colombia’s Vive Digital reflects the need to have realistic short-, medium- and long-term goals that will allow the government to continue to make progress toward meeting the plan’s goals.

CASE STUDY: Chile demonstrates its commitment to UAS by setting clear objectives and seeking assistance from the private sector Consistent efforts toward universal access in the past 10 years have helped make Chile the highest ranked country from Latin America in the World Economic Forum index. The “Digital Development Strategy 2007-2012” is the Chilean government’s ambitious plan to achieve digital inclusion in a country that already has one of the highest mobile penetration rates in Latin America. Under the government plan:

• Broadband access will be enabled for 2.3m people and to 90% of rural areas • The development of business incubators will be made to promote the growth of SMEs in

Chile and to provide ICT skills training for entrepreneurs • E-government services will become more ubiquitous • Chile will obtain the goal of having at least one computer for every 10 students in the

country To support the above initiatives, it is expected that $100m, of which 70% will come from Chile’s Telecoms Development Fund, will be needed. The Committee of Ministers for Digital Development will also be expanded from five to nine members. A follow up to the “Digital Development Strategy 2007-2012,” the “Digital Action Plan 2010-2014” aims to transform Chile into a knowledge society. The axes of this new plan have shifted focus to:

The modernization of the Chilean state through increased efficiency in the delivery of government services through utilization of digital platforms that are clear and easy to use

The deepening of the use of ICTs in every sector of Chilean society, including health, education, innovation and job creation

The development of a partnership between the Chilean government, the Chilean Association of Information Technology Companies (ACTI), Movistar and the International Data Corporation resulted in a Digital Development Index to monitor the levels of evolution and adoption of ICTs starting in 2011. This index should provide helpful indicators as Chile strives to make progress in universal access in the next few years.

CASE STUDY: Brazil aims to reach universal access to broadband Internet with a minimum of 1Mbps at R$35 per month The Brazilian National Broadband Plan ― Programa Nacional de Banda Larga (PNBL) ― was officially launched in May 2010 as a government initiative to promote and facilitate the development of broadband infrastructure, and consequently to increase access to broadband Internet to 40m households, to 100% of hospitals and schools in rural areas, to 100% of all public institutions, and the deployment of 100,000 new telecenters with free access across the

country. According to the plan, the key objectives are:

To create opportunity

To increase socioeconomic development

To promote digital inclusion

To reduce social and regional inequality

To promote employment and income generation

To augment e-government services and facilitate its use by citizens

To promote ICT capacity and training to the population

To increase Brazil’s technological competitiveness

Key to achieving these objectives are: the expansion of the network and coverage, the increase in minimum bandwidth capacity to 1Mbps, and lowering broadband prices in the country to at most R$35 per month. The government has also restructured Telebras, a state-owned operator, to become a national backbone operator and provide wholesale broadband services on an open access basis. The goal of the government is to avoid vertical integration and create opportunities for public-private partnerships in the development of fiber-optic infrastructure, particularly in remote areas. Therefore, and based on extensive consultations conducted with key stakeholders under the “Digital Brazil Forum,” the plan rests on four key pillars of action (see Exhibit 9), and the government is working in a coordinated way with public and private industry players to develop programs and projects that will allow for the implementation of the plan and the achievement of the plan’s goals.

National broadband plans (NBPs) have been introduced in several Latin America countries and provide clear road maps and targets for the sector to develop in a coordinated and fully participatory way. NBPs raise the profile of the ICT sector in the context of the countries’ overall socioeconomic development plans and are critical to demonstrate a country’s commitment to universal access and consequently the Information Society.

Plans developed in consultation with all stakeholders ― regulators, operators, government ministries across sectors and civil society ― are more likely to be successful because all parties have a vested interest in the implementation and successful outcome of the plan.

Public-private partnerships provide unique opportunities for governments and operators to collaborate and maximize resources, which would otherwise be insufficient to reach desired expansion of the infrastructure and adoption of services, especially in remote and rural areas.

NBPs provide guidance to the sector to address the access gap and ensure that access to and use of ICTs is a right of all citizens and a reality to all types of institutions (from hospitals and schools to SMEs).

Recommendations

Governments — Develop clear national broadband plans by engaging all stakeholders in the process, from the early planning stages through the implementation of projects and programs. Governments and their representatives should ensure that the ICT sector has a clear road map for its development and for its contribution to the overall progress and growth in the country.

Operators — Be active participants in the NBP development process because you are likely to make significant investments but are also likely to benefit from increased investment resources and consequently additional income-generating opportunities.

Regulators — Take responsibility for the critical role in paving the way to promote and facilitate development of infrastructure, the sharing of such investments (through sharing mechanisms and open-access solutions) and the elimination of any barriers to competition.

Civil society— It needs to be involved in the NBP development process to ensure that the specific wants and needs all consumers (rural, urban, women, men, young, older, physically challenged, lower or medium income) are considered in the process and addressed by the critical projects and programs to be implemented.

Related resources Mobile Social Networks Set to Experience Rapid Growth as Mobile Penetration Rates Rise Telecom Insider published October 2011 Pyramid Research believes mobile devices will become the platform of choice for accessing social networking sites in LA. To catch up with the developed world, where mobile social networking is increasing business opportunities, there are some changes that Latin American operators and device manufacturer need to make. This report discusses those changes and how much progress LA operators have made thus far.

Brazil: Mobile Data and Prepaid Mobile Drive Unprecedented Telecom Revenue Growth by 2015 Country Intelligence Report published March 2011 Pyramid Research estimates that total telecom revenue in Brazil reached $67.4bn by year-end 2010, up $13.4bn from 2009, and will total $88.7bn in 2015, with a CAGR of 5.6%, fueled by expansion in mobile data services and broadband Internet access.

Operators Take Mobile Banking to the Masses, with 65% Annual Growth Expected until 2015 Telecom Insider published May 2011 With mobile penetration in Latin America close to 100% and voice services barely showing organic growth, mobile operators are now open to mobile financial services. Pyramid Research believes that Latin America has achieved the right conditions to smoothly increase the uptake of mobile financial services, including banking and payments. Currently, around 18m users in Latin America use financial services from their mobile devices and this number may rise to more than 140m by 2015.

Why Cloud Computing Services Are Good for Operators and SMEs in Latin America Telecom Insider published July 2011 Cloud computing can help operators in Latin America reduce their internal costs and develop competencies that can help them sell these same services to small and midsize clients needing to become leaner and more agile in a global marketplace. And since cloud computing rides on top of the broadband networks being built out by operators today, it provides another important way for operators to achieve a greater return on their investment. This report examines what cloud computing is, the framework behind this model and identifies the main drivers behind its adoption in Latin America. Three case studies look at fixed operators in Mexico that offer cloud services with an eye to what they understand to be cloud computing, the main reasons they adopted cloud computing, and the different services they offer.

TV Anywhere: How the Internet and Mobile Technologies Will Change the Pay-TV Industry Research Report published October 2010 In this report, Pyramid Research analyzes trends and strategies related to IPTV, which include how emerging Internet TV and established pay-TV offerings are both parts of a broader market dynamic that places content providers, Internet access providers, pay-TV service providers and even consumer electronics suppliers together as collaborators and competitors, sometimes both at once. It analyzes technological and behavioral trends for viewing content on a wide variety of devices, describes and compares the latest devices and software for delivering and distributing content and examines Internet TV business models in detail. Developments and opportunities related to the growth and implications of Internet TV for all of the players are also discussed.

Global Mobile Data Forecast Forecasts published quarterly Updated on a quarterly basis, this Mobile Data Forecast product provides a complete picture of demand trends for the global market. The Excel output includes five years of historical data and five years of market projections for metrics such as penetration, mobile subscriptions (by type of package, by operator or MVNO and by network technology), users of specific data services (SMS, music, etc.), MOU, ARPS (by operator, by subscription type, by service, by application) and revenue (by messaging and non-messaging applications). The Forecast is based on extensive field research and uses a consistent methodology, aiming to capture the total spending on mobile data services on an aggregate global level. Data from these Forecasts is available online for subscribers to our DataTracker service.

To learn more about Pyramid Research’s product offerings and how they can be of service to your company, please contact [email protected] or visit us on the Web at

SUBSCRIBER LICENSE AGREEMENT Any Pyramid Research Insider report ("Report") and the information therein are the property of or licensed to Pyramid Research and permission to use the same is granted to annual or single-report subscribers ("Subscribers") under the terms of this Subscriber License Agreement ("Agreement") which may be amended from time to time without notice. When requesting a Report, Subscriber acknowledges that it is bound by the terms and conditions of this Agreement and any amendments thereto. Pyramid Research therefore recommends that you review this page for amendments to this Agreement prior to requesting any additional Reports. OWNERSHIP RIGHTS All Reports are owned by Pyramid Research and protected by United States Copyright and international copyright/intellectual property laws under applicable treaties and/or conventions. Subscriber agrees not to export any Report into a country that does not have copyright/intellectual property laws that will protect Pyramid Research’s rights therein. GRANT OF LICENSE RIGHTS Pyramid Research hereby grants Subscriber a personal, non-exclusive, non-refundable, non-transferable license to use the Report for research purposes only pursuant to the terms and conditions of this Agreement. Pyramid Research retains exclusive and sole ownership of each Report disseminated under this Agreement. Subscriber agrees not to permit any unauthorized use, reproduction, distribution, publication or electronic transmission of any Report or the information/forecasts therein without the express written permission of Pyramid Research. Subscribers purchasing site licenses may make a Report available to other persons from their organization at the specific physical site covered by the agreement, but are prohibited from distributing the report to people outside the organization, or to other sites within the organization. Enterprise-level Subscribers, however, may make a Report available for access on intranets or closed computer systems for internal use under their service agreements with Pyramid Research. DISCLAIMER OF WARRANTY AND LIABILITY Pyramid Research has used its best efforts in collecting and preparing each Report. Pyramid Research, its employees, affiliates, agents and licensors do not warrant the accuracy, completeness, currentness, noninfringement, merchantability or fitness for a particular purpose of any reports covered by this agreement. Pyramid Research, its employees, affiliates, agents or licensors shall not be liable to subscriber or any third party for losses or injury caused in whole or part by our negligence or contingencies beyond Pyramid Research’s control in compiling, preparing or disseminating any report or for any decision made or action taken by subscriber or any third party in reliance on such information or for any consequential, special, indirect or similar damages, even if Pyramid Research was advised of the possibility of the same. Subscriber agrees that the liability of Pyramid Research, its employees, affiliates, agents and licensors, if any, arising out of any kind of legal claim (whether in contract, tort or otherwise) in connection with its goods/services under this agreement shall not exceed the amount paid to Pyramid Research for use of the report in question. About Pyramid Research Pyramid Research (www.pyramidresearch.com) offers practical solutions to the complex demands our clients face in the global communications industry. Our analysis is uniquely positioned at the intersection of emerging markets, emerging technologies and emerging business models, powered by the bottom-up methodology of our market forecasts for more than 100 countries — a distinction that has remained unmatched for more than 25 years. As a telecom research arm of the Light Reading Communications Network (www.lrcn.com), Pyramid Research contributes to the only integrated business information platform serving the $4 trillion global communications industry.