24

QSC AG Company Presentation Results Q1 2015 Cologne, 11 May 2015

| Date post: | 23-Jul-2015 |

| Category: |

Investor Relations |

| Upload: | qsc-ag |

| View: | 109 times |

| Download: | 0 times |

QSC AG Company Presentation

Results Q1 2015

Cologne, 11 May 2015

2

AGENDA

1. Strategic Update

2. Financial Update and Outlook 2015

3. Questions & Answers

3

QSC WITH A GOOD START TO Q1 2015

• Strong TC revenues led to total revenues of € 104.7 million (Q1 2014: € 109.1million)

• TCV rises to € 64.2 million (Q1 2014: € 27.3 million), mainly driven by a € 40 million order

from SÜWAG (revenue impact from 2016 onwards)

• Improvement in earnings: EBIT higher than in Q3 and Q4 2014

• Staff cuts: Termination of around 100 employee contracts agreed by end of April

• Progress in Cloud business: Vodafone will integrate FTAPI technology into its

“Secure E-Mail” solution

• New segment reporting gives a better view of each business segment

4

• B-B-B segment, which offers voice and data services to medium-sized companies,

has been stable and profitable for years now

• QSC’s access product portfolio for business customers is very competitive

• Our network benefits our customers in the Outsourcing segment

• Security and reliability will be very important for cloud services

QSC DECIDED TO CONTINUE OPERATING

ITS DSL NETWORK

5

PARADIGM SHIFT IN OUTSOURCING BUSINESS

• Recent market studies show an increasing demand for outsourcing

• Standardisation of IT services is very important for our business customers,

due to cost-cutting requirements

• Our infrastructure (IP network and data centres) supports our strategy

• QSC will offer multi-cloud services and migrate traditional outsourcing services to the cloud

6

• Market for IT Consulting shows stable growth with yearly growth rates of 4-5%

• Consulting is essential for Cloud onboarding

• Consulting business is a good door-opener for Outsourcing business

• The relevance of industry-specific know-how is growing fast

CONSULTING MARKET SHOWS STABLE GROWTH

7

OUR WHOLESALE APPROACH AND EXPERIENCE

FIT PERFECTLY WITH CLOUD PRODUCTS

• Vodafone will be relying in future on encryption

technology from QSC’s subsidiary FTAPI

• Consistent end-to-end encryption

• Automatic key exchange

• Integration and further use of existing e-mail accounts

• QSC is currently in talks with other European telcos

– to multiply this wholesale approach

8

AGENDA

1. Strategic Update

2. Financial Update and Outlook 2015

3. Questions & Answers

QSC STARTED Q1 2015 BETTER THAN EXPECTED

9

Revenues:

• TC and Outsourcing weaker

than in the previous year

• Consulting and Cloud business

improved

EBIT:

• Below Q1 2014

• Better than Q3 & Q4 2014

• Too early to notice a huge

impact of the cost-cutting

programme

10

NEW SEGMENTATION REFLECTS PRODUCT-ORIENTED

MANAGEMENT SYSTEM

• From 1 January 2015 on, segment reporting

will be based on the current product portfolio:

• Telecoms

• Consulting

• Outsourcing

• Cloud

11

STABLE TELECOMS BUSINESS

• Stability despite negative regulatory

impact of € 2.5 million per quarter

in 2015

• Stable B-B-B revenues since Q2 2014

• Decline in B-B-C revenues softened

by very efficient network operations

• Consumer market still characterised

by tough competition

12

OUTSOURCING’S FUTURE FOCUS IS ON SMEs

• Focus on medium-sized customers

• Focus on specific industries such

as energy, financial services,

manufacturing and transportation

13

CONSULTING IS WELL ON TRACK

• After the setback in H1 2014,

Consulting is well back on track

• Revenue driver: SAP applications

• Consulting – a good door-opener

for the Cloud business

14

CLOUD BUSINESS STILL CHARACTERIZED

BY PROJECTS AND PILOTS

• +86% growth compared to Q1 2014

• Cloud business still in the early

stages, characterised by

• Development activities

• Pilot projects

• Initial market successes

• Next steps:

• Recurring revenues (e.g. Vodafone)

• Strengthening of online sales

15

GROSS MARGIN BACK AT THE LEVEL OF Q2 2014

• In Q1 2015, QSC earned a

gross margin of 25.9%

• Cost of revenues influenced

by lower ongoing costs and

first reductions in personnel

costs

16

EBITDA DEVELOPED AS PLANNED IN Q1 2015

• In Q1 2015, QSC earned

an EBITDA margin of 8.7%

• Strengthening of sales

activities for the Cloud

business prevents higher

increase

17

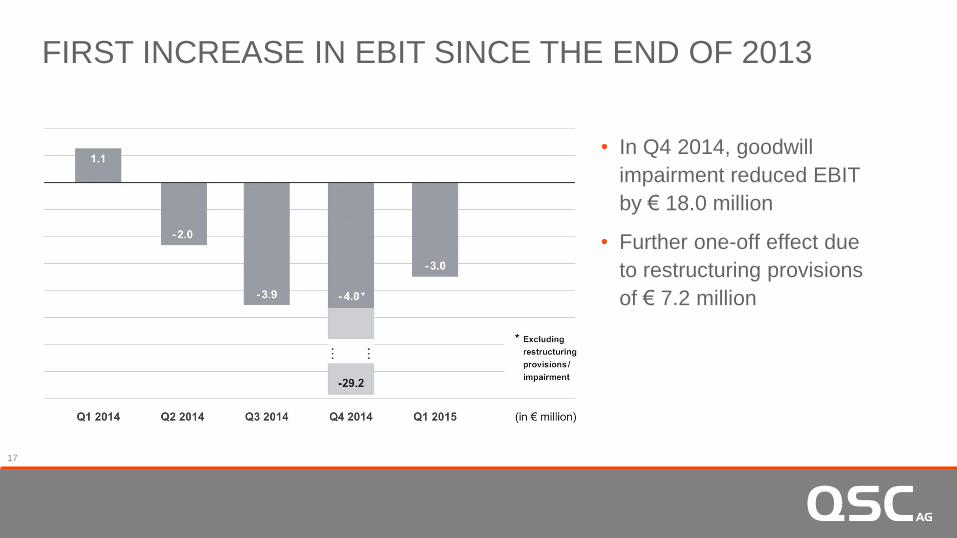

FIRST INCREASE IN EBIT SINCE THE END OF 2013

• In Q4 2014, goodwill

impairment reduced EBIT

by € 18.0 million

• Further one-off effect due

to restructuring provisions

of € 7.2 million

LOWER LEVEL OF CAPEX

18

• 70% of CAPEX in Q1 2015

were customer-driven

• Low investments in infrastructure

• Shift from CAPEX to OPEX of

development activities

SOLID BALANCE SHEET

19

• Financing matches maturity:

Long-term liabilities and equity

cover 130% of long-term assets

• Strong cash position of € 80.5 million

QSC AIMS TO INCREASE EBITDA AND FREE CASH FLOW

20

• Effects of the cost-cutting

programme will be seen from

H2 2015 onwards

• Financial strength will be

supported by CAPEX reduction

to € 25 million

21

AGENDA

1. Strategic Update

2. Financial Update and Outlook 2015

3. Questions & Answers

22

QSC AG

Arne Thull

Head of Investor Relations

Mathias-Brüggen-Strasse 55

50829 Cologne

twitter.com/QSCIRde

twitter.com/QSCIRen

blog.qsc.de

xing.com/companies/QSCAG

slideshare.net/QSCAG

paulrobertloyd.com/2009/06/social_media_icons

Phone +49-221-669-8724

Fax +49-221-669-8009

E-mail [email protected]

Web www.qsc.de

CONTACT

23

SAFE HARBOR STATEMENT

This presentation includes forward-looking statements as such term is defined in the U.S. Private Securities

Litigation Act of 1995. These forward-looking statements are based on management’s current expectations and

projections of future events and are subject to risks and uncertainties. Many factors could cause actual results to

vary materially from future results expressed or implied by such forward-looking statements, including, but not

limited to, changes in the competitive environment, changes in the rate of development and expansion of the

technical capabilities of DSL technology, changes in prices of DSL technology and market share of our competitors,

changes in the rate of development and expansion of alternative broadband technologies and changes in prices of

such alternative broadband technologies, changes in government regulation, legal precedents or court decisions

relating, among other things, to line sharing, rent for co-location and unbundled local loops, the pricing and timely

availability of leased lines, and other matters that might have an effect on our business, the timely development of

value-added services, our ability to maintain and expand current marketing and distribution agreements and enter

into new marketing and distribution agreements, our ability to receive additional financing if management planning

targets are not met, the timely and complete payment of outstanding receivables from our distribution partners and

resellers of QSC services and products, as well as the availability of sufficiently qualified employees.

A complete list of the risks, uncertainties and other factors facing us can be found in our public reports and filings

with the U.S. Securities and Exchange Commission.

24

DISCLAIMER • This document has been produced by QSC AG (the “Company”) and is furnished to you

solely for your information and may not be reproduced or redistributed, in whole or in part,

to any other person

• No representation or warranty (express or implied) is made as to, and no reliance should be

placed on, the fairness, accuracy or completeness of the information contained herein and,

accordingly, none of the Company or any of its parent or subsidiary undertakings or any of

such person’s officers or employees accepts any liability whatsoever arising directly or

indirectly from the use of this document

• The information contained in this document does not constitute or form a part of, and should

not be construed as, an offer of securities for sale or invitation to subscribe for or purchase

any securities and neither this document nor any information contained herein shall form the

basis of, or be relied on in connection with, any offer of securities for sale or commitment

whatsoever