www.quantifsolutions.com Authored by David Kelly (Quantif) • Key data and technology challenges • Current trends and best practices WHITE PAPER CHALLENGES IN IMPLEMENTING A COUNTERPARTY RISK MANAGEMENT PROCESS

Transcript

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

Challenges in Implementing aCounterparty Risk Management Process

Introduction

Most banks are in the process o setting up counterparty risk management processes or improving

existing ones. Unlike market risk, which can be eectively managed by individual trading desks or traders,

counterparty risk is increasingly being priced and managed by a central CVA desk or risk control group since

the exposure tends to span multiple asset classes and business lines. Moreover, aggregated counterparty

exposure may be signicantly impacted by collateral and cross-product netting agreements.

Gathering transaction and market data rom potentially many trading systems, along with legal agreements

and other reerence data, involves signicant and oten underestimated data management issues.The ability to calculate credit value adjustments (CVA) and exposure metrics on the entire portolio,

incorporating all relevant risk actors, adds substantial analytical and technological challenges. Furthermore,

traders and salespeople expect near real-time perormance o incremental CVA pricing o new transactions.

Internal counterparty risk management must also be integrated with regulatory processes.

In short, the data, technological, and operational challenges involved in implementing a counterparty

risk management process can be overwhelming. This paper outlines the key challenges, starting with an

overview o the main business objectives, ollowed by a discussion o data and technology issues, and

current trends in best practices.

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

The objectives in setting up a counterparty risk management process can be split into three categories – CVA

pricing, exposure management, and regulatory requirements. The ollowing is a summary o the objectives to

provide context or the data and technology discussions.

CVA Pricing

CVA is the amount banks charge their counterparties to compensate or the expected loss rom deault. Since

both counterparties can deault, the net charge should theoretically be the bilateral CVA, which includes a debt

value adjustment (DVA) or gain rom the bank’s own deault. CVA pricing can be split into the inter-bank and

corporate customer markets. New legislation, including the Dodd-Frank Bill in the U.S. and the European Market

Inrastructure Regulations (EMIR), along with Basel III, are mandating or incentivising clearing and increased use

o collateral over CVA as the principal means or managing counterparty risk in the inter-bank market.

Uncollateralised exposure is more prevalent in the corporate derivatives market and banks compete

aggressively on CVA pricing. CVA pricing is inherently complex or two reasons. First, the incremental (ormarginal) CVA or each trade should refect the application o collateral and netting agreements across all

transactions with that counterparty. Second, CVA pricing models not only need to incorporate all o the

risk actors o the underlying instrument, but also the counterparty’s ‘option’ to deault and the correlation

between the deault probability and the exposure, i.e., right- or wrong-way risk.

Given the complexity, two problems arise. Some banks are not able to compete or lucrative corporate

derivatives transactions because they do not take ull advantage o collateral and netting agreements with their

counterparties in calculating CVA. Or, they win transactions because their models under-price some o the risks

and subject the bank to losses. The complexity is compounded by the need or derivatives salespeople to make

an executable price in near real-time.

Risk Management

While CVA covers the expected loss rom counterparty deaults, there is also the risk o unexpected losses,

as well as mark-to-market gains and losses on the CVA. These risks are managed through a combination

o exposure limits, reserves and replication or hedging. Unexpected losses are calculated by simulating

exposures through time, taking into account netting and collateral agreements, and using the potential

uture exposure (PFE) prole at a specied percentile, e.g. 99%, and the counterparty’s deault probability to

calculate the unexpected loss or economic capital (EC), net o CVA.

Many banks strictly rely on reserves and exposure limits to manage these risks but the trend is towards

more active management. Hedging CVA has become increasingly important to oset signicantly higher

regulatory capital requirements and to reduce the impact o CVA volatility on the bank’s earnings. The mainproblem is that some o the risks can’t be eectively hedged. For example, there may be limited or no

liquid CDS reerencing some o the counterparties and there are complex correlation and second-order risks

that can be dicult to quantiy and hedge. The diculties are amplied by the computational constraints in

running Monte Carlo simulations on the entire portolio or each perturbed input.

Regulatory Requirements

Subject to approval, the Internal Model Method (IMM) specied in the Basel accord allows banks to use their

own models to calculate regulatory capital. The counterparty deault risk charge is calculated using current

market data, either implied or calibrated rom historical data. Banks using market-implied or risk-neutral

calibrations, appropriate or hedging, must also run the simulations with historical calibrations. Three-yearso historical data are required, including a period o stress to counterparty credit spreads. The data must be

updated quarterly or more requently i warranted by market conditions. The counterparty deault risk charge

is the greater o the charge based on current market data and the charge based on the stress calibration.

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

Basel III introduces a CVA risk capital charge, as CVA losses were greater than unexpected losses in many

cases during the recent crisis. The charge is the sum o the non-stressed and stressed CVA VaR, based

on changes in credit spreads over a three-year period. For the stressed CVA VaR, the three-year period

includes a one-year period o stress to counterparty credit spreads. Banks need not include securities

nancing transactions (SFTs) in the CVA risk capital charge unless the risk is deemed material. Cleared

transactions are also omitted. However, eligible credit hedges should be included in all calculations. The

total regulatory capital charge or counterparty risk is the sum o the counterparty deault risk charge and

CVA risk capital charge.

Regulatory approval is contingent on model validation. Back-testing o representative portolios over several

historical dates covering a wide range o market conditions is the primary mechanism or validating the

capital model. Back-testing involves comparing exposure projections with realised exposures or selected

time buckets, e.g., one year. Banks must also perorm stress tests on the principal market risk actors to

identiy general wrong-way risks, concentrations o risks among industries or regions, and large directional,

basis and curve risks. Reverse stress testing to identiy plausible loss scenarios may also be required.

Summary

The key objectives o the counterparty risk management process can be summarised as ollows:

• Central storage o counterparty legal entity structures, including a history o corporate actionsand credit events

• Central storage o collateral & netting legal agreements by counterparty

• Ability to load all OTC derivatives and other counterparty transactions rom various booking systems

• Collateral position management and integration with counterparty risk calculations

• Market data required to value counterparty transactions, plus market-implied and historicalvolatilities and correlations or generating exposure distributions, and deault probabilities orcalculating CVA, DVA and economic capital

• Near-time incremental CVA pricing o new trades, refecting collateral & netting agreements

• CVA pricing models that incorporate all dimensions o risk, including right- and wrong-way risk

• Expected exposure (EE) and potential uture exposure (PFE) proles or counterparty limitmonitoring on a daily basis

• CVA, DVA and economic capital calculations or expected and unexpected loss management

• CVA sensitivities across all risk actors or actively managing counterparty risk

• Credit hedges refected in exposure and loss metrics, and market hedges refected in CVA sensitivities

• Regulatory counterparty risk capital calculation using market-implied and historical calibrations,including a stress calibration

• Historical CVA VaR using the recent three-year period and a stress period

• Back-testing o representative portolios over multiple time periods to validate exposure projection model

• Stress testing to identiy wrong-way risks and concentrations

• Reporting o all counterparty risk metrics minimally by counterparty, industry, and region with

diagnostic drill-down capabilities

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

The counterparty risk management objectives and corresponding data requirements summarised in the

previous two sections translate into a very challenging technology agenda. Data management is certainly

a top priority, as well as robust CVA pricing and risk analytics. Centralising counterparty risk managementor the entire trading book places a high priority on scalability, while providing near-time perormance

or marginal pricing o new trades. Given the large amount o inormation, a congurable reporting

environment is a necessity. For regulatory approval, the inrastructure must also support back-testing,

stress testing and VaR. Each o these issues is addressed below.

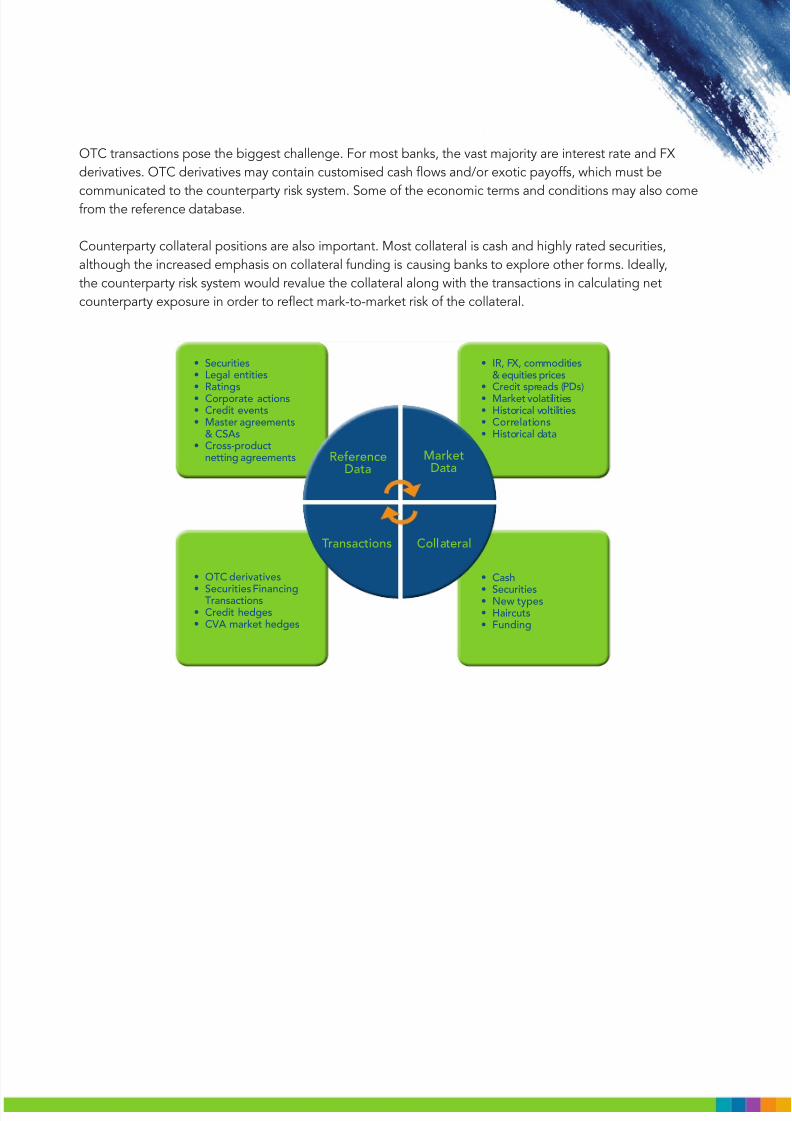

Data Management

Most banks have multiple systems or reerence data, market data, and transactions, which may be dierent

or each business unit. These systems may be urther sub-divided into ront-oce analytical tools and back-

oce booking systems, each with its own repository o reerence data. There may also be several internal and

external sources or market data. The counterparty risk system must integrate with potentially many o these

systems in order to extract the data needed to produce a comprehensive set o counterparty risk metrics.

Systems integration presents several technical challenges. Source systems may be built with a variety o

technologies, such as C++, Java, and .NET, which means the counterparty risk system may have to ‘speak’

many languages. Some systems may have well-developed interaces and APIs while others may not, which not

only adds to the cost o development but also increases the ailure rate in terms o missing or erroneous data.

Related issues include symbology mapping and data conversion. Source systems may use their own

symbols to identiy securities and other parameters, such as holiday codes and reerence indices. Use o

industry standard ticker symbols lessens the problem but invariably, the counterparty risk system must be

able to interpret a variety o naming conventions. Source systems also store data in proprietary ormats.While loading the data, the counterparty risk system must convert it into its own ormat. Expanded use

o open XML ormats, such as FIXML and FpML, as more products become standardised or clearing, is a

positive development.

Once the systems have been connected and data translations in place, the counterparty risk system must

receive incremental updates rom the upstream systems. Daily updates are sucient or most purposes but

incremental CVA pricing depends on up to date position and market data.

Analytics

Analytical components can be categorised into pricing models, the simulation engine, and market data

calibrators. Most institutions have their own proprietary libraries o pricing models or ront-oce pricing and

hedging. Ideally, the bank would use the same pricing models or counterparty risk to ensure consistency.

Market data calibrators provide the market-implied and historical volatilities and correlations as inputs to the

simulation engine.

The simulation engine uses pricing models in generating the exposure distribution over a specied set o

uture dates. The rst step is to simulate market scenarios using a risk neutral or historical calibration. The next

step is to value each transaction over all scenarios and time steps to create the exposure distribution. The

exposures are aggregated by counterparty ‘netting set’, according to legal netting agreements. Collateral

terms are then applied to determine uncollateralised exposure by netting set.

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

In applying collateral thresholds, the ‘margin period o risk’ and collateral mark-to-market risk must be

considered. EE, PFE and various Basel metrics including expected positive exposure (EPE) can be directly

calculated rom the exposure distribution. The nal step is to ‘integrate’ the exposure distribution to calculateCVA, DVA and economic capital. Incorporating right- and wrong-way risk into these calculations is important,

especially or credit derivative transactions, and non-trivial to implement.

Several analytical issues arise in perorming the above steps. First and oremost, pricing models must be

able to perorm orward valuations or the simulated market scenarios. Early termination or mutual ‘put’

eatures should be refected. For path-dependent and other exotic payos, the simulation engine should

provide sucient path-level inormation to the pricing model to prevent valuation inconsistencies (and

perormance bottlenecks) rom having to run simulations within the simulation.

In order or pricing models to re-use market scenarios or paths, the simulation engine should use risk neutral

calibrations o the various risk actors. For example, i pricing models use a Libor market model, e.g., BGM,to price interest rate derivatives, the simulation engine should use the same model, which means calibrating

orward rates, volatities and correlations rom current market data. This calibration can also be used to

calculate CVA sensitivities or hedging purposes. The simulation engine must also support calibrations

based on historical data to calculate the various metrics required by Basel.

Perormance & Scalability

For a large bank, the counterparty risk system may price something on the order o one million transactions

over one thousand scenarios and one hundred time steps, or 100 billion valuations. I the bank actively

hedges CVA, the number o valuations is roughly multiplied that by the number o sensitivities required.

Pricing models must be as ecient as possible in order to generate counterparty risk metrics on a dailybasis. Since banks preer to use their own pricing models or consistency, additional tuning or substitution

o less sophisticated models or valuation o complex products, at the expense o some accuracy, may be

necessary. Another approach is to use pre-calculated pricing grids to reduce the number o valuations.

Scalability can also be addressed through parallel processing. Distributing computations across servers and

processor cores using grid technology and multi-threading should allow acceptable levels o perormance

to be achieved by adding hardware resources. O course, complexity and potential or ailure increases with

the amount o hardware.

Re-running simulations on the entire portolio to determine the impact (marginal price) o a new transaction

is not practical or intra-day pricing. The typical solution involves saving valuations at the netting set level or

each scenario and time step in the database. Marginal pricing is then reduced to simulating the new trade

along the same scenarios and time steps and aggregating with the saved netting set valuations, re-applying

netting and collateral agreements. O course, adjustments or re-simulation may be necessary or changes in

portolio composition or signicant market moves.

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

With the huge amount o data involved and analytical complexity, the ability to view the various counterparty

risk metrics across a variety o dimensions is absolutely essential. At the very least, the system should show

CE, EE, PFE, CVA, DVA and economic capital by counterparty, industry and region. The system should also

display EE and PFE proles along specied uture time buckets out to the maximum maturity date. The abilityto inspect reerence, market and transaction data inputs is vital in veriying calculated results and tracking

down errors. The system must also provide reports or back-testing, stress testing and VaR outputs with similar

aggregation and drill-down capabilities.

Back-testing,StressTesting&VaR

The counterparty risk system’s inrastructure must provide back-testing, stress testing and ull-reval historical

VaR. For back-testing, the system should record all data necessary to simulate exposures or representative

portolios over multiple historical dates. Stess testing unctionality should support conguration o a set o shits

to any or all o the current market data used to value the portolio. Flexibility to ‘steepen’ or ‘fatten’ curves

must be provided, as well as shiting basis spreads. VaR is similar to stress testing in that it involves a set o shits. The shits are derived rom a time series o historical market data, typically daily. In some institutions,

the market risk group provides a set o shit ‘les’ that the risk system should load to run VaR and stress tests.

•Simulation engine•Risk-neutral & historical

calibrations• Netting & collateral•

Right/wrong-way risk• Exotic payos

•Large cross-assetportolios

•Pricing modelperormance

•Near-time CVA pricing•

CVA sensitivities• Daily and intra-daymetrics

•CE, EE, PFE, CVA, ECby counterparty,industry & region

•EE & PFE prolesover time

•Data inspection &

drill-downs•Back-testing, stress

testing, VaR outputs

•Back-test exposureprojections vs.Realizations

•Curve steepening& fattening stress

scenarios•Stress basis spreads•Full reval historical VaR

•Multiple data sources•Systems integration•Symbology mapping•Data ormat

conversions•Incremental updates

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process

Post crisis, the ability or senior management to get a comprehensive view o the bank’s counterparty risks

is a critical priority. Consolidated risk reporting has been elusive due to ront-oce driven business models.

As infuential revenue producers, trading desks have maintained a tight grip on data ownership, modeldevelopment and ront-oce technology. This has resulted in a prolieration o systems, making the job o

aggregating risks across business lines excessively complicated. Continuous development o new types o

derivative payos and structured products has exacerbated the problem. But the ailures and near ailures o

several global banks have changed the traditional mentality. Banks are now taking a ‘top-down’ approach to

risk management. Decision-making authority is transitioning rom the ront-oce to central market and credit

risk management groups. This authority includes tighter controls on data and technology.

A key component o the top-down approach to risk management is the central CVA desk or counterparty

risk group. This group is responsible or marginal CVA pricing o new trades originated by the individual

business units and then managing the resultant credit risk. In practice, the CVA desk sells credit protection

to the originating trading desk, insuring them against losses in the event o a counterparty deault. Thereare several advantages to this approach. Housing counterparty risk in one place allows senior management

to get a consolidated picture o the exposures and proactively address risk concentrations and other

issues. It also addresses the competitive CVA pricing issues described in a previous section. As banks

continue to ramp up active management o CVA, having a specialised group allows careul management o

complex risks arising rom liquidity, correlation and analytical limitations.

The reasons or not creating a central CVA desk or counterparty risk group tend to be practical issues

particular to the institution. Decentralised inrastructures may make the data and technology challenges

too great to ensure provision o meaningul consolidated counterparty risk metrics on a timely basis. Some

banks have aligned counterparty risk management by business line in order to more eectively manage

the data and analytical issues at the expense o certain benets, like netting. For centralised CVA desks,

there is also the challenge o internal pricing and P&L policies. Most banks position CVA desks as utility

unctions that simply attempt to recover hedging costs in CVA pricing.

Recent regulatory activity has also had a proound impact on counterparty risk management, mostly due

to central clearing requirements and higher capital ratios. Mandating central clearing or an expanding

scope o derivative products eectively moves counterparty risk out o complex CVA and economic capital

models and into more deterministic and transparent margining ormulas. The heavily collateralised inter-

dealer market is also undergoing signicant changes due to the widening o Libor basis spreads during the

crisis. A new standard or pricing collateralised trades is emerging, based on OIS discounting. Institutions

are now looking more closely at optimising collateral unding through cheapest-to-deliver collateral, re-couponing existing trades to release collateral, and moving positions to central counterparties in order to

access valuation discrepancies or more avorable collateral terms.

It is expected that most corporate derivatives transactions will remain exempt rom clearing mandates since

banks provide valuable hedging services in the orm o derivative lines. The cost o extending these lines is

increasing due to signicantly higher regulatory capital requirements. Thereore, competitive CVA pricing and

economic capital optimisation will remain priorities or corporate counterparty risk management alongside

collateral and clearing processes.

8/7/2019 Quantifi Whitepaper - Challenges in Implementing a Counter Party Risk Management Process