16

QUARTERLY INVESTMENT REVIEW SECOND QUARTER 2010 Crestline Capital, LLC CC

| Date post: | 28-Mar-2016 |

| Category: |

Documents |

| Upload: | crestline-capital |

| View: | 216 times |

| Download: | 3 times |

QUARTERLYINVESTMENTREVIEW

SECONDQUARTER2010

Crestline Capital, LLCCC

USLargeCompaniesStocks

USSmallCompanyStocks

USREITStocks

InternaAonalDevelopedStocks

USBondMarket

USTreasuryOneMonthTreasuryBills

‐11.43% ‐9.93% ‐4.13% ‐13.97% +3.49% +0.02%

Marketsegment(IndexrepresentaAon)asfollows:USLargeCompanyStocks(S&P500Index);USSmallCompanyStocks(Russell2000Index),USValueStocks(Russell1000ValueIndex).USRealEstateMarket(DowJonesUSSelectREITIndex),InternaAonalDeveloped(MSCIEAFEIndex(netdiv.)),EmergingMarkets(MSCIEmergingMarketsIndex(grossdiv)),USBondMarket(BarclaysCapitalUSAggregateBondIndex),andTreasury(One‐MonthUSTreasuryBills).TheS&PdataareprovidedbyStandard&Poor'sIndexServicesGroup.Russelldatacopyright©RussellInvestmentGroup1995‐2010,all rightsreserved.MSCIdatacopyrightMSCI2010,all rightsreserved.DowJonesdata(formerlyDowJonesWilshire)providedbyDowJones Indexes.BarclaysCapitaldataprovidedbyBarclaysBankPLC.USlong‐termbonds,bills,andinflaAondata©Stocks,Bonds,Bills,andInflaAonYearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield).Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

MarketsUpdate:AQuarterinReviewSecondQuarter2010

EmergingMarketsStocks

‐8.29%

2

BONDSSTOCKS

USValueStocks

‐11.14%

MarketsUpdate:AQuarterinReviewSecondQuarter2010

3

• Aker four consecuAvequarterswith very strong performance,which conAnued intoApril, theUS equitymarket saw asharpreversalinMayandJuneandendedthesecondquarterwithlargenegaAvereturns.ThebroadUSmarketlostover11%inthequarter,withmostassetclassesdeliveringdouble‐digitnegaAvereturns.

• Performanceinotherdevelopedmarketsaroundtheworldwasgenerallyworse,especiallyinEurope.Indeed,theworst‐performingdevelopedmarketsinthequarterweremainlyEuropeancountriesinthemidstofseveresovereign‐debtcrisessuchasGreeceandSpain.DevelopedmarketsintheAsiaPacificregiongenerallyfaredbeler,especiallySingapore,whichhadaflatreturnandwasbyfarthebest‐performingdevelopedmarketinthesecondquarter.TheUSdollargainedgroundagainstmostmajorcurrencies,especiallytheeuroandtheAustraliandollar,whichhurtthedollar‐denominatedreturnsofdevelopedmarketequiAes.

• Akerbeingthetop‐performingassetclassin2009,emergingmarketsconAnuedtocooloffinthesecondquarter,althoughreturns thereweregenerallybeler than indevelopedcountries.As in thecaseofdevelopedmarkets, therewasmuchdispersion in theperformanceofdifferentemergingmarketsandasset classes. The fall in commoditypricesnegaAvelyimpactedtwoofthelargercommodity‐richemergingcountries,RussiaandBrazil,whichhadsharplynegaAvereturns.Ontheotherhand,somesmalleremergingmarkets,suchasChile, Indonesia,andthePhilippinesmanagedtopostposiAvereturns for the quarter. TheUS dollar also gained ground against themain emergingmarket currencies in the secondquarter,whichhurtthedollar‐denominatedreturnsofemergingmarketequiAes.

• Value stockshadmixedperformance relaAve togrowthstocks in theUSduring the secondquarter. Inotherdevelopedmarkets, value stocks greatly underperformed growth stocks across all market capitalizaAon segments. In emergingmarkets,valuestocksoutperformedgrowthstocksacrossallmarketcapitalizaAonsegments.

• AlongthemarketcapitalizaAondimension,smallcapsoutperformedlargecapsintheUS,inotherdevelopedmarkets,andinemergingmarkets.

• NotwithstandingtheconAnuedweaknessinthecommercialandresidenAalrealestatemarkets,realestatesecuriAeshadnegaAvereturns,butgoodperformancerelaAvetootherassetclasses.

• FixedincomesecuriAeshadgoodreturnsinthesecondquarter,astherewasaflighttosafetyinthesecondquarterasaresultofthesovereigndebtproblemsinEuropeandweakeconomicdataintheUSandabroad.IntermediategovernmentsecuriAesandinflaAon‐protectedsecuriAesdidparAcularlywell.

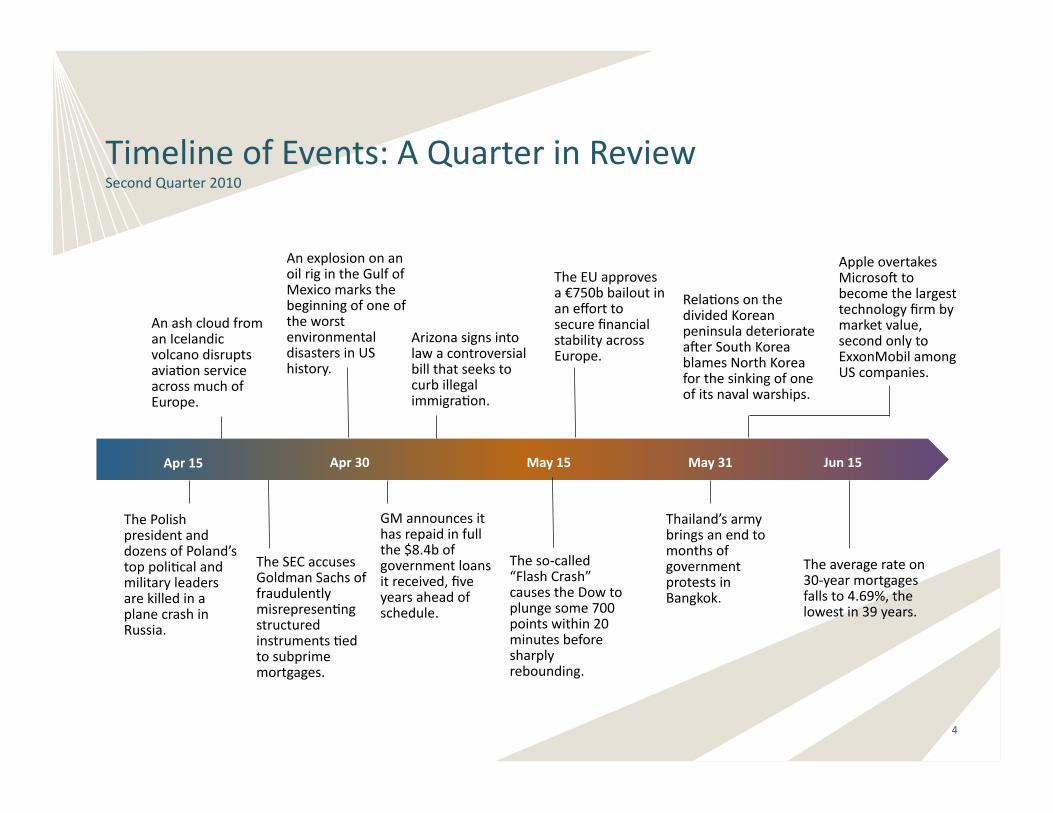

TimelineofEvents:AQuarterinReviewSecondQuarter2010

ThePolishpresidentanddozensofPoland’stoppoliAcalandmilitaryleadersarekilledinaplanecrashinRussia.

Thailand’sarmybringsanendtomonthsofgovernmentprotestsinBangkok.

GMannouncesithasrepaidinfullthe$8.4bofgovernmentloansitreceived,fiveyearsaheadofschedule.

Apr15 May31 Jun15

AnexplosiononanoilrigintheGulfofMexicomarksthebeginningofoneoftheworstenvironmentaldisastersinUShistory.

ArizonasignsintolawacontroversialbillthatseekstocurbillegalimmigraAon.

Theso‐called“FlashCrash”causestheDowtoplungesome700pointswithin20minutesbeforesharplyrebounding.

May15

TheEUapprovesa€750bbailoutinanefforttosecurefinancialstabilityacrossEurope.

Apr30

AnashcloudfromanIcelandicvolcanodisruptsaviaAonserviceacrossmuchofEurope.

TheSECaccusesGoldmanSachsoffraudulentlymisrepresenAngstructuredinstrumentsAedtosubprimemortgages.

RelaAonsonthedividedKoreanpeninsuladeteriorateakerSouthKoreablamesNorthKoreaforthesinkingofoneofitsnavalwarships.

Theaveragerateon30‐yearmortgagesfallsto4.69%,thelowestin39years.

AppleovertakesMicrosoktobecomethelargesttechnologyfirmbymarketvalue,secondonlytoExxonMobilamongUScompanies.

4

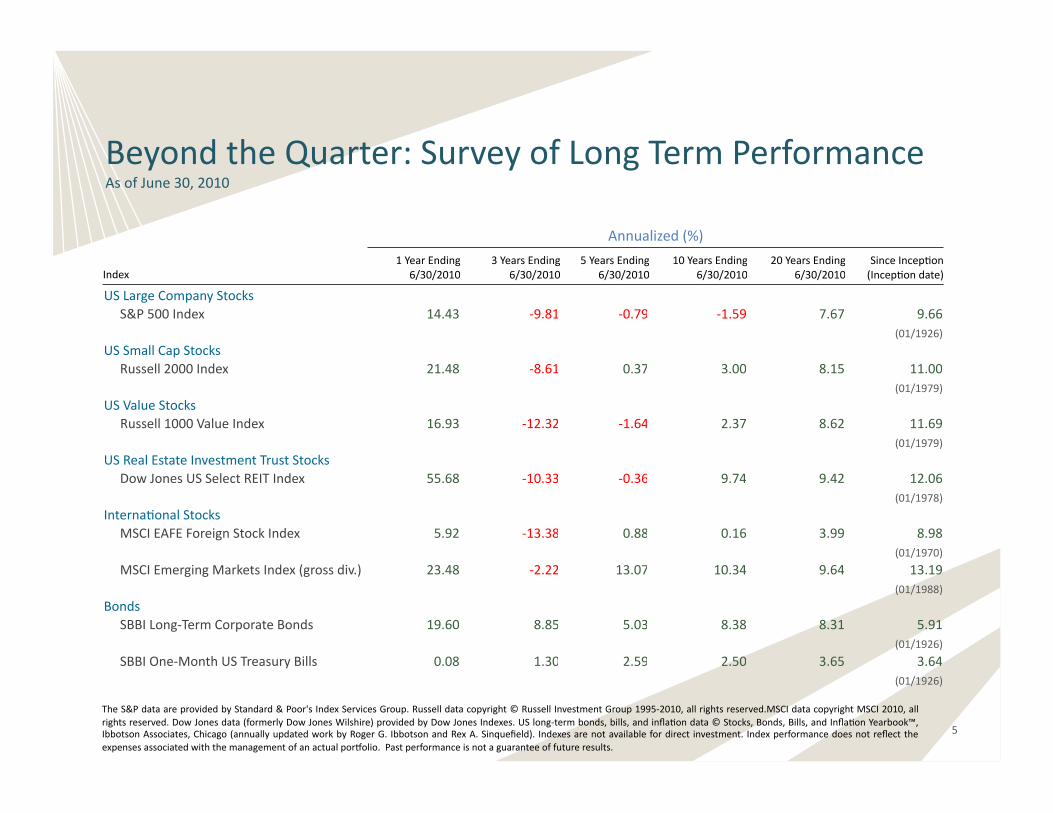

Annualized(%)

Index1YearEnding

6/30/20103YearsEnding

6/30/20105YearsEnding

6/30/201010YearsEnding

6/30/201020YearsEnding

6/30/2010SinceIncepAon(IncepAondate)

USLargeCompanyStocksS&P500Index 14.43 ‐9.81 ‐0.79 ‐1.59 7.67 9.66

(01/1926)

USSmallCapStocksRussell2000Index 21.48 ‐8.61 0.37 3.00 8.15 11.00

(01/1979)

USValueStocksRussell1000ValueIndex 16.93 ‐12.32 ‐1.64 2.37 8.62 11.69

(01/1979)

USRealEstateInvestmentTrustStocksDowJonesUSSelectREITIndex 55.68 ‐10.33 ‐0.36 9.74 9.42 12.06

(01/1978)

InternaAonalStocksMSCIEAFEForeignStockIndex 5.92 ‐13.38 0.88 0.16 3.99 8.98

(01/1970)

MSCIEmergingMarketsIndex(grossdiv.) 23.48 ‐2.22 13.07 10.34 9.64 13.19(01/1988)

BondsSBBILong‐TermCorporateBonds 19.60 8.85 5.03 8.38 8.31 5.91

(01/1926)

SBBIOne‐MonthUSTreasuryBills 0.08 1.30 2.59 2.50 3.65 3.64(01/1926)

BeyondtheQuarter:SurveyofLongTermPerformanceAsofJune30,2010

5

TheS&PdataareprovidedbyStandard&Poor'sIndexServicesGroup.Russelldatacopyright©RussellInvestmentGroup1995‐2010,allrightsreserved.MSCIdatacopyrightMSCI2010,allrightsreserved.DowJonesdata(formerlyDowJonesWilshire)providedbyDowJonesIndexes.USlong‐termbonds,bills,andinflaAondata©Stocks,Bonds,Bills,andInflaAonYearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield). Indexesarenotavailablefordirect investment. Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

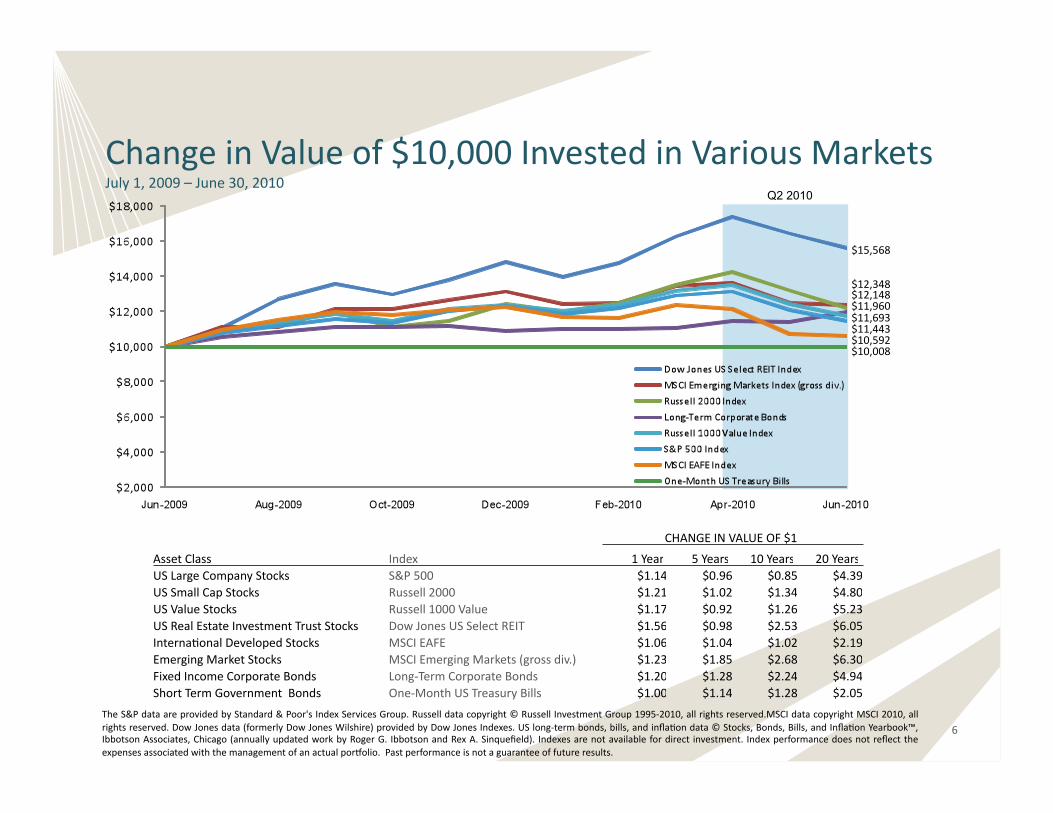

ChangeinValueof$10,000InvestedinVariousMarketsJuly1,2009–June30,2010

Q2 2010

$12,348$12,148$11,960

$11,443

$10,008

$11,693

$10,592

6

CHANGEINVALUEOF$1

AssetClass Index 1Year 5Years 10Years 20YearsUSLargeCompanyStocks S&P500 $1.14 $0.96 $0.85 $4.39USSmallCapStocks Russell2000 $1.21 $1.02 $1.34 $4.80USValueStocks Russell1000Value $1.17 $0.92 $1.26 $5.23USRealEstateInvestmentTrustStocks DowJonesUSSelectREIT $1.56 $0.98 $2.53 $6.05InternaAonalDevelopedStocks MSCIEAFE $1.06 $1.04 $1.02 $2.19EmergingMarketStocks MSCIEmergingMarkets(grossdiv.) $1.23 $1.85 $2.68 $6.30FixedIncomeCorporateBonds Long‐TermCorporateBonds $1.20 $1.28 $2.24 $4.94ShortTermGovernmentBonds One‐MonthUSTreasuryBills $1.00 $1.14 $1.28 $2.05

TheS&PdataareprovidedbyStandard&Poor'sIndexServicesGroup.Russelldatacopyright©RussellInvestmentGroup1995‐2010,allrightsreserved.MSCIdatacopyrightMSCI2010,allrightsreserved.DowJonesdata(formerlyDowJonesWilshire)providedbyDowJonesIndexes.USlong‐termbonds,bills,andinflaAondata©Stocks,Bonds,Bills,andInflaAonYearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield). Indexesarenotavailablefordirect investment. Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

$15,568

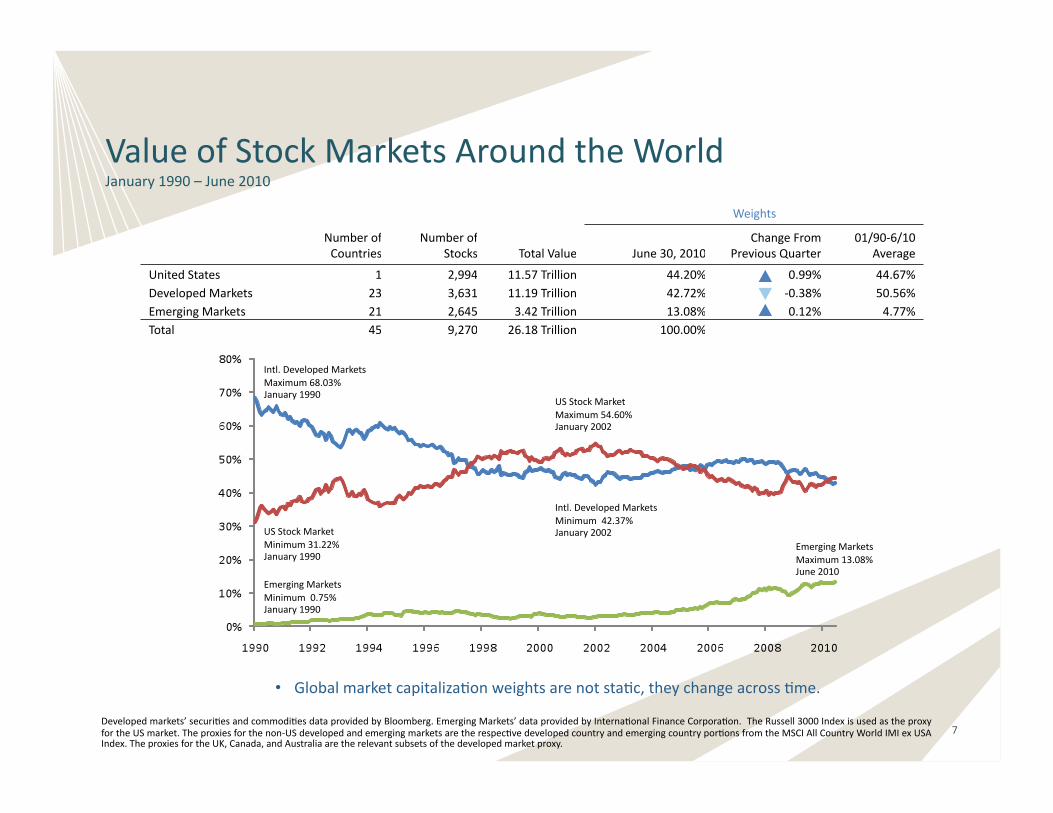

ValueofStockMarketsAroundtheWorldJanuary1990–June2010

• GlobalmarketcapitalizaAonweightsarenotstaAc,theychangeacrossAme.

Developedmarkets’securiAesandcommodiAesdataprovidedbyBloomberg.EmergingMarkets’dataprovidedbyInternaAonalFinanceCorporaAon.TheRussell3000IndexisusedastheproxyfortheUSmarket.Theproxiesforthenon‐USdevelopedandemergingmarketsaretherespecAvedevelopedcountryandemergingcountryporAonsfromtheMSCIAllCountryWorldIMIexUSAIndex.TheproxiesfortheUK,Canada,andAustraliaaretherelevantsubsetsofthedevelopedmarketproxy.

Weights

NumberofCountries

NumberofStocks TotalValue June30,2010

ChangeFromPreviousQuarter

01/90‐6/10Average

UnitedStates 1 2,994 11.57Trillion 44.20% 0.99% 44.67%DevelopedMarkets 23 3,631 11.19Trillion 42.72% ‐0.38% 50.56%EmergingMarkets 21 2,645 3.42Trillion 13.08% 0.12% 4.77%Total 45 9,270 26.18Trillion 100.00%

Intl.DevelopedMarketsMaximum68.03%January1990

USStockMarketMinimum31.22%January1990

EmergingMarketsMinimum0.75%January1990

Intl.DevelopedMarketsMinimum42.37%January2002

USStockMarketMaximum54.60%January2002

EmergingMarketsMaximum13.08%June2010

7

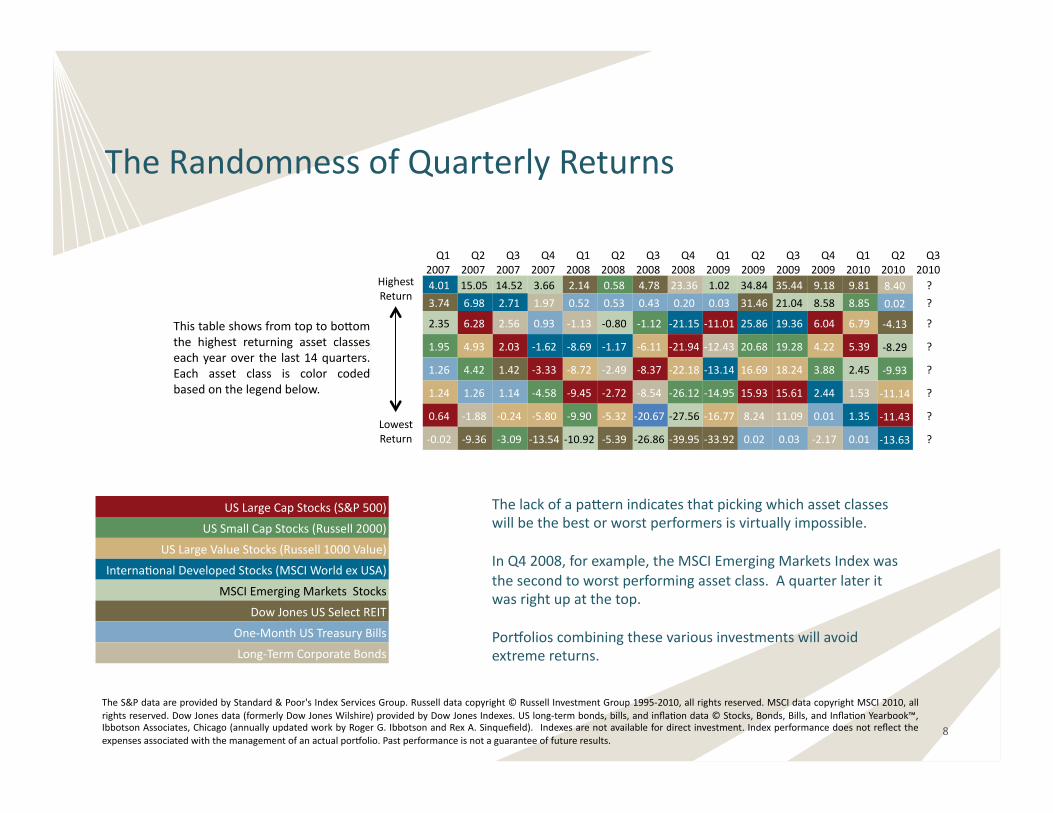

TheRandomnessofQuarterlyReturns

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

4.01 15.05 14.52 3.66 2.14 0.58 4.78 23.36 1.02 34.84 35.44 9.18 9.81 8.40 ?

3.74 6.98 2.71 1.97 0.52 0.53 0.43 0.20 0.03 31.46 21.04 8.58 8.85 0.02 ?

2.35 6.28 2.56 0.93 ‐1.13 ‐0.80 ‐1.12 ‐21.15 ‐11.01 25.86 19.36 6.04 6.79 ‐4.13 ?

div.) 1.95 4.93 2.03 ‐1.62 ‐8.69 ‐1.17 ‐6.11 ‐21.94 ‐12.43 20.68 19.28 4.22 5.39 ‐8.29 ?

) 1.26 4.42 1.42 ‐3.33 ‐8.72 ‐2.49 ‐8.37 ‐22.18 ‐13.14 16.69 18.24 3.88 2.45 ‐9.93 ?

1.24 1.26 1.14 ‐4.58 ‐9.45 ‐2.72 ‐8.54 ‐26.12 ‐14.95 15.93 15.61 2.44 1.53 ‐11.14 ?

0.64 ‐1.88 ‐0.24 ‐5.80 ‐9.90 ‐5.32 ‐20.67 ‐27.56 ‐16.77 8.24 11.09 0.01 1.35 ‐11.43 ?

‐0.02 ‐9.36 ‐3.09 ‐13.54 ‐10.92 ‐5.39 ‐26.86 ‐39.95 ‐33.92 0.02 0.03 ‐2.17 0.01 ‐13.63 ?

TheS&PdataareprovidedbyStandard&Poor'sIndexServicesGroup.Russelldatacopyright©RussellInvestmentGroup1995‐2010,allrightsreserved.MSCIdatacopyrightMSCI2010,allrightsreserved.DowJonesdata(formerlyDowJonesWilshire)providedbyDowJonesIndexes.USlong‐termbonds,bills,andinflaAondata©Stocks,Bonds,Bills,andInflaAonYearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield). Indexesarenotavailablefordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

HighestReturn

LowestReturn

Thistableshowsfromtoptobolomthe highest returning asset classeseachyearover the last14quarters.Each asset class is color codedbasedonthelegendbelow.

Thelackofapalernindicatesthatpickingwhichassetclasseswillbethebestorworstperformersisvirtuallyimpossible.

InQ42008,forexample,theMSCIEmergingMarketsIndexwasthesecondtoworstperformingassetclass.Aquarterlateritwasrightupatthetop.

Porholioscombiningthesevariousinvestmentswillavoidextremereturns.

8

USLargeCapStocks(S&P500)

USSmallCapStocks(Russell2000)

USLargeValueStocks(Russell1000Value)

InternaAonalDevelopedStocks(MSCIWorldexUSA)

MSCIEmergingMarketsStocks

DowJonesUSSelectREIT

One‐MonthUSTreasuryBills

Long‐TermCorporateBonds

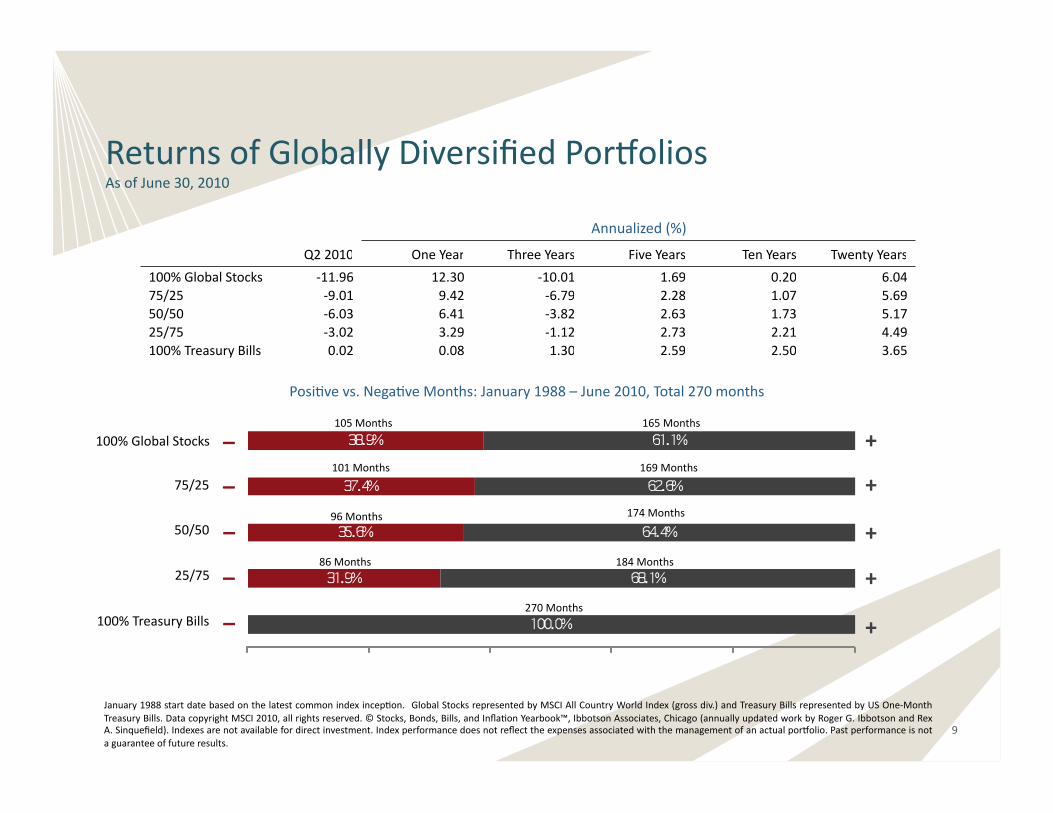

ReturnsofGloballyDiversifiedPorholiosAsofJune30,2010

January1988startdatebasedonthelatestcommonindexincepAon. GlobalStocksrepresentedbyMSCIAllCountryWorldIndex(grossdiv.)andTreasuryBillsrepresentedbyUSOne‐MonthTreasuryBills.DatacopyrightMSCI2010,allrightsreserved.©Stocks,Bonds,Bills,andInflaAonYearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield).Indexesarenotavailablefordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

Annualized(%)

Q22010 OneYear ThreeYears FiveYears TenYears TwentyYears

100%GlobalStocks ‐11.96 12.30 ‐10.01 1.69 0.20 6.0475/25 ‐9.01 9.42 ‐6.79 2.28 1.07 5.6950/50 ‐6.03 6.41 ‐3.82 2.63 1.73 5.1725/75 ‐3.02 3.29 ‐1.12 2.73 2.21 4.49100%TreasuryBills 0.02 0.08 1.30 2.59 2.50 3.65

100%GlobalStocks

50/50

25/75

100%TreasuryBills

75/25

105Months 165Months

101Months 169Months

96Months 174Months

86Months 184Months

270Months

–

–

–

–

–

+

+

+

+

+

PosiAvevs.NegaAveMonths:January1988–June2010,Total270months

9

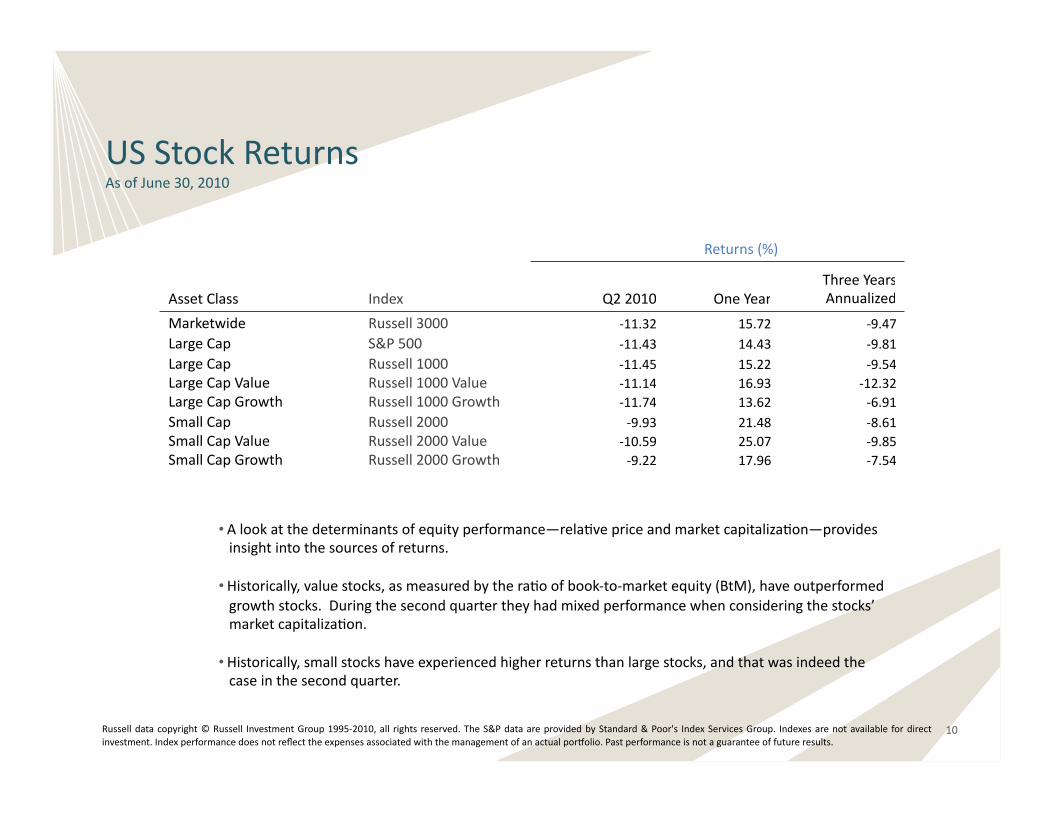

USStockReturnsAsofJune30,2010

Russelldatacopyright©Russell InvestmentGroup1995‐2010,all rights reserved.TheS&PdataareprovidedbyStandard&Poor's IndexServicesGroup. Indexesarenotavailable fordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

Returns(%)

AssetClass Index Q22010 OneYearThreeYearsAnnualized

Marketwide Russell3000 ‐11.32 15.72 ‐9.47LargeCap S&P500 ‐11.43 14.43 ‐9.81LargeCap Russell1000 ‐11.45 15.22 ‐9.54LargeCapValue Russell1000Value ‐11.14 16.93 ‐12.32LargeCapGrowth Russell1000Growth ‐11.74 13.62 ‐6.91SmallCap Russell2000 ‐9.93 21.48 ‐8.61SmallCapValue Russell2000Value ‐10.59 25.07 ‐9.85SmallCapGrowth Russell2000Growth ‐9.22 17.96 ‐7.54

• Alookatthedeterminantsofequityperformance—relaAvepriceandmarketcapitalizaAon—providesinsightintothesourcesofreturns.

• Historically,valuestocks,asmeasuredbytheraAoofbook‐to‐marketequity(BtM),haveoutperformedgrowthstocks.Duringthesecondquartertheyhadmixedperformancewhenconsideringthestocks’marketcapitalizaAon.

• Historically,smallstockshaveexperiencedhigherreturnsthanlargestocks,andthatwasindeedthecaseinthesecondquarter.

10

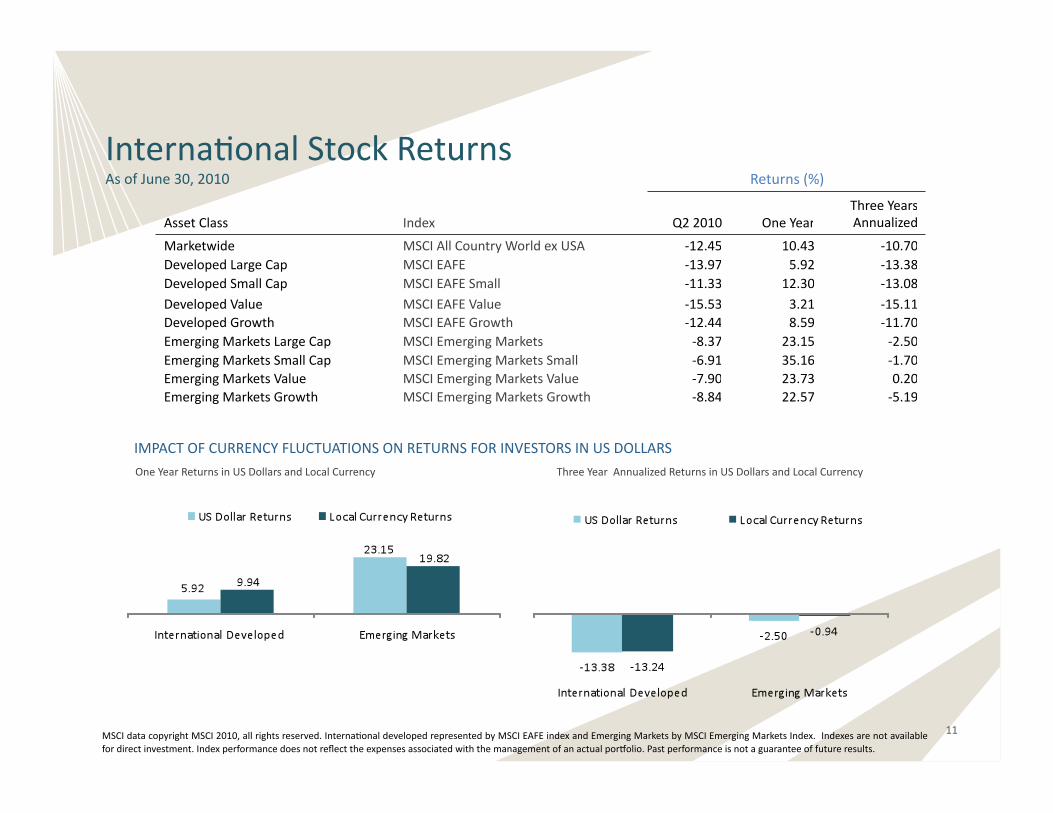

InternaAonalStockReturnsAsofJune30,2010 Returns(%)

AssetClass Index Q22010 OneYearThreeYearsAnnualized

Marketwide MSCIAllCountryWorldexUSA ‐12.45 10.43 ‐10.70DevelopedLargeCap MSCIEAFE ‐13.97 5.92 ‐13.38DevelopedSmallCap MSCIEAFESmall ‐11.33 12.30 ‐13.08DevelopedValue MSCIEAFEValue ‐15.53 3.21 ‐15.11DevelopedGrowth MSCIEAFEGrowth ‐12.44 8.59 ‐11.70EmergingMarketsLargeCap MSCIEmergingMarkets ‐8.37 23.15 ‐2.50EmergingMarketsSmallCap MSCIEmergingMarketsSmall ‐6.91 35.16 ‐1.70EmergingMarketsValue MSCIEmergingMarketsValue ‐7.90 23.73 0.20EmergingMarketsGrowth MSCIEmergingMarketsGrowth ‐8.84 22.57 ‐5.19

MSCIdatacopyrightMSCI2010,allrightsreserved.InternaAonaldevelopedrepresentedbyMSCIEAFEindexandEmergingMarketsbyMSCIEmergingMarketsIndex.Indexesarenotavailablefordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

IMPACTOFCURRENCYFLUCTUATIONSONRETURNSFORINVESTORSINUSDOLLARSOneYearReturnsinUSDollarsandLocalCurrency ThreeYearAnnualizedReturnsinUSDollarsandLocalCurrency

11

OneYearReturnsinUSDollarsandLocalCurrency

ReturnUS

Dollars

ReturnLocal

CurrencyImpactofCurrency

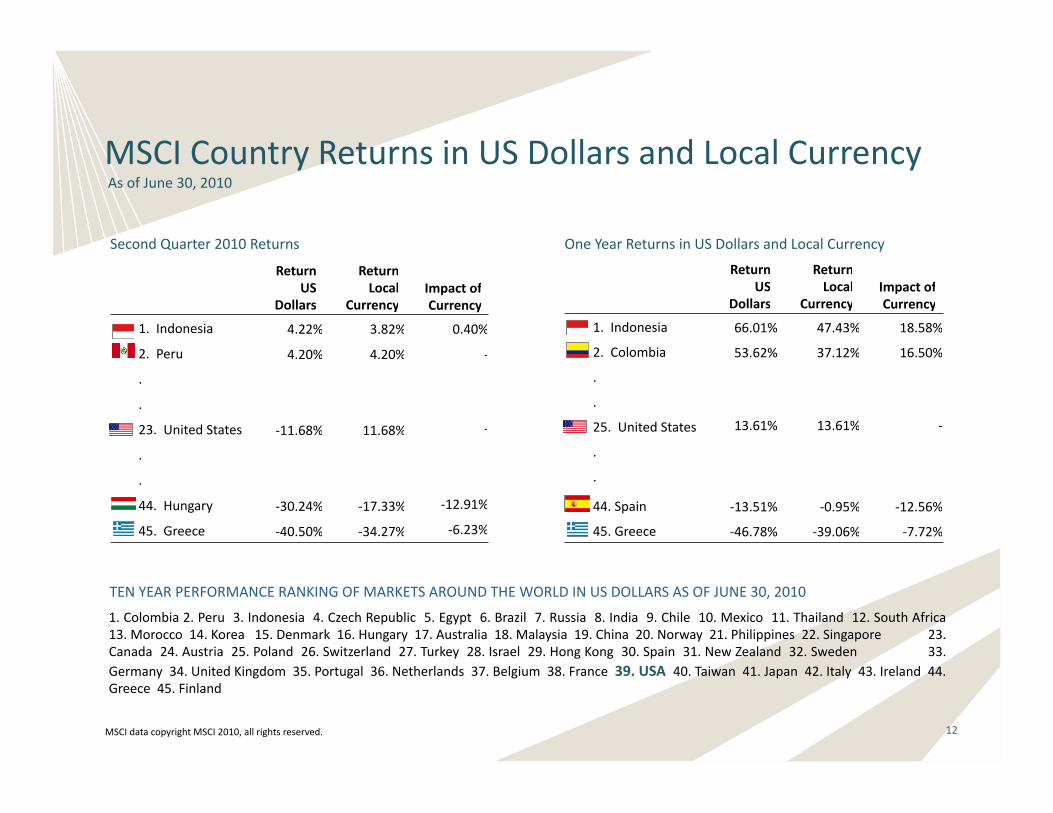

1.Indonesia 66.01% 47.43% 18.58%

2.Colombia 53.62% 37.12% 16.50%

.

.

25.UnitedStates 13.61% 13.61% ‐

.

.

44.Spain ‐13.51% ‐0.95% ‐12.56%

45.Greece ‐46.78% ‐39.06% ‐7.72%

SecondQuarter2010Returns

ReturnUS

Dollars

ReturnLocal

CurrencyImpactofCurrency

1. Indonesia 4.22% 3.82% 0.40%

2.Peru 4.20% 4.20% ‐

.

.

23.UnitedStates ‐11.68% 11.68% ‐

.

.

44.Hungary ‐30.24% ‐17.33% ‐12.91%

45.Greece ‐40.50% ‐34.27% ‐6.23%

MSCICountryReturnsinUSDollarsandLocalCurrencyAsofJune30,2010

12MSCIdatacopyrightMSCI2010,allrightsreserved.

TENYEARPERFORMANCERANKINGOFMARKETSAROUNDTHEWORLDINUSDOLLARSASOFJUNE30,2010

1.Colombia2.Peru3.Indonesia4.CzechRepublic5.Egypt6.Brazil 7.Russia8.India9.Chile10.Mexico11.Thailand12.SouthAfrica13.Morocco14.Korea15.Denmark16.Hungary17.Australia18.Malaysia19.China20.Norway21.Philippines22.Singapore23.Canada24.Austria25.Poland26.Switzerland27.Turkey28.Israel29.HongKong30.Spain31.NewZealand32.Sweden33.Germany34.UnitedKingdom35.Portugal36.Netherlands37.Belgium38.France39.USA40.Taiwan41.Japan42.Italy43.Ireland44.Greece45.Finland

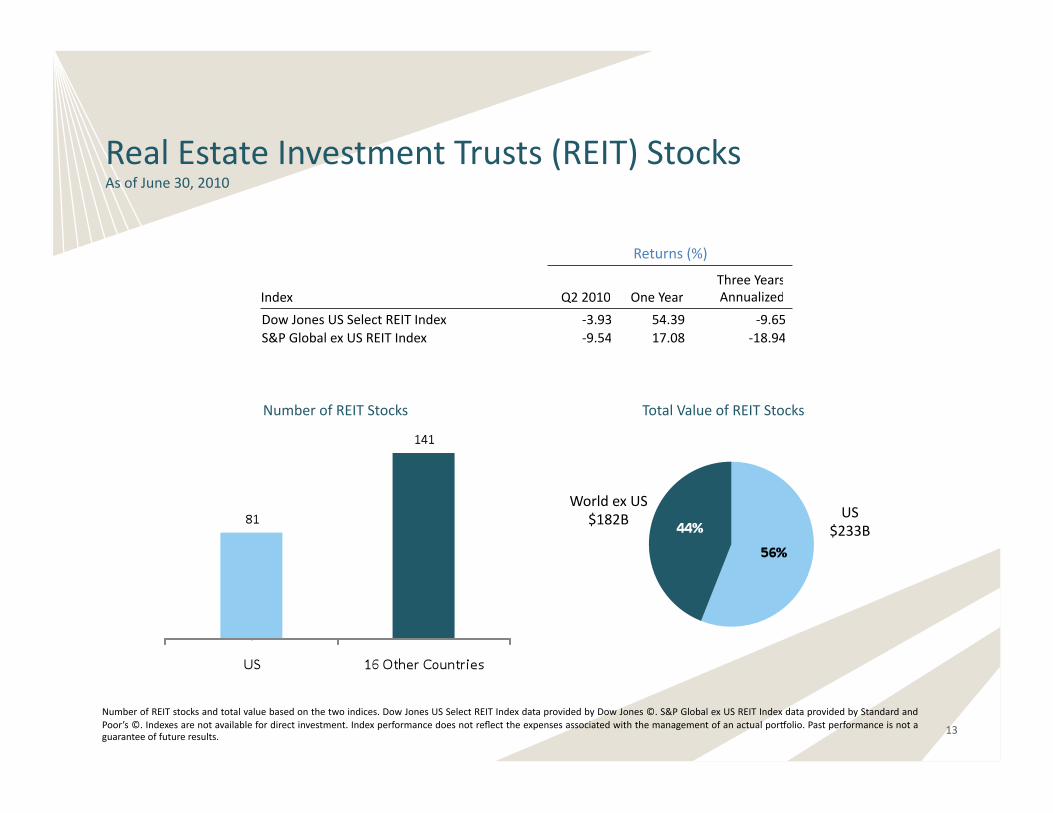

RealEstateInvestmentTrusts(REIT)StocksAsofJune30,2010

NumberofREITstocksandtotalvaluebasedonthetwoindices.DowJonesUSSelectREITIndexdataprovidedbyDowJones©.S&PGlobalexUSREITIndexdataprovidedbyStandardandPoor’s©.Indexesarenotavailablefordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

13

Returns(%)

Index Q22010 OneYearThreeYearsAnnualized

DowJonesUSSelectREITIndex ‐3.93 54.39 ‐9.65 S&PGlobalexUSREITIndex ‐9.54 17.08 ‐18.94

NumberofREITStocks TotalValueofREITStocks

56%

US$233B

WorldexUS$182B

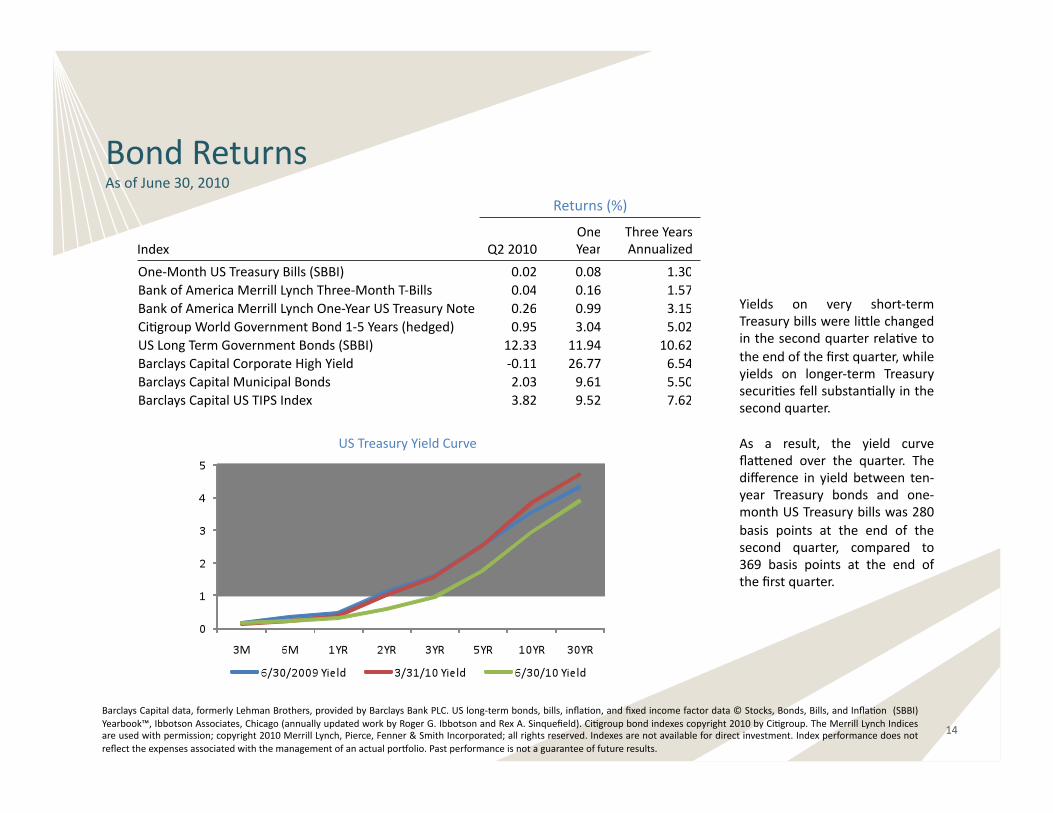

BondReturnsAsofJune30,2010

BarclaysCapitaldata,formerlyLehmanBrothers,providedbyBarclaysBankPLC.USlong‐termbonds,bills,inflaAon,andfixedincomefactordata©Stocks,Bonds,Bills,andInflaAon (SBBI)Yearbook™,IbbotsonAssociates,Chicago(annuallyupdatedworkbyRogerG.IbbotsonandRexA.Sinquefield).CiAgroupbondindexescopyright2010byCiAgroup.TheMerrillLynchIndicesareusedwithpermission;copyright2010MerrillLynch,Pierce,Fenner&SmithIncorporated;allrightsreserved.Indexesarenotavailablefordirectinvestment.Indexperformancedoesnotreflecttheexpensesassociatedwiththemanagementofanactualporholio.Pastperformanceisnotaguaranteeoffutureresults.

Returns(%)

Index Q22010OneYear

ThreeYearsAnnualized

One‐MonthUSTreasuryBills(SBBI) 0.02 0.08 1.30BankofAmericaMerrillLynchThree‐MonthT‐Bills 0.04 0.16 1.57BankofAmericaMerrillLynchOne‐YearUSTreasuryNote 0.26 0.99 3.15CiAgroupWorldGovernmentBond1‐5Years(hedged) 0.95 3.04 5.02USLongTermGovernmentBonds(SBBI) 12.33 11.94 10.62BarclaysCapitalCorporateHighYield ‐0.11 26.77 6.54BarclaysCapitalMunicipalBonds 2.03 9.61 5.50BarclaysCapitalUSTIPSIndex 3.82 9.52 7.62

USTreasuryYieldCurve

Yields on very short‐termTreasurybillswerelillechangedinthesecondquarterrelaAvetotheendofthefirstquarter,whileyields on longer‐term TreasurysecuriAesfellsubstanAallyinthesecondquarter.

As a result, the yield curveflalened over the quarter. Thedifference in yield between ten‐year Treasury bonds and one‐monthUSTreasurybillswas280basis points at the end of thesecond quarter, compared to369 basis points at the end ofthefirstquarter.

14

15TreasuryNotesdatasource:Bloomberg.WallStreetJournalsurveyavailableathlp://online.wsj.com/.

QuarterlyTopic:ForecasAngInterestRatesSecondQuarter2010

It seemed so obvious. With the economy slowly recovering last year from the worst recession in decades and the federalgovernmentspendingtensofbillionstosAmulatejobgrowth,bothlaymenandexpertsalikeseemedtoagreethatinterestrateshadnowheretogobutup.Theyieldontheten‐yearU.S.TreasurynoteasofJune30,2009was3.52%,downfrom5.25%inJune2007butwellabovethe2.09%levelregisteredamidsttheworstofthecreditcrisisthepreviousDecember.WithretailsalesandhousingacAvityshowingsignsofgradualimprovement,theonlyquesAonappearedtobehowmuchhigherinterestrateswouldgo.

Amongfikyeconomic forecasters surveyedby theWSJ in2009, forty‐threeexpected the ten‐yearU.S.Treasurynoteyield tomovehigherovertheyearahead,withanaverageesAmateof4.13%.Sevenexpectedarateof5.00%orhigherwhileonlytwopredictedratestofallbelow3.00%.Theresult?Theten‐yearTreasuryyieldslumpedto2.95%onJune30,2010andrateson30‐yearmortgagesfelltotheirlowestlevelsinceFannieMaebegantrackingthemin1971.

Someobserversmaybetemptedtopokefunatthesehapless“experts”,implyingtheyareincompetentorpoorlyinformed.ThisinterpretaAon is flawed since it suggests that a teamof beler expertswould achieve amore accurate result. AmoreusefulexplanaAon is that even the most talented analysts are unlikely to make reliable predicAons and the poor showing by thisparAculargroupissimplywhatwewouldexpecttosee,justasokenasnot,ifmarketsareworkingfreelyandfairly.Today’sbondpricesalreadyreflectexpectaAonsfortomorrow’sbusinesscondiAonsandinflaAonandtheseexpectaAonscanchangequicklyinresponsetonewinformaAon.HowevertempAngitmaybetobelievethatwecanpredictthefuturebelerthanothermarketparAcipants throughcareful study, the resultsof theWSJ surveyaswell asnumerousotherefforts suggest this confidence ismisplaced.

Whatisthemessageforinvestors?PredicAnginterestratesandbondpricesisnoeasierthanpredicAngstockprices,andmakingdecisionsbasedonwhatappeartobecertainoutcomesattheAmecanokenprovecostly.Many investorsreconfiguredtheirporholiosinanAcipaAonofhigherinterestratesandhavepenalizedtheirresultswhiletheyarewaiAng. Insteadofseekingtopredicttheunpredictable,investorsaremuchmorelikelytoenhancetheirresultsbyfocusingontheelementstheycancontrol–riskexposure,diversificaAonandminimizingcostsandtaxes.

16

MichaelMoore

1120CrestlineCourt•LakeOswego•OR97034

Telephone:503‐635‐4457

www.crestlinecapital.net

Crestline Capital, LLCCC