18

1 Q1 2006 RESULTS 10 May 2006

1

Q1 2006 RESULTS10 May 2006

2

Industry

• Crude oil up 35% y-o-y (and 13% vs last quarter) due to political tension and strong demand from China and India

• Refining margins off to a slow start in January, then gradually recovering in February and March

Overall, refining margins below last year levels and expected 2006 average (strong in May)

• Marketing volumes stable vs last year: increase in gasoil volumes offset by gasoline decline

Margins in line with Q1 2005 levels, but below last year average

Oil Price

Refining

Marketing

3

Operational Results - Refining

• Q1 2006 refining margins lower than industry because of a temporary loss of yields due to:

Major maintenance stop – 36 days, 28 of which in March and 8 in April – impacting both total production and yields

– Yields expected to be partially recovered in the forthcoming months

Power distribution grid black-out affecting yields in January, partially recovered in February (previous black-outs occurred in 2003 and 2005)

• Bitumen production recovery – in line with budget – though winter market is traditionally not significant

4

Operational Results - Marketing

• Retail sales far above Q1 2005 following IP network acquisition

Breakdown between two brands shows above-market performance for api and a partial retrenchment for IP

• Bitumen sales recovery thanks to restored production

• Retail margins in line with Q1 2005, but below last year average.

Usually, less favourable performance in refining is balanced by higher marketing margins: the anomaly that took place in Q1 2006 was mainly due to sudden spike in commodity prices, coupled with a weak domestic economic environment resulting in consumers’ lack of confidence

• Wholesale margins in line with expectations and in line with last year

5

Operational Results - Powergen

• Major maintenance stop (36 days from end of January to beginning of March) impacting on total production

• Better performance than Q1 2005 thanks to improved plant efficiency

• Higher tariff following the increase in the fuel component

6

Operational Results – Summary Overview

• In summary, we have experienced an unfavourable R&M environment – though gradually improving – as well as the effect of the major maintenance at both the refinery and the power generation plant

• Other costs are in line with budget thanks to a strict cost discipline

7

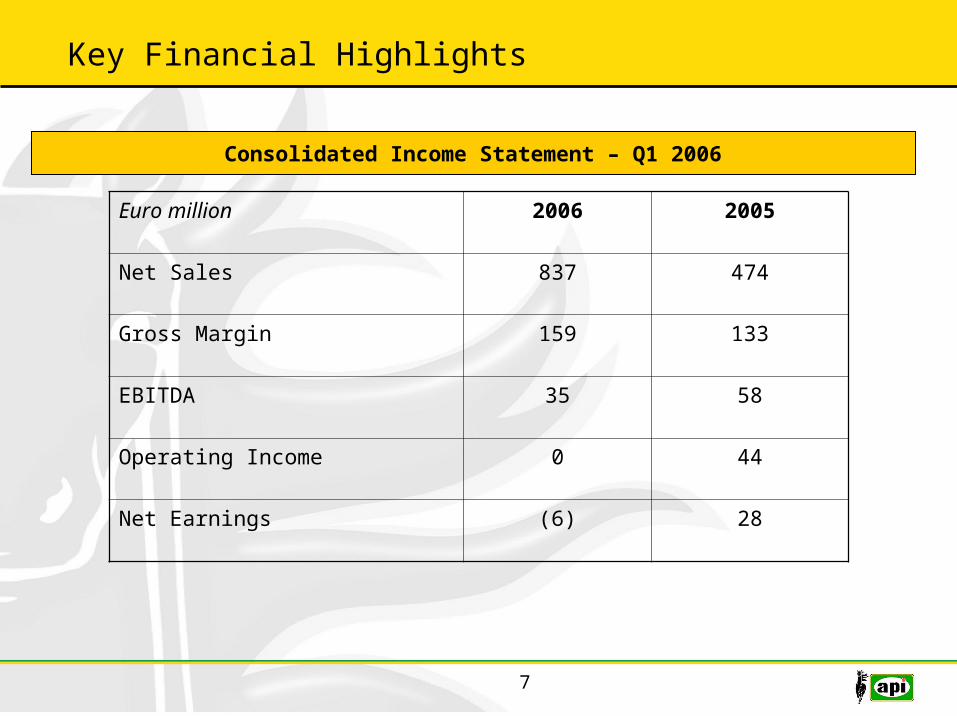

Key Financial Highlights

Euro million 2006 2005

Net Sales 837 474

Gross Margin 159 133

EBITDA 35 58

Operating Income 0 44

Net Earnings (6) 28

Consolidated Income Statement – Q1 2006

8

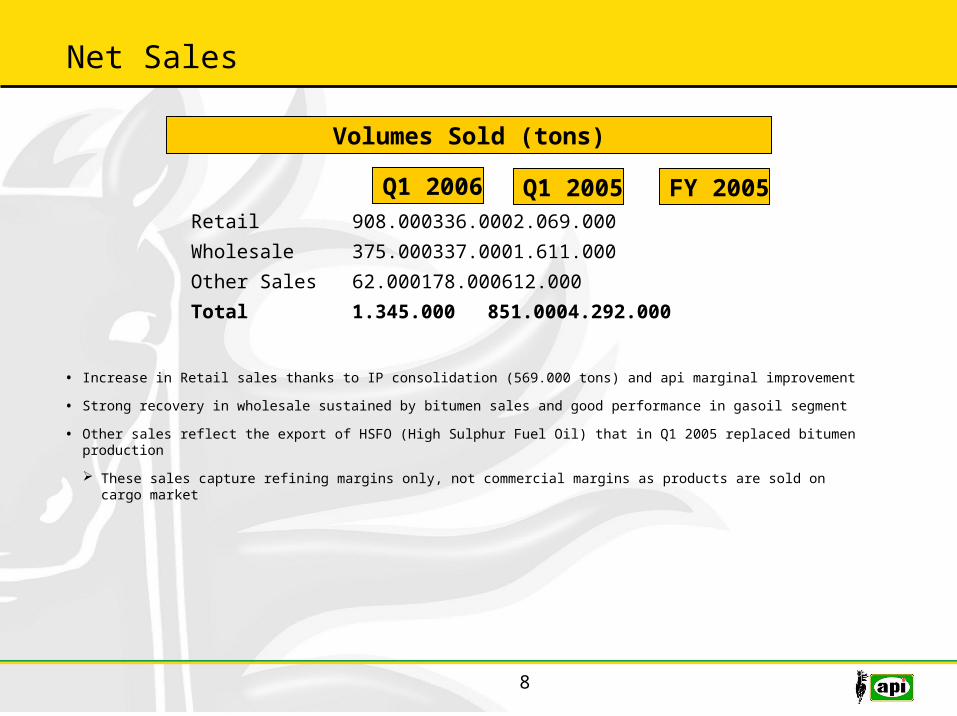

Net Sales

• Increase in Retail sales thanks to IP consolidation (569.000 tons) and api marginal improvement

• Strong recovery in wholesale sustained by bitumen sales and good performance in gasoil segment

• Other sales reflect the export of HSFO (High Sulphur Fuel Oil) that in Q1 2005 replaced bitumen production

These sales capture refining margins only, not commercial margins as products are sold on cargo market

Volumes Sold (tons)

Retail 908.000336.0002.069.000Wholesale 375.000337.0001.611.000Other Sales 62.000178.000 612.000Total 1.345.000851.0004.292.000

Q1 2006 Q1 2005 FY 2005

9

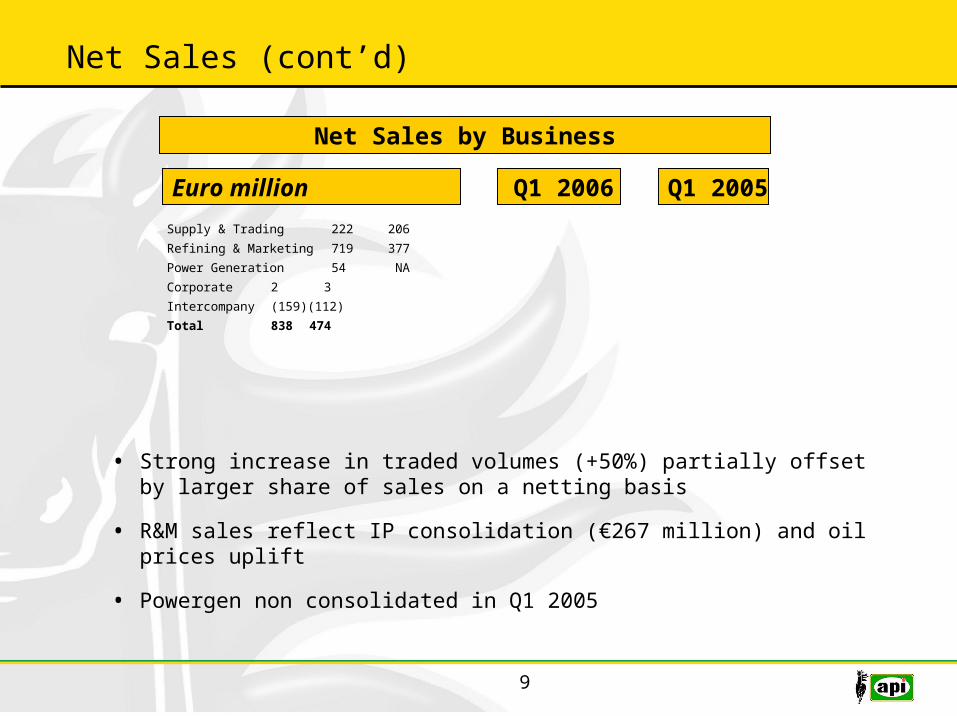

• Strong increase in traded volumes (+50%) partially offset by larger share of sales on a netting basis

• R&M sales reflect IP consolidation (€267 million) and oil prices uplift

• Powergen non consolidated in Q1 2005

Net Sales (cont’d)

Net Sales by Business

Supply & Trading 222 206Refining & Marketing 719 377Power Generation 54 NACorporate 2 3Intercompany (159) (112)Total 838 474

Q1 2006 Q1 2005Euro million

10

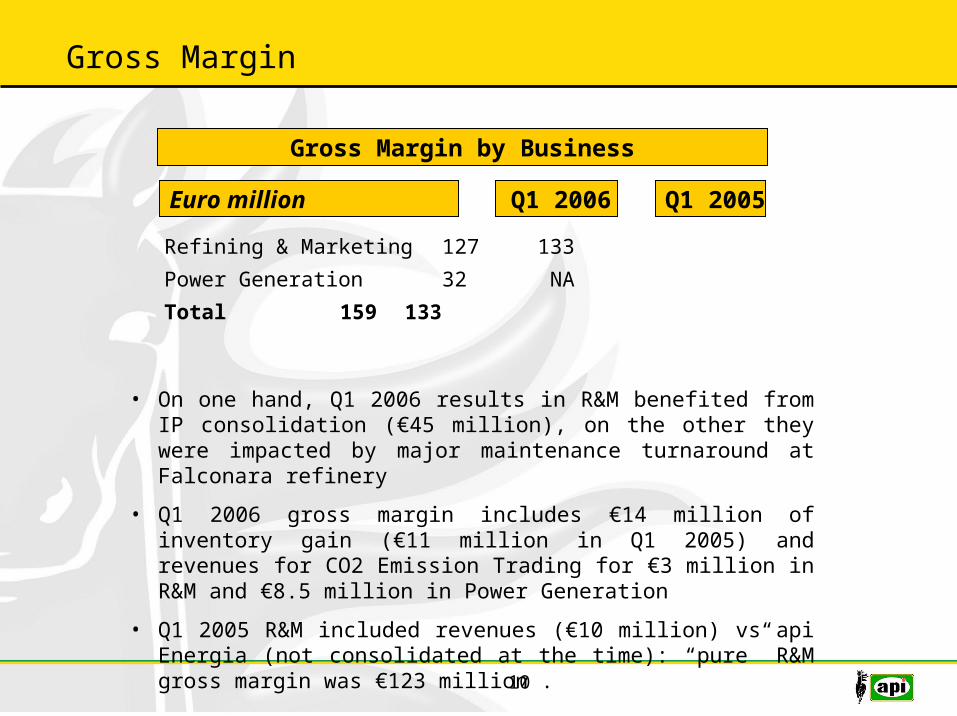

• On one hand, Q1 2006 results in R&M benefited from IP consolidation (€45 million), on the other they were impacted by major maintenance turnaround at Falconara refinery

• Q1 2006 gross margin includes €14 million of inventory gain (€11 million in Q1 2005) and revenues for CO2 Emission Trading for €3 million in R&M and €8.5 million in Power Generation

• Q1 2005 R&M included revenues (€10 million) vs api Energia (not consolidated at the time): “pure” R&M gross margin was €123 million .

Gross Margin

Gross Margin by Business

Refining & Marketing 127 133Power Generation 32 NATotal 159 133

Q1 2006 Q1 2005Euro million

11

EBITDA

EBITDA by Business

Supply & Trading 0 0Refining & Marketing 24 64Power Generation 25 NACorporate (14) (6)Total 35 58

Q1 2006 Q1 2005Euro million

• Q1 2006 results in R&M were impacted by one time costs due to major maintenance turnaround at Falconara refinery and at the IGCC plant (included in the R&M costs and then charged back to api energia on an even basis in the following months)

• Operating costs are in line with budget

12

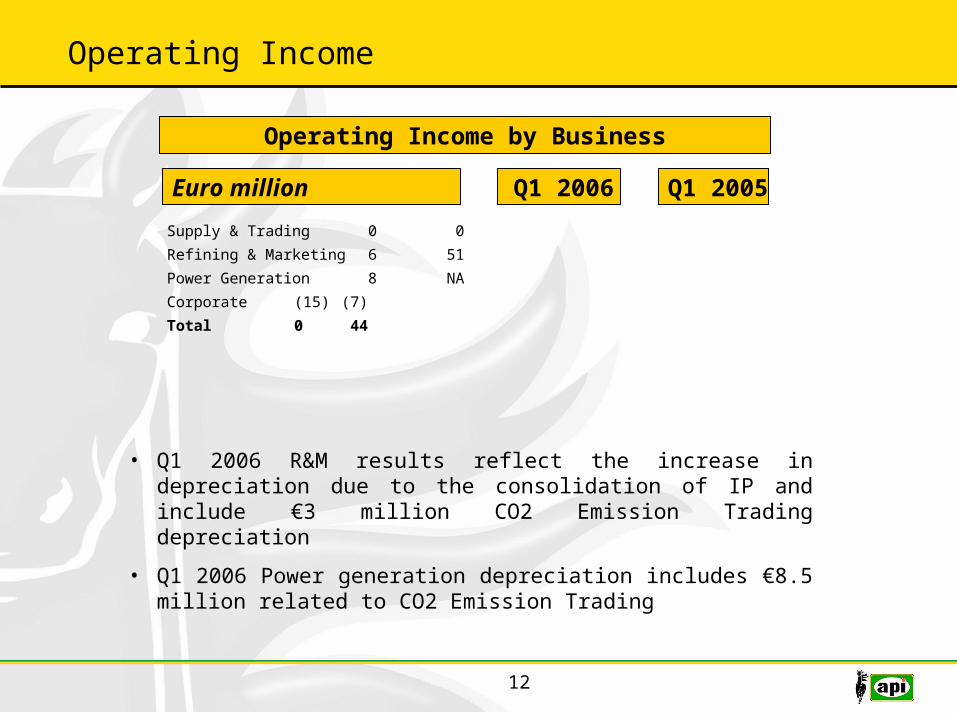

Operating Income

Operating Income by Business

Supply & Trading 0 0Refining & Marketing 6 51Power Generation 8 NACorporate (15) (7)Total 0 44

Q1 2006 Q1 2005Euro million

• Q1 2006 R&M results reflect the increase in depreciation due to the consolidation of IP and include €3 million CO2 Emission Trading depreciation

• Q1 2006 Power generation depreciation includes €8.5 million related to CO2 Emission Trading

13

Net Income

Operating Income 0 44Net financial charges (8) 1Tax 2 (17)Net Income (6) 28

Q1 2006 Q1 2005Euro million

• Q1 2006 results are affected by the increase of financial expenses due to the acquisition and consolidation of IP and api Energia

In year 2005, api energia was accounted using net equity method, thus reducing financial charges by around €3 million

• Tax rate is only 26% due to IRAP calculation effect: no effect on an annual basis

14

Cash Flow - Net Financial Position

Cash Flow

Initial Net Financial Position (887) (357)Net Profit/(Loss) (6) 28Depreciation ad Amortization 35 14Capex (58) (11)Delta Working Capital 59 69Net Financial Position (857) (257)

Q1 2006 Q1 2005Euro million

Net financial position improved by €30 million in Q1 2006

• Working capital: recovery of the anticipated excise taxes and VAT partially offset by higher inventory levels due to the refinery stop for major maintenance

• Capex: high investments due to refinery and IGCC maintenance and acquisition of the Di.Car. retail network (€20 million)

15

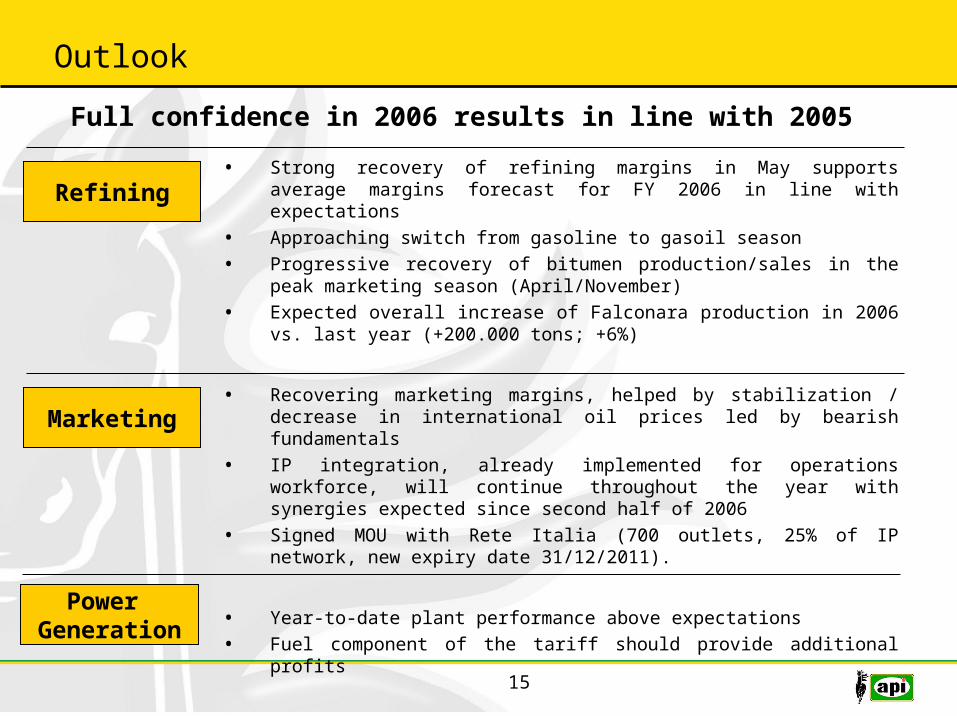

Outlook

• Strong recovery of refining margins in May supports average margins forecast for FY 2006 in line with expectations

• Approaching switch from gasoline to gasoil season• Progressive recovery of bitumen production/sales in the peak

marketing season (April/November)• Expected overall increase of Falconara production in 2006 vs. last

year (+200.000 tons; +6%)

• Recovering marketing margins, helped by stabilization / decrease in international oil prices led by bearish fundamentals

• IP integration, already implemented for operations workforce, will continue throughout the year with synergies expected since second half of 2006

• Signed MOU with Rete Italia (700 outlets, 25% of IP network, new expiry date 31/12/2011).

• Year-to-date plant performance above expectations• Fuel component of the tariff should provide additional profits

Power Generation

Refining

Marketing

Full confidence in 2006 results in line with 2005

16

Appendices

17

Marketing Margins vs Brent: Gasoline

70

90

110

130

150

170

190

210

230

250

1-Jan-02 1-Jul-02 1-Jan-03 1-Jul-03 1-Jan-04 1-Jul-04 1-Jan-05 1-Jul-05 1-Jan-06

Brent Margin - Gasoline

Gross Marketing MarginsVolatility in the short-term (on a monthly basis)

Stability in the medium term (on an annual basis)

Note: based on Platts and retail prices from Staffetta Quotidiana

18

Marketing Margins vs Brent: Gasoil

70

90

110

130

150

170

190

210

230

250

1-Jan-02 1-Jul-02 1-Jan-03 1-Jul-03 1-Jan-04 1-Jul-04 1-Jan-05 1-Jul-05 1-Jan-06

Brent Margin - Gasoil

Gross Marketing MarginsVolatility in the short-term (on a monthly basis)

Stability in the medium term (on an annual basis)

Note: based on Platts and retail prices from Staffetta Quotidiana