23

Q1 2021 RESULTS INVESTOR & ANALYST PRESENTATION May 12, 2021 Dr. Cornelius Patt, CEO

Q1 2021 RESULTS

INVESTOR & ANALYST PRESENTATION

May 12, 2021

Dr. Cornelius Patt, CEO

ZOOPLUS OPERATES IN A

HIGHLY ATTRACTIVE CATEGORYQ1 2021 Investor & Analyst Call

3

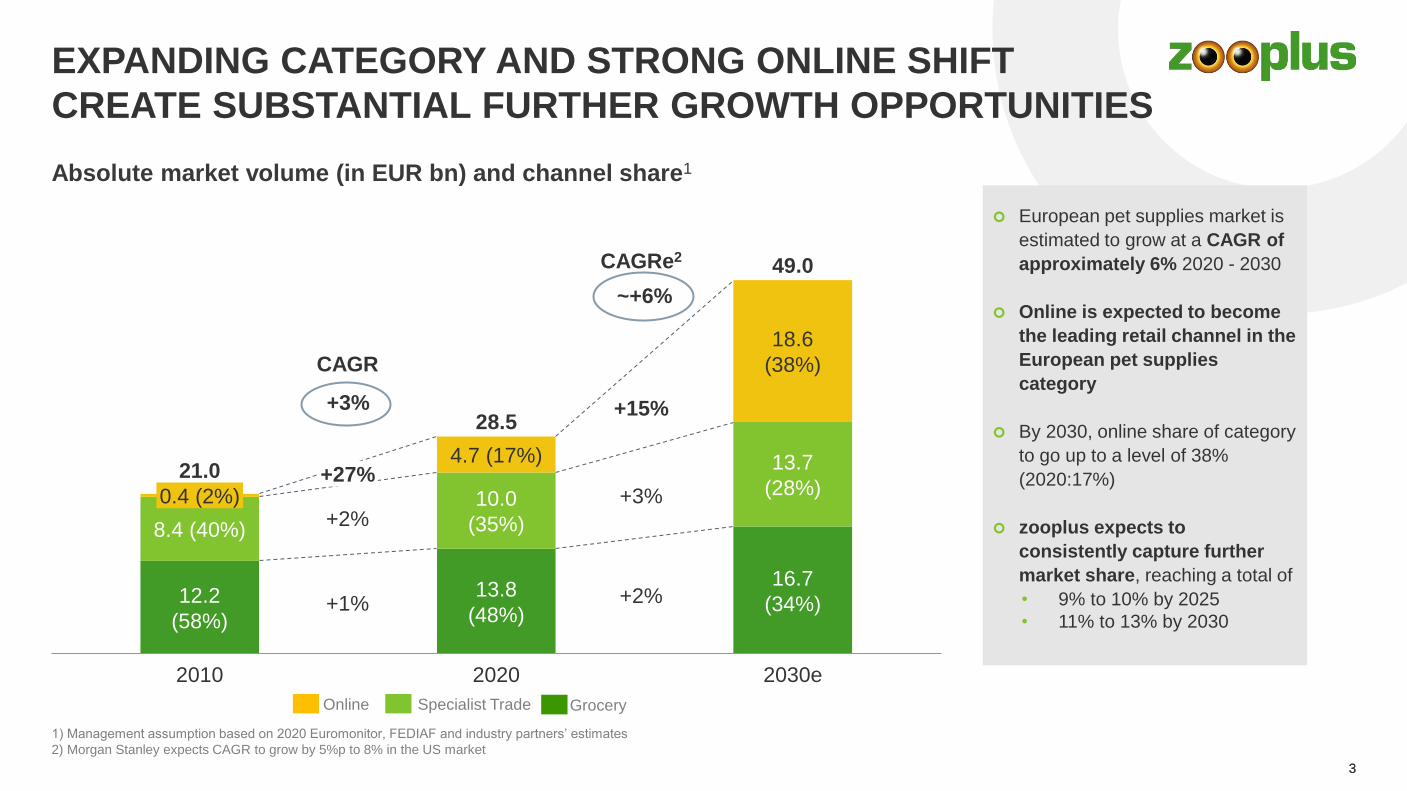

EXPANDING CATEGORY AND STRONG ONLINE SHIFT

CREATE SUBSTANTIAL FURTHER GROWTH OPPORTUNITIES

European pet supplies market is

estimated to grow at a CAGR of

approximately 6% 2020 - 2030

Online is expected to become

the leading retail channel in the

European pet supplies

category

By 2030, online share of category

to go up to a level of 38%

(2020:17%)

zooplus expects to

consistently capture further

market share, reaching a total of

• 9% to 10% by 2025

• 11% to 13% by 2030

Absolute market volume (in EUR bn) and channel share1

Online Specialist Trade Grocery

1) Management assumption based on 2020 Euromonitor, FEDIAF and industry partners’ estimates

2) Morgan Stanley expects CAGR to grow by 5%p to 8% in the US market

3

10.0

(35%)

0.4 (2%)

12.2

(58%)

2020

13.8

(48%)

8.4 (40%)

2010

4.7 (17%)

18.6

(38%)

13.7

(28%)

16.7

(34%)

2030e

21.0

28.5

49.0

+3%

~+6%

+27%

+15%

+2%+3%

+1% +2%

CAGRe2

CAGR

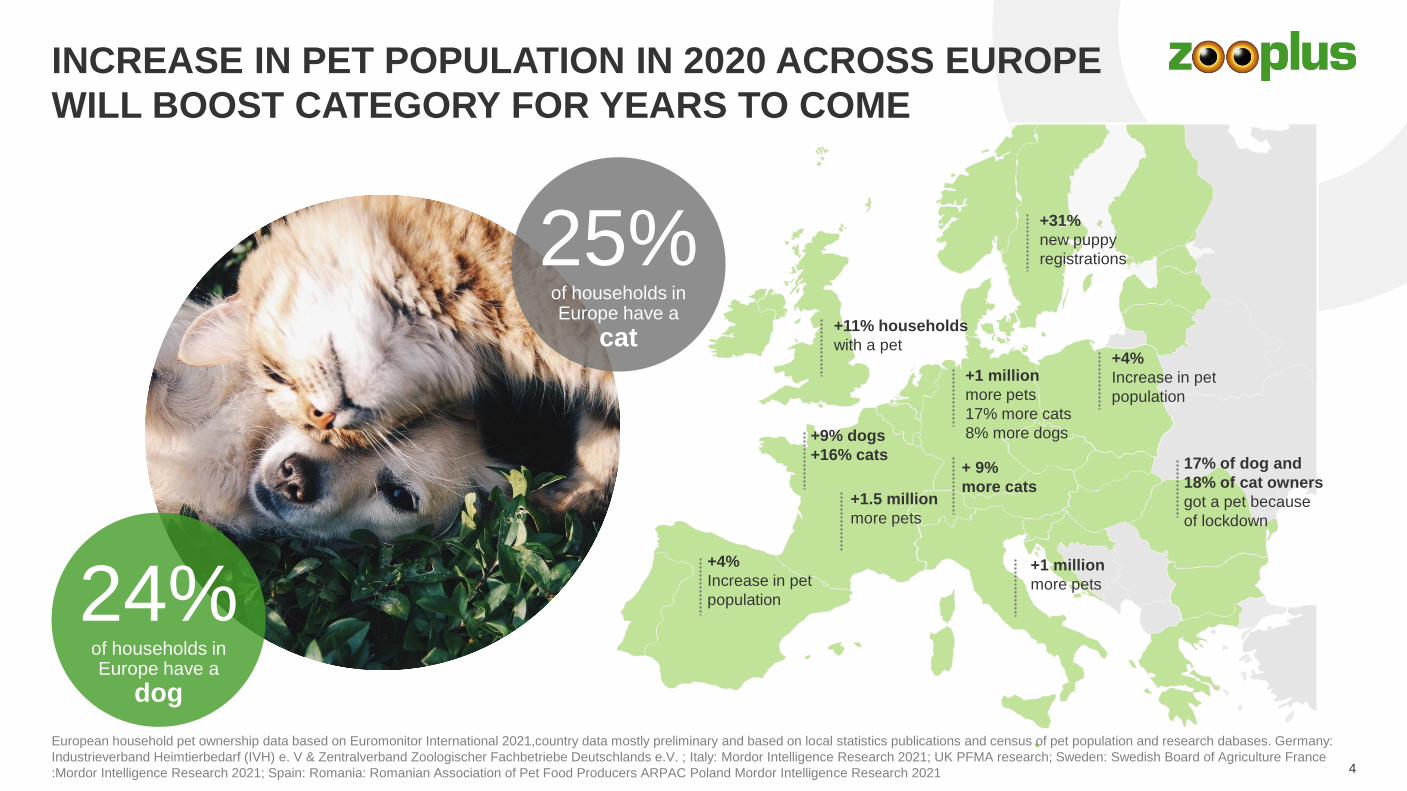

INCREASE IN PET POPULATION IN 2020 ACROSS EUROPE

WILL BOOST CATEGORY FOR YEARS TO COME

4

+1 million

more pets

17% more cats

8% more dogs

+31%

new puppy

registrations

+11% households

with a pet

+1 million

more pets

+ 9%

more cats+1.5 million

more pets

+4%

Increase in pet

population

17% of dog and

18% of cat owners

got a pet because

of lockdown

+9% dogs

+16% cats

+4%

Increase in pet

population

24%of households in Europe have a

dog

25%of households in Europe have a

cat

European household pet ownership data based on Euromonitor International 2021,country data mostly preliminary and based on local statistics publications and census of pet population and research dabases. Germany:

Industrieverband Heimtierbedarf (IVH) e. V & Zentralverband Zoologischer Fachbetriebe Deutschlands e.V. ; Italy: Mordor Intelligence Research 2021; UK PFMA research; Sweden: Swedish Board of Agriculture France

:Mordor Intelligence Research 2021; Spain: Romania: Romanian Association of Pet Food Producers ARPAC Poland Mordor Intelligence Research 2021

OPERATIONAL HIGHLIGHTSQ1 2021 Investor & Analyst Call

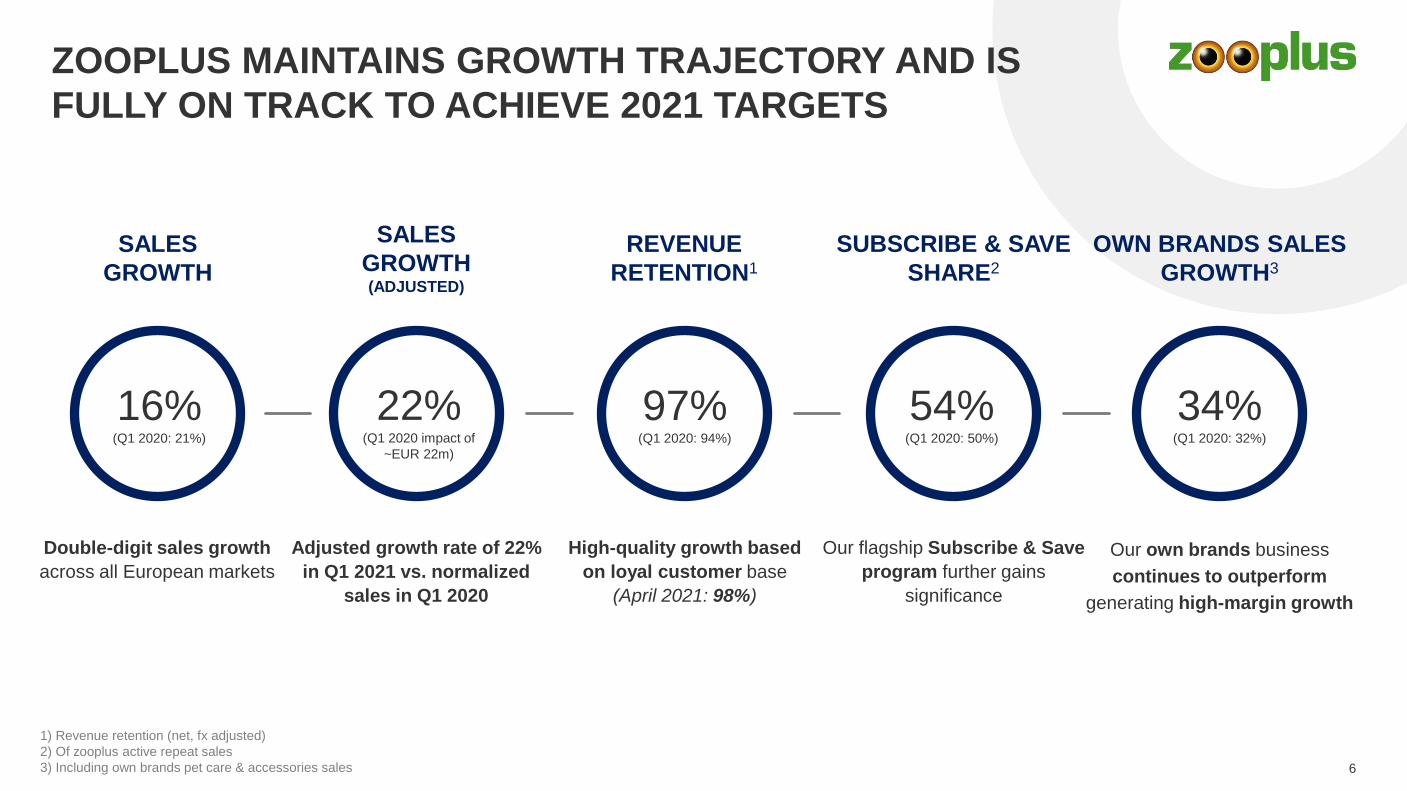

ZOOPLUS MAINTAINS GROWTH TRAJECTORY AND IS

FULLY ON TRACK TO ACHIEVE 2021 TARGETS

6

High-quality growth based

on loyal customer base

(April 2021: 98%)

REVENUE

RETENTION1

Our flagship Subscribe & Save

program further gains

significance

SUBSCRIBE & SAVE

SHARE2

Our own brands business

continues to outperform

generating high-margin growth

OWN BRANDS SALES

GROWTH3

1) Revenue retention (net, fx adjusted)

2) Of zooplus active repeat sales

3) Including own brands pet care & accessories sales

34%(Q1 2020: 32%)

97%(Q1 2020: 94%)

54%(Q1 2020: 50%)

Double-digit sales growth

across all European markets

SALES

GROWTH

16%(Q1 2020: 21%)

SALES

GROWTH (ADJUSTED)

22%(Q1 2020 impact of

~EUR 22m)

Adjusted growth rate of 22%

in Q1 2021 vs. normalized

sales in Q1 2020

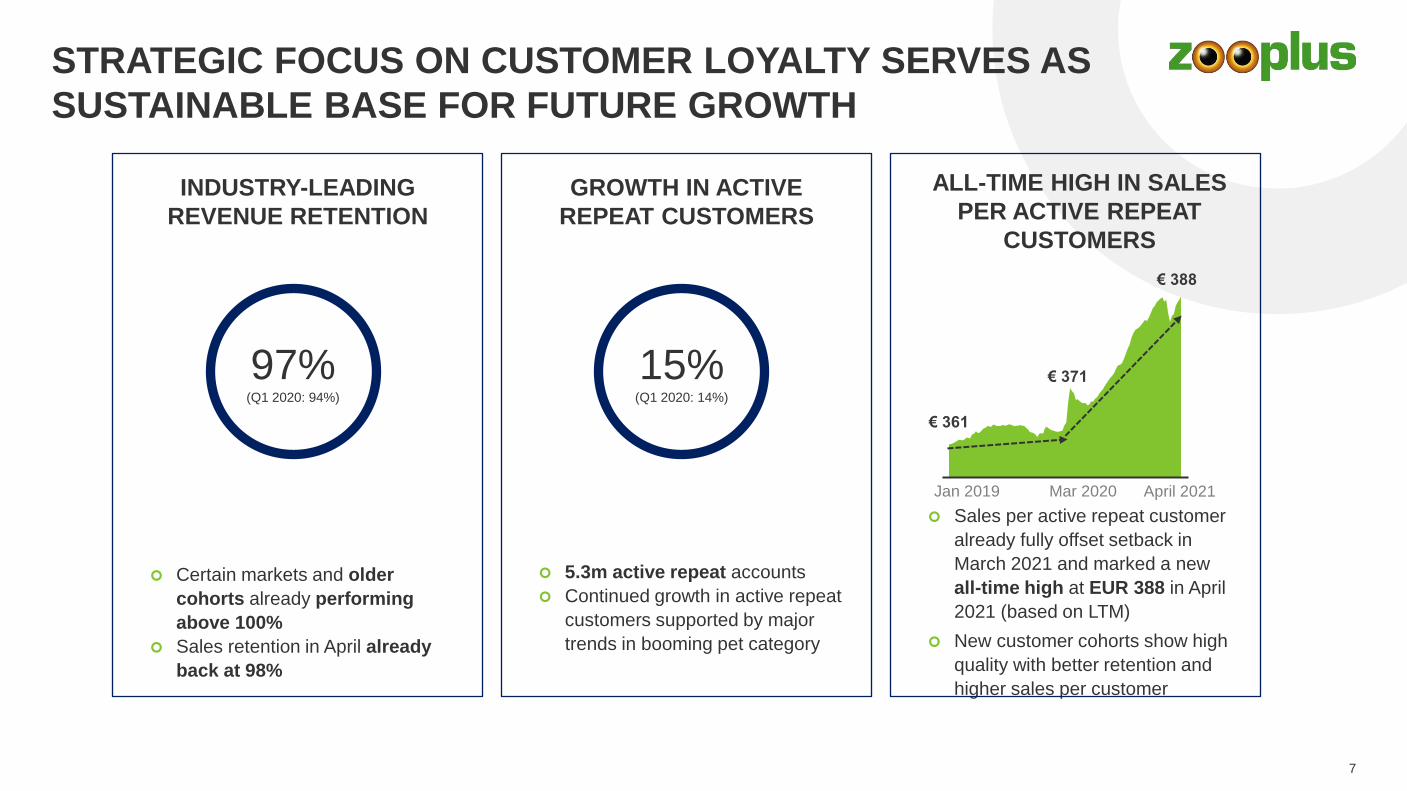

STRATEGIC FOCUS ON CUSTOMER LOYALTY SERVES AS

SUSTAINABLE BASE FOR FUTURE GROWTH

7

5.3m active repeat accounts

Continued growth in active repeat

customers supported by major

trends in booming pet category

GROWTH IN ACTIVE

REPEAT CUSTOMERS

Sales per active repeat customer

already fully offset setback in

March 2021 and marked a new

all-time high at EUR 388 in April

2021 (based on LTM)

New customer cohorts show high

quality with better retention and

higher sales per customer

ALL-TIME HIGH IN SALES

PER ACTIVE REPEAT

CUSTOMERS

Mar 2020Jan 2019 April 2021

€ 361

€ 371

€ 388

(2019: 91%)

99%15%

(Q1 2020: 14%)

Certain markets and older

cohorts already performing

above 100%

Sales retention in April already

back at 98%

INDUSTRY-LEADING

REVENUE RETENTION

(2019: 91%)

99%97%

(Q1 2020: 94%)

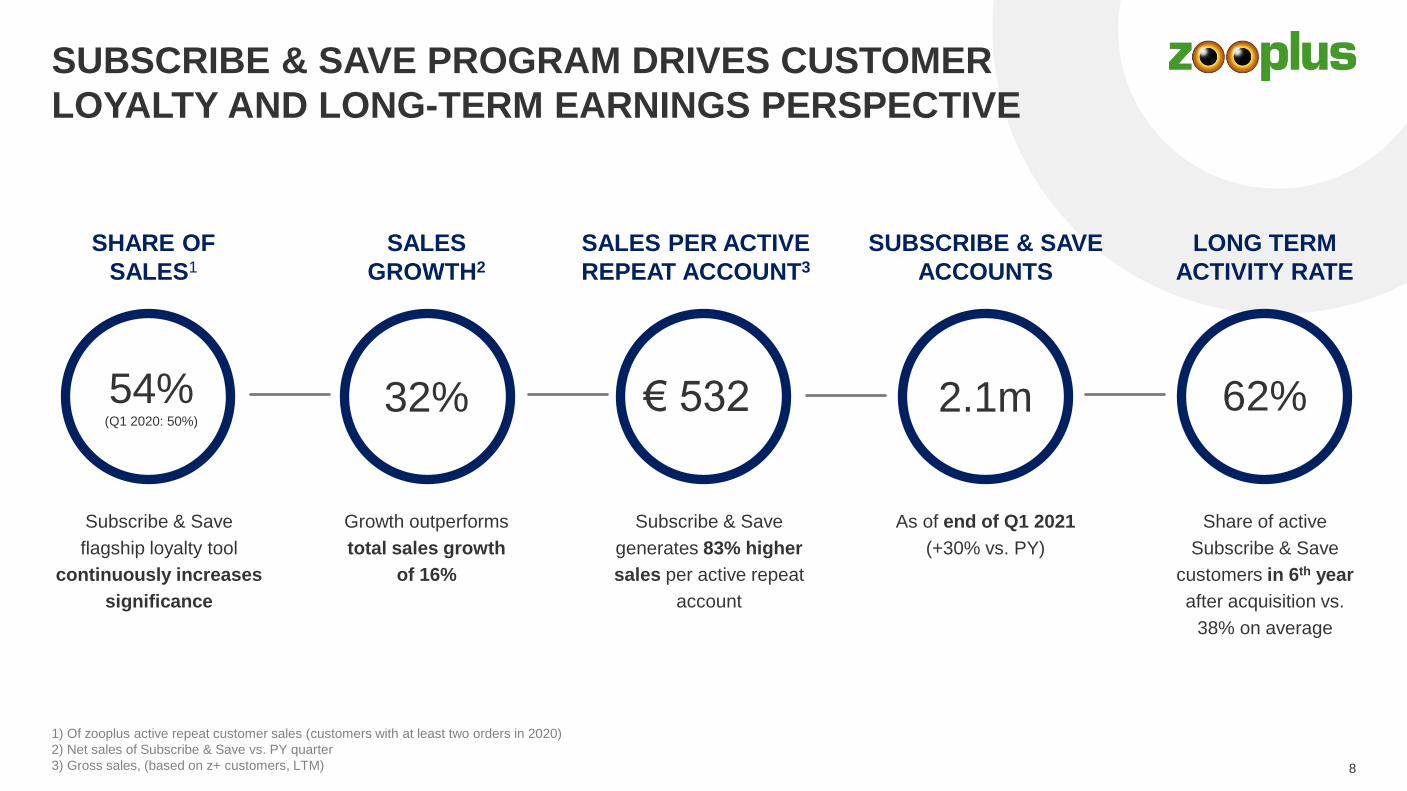

1) Of zooplus active repeat customer sales (customers with at least two orders in 2020)

2) Net sales of Subscribe & Save vs. PY quarter

3) Gross sales, (based on z+ customers, LTM)

SUBSCRIBE & SAVE PROGRAM DRIVES CUSTOMER

LOYALTY AND LONG-TERM EARNINGS PERSPECTIVE

8

Subscribe & Save

flagship loyalty tool

continuously increases

significance

54%(Q1 2020: 50%)

SHARE OF

SALES1

Growth outperforms

total sales growth

of 16%

32%

SALES

GROWTH2

Subscribe & Save

generates 83% higher

sales per active repeat

account

€ 532

SALES PER ACTIVE

REPEAT ACCOUNT3

Share of active

Subscribe & Save

customers in 6th year

after acquisition vs.

38% on average

62%

LONG TERM

ACTIVITY RATE

As of end of Q1 2021

(+30% vs. PY)

2.1m

SUBSCRIBE & SAVE

ACCOUNTS

9

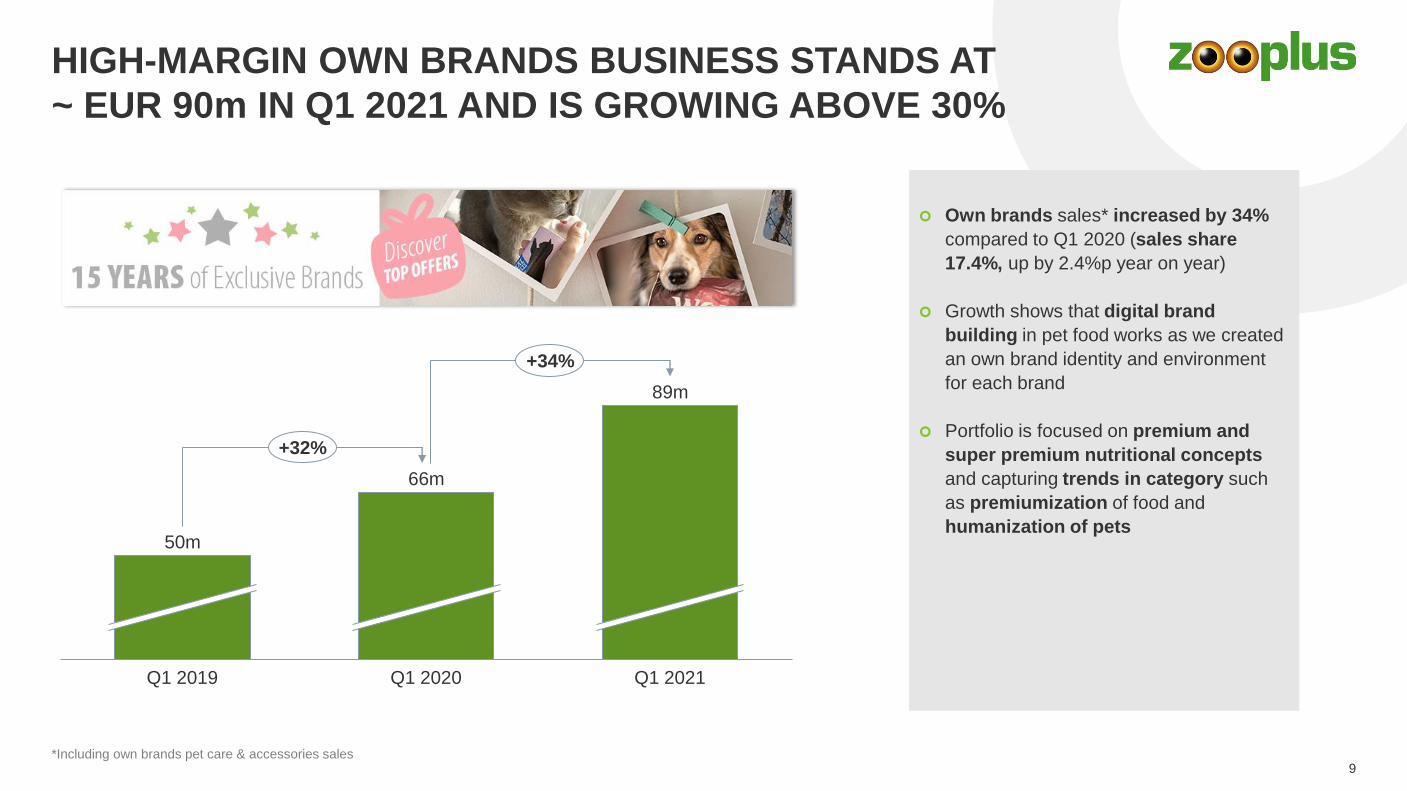

HIGH-MARGIN OWN BRANDS BUSINESS STANDS AT

~ EUR 90m IN Q1 2021 AND IS GROWING ABOVE 30%

Q1 2021Q1 2019 Q1 2020

50m

66m

89m

+32%

+34%

Own brands sales* increased by 34%

compared to Q1 2020 (sales share

17.4%, up by 2.4%p year on year)

Growth shows that digital brand

building in pet food works as we created

an own brand identity and environment

for each brand

Portfolio is focused on premium and

super premium nutritional concepts

and capturing trends in category such

as premiumization of food and

humanization of pets

*Including own brands pet care & accessories sales

FINANCIAL HIGHLIGHTSQ1 2021 Investor & Analyst Call

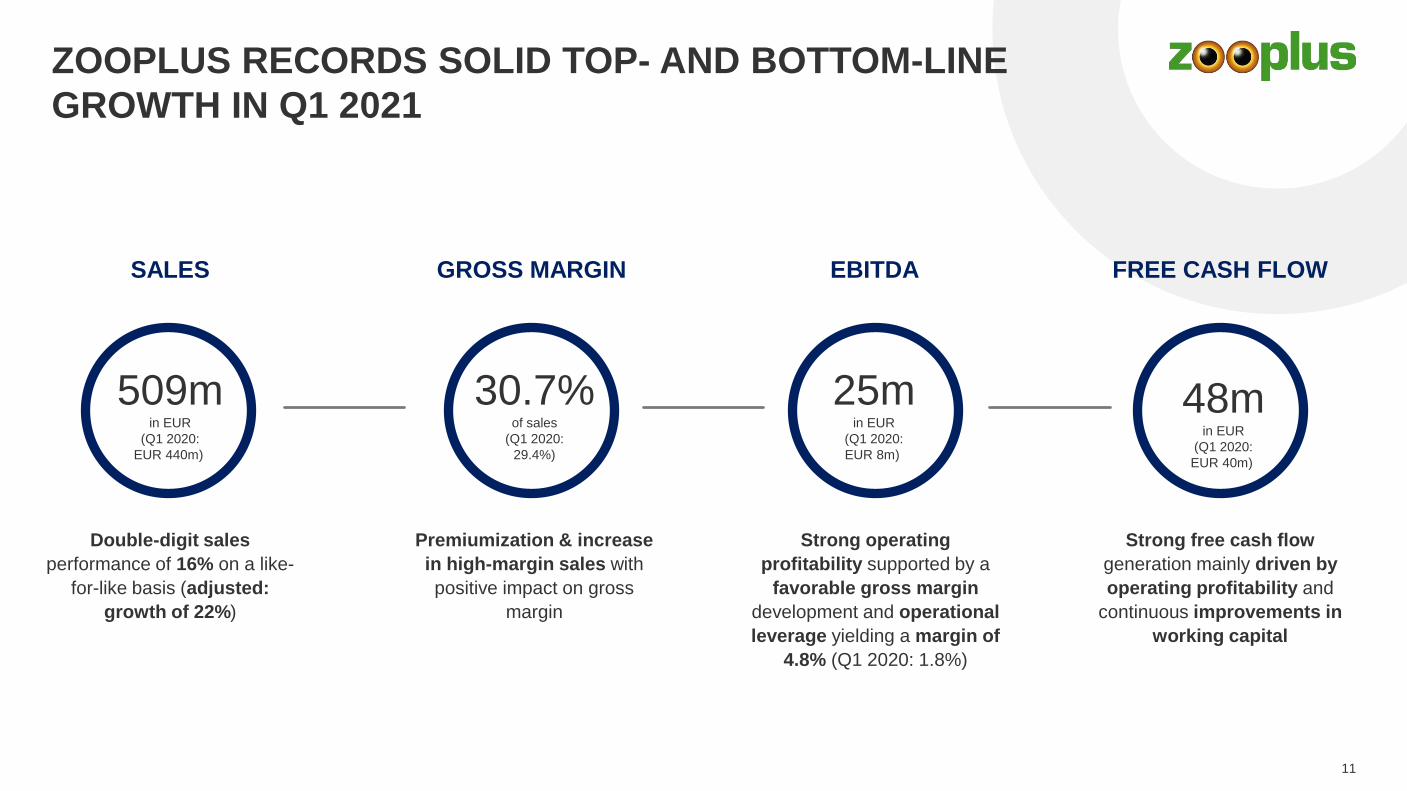

ZOOPLUS RECORDS SOLID TOP- AND BOTTOM-LINE

GROWTH IN Q1 2021

11

Premiumization & increase

in high-margin sales with

positive impact on gross

margin

GROSS MARGIN EBITDA FREE CASH FLOW

48min EUR

(Q1 2020:

EUR 40m)

30.7%of sales

(Q1 2020:

29.4%)

25min EUR

(Q1 2020:

EUR 8m)

Double-digit sales

performance of 16% on a like-

for-like basis (adjusted:

growth of 22%)

SALES

509min EUR

(Q1 2020:

EUR 440m)

Strong operating

profitability supported by a

favorable gross margin

development and operational

leverage yielding a margin of

4.8% (Q1 2020: 1.8%)

Strong free cash flow

generation mainly driven by

operating profitability and

continuous improvements in

working capital

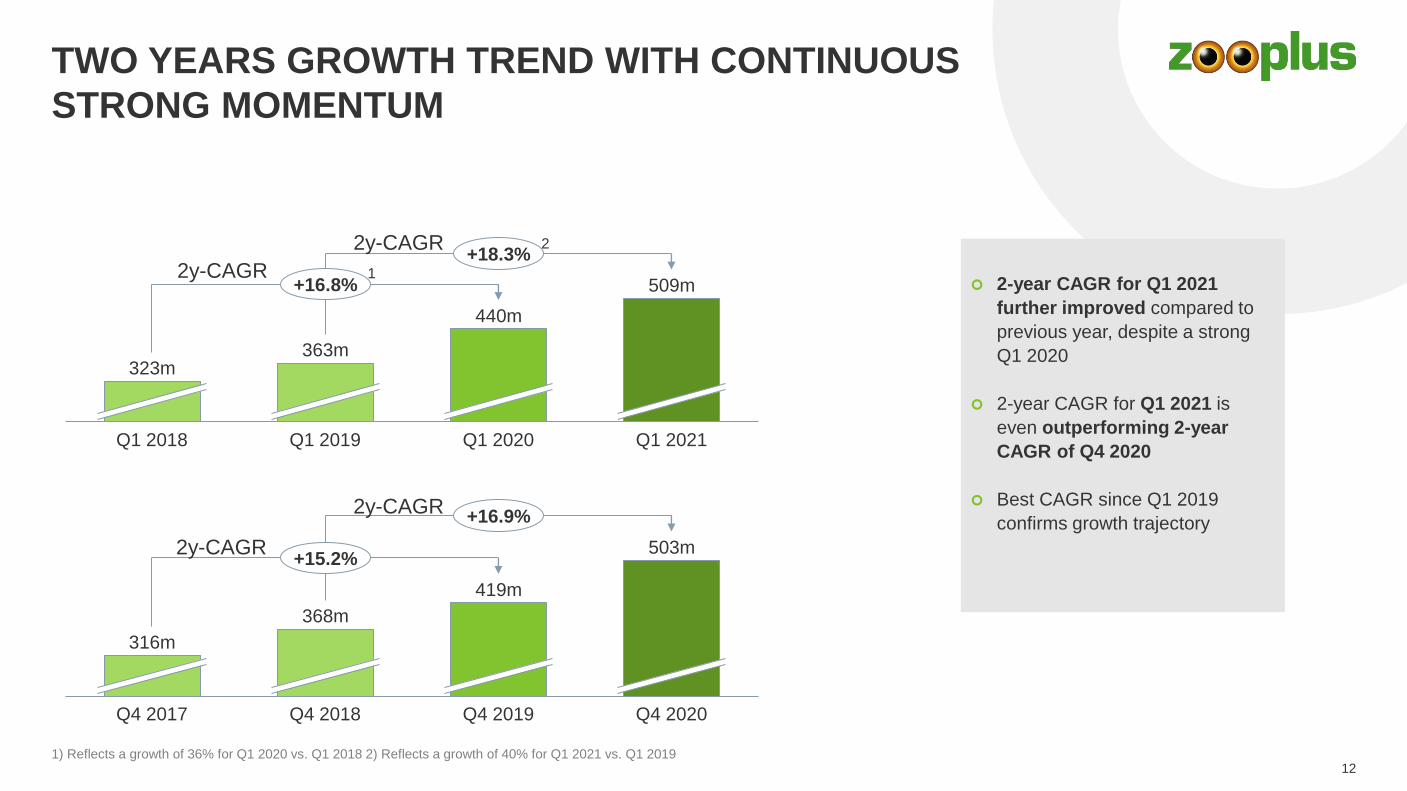

TWO YEARS GROWTH TREND WITH CONTINUOUS

STRONG MOMENTUM

12

Q1 2021

440m

509m

Q1 2018 Q1 2019 Q1 2020

323m363m

+16.8%

+18.3%

368m

Q4 2020Q4 2018Q4 2017

316m

Q4 2019

419m

503m+15.2%

+16.9%

2-year CAGR for Q1 2021

further improved compared to

previous year, despite a strong

Q1 2020

2-year CAGR for Q1 2021 is

even outperforming 2-year

CAGR of Q4 2020

Best CAGR since Q1 2019

confirms growth trajectory

2y-CAGR

2y-CAGR

2y-CAGR

2y-CAGR

1) Reflects a growth of 36% for Q1 2020 vs. Q1 2018 2) Reflects a growth of 40% for Q1 2021 vs. Q1 2019

1

2

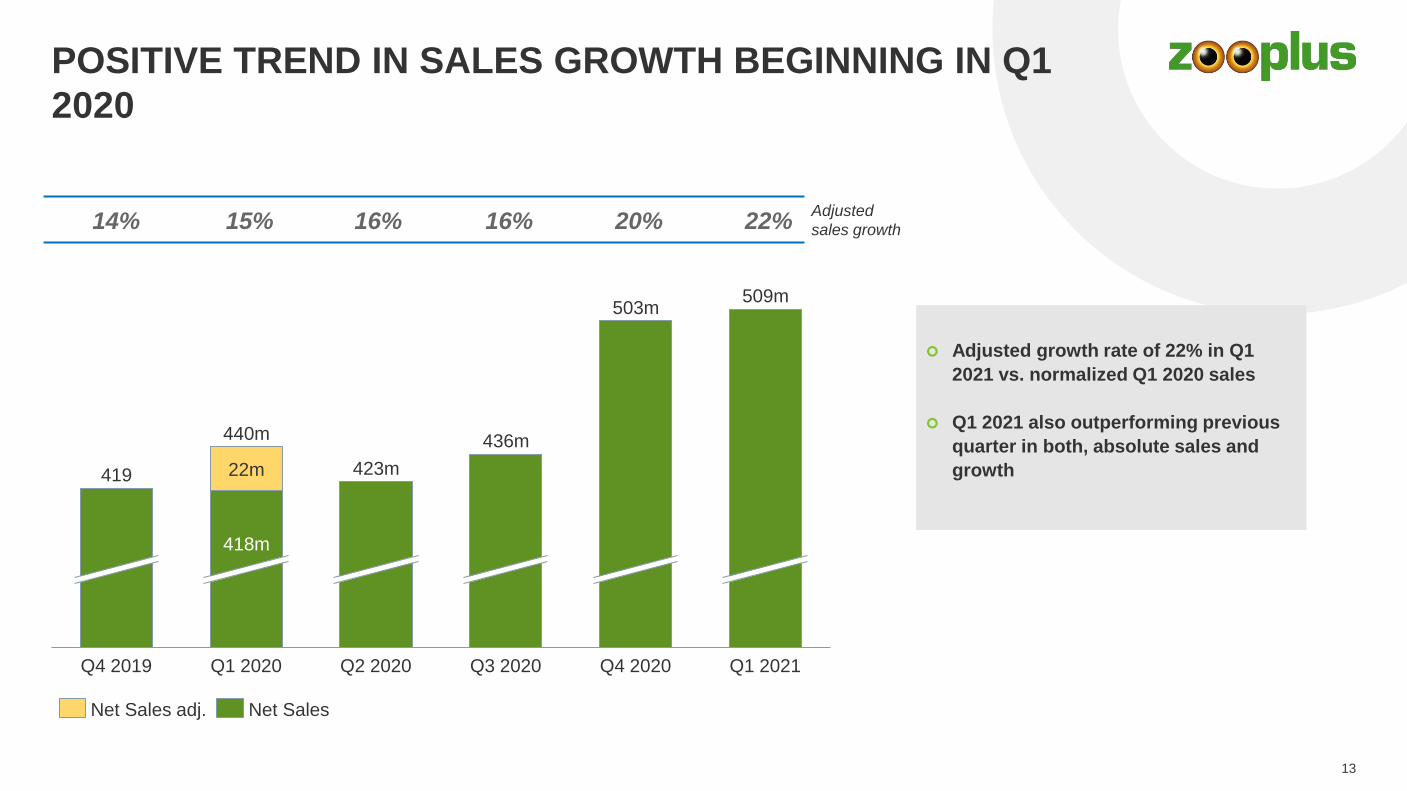

423m

509m

22m

418m

Q1 2020 Q2 2020 Q3 2020

503m

Q4 2020Q4 2019

419

440m

Q1 2021

436m

13

POSITIVE TREND IN SALES GROWTH BEGINNING IN Q1

2020

Net Sales adj. Net Sales

Adjusted

sales growth15% 16% 16% 20% 22%

Adjusted growth rate of 22% in Q1

2021 vs. normalized Q1 2020 sales

Q1 2021 also outperforming previous

quarter in both, absolute sales and

growth

14%

30.2%29.4%

31.6%30.6%

29.9%30.7%

14%12% 11%

13% 13% 13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

24%

26%

28%

30%

32%

Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021

Gross margin Loss-making orders

14

PREMIUMIZATION AND HIGH MARGIN SALES DRIVE

GROSS MARGIN

Gross margin and share of loss-making orders Strong gross margins

benefitting from increased

premiumization, more high

margin sales and less

promotional activities

High-margin own brands

expansion supporting gross

margin (+34% sales increase vs.

Q1 2020)

Intelligent pricing supporting

gross margin

Loyalty benefits included in

gross margin

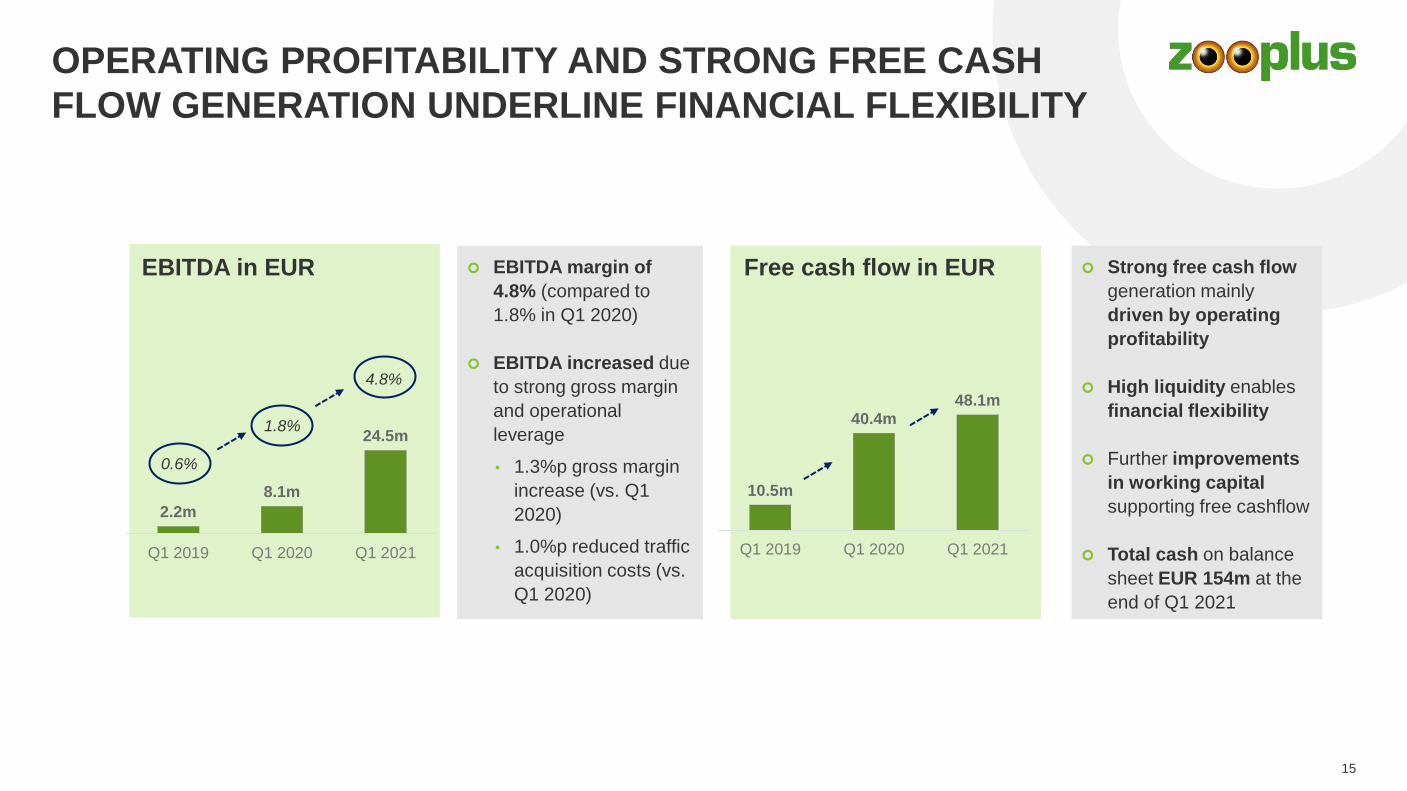

OPERATING PROFITABILITY AND STRONG FREE CASH

FLOW GENERATION UNDERLINE FINANCIAL FLEXIBILITY

15

EBITDA margin of

4.8% (compared to

1.8% in Q1 2020)

EBITDA increased due

to strong gross margin

and operational

leverage

• 1.3%p gross margin

increase (vs. Q1

2020)

• 1.0%p reduced traffic

acquisition costs (vs.

Q1 2020)

Strong free cash flow

generation mainly

driven by operating

profitability

High liquidity enables

financial flexibility

Further improvements

in working capital

supporting free cashflow

Total cash on balance

sheet EUR 154m at the

end of Q1 2021

2.2m

8.1m

24.5m

Q1 2019 Q1 2020 Q1 2021

10.5m

40.4m48.1m

Q1 2019 Q1 2020 Q1 2021

1.8%

4.8%

0.6%

EBITDA in EUR Free cash flow in EUR

2021 GUIDANCE &

OUTLOOK 2025Q1 2021 Investor & Analyst Call

WELL ON TRACK TO ACHIEVE FY 2021 GUIDANCE

*Management Board currently assumes FY 2021

sales and EBITDA in the mid- to upper range.

SALES EBITDA MARGINEBITDA

From

EUR 2.04bn

to

EUR 2.14bn*

17

From

EUR 40m

to

EUR 80m*

From

2%

to

4%

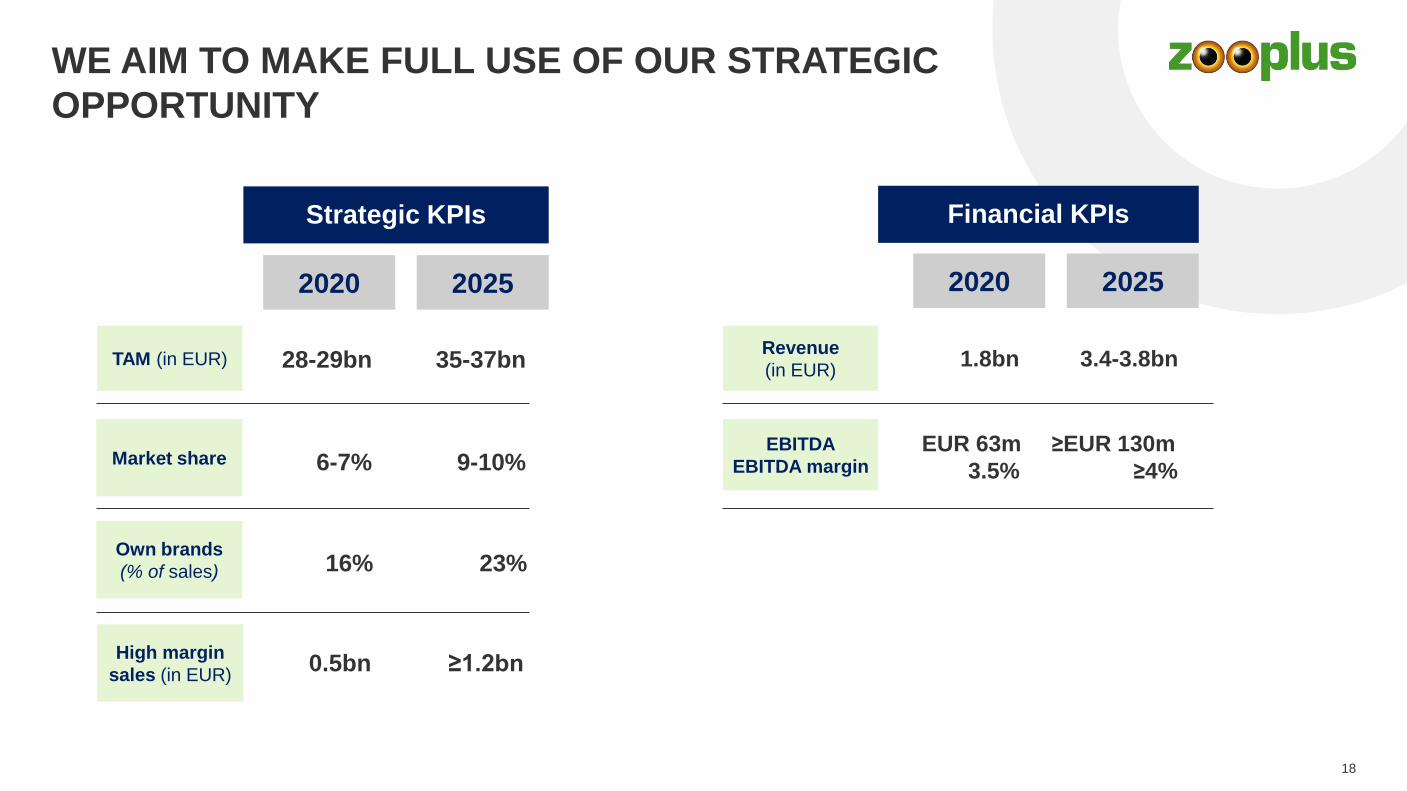

WE AIM TO MAKE FULL USE OF OUR STRATEGIC

OPPORTUNITY

2020

Strategic KPIs

2020

Financial KPIs

2025

TAM (in EUR)Revenue

(in EUR)

EBITDA

EBITDA marginMarket share

Own brands

(% of sales)

28-29bn 1.8bn 3.4-3.8bn

High margin

sales (in EUR)

EUR 63m

3.5%6-7%

16%

0.5bn

≥EUR 130m

≥4%9-10%

≥1.2bn

23%

35-37bn

2025

18

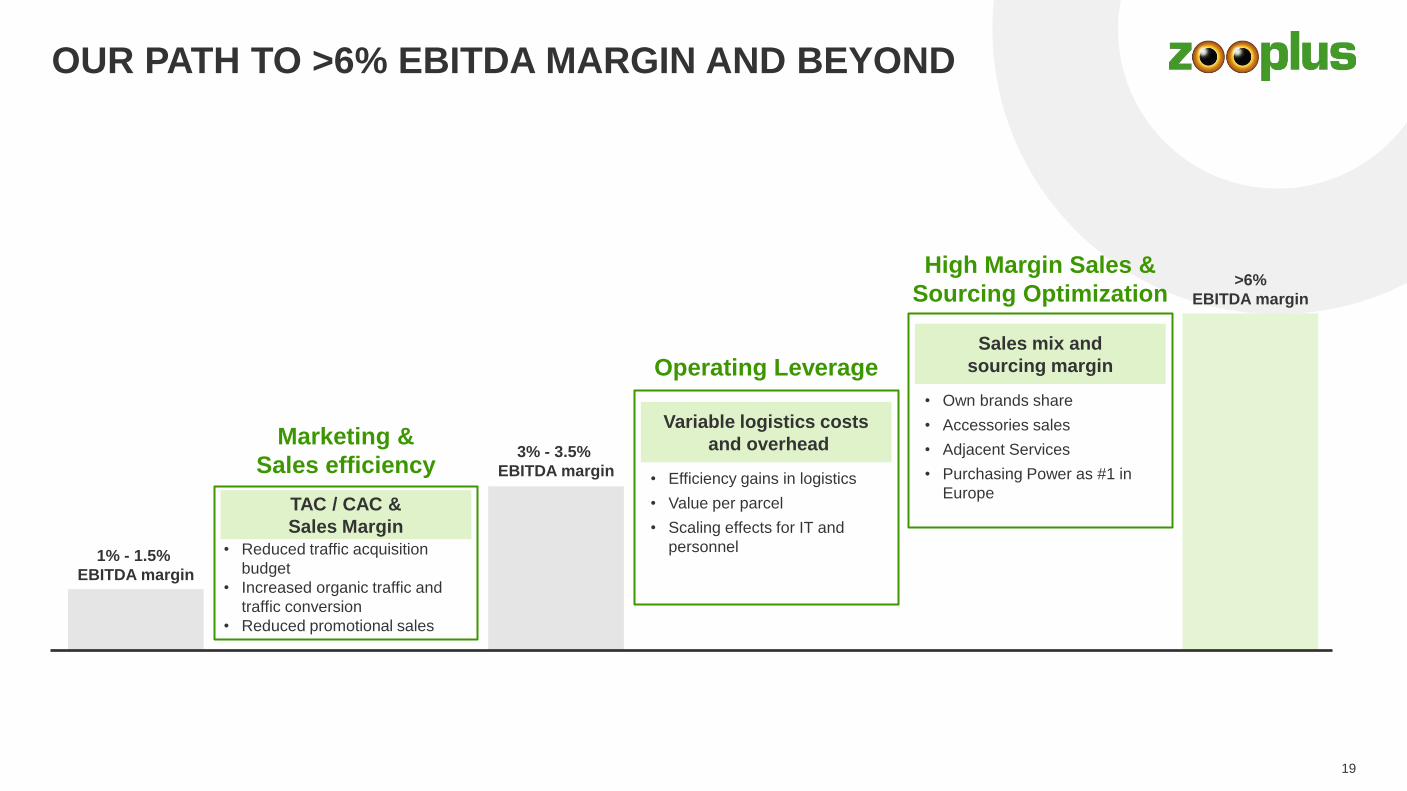

OUR PATH TO >6% EBITDA MARGIN AND BEYOND

3% - 3.5%

EBITDA margin

Sales mix and

sourcing margin

>6%

EBITDA margin

Variable logistics costs

and overhead

Operating Leverage

High Margin Sales &

Sourcing Optimization

19

• Reduced traffic acquisition

budget

• Increased organic traffic and

traffic conversion

• Reduced promotional sales

TAC / CAC &

Sales Margin

Marketing &

Sales efficiency

1% - 1.5%

EBITDA margin

• Efficiency gains in logistics

• Value per parcel

• Scaling effects for IT and

personnel

• Own brands share

• Accessories sales

• Adjacent Services

• Purchasing Power as #1 in

Europe

Q&AQ1 2021 Investor & Analyst Call

THANK

YOU

22

SAFE HARBOR STATEMENT

This document includes supplemental financial measures that are or may be non-GAAP financial measures. These supplemental financial

measures should not be viewed in isolation as alternatives to measures of zooplus’ financial condition, results of operations or cash flows

as presented in accordance with IFRS in its Consolidated Financial Statements. Other companies that report or describe similarly titled

financial measures may calculate them differently.

This document contains statements related to our future business and financial performance and future events or developments involving

zooplus that may constitute forward-looking statements. We may also make forward-looking statements in other reports, in presentations,

in material delivered to stockholders and in press releases. In addition, our representatives may from time to time make oral forward-

looking statements. Such statements are based on the current expectations and certain assumptions of zooplus’ management, and are,

therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond zooplus’ control, affect zooplus’

operations, performance, business strategy and results and could cause the actual results, performance or achievements of zooplus to be

materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking

statements or anticipated based on historical trends. Further information about risks and uncertainties affecting zooplus is included

throughout our most recent annual and interim reports, which are available on the zooplus website, www.zooplus.de. Should one or more

of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results, performance or achievements

of zooplus may vary materially from those described in the relevant forward-looking statement as being expected, anticipated, intended,

planned, believed, sought, estimated or projected. zooplus neither intends, nor assumes any obligation, to update or revise these forward-

looking statements in light of developments which differ from those anticipated.

Due to rounding, numbers presented throughout this and other documents may not add up precisely to the totals provided and

percentages may not precisely reflect the absolute figures.

SOURCES PET POPULATION

23

• European Households with Pets: Euromonitor International 2021

• Belgium: Flanders region, https://dierenwelzijn.vlaanderen.be/aantal-honden-in-vlaanderen; https://dierenwelzijn.vlaanderen.be/aantal-

katten-in-vlaanderen

• France: SPA Society for the Protection of Animals https://www.la-spa.fr/actualites/spa/pres-de-38-000-adoptions-en-2020-reflexespa;

Mordor Intelligence Research 2021

• Germany: Industrieverband Heimtierbedarf (IVH) e. V & Zentralverband Zoologischer Fachbetriebe Deutschlands e.V.

https://www.zzf.de/fileadmin/files/ZZF/Marktdaten/ZZF_IVH_Folder_Der_deutsche_Heimtiermarkt_2020_und_Anzahl_der_Heimtiere_in_

Deutschland.pdf; TASSO e.V.

• Italy: https://www.aboutpharma.com/blog/2020/10/05/effetto-lockdown-in-italia-e-boom-di-animali-da-

compagnia/?comingfrom=aboutpharma; Mordor Intelligence Research 2021

• Poland Mordor Intelligence Research 2021

• Romania: Romanian Association of Pet Food Producers ARPAC https://www.arpac.ro/noutati/74-studiu-arpac-numarul-romanilor-din-

mediul-urban-care-detin-animale-de-companie-a-crescut-in-perioada-starii-de-urgenta

• Sweden: Swedish Board of Agriculture; Figures based on March 2021 vs. March 2020 https://jordbruksverket.se/e-tjanster-databaser-

och-appar/e-tjanster-och-databaser-djur/hundregistret/statistik-ur-hundregistret

• Switzerland https://www.luzernerzeitung.ch/wirtschaft/auf-homeoffice-folgt-haustierboom-bello-miezi-und-co-sind-wegen-corona-beliebter-

denn-je-ld.1274809

• Spain: https://www.anfaac.org/datos-sectoriales/ OK diario https://okdiario.com/mascotas/5-mascotas-mas-comunes-espana-2021-

6703589 ; Mordor Intelligence Research 2021

• UK; PFMA https://pfma-reports.co.uk/ PFMA research released in September 2020 highlighted that 11% of UK households had acquired a

new pet during the pandemic and a further 10% were planning to do so.;