44

Q3 Investment Update October 25, 2017 Russ Allen, CIO

Q3 Investment Update

October 25, 2017

Russ Allen, CIO

DisclosuresImportant Disclosures:

This information is for discussion purposes only and is being furnished on October 25, 2017. This information is not to be re-transmitted in whole or in part without the prior consent of Berman Capital Advisors.

While all the information prepared in this presentation is believed to be accurate, Berman Capital Advisors makes no express warranty as to its completeness or accuracy nor can it accept responsibility for errors appearing in the presentation.

No information provided herein shall constitute, or be construed as, an offer to sell or a solicitation of an offer to acquire any security, investment product or service, nor shall any such security, product or service be offered or sold in any jurisdiction where such an offer or solicitation is prohibited by law or registration.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable or be suitable for your portfolio or individual situation. Please contact Berman Capital Advisors to discuss your individual situation.

Berman Capital Advisors / 2

Major Asset Class Performance

Berman Capital Advisors / 3

• Markets continue to be strong and volatility remains very low. The rally broadened this quarter.

• Emerging Markets continue to outperform.

• There was some rotation in the final weeks of the quarter toward cyclical stocks.

• Oil prices rebounded, primarily due to signs of slowing shale productivity.

Index Q3 2017 YTD 2017MSCI Emerging Markets 7.9% 27.8%Russell 1000 Growth 5.8% 20.7%MSCI Europe 6.5% 22.8%MSCI EAFE (International) 5.4% 20.0%S&P 500 4.5% 14.2%Russell Midcap 3.5% 11.7%Japan 4.5% 14.8%Russell 1000 Value 3.1% 7.9%High Yield Bonds 2.0% 7.0%Russell Small Cap 5.7% 10.9%US Aggregate Bond 0.9% 3.1%Crude Oil 12.0% -6.3%Source: Bloomberg, Ned Davis Research

Note: International market returns reported in U.S. Dollars, not local currency

Index Total Return

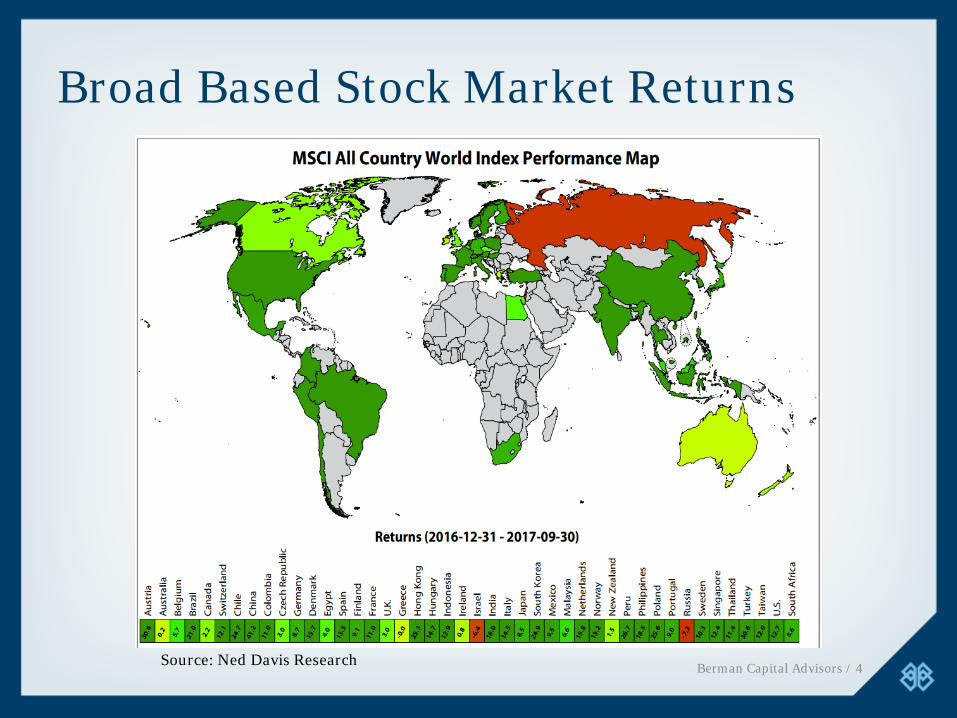

Broad Based Stock Market Returns

Berman Capital Advisors / 4Source: Ned Davis Research

International Stocks’ Comeback

Berman Capital Advisors / 5Source: Bloomberg

Fixed Income Performance

Berman Capital Advisors / 6

Continued strength in high yield as credit conditions remain strong.

Source: Ned Davis Research

Investment Themes• Asset prices continued to march higher in the third quarter despite worry

over high valuations and the current political environment. Investors are right to worry about valuations, but they could be resolved by a sideways market, rather than a sharp drop.

• Fundamentals for “risk-on” assets (stocks, corporate credit, structured finance) remain positive. Rising earnings, still-low interest rates and recovering optimism in international markets.

• The Fed’s reversal of quantitative easing (quantitative tightening!) has been well telegraphed and has not disturbed investors. As the Fed’s easing was unprecedentedly large, the unwind bears close watching, as well. Faster than expected inflation could be a negative catalyst.

• The global economy appears to be gathering more strength, which has supported international stocks and large cap multi-national companies. We think we are in the early innings of international outperformance versus U.S. stocks.

Berman Capital Advisors / 7

Global Economy & Investment Implications

Berman Capital Advisors / 8

Synchronized Global Upturn

Berman Capital Advisors / 9

Synchronized Global Upturn

Berman Capital Advisors / 10

Global Purchasing Managers’ Index upswing illustrated in chart.

Synchronized Global Upturn

Berman Capital Advisors / 11

Leading economic indicators and industrial production still strengthening.

Source: BCA Research

Synchronized Global Upturn

Berman Capital Advisors / 12

Consumer and business confidence are both back to pre-crisis levels…

Source: BCA Research

Synchronized Global Upturn

Berman Capital Advisors / 13

…and Capex is responding.

GDP Expectations Now Being Exceeded

Berman Capital Advisors / 14

Real Rates are Still Very Low

Berman Capital Advisors / 15

The policy backdrop is still easy, as interest rates adjusted for inflation are close to zero. Rising confidence is creating even looser financial conditions in the near term.

Source: Ned Davis Research

Profit Outlook Remains Strong

Berman Capital Advisors / 16

The Cycle Could Continue Even Longer

Berman Capital Advisors / 17

Earnings and Price Appreciation

Berman Capital Advisors / 18

Recessions Drive Larger Market Corrections

Berman Capital Advisors / 19

Currently Not Lined Up for Recession

Berman Capital Advisors / 20

Future Upside Limited, but Tough to Time

Berman Capital Advisors / 21

Implications of Possible Inflation

Berman Capital Advisors / 22

Tightening Labor Market = Inflation?

Berman Capital Advisors / 23

Why No Taper-Tantrum Repeat?

• Fed has telegraphed its balance sheet plans.

• Stronger growth may be offsetting concerns about tighter policy, keeping volatility contained.

• The stock of central bank assets is likely to remain high for a long time.

• Euro Crisis appears to be over, unlike 2011.

Berman Capital Advisors / 24

Fed Chair Odds

Berman Capital Advisors / 25

Source: Predictit.com Market

Implications for Bonds: Duration Risk

Berman Capital Advisors / 26

Implications for Bonds: Credit Risk

Berman Capital Advisors / 27

Weakening Loan Standards?

Berman Capital Advisors / 28

Focus on International Markets

Berman Capital Advisors / 29

Europe - Deleveraging

Berman Capital Advisors / 30

Source: Eurostat, WSJ.com

Relative Stock Market Valuation

• No matter how you slice it, the U.S. markets are more expensive than others’.

• This is true even if you adjust for sector weights.

Berman Capital Advisors / 31

Source: BCA Research

Chinese Economy

Berman Capital Advisors / 32

Official (and unofficial) measures show Chinese output increasing.

Improving profitability helps indebted companies more easily repay loans.

Source: BCA Research

Who Will Grow in the Long Term?

Berman Capital Advisors / 33Source: OECD

Focus on Midstream Energy (MLPs)

Berman Capital Advisors / 34

• Energy infrastructure are the physical assets to gather, transport and store energy products.

• These assets are critical to move oil, gas and natural gas liquids (NGLs) from production to end-user.

• MLPs are a tax-advantaged (but K-1 producing) partnerships that trade like stocks.

• MLPs typically have high cash distribution and are held for income and growth.

What is Energy Infrastructure?

Source: Kayne Anderson, October 2017

Berman Capital Advisors / 36

Oil prices and Energy Stocks

The recent correlation between MLPs and Crude has also broken down.

Berman Capital Advisors / 37

Oil prices and Midstream Stocks

Source: Bloomberg

The Energy Downturn and Oil Correlation

• MLPs were presented as little correlated to oil prices, but rather as a toll road paid on volumes. MLPs indeed traded that way from 2000 –2014.

• During the huge oil plunge of 2015, fear of customer

bankruptcy and too much MLP debt greatly increased fear and correlation to the price of oil.

• This is despite the fact that MLPs get the majority of their revenue from natural gas, and that actual MLP cash flow production MLPs held up as advertised.

Source: Kayne Anderson, October 2017

• MLPs and Midstream Corporations Are Trading Below Historic Cash Flow Multiples

• New expansion projects with long-term commitments are coming online in late 2017 and 2018. These will increase cash flows.

• Increasing utilization of existing assets are driving cash flows higher with less need for capex.

• Many midstream companies are trading below replacement cost on a trailing and/or forward multiple basis .

• Multiple expansion possible as the volume story unfolds.

MLP Valuation

Source: Bloomberg, as of June 16, 2017

• Dislocation has created very attractive relative yield spreads. We believe fundamentals are fine and distribution cuts are largely behind us.

MLP Valuation

Source: Bloomberg, Alerian, and NAREIT. Utilities yields based on the S&P 500 Utilities index, REIT yields based on the FTSE NAREIT Real Estate 50 Index (FNR5), and BBB Bonds based on the BAML BBB US Corporate Index MLPs are represented by AMZX Index

MLP Valuation

Source: Bloomberg, Alerian, and NAREIT. Utilities yields based on the S&P 500 Utilities index, REIT yields based on the FTSE NAREIT Real Estate 50 Index (FNR5), and BBB Bonds based on the BAML BBB US Corporate Index MLPs are represented by AMZX Index

• MLP Yields are now much higher than competing investments.

• The electric car won’t hurt gasoline demand until years from now. Demand in the emerging markets is resulting in higher demand year over year.

• What are electric cars powered by? Electricity is produced from natural gas, coal, then renewables. Low natural gas prices is stimulating demand despite solar subsidies from governments.

• Energy infrastructure will be needed for many years to come.

Existential Worries?

Conclusion

Berman Capital Advisors / 43

• Despite high valuations, the near term backdrop is still positive for asset prices.

• Interest rates and relative economic strength are key factors to watch for potential tactical moves.

• Faster than expected growth could significantly hurt bond proxy equities and high duration bonds.

• Return expectations should be muted from traditional asset classes. We will continue to recommend more niche investments.

Thank You