130

1 QIS Industry Workshop 3 March 2010 Katrina Squires Judy Lau Kelly Yeung Denis Gorey Guy Eastwood Anna Sofianaris Michael Booth

1

QIS Industry Workshop3 March 2010

Katrina SquiresJudy Lau

Kelly YeungDenis Gorey

Guy EastwoodAnna SofianarisMichael Booth

2

Topics for the day

• Overview

• Definition of capital

• Leverage ratio

• Liquidity

• CCR and TB

• Smoothing MRC

• Securitisation

• Operational risk

• Wrap up

3

Overview

• Australian participants

• Activity to date

• Timetable

• Prioritisation of worksheets

• FAQ process

• Weekly progress reports

4

Australian participants

ANZ Suncorp

CBA CU Australia

NAB Wide Bay

WBC Heritage BS

Macquarie Citibank

Bank of Queensland HSBC

Bendigo and Adelaide Bank

5

Activity to date

•22 Dec: draft spreadsheets for DefCap, DefCapTier1, DefCapTier23 and Liquidity provided to

advanced ADIs

•14 Jan: draft workbook and instructions sent to all ADIs

•18 Feb: final spreadsheets circulated

6

Timetable• 25 March: QIS working group meeting

• 16 April: draft (core) spreadsheets to APRA

• 30 April: final (core) spreadsheets to APRA

• 17 May: submission to Secretariat

• 21 May: submission of TB, CCR, Securitisation, Ops Risk, Smoothing MRC and supplementary liquidity worksheets to APRA

• 10-11 June: QIS working group meeting

• 14-15 July: preliminary analysis presented to the Basel Committee

• End 2010: finalisation of proposals

7

Prioritisation of worksheets

Spreadsheets required by 16 April (draft) and 30 April (final)

• Gen info (minimum 3 years (latest) for capital distribution data)

• Defcapcalc

• Defcap

• DefcapTier1

• DefcapTier23

• Leverage ratio (minimum 3 years (latest))

• Liquidity (Level 2)

8

Prioritisation of worksheets

Spreadsheets required by 21 May (final)

• CCR

• Securitisation

• OpRisk

• Smoothing MRC

• Liquidity (Level 1 data (only applicable to the four major banks) separately for i) all Australian operations, ii) NZ banking subsidiary; and iii) UK banking subsidiary)

9

Prioritisation of worksheets

Spreadsheets required by 21 May (final)

• TB

• TB securitisation

• TB correlation trading

• TB securitisation LSS

• TB correlation trading LSS

• TB securitisation wide

• TB correlation trading wide

10

Prioritisation of worksheets

N/A – no information required • CCR memo

• DefcapcalcCOREP

11

FAQ process

• BIS FAQ (refer http://www.bis.org/bcbs/qis/index.htm) • APRA FAQ (refer

http://www.apra.gov.au/ADI/upload/APRA-FAQ.pdf)

• Bilateral responses

12

Weekly progress reports

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%General info

Defcap

DefcapTier1

DefcapTier23

Defcapcalc

Leverage ratio

Liquidity (Level 2)

Worksheets required by 30 April 2010

Percentage of worksheet completedDate Worksheet

13

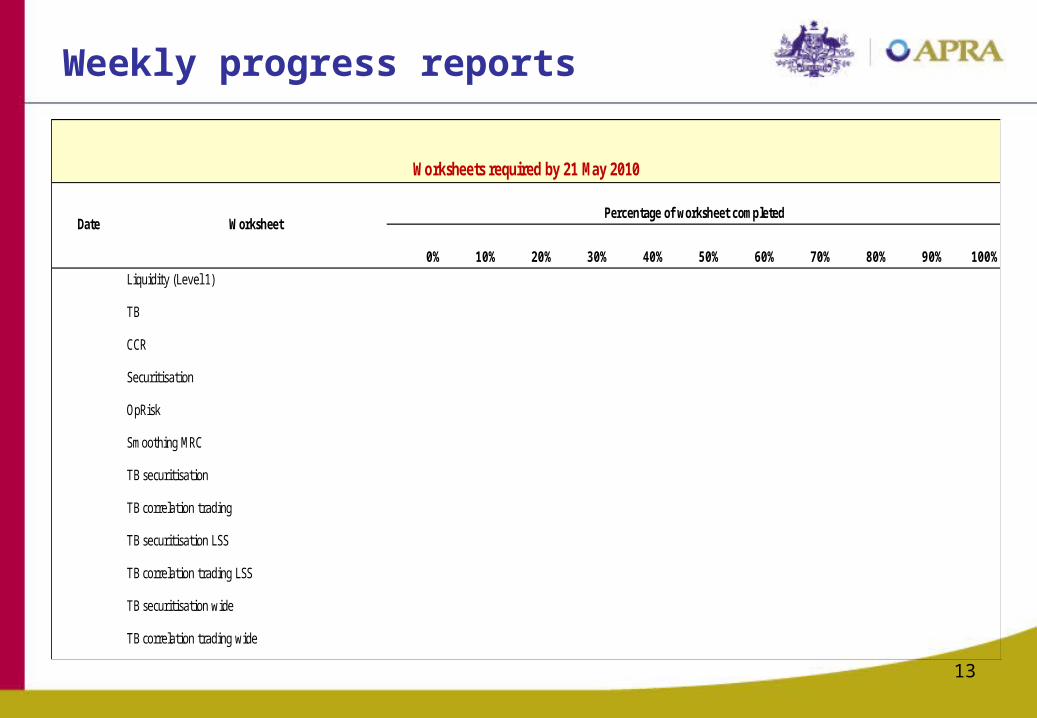

Weekly progress reports

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Liquidity (Level 1)

TB

CCR

Securitisation

OpRisk

Smoothing MRC

TB securitisation

TB correlation trading

TB securitisation LSS

TB correlation trading LSS

TB securitisation wide

TB correlation trading wide

Worksheets required by 21 May 2010

Date Worksheet Percentage of worksheet completed

Definition of capital

Judy Lau

14

15

Background

Changes to capital framework aimed at raising:

• Quality

• Consistency

• Transparency

16

Quality

• Stricter requirements to qualify as Tier 1 capital

• Emphasis on tangible common equity

• Predominant Tier 1 to comprise common shares and retained earnings

• Innovative hybrids phased out

• Tier 3 capital abolished

17

Consistency

• Regulatory adjustments harmonised

• Filters applied to predominant Tier 1

• Tier 2 capital harmonised

• Explicit minimum ratios for

– predominant Tier 1/risk-weighted assets – Total Tier 1/risk-weighted assets – Total capital/risk-weighted assets

18

Tier 1 Capital

Worksheet DefCapTier 1

• Column for each ‘group’ of instruments for which answers same

• All sections completed for each instrument ‘group’, except where question is not applicable for Australia

• All Tier 1 capital instruments accounted for in worksheet

Current regulatory capital classification

• Tier 1 – unlimited inclusionAPRA Fundamental Tier 1 capital

• Tier 1 – limited inclusion but the limit exceeding 15%APRA Non-innovative Residual Tier 1 capital

• Tier 1 – inclusion limited to 15% (or less)APRA Innovative Tier 1 capital

19

Common equity

Only paid –up ordinary shares will qualify

Questions not applicable for Australia:

• Is the instrument capital under national law? (Row18)

• The paid-in amount is recognised as equity (ie not recognised as a liability) for determining balance sheet insolvency. (Q9 under Common Equity criteria)

20

Tier 1 additional going concern capital

• Existing instruments may not meet all criteria

• Innovative instruments ineligible

• No maturity date nor incentive to redeem

• Call options subject to strict governance arrangements

Q10 and Q11 relating to liabilities contributing to balance sheet insolvency not applicable in Australia

21

Tier 2 capital

Worksheet DefCapTier 23

• Only one class of Tier 2 capital

• Eligibility comparable to APRA Lower Tier 2 capital

• No incentives to redeem

Questions on lock-in features not applicable in Australia

22

Assessing impact of capital proposal

Worksheet DefCap

• Regulatory adjustments reflect proposals in Consultative Document

• Variations to the baseline proposal for a number of items

• Completion on a “best-efforts” basis

23

Change in risk-weighted assets

• As a result of capital adjustments under the proposal

• Assets deducted from capital excluded from RWA

• Relevant where deductions not applicable in existing national rule

• Since all baseline adjustments are APRA deductions, no change

• Enter in ‘Other’ any current APRA deductions not required under proposal

24

Paid in capital, reserves and AOCI

Total should equal APRA Fundamental Tier 1 capital minusminority interests

plusFull value of asset revaluation reserves as defined in Attachment B of APS111

25

Minority interest

Variations to identify:

• Amounts attributable to different types of capital instruments

• Total risk-weighted assets of the subsidiaries

• ‘Surplus’ capital in the subsidiaries

Follow instructions and complete on “best-efforts” basis

26

Unrealised gains and losses

Variations separately identify net unrealised gains (losses):

• on financial assets according to accounting classification andfair value hierarchy

• on financial assets by fair value hierarchy andregulatory banking book/trading book

• on property assets according to accounting treatment and regulatory banking book/trading book

27

Goodwill and other intangibles

• Associated deferred tax liabilities entered as positive numbers

• Selected intangible items separately identified

• Further categorisation as detailed in instructions

28

Deferred tax assets

Netting of deferred tax assets and deferred tax liabilities per APRA rules

(refer Attachment D of APS 111)

Separately identify amounts whose realisation:

• depends on future profitability of the bank

• Do not rely on future profitability

Exclude from deferred tax liabilities amounts associated with goodwill

and intangibles 29

Investment in own shares

• Not relevant to the extent holdings are derecognised under IFRS

• Indirect investments have to be reported

• Report obligations to purchase or provide financing

30

Investments in the capital of banking, financial and insurance entities

• Investments which have not been consolidated

• Distinguish holdings of common shares, other Tier 1 instruments and Tier 2 instruments

• Five variations as detailed in instructions

31

Provisions and expected losses

Basel II IRB banks to provide details on• Eligible provisions• Expected losses

Standardised banks to provide data on provisions eligible for inclusion in Tier 2 capital

32

Cash flow hedge reserves

Report total positive or (negative) value of cash flow hedge reserve

with breakdown into:

• Amount relating to the hedging of projected cash flows which are not recognised on balance sheet

• Amount relating to the hedging of projected cash flows on assets recognised but not fair valued on balance sheet

• Amount relating to the hedging of projected cash flows on liabilities recognised but not fair valued on balance sheet

33

Gains and losses due to changes in own credit risk

Report net gains and losses in equity due to changes inbank’s own credit worthiness

Further split into:

• Amount relating to liabilities fair valued under fair value option

• Amount relating to liabilities fair valued due to their accounting classification

34

Defined benefit pension fund assets

• Surplus in any ADI-sponsored defined benefit fund

• Separately report any surplus amount that the ADI has demonstrated it has unrestricted and unfettered access to APRA’s satisfaction

• The risk-weighted amount of the assets that the ADI has unrestricted and unfettered access

• Deficits in any ADI-sponsored defined benefit fund

35

Additional deductions

Separately identify the following items currently deducted 50:50 from Tier 1 and Tier 2 capital:

• Certain securitisation exposures• Securitisation gain on sale• Equity exposures under the PD/LGD approach• Non-payment/delivery on non-DvP and non-PvP

transactions• Significant investments in commercial entities

36

Country specific calculation

Worksheet DefCap Calc

ARF 110

37

General info template

Eligible Capital and Regulatory Adjustments (Current Rules)

Asks for information on capital composition and regulatory deductions

under current rules

Amounts reported for Tier 1 capital, Tier 2 capital and total capital should

match public/supervisory reports

Amounts eligible to meet the predominance test should equal Fundamental Tier 1 capital

38

General info template

Capital distribution data

Relevant for consideration of capital conservation and countercyclical capital buffers

Conserving capital to counter cyclicality

Distribution as percentage of earnings

Capital raisings

39

Discretionary bonus payments

• Discretionary

• Both in cash and/or shares

• Results in reduction in Total Tier 1 capital

• Net of tax

(Deduct any potential purchase from Investment in Own Shares)

40

Leverage ratio

Katrina Squires

41

42

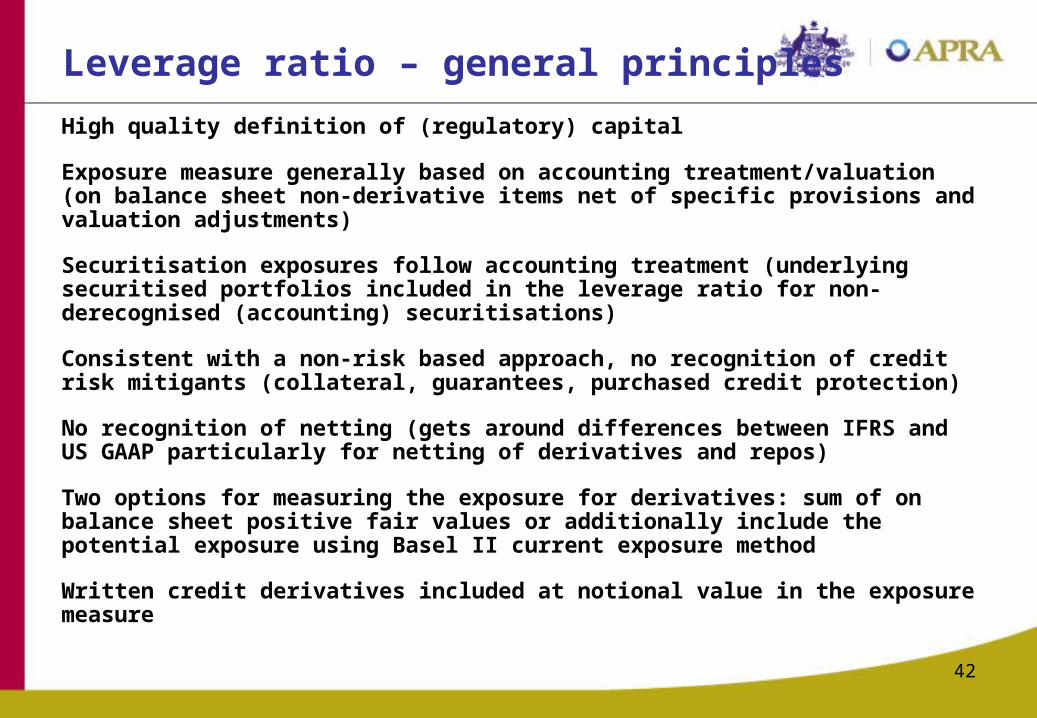

Leverage ratio – general principlesHigh quality definition of (regulatory) capital

Exposure measure generally based on accounting treatment/valuation (on balance sheet non-derivative items net of specific provisions and valuation adjustments)

Securitisation exposures follow accounting treatment (underlying securitised portfolios included in the leverage ratio for non-derecognised (accounting) securitisations)

Consistent with a non-risk based approach, no recognition of credit risk mitigants (collateral, guarantees, purchased credit protection)

No recognition of netting (gets around differences between IFRS and US GAAP particularly for netting of derivatives and repos)

Two options for measuring the exposure for derivatives: sum of on balance sheet positive fair values or additionally include the potential exposure using Basel II current exposure method

Written credit derivatives included at notional value in the exposure measure

43

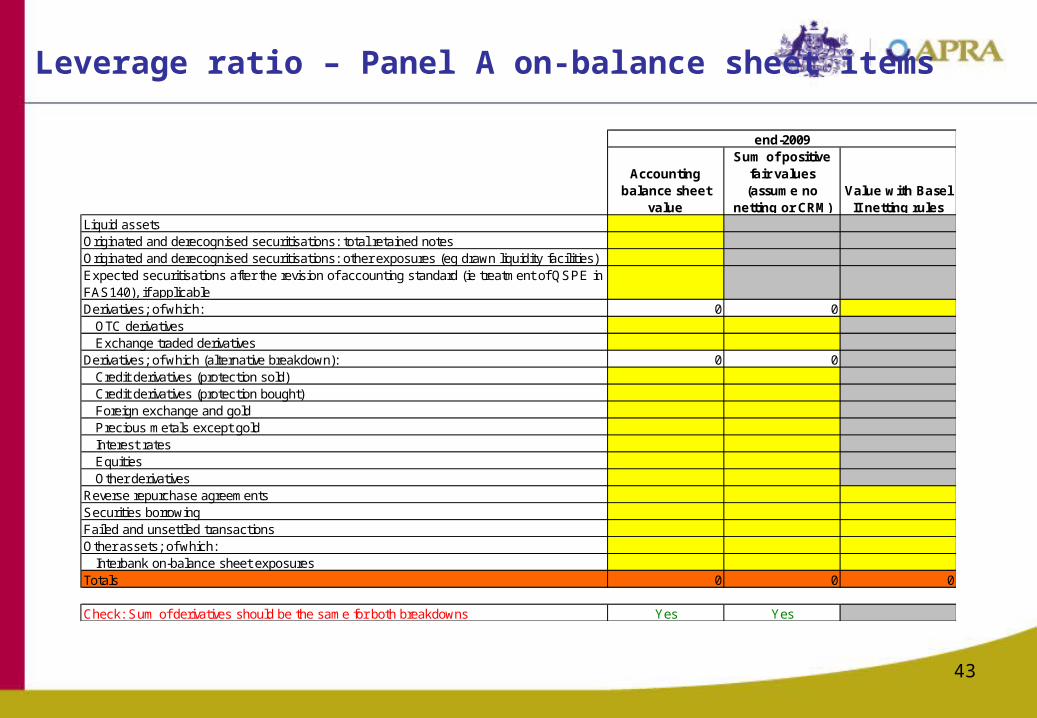

Leverage ratio – Panel A on-balance sheet items

Accounting balance sheet

value

Sum of positive fair values (assume no

netting or CRM)Value with Basel

II netting rulesLiquid assetsOriginated and derecognised securitisations: total retained notesOriginated and derecognised securitisations: other exposures (eg drawn liquidity facilities)Expected securitisations after the revision of accounting standard (ie treatment of QSPE in FAS140), if applicableDerivatives; of which: 0 0

OTC derivativesExchange traded derivatives

Derivatives; of which (alternative breakdown): 0 0Credit derivatives (protection sold)Credit derivatives (protection bought)Foreign exchange and goldPrecious metals except goldInterest ratesEquitiesOther derivatives

Reverse repurchase agreementsSecurities borrowingFailed and unsettled transactionsOther assets; of which:

Interbank on-balance sheet exposuresTotals 0 0 0

Check: Sum of derivatives should be the same for both breakdowns Yes Yes

end-2009

44

Leverage ratio – Panel B derivatives and off-balance sheet items

Regulatory potential exposure(Current

exposure method; assume

no netting or CRM)

Regulatory potential exposure (Current

exposure method; apply Basel II netting

rules) Notional amountB1 ) DerivativesDerivatives; of which: 0 0

OTC derivativesExchange traded derivatives

Derivatives; of which (alternative breakdown): 0 0Credit derivatives (protection sold)Credit derivatives (protection bought)Foreign exchange and goldPrecious metals except goldInterest ratesEquitiesOther derivatives

B2) Off-balance sheet itemsOriginated securitisations: off-balance sheet exposures

undrawn liquidity facilities and other commitments related to derecognised securitisationsderecognised securitisations: total underlying assets

Off-balance sheet items with a 0% CCF in the RSA; of which:credit cards

Off-balance sheet items with a 20% CCF in the RSA; of which:loan commitment with original maturity ≤ 1 year

Off-balance sheet items with a 50% CCF in the RSA; of which: OBS securitisation related exposures

loan commitments with an original maturity greater than 1 yearOff-balance sheet items with a 100% CCF in the RSA; of which: OBS securitisation related exposures

direct credit substitutes (see para 83(i))repurchase agreements and asset sales with recourse (see para 83(ii))forward asset purchases, forward forward deposits and partly-paid shares and securities (see para 84(i))

Totals 0 0 0CCFs according to Basel I or Basel II?

Check: Sum of derivatives should be the same for both breakdowns Yes Yes

end-2009

45

Leverage ratio – general issues

• Consolidation to be based on APRA’s definition of the Level 2 consolidated banking group (refer APS 110)

• Items deducted from capital (or risk weighted at 1250%) may be deducted from the measure of exposure

• For pre-Basel II reporting periods (2007 and 2006) use Basel I regulatory rules

• For pre-IFRS reporting periods use accounting rules in force at the time

• Securitised assets:– non-derecognised securitised portfolios/assets are to be recorded in

Panel A line item 26 in the ‘Other Assets’ category– total underlying assets of derecognised portfolios/assets to be recorded

in Panel B line item 51 ‘Derecognised securitisations: total underlying assets’

46

Leverage ratio – general issues

• Panel A Line item 11 is not relevant for Australia, ie. ‘Expected securitisations after the revision of accounting standard (ie treatment of QSPE in FAS 140), if applicable’

• Availability of requested data: ‘best efforts’ basis

47

Leverage ratio – outstanding issues

Calibration – how much?

Pillar 1 or Pillar 2 or Pillar 3?

Pillar 3 disclosures

Liquidity

Kelly Yeung

48

49

Presentation outline

• Background of the liquidity QIS

• “Walk-through” the QIS liquidity worksheet

• Questions and answers

50

Background

International framework for liquidity risk measurement, standards and monitoring, BCBS consultative document December 2009

•Proposing a global quantitative framework for liquidity risk supervision

•Objectives

-Strengthen banks’ resilience to liquidity stress

-Promote stronger liquidity buffers (quantity and quality) at banks

-Enhance international harmonisation of liquidity risk supervision

51

Background (cont’d)

• Propose two global quantitative liquidity standards (regulatory metrics)

- Liquidity Coverage Ratio (LCR)

i) Promote short-term resiliency of banks’ liquidity risk profiles

ii) Ensure banks have sufficient high quality liquid resources to survive an acute stress scenario lasting for one month

- Net Stable Funding Ratio (NSFR)

i) Promote banks’ resiliency over longer-term time horizons

ii) Establish a minimum acceptable amount of stable funding for a bank’s assets and off-balance sheet activities over a one year horizon

52

Background (cont’d)Purpose of the liquidity QIS

•Gather relevant data to assess the impact of the two regulatory metrics on banks

-LCR: Analyse the trade-offs between the severity of the stress scenario and the minimum levels of liquidity to be held by banks

-NSFR: Analyse the impact of the minimum amount of stable funding required of banks to support relevant assets and business activities

•QIS results will be used to recalibrate the parameters of the two regulatory metrics and for considering other possible options

-Ensure these regulatory metrics create strong incentives for banks to maintain prudent funding liquidity profiles while minimise negative impact on the financial system and broader economy

53

Background (cont’d)

QIS liquidity worksheet

•Capture relevant data for the LCR and NSFR measures

-Data in line with the liquidity consultative document

-A few areas with additional granularity for further analysis

-Mainly involves reporting of outstanding balances of on- and off-balance sheet assets and liabilities

54

QIS liquidity worksheet

General information

• Basis of reporting: Level 2 consolidated group

• Reporting period: end-Sept 2009 or end-Dec 2009 (must be consistent with other worksheets)

• Reporting currency: AUD (all foreign currency amounts should be converted into AUD using the exchange rate applicable at the reporting date)

55

QIS liquidity worksheet (cont’d)

General information (cont’d)

• Additional data requirements for the four major banks

- Provide separate equivalent data for Australia, New Zealand and UK

i) Australia: all ADIs and their overseas branches

ii) NZ: NZ banking subsidiaries (basis of reporting in line with RBNZ’s requirements)

(Note: Seek institution’s consent to share the NZ data with RBNZ)

iii) UK: UK banking subsidiaries (basis of reporting in line with the FSA’s requirements)

56

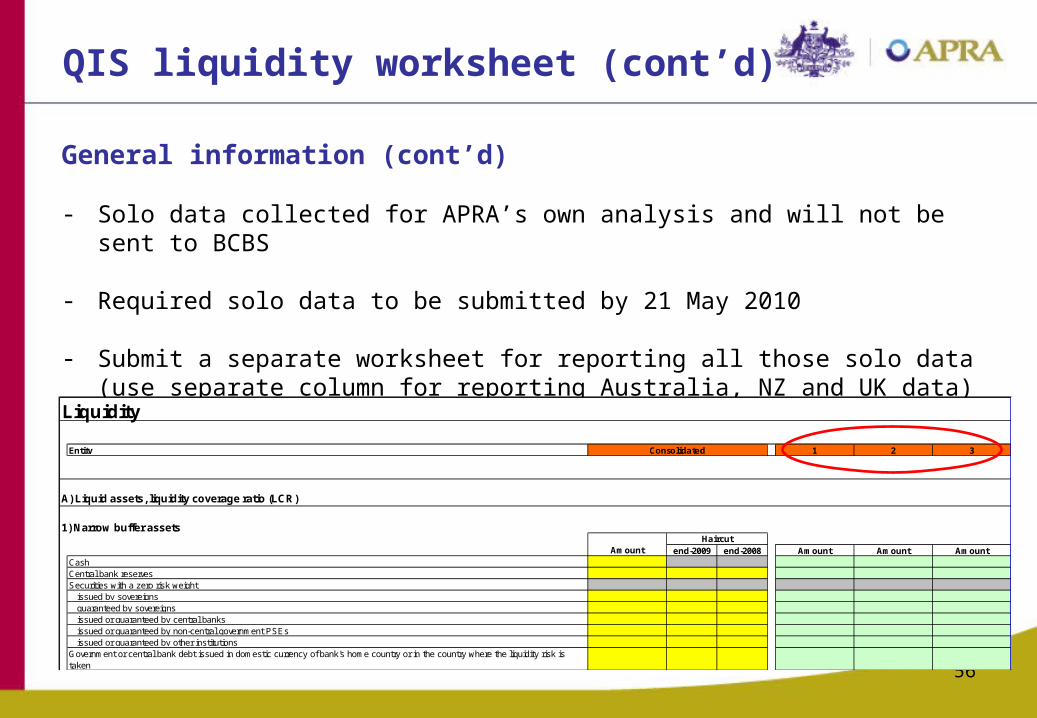

QIS liquidity worksheet (cont’d)

General information (cont’d)

- Solo data collected for APRA’s own analysis and will not be sent to BCBS

- Required solo data to be submitted by 21 May 2010

- Submit a separate worksheet for reporting all those solo data (use separate column for reporting Australia, NZ and UK data)

Liquidity

Entity 1 2 3

A) Liquid assets, liquidity coverage ratio (LCR)

1) Narrow buffer assets

end-2009 end-2008 Amount Amount AmountCashCentral bank reservesSecurities with a zero risk weight

issued by sovereignsguaranteed by sovereignsissued or guaranteed by central banksissued or guaranteed by non-central government PSEsissued or guaranteed by other institutions

Government or central bank debt issued in domestic currency of bank's home country or in the country where the liquidity risk is taken

Consolidated

AmountHaircut

57

QIS liquidity worksheet (cont’d)

General information (cont’d)

- Reporting period: end-Sept 2009 or end-Dec 2009 (must be consistent with the Level 2 data)

- Reporting currency: AUD (all foreign currency amounts should be converted into AUD using the exchange rate applicable at the reporting date)

58

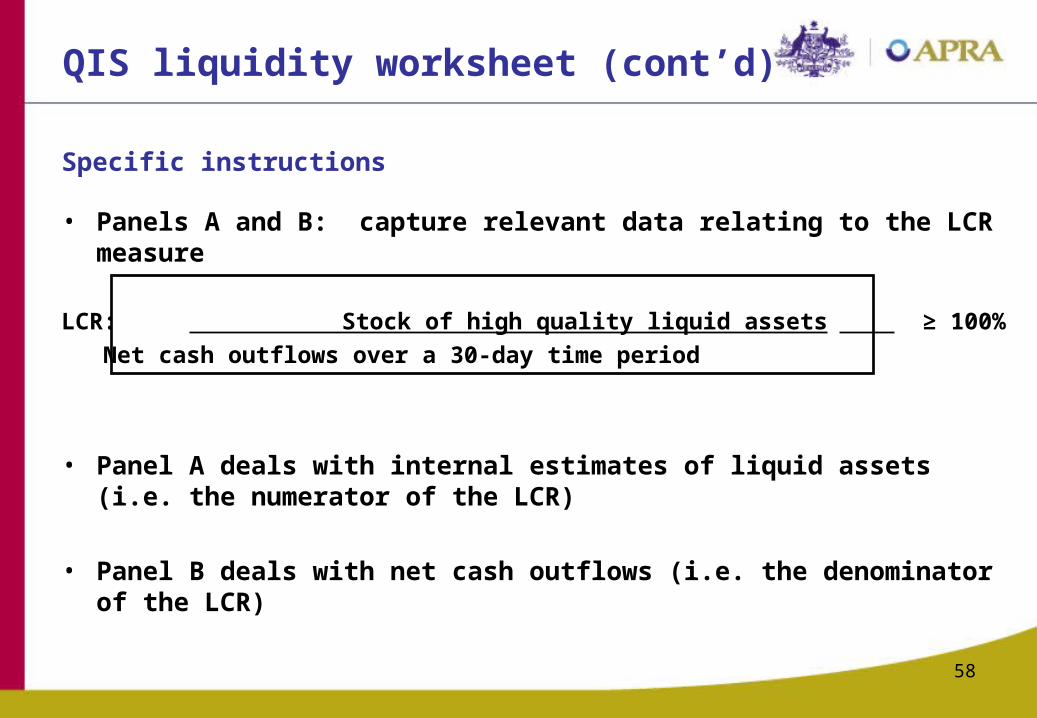

QIS liquidity worksheet (cont’d)

Specific instructions

• Panels A and B: capture relevant data relating to the LCR measure

LCR: Stock of high quality liquid assets ≥ 100% Net cash outflows over a 30-day time period

• Panel A deals with internal estimates of liquid assets (i.e. the numerator of the LCR)

• Panel B deals with net cash outflows (i.e. the denominator of the LCR)

59

QIS liquidity worksheet (cont’d)

Panel A: Liquid assets

• Panel A1 Narrow buffer assets

- In line with the proposed narrow definition of liquid assets set out in the BCBS liquidity consultative document

- Report ESA balances under line item 10 “Central bank reserves”

1) Narrow buffer assets

end-2009 end-2008 Amount Amount AmountCashCentral bank reservesSecurities with a zero risk weight

issued by sovereignsguaranteed by sovereignsissued or guaranteed by central banksissued or guaranteed by non-central government PSEsissued or guaranteed by other institutions

Government or central bank debt issued in domestic currency of bank's home country or in the country where the liquidity risk is taken

AmountHaircut

60

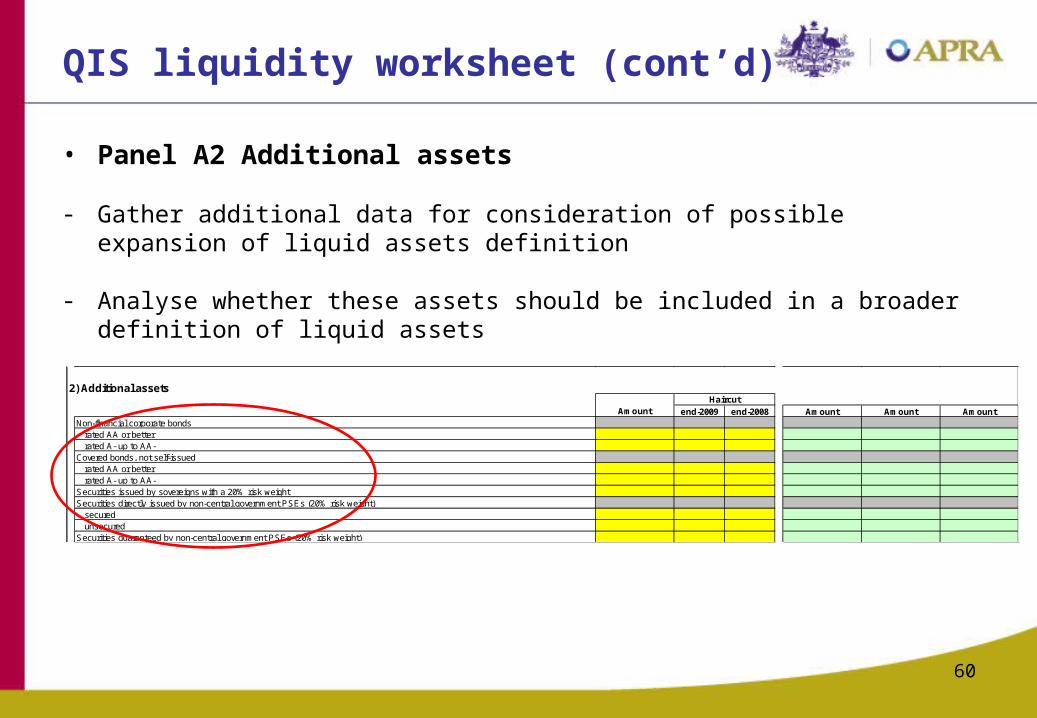

QIS liquidity worksheet (cont’d)

• Panel A2 Additional assets

- Gather additional data for consideration of possible expansion of liquid assets definition

- Analyse whether these assets should be included in a broader definition of liquid assets

2) Additional assets

end-2009 end-2008 Amount Amount AmountNon-financial corporate bonds

rated AA or better rated A- up to AA-

Covered bonds, not self-issuedrated AA or betterrated A- up to AA-

Securities issued by sovereigns with a 20% risk weightSecurities directly issued by non-central government PSEs (20% risk weight)

securedunsecured

Securities guaranteed by non-central government PSEs (20% risk weight)

AmountHaircut

61

QIS liquidity worksheet (cont’d)

• All assets reported under Panel A must be unencumbered and freely available for the next 30 days

- Any of the assets listed under Panel A received by the ADI as collateral (e.g. under reverse repos) can only be included if they remain at the ADI’s disposal throughout the 30-day time period

• All assets reported under Panel A must be central bank-eligible and cannot be issued by a bank, investment firm or insurance firm

• Once included in Panel A, those assets cannot be reported as cash inflows under Panel B2 to avoid double counting

• All securities should be reported at market value

62

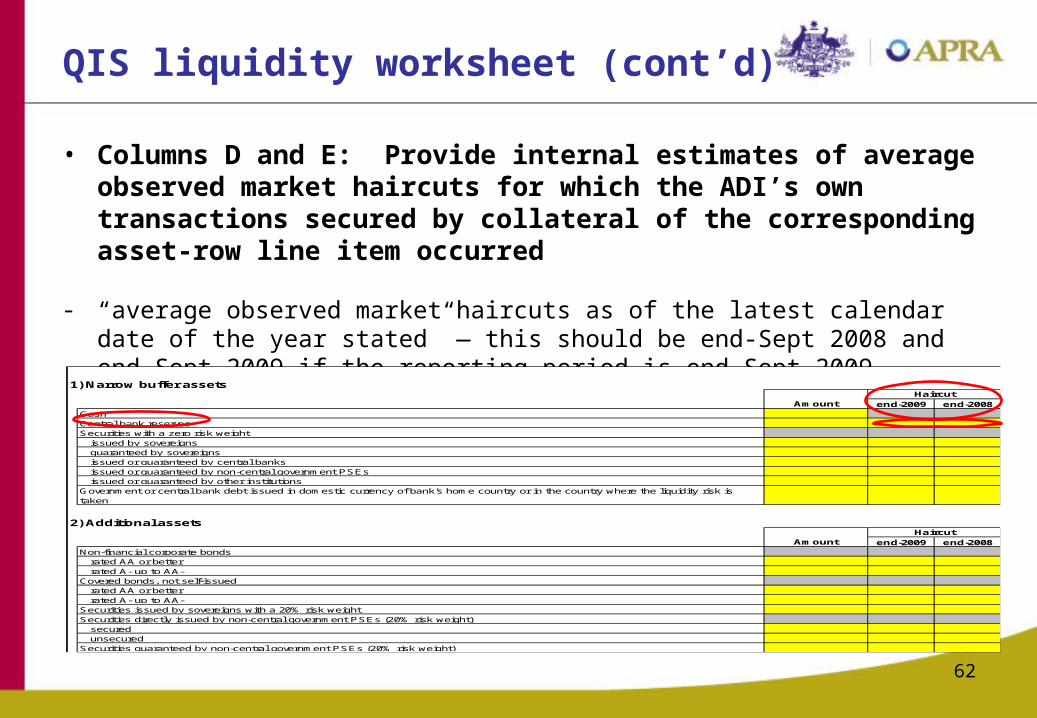

QIS liquidity worksheet (cont’d)

• Columns D and E: Provide internal estimates of average observed market haircuts for which the ADI’s own transactions secured by collateral of the corresponding asset-row line item occurred

- “average observed market haircuts as of the latest calendar date of the year stated” — this should be end-Sept 2008 and end-Sept 2009 if the reporting period is end-Sept 2009

1) Narrow buffer assets

end-2009 end-2008CashCentral bank reservesSecurities with a zero risk weight

issued by sovereignsguaranteed by sovereignsissued or guaranteed by central banksissued or guaranteed by non-central government PSEsissued or guaranteed by other institutions

Government or central bank debt issued in domestic currency of bank's home country or in the country where the liquidity risk is taken

2) Additional assets

end-2009 end-2008Non-financial corporate bonds

rated AA or better rated A- up to AA-

Covered bonds, not self-issuedrated AA or betterrated A- up to AA-

Securities issued by sovereigns with a 20% risk weightSecurities directly issued by non-central government PSEs (20% risk weight)

securedunsecured

Securities guaranteed by non-central government PSEs (20% risk weight)

AmountHaircut

AmountHaircut

63

QIS liquidity worksheet (cont’d)

• Haircut for central bank reserves: leave blank if inapplicable

• Can ADIs use central bank haircuts for “narrow buffer assets”?

64

QIS liquidity worksheet (cont’d)

Panel B: Net cash outflows

Panel B1 Cash outflows

• Capture outstanding liabilities that fall due within the 30-day window

• Include term deposits where withdrawal penalty is no greater than the loss of interest

65

QIS liquidity worksheet (cont’d)

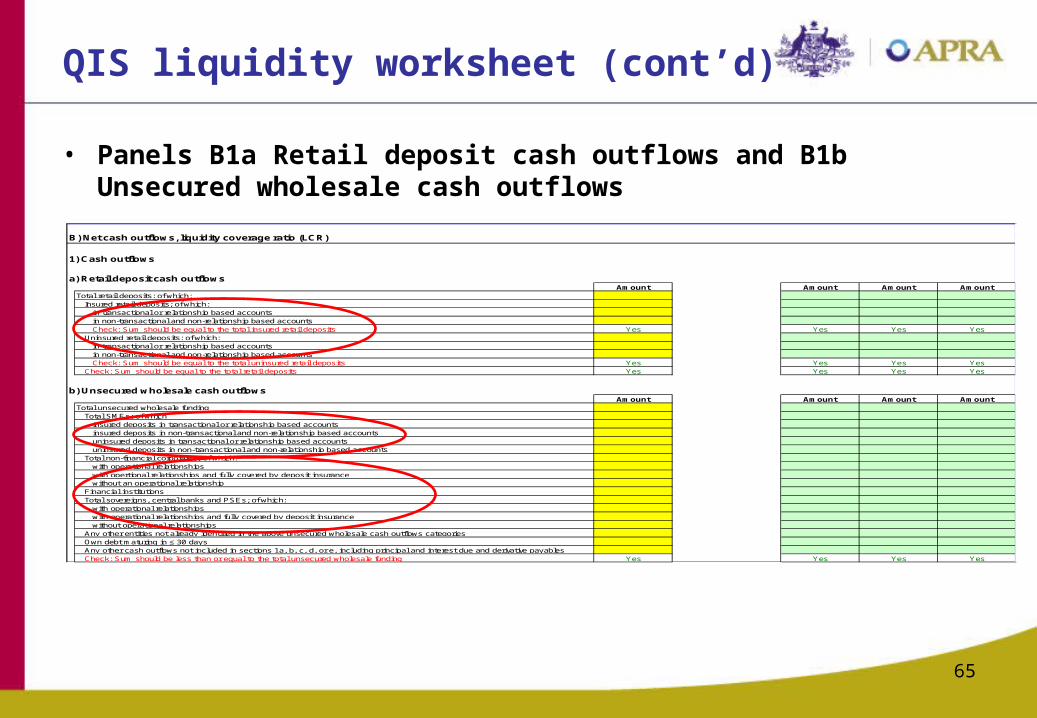

• Panels B1a Retail deposit cash outflows and B1b Unsecured wholesale cash outflows

B) Net cash outflows, liquidity coverage ratio (LCR)

1) Cash outflows

a) Retail deposit cash outflowsAmount Amount Amount Amount

Total retail deposits; of which:Insured retail deposits; of which:

in transactional or relationship based accountsin non-transactional and non-relationship based accountsCheck: Sum should be equal to the total insured retail deposits Yes Yes Yes Yes

Uninsured retail deposits; of which:in transactional or relationship based accountsin non-transactional and non-relationship based accountsCheck: Sum should be equal to the total uninsured retail deposits Yes Yes Yes Yes

Check: Sum should be equal to the total retail deposits Yes Yes Yes Yes

b) Unsecured wholesale cash outflowsAmount Amount Amount Amount

Total unsecured wholesale fundingTotal SMEs; of which

insured deposits in transactional or relationship based accountsinsured deposits in non-transactional and non-relationship based accountsuninsured deposits in transactional or relationship based accountsuninsured deposits in non-transactional and non-relationship based accounts

Total non-financial corporates; of which:with operational relationships with opertional relationships and fully covered by deposit insurancewithout an operational relationship

Financial institutionsTotal sovereigns, central banks and PSEs; of which:

with operational relationshipswith operational relationships and fully covered by deposit insurancewithout operational relationships

Any other entities not already identified in the above unsecured wholesale cash outflows categoriesOwn debt maturing in ≤ 30 daysAny other cash outflows not included in sections 1a, b, c, d, or e, including principal and interest due and derivative payablesCheck: Sum should be less than or equal to the total unsecured wholesale funding Yes Yes Yes Yes

66

QIS liquidity worksheet (cont’d)

- The QIS requires retail deposits and certain unsecured wholesale funding to be split by ‘transactional or relationship’ and ‘operational relationships’

i) The required data to be provided on a best-effort basis

ii) Where data is not available, ADIs can provide estimates

iii) Any assumptions used in making such estimates should be included in the qualitative document

iv) The QIS instructions provide some guidance on transactional and relationship based accounts and on operational relationships

67

QIS liquidity worksheet (cont’d)

• Panel B1c Secured funding cash outflow (due to failure to roll secured funding)

- Report outstanding amount of secured funding / repo transactions that will mature ≤ 30 days and are backed by relevant underlying assets (which mirror those assets under Panel A)

c) Secured funding cash outflow (due to failure to roll secured funding)Amount Amount Amount Amount

Overnight borrowings from central banksOther borrowings from central banks with remaining maturity of 30 days or lessTransactions backed by:

Securities with a zero risk weight, issued by sovereigns Securities with a zero risk weight, guaranteed by sovereigns Securities with a zero risk weight, issued or guaranteed by central banks Securities with a zero risk weight, issued or guaranteed by non-central government PSEs Securities with a zero risk weight, issued or guaranteed by other institutions Government or central bank debt issued in domestic currency of bank's home country or in country where the liquidity risk is takenNon-financial corporate bonds

rated AA or better rated A- up to AA-

Equities of non-financial entities listed on major index in recognised exchangeCovered bonds, not self-issued

rated AA or better rated A- up to AA-

Securities issued by sovereigns with a 20% risk weightSecurities directly issued by non-central government PSEs (20 % risk weight)

securedunsecured

Securities guaranteed by non-central government PSEs (20% risk weight)All other assets

68

QIS liquidity worksheet (cont’d)

• Panel B1d Additional requirements

- Report off-balance sheet items that may give rise to cash outflows in the next 30 days due to contractual obligations

d) Additional requirementsAmount Amount Amount Amount

Additional collateral that would need to be posted for short term financing transactions, derivatives and other contracts, due to a downgrade of up to three notches from current ratingEstimated outflows due to valuation changes on derivatives

Potential liquidity exposureLargest 30 day net outflow over the past 18 months related to these valuation changes

Outstanding amount of collateral posted for derivative transactionsCash and assets as defined in panel A1For collateral other than the assets described in panel A1

ABCP, conduits, SIVs and other financial facilitiesMaturing short-term debtMaturing longer-term debt, or non-maturing debt with embedded options

Amount of assets related to ABCP, conduits, SIVs and other financial facilities which could contractually be "returned" to the bankTerm ABS, covered bonds and other structured financing instruments not covered above – all maturing portions

Undrawn committed credit facilities to non-financial corporates Undrawn committed liquidity facilities to non-financial corporates Undrawn committed credit and liquidity facilities to…

retail clients financial institutionssovereigns, central banks or any other entity not included in other drawdown categories (not including intra-group facilities)

69

QIS liquidity worksheet (cont’d)

- Estimate potential liquidity exposure (outflows) in the next 30 days due to valuation changes on derivatives (line item 96)

i) The assumptions used in making such estimate should be included in the qualitative document

70

QIS liquidity worksheet (cont’d)

• Panel B1e Other cash outflows — non liquidity stress, non contractual triggers and other

- Other contingent funding obligations (line item 121)

i) An estimate of cash outflows associated with other contingent funding obligations occurring in 30 days or less

ii) The assumptions used in making such estimate should be included in the qualitative document

e) Other cash outflows – non liquidity stress, non contractual triggers and otherAmount Amount Amount Amount

Unconditionally revocable "uncommitted" credit and liquidity facilitiesGuaranteesLetters of creditOther trade finance instrumentsTotal amount outstanding of sponsored transactions, including conduits, SIVs, money market mutual funds and other such financing facilitiesFor banks with an affiliated broker dealer, amount of outstanding own debt securities with maturities beyond 30 daysOther contingent funding obligationsAny other cash outflows not included above, including principal and interest due and derivative payables

71

QIS liquidity worksheet (cont’d)

- Any other cash outflows not included above (line item 122)

i) This item may conflict with line item 66

ii) In any case, avoid double counting

72

QIS liquidity worksheet (cont’d)

Panel B2 Cash inflows

• Report expected contractual cash inflows over the next 30 days

• Panel B2b Wholesale unsecured and other

- Include lending exposures in the form of holdings of debt securities issued by those entities

i) If those securities have already been included in Panel A (e.g. non-financial corporate bonds), then they should not be included in Panel B2b in order to avoid double counting

b) Wholesale unsecured and otherAmount Amount Amount Amount

Contractual inflows from fully performing loans to…SMEsnon-financial corporatesfinancial institutionsother entities

Contractual inflows related to ABCP, conduits, SIVs and other such financing facilitiesOwn account, performing security cash flows (maturities and forward purchase/sales)Undrawn committed credit and liquidity facilities extended to the bankDeposits held at other financial institutionsOther cash inflows, including contractual receivables from derivatives

73

QIS liquidity worksheet (cont’d)

ii) Otherwise, include contractual inflows arising from these securities (e.g. principal amount and/or interest received) in the next 30 days

74

QIS liquidity worksheet (cont’d)

• Panel B2c Secured lending / reverse repo cash inflow

- Report cash inflows arising from secured lending / reverse repo transactions that mature in 30 days or less

- The underlying collateral should not be included as assets under Panel A

c) Secured funding/reverse repo cash inflowAmount Amount Amount Amount

Reverse repo and other secured funding transactions backed bySecurities issued by sovereigns with a zero risk weightSecurities guaranteed by sovereigns with a zero risk weightSecurities issued or guaranteed by central banks with a zero risk weightSecurities issued or guaranteed by non-central government PSEs with a zero risk weightSecurities issued or guaranteed by other institutions with a zero risk weightGovernment or central bank debt issued in domestic currency of bank's home country or in the country where the liquidity risk is Non-financial corporate bonds

rated AA or better rated A- up to AA-

Equities of non-financial entities listed on major index in recognised exchangeCovered bonds, not self-issued

rated AA or betterrated A- up to AA-

Securities issued by sovereigns with a 20% risk weightSecurities directly issued by non-central government PSEs (20% risk weight)

securedunsecured

Securities guaranteed by non-central government PSEs (20% risk weight)All other assets

75

QIS liquidity worksheet (cont’d)

Panel B3 Memo items for banks submitting legal entity information

• Only applicable to the four major banks

• Report separately intra-group flows between Australia / NZ / UK banking operations and other group entities

• Report separately undrawn committed credit and liquidity facilities provided by Australia / NZ / UK banking operations to other group members and vice versa

3) Memo items for banks submitting legal entity informationAmount Amount Amount Amount

Intra group cash inflows – maturing ≤ 1 monthIntra group cash outflows – maturing ≤ 1 monthIntra group – undrawn committed credit and liquidity facilities provided by other group membersIntra group – undrawn committed credit and liquidity facilities provided to other group members

76

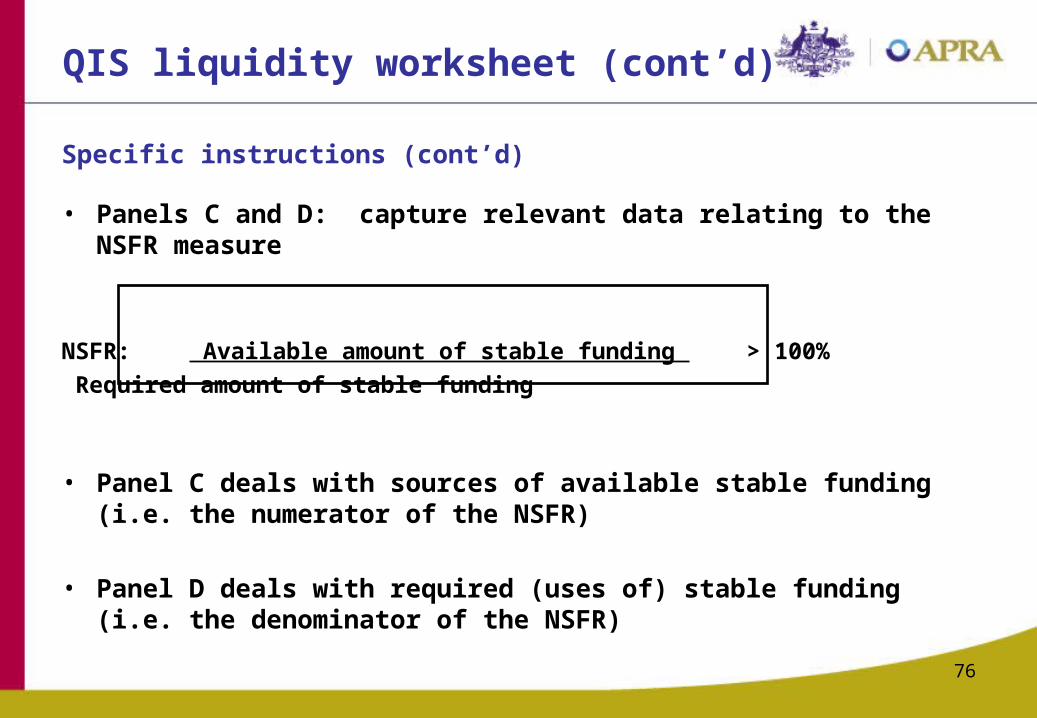

QIS liquidity worksheet (cont’d)

Specific instructions (cont’d)

• Panels C and D: capture relevant data relating to the NSFR measure

NSFR: Available amount of stable funding > 100% Required amount of stable funding

• Panel C deals with sources of available stable funding (i.e. the numerator of the NSFR)

• Panel D deals with required (uses of) stable funding (i.e. the denominator of the NSFR)

77

QIS liquidity worksheet (cont’d)

Panel C: Available stable funding

• Breakdown of various categories of outstanding liabilities with maturities:

- < 1 year- ≥ 1 year

• Further breakdown of liabilities with maturities < 1 year by time buckets of:

- < 3 months- ≥ 3 months to < 6 months- ≥ 6 months to < 12 months

78

QIS liquidity worksheet (cont’d)

Panel D: Required stable funding

• Breakdown of various categories of assets (e.g. loans, securities, etc) with maturities:

- < 1 year- ≥ 1 year

• Undrawn committed credit and liquidity facilities to fiduciaries (line items 256 and 257)

- Errors in the QIS instructions (make reference to fiduciaries in both line items)

- Will clarify with the BCBS QIS Working Group

79

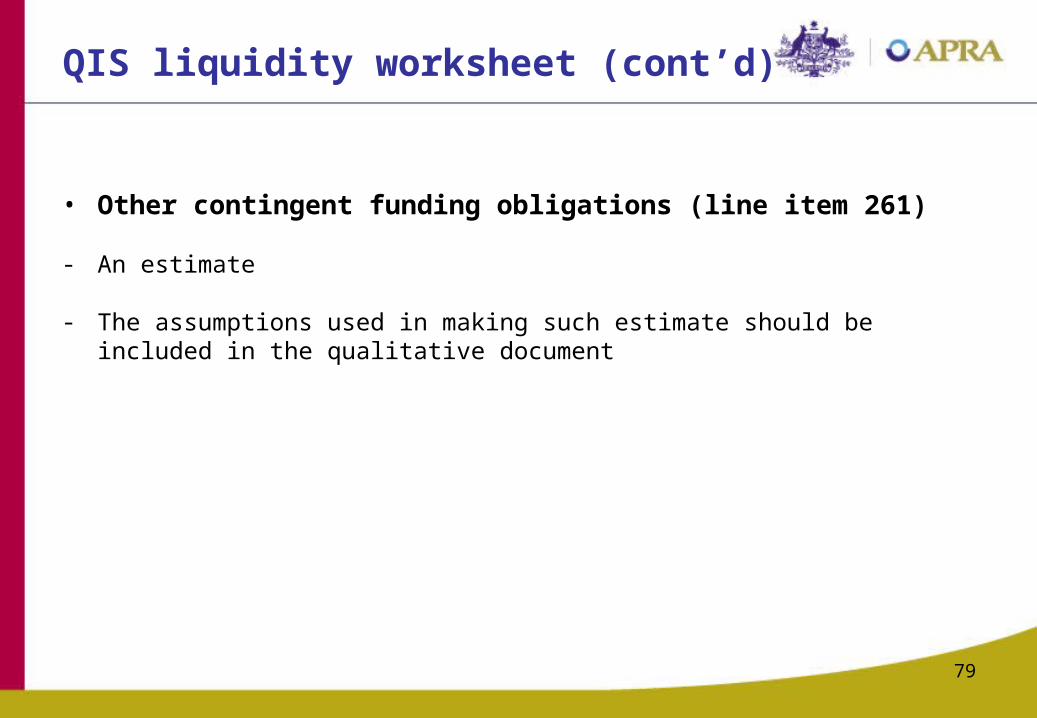

QIS liquidity worksheet (cont’d)

• Other contingent funding obligations (line item 261)

- An estimate

- The assumptions used in making such estimate should be included in the qualitative document

Counterparty credit risk and trading book

Denis Gorey

80

81

Trading Book• General comments• “TB” tab• “TB Securitisation” tabs• “TB Correlation” tabs

Counterparty Credit Risk• General comments• “General Info” tab• “CCR” tab

Agenda

82

Trading Book• General comments• “TB” tab• “TB Securitisation” tabs• “TB Correlation” tabs

Counterparty Credit Risk• General comments• “General Info” tab• “CCR” tab

Agenda

83

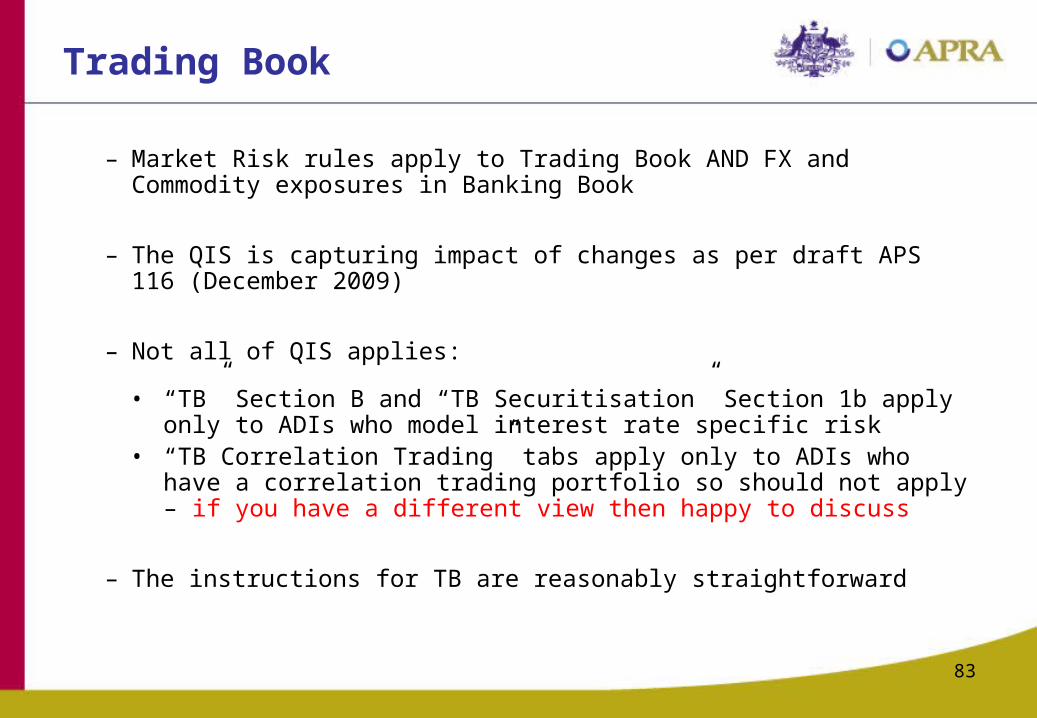

Trading Book

– Market Risk rules apply to Trading Book AND FX and Commodity exposures in Banking Book

– The QIS is capturing impact of changes as per draft APS 116 (December 2009)

– Not all of QIS applies:• “TB” Section B and “TB Securitisation” Section 1b apply only

to ADIs who model interest rate specific risk • “TB Correlation Trading” tabs apply only to ADIs who have a

correlation trading portfolio so should not apply – if you have a different view then happy to discuss

– The instructions for TB are reasonably straightforward

84

• General comments

• “TB” tab– Equity specific risk: Section A– Stressed VaR: Section B

• “TB Securitisation” tabs

Trading Book

85

• Zero unless:

– You have equity exposures subject to the standard method for equity specific risk

AND

– Some of these are subject to a 4% charge under paragraph 36 of Attachment B to APS 116 due to their classification as being both liquid and well-diversified (as would be reported in Column 2 of ARF_116_0_3)

Section A: Equity specific risk

86

• General comments

• “TB” tab– Equity specific risk– Stressed VaR

• “TB Securitisation” tabs

Trading Book

87

• Stressed VaR contribution– Stressed VaR observation period must be exactly one year – The draft standard says “from a continuous 12 month period of significant

financial stress relevant to the ADI‟s portfolio”. I suggest for QIS purposes: any 12 month period which includes all of the last quarter of 2008 should suffice

• Non-stressed VaR observation period– Ideally ending 31 Dec 2006 – is this feasible? If not then let’s discuss (the fall-

back is a choice of period that doesn’t include the GFC)

– No specification of length of period (but must be at least a year)

– Need to supply a description of approach used in an accompanying document

Section B: Stressed VaR

88

• General comments

• “TB” tab– Equity specific risk– Stressed VaR

• “TB Securitisation” tabs

Trading Book

89

• Should be relatively straightforward

• “Re-securitisation” as defined in the draft APS 120

• “10 most relevant instrument types” – classify in the same way as for the “Securitisation “ tab

“TB Securitisation” tabs

90

Trading Book• General comments• “TB” tab• “TB Securitisation” tabs• “TB Correlation” tabs

Counterparty Credit Risk• General comments• “General Info” tab• “CCR” tab

Agenda

91

Counterparty Credit Risk

– CCR rules calculate a loan equivalent Exposure at Default (EAD) for OTC derivatives, repos, stock lending and borrowing and other securities financing transactions (SFTs) but Section E of “CCR” tab also applies to loan activity

– Under Basel framework: 3 ways of calculating EAD• Current exposure method (currently used)• Standardised method• Internal Model Method

– QIS generally focuses on IMM – so much doesn’t apply• Sections A1, B2, C, D, and G of “CCR” tab do not apply• Focus only on sections A2, B1, E and F of “CCR” tab

92

• General comments

• “General Info” tab – current CCR capital – should be straightforward

• “CCR” tab– CVA loss charge– Asset value correlation– Central counterparties– Impact summary

Counterparty Credit Risk

93

• General comments

• “General Info” tab

• “CCR” tab– CVA loss charge: Section B1– Asset value correlation: Section E– Central counterparties: Section F– Impact summary: Section A2

Counterparty Credit Risk

94

• Bond equivalent CVA charge First step: determine EAD (as done currently,

APS112)

Second step: determine Effective Maturity

For each instrument in a netting set, Effective Maturity is calculated in accordance with the calculation of M in paragraphs 33-34 or attachment B to APS 113 (either weighted by cash-flows or, more conservatively, notional maturity) except that:

• To calculate the CVA capital charge, the maturity M to use in the subsequent calculations is the longest Effective Maturity (as calculated above) across all netting sets with the counterparty.

• It should not be capped at five years, since CVA is the lifetime discounted expected loss of the counterparty.

Section B1: CVA charge

95

• Bond equivalent CVA chargeThird step: obtain a CDS spread for the counterparty

• The spread used to calculate the CVA of the counterparty should be used.

• If a CDS spread or bond spread is available for the counterparty use this

• If no CDS or bond spread is available for the counterparty, then map the counterparty to a generic spread curve, for example by rating, industry and country.

• This curve provides the spread that should be used in the calculation of the bond-equivalent CVA capital charge.

• If the bank has to make approximations or extrapolations for some tenors of the CDS spread curve when determining the CVA, these same extrapolated CDS spread tenors should be used in the calculation of the bond-equivalent capital charge.

• For the capital charge, only one tenor is needed: the tenor corresponding to the Effective Maturity determined in Step 2.

Section B1: CVA charge

96

• Bond equivalent CVA chargeFourth step: determine the market risk charge for CVA

This is an approximation for the CVA of a counterparty with

• expected exposure on average equal to EAD• effective maturity equal to M• annualized CDS spread at the tenor M equal to s• r is the annualized risk-free interest rate

Note that the PV is negative, which reflects the fact that CVAs are subtracted from the counterparty-risk-free value of derivatives to obtain fair value.

Section B1: CVA charge

97

• Bond equivalent CVA chargeFourth step (a): determine the market risk charge for CVA

Calculate charge twice: • (1) once using exposure as shown on previous slide• (2) second time using EAD

For both calculations:

• Total market risk charge = Interest rate specific risk charge + Interest rate general market risk change (both calculated according to Attachment B to APS 116)

• CVA charge = total market risk charge x 5

• RWA for CVA = CVA charge x 12.5 (risk weight of 8% to be used)

ADIs are NOT required to calculate internal model numbers (as they use SMM for interest rate specific risk), but happy to discuss this.

Section B1: CVA charge

98

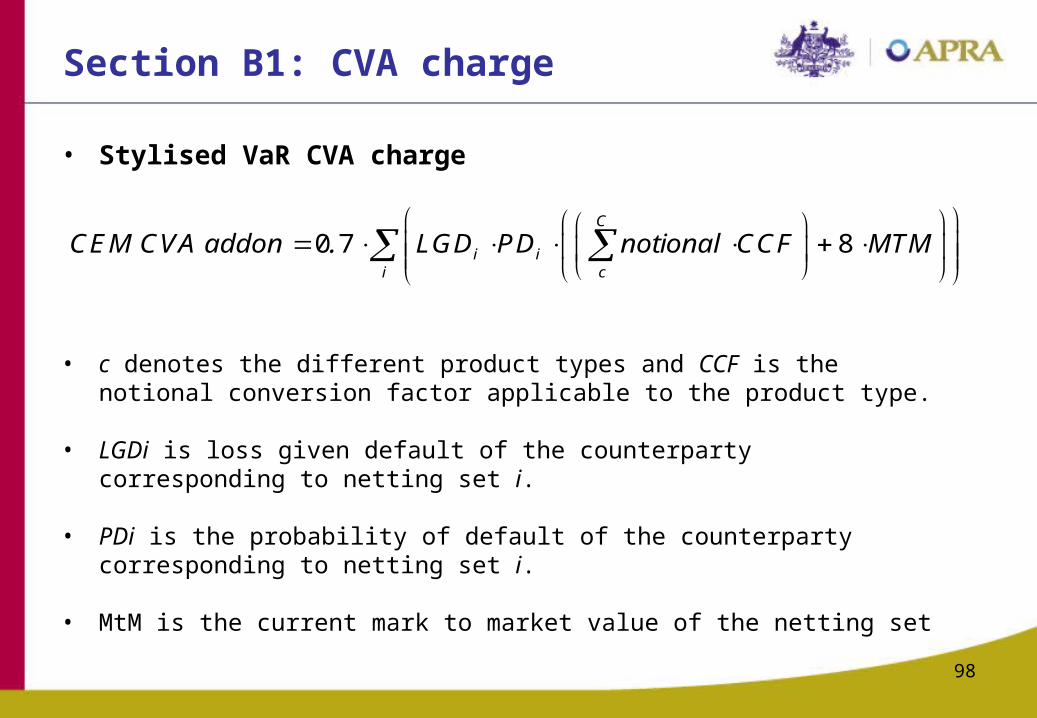

• Stylised VaR CVA charge

• c denotes the different product types and CCF is the notional conversion factor applicable to the product type.

• LGDi is loss given default of the counterparty corresponding to netting set i.

• PDi is the probability of default of the counterparty corresponding to netting set i.

• MtM is the current mark to market value of the netting set

0 7 8C

i ii c

CEM CVA addon . LGD PD notional CCF MTM

Section B1: CVA charge

99

• Rows 52 to 57: Impact of CVA on EL and EAD? Will be seeking more clarification from Basel

• Rows 62 to 65: Do not complete Column I

Section B1: CVA charge

100

• General comments

• “General Info” tab

• “CCR” tab– CVA loss charge: Section B1– Asset value correlation: Section E– Central counterparties: Section F– Impact summary: Section A2

Counterparty Credit Risk

101

• Apply 1.25x multiplier to AVC for exposures to “Financial Counterparties” (i.e. 12-24% range becomes 15%-30%)

• Broad definition include:• Regulated banks and non-banks (subject to a threshold, with two thresholds

investigated), and• unregulated Financial Institutions and other financial intermediaries (e.g.

highly levered entities)

• AVC increase applies to all exposures to Financial Counterparties (e.g. loans) – not just CCR

• Awaiting Basel guidance/ clarification on calculation of threshold, in particular:

• Individual counterparties or consolidated group• Definition of regulated• Which unregulated entities are to be included• Definition of “highly leveraged”

Section E: Asset Value Correlation

102

• General comments

• “General Info” tab

• “CCR” tab– CVA loss charge: Section B1– Asset value correlation: Section E– Central counterparties: Section F – should be straightforward– Impact summary: Section A2

Counterparty Credit Risk

103

• General comments

• “General Info” tab

• “CCR” tab– CVA loss charge: Section B1– Asset value correlation: Section E– Central counterparties: Section F– Impact summary: Section A2 – should be straightforward

Counterparty Credit Risk

Smoothing minimum required capital (procyclicality)

Guy Eastwood

104

Smoothing MRC• Cyclicality of minimum capital requirements (MRC) is one

aspect of the wider issue of procyclical behaviour within the financial system

• BII Framework, as well as being more risk sensitive (particularly IRB), is also more cyclical

• Cyclicality issues, in part, influenced the design of the BII Framework (eg IRB risk weighting functions, stress test requirements)

• Basel Committee is now considering whether additional measures should be introduced to deal with cyclicality of MRC, eg more formal means of building up capital buffers in good times & allowing access in downturns (smoothing MRC)

• Difficult issue in practice. QIS aims to help inform discussion on the need for additional measures in this area, their potential magnitude & mechanics of operation 105

106

Smoothing MRC

The portfolio-level PD at time t is calculated as the average of assigned grade PDs weighted by the number of counterparties in each grade.

The portfolio-level PD changes over the cycle as the result of the migration of borrowers across grades and possible changes of grade PD. At any particular point in time, a scaling factor could be determined by comparing this portfolio-level PD to some PD benchmark.

gk

g

gk

g

g

N

NPD

1

1

107

Smoothing MRC

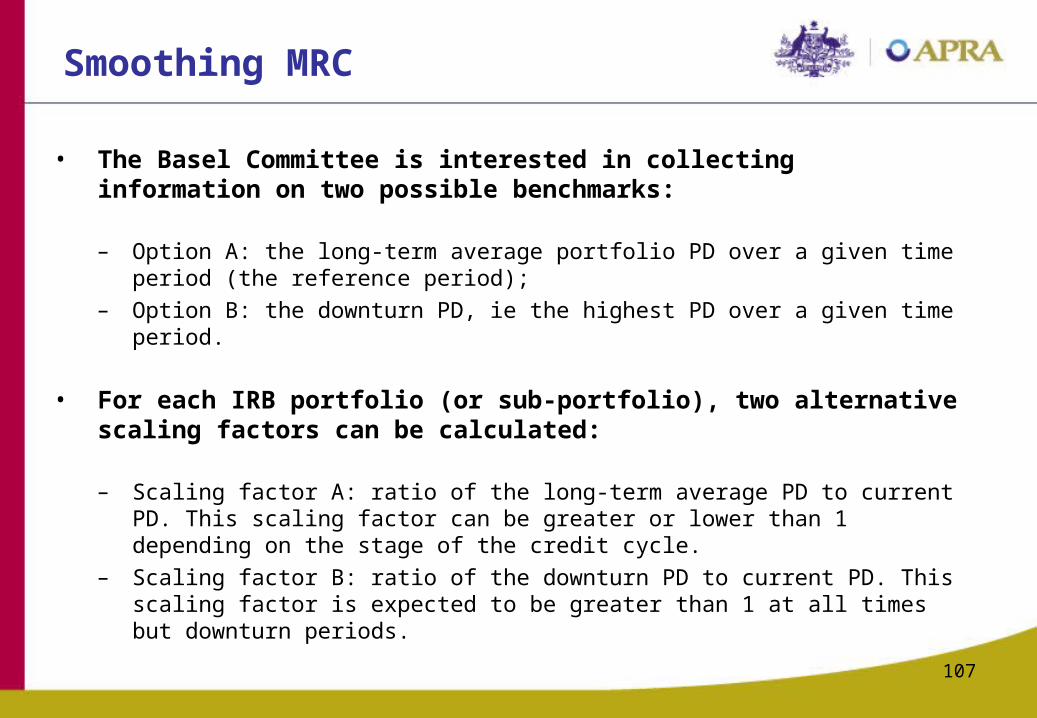

• The Basel Committee is interested in collecting information on two possible benchmarks:

– Option A: the long-term average portfolio PD over a given time period (the reference period);

– Option B: the downturn PD, ie the highest PD over a given time period.

• For each IRB portfolio (or sub-portfolio), two alternative scaling factors can be calculated:

– Scaling factor A: ratio of the long-term average PD to current PD. This scaling factor can be greater or lower than 1 depending on the stage of the credit cycle.

– Scaling factor B: ratio of the downturn PD to current PD. This scaling factor is expected to be greater than 1 at all times but downturn periods.

108

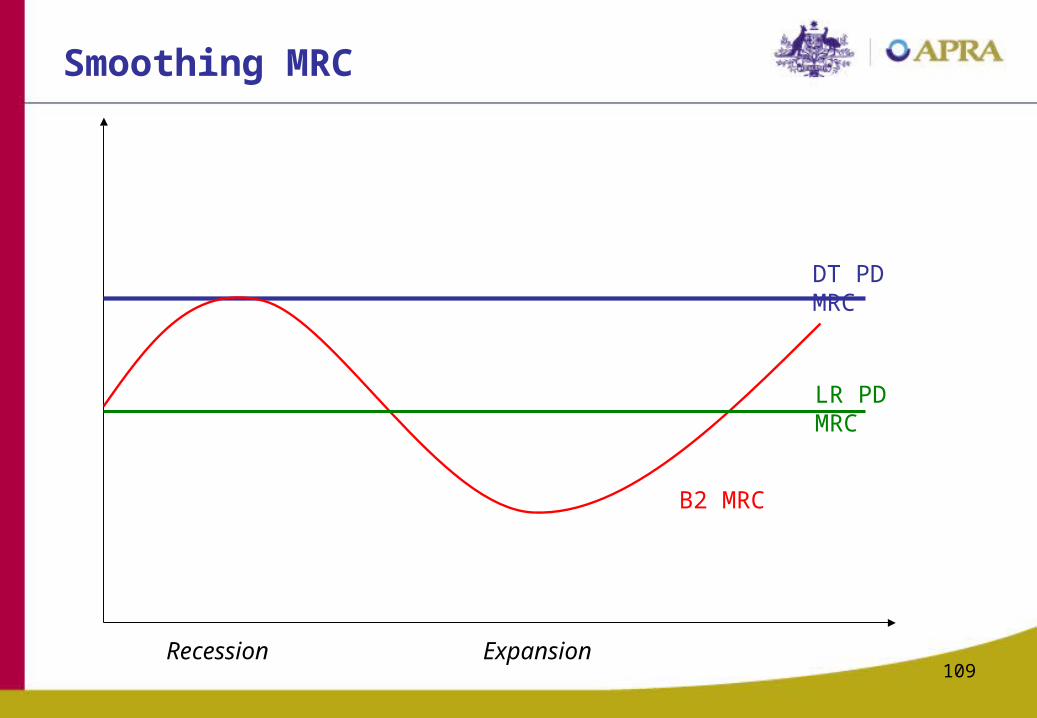

Smoothing MRCSteps:• For each rating grade, the scaling factors can used to

adjust current grade PDs.

• For each grade, a capital buffer can then be determined as the difference between the amount of capital computed using the current PD and the amount computed using the PD adjusted with either scaling factor A or scaling factor B.

• For each portfolio, the overall buffer would the sum of grade-level buffers using one or the other scaling factor:– The buffer would increase in expansion and decrease in recession,

according to the path followed by PDs: – Under Option A, the idea is that portfolio-level PDs estimated

through a point-in-time rating system would be transformed into something like through-the-cycle PDs;

– Under Option B, portfolio-level PDs would be transformed into recessionary PDs incorporating the impact of stressed conditions.

109

Smoothing MRC

Recession Expansion

DT PD MRC

LR PD MRC

B2 MRC

110

Smoothing MRC worksheet

Main features:

• Only for IRB banks

• Scaling information requested only for IRB portfolio subject to a PD/LGD approach

• 4 dates: 2006-2009 time-dynamics is crucial

• Best effort basis for the calculation of downturn and long-term PD but banks should be encouraged to provide estimates based on sufficiently long-time series

111

Smoothing MRC worksheet

No distinction between drawn, undrawn and other off-balance sheet items. Only non-defaulted exposures should be included.WHY ARE WE ASKING THIS?To assess the share of portfolios subject to PD/LGD approach as a percentage of total banking book and IRB portfolios

pre-CCF and pre-CRM

post-CCF and post-CRM

Total corporate (not including receivables); of which:Corporate (not including SMEs, specialised lending and receivables)Other SLSL HVCRESME treated as corporateUnassigned

SovereignBankRetail; of which:

Residential mortgagesOther retail Qualifying revolving retail exposuresUnassigned

Equity: PD/LGD approachPurchased receivablesTotal IRB perimeterTotal banking book

IRB exposure

Columns F and G

Data on exposures

112

Smoothing MRC worksheet

Only non-defaulted exposures should be included.WHY ARE WE ASKING THIS?Data on PDs are the main input of the approach.The quality of the estimates for downturn and LT PDs affects the quality of the whole exercise

Columns H, I and J

Data on PDs (1/2) These are the most important data

Current Long term avg Downturn

Total corporate (not including receivables); of which:Corporate (not including SMEs, specialised lending and receivables)Other SLSL HVCRESME treated as corporateUnassigned

SovereignBankRetail; of which:

Residential mortgagesOther retail Qualifying revolving retail exposuresUnassigned

Equity: PD/LGD approachPurchased receivables

PD

gk

g

gk

g

g

N

NPD

1

1

113

Smoothing MRC worksheet

Bank A does have time series on PDs for 10 years, for each regulatory portfolio.

For the corporate portfolio data are as follows:

Data on PDs (2/2): an example

YEAR PD 2000 0.012001 0.032002 0.052003 0.062004 0.042005 0.022006 0.03 current PD for 20062007 0.04 current PD for 20072008 0.06 current PD for 20082009 0.09 current PD for 2009

LT PD (mean 2000-09) 0.043DT PD (max 2000-09) 0.09

gk

g

gk

g

g

N

NPD

1

1

Following steps:1) Scaling factor at the portfolio level2) Applied at each grade PD3) Rescaled grade PD used for determining grade RWAs

114

Smoothing MRC worksheet

Only non-defaulted exposures should be included.WHY ARE WE ASKING THIS?RWAs are used for calculating the buffers.They are to be computed at the grade level and then aggregated to the portfolio level

Columns K, L and M

Data on RWAs

Current Long term avg Downturn

Total corporate (not including receivables); of which:Corporate (not including SMEs, specialised lending and receivables)Other SLSL HVCRESME treated as corporateUnassigned

SovereignBankRetail; of which:

Residential mortgagesOther retail Qualifying revolving retail exposuresUnassigned

Equity: PD/LGD approachPurchased receivables

Risk-weighted assets

For each reference date use that year’s current & rescaled PDs but 2009 data for all other inputs into the RWA calculations

115

Smoothing MRC worksheet

WHY ARE WE ASKING THIS?The QIS instructions ask banks to use sufficiently long time series, but do not predefine a minimum no of years.It is thus important to know what banks actually did.

Columns C, D and E

Info on time series-used

Start year End year

Total corporate (not including receivables); of which:Corporate (not including SMEs, specialised lending and receivables)Other SLSL HVCRESME treated as corporateUnassigned

SovereignBankRetail; of which:

Residential mortgagesOther retail Qualifying revolving retail exposuresUnassigned

Equity: PD/LGD approachPurchased receivables

Time span for calculation of PD long

term avg and PD downturn Ref year for

the PD downturn

Following the previous example, bank A would indicate for the corporate portfolio: 2000 as start year, 2009 as end year and 2009 as the reference year for DT PD

116

Smoothing MRC worksheet

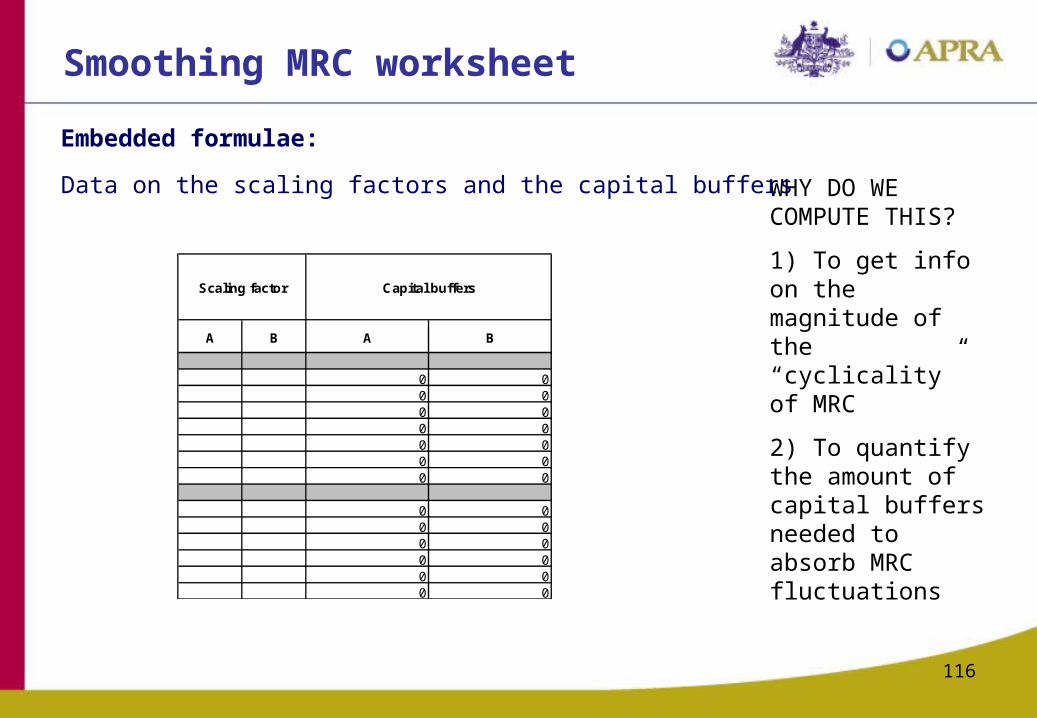

WHY DO WE COMPUTE THIS?1) To get info on the magnitude of the “cyclicality” of MRC2) To quantify the amount of capital buffers needed to absorb MRC fluctuations

Embedded formulae: Data on the scaling factors and the capital buffers

A B A B

0 00 00 00 00 00 00 0

0 00 00 00 00 00 0

Scaling factor Capital buffers

117

Smoothing MRC worksheet

Only non-defaulted exposures should be included.WHY ARE WE ASKING THIS?To have some preliminary evidence on the impact on the numerator (via regulatory calculation difference) + some info for dynamic provisions

Columns N, O and P

Memo items: Provisions and ELTotal eligible provisions 0

Current Long term avg Downturn

Total corporate (not including receivables); of which:Corporate (not including SMEs, specialised lending and receivables)Other SLSL HVCRESME treated as corporateUnassigned

SovereignBankRetail; of which:

Residential mortgagesOther retail Qualifying revolving retail exposuresUnassigned

Equity: PD/LGD approachPurchased receivables

EL

118

Concluding remarks • Having an annual PD series of reasonable length and quality is

crucial to gain anything meaningful from this part of the QIS

– this will require professional judgment in developing back estimates of PD and determining how far back to go … BUT we’re not insisting on precision here, just something reasonable to be working with – interested in hearing at an early stage how respondents might intend to

do this. Is there value in us all getting together to discuss way(s) forward?

• Also our thought is that use of 2009 inputs into the RWA calculations (except for PD) for all reference dates should make the data gathering/calculation burden much less. Do respondents agree? Are respondents clear on what has been asked for or are there issues/complications that we might not be seeing? Again, is there value in meeting on an industry basis to discuss?

QUESTIONS/COMMENTS?

Securitisation

Anna Sofianaris

119

120

Securitisation• “Current” columns completed in accordance with APS 120

Securitisation (January 2008)

• “New” columns completed in accordance with draft APS 120 Securitisation (December 2009)

• Exposure amounts reported: - after application of credit conversion factors - without recognition of any cap or provisions/value adjustments

• Exclude deductions for gain-on-sale

• Exclude exposures in the trading book

• Exclude modifications to APS 120 reflecting additional APRA proposals (i.e. focus is on Basel II enhancements)

121

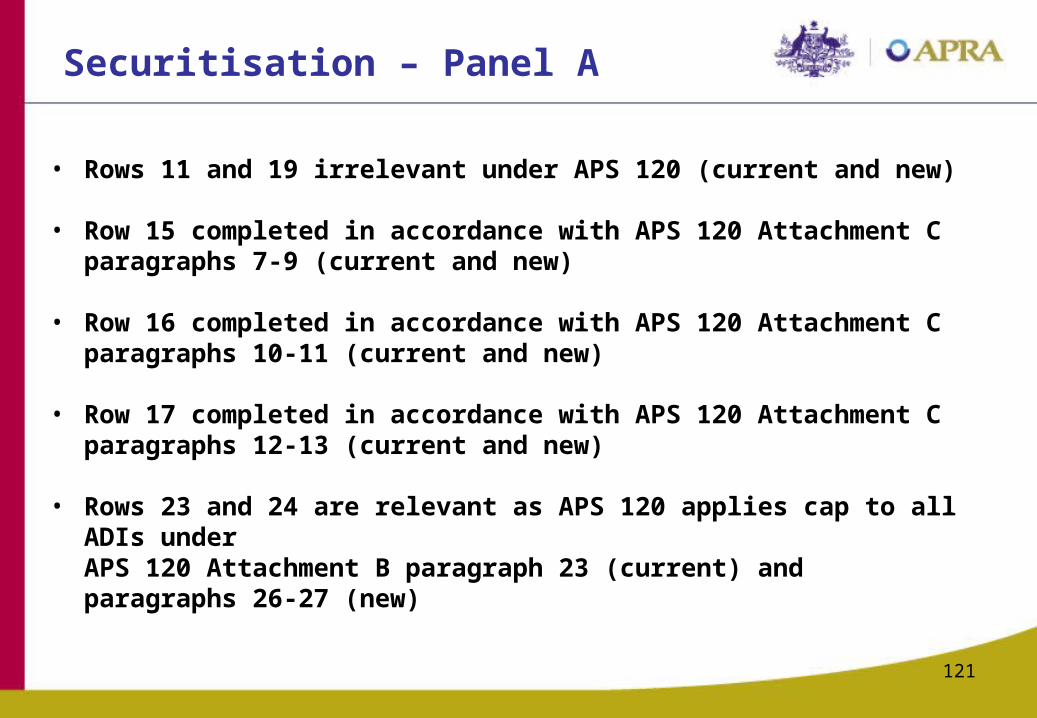

Securitisation – Panel A

• Rows 11 and 19 irrelevant under APS 120 (current and new)

• Row 15 completed in accordance with APS 120 Attachment C paragraphs 7-9 (current and new)

• Row 16 completed in accordance with APS 120 Attachment C paragraphs 10-11 (current and new)

• Row 17 completed in accordance with APS 120 Attachment C paragraphs 12-13 (current and new)

• Rows 23 and 24 are relevant as APS 120 applies cap to all ADIs under APS 120 Attachment B paragraph 23 (current) and paragraphs 26-27 (new)

122

Securitisation – Panel B• Rows 45, 64, 70 and 76 are irrelevant under APS 120 (current

and new)• Rows 33, 52 and 82 not applicable to Australian ADIs• Rows 32-44 completed in accordance with APS 120 Attachment

D paragraphs 4-10 (current) and paragraphs 4-11 (new)• Rows 51-63 completed in accordance with APS 120 Attachment

D paragraphs 11-14 (current) and paragraphs 12-15 (new)• Rows 68-69 completed in accordance with APS 120 Attachment

D paragraphs 15-36 (current) and paragraphs 16-37 (new)• Row 74 relates to treatment under APS 120 Attachment D

paragraph 37 (current) and paragraph 38 (new)• Rows 80-81 relate to APS 120 Attachment B paragraph 23

(current) and paragraphs 26-27 (new)

Operational risk

Michael Booth

123

124

OpRisk – background / general

• Gross Income & assets are only partial indicators for OpRisk capital

• Collect additional data to support SIGOR’s review of OpRisk metrics– Review the appropriateness / calibration of BIA & TSA– Are there additional or alternate measures?– Assess influences of BIA & TSA on AMA implementation

• General Info worksheet:– Participated in 2008 LDCE ? (Cell C26)– OpRisk risk-weighted assets: ASA / AMA (Rows 99,100)

• DefCapCal worksheet – Rows 123,124

125

OpRisk – general information

• OpRisk worksheet required for AMA banks only!

• By year: 2006 to 2009

• Approach: ASA or AMA

• M & A: Yes / No (default)

• Disposals: Yes / No (default)

Year Approach

Mergers/ acquisitions with relevant effects on the

operational risk regulatory capital

Disposals with relevant effects on the operational

risk regulatory capital

2006 No No 2007 No No 2008 No No 2009 No No

126

OpRisk – exposure indicators

• By reference year (2005 to 2009)

• By Basel business line* where applicable (“best effort” basis)

• Potential Alternatives to Gross Income– Size / Complexity– On- /off-balance sheet items– Income statement

• Gross Income and its components

• Generally IAS / IFRS definitions (Please document any deviations)

• See QIS documentation for more detailed information

127

OpRisk – Operational Risk Losses

• By discovery year or year of financial impact (2005 to 2009)

• By whole-firm & Basel business line

• Number:– Loss events ≥ €10,000 (AUD $20,000) or ≥ €20,000 (AUD $34,000*)

• Severity:– Total amount of losses ≥ €20,000 (AUD $34,000)– Sum of the five largest losses– Maximum loss

• *Exchange rate: 1 AUD = 0.5882 € (for €20,000 loss threshold)

128

OpRisk – QIS & APRA• Parts of the current framework can be further enhanced

• APRA is actively involved in SIGOR discussions and working groups

• Information collected will provide additional information for analysis on the size, scale and nature of the ADI’s and provide comparisons between jurisdictions

• Important to note that the overall operational risk profile of an entity depends on the combined influence of many different drivers, such as: its nature, complexity and size; internal operating environment, external environment, material changes and culture. The information being collected does not cover all these aspects

• Further work towards understanding the operational risk profiles is being undertaken as part of APRA’s internal loss and scenario analysis data collection exercises

129

OpRisk – Questions?

• Question. Are we there yet?

• Answer. ALMOST…

130

Wrap-up

Slides will be made available on the APRA website

Questions