39

Q2 2016 RESULTS July 29, 2016

| Date post: | 21-Jan-2017 |

| Category: |

Health & Medicine |

| Upload: | sanofi |

| View: | 19,480 times |

| Download: | 0 times |

Q2 2016 RESULTS July 29, 2016

2

Forward Looking Statements

This presentation contains forward-looking statements as defined in the Private Securities Litigation Reform Act of

1995, as amended. Forward-looking statements are statements that are not historical facts. These statements include

projections and estimates and their underlying assumptions, statements regarding plans, objectives, intentions and

expectations with respect to future financial results, events, operations, services, product development and potential,

and statements regarding future performance. Forward-looking statements are generally identified by the words

“expects”, “anticipates”, “believes”, “intends”, “estimates”, “plans” and similar expressions. Although Sanofi’s

management believes that the expectations reflected in such forward-looking statements are reasonable, investors are

cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which

are difficult to predict and generally beyond the control of Sanofi, that could cause actual results and developments to

differ materially from those expressed in, or implied or projected by, the forward-looking information and statements.

These risks and uncertainties include among other things, the uncertainties inherent in research and development,

future clinical data and analysis, including post marketing, decisions by regulatory authorities, such as the FDA or the

EMA, regarding whether and when to approve any drug, device or biological application that may be filed for any such

product candidates as well as their decisions regarding labelling and other matters that could affect the availability or

commercial potential of such product candidates, the absence of guarantee that the product candidates if approved will

be commercially successful, the future approval and commercial success of therapeutic alternatives, the Company’s

ability to benefit from external growth opportunities and/or obtain regulatory clearances, risks associated with

intellectual property and any related pending or future litigation and the ultimate outcome of such litigation, trends in

exchange rates and prevailing interest rates, volatile economic conditions, the impact of cost containment initiatives

and subsequent changes thereto, the average number of shares outstanding as well as those discussed or identified in

the public filings with the SEC and the AMF made by Sanofi, including those listed under “Risk Factors” and

“Cautionary Statement Regarding Forward-Looking Statements” in Sanofi’s annual report on Form 20-F for the year

ended December 31, 2015. Other than as required by applicable law, Sanofi does not undertake any obligation to

update or revise any forward-looking information or statements.

3

Agenda

3

Key Highlights

● Olivier Brandicourt - Chief Executive Officer

Sustaining Innovation in R&D

● Elias Zerhouni - President, Global R&D

Financial Results

● Jérôme Contamine - Executive Vice President, Chief Financial Officer

Q&A Session

● Olivier Charmeil - Executive Vice President, General Medicines & Emerging Markets

● Peter Guenter - Executive Vice President, Diabetes & Cardiovascular

● Carsten Hellmann - Executive Vice President, Merial

● David Loew - Executive Vice President, Sanofi Pasteur

● David P. Meeker - Executive Vice President, Sanofi Genzyme

KEY HIGHLIGHTS

4

Olivier Brandicourt

Chief Executive Officer

Q2 2016 FX

Impact

-€0.07

Decremental

EPS at CER

-€0.03

Q2 2015

Aggregate(1) Company Sales Business EPS

Aggregate Sales Down Slightly in Q2 2016 Largely Due to

Currency Headwinds in Emerging Markets

5

(1) Including Merial

(2) Reflecting reclassification of VaxServe from Sales to Other revenues

(3) On a reported basis, Q2 2016 Aggregate Sales were down -4.3% and Business EPS was down -7.1%

-2.1% at CER(3)

Q2 2016 FX

Impact

-€382m

Venezuela

-€193m

Incremental

Sales at

CER

+€175m

Q2 2015

-0.2% at CER(3)

€9,268m

€8,868m

€1.41

€1.31

(2)

6

Growth

at CER

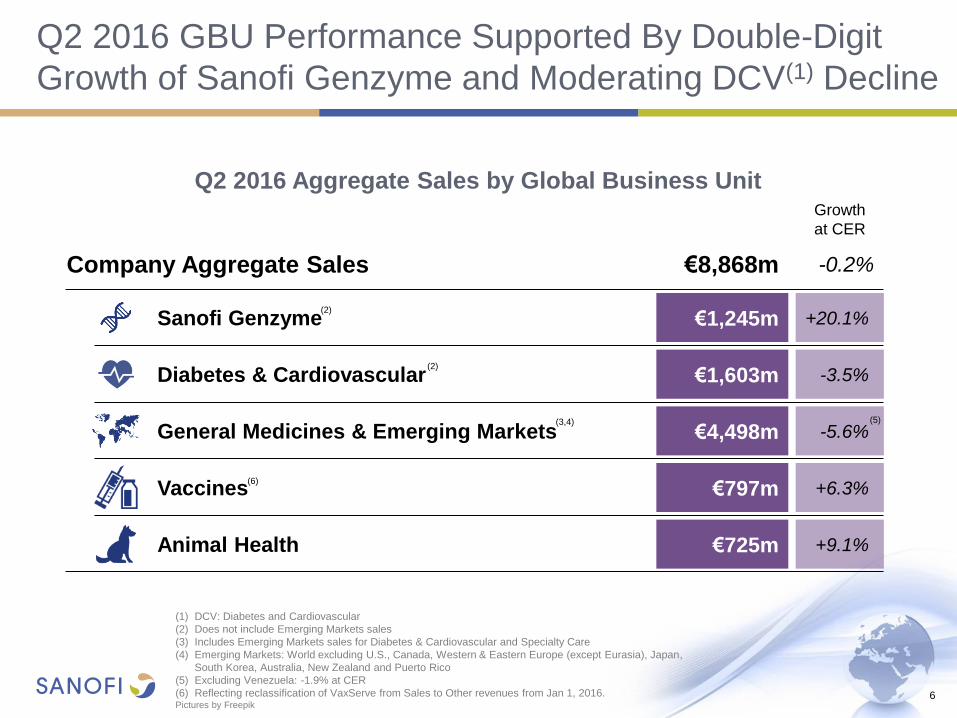

Q2 2016 GBU Performance Supported By Double-Digit

Growth of Sanofi Genzyme and Moderating DCV(1) Decline

(1) DCV: Diabetes and Cardiovascular

(2) Does not include Emerging Markets sales

(3) Includes Emerging Markets sales for Diabetes & Cardiovascular and Specialty Care

(4) Emerging Markets: World excluding U.S., Canada, Western & Eastern Europe (except Eurasia), Japan,

South Korea, Australia, New Zealand and Puerto Rico

(5) Excluding Venezuela: -1.9% at CER

(6) Reflecting reclassification of VaxServe from Sales to Other revenues from Jan 1, 2016. Pictures by Freepik

Q2 2016 Aggregate Sales by Global Business Unit

Company Aggregate Sales €8,868m

-0.2%

€725m

Animal Health

+9.1%

€1,603m

Diabetes & Cardiovascular -3.5% (2)

€1,245m

Sanofi Genzyme +20.1% (2)

€4,498m

General Medicines & Emerging Markets -5.6% (5) (3,4)

€797m

Vaccines

+6.3% (6)

7

Franchise Sales Driven by Specialty Care, Vaccines and

Animal Health Offset by Established Products

(1) Excluding Venezuela sales were up +11.4% at CER

(2) Excluding Plavix® in Japan, sales were down -4.9% at CER

(3) Excluding Venezuela sales were up +1.5% at CER

(4) Excluding Venezuela sales were down -1.8% at CER

Q2 2016 Aggregate Sales by Franchise

Developed Markets Emerging Markets

Growth

at CER

Total

Sales Growth Sales

Animal Health

+9.1% €725m +15.6% +7.3% €565m €160m

Specialty Care +19.5% €1,493m

+16.8% +20.1% €1,245m

€248m

Diabetes & Cardiovascular -2.0% €1,962m

+4.7% -3.5% €1,603m

€359m

Sales Growth

Vaccines

+6.3% €797m

+9.8% +3.8% €463m

€334m

Established Rx Products -9.7% €2,617m

-7.7% -10.9% €1,676m

€941m

Generics -1.9% €474m +2.6% -5.5% €271m €203m

Consumer Healthcare -4.3% €800m

-13.0% +2.1% €511m

€289m

(1)

(3)

(4)

(6)

(5) Excluding Venezuela sales were up +8.2% at CER

(6) Reflecting reclassification of VaxServe from Sales to Other revenues

from Jan 1, 2016

(5)

(2)

Q2 2015 Q2 2016

RareDiseases

MultipleSclerosis

Oncology

8

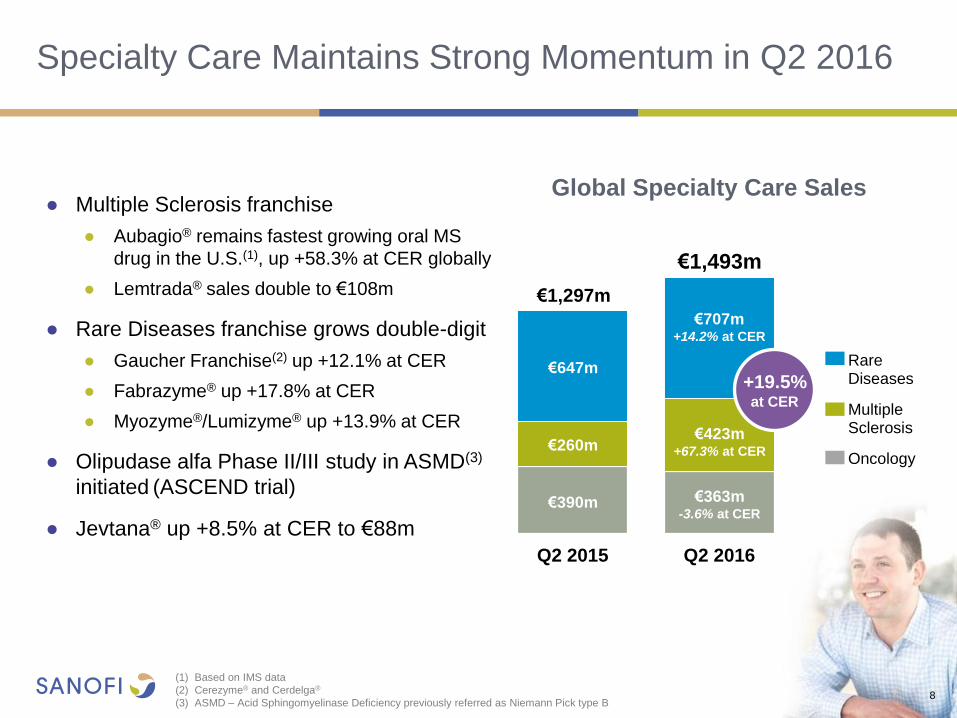

Specialty Care Maintains Strong Momentum in Q2 2016

● Multiple Sclerosis franchise

● Aubagio® remains fastest growing oral MS

drug in the U.S.(1), up +58.3% at CER globally

● Lemtrada® sales double to €108m

● Rare Diseases franchise grows double-digit

● Gaucher Franchise(2) up +12.1% at CER

● Fabrazyme® up +17.8% at CER

● Myozyme®/Lumizyme® up +13.9% at CER

● Olipudase alfa Phase II/III study in ASMD(3)

initiated (ASCEND trial)

● Jevtana® up +8.5% at CER to €88m

€243m

€647m

€1,493m

€707m +14.2% at CER

€423m +67.3% at CER

Global Specialty Care Sales

€260m

(1) Based on IMS data

(2) Cerezyme® and Cerdelga®

(3) ASMD – Acid Sphingomyelinase Deficiency previously referred as Niemann Pick type B

€390m €363m

-3.6% at CER

€1,297m

+19.5% at CER

Vaccines Grow due to Strong PPH Franchise in Q2

Dengvaxia® Uptake Delayed

9

PPH: Polio, Pertussis, Hib vaccines

(1) After VaxServe reclassification from the Sales P&L line to the Other revenues P&L line from January 1, 2016

● PPH franchise growth of +28.6% at CER

● Strong sales in Emerging Markets (+43.6%)

and Europe (+45.8%)

● Stable sales in the U.S. due to gradual

Pentacel® supply improvement

● Dengvaxia®

● Recent political changes and economic

volatility in Latin America delaying uptake

● Work progressing towards market access:

● Paraná becomes first Brazilian State to

announce immunization program

● Costa Rica becomes 5th country to approve

● 2016 sales unlikely to meet previous

company expectations

Sanofi Pasteur Sales(1)

Q2 2016

€797m

Q2 2015

€777m

Travel/Endemic

Meningitis/Pneumo

Other

Adult Boosters

Polio/Pertussis/Hib

Influenza Vaccines

(1)

+6.3% at CER

10

Diabetes Franchise Performs In-Line with Expectations

● Global Diabetes sales decline -3.2% at CER(1)

to €1,857m

● U.S. sales down -7.1%

● Emerging Markets sales up +5.0%(2)

● Toujeo® reached €141m in global sales

and 6.1% TRx market share in the U.S.(3)

● Adlyxin™ (lixisenatide), a once-daily mealtime

GLP-1R, FDA approved in July

● LixiLan(4) recommended for approval by FDA

Advisory Committee

(1) Growth excluding Venezuela was -2.0% at CER

(2) Growth excluding Venezuela +11.7% at CER

(3) IMS Rapid weekly as of July 15th 2016

(4) LixiLan is a project name and is not the intended brand name for the combination of insulin glargine and lixisenatide

€7m €13m

€46m

€98m €103m

€141m

Q1 Q2 Q3 Q4 Q1 Q2

Ex U.S.

U.S.

Quarterly Sales

2015 2016

Launch of Praluent® Progressing Globally

● Q2 2016 sales of €21m

● Market Access progressing

● Gradual improvement of U.S. payer

utilization management criteria

● UK NICE issues positive recommendation

● Additional reimbursement achieved in

Canada, Spain, Netherlands and Austria

● Praluent approved in Japan early July

● 300mg once-monthly dosing filed in U.S.

and EU

● ODYSSEY OUTCOMES second interim

data analysis for futility and overwhelming

efficacy potentially in Q4 2016(1)

U.S. TRx Market Share(2)

(1) When 75% of the targeted number of primary events have occurred

(2) IMS Rapid data week ending July 15th 2016 11

0%

10%

20%

30%

40%

50%

60%

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16

Emerging

Markets

€289m (-12.7%)

or

-1.5% excluding

Venezuela

12

CHC Franchise Grows by +2.7%

Excluding Venezuela Impact and at Constant Structure(1)

● Developed Markets

● Europe (+8.5%)(2) driven by cough and cold

season delayed to Q2 and strong Doliprane

performance due to successful DTC campaign

● U.S. sales (-0.8%) impacted by mild allergy

season

● Emerging Markets

● Down -12.7% as a result of Venezuela

currency devaluation and challenging

economic environment in Russia

● Boehringer Ingelheim asset swap signed in

June and expected to close by end of 2016(3)

(1) -4.3% at CER including Venezuela and small divested products

(2) Including the sales of small divested products in the 2015 base, growth at CER was +0.9%

(3) Subject to regulatory clearances

(4) Including the sales of small divested products in the 2015 base, growth at CER was +2.1%

Q2 2016 CHC Sales (growth at CER and constant structure)

36% 64%

Developed

Markets

€511m (+5.4%)(4)

€3,118m

€2,360m

€804m

€856m

€698m

EUROPE

+3.3%

ASIA

+5.3%

ROW(3)

-12.3%

LATAM(6)

-15.1%

U.S.

Balanced Geographic Profile Offset Challenges in

Select Countries in Q2 2016

13

Emerging Markets(1,2) €2,534m up +6.7% excluding Venezuela

+1.3%

€736m

AMESA(5)

+10.3%

€270m

EURASIA(4)

+4.3%

All Growth at Constant Exchange Rates

(1) World excluding U.S., Canada, Europe, Japan, South Korea, Australia, New

Zealand and Puerto Rico

(2) Growth including Venezuela was -0.5% at CER

(3) RoW: Japan, South Korea, Canada, Australia, New Zealand and Puerto Rico

(4) Eurasia: Russia, Ukraine, Georgia, Belarus, Armenia

and Turkey

(5) AMESA: Africa, Middle East and South Asia

(6) LATAM excluding Venezuela was +5.7% at CER

+5.7% Ex. VZ

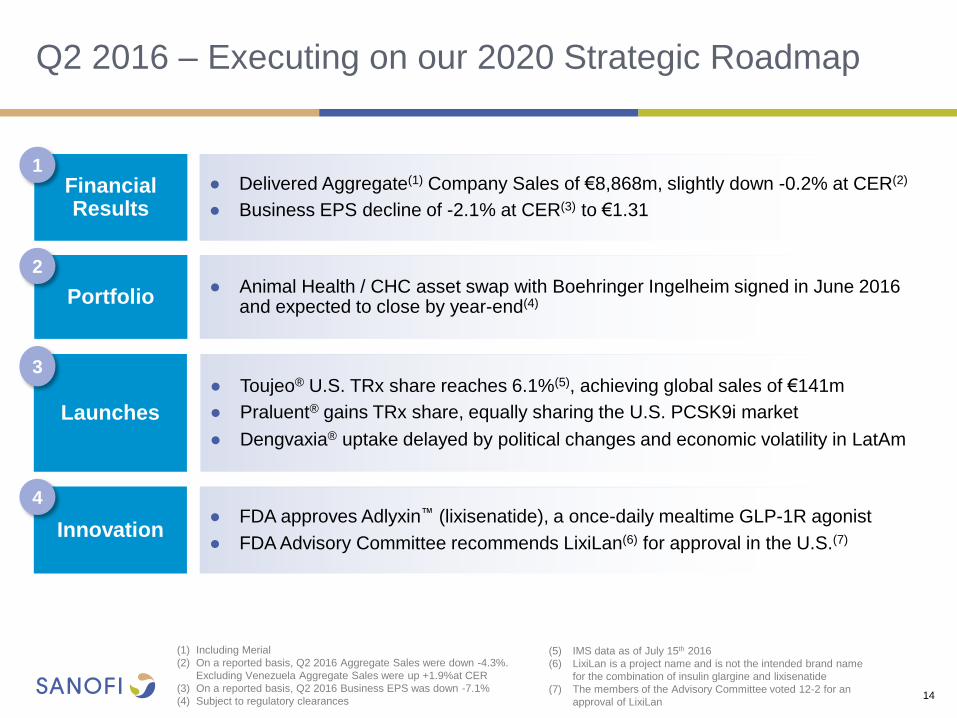

Q2 2016 – Executing on our 2020 Strategic Roadmap

14

(1) Including Merial

(2) On a reported basis, Q2 2016 Aggregate Sales were down -4.3%.

Excluding Venezuela Aggregate Sales were up +1.9%at CER

(3) On a reported basis, Q2 2016 Business EPS was down -7.1%

(4) Subject to regulatory clearances

● Toujeo® U.S. TRx share reaches 6.1%(5), achieving global sales of €141m

● Praluent® gains TRx share, equally sharing the U.S. PCSK9i market

● Dengvaxia® uptake delayed by political changes and economic volatility in LatAm

Launches

3

● Delivered Aggregate(1) Company Sales of €8,868m, slightly down -0.2% at CER(2)

● Business EPS decline of -2.1% at CER(3) to €1.31

Financial Results

1

● Animal Health / CHC asset swap with Boehringer Ingelheim signed in June 2016 and expected to close by year-end(4)

Portfolio

2

● FDA approves Adlyxin™ (lixisenatide), a once-daily mealtime GLP-1R agonist

● FDA Advisory Committee recommends LixiLan(6) for approval in the U.S.(7) Innovation

4

(5) IMS data as of July 15th 2016

(6) LixiLan is a project name and is not the intended brand name

for the combination of insulin glargine and lixisenatide

(7) The members of the Advisory Committee voted 12-2 for an

approval of LixiLan

SUSTAINING INNOVATION IN R&D

15

Elias Zerhouni

President, Global R&D

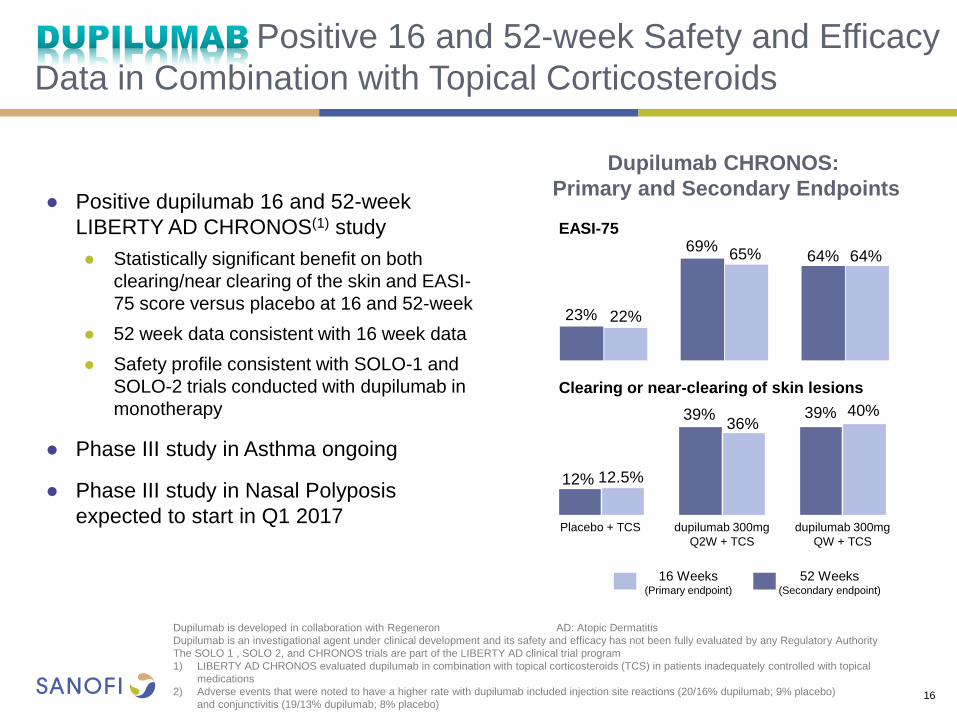

Positive 16 and 52-week Safety and Efficacy

Data in Combination with Topical Corticosteroids

16

● Positive dupilumab 16 and 52-week

LIBERTY AD CHRONOS(1) study

● Statistically significant benefit on both

clearing/near clearing of the skin and EASI-

75 score versus placebo at 16 and 52-week

● 52 week data consistent with 16 week data

● Safety profile consistent with SOLO-1 and

SOLO-2 trials conducted with dupilumab in

monotherapy

● Phase III study in Asthma ongoing

● Phase III study in Nasal Polyposis

expected to start in Q1 2017

Dupilumab is developed in collaboration with Regeneron AD: Atopic Dermatitis

Dupilumab is an investigational agent under clinical development and its safety and efficacy has not been fully evaluated by any Regulatory Authority

The SOLO 1 , SOLO 2, and CHRONOS trials are part of the LIBERTY AD clinical trial program

1) LIBERTY AD CHRONOS evaluated dupilumab in combination with topical corticosteroids (TCS) in patients inadequately controlled with topical

medications

2) Adverse events that were noted to have a higher rate with dupilumab included injection site reactions (20/16% dupilumab; 9% placebo)

and conjunctivitis (19/13% dupilumab; 8% placebo)

Clearing or near-clearing of skin lesions

39% 40%

dupilumab 300mg

QW + TCS

Placebo + TCS dupilumab 300mg

Q2W + TCS

12% 12.5%

39% 36%

52 Weeks (Secondary endpoint)

16 Weeks (Primary endpoint)

65% 64%

22%

64% 69%

23%

EASI-75

Dupilumab CHRONOS:

Primary and Secondary Endpoints

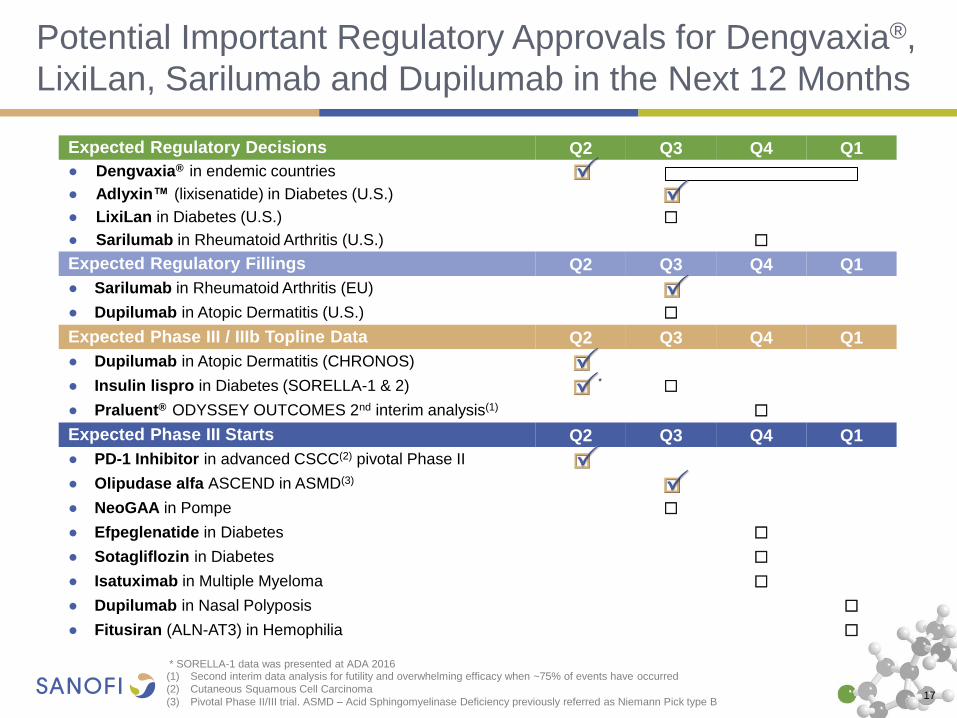

Expected Regulatory Decisions Q2 Q3 Q4 Q1

● Dengvaxia® in endemic countries

● Adlyxin™ (lixisenatide) in Diabetes (U.S.)

● LixiLan in Diabetes (U.S.)

● Sarilumab in Rheumatoid Arthritis (U.S.)

Expected Regulatory Fillings Q2 Q3 Q4 Q1

● Sarilumab in Rheumatoid Arthritis (EU)

● Dupilumab in Atopic Dermatitis (U.S.)

Expected Phase III / IIIb Topline Data Q2 Q3 Q4 Q1

● Dupilumab in Atopic Dermatitis (CHRONOS)

● Insulin lispro in Diabetes (SORELLA-1 & 2)

● Praluent® ODYSSEY OUTCOMES 2nd interim analysis(1)

Expected Phase III Starts Q2 Q3 Q4 Q1

● PD-1 Inhibitor in advanced CSCC(2) pivotal Phase II

● Olipudase alfa ASCEND in ASMD(3)

● NeoGAA in Pompe

● Efpeglenatide in Diabetes

● Sotagliflozin in Diabetes

● Isatuximab in Multiple Myeloma

● Dupilumab in Nasal Polyposis

● Fitusiran (ALN-AT3) in Hemophilia

17

Potential Important Regulatory Approvals for Dengvaxia®,

LixiLan, Sarilumab and Dupilumab in the Next 12 Months

* SORELLA-1 data was presented at ADA 2016

*

(1) Second interim data analysis for futility and overwhelming efficacy when ~75% of events have occurred

(2) Cutaneous Squamous Cell Carcinoma

(3) Pivotal Phase II/III trial. ASMD – Acid Sphingomyelinase Deficiency previously referred as Niemann Pick type B

FINANCIAL RESULTS

Jérôme Contamine

Executive Vice President, Chief Financial Officer

18

CER: Constant Exchange Rates

(1) Reflecting reclassification of VaxServe from Sales to Other revenues. VaxServe sales of non-Company products were €110m in Q2 2015

and €89m in Q2 2016 19

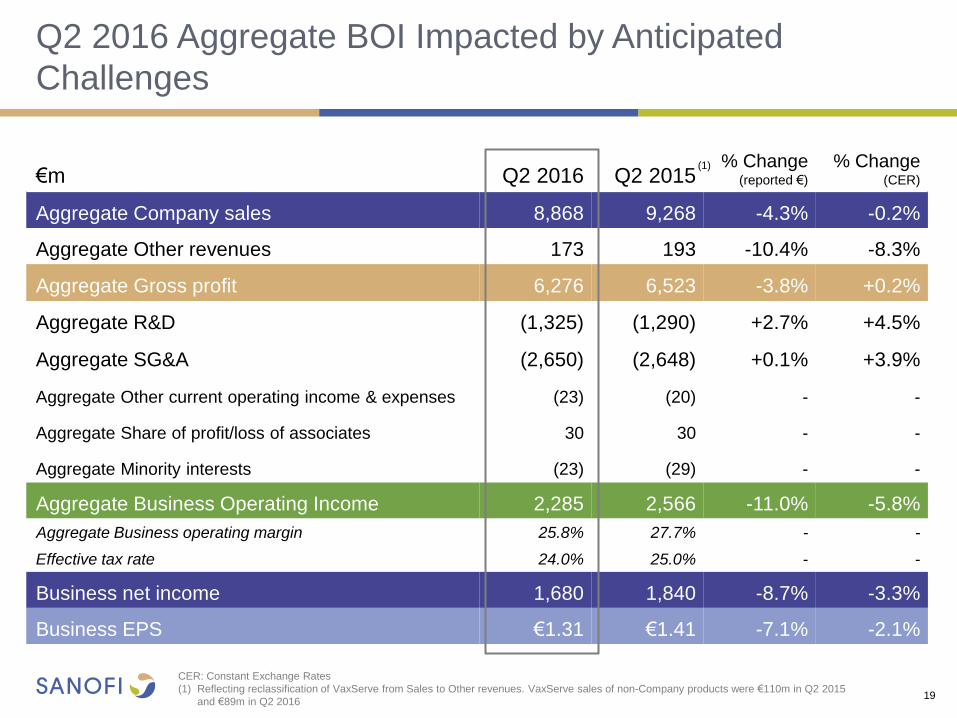

Q2 2016 Aggregate BOI Impacted by Anticipated

Challenges

€m Q2 2016 Q2 2015 % Change

(reported €)

% Change (CER)

Aggregate Company sales 8,868 9,268 -4.3% -0.2%

Aggregate Other revenues 173 193 -10.4% -8.3%

Aggregate Gross profit 6,276 6,523 -3.8% +0.2%

Aggregate R&D (1,325) (1,290) +2.7% +4.5%

Aggregate SG&A (2,650) (2,648) +0.1% +3.9%

Aggregate Other current operating income & expenses (23) (20) - -

Aggregate Share of profit/loss of associates 30 30 - -

Aggregate Minority interests (23) (29) - -

Aggregate Business Operating Income 2,285 2,566 -11.0% -5.8%

Aggregate Business operating margin 25.8% 27.7% - -

Effective tax rate 24.0% 25.0% - -

Business net income 1,680 1,840 -8.7% -3.3%

Business EPS €1.31 €1.41 -7.1% -2.1%

(1)

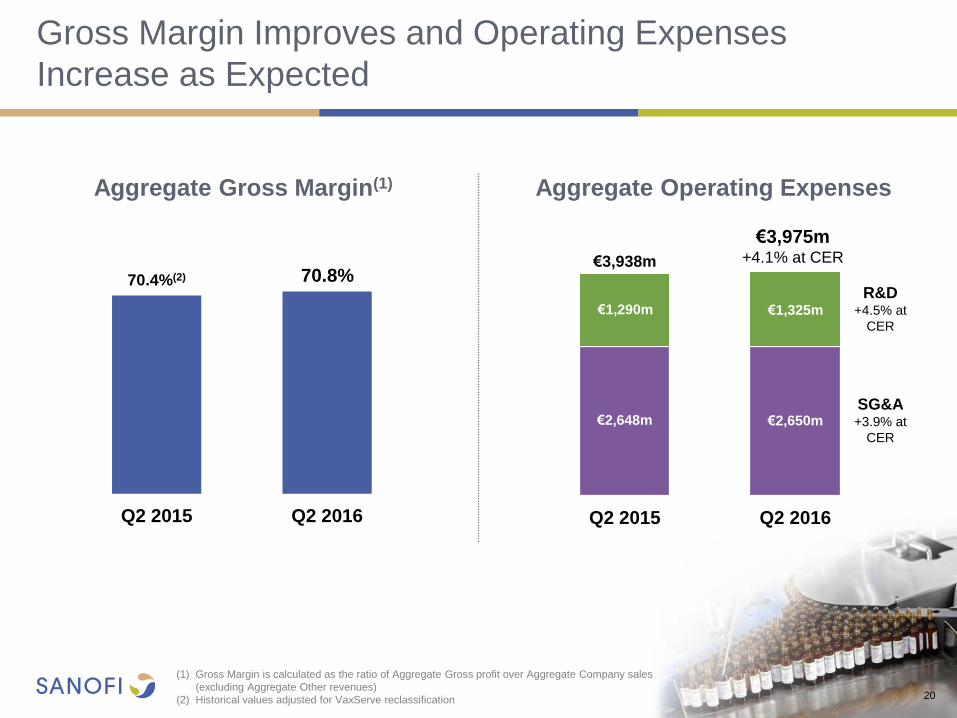

Q2 2015 Q2 2016

€3,975m +4.1% at CER €3,938m

€1,325m €1,290m

€2,650m €2,648m

R&D +4.5% at

CER

SG&A +3.9% at

CER

Gross Margin Improves and Operating Expenses

Increase as Expected

20

Aggregate Operating Expenses

(1) Gross Margin is calculated as the ratio of Aggregate Gross profit over Aggregate Company sales

(excluding Aggregate Other revenues)

(2) Historical values adjusted for VaxServe reclassification

Q2 2015 Q2 2016

Aggregate Gross Margin(1)

70.4%(2) 70.8%

21

FX Remains a Headwind due Largely to Evolution of

Emerging Market Currencies in H1 2016

(1) Main currency impact on sales in Q2 2016: U.S. Dollar (-€66.7m), Argentine Peso (-€45.3m), Brazilian Real (-€44.1m),

Chinese Yuan Renminbi (-€38.1m), Russian Ruble (-€29.2m), Mexican Peso (-€24.7m) and Japanese Yen (+€34.8m)

(2) Excluding VaxServe in Aggregate Company Sales

+11.1%

+€888m

+5.6%

+€487m

-2.6%

-€228m

Q2 2016

Q2 2015 Q3 2015 Q4 2015

Q1 2016

+3.7%

+€332m

Q2 2016

Q2 2015 Q3 2015 Q4 2015

Q1 2016

+15.4%

+€0.18

+€0.05

+3.4%

+7.1%

+€0.10

-3.8%

-€0.05

Currency Impact

Aggregate Company Sales(1,2) Business EPS

-4.1%

-€382m

-5.0%

-€0.07

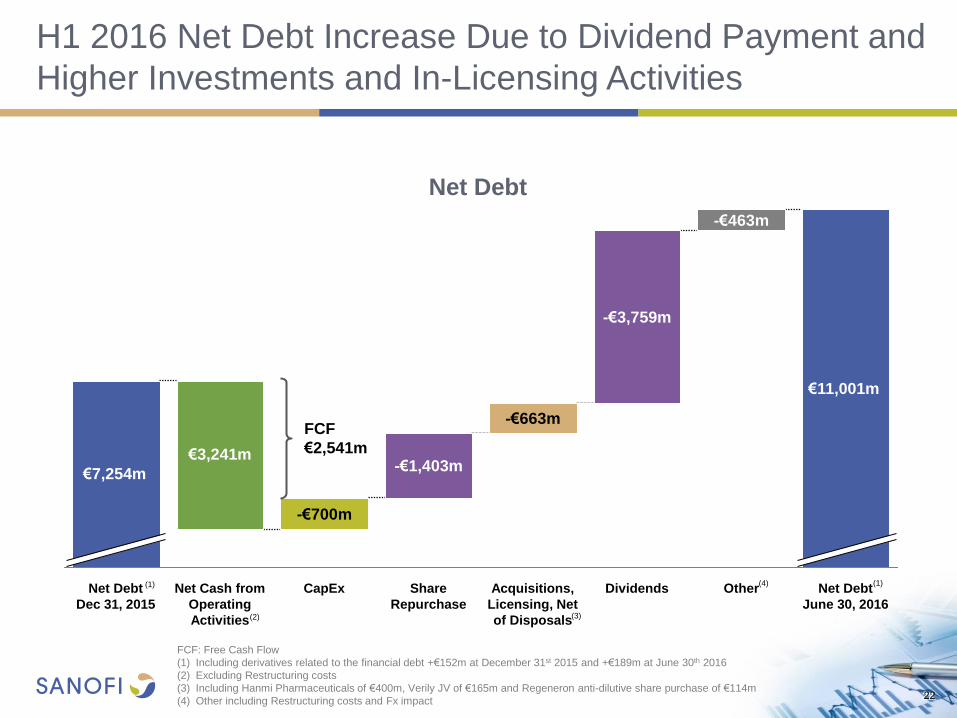

Net Debt

June 30, 2016

Other

-€463m

Dividends

-€3,759m

Acquisitions,

Licensing, Net

of Disposals

-€663m

Share

Repurchase

-€1,403m

CapEx

-€700m

Net Cash from

Operating

Activities

Net Debt

Dec 31, 2015

22

(1)

(2)

€7,254m

€11,001m

€3,241m

(4) (1)

FCF

€2,541m

(3)

FCF: Free Cash Flow

(1) Including derivatives related to the financial debt +€152m at December 31st 2015 and +€189m at June 30th 2016

(2) Excluding Restructuring costs

(3) Including Hanmi Pharmaceuticals of €400m, Verily JV of €165m and Regeneron anti-dilutive share purchase of €114m

(4) Other including Restructuring costs and Fx impact

Net Debt

22

H1 2016 Net Debt Increase Due to Dividend Payment and

Higher Investments and In-Licensing Activities

23

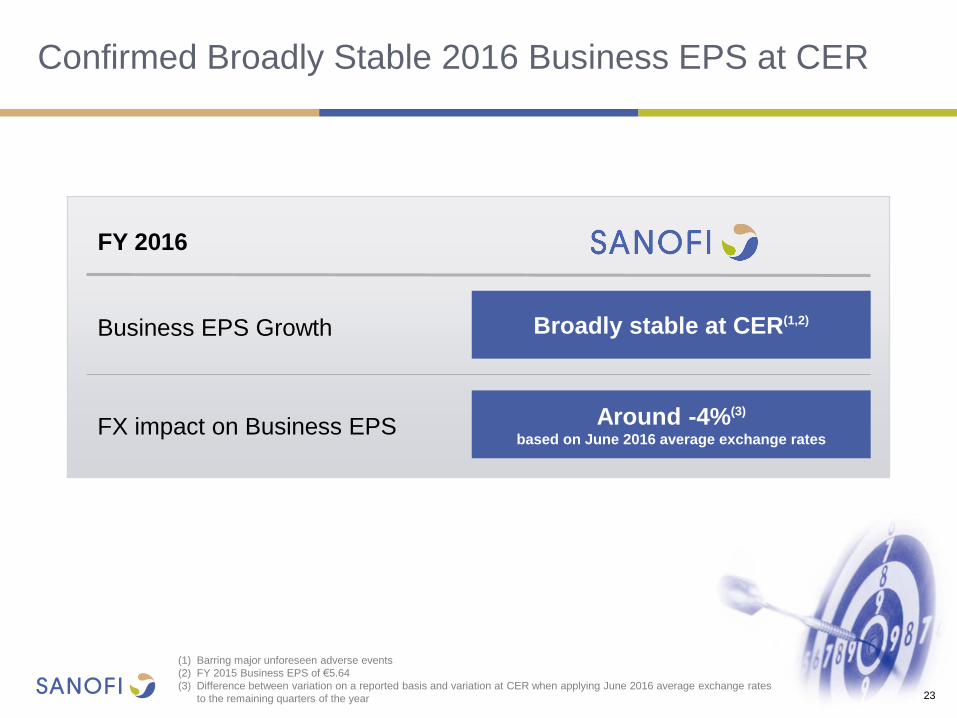

(1) Barring major unforeseen adverse events

(2) FY 2015 Business EPS of €5.64

(3) Difference between variation on a reported basis and variation at CER when applying June 2016 average exchange rates

to the remaining quarters of the year

Confirmed Broadly Stable 2016 Business EPS at CER

Business EPS Growth

Around -4%(3)

based on June 2016 average exchange rates

Broadly stable at CER(1,2)

FY 2016

FX impact on Business EPS

CLOSING REMARKS

24

Olivier Brandicourt

Chief Executive Officer

25

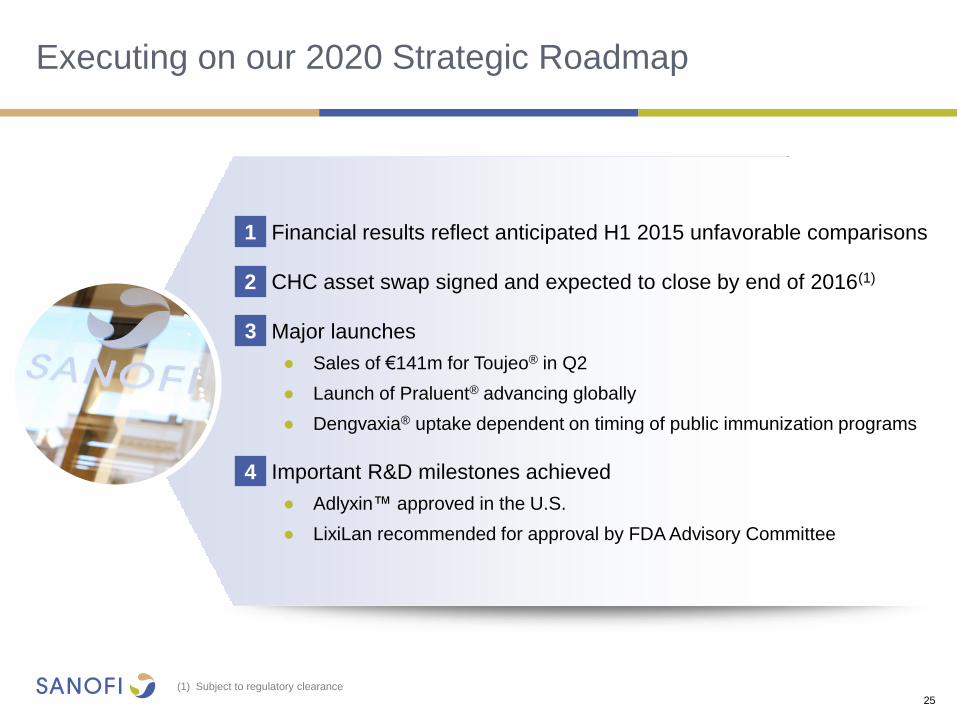

Executing on our 2020 Strategic Roadmap

● Financial results reflect anticipated H1 2015 unfavorable comparisons

● CHC asset swap signed and expected to close by end of 2016(1)

● Major launches

● Sales of €141m for Toujeo® in Q2

● Launch of Praluent® advancing globally

● Dengvaxia® uptake dependent on timing of public immunization programs

● Important R&D milestones achieved

● Adlyxin™ approved in the U.S.

● LixiLan recommended for approval by FDA Advisory Committee

1

2

4

3

(1) Subject to regulatory clearance

26

Q&A SESSION

27

APPENDICES

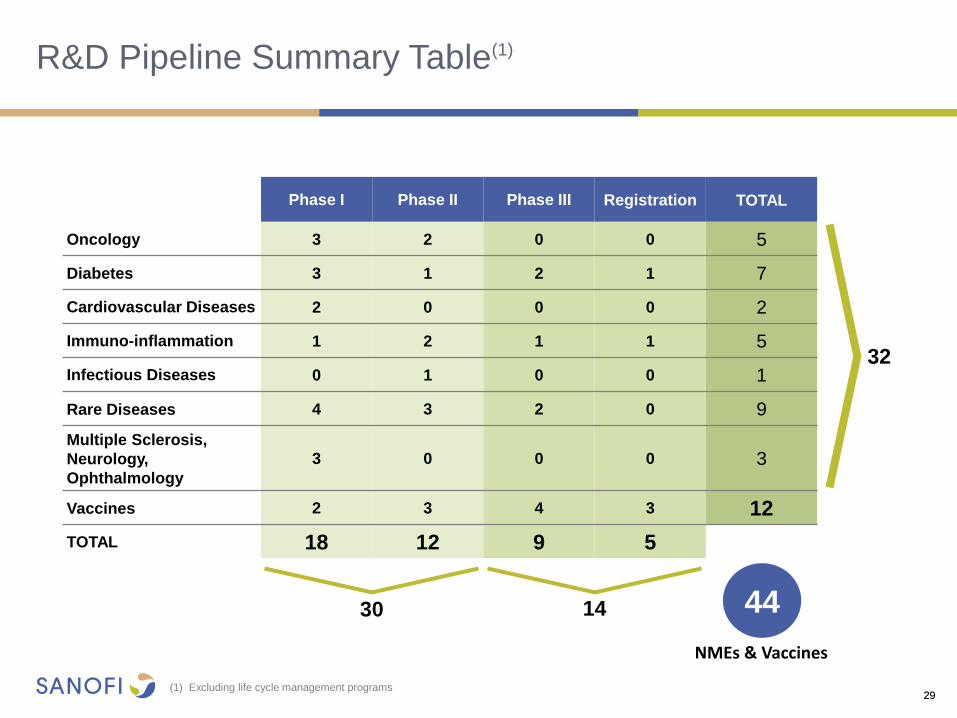

R&D Pipeline

dupilumab Anti-IL4Rα mAb Nasal polyposis;

Eosinophilic oesophagitis

olipudase alfa rhASM Deficiency

Niemann-Pick type B

SAR156597 IL4/IL13 Bi-specific mAb

Idiopathic pulmonary fibrosis

GZ402671 Oral GCS inhibitor

Fabry Disease

SAR100842 LPA1 receptor antagonist

Systemic sclerosis

SAR422459 ABCA4 gene therapy

Stargardt disease

sotagliflozin Oral SGLT-1&2 inhibitor

Type 2 diabetes

Combination

ferroquine / OZ439 Antimalarial

efpeglenatiden Long-acting GLP-1 receptor agonist

Type 2 diabetes

Rabies VRVg Purified vero rabies vaccine

sarilumab Anti-IL6R mAb

Uveitis

Tuberculosis Recombinant subunit vaccine

isatuximab Anti-CD38 naked mAb

Multiple myeloma

Fluzone® QIV HD Quadrivalent inactivated

influenza vaccine - High dose

SAR439684 PD-1 inhibitor

Advanced CSCC (Skin cancer)

Immuno-inflammation

Infectious Diseases

MS, Neurology, Ophthalmology

GZ402668 GLD52 (anti-CD52 mAb)

Relapsing multiple sclerosis

GZ402666 neoGAA

Pompe Disease

GZ389988 TRKA antagonist

Osteoarthritis

SAR339375 Anti-miR21 RNA

Alport syndrome

SAR425899 GLP-1R/GCGR dual agonist

Type 2 diabetes

fitusiran (ALN-AT3)

siRNA targeting Anti-Thrombin

Hemophilia

SAR438335 GLP-1R/GIPR dual agonist

Type 2 diabetes

UshStat® Myosin 7A gene therapy

Usher syndrome 1B

SAR440067 (LAPS Insulin 115)nn

Long acting insulin analog

Type 1 & 2 diabetes

SAR228810 Anti-protofibrillar AB mAb

Alzheimer’s disease

SAR566658

Maytansin-loaded anti-CA6 mAb

Solid tumors

SAR439152 Myosin inhibitor

Hypertrophic cardiomyopathy

SAR408701 Maytansin-loaded

Anti-CEACAM5 mAb

Solid tumors

SAR407899 rho kinase

Microvascular angina

SAR428926 Maytansin loaded anti-Lamp1 mAb

Cancer

SAR366234 EP2 receptor agonist

Elevated intraocular pressure

Streptococcus pneumonia Meningitis & pneumonia vaccine

Herpes Simplex Virus Type 2 HSV-2 vaccine

R&D Pipeline – Pharma & Vaccines

Phase I

N

N

N

N

N

N

N

N

N

N

N

N

N

N

Phase II N

N

N N

N

SAR342434 insulin lispro

Type 1+2 diabetes

sotagliflozin n

Oral SGLT-1&2 inhibitor

Type 1 diabetes

dupilumab Anti-IL4Rα mAb

Atopic dermatitis, Asthma

patisiran (ALN-TTR02)

siRNA inhibitor targeting TTR Familial amyloidotic polyneuropathy

revusiran (ALN-TTRsc)

siRNA inhibitor targeting TTR Familial amyloidotic cardiomyopathy

Clostridium difficile Toxoid vaccine

VaxiGrip® QIV IM Quadrivalent inactivated

influenza vaccine (6-35 months)

Pediatric pentavalent vaccine DTP-Polio-Hib

Japan

Men Quad TT 2nd generation meningococcal

ACYW conjugate vaccine

Phase III

N

N

N

N

Registration

LixiLan Fixed-Ratio insulin glargine+lixisenatide

Type 2 diabetes, U.S., EU

sarilumab Anti-IL6R mAb

Rheumatoid arthritis, U.S., EU

Dengvaxia®(1) Mild-to-severe

dengue fever vaccine

PR5i DTP-HepB-Polio-Hib

Pediatric hexav. vaccine, U.S.

VaxiGrip® QIV IM Quadrivalent inactivated

influenza vaccine (3 years+)

N

N

N

(1) Approved in Brazil, Mexico, the Philippines, El Salvador and Costa Rica 28

N N

N

N New Molecular Entity

Rare Diseases

Oncology Diabetes

Vaccines

Cardiovascular Diseases

N

N

N

29

Phase I Phase II Phase III Registration TOTAL

Oncology 3 2 0 0 5

Diabetes 3 1 2 1 7

Cardiovascular Diseases 2 0 0 0 2

Immuno-inflammation 1 2 1 1 5

Infectious Diseases 0 1 0 0 1

Rare Diseases 4 3 2 0 9

Multiple Sclerosis,

Neurology,

Ophthalmology

3 0 0 0 3

Vaccines 2 3 4 3 12

TOTAL 18

12 9 5

R&D Pipeline Summary Table(1)

30 14

NMEs & Vaccines

44

29

32

(1) Excluding life cycle management programs

30

Expected R&D Milestones

30

Product Event Timing

Dengvaxia® Expected regulatory decisions in endemic countries Throughout 2016

dupilumab Expected U.S. regulatory filing in Atopic Dermatitis Q3 2016

insulin lispro Expected SORELLA 2 Phase III top line results in Diabetes Q3 2016

NeoGAA (GZ402666) Expected start of Phase III trial in Pompe Disease Q3 2016

LixiLan Expected U.S. regulatory decision in Type 2 Diabetes Q3 2016

sarilumab Expected U.S. regulatory decision in Rheumatoid Arthritis Q4 2016

Praluent® Expected results of ODYSSEY OUTCOMES 2nd interim analysis(2) Q4 2016

VaxiGrip® QIV IM (3 years+) Expected EU regulatory decision Q4 2016

sotagliflozin Expected start of Phase III trial in Type 2 Diabetes Q4 2016

efpeglenatide Expected start of Phase III trial in Type 2 Diabetes Q4 2016

isatuximab (anti-CD38) Expected start of Phase III trial in Multiple Myeloma Q4 2016

dupilumab Expected start of Phase III trial in Nasal Polyposis Q1 2017

fitusiran Expected start of Phase III trial in Hemophilia Q1 2017

(1) Name received conditional approval

(2) Second interim data analysis for futility and overwhelming efficacy when ~75% of events have occurred

APPENDICES

FINANCE

31

Business EPS Currency Sensitivity

Currency Exposure on Q2 2016 Sales Currency Average Rates

2016 - Currency Sensitivity

32

Q2 2015 Q2 2016 % change

EUR/USD 1.10 1.13 +2.2%

EUR/JPY 134.14 121.98 -9.1%

EUR/CNY 6.85 7.38 +7.7%

EUR/BRL 3.39 3.96 +16.8%

EUR/RUB 58.12 74.35 +27.9%

Currency Variation Business EPS Sensitivity

U.S. Dollar -0.05 USD/EUR +EUR 0.13

Japanese Yen +5 JPY/EUR -EUR 0.02

Chinese Yuan +0.2 CNY/EUR -EUR 0.02

Brazilian Real +0.4 BRL/EUR -EUR 0.01

Russian Ruble +10 RUB/EUR -EUR 0.04

€ 24.5%

US $ 36.1%

Chinese Yuan 5.8%

Japanese Yen 4.9%

Brazilian Real 2.7%

British £ 1.9%

Australian $ 1.6%

Canadian $ 1.4%

Mexican Peso 1.3%

Russian Ruble1.2%

Others 18.6%

33

Business Net Income Statement

* Net of tax.

** Determined on the basis of Business income before tax, associates and non-controlling interests.

*** Based on an average number of shares outstanding of 1,286.8 million in the second quarter of 2016 and 1,305.9 million in the second quarter of 2015.

(1) Pursuant to IFRS5 presentation requirement as "discontinued operations”, Animal Health business net result is reported on the single income statement line Net income from

held-for-exchange Animal Health business for 2016 and prior years. Until the closing of the transaction, Animal Health remains an operating segment of the Company.

(2) Including Animal Health Business which is reported on a single line in the consolidated income statements in accordance with IFRS5 (Non-current held for sale and

discontinued operations).

(3) As per a change in accounting presentation, VaxServe sales of non-Company products are reported in Other revenues from 2016 onwards. Prior period Net sales and Other

revenues have been represented accordingly.

(4) Aggregate amount including Animal Health business.

Second Quarter 2016 Pharmaceuticals Vaccines Others Total Company Animal Health (1) Total: aggregate basis (2)

€ million Q2 2016 Q2 2015 Change Q2 2016 Q2 2015 Change Q2 2016 Q2 2015 Q2 2016 Q2 2015 Q2 2016 Q2 2015 Change Q2 2016 Q2 2015 Change

Net sales 7,346 7,800 (5.8%) 797 777 2.6% - - 8,143 8,577 725 691 4.9% 8,868 9,268 (4.3%)

Other revenues (3) 68 67 1.5% 97 118 (17.8%) - - 165 185 8 8 - 173 193 (10.4%)

Cost of sales (2,046) (2,252) (9.1%) (477) (450) 6.0% - - (2,523) (2,702) (242) (236) 2.5% (2,765) (2,938) (5.9%)

As % of net sales (27.9%) (28.9%) (59.8%) (57.9%) - - (31.0%) (31.5%) (33.4%) (34.2%) (31.2%) (31.7%)

Gross profit 5,368 5,615 (4.4%) 417 445 (6.3%) - - 5,785 6,060 491 463 6.0% 6,276 6,523 (3.8%)

As % of net sales 73.1% 72.0% 52.3% 57.3% - - 71.0% 70.7% 67.7% 67.0% 70.8% 70.4%

Research and development

expenses (1,138) (1,104) 3.1% (141) (142) (0.7%) - - (1,279) (1,246) (46) (44) 4.5% (1,325) (1,290) 2.7%

As % of net sales (15.5%) (14.2%)

(17.7%) (18.3%) - - (15.7%) (14.5%) (6.3%) (6.4%) (14.9%) (13.9%)

Selling and general expenses (2,215) (2,216) (0.0%) (182) (188) (3.2%) - - (2,397) (2,404) (253) (244) 3.7% (2,650) (2,648) 0.1%

As % of net sales (30.2%) (28.4%) (22.8%) (24.2%) - - (29.4%) (28.0%) (34.9%) (35.3%) (29.9%) (28.6%)

Other current operating

income/expenses 3 (11) (1) 1 (25) (15) (23) (25) - 5 (23) (20)

Share of profit/loss of

associates* and joint ventures 28 29 2 1 - - 30 30 - - 30 30

Net income attributable to

non-controlling interests (23) (29) - - - - (23) (29) - - (23) (29)

Business operating income 2,023 2,284 (11.4%) 95 117 (18.8%) (25) (15) 2,093 2,386 192 180 6.7% 2,285 2,566 (11.0%)

As % of net sales 27.5% 29.3% 11.9% 15.1% 25.7% 27.8% 26.5% 26.0% 25.8% 27.7%

Financial income and

expenses (4) (76) (112)

Income tax expense (4) (529) (614)

Tax rate** 24.0% 25.0%

Business net income 1,680 1,840 (8.7%)

As % of net sales 18.9% 19.9%

Business earnings per

share*** (in euros) 1.31 1.41 (7.1%)

34

Business Net Income Statement

* Net of tax.

** Determined on the basis of Business income before tax, associates and non-controlling interests.

*** Based on an average number of shares outstanding of 1,287.6 million in the first semester of 2016 and 1,307.2 million in the first semester of 2015.

(1) Pursuant to IFRS5 presentation requirement as "discontinued operations”, Animal Health business net result is reported on the single income statement line Net income

from held-for-exchange Animal Health business for 2016 and prior years. Until the closing of the transaction, Animal Health remains an operating segment of the Company.

(2) Including Animal Health Business which is reported on a single line in the consolidated income statements in accordance with IFRS5 (Non-current held for sale and

discontinued operations).

(3) As per a change in accounting presentation, VaxServe sales of non-Company products are reported in Other revenues from 2016 onwards. Prior period Net sales and

Other revenues have been represented accordingly.

(4) Aggregate amount including Animal Health business.

First Half 2016 Pharmaceuticals Vaccines Others Total Company Animal Health (1) Total: aggregate basis (2)

€ million H1 2016 H1 2015 Change H1 2016 H1 2015 Change H1 2016 H1 2015 H1 2016 H1 2015 H1 2016 H1 2015 Change H1 2016 H1 2015 Change

Net sales 14,504 15,255 (4.9%) 1,422 1,374 3.5% - - 15,926 16,629 1,485 1,349 10.1% 17,411 17,978 (3.2%)

Other revenues (3) 122 129 (5.4%) 188 224 (16.1%) - - 310 353 18 20 (10.0%) 328 373 (12.1%)

Cost of sales (4,143) (4,442) (6.7%) (827) (826) 0.1% - - (4,970) (5,268) (488) (456) 7.0% (5,458) (5,724) (4.6%)

As % of net sales (28.6%) (29.1%) (58.2%) (60.1%) - - (31.2%) (31.7%) (32.9%) (33.8%) (31.3%) (31.8%)

Gross profit 10,483 10,942 (4.2%) 783 772 1.4% - - 11,266 11,714 1,015 913 11.2% 12,281 12,627 (2.7%)

As % of net sale 72.3% 71.7% 55.1% 56.2% - - 70.7% 70.4% 68.4% 67.7% 70.5% 70.2%

Research and development

expenses (2,246) (2,143) 4.8% (268) (262) 2.3% - - (2,514) (2,405) (89) (84) 6.0% (2,603) (2,489) 4.6%

As % of net sales (15.5%) (14.0%) (18.8%) (19.1%) - - (15.8%) (14.5%) (6.0%) (6.2%) (15.0%) (13.8%)

Selling and general expenses (4,261) (4,310) (1.1%) (348) (344) 1.2% - - (4,609) (4,654) (459) (432) 6.3% (5,068) (5,086) (0.4%)

As % of net sales (29.4%) (28.3%) (24.5%) (25.0%) - - (28.9%) (28.0%) (30.9%) (32.0%) (29.1%) (28.3%)

Other current operating

income/expenses 110 (39) (1) 2 (39) (55) 70 (92) (14) 5 56 (87)

Share of profit/loss of

associates* and joint ventures 44 61 9 - - - 53 61 - - 53 61

Net income attributable to

non-controlling interests (50) (62) - - - - (50) (62) - - (50) (62)

Business operating income 4,080 4,449 (8.3%) 175 168 4.2% (39) (55) 4,216 4,562 453 402 12.7% 4,669 4,964 (5.9%)

As % of net sales 28.1% 29.2% 12.3% 12.2% - 26.5% 27.4% 30.5% 29.8% 26.8% 27.6%

Financial income and

expenses (4) (194) (209)

Income tax expense (4) (1,073) (1,189)

Tax rate** 24.0% 25.0%

Business net income 3,402 3,566 (4.6%)

As % of net sales 19.5% 19.8%

Business earnings per

share*** (in euros) 2.64 2.73 (3.3%)

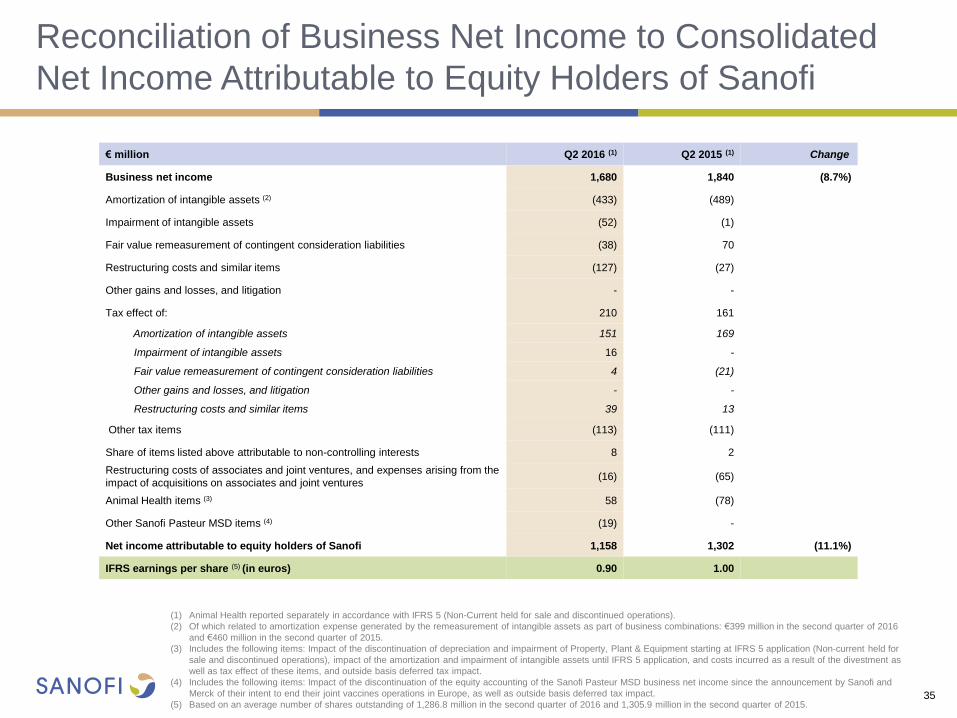

Reconciliation of Business Net Income to Consolidated

Net Income Attributable to Equity Holders of Sanofi

35

(1) Animal Health reported separately in accordance with IFRS 5 (Non-Current held for sale and discontinued operations).

(2) Of which related to amortization expense generated by the remeasurement of intangible assets as part of business combinations: €399 million in the second quarter of 2016

and €460 million in the second quarter of 2015.

(3) Includes the following items: Impact of the discontinuation of depreciation and impairment of Property, Plant & Equipment starting at IFRS 5 application (Non-current held for

sale and discontinued operations), impact of the amortization and impairment of intangible assets until IFRS 5 application, and costs incurred as a result of the divestment as

well as tax effect of these items, and outside basis deferred tax impact.

(4) Includes the following items: Impact of the discontinuation of the equity accounting of the Sanofi Pasteur MSD business net income since the announcement by Sanofi and

Merck of their intent to end their joint vaccines operations in Europe, as well as outside basis deferred tax impact.

(5) Based on an average number of shares outstanding of 1,286.8 million in the second quarter of 2016 and 1,305.9 million in the second quarter of 2015.

€ million Q2 2016 (1) Q2 2015 (1) Change

Business net income 1,680 1,840 (8.7%)

Amortization of intangible assets (2) (433) (489)

Impairment of intangible assets (52) (1)

Fair value remeasurement of contingent consideration liabilities (38) 70

Restructuring costs and similar items (127) (27)

Other gains and losses, and litigation - -

Tax effect of: 210 161

Amortization of intangible assets 151 169

Impairment of intangible assets 16 -

Fair value remeasurement of contingent consideration liabilities 4 (21)

Other gains and losses, and litigation - -

Restructuring costs and similar items 39 13

Other tax items (113) (111)

Share of items listed above attributable to non-controlling interests 8 2

Restructuring costs of associates and joint ventures, and expenses arising from the

impact of acquisitions on associates and joint ventures (16) (65)

Animal Health items (3) 58 (78)

Other Sanofi Pasteur MSD items (4) (19) -

Net income attributable to equity holders of Sanofi 1,158 1,302 (11.1%)

IFRS earnings per share (5) (in euros) 0.90 1.00

Reconciliation of Business Net Income to Consolidated

Net Income Attributable to Equity Holders of Sanofi

36

(1) Animal Health reported separately in accordance with IFRS 5 (Non-Current Assets Held for Sale and Discontinued Operations).

(2) Of which related to amortization expense generated by the remeasurement of intangible assets as part of business combinations: 809 million in the first semester of 2016 and

€931 million in the first semester of 2015.

(3) Includes the following items: Impact of the discontinuation of depreciation and impairment of Property, Plant & Equipment starting at IFRS 5 application

(Non-current held for sale and discontinued operations), impact of the amortization and impairment of intangible assets until IFRS 5 application, and costs incurred as a result

of the divestment as well as tax effect of these items.

(4) Includes the following items: Impact of the discontinuation of the equity accounting of the Sanofi Pasteur MSD business net income since the announcement by Sanofi and Merck of

their intent to end their joint vaccins operations in Europe, as well as outside basis deferred tax impact.

(5) Based on an average number of shares outstanding of 1,287.6 million in the first semester of 2016 and 1,307.2 million in the first semester of 2015.

€ million H1 2016 (1) H1 2015 (1) Change

Business net income 3,402 3,566 (4.6%)

Amortization of intangible assets (2) (877) (988)

Impairment of intangible assets (52) (28)

Fair value remeasurement of contingent consideration liabilities (67) 71

Restructuring costs (627) (380)

Other gains and losses, and litigation - -

Tax effect of items listed above: 548 473

Amortization of intangible assets 307 343

Impairment of intangible assets 16 10

Fair value remeasurement of contingent consideration liabilities 15 (14)

Other gains and losses, and litigation - -

Restructuring costs and similar items 210 134

Other tax items (113) (111)

Share of items listed above attributable to non-controlling interests 9 3

Restructuring costs of associates and joint ventures, and expenses arising from the

impact of acquisitions on associates and joint ventures 54 (127)

Animal Health items (3) (13) (154)

Other Sanofi Pasteur MSD items (4) (19) -

Net income attributable to equity holders of Sanofi 2,245 2,325 (3.4%)

Consolidated earnings per share (5) (in euros) 1.74 1.78

37

Consolidated Income Statements

(1) Including Animal Health Business which is reported on a single line in the consolidated income statements in accordance with IFRS5

(Non-current held for sale and discontinued operations).

(2) As per a change in accounting presentation, VaxServe sales of non-Company products are reported in Other revenues from 2016 onwards. Prior period

Net sales and Other revenues have been restated accordingly.

€ million Q2 2016 (1) Q2 2015 (1)(2) H1 2016 (1) H2 2015 (1)(2)

Net sales 8,143 8,577 15,926 16,629

Other revenues 165 185 310 353

Cost of sales (2,523) (2,702) (4,970) (5,268)

Gross profit 5,785 6,060 11,266 11,714

Research and development expenses (1,279) (1,246) (2,514) (2,405)

Selling and general expenses (2,397) (2,404) (4,609) (4,654)

Other operating income 48 40 265 74

Other operating expenses (71) (65) (195) (166)

Amortization of intangible assets (433) (489) (877) (988)

Impairment of intangible assets (52) (1) (52) (28)

Fair value remeasurement of contingent consideration liabilities (38) 70 (67) 71

Restructuring costs and similar items (127) (27) (627) (380)

Operating income 1,436 1,938 2,590 3,238

Financial expenses (112) (131) (241) (262)

Financial income 38 21 50 57

Income before tax and associates and joint ventures 1,362 1,828 2,399 3,033

Income tax expense (380) (508) (497) (692)

Share of profit / loss of associates and joint ventures 5 (35) 98 (66)

Net income excluding the held for exchange Animal Health business 987 1,285 2,000 2,275

Net income from the held for exchange Animal Health Business 186 44 286 109

Net income 1,173 1,329 2,286 2,384

Net income attributable to non-controlling interests 15 27 41 59

Net income attributable to equity holders of Sanofi 1,158 1,302 2,245 2,325

Average number of shares outstanding (million) 1,286.8 1,305.9 1,287.6 1,307.2

Earnings per share excluding the held for exchange Animal Health Business (in euros) 0.76 0.96 1.52 1.70

IFRS earnings per share (in euros) 0.90 1.00 1.74 1.78

38

Cash Flow Statements

(1) Excluding restructuring costs and similar items.

€ million 2016 2015

Business net income 3,402 3,566

Depreciation amortization and impairment of property, plant and equipment and software 638 628

Gains and losses on disposals of non-current assets, net of tax (27) (44)

Other non-cash items (19) (218)

Operating cash flow before changes in working capital(1) 3,994 3,932

Changes in working capital(1) (753) (181)

Acquisitions of property, plant and equipment and software (700) (667)

Free cash flow(1) 2,541 3,084

Acquisitions of intangibles assets, excluding software (556) (280)

Acquisitions of investments in consolidated undertakings including assumed debt (1) (369) (169)

Restructuring costs and similar items paid (347) (345)

Proceeds from disposals of property, plant and equipment, intangibles assets and other non-current assets, net of

tax 262 86

Issuance of Sanofi shares 17 462

Dividends paid to shareholders of Sanofi (3,759) (3,694)

Acquisition of treasury shares (1,403) (1,243)

Disposals of treasury shares, net of tax - 1

Transactions with non-controlling interests including dividends (9) (16)

Foreign exchange impact 107 (391)

Other items (231) (50)

Change in net debt (3,747) (2,555)

39

Balance Sheets

ASSETS

€ million 06/30/16 12/31/15

LIABILITIES & EQUITY

€ million 06/30/16 12/31/15

Equity attributable to equity holders of Sanofi 54,190 58,049

Equity attributable to non-controlling interests 157 161

Total equity 54,347 58,210

Long-term debt 14,850 13,118

Property, plant and equipment 9,819 9,943 Non-current liabilities related to business combinations and

to non-controlling interests 1,027 1,121

Intangible assets (including goodwill) 50,514 51,583 Provisions and other non-current liabilities 9,895 9,169

Non-current financial assets & investments in

associates and deferred tax assets 10,435 10,115 Deferred tax liabilities 2,774 2,895

Non-current assets 70,768 71,641 Non-current liabilities 28,546 26,303

Accounts payable & Other current liabilities 12,607 13,259

Inventories, accounts receivable and other current

assets 16,259 15,780

Current liabilities related to business combinations and to

non-controlling interests 210 130

Cash and cash equivalents 6,076 9,148 Short-term debt and current portion of long-term debt 2,427 3,436

Current assets 22,335 24,928 Current liabilities 15,244 16,825

Assets held for sale or exchange 6,010 5,752 Liabilities related to assets held for sale or exchange 976 983

TOTAL ASSETS 99,113 102,321 TOTAL LIABILITIES & EQUITY 99,113 102,321