23

November 2013 Q3 2013 Investor Presentation FINANCIAL & BUSINESS RESULTS

November 2013

Q3 2013 Investor Presentation

FINANCIAL & BUSINESS RESULTS

This document does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of AFI Development Plc (the "Company") or any of its subsidiaries in any jurisdiction or an inducement to enter into investment activity. No part of this document, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with the document.

This communication is only being distributed to and is only directed at (1) qualified institutional buyers (within the meaning of Rule 144A of the United States Securities Act of 1933, as amended (the "Securities Act") or (2) accredited investors (as defined in Rule 501(a) of Regulation D adopted pursuant to the Securities Act). Any person who is not a "qualified institutional buyer" or "accredited investor" should not act or rely on this document or any of its contents.

This document contains "forward-looking statements", which include all statements other than statements of historical facts, including, without limitation, any statements preceded by, followed by or that include the words "targets", "believes", "expects", "aims", "intends", "will", "may", "anticipates", "would", "could" or similar expressions or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company's control that could cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking, including, among others, the achievement of anticipated levels of profitability, growth, cost and synergy of recent acquisitions, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of our shares or GDRs, financial risk management and the impact of general business and global economic conditions.

Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. These forward-looking statements speak only as at the date as of which they are made, and the Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company's expectations with regard thereto or any change in events, conditions or circumstances on which any such statements are based.

Neither the Company, nor any of its agents, employees or advisors intends or has any duty or obligation to supplement, amend, update or revise any of the forward-looking statements contained in this document.

The information contained in this document is provided as at the date of this document and is subject to change without notice.

Disclaimer

2

•Full cycle real estate developer

•Focus on unique large scale commercial and residential projects

•Primary market: Moscow, Russia

BUSINESS

•12 years on the market

•Admitted to LSE in 2007

•Premium listing from 2010

•Free float – 35,12%

HISTORY

•Strong global brand

•Affiliate of Africa Israel Group (64,88% owner) , a major conglomerate with global focus on real estate, construction and infrastructure

BRAND

•Strong liquidity position: US$ 140,3 mn as at September 30, 2013

•Secured financing for on-going projects

• 30% Debt to Total Assets**

FINANCIAL STABILITY

•16 completed projects with total c. 0,6 mln sqm of space

•Impeccable credit history

•Market reputation for high quality and professional property management

TRACK RECORD

•Substantial income generating

portfolio. Major project

AFIMALL

•2 projects are in active stage of development

•5 Pipeline projects & land bank

PORTFOLIO

** Bank loans only

AFI Development at Glance

Portfolio Value*

* Gross Asset Value of Portfolio based on C&W Valuation as for

30 June 2013 and BV of Land Bank projects, Trading Properties

and Hotels

Market Cap, as of Nov 18, 2013 US$ 0.85 bn

Price per share as of Nov 18, 2013 US$ 0.81

NAV (Equity), as of September 30, 2013 US$ 1.71 bn

NAV per share, as of September 30, 2013 US$ 1.64

Portfolio Value* US$ 2.5 bn

3

Current Portfolio

Note: the NOI projections are “forward looking statements” based on C&W valuation assumptions and Company estimations and they can be realized or not realized due to factors beyond the Company's control including, among others, the impact of

competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of our shares or GDRs, financial risk

management and the impact of general business and global economic conditions

Key Projects in Moscow

Yielding Assets (retail, offices and hotels)

Development Projects

Ownership:50%

Aquamarine Complex

Four Winds

H2O Office

Four Winds***

Berejkovskaya

Paveletskaya, 1

Tverskaya Plazas

Otradnoe Kosinskaya

Pochtovaya, Phase I

Botanic Garden

Paveletskaya,

Phase # II

Other

AFIMALL City

Land Bank

*** Odinburg presented with cost value

* Outside of Moscow

Value** (afid share, C&W):

US$ 1.7 bn

GLA(excl. hotels),sqm: 204K sqm

NOI stab. ( excl. hotels):

US$ 217 mn

Value*** (C&W): US$ 747 mn

GLA,sqm: 252K

GSA, sqm: 574,3K

NOI stab: US$ 142,3 mn

Value (BV): US$ 20 mn

AFIMALL City Berezkovskaya

Paveletskaya, 1

Tverskaya Ib, II

Ozerkovskaya III Aquamarine Hotel

Plaza SPA Zhel* Plaza SPA Kisl * H2O

Pochtovaya Tverskaya Plazas Odinburg*

Kosinskaya Paveletskaya II

** Hotels presented with cost value

4

SECTION 1

Project Update

Yielding Projects

AFIMALL City Update (1/3)

PROJECT HIGHLIGHTS

(as of September 2013)

Total GLA(shops, offices, storage), sqm 107.2K

Total GLA shops only, sqm 96,8K

% of GLA shops only 85%

Stabilized NOI (C&W est.) US$151.2 mn

MV (C&W est.) US$ 1.160 bn

Loan balance as for September, 2013 US$ 603 mn

CURRENT STATUS:

NOI for the 9m 2013 reached US$ 48,4 mn compared to US$ 38,9 mn due to

increase in AFIMALL operating activity

Growth in occupancy with total leased area reaching circa 82,046 sq.m. as at 30

September 2013 (from 80,020 sq.m. as at 30 June 2013 and 74,353 sq.m. at year-

end 2012)

One of the most renowned department stores in Moscow TSUM has sighed a long-

term lease for 1,688 sqm at the 1st floor and became the new main tenant

during Q3.

The AFIMALL sustainable increases its popularity and awareness by the

management quality work in improvement of tenant mix

AFIMALL became one of the top stages holding Annual Russian Fashion Week

Show

The Company reduced the interest rate for US portion of the loan from

Libor+6,6% to Libor +5.02%

6

Up to 24%

Q1 2013 Q2 2013 Q3 2013 9M 2013 9M 2012

Revenue 23.2 24.9 26.5 74.6 62.1

Operating expenses (8.6) (8.1) (9.5) (26.2) (23.3)

NOI 14.6 16.7 17.0 48.4 38.9

AFIMALL and Moscow-City Development (2/3)

AFIMALL

MOSCOW CITY DEVELOPMENT

Moscow City existing office space is approximately 500K sq

m, with another 600K sq m of office space expected to be

constructed by 2015.

The Moscow City vacancy rate is c. 25% (existing buildings)

Hotel Novotel, launched last quarter, will add additional visitors

to the Mall. Existing supply (number of rooms) – 360,

pipeline (number of rooms) - 319

The following buildings are expected to be completed:

Federation Tower (East), Eurasia Tower(107,5K) and

OKO(gla:87K sqm) — by the end of 2014, IQ-quarter

(gla:107K and Evolution Tower — by the end of 2015 (about

600,000 sq m of office area in total)

2 additional metro lines: Prolongation of Tretyakovskaya till

Ramenki, construction of Hordovaya with 4 different lines

connections (Vystovochnaya, Polezhaevskaya, Hodinskoye

Pole, Dinamo, Savelovskaya) by 2014 (see next slide)

Existing Office Complex

0 – Tower 2000

4 – Imperia Tower

8 – CityPoint

9 – Capital City

10 – Naberezhnaya Tower

13a – Federation Tower (West)

19 – Northern Tower

6, 7 – Central Core (AFIMALL

City)

Under Construction 2, 3 – Evolution Tower

11 – IQ-quarter

12 – Eurasia Tower

13b – Federation Tower (East)

14 – Mercury City Tower

16a – OKO

16b – Parking

Planned

15 – Moscow City Government Building

20 – Exposition and Business Center

7

AFIMALL and Moscow-City Transport Infrastructure(3/3)

Today: (0) –

“Vistavochnaya” – metro

station at the lowest level of

AFIMALL City

Till the end of 2013 (start of

2014): Point (1) – “Delovoy

Center” will be connected

with Point (2) - “Park

Pobedy”.

“Delovoy Center” is

going to be an additional

station at the lowest level of

AFIMALL City

2015: Point (1) – “Delovoy

Center” will be connected

with Point (3) –

“Khoroshevskaya”

Point (2) - “Park

Pobedy” will be connected

with Point (4) -“Ramenki”

0

1

2

3

4

(2014

8

Ozerkovskaya (Aquamarine III)

PROJECT HIGHLIGHTS*

(as of September 2013)

GBA, sqm: 73,4K

GLA, sqm 55,4K

MV (C&W est.) US$ 389 mn

Loan balance as for September, 2013 US$ 220 mn

CURRENT STATUS:

AFID reached a binding agreement to dispose Bld#1 in Aquamarine

Complex to a Russian State controlled corporation.

Total transacted area of Bld #1 is approximately 11,994 sq.m and includes

terraces & 71 parking spaces.

The consideration amounts to US$91.5 mn excluding VAT, AFID expects

to receive net profit on the transaction in the amount of approximately

US$14.6 million (expected to be recognized in Q4 2013).

Bld # 1

* The data presented for all project ( Four Buildings) before disposal of Bld # 1.

9

Yielding Properties

10

* Current Net rent for AFIMALL presented as for the end of September, 2013 and does not include discounts

** MV based on C&W valuation as for 30.06.2013. Hotels presented by cost value

***Project is not leased yet

*

***

Building AFIMALL BerezkovskayaPaveletskaya, bld.

1H2O

Tvesrkaya Plaza

Ib

Tverskaya Plaza

II

Ozerkovskaya

III***

Aquamarine

Hotel

Plaza Spa

Kislovodsk

Plaza SPA

Zheleznovodsk

Ownership 100% 74% 99.1% 100% 100% 100% 100% 100% 50% 100%

Moscow Moscow Moscow Moscow Moscow Moscow Moscow Moscow

Moscow City CBD CBD CBD CBD

GBA, sqm 304,205 11,612 16,246 10,698 2,104 6,008 73,346 11,701 25,000 8,931

GLA, sqm 107,208 10,250 14,085 8,990 1,909 6,008 55,422 159 keys 275 keys 134 keys

Parking lots (total), # 2,075 150 126 81 - - 551 15 - 15

Ocupancy rate (shops only), % 85% 86% 96% 73% 87% 87% - 79% 52% 62%

Current Net Rent as of

30.06.2013, $/sq m1,251* 443 244 206 527 455 750 ADR 242 ADR 379 ADR 229

Class Retail Office B Office B Office B Street retail &

Office

Street retail &

Office

Office A & Street

Retail Hotel Hotel Hotel

NOI stab (C&W est.), US mn 151.6 5.8 4.6 2.9 1.3 4.5 46.0 - - -

MV(AFID share),US$ mn** 1,160 31.3 30.1 18.3 9.0 31.5 389.1 31.0 25.0 23.0

CAP Rate 10% 12% 13.5% 14% 12% 11.5% 10% 9.5% 13% 13%

Location Kavkaz region Kavkaz region

10

SECTION 2

Project Update

Projects next for Development

Pipeline Projects Development Status

CURRENT STATUS:

• The first construction works on the land plot, allocated for the 1st stage in Phase # 1 have been launched

(54,5K sqm from 200,8K sqm of GBA)

• The mortgage accreditation was passed with one bank

CURRENT STATUS:

• The end of construction works was shifted from Q4 2013 to H1 2014

• The project was submitted to top Russian banks

CURRENT STATUS:

• Approval documentation GPZU and GZK are in place

• Design works are in process. Project design stage – stage P finalized

• The company finalized the top list to choose General Contractor

• Start of construction : H1 2014

CURRENT STATUS:

• Design works are in process

• Securing approval documentation

CURRENT STATUS (Plaza IV):

• Land plot’s borders clarification has been finalized

• Securing approval documentation

PARAMETERS:

Type:

Residential

GBA(Phase I), sqm: 200,8K

GSA(Phase I total), sqm: 149,4K

# of Apartments: 2,620

PARAMETERS:

Type: Mix

GBA, sqm: 111,7K

GLA, sqm: 90,3K

MV(C&W),mn: S$ 103,5

PARAMETERS:

Type: Office

GBA, sqm: 51,2K

GLA, sqm: 32,5K

MV(C&W): US$ 105,8 mn

PARAMETERS:

Type: Office, Retail

GBA/GLA, sqm: 108K/61,4K

MV(C&W): US$ 168,6 mn

PARAMETERS:

Type: Residential

GBA, sqm: 170,4K

GSA/GLA, sqm: 63,2K/28,0K

MV(C&W),: US$ 142,3mn

ODINBURG

KOSINSKAYA

TVERSKAYA IC

BOLSHAYA POCHTOVAYA

PARAMETERS:

Type: Office

GBA, sqm: 10,5K

GLA, sqm: 7,6K

MV(C&W),mn: US$ 12,4

CURRENT STATUS:

• According to the article dated 29.10.2013 and published on the official web-site of the Moscow Government, the Construction Department of Moscow Government has made decision to start an active phase of redevelopment at Tverskaya Zastava Square already in 2014 (and the first stage of redevelopment will focus on construction of an additional overhead road across the railway lines), whereas the date of completion of these works remains unclear, which will incur significant delay and, thus, pose high uncertainty with the timeline of the subject Plaza IIa project TVERSKAYA

PlAZA IIA

PLAZA IV

12

Paveletskaya II: change in Value

PROJECT HIGHLIGHTS

(as of September 2013)

Type Business class

Residential

GBA, sqm: 151,4K

GSA/GLA, sqm: 53,2K/21,0K

BV(cadastral value), mn: 11,6

MV(C&W), mn: 92,6

CURRENT STATUS:

The Company finalized negotiations with Moscow City Government to

change the permitted usage of land plot

In November AFID has received a signed land lease agreement for 6 years

for further development

Thus, assumptions in valuation report made by Cushman & Wakefield

have to be adopted for company valuation

Land lease agreement for construction of residential and commercial space

signed at Paveletskaya II in November 2013 resulting US$81.0 million

gross valuation gain (US$64.8 million net of taxation), which is included

in Company Q3 2013 result

13

Extensive land bank

Land bank – projects of the Company is currently put on hold

Land bank strategy

Activate projects upon securing required financing and evaluation of demand level from prospective tenants/buyer

Full flexibility regarding future development in various cycles of the economy – the major competitive advantage for the

Company

Land Bank Projects

Project Type Land (ha) GBA upon completion (sqm) BV as of 30.06.2013, US$ mn

Park Plaza Kislovodsk Hotel resort 5.3 40,000 7,2

Versailles, Kislovodsk Hotel resort 0.6 12,350 7,2

Ruza Mixed use 387 n/a 3,6

St. Petersburg Mixed use 3.07 n/a 1,8

TOTAL 19,8

Note: MV upon completion and GBA upon completion are “forward looking statements” based on JLL valuation assumptions and they can be realized or not realized due to factors beyond the Company's control including, among

others, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of

our shares or GDRs, financial risk management and the impact of general business and global economic conditions

14

SECTION 3

Financial Update

Income Statement and Statement of Financial Position

16

Q1 2013 9M 2012

Actual Actual Actual Actual Actual

(1) Construction consulting/management services 0.0 0.0 0.0 0.1 2.2

(2) Rental income 33.1 35.4 36.6 105.1 84.9

(3) Sale of residential and trading property 0.2 55.0 1.8 57.1 4.6

(4) TOTAL REVENUE 33.4 90.5 38.4 162.3 91.8

(5) Other income 3.2 0.4 0.8 4.4 0.2

(6) Operating expenses (21.4) (17.8) (18.3) (57.5) (44.2)

(7) Administrative expenses (4.0) (7.0) (2.1) (13.0) (15.7)

(8) Cost of sales of residential and trading property (0.2) (31.8) (1.3) (33.2) (3.8)

(9) Other expenses (1.8) (0.8) (1.5) (4.1) (1.0)

(10) TOTAL EXPENSES (24.2) (56.9) (22.3) (103.4) (64.5)

(11) Share of profit of equity-accounted investees (0.6) (0.1) 0.3 (0.5) 6.3

(12) GROSS PROFIT 8.6 33.5 16.3 58.4 33.5

(13) Valuation gains on investment property 16.5 41.0 47.4 104.9 (243.4)

(14) Impairement loss for trading property and hotels - - (65.4)

(15) RESULTS FROM OPERATING ACTIVITIES 25.1 74.5 63.7 163.3 (275.3)

(16) Profit on sale/disposal of properties/investment 32.1 - - 32.1 2.3

(17) Finance income 15.7 1.5 1.2 18.5 13.0

(18) Finance expense (16.8) (17.7) (16.8) (51.2) (45.4)

(19) FX Gain/( Loss) (9.2) (19.6) 5.1 (23.7) 16.7

(20) Translation reserve reclassification due to disposal of subsidiary (30.3) - - (30.3) -

(21) Net finance income/(costs) (40.5) (35.8) (10.5) (86.7) (15.7)

(22) PROFIT BEFORE INCOME TAX 16.7 38.8 53.2 108.7 (288.7)

(23) Current income tax (0.4) (0.4) (0.5) (1.3) (3.0)

(24) Deferred income tax (0.7) (10.7) (11.9) (23.3) 15.1

(25) PROFIT FROM CONTINUING OPERATION 15.6 27.7 40.8 84.1 (276.6)

9M 2013# ITEM ('000)

Q2 2013 Q3 2013 (4) Revenue reached US$ 162,3 mn since the

beginning of the year, which is 77% higher

that same quarter last year

(2) Rental income achieved USD 105,1 mn

for 9m2013, which is 24% higher than same

period 2012

AFIMALL contribution in rental income is

US$ 74,5 mn

(12) Gross profit went up to 74% compared

September 2012 and come up to USD 58,4

mn as for |September 2013

(13) Valuation gain US$ 47,4 mn is mostly

related to change in value of Paveletskaya II

and Plaza IIa

(25)Profit from continuing operation

amounted to US$ 84,1 mn compared to loss in

US$ 276,6 mn for the comparative period in

2012

16

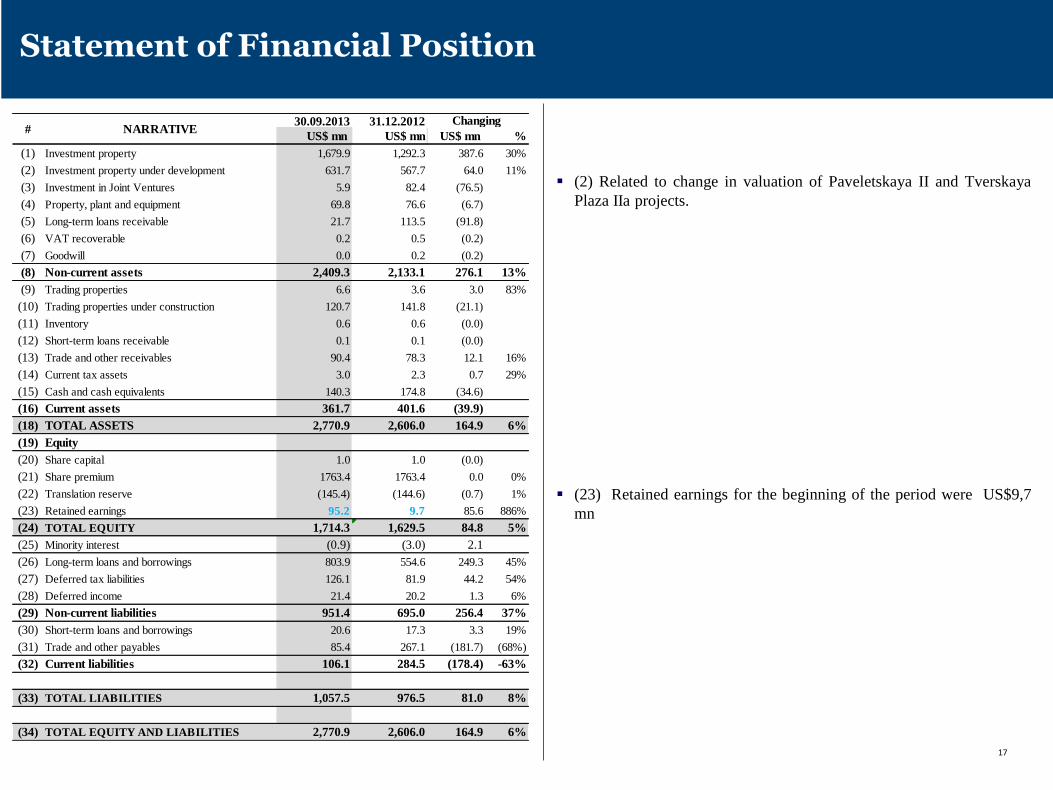

30.09.2013 31.12.2012

US$ mn US$ mn US$ mn %

(1) Investment property 1,679.9 1,292.3 387.6 30%

(2) Investment property under development 631.7 567.7 64.0 11%

(3) Investment in Joint Ventures 5.9 82.4 (76.5)

(4) Property, plant and equipment 69.8 76.6 (6.7)

(5) Long-term loans receivable 21.7 113.5 (91.8)

(6) VAT recoverable 0.2 0.5 (0.2)

(7) Goodwill 0.0 0.2 (0.2)

(8) Non-current assets 2,409.3 2,133.1 276.1 13%

(9) Trading properties 6.6 3.6 3.0 83%

(10) Trading properties under construction 120.7 141.8 (21.1)

(11) Inventory 0.6 0.6 (0.0)

(12) Short-term loans receivable 0.1 0.1 (0.0)

(13) Trade and other receivables 90.4 78.3 12.1 16%

(14) Current tax assets 3.0 2.3 0.7 29%

(15) Cash and cash equivalents 140.3 174.8 (34.6)

(16) Current assets 361.7 401.6 (39.9)

(18) TOTAL ASSETS 2,770.9 2,606.0 164.9 6%

(19) Equity

(20) Share capital 1.0 1.0 (0.0)

(21) Share premium 1763.4 1763.4 0.0 0%

(22) Translation reserve (145.4) (144.6) (0.7) 1%

(23) Retained earnings 95.2 9.7 85.6 886%

(24) TOTAL EQUITY 1,714.3 1,629.5 84.8 5%

(25) Minority interest (0.9) (3.0) 2.1

(26) Long-term loans and borrowings 803.9 554.6 249.3 45%

(27) Deferred tax liabilities 126.1 81.9 44.2 54%

(28) Deferred income 21.4 20.2 1.3 6%

(29) Non-current liabilities 951.4 695.0 256.4 37%

(30) Short-term loans and borrowings 20.6 17.3 3.3 19%

(31) Trade and other payables 85.4 267.1 (181.7) (68%)

(32) Current liabilities 106.1 284.5 (178.4) -63%

(33) TOTAL LIABILITIES 1,057.5 976.5 81.0 8%

(34) TOTAL EQUITY AND LIABILITIES 2,770.9 2,606.0 164.9 6%

# NARRATIVE Changing

17

Statement of Financial Position

(2) Related to change in valuation of Paveletskaya II and Tverskaya

Plaza IIa projects.

(23) Retained earnings for the beginning of the period were US$9,7

mn

17

Loans and cash position as of September 30, 2013

Gross balance of the bank loan portfolio (as of September 30, 2013) – US$ 823 mn

Total cash balance and deposits (as of September 30, 2013) – US$ 140,3 mn

The Company decreased the interest rate on the AFIMALL City loan in US dollars from 3 months LIBOR+6.7% to 3 months

LIBOR+5.02%. The average rate for AFIMALL loan decreased from 8,2% to 7,3%

Financial covenants

AFIMALL

Liquidation Value of the property should be higher than sum of the outstanding principal and six months interest

Q3 Revenue: not less than US$ 19,8 mn (including VAT)

As of September 30, 2013 the Company is in line with the covenants

*

Project Bank

Balance as of

September 30,

2013

Available

(US$ mn)Nominal Interest rate Currency Maturity

RCB $294 - 9.5% RUB 01.04.2018

RCB $309 - 3-m Libor+5,02% USD

TOTAL AFIMALL RATE $603 $41 7.30%

Ozerkovskaya III (100%) VTB $220 $0 3-m Libor+5,7% RUB 26.01.2015

TOTAL/BLENDED RATE $823

AFIMALL (Refinance)

18

Portfolio NAV as of September 30, 2013

*

PROJECT Book Value Bank Loan

30.09.2013 30.09.2013

AFI Mall 1,160 (603) 557

Berezkovskaya (100%) 42 42

Paveletskaya I (1) 30 30

Plaza H20 18 18

Ozerkovskaya III 388 (220) 168

Plaza Ib 9 9

Plaza II 32 32

TOTAL INVESTMENT PROPERTY: 1,680 823 856

Plaza Ic 106 106

Plaza II a 12 12

Plaza IV (100%) 169 169

Kosinskaya 104 104

Bolyshaya Pochtovaya 142 142

Paveletskaya II 93 93

Ruza 4 4

St. Petrsburg 2 2

Ozerkovskaya III (underground utilities) 1 1

TOTAL INVESTMENT PROPERTY UNDER DEVELOPMENT: 632 0 631

Ozerkovskaya Phase II (26) 6 6

TOTAL TRADING PROPERTY: 6 0 6

Aquamarine/Ozerkovskaya 26 31 31

Plaza SPA Zheleznovodsk 23 23

Pyatigorskaya (Park Plaza Kislovodsk) 7 7

Plaza Spa Kislovodsk (Tirel) (50%) 25 25

Versailles (Kislovodsk) 7 9

TOTAL PROPERTY PLANT AND EQUIPMENT: 94 0 95

Odinburg 121 121

TOTAL TRADING PROPERTY UNDER DEVELOPMENT: 121 0 121

TOTAL PORTFOLIO: 2,532 823 1,710

CASH AND CASH EQUIVALENT 140

DEFFERED TAX LIABILITY (126)

TOTAL OTHER ASSETS AND LIABILITIES (10)

TOTAL EQUITY: 1,714

NAV

LTV= 33%

LTE = 48%

19

ANNEX

Market Overview

Yielding Projects

Market Overview (1/2)

Source: Commercial Real Estate Report, JLL; Cushman and Wakefield Report; EIU Russia,

Rosstat

MACROECONOMIC UPDATE

MOSCOW OFFICE MARKET OVERVIEW

MACROECONOMIC UPDATE

• GDP: In Q3 Russian economy entered stagnation phase and GDP growth

reached 1,3% compared to 1,2% in Q2 2013 and 1,0% compared to Q3

2012. So far Russia is still ahead of Eurozone with its 0.3% growth rate but

way below other BRIC partners and even USA with their 2.5%.

• Oil price (Brent): In September oil price slowed down compared to Q2

2013 on 0,7% and increased on 1,4% compared to September 2012. The

World oil prices in the medium term will be reduced, their current level looks

a bit overstated as a result of the existing political risks.

• Consumer sector: Economy is supported primarily by consumer market,

which is fuelled by increase of pensions and salaries in public sector. Retail

trade turnover is growing at about 4% - much faster than economy in general.

• Inflation: Consumer prices in Q32013 increased by 1.1%, with YTD

inflation totaling 4.7%. Probability to meet inflation yearly target of 6%

remains very high.

MOSCOW OFFICE MARKET OVERVIEW

Key indicators Units

Prime rate

(trophy assets)*

(US$/sqm/year)

1,150

Base rent Class A

(US$/sqm/year)

850

Yields (prime) 8,5%

Overall

Vacancy rate

13,1%

Vacancy rate, Class

A

18,9%

*Prime base rents refer to rents in high quality

buildings in the Central Business District (CBD).

`

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

United States Europe

Germany United Kingdom

Czech Republic Poland

Russia

109.2

20

40

60

80

100

120

140 Oil price (Brent, US$ per barrel)

1,000

1,400

620 650

850 850 850 870 850

1,500

2,000

800 850

1,200 1,150 1,150 1,150 1,150

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2007 2008 2009 2010 2011 2012 Q12013

Q22013

Q32013

US$

/psq

m/p

a

average Class A class A CBD Prime

source: AFID, JLL, C&W

• Supply: Over Q3 2013 6 new office buildings were brought on the market

with rentable area of c. 240K sq m. More than 50% of completed office space

in this quarter is Class A developments, the most significant of which are

Mercury City Tower (87,574 sq m). More than 80% of supply – areas

outside of TTR.

• Vacancy: Despite the strong new supply in Q3, the overall vacancy rate

remained stable at the level of 13.1% Nevertheless, vacancy rates for

Class A are particularly high at 18.9% as several new high-quality

developments added available spaces to the market.

• Rental rates: The rental market remained flat over this quarter with prime

rents at USD1,000 to USD1,150/sq m per year, Class A rents stand

between USD600 and USD850, for Class B+ USD350–600/sq m per year

and for Class B- falling in the range USD250–400.

• Yield(prime): The capitalization rates in Moscow remained almost the same

in Q2 2013 ( 8,5%) 21

Market Overview (2/2)

Source: Q3 Marketbit C&W report; Blackwood report, intermarksavills

MOSCOW RESIDENTIAL MARKET MOSCOW RESIDENCTIAL MARKET

MOSCOW RETAIL MARKET OVERVIEW

• Supply: One shopping center opened in Moscow this quarter - Raikin Plaza

(GLA of 35,000 sq m). Other two big openings were in St-Peterburg (GLA of

48K sqm) and Syktyvkar (GLA of 30K sqm.)

• Vacancy: Vacancy rate has been stable in Q3. The share of vacant spaces in

quality premises is 2.5%. It is significantly lower compared to most

European capitals.

• Rental rates: No significant changes were witnessed in rental rates over the

quarter. The prime rent for 100 sqm. space in quality premises remains at the

level of USD3,000–4,500 sq m/year. Average rental rate in shopping centres

is USD 500–1,800 sq m/year.

• Yield(prime): The capitalization rates in Moscow remained the same as in Q1

2013 and amounted at 9% for retail sector

MOSCOW RETAIL MARKET OVERVIEW

Key indicators Units

CBD prime rates

(US$/sqm/year)

3,000 – 4,500

Average base rent

(US$/sqm/year)

500 – 1,800

Prime Yields 9%

Vacancy rate

(market average)

2,5%

• Supply: As the end of Q3 213 the supply of new residential remained

stable and amounted to 1,5 mln sqm (incl. apartments and elite class).

Business class and comfort class took the significant part of supply.

• Prices Moscow: The average price in Q3 2013 for primary business-class

residential premises(incl. apartments) amounted to US$ 7,500 psqm

compared to US$ 7,390 in Q2 2013.

• At the moment the price for business-class residential unit in CBD of

Moscow in the primary market reached a level of US$ 11,000 – 13,000 US$

psqm.

• Prices in the Moscow region was unchanged and stood at the average rate

c. US$ 3,000 psqm

Key indicators

(Moscow)

Units

CBD prime

(US$/sqm)

13,000

Average price

(US$/sqm)

7,500

Key indicators

(Moscow Region)

Units

Average Price

(US$/sqm)

3,000

4,500

4,800

3,700

4,000 4,000 4,000

4,500 4,500 4,500

4,500

1,700 2,000

1,200 1,350

1,350 1,350

1,150 1,150

1,150

1,800

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

USD

psq

m p

a

Prime rents Base rents

7,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

2010 2011 2012 2013

22

Contact Information

Registered office AFI DEVELOPMENT PLC Spryou Araouzou 165, Lordos Waterfront Building 5th Floor, Flat/Office 505, 3035 Limassol, Cyprus Tel. +357 25 310975 Principal office of operating subsidiary AFI RUS 16 A Berezhkovskaya Embankment, building 5, Moscow, 121059, Russian Federation. Tel: +7 495 796 99 88 http://investors.afi-development.ru

23