Page 1

Asymptotic Normality of Quantile Estimator

Quantile Regressions: Estimations, Asymptotic

Normality and Hypothesis Testing

MEI-YUAN CHEN

Department of Finance

National Chung Hsing University

August 13, 2016

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 1 / 86

Page 2

Asymptotic Normality of Quantile Estimator

Scope of Quantile Regressions

1 Cross-sectional Data:

1 Quantile regressions: wage equation

2 Censored quantile regressions

2 Time-Series Data:

1 Qauntile regressions for non-causality test

2 Quantile regressions with breaks

3 Quantile autoregression

4 Quantile ARCH and GARCH

5 Quantile unit root and cointegration

3 Panel Data:

1 Panel quantile regressions

2 Panel censored quantile regressionsM.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 2 / 86

Page 3

Asymptotic Normality of Quantile Estimator

Why Quantile?

A univariate random variable Y is defined as

Y : Ω → y1, y2, . . . = DY (µY , var(Y ), α3(Y ), α4(Y )).

The distribution of realizations is demonstrated by measures E(Y )

(unconditional mean), var(Y ) (unconditional variance), α3(Y )

(unconditional skewness), α4(Y ) (unconditional kurtosis). Of course,

the distribution of all realizations can be captured by the cumulative

distribution function FY and the probability density function fY if FYis globally differentiable.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 3 / 86

Page 4

Asymptotic Normality of Quantile Estimator

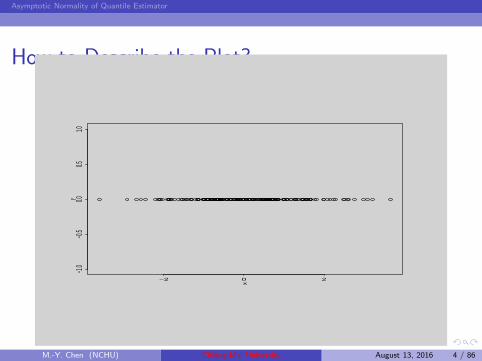

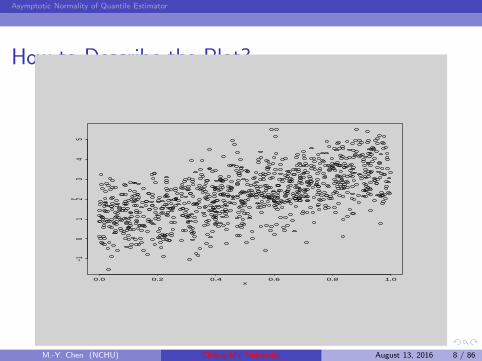

How to Describe the Plot?

−2 0 2

−1.0

−0.5

0.00.5

1.0

x

y

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 4 / 86

Page 5

Asymptotic Normality of Quantile Estimator

Bivariate random variables X and Y are defined as

(X,Y ) : Ω → (x1, y1), (x2, y2), (x3, y3), . . .= DX,Y (µX , σ

2X , α3(X), α4(X), µY , σ

2Y , α3(Y ), α4(Y ), cov(X,Y )).

That is, the plot (distribution) of realizations (x, y) can be

demonstrated by measures µX , σ2X , α3(X), α4(X) for X ,

µY , σ2Y , α3(Y ), α4(Y ) for Y , and cov(X, Y ) for the covariance

between X and Y .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 5 / 86

Page 6

Asymptotic Normality of Quantile Estimator

The conditional random variable Y on X = x is defined as

(Y |X = x) : Ω → (x, y1), (x, y2), . . .= DY |X=x(E(Y |X = x), var(Y |X = x), α3(Y |X = x), α4(Y |X = x))

The distribution of realizations is demonstrated by measures

E(Y |X = x) (conditional mean), var(Y |X = x) (conditional

variance), α3(Y |X = x) (conditional skewness), α4(Y |X = x)

(conditional kurtosis). Similarly, the distribution of all realizations can

be captured by the cumulative distribution function FY |X=x and the

probability density function fY |X=x if FY |X=x is globally differentiable.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 6 / 86

Page 7

Asymptotic Normality of Quantile Estimator

Purpose of Exploring the Conditional Distribution

To answer whether DY |X=x = DY , i.e.,

H0 : DY |X=x = DY , ∀x ∈ R. If the answer is NOT, the

information about X is valuable to understand the disytribution

of Y .

H0 : E(Y |X = x) = E(Y ), ∀x ∈ R;

H0 : var(Y |X = x) = var(Y ), ∀x ∈ R;

H0 : α3(Y |X = x) = α3(Y ), ∀x ∈ R;

H0 : α4(Y |X = x) = α4(Y ), ∀x ∈ R;

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 7 / 86

Page 8

Asymptotic Normality of Quantile Estimator

How to Describe the Plot?

0.0 0.2 0.4 0.6 0.8 1.0

−10

12

34

5

x

y

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 8 / 86

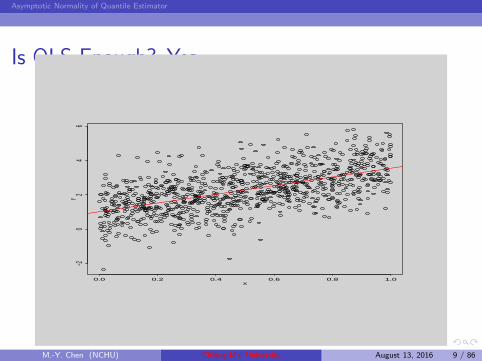

Page 9

Asymptotic Normality of Quantile Estimator

Is OLS Enough? Yes

0.0 0.2 0.4 0.6 0.8 1.0

−20

24

6

x

y

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 9 / 86

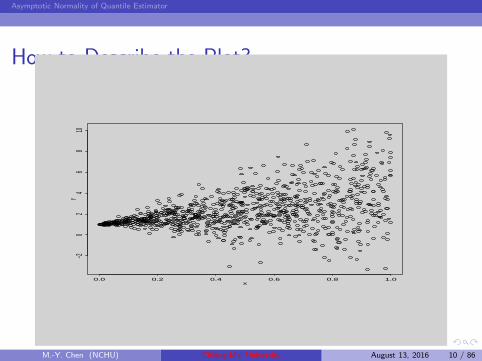

Page 10

Asymptotic Normality of Quantile Estimator

How to Describe the Plot?

0.0 0.2 0.4 0.6 0.8 1.0

−20

24

68

10

x

y

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 10 / 86

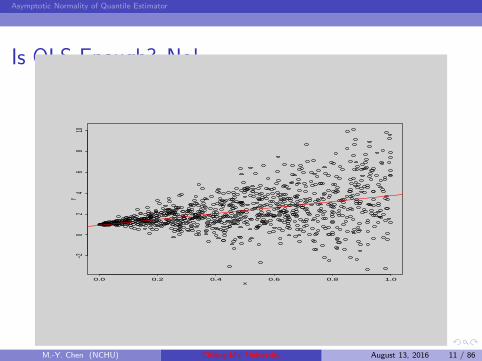

Page 11

Asymptotic Normality of Quantile Estimator

Is OLS Enough? No!

0.0 0.2 0.4 0.6 0.8 1.0

−20

24

68

10

x

y

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 11 / 86

Page 12

Asymptotic Normality of Quantile Estimator

Let Y denote the today’s stock return and X = 1 for having positive

and X = 0 for negative yesterday’s return. Then DY |X=x = DY

implies that knowing previous day’s return is positive or negative has

no help for understanding the distribution of today’s stock return. In

contrast, DY |X=x 6= DY indicates that knowing yesterday’s return is

positive or negative is useful to understanding the distribution of

today’s return. The information of X = 1 or X = 0 is valuable to

understand the distribution of today’s stock return. In other words,

checking DY |X=x = DY or not is equivalent to study whether the

information X is valuable or not.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 12 / 86

Page 13

Asymptotic Normality of Quantile Estimator

Best PredictorAs the mean E(Y ) is the best predictor of a random variable Y in

the sense that

E(Y ) = arg minm∈R

E[(Y −m)2] = arg minm∈R

var[(Y −m)].

Thus, all realizations of random variable Y can be decomposed based

on mean as

Y = µY + ǫY−µY

= µY + σY ǫY −µYσY

= µY + σY ǫ.

That is,

Y − µYσY

= ǫ.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 13 / 86

Page 14

Asymptotic Normality of Quantile Estimator

Obviously, for the realization equal to E(Y ), we have

E(Y )− µYσY

= E(ǫ) = 0,

and for the realization equal to the τ th quantile, Qτ (Y ), we have

Qτ (Y )− µYσY

= Qτ (ǫ).

Thus, the τ th quantile of Y , Qτ (Y ), is equal to F−1Y (τ) and can also

be represented as

Qτ (Y ) = µY + σY F−1ǫ (τ).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 14 / 86

Page 15

Asymptotic Normality of Quantile Estimator

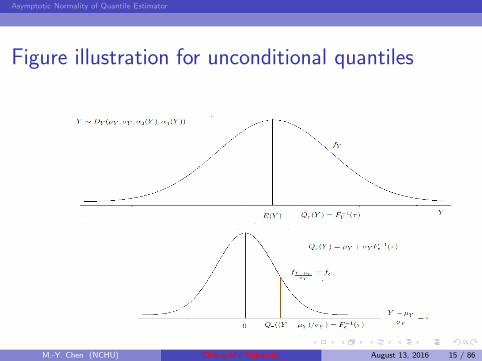

Figure illustration for unconditional quantiles

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 15 / 86

Page 16

Asymptotic Normality of Quantile Estimator

With no doubt that all realizations of random variable Y can also be

decomposed based on any location measure, say the first quartertile,

Q0.25(Y ), as

Y = Q0.25(Y ) + ǫ0.25

or say the third quartertile Q0.75(Y ), as

Y = Q0.75(Y ) + ǫ0.75

In general, the decomposition based on the τ th quantile can be

represented as

Y = Qτ (Y ) + ǫτ

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 16 / 86

Page 17

Asymptotic Normality of Quantile Estimator

Conditional Mean DecompositionSimilarly, the conditional mean E(Y |X = x) is the best predictor of the

conditional random variable (Y |X = x), i.e.,

E(Y |X = x) = arg minm∈R

E[((Y |X = x) −m)2] = arg minm∈R

var[(Y |X = x)−m].

Thus, all realizations of random variable Y conditional on X = x can be

decomposed as

(Y |X = x) = µ(Y |X=x) + ǫ(Y |X=x)−µ(Y |X=x)

= µ(Y |X=x) + σ(Y |X=x)ǫ (Y |X=x)−µ(Y |X=x)σ(Y |X=x)

= µ(Y |X=x) + σ(Y |X=x)ǫ.

That is,

(Y |X = x)− µ(Y |X=x)

σ(Y |X=x)= ǫ.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 17 / 86

Page 18

Asymptotic Normality of Quantile Estimator

Obviously, for the realization equal to E(Y |X = x), we have

E(Y |X = x)− µ(Y |X=x)

σ(Y |X=x)= E(ǫ) = 0,

and for the realization equal to the τth quantile, Qτ (Y |X = x), we have

Qτ (Y |X = x)− µ(Y |X=x)

σ(Y |X=x)= Qτ (ǫ).

The τth quantile of Y |X = x, Qτ (Y |X = x), is equal to F−1(Y |X=x)(τ) and can

also be represented as

Qτ (Y |X = x) = µ(Y |X=x) + σ(Y |X=x)F−1ǫ (τ). (1)

Similarly, the realizations of (Y |X = x) can be decomposed based on the

conditional τth quantile, Qτ (Y |X = x), as

(Y |X = x) = Qτ (Y |X = x) + ǫτ .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 18 / 86

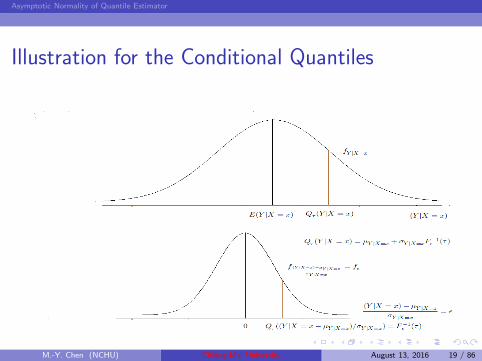

Page 19

Asymptotic Normality of Quantile Estimator

Illustration for the Conditional Quantiles

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 19 / 86

Page 20

Asymptotic Normality of Quantile Estimator

Extend the dimension of X and k-dimension and replace the notation with X.

Taking E(Y |X = x) = x′β0 and σ(Y |X=x) = x′γ0, we have

Qτ (Y |X = x) = µ(Y |X=x) + σ(Y |X=x)F−1ǫ (τ)

= x′β0 + x′γ0F−1ǫ (τ).

Then, the decomposition of realization of Y on X = x can be represented as

(Y |X = x) = x′β0 + x′γ0F−1ǫ (τ) + ǫτ

= x′[β0 + γ0 × F−1ǫ (τ)] + ǫτ

= x′βτ + ǫτ . (2)

Since x′β0 and x′γ0 represented the location and scale of the conditional random

variable (Y |X = x), (2) is called the location-scale quantile regression model.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 20 / 86

Page 21

Asymptotic Normality of Quantile Estimator

As σ(Y |X=x) = x′γ0 and let x = (1, z′)′ and γ = (γ0,γ′1)

′,

Qτ (Y |X = x) = x′β0 + x′γ0F−1ǫ (τ)

= x′β0 + (1, z′)(γ00,γ′01)

′F−1ǫ (τ)

= x′β0 + γ00F−1ǫ (τ) + z′γ01F

−1ǫ (τ).

location shift model: γ00 6= 0 and γ01 = 0;

location-scale shift model: γ00 6= 0 and γ01 6= 0.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 21 / 86

Page 22

Asymptotic Normality of Quantile Estimator

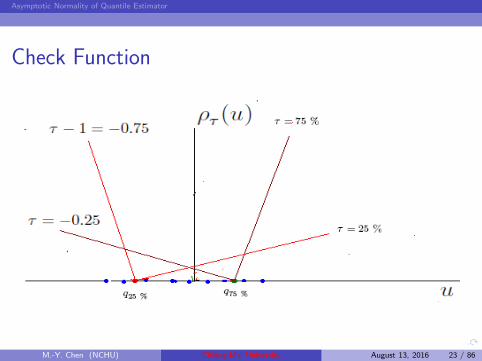

Population Quantiles

Definition 3.1: For any real valued random variable, Y, distributed

according to F (y) = Prob(Y ≤ y) , while for any 0 < τ < 1,

Qτ (Y ) = infy : F (y) ≥ τ

is called the τ th quantile of Y. The population quantile τ can also be

defined as

Qτ (Y ) = β = arg minβ∈R1

E[ρτ (yt − β)],

where ρτ (u) = u(τ − I(u < 0)) is called the check function by its

shape.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 22 / 86

Page 23

Asymptotic Normality of Quantile Estimator

Check Function

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 23 / 86

Page 24

Asymptotic Normality of Quantile Estimator

To show why β is equivalent to the τ th population quantile, observethat

E (ρτ (yt − β)) = τ

∫

y>β

(y − β)dF (y)− (1 − τ)

∫

y<β

(y − β)dF (y). (3)

Diffrentiating (3) with respect to β and by a variant of Liebniz’s

rule: Given V (r) =∫ B(r)

A(r)f(y, r)dy, the Liebniz’s rule is stated as

V ′(r) = f(B(r), r)∂B(r)

∂r− f(A(r), r)

∂A(r)

∂r+

∫ B(r)

A(r)

∂f(y, r)

∂rdy.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 24 / 86

Page 25

Asymptotic Normality of Quantile Estimator

By the Liebniz’s rule

∂

(

∫ g(x)

−∞

ψ(x, y)dy

)

/∂x =

∫ g(x)

−∞

∂ψ

∂xdy +

(

∂g

∂x

)

ψ(x, g(x)),

one gets, with g = β with y < β and ψ = y − β,

∂

(

∫ y<β

−∞

(y − β)dF (y)

)

/∂β =

∫ y<β

−∞

∂(y − β)

∂βdF (y) +

∂β

∂β(β − β)

= −∫ y<β

−∞

dF (y) + 0 = −F (y < β).

∂E (ρt(yt − β)) /∂β

= τ∂

(∫

y>β

(y − β)dF (y)

)

/∂β − (1− τ)∂

(∫

y<β

(y − β)dF (y)

)

/∂β

= τ [−F (y > β)]− (1− τ) [−F (y < β)]

= τ [−(1− F (y < β))] + (1− τ)F (y < β) = F (y < β)− τset= 0

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 25 / 86

Page 26

Asymptotic Normality of Quantile Estimator

Sample Quantiles

Given a sample y1, y2, . . . , yT, the sample counterpart ofE[ρτ (yt − β)] is T−1

∑Tt=1 ρτ (yt − β). Then, the sample τ th quantile

estimator is obtained by solving

Qτ(Y ) = βT = arg minβ∈R1

1

T

T∑

t=1

ρτ (yt − β)

= argminβ∈R

1

T

T∑

t=1

[τ − I(yt − β < 0)] (yt − β)

= minβ∈R

1

T

∑

t∈t:yt≥β

τ |yt − β|+∑

t∈t:yt<β

(1− τ)|yt − β|

.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 26 / 86

Page 27

Asymptotic Normality of Quantile Estimator

Regression Quantiles: Koenker and Bassett (1978)Consider the τ th conditional quantile of yt on xt as

Qτ (yt|xt) = x′

tβτ .

It is ready to see

τ =

∫ x′

tβτ

−∞

fy|x(s)ds

where fy|x(·) is the conditional density function of Y on X. Then,

the τ th conditional quantile regression model can be written as

yt = x′

tβτ + ut,τ

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 27 / 86

Page 28

Asymptotic Normality of Quantile Estimator

Quantile Regression vs Random Coefficient Model

Consider that there is a random coefficient model for yt as

yt = X ′tβ(Ut) + et

= β1(Ut) + β2(Ut)xt2 + · · ·+ βk(Ut)xtk + et,

where Ut ∼ i.i.d.U(0, 1) and βi(Ut), i = 1, . . . , k are assumed to be

comonotonic in Ut. Then

Qyt|xt(τ) = x′

tβτ .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 28 / 86

Page 29

Asymptotic Normality of Quantile Estimator

Comonotonicity

Two random variables (X,Y ) : Ω → R are comonotonic if there exists a third

random variable Z : Ω → R and increasing functions f and g such that

X = f(Z) and Y = g(Z).

1 If X and Y are comonotonic they have rank correlation one.

2 F−1X+Y (τ) = F−1

X (τ) + F−1Y (τ).

3 X and Y are driven by the same random (uniform) variable.

Besides, for any monotone increasing function g and standard uniform random

variable, U , we have Qg(U)(τ) = g[QU (τ)] = g(τ)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 29 / 86

Page 30

Asymptotic Normality of Quantile Estimator

Proof

Qyt|xt(τ) = Qβ1(Ut)+β2(Ut)xt2+···+βk(Ut)xtk

(τ)

= Qβ1(Ut)(τ) +Qβ2(Ut)xt2(τ) + · · ·+Qβk(Ut)xtk(τ)

= β1[QUt(τ)] + β2[QUt

(τ)]xt2 + · · ·+ βk[QUt(τ)]xtk

= β1(τ) + β2(τ)xt2 + · · ·+ βk(τ)xtk

= x′tβτ

This result holds for all τ ∈ (0, 1).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 30 / 86

Page 31

Asymptotic Normality of Quantile Estimator

The point estimators βτ of the linear quantile regression parameters,βτ , are obtained by solving

βτ = arg minβ∈Rp

1

T

T∑

t=1

ρτ (yt − x′

tβ)

= arg minβ∈Rp

1

T

T∑

t=1

[

τ − I(yt − x′

tβ < 0)]

(yt − x′

tβ)

= arg minβ∈Rp

1

T

∑

t∈t:yt≥x′tβ

τ |yt − x′

tβ|+∑

t∈t:yt<x′tβ

(1− τ)|yt − x′

tβ|

.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 31 / 86

Page 32

Asymptotic Normality of Quantile Estimator

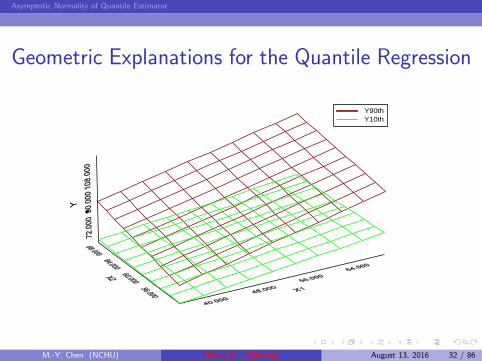

Geometric Explanations for the Quantile Regression

Y90thY10th

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 32 / 86

Page 33

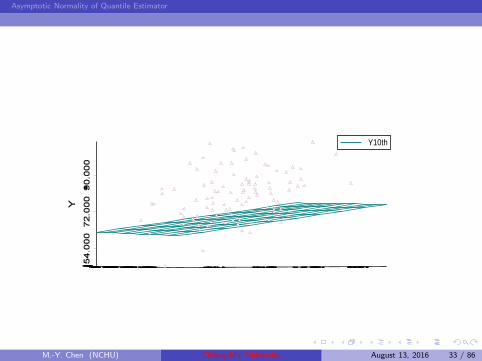

Asymptotic Normality of Quantile Estimator

Y10th

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 33 / 86

Page 34

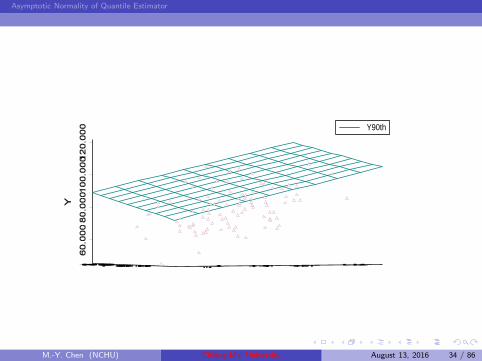

Asymptotic Normality of Quantile Estimator

Y90th

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 34 / 86

Page 35

Asymptotic Normality of Quantile Estimator

Characteristics of Regression Quantiles

Robustness

Equivariant Properties: ifβ∗(τ, y,X) ∈ B∗(τ, y,X), where

B∗(τ, y,X) is the set of regression quantiles,

β∗(τ, λy,X) = λβ∗(τ, y,X), λ ∈ [0,∞),

β∗(1− τ, λy,X) = λβ∗(τ, y,X), λ ∈ (−∞, 0],

β∗(τ, y +Xγ,X) = β∗(τ, y,X) + γ, γ ∈ Rp,

β∗(τ, y,XA) = A−1β∗(τ, y,X), AP×P nonsingular.

Capability of Exploring Conditional Distributions

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 35 / 86

Page 36

Asymptotic Normality of Quantile Estimator

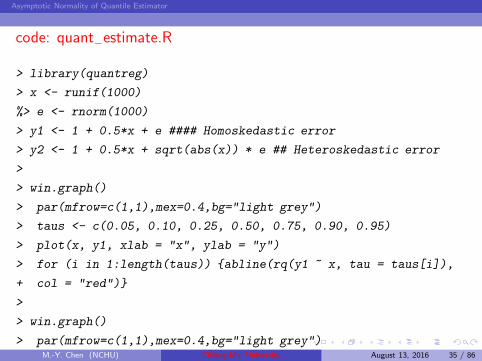

code: quant−estimate.R

> library(quantreg)

> x <- runif(1000)

%> e <- rnorm(1000)

> y1 <- 1 + 0.5*x + e #### Homoskedastic error

> y2 <- 1 + 0.5*x + sqrt(abs(x)) * e ## Heteroskedastic error

>

> win.graph()

> par(mfrow=c(1,1),mex=0.4,bg="light grey")

> taus <- c(0.05, 0.10, 0.25, 0.50, 0.75, 0.90, 0.95)

> plot(x, y1, xlab = "x", ylab = "y")

> for (i in 1:length(taus)) abline(rq(y1 ~ x, tau = taus[i]),

+ col = "red")

>

> win.graph()

> par(mfrow=c(1,1),mex=0.4,bg="light grey")M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 35 / 86

Page 37

Asymptotic Normality of Quantile Estimator

> plot(summary(rq(y1 ~ x,tau = 1:99/100)))

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 36 / 86

Page 38

Asymptotic Normality of Quantile Estimator

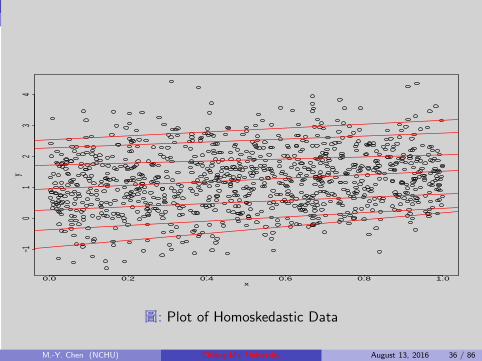

0.0 0.2 0.4 0.6 0.8 1.0

−10

12

34

x

y

圖: Plot of Homoskedastic Data

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 36 / 86

Page 39

Asymptotic Normality of Quantile Estimator

0.0 0.2 0.4 0.6 0.8 1.0

−2−1

01

23

4

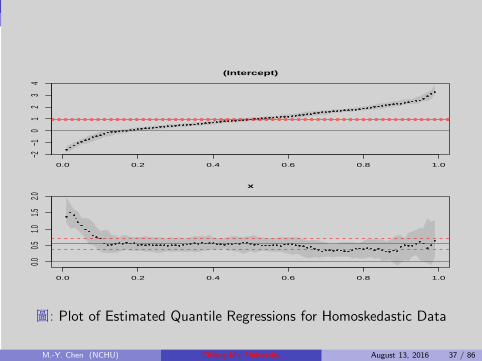

(Intercept)

0.0 0.2 0.4 0.6 0.8 1.0

0.00.5

1.01.5

2.0

x

圖: Plot of Estimated Quantile Regressions for Homoskedastic Data

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 37 / 86

Page 40

Asymptotic Normality of Quantile Estimator

> win.graph()

> par(mfrow=c(1,1),mex=0.4,bg="light grey")

> taus <- c(0.05, 0.10, 0.25, 0.50, 0.75, 0.90, 0.95)

> plot(x, y1, xlab = "x", ylab = "y")

> for (i in 1:length(taus)) abline(rq(y1 ~ x, tau = taus[i]),

+ col = "red")

>

> win.graph()

> par(mfrow=c(1,1),mex=0.4,bg="light grey")

> plot(summary(rq(y2 ~ x,tau = 1:99/100)))

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 38 / 86

Page 41

Asymptotic Normality of Quantile Estimator

0.0 0.2 0.4 0.6 0.8 1.0

−10

12

34

x

y

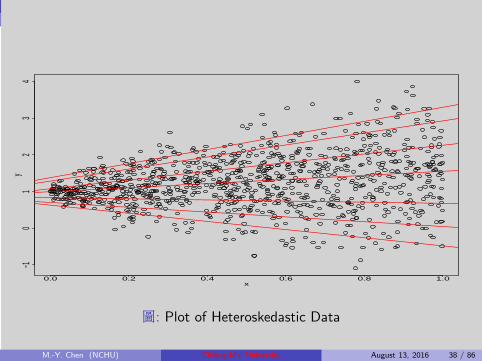

圖: Plot of Heteroskedastic Data

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 38 / 86

Page 42

Asymptotic Normality of Quantile Estimator

0.0 0.2 0.4 0.6 0.8 1.0

0.00.5

1.01.5

(Intercept)

0.0 0.2 0.4 0.6 0.8 1.0

−2−1

01

23

x

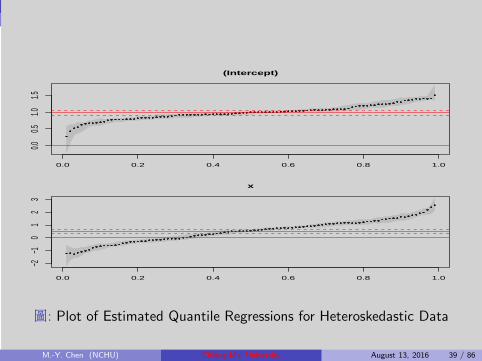

圖: Plot of Estimated Quantile Regressions for Heteroskedastic Data

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 39 / 86

Page 43

Asymptotic Normality of Quantile Estimator

Quantile Regression Estimation using quantreg

Estimation methods include:

method = ”br” : The default method is the modified version of

the Barrodale and Roberts algorithm for l1-regression;

method = ”fn” : Frisch-Newton interior point method;

method =“pfn” : the Frisch-Newton approach after

preprocessing;

method =“fnc”: enables the user to specify linear inequality

constraints on the fitted coefficients;

method =“lasso” : implement the lasso penalty and Fan and Li’s

smoothly clipped absolute deviation penalty;

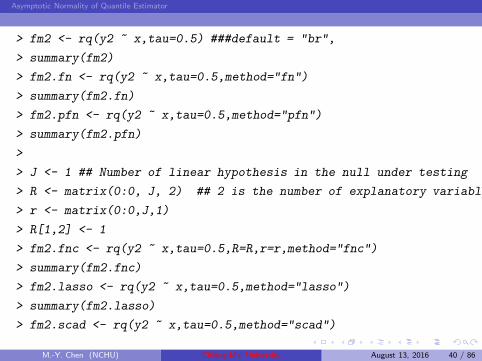

method =“scad” :M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 40 / 86

Page 44

Asymptotic Normality of Quantile Estimator

> fm2 <- rq(y2 ~ x,tau=0.5) ###default = "br",

> summary(fm2)

> fm2.fn <- rq(y2 ~ x,tau=0.5,method="fn")

> summary(fm2.fn)

> fm2.pfn <- rq(y2 ~ x,tau=0.5,method="pfn")

> summary(fm2.pfn)

>

> J <- 1 ## Number of linear hypothesis in the null under testing

> R <- matrix(0:0, J, 2) ## 2 is the number of explanatory variables,

> r <- matrix(0:0,J,1)

> R[1,2] <- 1

> fm2.fnc <- rq(y2 ~ x,tau=0.5,R=R,r=r,method="fnc")

> summary(fm2.fnc)

> fm2.lasso <- rq(y2 ~ x,tau=0.5,method="lasso")

> summary(fm2.lasso)

> fm2.scad <- rq(y2 ~ x,tau=0.5,method="scad")

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 40 / 86

Page 45

Asymptotic Normality of Quantile Estimator

> summary(fm2.scad)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 41 / 86

Page 46

Asymptotic Normality of Quantile Estimator

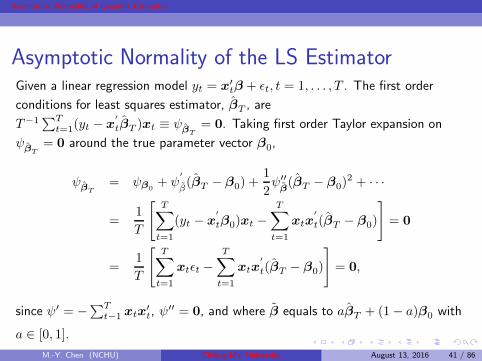

Asymptotic Normality of the LS EstimatorGiven a linear regression model yt = x′

tβ + ǫt, t = 1, . . . , T . The first order

conditions for least squares estimator, βT , are

T−1∑T

t=1(yt − x′

tβT )xt ≡ ψβT

= 0. Taking first order Taylor expansion on

ψβT

= 0 around the true parameter vector β0,

ψβT

= ψβ0+ ψ

′

β(βT − β0) +

1

2ψ′′β(βT − β0)

2 + · · ·

=1

T

[

T∑

t=1

(yt − x′

tβ0)xt −T∑

t=1

xtx′

t(βT − β0)

]

= 0

=1

T

[

T∑

t=1

xtǫt −T∑

t=1

xtx′

t(βT − β0)

]

= 0,

since ψ′ = −∑Tt−1 xtx

′t, ψ

′′ = 0, and where β equals to aβT + (1− a)β0 with

a ∈ [0, 1].

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 41 / 86

Page 47

Asymptotic Normality of Quantile Estimator

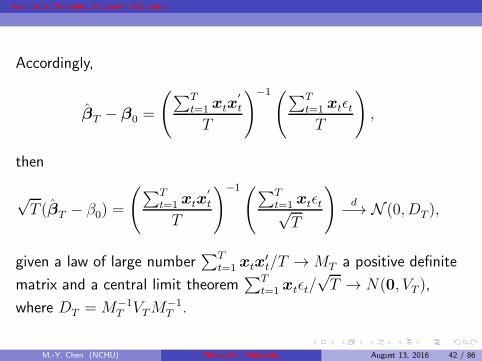

Accordingly,

βT − β0 =

(

∑Tt=1 xtx

′

t

T

)−1(∑T

t=1 xtǫtT

)

,

then

√T (βT − β0) =

(

∑Tt=1 xtx

′

t

T

)−1(∑T

t=1 xtǫt√T

)

d−→ N (0, DT ),

given a law of large number∑T

t=1 xtx′t/T →MT a positive definite

matrix and a central limit theorem∑T

t=1 xtǫt/√T → N(0, VT ),

where DT =M−1T VTM

−1T .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 42 / 86

Page 48

Asymptotic Normality of Quantile Estimator

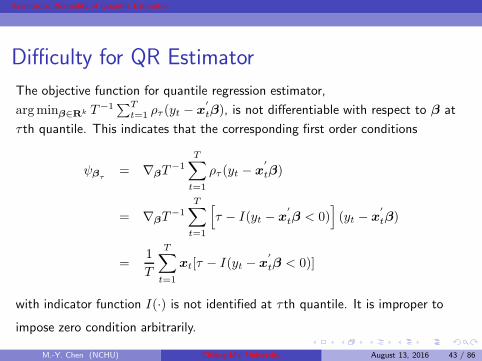

Difficulty for QR Estimator

The objective function for quantile regression estimator,

argminβ∈Rk T−1∑T

t=1 ρτ (yt − x′

tβ), is not differentiable with respect to β at

τth quantile. This indicates that the corresponding first order conditions

ψβτ= ∇βT

−1T∑

t=1

ρτ (yt − x′

tβ)

= ∇βT−1

T∑

t=1

[

τ − I(yt − x′

tβ < 0)]

(yt − x′

tβ)

=1

T

T∑

t=1

xt[τ − I(yt − x′

tβ < 0)]

with indicator function I(·) is not identified at τth quantile. It is improper to

impose zero condition arbitrarily.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 43 / 86

Page 49

Asymptotic Normality of Quantile Estimator

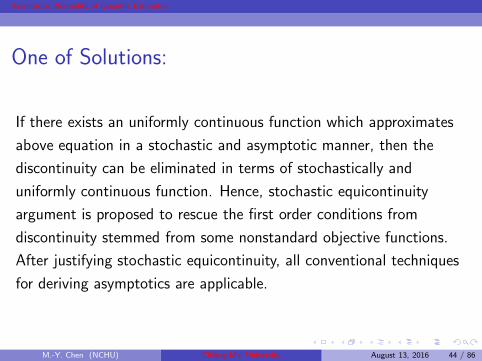

One of Solutions:

If there exists an uniformly continuous function which approximates

above equation in a stochastic and asymptotic manner, then the

discontinuity can be eliminated in terms of stochastically and

uniformly continuous function. Hence, stochastic equicontinuity

argument is proposed to rescue the first order conditions from

discontinuity stemmed from some nonstandard objective functions.

After justifying stochastic equicontinuity, all conventional techniques

for deriving asymptotics are applicable.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 44 / 86

Page 50

Asymptotic Normality of Quantile Estimator

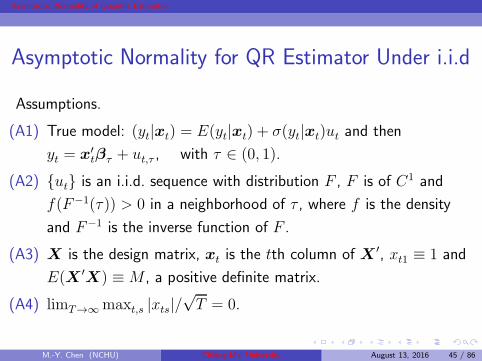

Asymptotic Normality for QR Estimator Under i.i.d

Assumptions.

(A1) True model: (yt|xt) = E(yt|xt) + σ(yt|xt)ut and then

yt = x′tβτ + ut,τ , with τ ∈ (0, 1).

(A2) ut is an i.i.d. sequence with distribution F , F is of C1 and

f(F−1(τ)) > 0 in a neighborhood of τ , where f is the density

and F−1 is the inverse function of F .

(A3) X is the design matrix, xt is the tth column of X ′, xt1 ≡ 1 and

E(X ′X) ≡M , a positive definite matrix.

(A4) limT→∞maxt,s |xts|/√T = 0.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 45 / 86

Page 51

Asymptotic Normality of Quantile Estimator

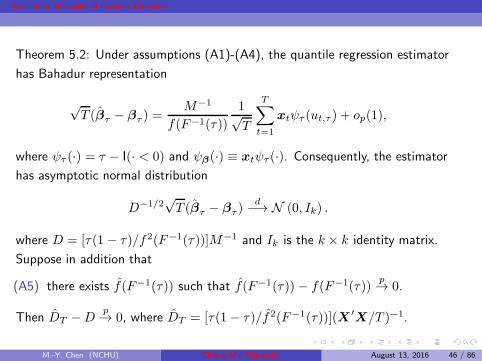

Theorem 5.2: Under assumptions (A1)-(A4), the quantile regression estimator

has Bahadur representation

√T (βτ − βτ ) =

M−1

f(F−1(τ))

1√T

T∑

t=1

xtψτ (ut,τ ) + op(1),

where ψτ (·) = τ − I(· < 0) and ψβ(·) ≡ xtψτ (·). Consequently, the estimator

has asymptotic normal distribution

D−1/2√T (βτ − βτ )

d−→ N (0, Ik) .

where D = [τ(1 − τ)/f2(F−1(τ))]M−1 and Ik is the k × k identity matrix.

Suppose in addition that

(A5) there exists f(F−1(τ)) such that f(F−1(τ)) − f(F−1(τ))p→ 0.

Then DT −Dp→ 0, where DT = [τ(1 − τ)/f2(F−1(τ))](X ′X/T )−1.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 46 / 86

Page 52

Asymptotic Normality of Quantile Estimator

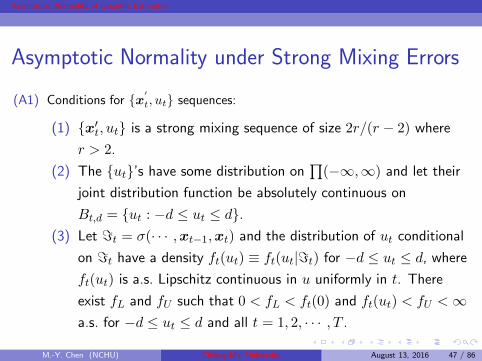

Asymptotic Normality under Strong Mixing Errors

(A1) Conditions for x′

t, ut sequences:

(1) x′t, ut is a strong mixing sequence of size 2r/(r − 2) where

r > 2.

(2) The ut’s have some distribution on∏

(−∞,∞) and let their

joint distribution function be absolutely continuous on

Bt,d = ut : −d ≤ ut ≤ d.(3) Let ℑt = σ(· · · ,xt−1,xt) and the distribution of ut conditional

on ℑt have a density ft(ut) ≡ ft(ut|ℑt) for −d ≤ ut ≤ d, where

ft(ut) is a.s. Lipschitz continuous in u uniformly in t. There

exist fL and fU such that 0 < fL < ft(0) and ft(ut) < fU <∞a.s. for −d ≤ ut ≤ d and all t = 1, 2, · · · , T .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 47 / 86

Page 53

Asymptotic Normality of Quantile Estimator

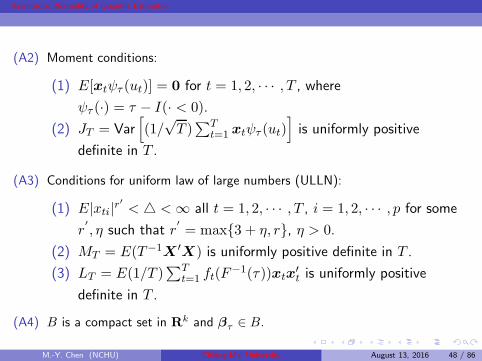

(A2) Moment conditions:

(1) E[xtψτ (ut)] = 0 for t = 1, 2, · · · , T , whereψτ (·) = τ − I(· < 0).

(2) JT = Var[

(1/√T )∑T

t=1 xtψτ (ut)]

is uniformly positive

definite in T .

(A3) Conditions for uniform law of large numbers (ULLN):

(1) E|xti|r′

< <∞ all t = 1, 2, · · · , T , i = 1, 2, · · · , p for some

r′

, η such that r′

= max3 + η, r, η > 0.

(2) MT = E(T−1X ′X) is uniformly positive definite in T .

(3) LT = E(1/T )∑T

t=1 ft(F−1(τ))xtx

′t is uniformly positive

definite in T .

(A4) B is a compact set in Rk and βτ ∈ B.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 48 / 86

Page 54

Asymptotic Normality of Quantile Estimator

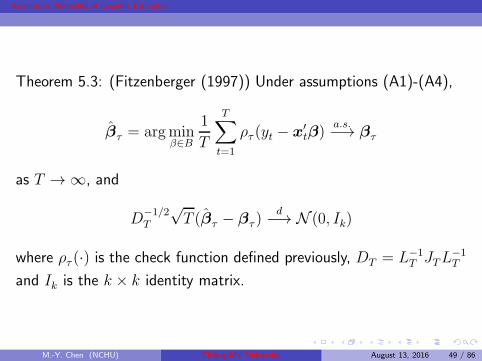

Theorem 5.3: (Fitzenberger (1997)) Under assumptions (A1)-(A4),

βτ = argminβ∈B

1

T

T∑

t=1

ρτ (yt − x′tβ)

a.s.−→ βτ

as T → ∞, and

D−1/2T

√T (βτ − βτ )

d−→ N (0, Ik)

where ρτ (·) is the check function defined previously, DT = L−1T JTL

−1T

and Ik is the k × k identity matrix.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 49 / 86

Page 55

Asymptotic Normality of Quantile Estimator

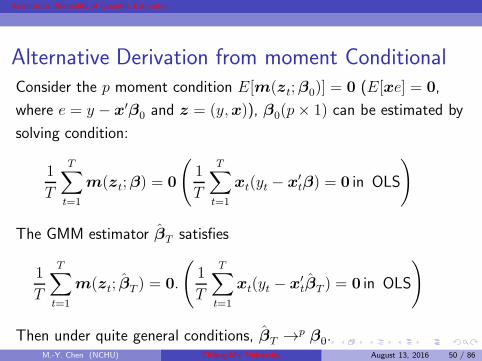

Alternative Derivation from moment ConditionalConsider the p moment condition E[m(zt;β0)] = 0 (E[xe] = 0,

where e = y − x′β0 and z = (y,x)), β0(p× 1) can be estimated by

solving condition:

1

T

T∑

t=1

m(zt;β) = 0

(

1

T

T∑

t=1

xt(yt − x′tβ) = 0 in OLS

)

The GMM estimator βT satisfies

1

T

T∑

t=1

m(zt; βT ) = 0.

(

1

T

T∑

t=1

xt(yt − x′tβT ) = 0 in OLS

)

Then under quite general conditions, βT →p β0.M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 50 / 86

Page 56

Asymptotic Normality of Quantile Estimator

Suppose that the following uniform law of large number is satisfied,

1

T

T∑

t=1

∇βm(zt; βT ) →p G0 := E[∇βm(zt;β0)],

−1

T

T∑

t=1

∇βxt(yt − x′tβT ) =

1

T

T∑

t=1

xtx′t →p G0 :=

1

T

T∑

t=1

E(xtx′t) in OLS

where G0 is nonsingular. Then, it can be shown that

√T (βT − β0) → N (0,G−1

0 Σ0G−10 ), (4)

where Σ0 = E[m(zt;β0)m(zt;β0)′] = var[m(zt,β0)] (is

E[xte2tx

′t] = var(xtet) in OLS).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 51 / 86

Page 57

Asymptotic Normality of Quantile Estimator

Ignoring the observations that yt = x′tβ (since the first derivative of

the objection is not identified), we can write the approximate, first

order condition of minimization is

1

T

T∑

t=1

ψβτ(yt − x′

tβ) =1

T

T∑

t=1

xt[τ − 1yt−x′

tβ<0] = op(1). (5)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 52 / 86

Page 58

Asymptotic Normality of Quantile Estimator

Assume that (yt,x′t)

′ are i.i.d. random vectors. Taking expectation of

(5) and given

E(1yt−x′

tβ<0|xt) = Fy|x(x′tβ),

we have

E

(

1

T

T∑

t=1

[ψβτ(yt − x′

tβ)]

)

= E[ψβτ(yt − x′

tβ)] = E[xt[τ − 1yt−x′

tβ<0]]

= Ext[τ −E(1yt−x′

tβ<0|xt)] = Ext[τ − Fy|x(x′tβ)].

As Fy|x(x′tβτ ) = τ , the moment condition is hold since

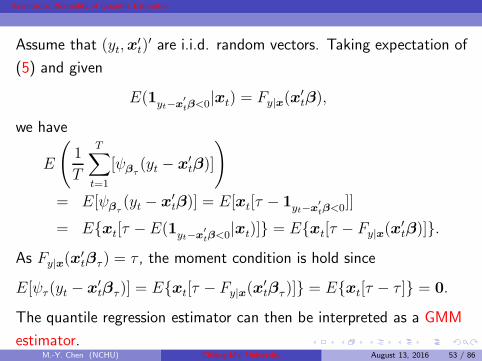

E[ψτ (yt − x′tβτ )] = Ext[τ − Fy|x(x

′tβτ )] = Ext[τ − τ ] = 0.

The quantile regression estimator can then be interpreted as a GMM

estimator.M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 53 / 86

Page 59

Asymptotic Normality of Quantile Estimator

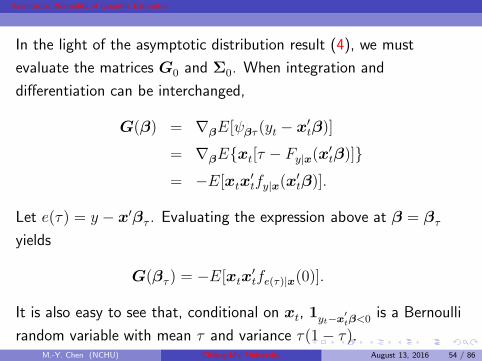

In the light of the asymptotic distribution result (4), we must

evaluate the matrices G0 and Σ0. When integration and

differentiation can be interchanged,

G(β) = ∇βE[ψβτ (yt − x′tβ)]

= ∇βExt[τ − Fy|x(x′tβ)]

= −E[xtx′tfy|x(x

′tβ)].

Let e(τ) = y − x′βτ . Evaluating the expression above at β = βτ

yields

G(βτ ) = −E[xtx′tfe(τ)|x(0)].

It is also easy to see that, conditional on xt, 1yt−x′

tβ<0 is a Bernoulli

random variable with mean τ and variance τ(1− τ).M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 54 / 86

Page 60

Asymptotic Normality of Quantile Estimator

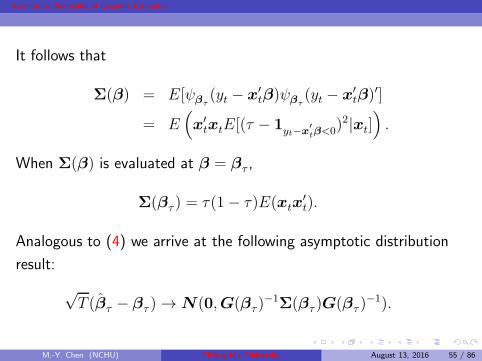

It follows that

Σ(β) = E[ψβτ(yt − x′

tβ)ψβτ(yt − x′

tβ)′]

= E(

x′txtE[(τ − 1yt−x

′

tβ<0)2|xt]

)

.

When Σ(β) is evaluated at β = βτ ,

Σ(βτ ) = τ(1 − τ)E(xtx′t).

Analogous to (4) we arrive at the following asymptotic distribution

result:

√T (βτ − βτ ) → N(0,G(βτ )

−1Σ(βτ )G(βτ )

−1).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 55 / 86

Page 61

Asymptotic Normality of Quantile Estimator

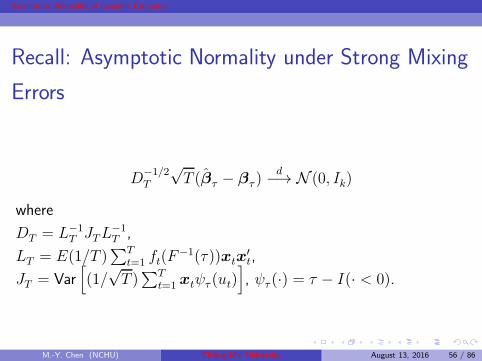

Recall: Asymptotic Normality under Strong Mixing

Errors

D−1/2T

√T (βτ − βτ )

d−→ N (0, Ik)

where

DT = L−1T JTL

−1T ,

LT = E(1/T )∑T

t=1 ft(F−1(τ))xtx

′t,

JT = Var[

(1/√T )∑T

t=1 xtψτ (ut)]

, ψτ (·) = τ − I(· < 0).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 56 / 86

Page 62

Asymptotic Normality of Quantile Estimator

Testing H0 : Rβτ = r

Wald Test: By Theorem 5.2, we have

R√T (βτ − βτ )

d−→ N (0,RDTR′),

or equivalently

Γ−1/2T R

√T (βτ − βτ )

d−→ N (0, Iq),

where ΓT = RDTR′.

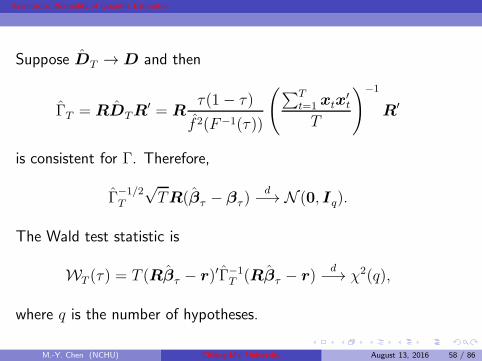

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 57 / 86

Page 63

Asymptotic Normality of Quantile Estimator

Suppose DT → D and then

ΓT = RDTR′ = R

τ(1− τ)

f 2(F−1(τ))

(

∑Tt=1 xtx

′t

T

)−1

R′

is consistent for Γ. Therefore,

Γ−1/2T

√TR(βτ − βτ )

d−→ N (0, Iq).

The Wald test statistic is

WT (τ) = T (Rβτ − r)′Γ−1T (Rβτ − r)

d−→ χ2(q),

where q is the number of hypotheses.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 58 / 86

Page 64

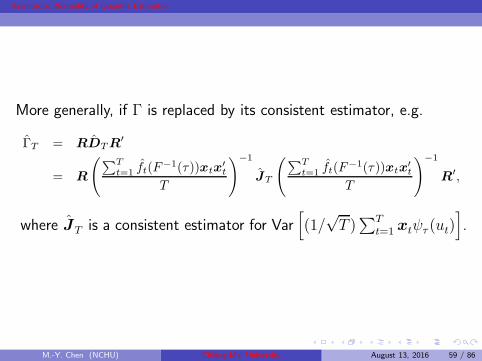

Asymptotic Normality of Quantile Estimator

More generally, if Γ is replaced by its consistent estimator, e.g.

ΓT = RDTR′

= R

(

∑Tt=1 ft(F

−1(τ))xtx′t

T

)−1

JT

(

∑Tt=1 ft(F

−1(τ))xtx′t

T

)−1

R′,

where JT is a consistent estimator for Var[

(1/√T )∑T

t=1 xtψτ (ut)]

.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 59 / 86

Page 65

Asymptotic Normality of Quantile Estimator

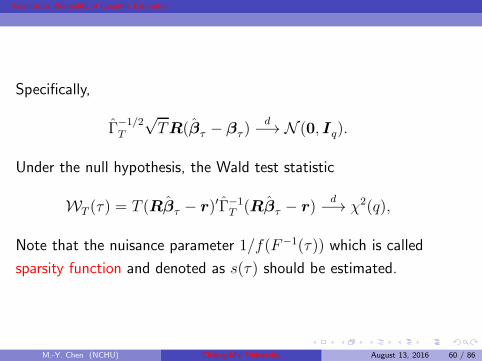

Specifically,

Γ−1/2T

√TR(βτ − βτ )

d−→ N (0, Iq).

Under the null hypothesis, the Wald test statistic

WT (τ) = T (Rβτ − r)′Γ−1T (Rβτ − r)

d−→ χ2(q),

Note that the nuisance parameter 1/f(F−1(τ)) which is called

sparsity function and denoted as s(τ) should be estimated.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 60 / 86

Page 66

Asymptotic Normality of Quantile Estimator

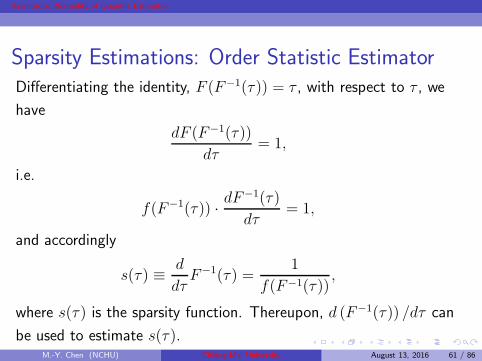

Sparsity Estimations: Order Statistic EstimatorDifferentiating the identity, F (F−1(τ)) = τ , with respect to τ , we

have

dF (F−1(τ))

dτ= 1,

i.e.

f(F−1(τ)) · dF−1(τ)

dτ= 1,

and accordingly

s(τ) ≡ d

dτF−1(τ) =

1

f(F−1(τ)),

where s(τ) is the sparsity function. Thereupon, d (F−1(τ)) /dτ can

be used to estimate s(τ).M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 61 / 86

Page 67

Asymptotic Normality of Quantile Estimator

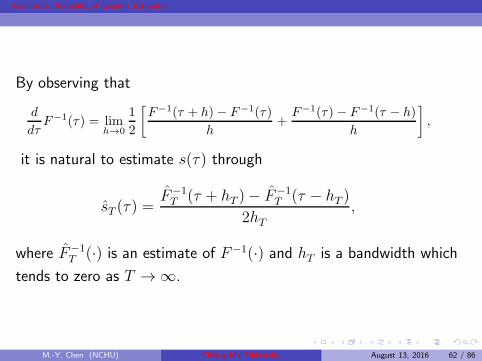

By observing that

d

dτF−1(τ) = lim

h→0

1

2

[

F−1(τ + h)− F−1(τ)

h+F−1(τ)− F−1(τ − h)

h

]

,

it is natural to estimate s(τ) through

sT (τ) =F−1T (τ + hT )− F−1

T (τ − hT )

2hT,

where F−1T (·) is an estimate of F−1(·) and hT is a bandwidth which

tends to zero as T → ∞.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 62 / 86

Page 68

Asymptotic Normality of Quantile Estimator

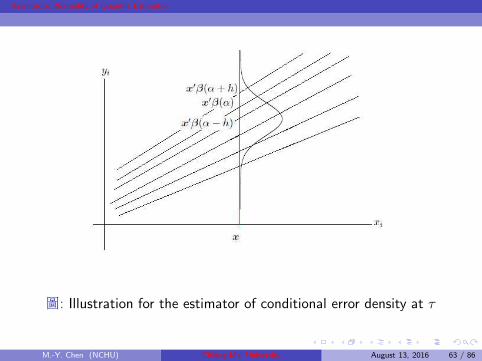

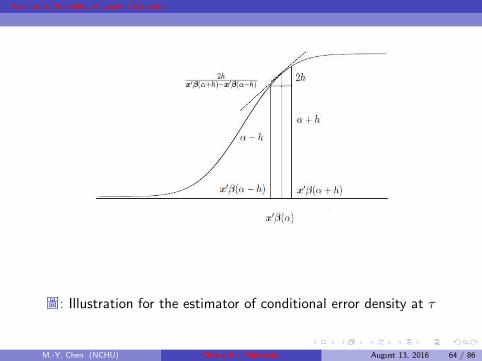

圖: Illustration for the estimator of conditional error density at τ

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 63 / 86

Page 69

Asymptotic Normality of Quantile Estimator

圖: Illustration for the estimator of conditional error density at τ

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 64 / 86

Page 70

Asymptotic Normality of Quantile Estimator

Questions

How to determine hT ?

How to estimate F−1(·)?

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 65 / 86

Page 71

Asymptotic Normality of Quantile Estimator

Bandwidth Selectors

Bofinger Bandwidth Selector:

hT = T−1/5

[

4.5φ4(Φ−1(τ))

(2Φ−1(τ)2 + 1)2

]1/5

,

Hall and Sheather Bandwidth Selector:

hT = T−1/3z2/3α

[

1.5φ2(Φ−1(τ))

2Φ−1(τ)2 + 1

]1/3

.

Chamberlain Bandwidth Selector:

hT = zα√

τ(1− τ)/T .

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 66 / 86

Page 72

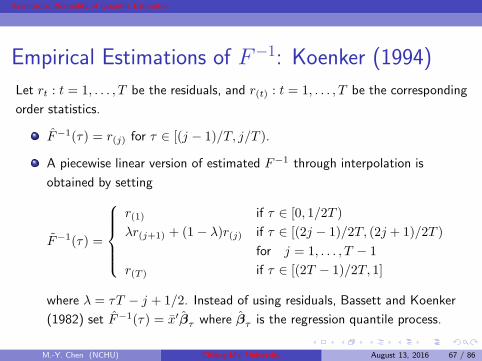

Asymptotic Normality of Quantile Estimator

Empirical Estimations of F−1: Koenker (1994)

Let rt : t = 1, . . . , T be the residuals, and r(t) : t = 1, . . . , T be the corresponding

order statistics.

F−1(τ) = r(j) for τ ∈ [(j − 1)/T, j/T ).

A piecewise linear version of estimated F−1 through interpolation is

obtained by setting

F−1(τ) =

r(1) if τ ∈ [0, 1/2T )

λr(j+1) + (1 − λ)r(j) if τ ∈ [(2j − 1)/2T, (2j + 1)/2T )

for j = 1, . . . , T − 1

r(T ) if τ ∈ [(2T − 1)/2T, 1]

where λ = τT − j + 1/2. Instead of using residuals, Bassett and Koenker

(1982) set F−1(τ) = x′βτ where βτ is the regression quantile process.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 67 / 86

Page 73

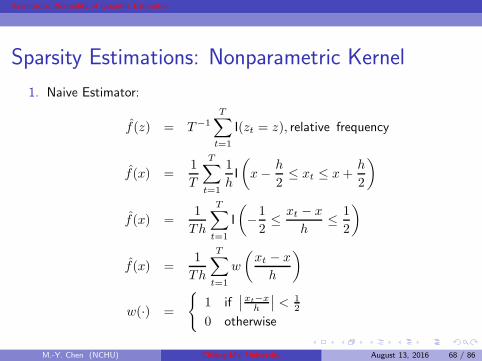

Asymptotic Normality of Quantile Estimator

Sparsity Estimations: Nonparametric Kernel

1. Naive Estimator:

f(z) = T−1T∑

t=1

I(zt = z), relative frequency

f(x) =1

T

T∑

t=1

1

hI

(

x− h

2≤ xt ≤ x+

h

2

)

f(x) =1

Th

T∑

t=1

I

(

−1

2≤ xt − x

h≤ 1

2

)

f(x) =1

Th

T∑

t=1

w

(

xt − x

h

)

w(·) =

1 if∣

∣

xt−xh

∣

∣ < 12

0 otherwise

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 68 / 86

Page 74

Asymptotic Normality of Quantile Estimator

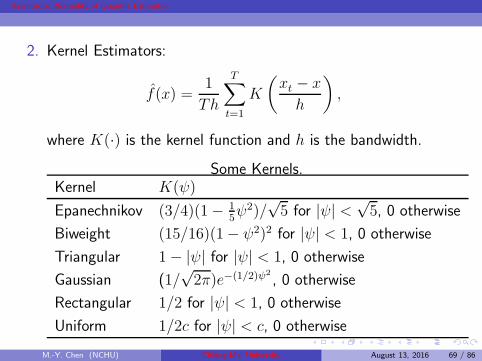

2. Kernel Estimators:

f(x) =1

Th

T∑

t=1

K

(

xt − x

h

)

,

where K(·) is the kernel function and h is the bandwidth.

Some Kernels.Kernel K(ψ)

Epanechnikov (3/4)(1− 15ψ2)/

√5 for |ψ| <

√5, 0 otherwise

Biweight (15/16)(1− ψ2)2 for |ψ| < 1, 0 otherwise

Triangular 1− |ψ| for |ψ| < 1, 0 otherwise

Gaussian (1/√2π)e−(1/2)ψ2

, 0 otherwise

Rectangular 1/2 for |ψ| < 1, 0 otherwise

Uniform 1/2c for |ψ| < c, 0 otherwise

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 69 / 86

Page 75

Asymptotic Normality of Quantile Estimator

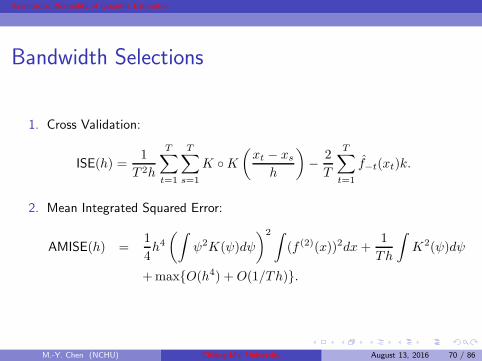

Bandwidth Selections

1. Cross Validation:

ISE(h) =1

T 2h

T∑

t=1

T∑

s=1

K K(

xt − xsh

)

− 2

T

T∑

t=1

f−t(xt)k.

2. Mean Integrated Squared Error:

AMISE(h) =1

4h4(∫

ψ2K(ψ)dψ

)2 ∫

(f (2)(x))2dx +1

Th

∫

K2(ψ)dψ

+maxO(h4) +O(1/Th).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 70 / 86

Page 76

Asymptotic Normality of Quantile Estimator

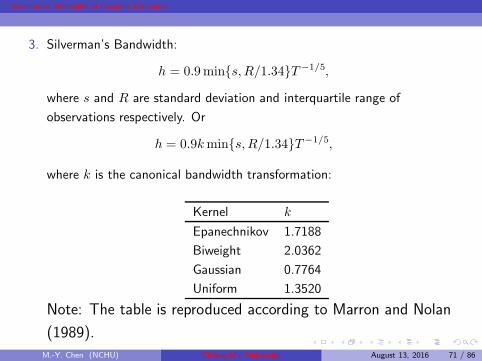

3. Silverman’s Bandwidth:

h = 0.9mins,R/1.34T−1/5,

where s and R are standard deviation and interquartile range of

observations respectively. Or

h = 0.9kmins,R/1.34T−1/5,

where k is the canonical bandwidth transformation:

Kernel k

Epanechnikov 1.7188

Biweight 2.0362

Gaussian 0.7764

Uniform 1.3520

Note: The table is reproduced according to Marron and Nolan

(1989).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 71 / 86

Page 77

Asymptotic Normality of Quantile Estimator

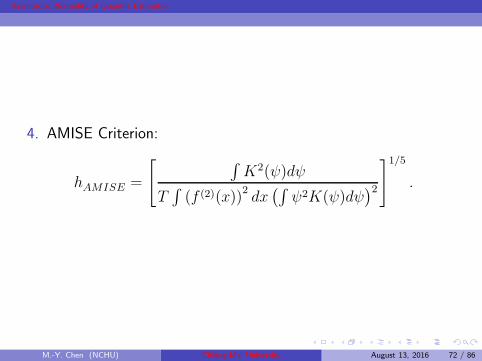

4. AMISE Criterion:

hAMISE =

[

∫

K2(ψ)dψ

T∫

(f (2)(x))2dx(∫

ψ2K(ψ)dψ)2

]1/5

.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 72 / 86

Page 78

Asymptotic Normality of Quantile Estimator

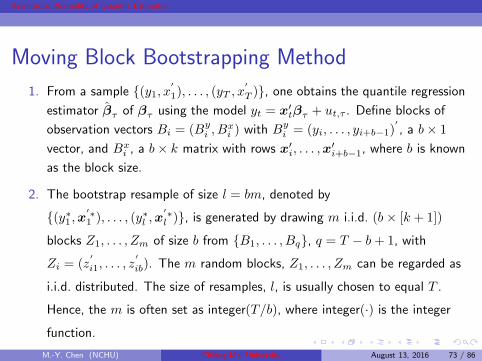

Moving Block Bootstrapping Method

1. From a sample (y1, x′

1), . . . , (yT , x′

T ), one obtains the quantile regression

estimator βτ of βτ using the model yt = x′tβτ + ut,τ . Define blocks of

observation vectors Bi = (Byi , B

xi ) with B

yi = (yi, . . . , yi+b−1)

′

, a b× 1

vector, and Bxi , a b× k matrix with rows x′

i, . . . ,x′i+b−1, where b is known

as the block size.

2. The bootstrap resample of size l = bm, denoted by

(y∗1 ,x′∗1 ), . . . , (y∗l ,x

′∗l ), is generated by drawing m i.i.d. (b × [k + 1])

blocks Z1, . . . , Zm of size b from B1, . . . , Bq, q = T − b + 1, with

Zi = (z′

i1, . . . , z′

ib). The m random blocks, Z1, . . . , Zm can be regarded as

i.i.d. distributed. The size of resamples, l, is usually chosen to equal T .

Hence, the m is often set as integer(T/b), where integer(·) is the integer

function.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 73 / 86

Page 79

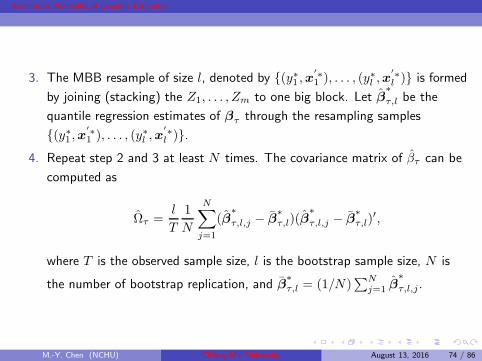

Asymptotic Normality of Quantile Estimator

3. The MBB resample of size l, denoted by (y∗1 ,x′∗1 ), . . . , (y∗l ,x

′∗l ) is formed

by joining (stacking) the Z1, . . . , Zm to one big block. Let β∗

τ,l be the

quantile regression estimates of βτ through the resampling samples

(y∗1 ,x′∗1 ), . . . , (y∗l ,x

′∗l ).

4. Repeat step 2 and 3 at least N times. The covariance matrix of βτ can be

computed as

Ωτ =l

T

1

N

N∑

j=1

(β∗

τ,l,j − β∗τ,l)(β

∗

τ,l,j − β∗τ,l)

′,

where T is the observed sample size, l is the bootstrap sample size, N is

the number of bootstrap replication, and β∗τ,l = (1/N)

∑Nj=1 β

∗

τ,l,j.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 74 / 86

Page 80

Asymptotic Normality of Quantile Estimator

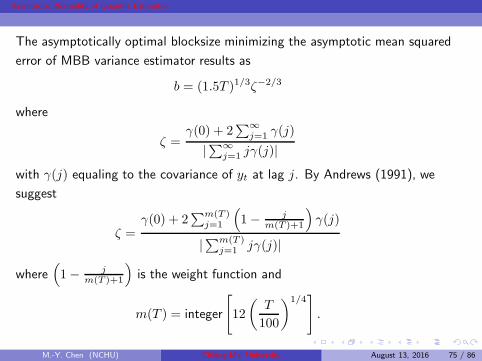

The asymptotically optimal blocksize minimizing the asymptotic mean squared

error of MBB variance estimator results as

b = (1.5T )1/3ζ−2/3

where

ζ =γ(0) + 2

∑∞j=1 γ(j)

|∑∞j=1 jγ(j)|

with γ(j) equaling to the covariance of yt at lag j. By Andrews (1991), we

suggest

ζ =γ(0) + 2

∑m(T )j=1

(

1− jm(T )+1

)

γ(j)

|∑m(T )j=1 jγ(j)|

where(

1− jm(T )+1

)

is the weight function and

m(T ) = integer

[

12

(

T

100

)1/4]

.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 75 / 86

Page 81

Asymptotic Normality of Quantile Estimator

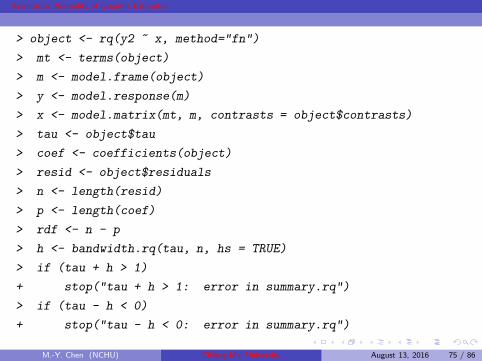

> object <- rq(y2 ~ x, method="fn")

> mt <- terms(object)

> m <- model.frame(object)

> y <- model.response(m)

> x <- model.matrix(mt, m, contrasts = object$contrasts)

> tau <- object$tau

> coef <- coefficients(object)

> resid <- object$residuals

> n <- length(resid)

> p <- length(coef)

> rdf <- n - p

> h <- bandwidth.rq(tau, n, hs = TRUE)

> if (tau + h > 1)

+ stop("tau + h > 1: error in summary.rq")

> if (tau - h < 0)

+ stop("tau - h < 0: error in summary.rq")

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 75 / 86

Page 82

Asymptotic Normality of Quantile Estimator

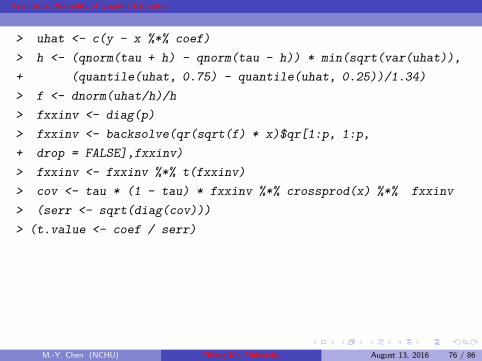

> uhat <- c(y - x %*% coef)

> h <- (qnorm(tau + h) - qnorm(tau - h)) * min(sqrt(var(uhat)),

+ (quantile(uhat, 0.75) - quantile(uhat, 0.25))/1.34)

> f <- dnorm(uhat/h)/h

> fxxinv <- diag(p)

> fxxinv <- backsolve(qr(sqrt(f) * x)$qr[1:p, 1:p,

+ drop = FALSE],fxxinv)

> fxxinv <- fxxinv %*% t(fxxinv)

> cov <- tau * (1 - tau) * fxxinv %*% crossprod(x) %*% fxxinv

> (serr <- sqrt(diag(cov)))

> (t.value <- coef / serr)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 76 / 86

Page 83

Asymptotic Normality of Quantile Estimator

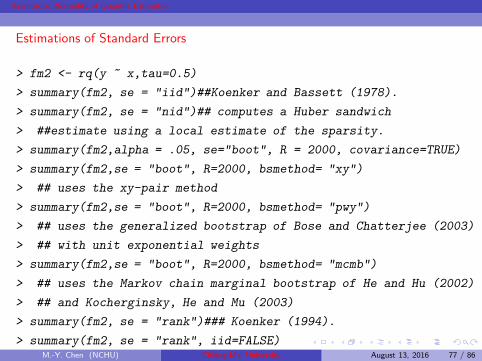

Estimations of Standard Errors

se = ”iid”: presumes that the errors are iid and computes an estimate of the

asymptotic covariance matrix as in KB(1978).

se = ”nid”: presumes local (in tau) linearity (in x) of the the conditional

quantile functions and computes a Huber sandwich estimate using a local

estimate of the sparsity.

se = ”boot”: implements one of several possible bootstrapping alternatives

for estimating standard errors.

se = ”rank”: produces confidence intervals for the estimated parameters by

inverting a rank test as described in Koenker (1994).

se = ”ker”: ”ker”which uses a kernel estimate of the sandwich as proposed

by Powell (1990).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 76 / 86

Page 84

Asymptotic Normality of Quantile Estimator

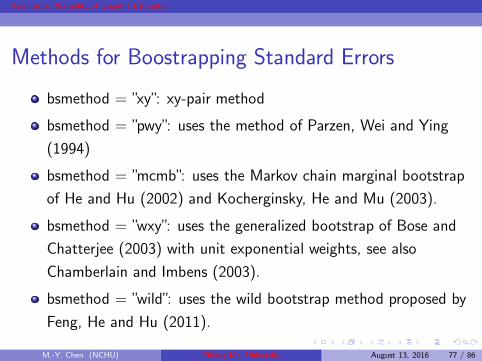

Methods for Boostrapping Standard Errors

bsmethod = ”xy”: xy-pair method

bsmethod = ”pwy”: uses the method of Parzen, Wei and Ying

(1994)

bsmethod = ”mcmb”: uses the Markov chain marginal bootstrap

of He and Hu (2002) and Kocherginsky, He and Mu (2003).

bsmethod = ”wxy”: uses the generalized bootstrap of Bose and

Chatterjee (2003) with unit exponential weights, see also

Chamberlain and Imbens (2003).

bsmethod = ”wild”: uses the wild bootstrap method proposed by

Feng, He and Hu (2011).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 77 / 86

Page 85

Asymptotic Normality of Quantile Estimator

Estimations of Standard Errors

> fm2 <- rq(y ~ x,tau=0.5)

> summary(fm2, se = "iid")##Koenker and Bassett (1978).

> summary(fm2, se = "nid")## computes a Huber sandwich

> ##estimate using a local estimate of the sparsity.

> summary(fm2,alpha = .05, se="boot", R = 2000, covariance=TRUE)

> summary(fm2,se = "boot", R=2000, bsmethod= "xy")

> ## uses the xy-pair method

> summary(fm2,se = "boot", R=2000, bsmethod= "pwy")

> ## uses the generalized bootstrap of Bose and Chatterjee (2003)

> ## with unit exponential weights

> summary(fm2,se = "boot", R=2000, bsmethod= "mcmb")

> ## uses the Markov chain marginal bootstrap of He and Hu (2002)

> ## and Kocherginsky, He and Mu (2003)

> summary(fm2, se = "rank")### Koenker (1994).

> summary(fm2, se = "rank", iid=FALSE)M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 77 / 86

Page 86

Asymptotic Normality of Quantile Estimator

> ## option iid = FALSE implements the proposal of Koenker and

> ## Machado (1999)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 78 / 86

Page 87

Asymptotic Normality of Quantile Estimator

Provided Tests in quantreg

anova

KhmaladzeTest

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 78 / 86

Page 88

Asymptotic Normality of Quantile Estimator

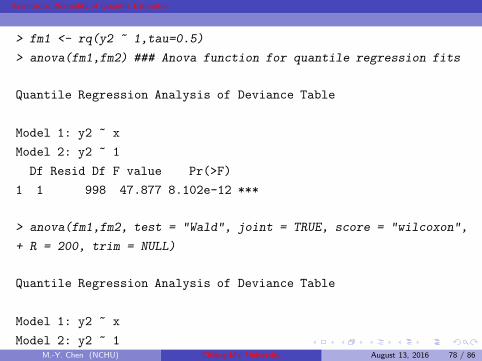

> fm1 <- rq(y2 ~ 1,tau=0.5)

> anova(fm1,fm2) ### Anova function for quantile regression fits

Quantile Regression Analysis of Deviance Table

Model 1: y2 ~ x

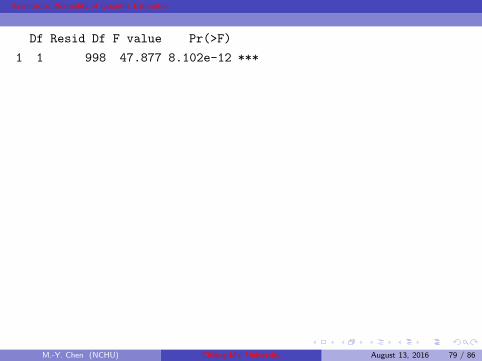

Model 2: y2 ~ 1

Df Resid Df F value Pr(>F)

1 1 998 47.877 8.102e-12 ***

> anova(fm1,fm2, test = "Wald", joint = TRUE, score = "wilcoxon",

+ R = 200, trim = NULL)

Quantile Regression Analysis of Deviance Table

Model 1: y2 ~ x

Model 2: y2 ~ 1M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 78 / 86

Page 89

Asymptotic Normality of Quantile Estimator

Df Resid Df F value Pr(>F)

1 1 998 47.877 8.102e-12 ***

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 79 / 86

Page 90

Asymptotic Normality of Quantile Estimator

Khmaladze Test

Tests of location and location-scale shift hypotheses for linear models

of Koenker and Xio (2002).

location shift model: γ00 6= 0 and γ01 = 0;

location-scale shift model: γ00 6= 0 and γ01 6= 0.

location shift: H0 : γ01 = 0,

location-sacle shift: H0 : γ00 = 0,γ01 = 0.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 79 / 86

Page 91

Asymptotic Normality of Quantile Estimator

> KhmaladzeTest(y2 ~ x, data = NULL, taus = -1, nullH = "location")

> KhmaladzeTest(y2 ~ x, taus = seq(.05,.95,by = .01))

> KhmaladzeTest(y2 ~ x, data = NULL, taus = -1,

+ nullH = "location-scale")

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 79 / 86

Page 92

Asymptotic Normality of Quantile Estimator

code: Wald.R

> ## clear all existing objects

> rm(list=ls(all=TRUE))

> options(digits = 4)

> library(quantreg) # For quantile regression

> library(qpcR) # for the Hannan Quinn Criterion

> library(sandwich) #for HAC Estimator

> library(car) #for linearHypothesis

> library(lmtest) #for coeftest

> x1 <- rnorm(1000, 1, 1)

> x2 <- runif(1000)

> x3 <- rnorm(1000, 10, 3)

> e <- rnorm(1000)

> y <- 1 + 0.1*x1 - 0.3 * x2 + 0.2 * x3 + sqrt(x3) * e

> x <- cbind(x1, x2, x3)

>M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 79 / 86

Page 93

Asymptotic Normality of Quantile Estimator

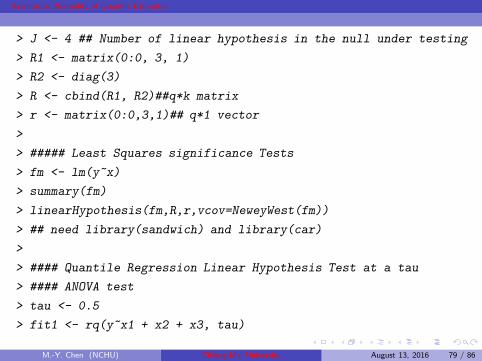

> J <- 4 ## Number of linear hypothesis in the null under testing

> R1 <- matrix(0:0, 3, 1)

> R2 <- diag(3)

> R <- cbind(R1, R2)##q*k matrix

> r <- matrix(0:0,3,1)## q*1 vector

>

> ##### Least Squares significance Tests

> fm <- lm(y~x)

> summary(fm)

> linearHypothesis(fm,R,r,vcov=NeweyWest(fm))

> ## need library(sandwich) and library(car)

>

> #### Quantile Regression Linear Hypothesis Test at a tau

> #### ANOVA test

> tau <- 0.5

> fit1 <- rq(y~x1 + x2 + x3, tau)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 79 / 86

Page 94

Asymptotic Normality of Quantile Estimator

> fit2 <- rq(y~x1, tau)

> anova(fit1,fit2, test = "Wald", joint = TRUE,

+ score = "tau", se = "nid", R = 200, trim = NULL)

>

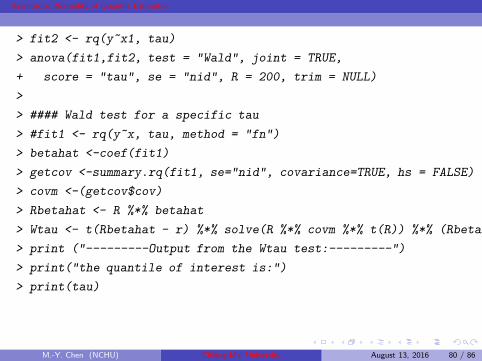

> #### Wald test for a specific tau

> #fit1 <- rq(y~x, tau, method = "fn")

> betahat <-coef(fit1)

> getcov <-summary.rq(fit1, se="nid", covariance=TRUE, hs = FALSE)

> covm <-(getcov$cov)

> Rbetahat <- R %*% betahat

> Wtau <- t(Rbetahat - r) %*% solve(R %*% covm %*% t(R)) %*% (Rbetahat

> print ("---------Output from the Wtau test:---------")

> print("the quantile of interest is:")

> print(tau)

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 80 / 86

Page 95

Asymptotic Normality of Quantile Estimator

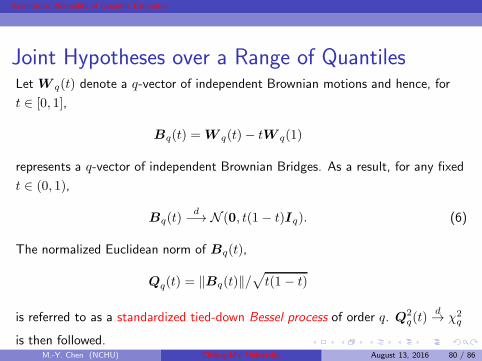

Joint Hypotheses over a Range of QuantilesLet W q(t) denote a q-vector of independent Brownian motions and hence, for

t ∈ [0, 1],

Bq(t) = W q(t)− tW q(1)

represents a q-vector of independent Brownian Bridges. As a result, for any fixed

t ∈ (0, 1),

Bq(t)d−→ N (0, t(1− t)Iq). (6)

The normalized Euclidean norm of Bq(t),

Qq(t) = ‖Bq(t)‖/√

t(1 − t)

is referred to as a standardized tied-down Bessel process of order q. Q2q(t)

d→ χ2q

is then followed.M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 80 / 86

Page 96

Asymptotic Normality of Quantile Estimator

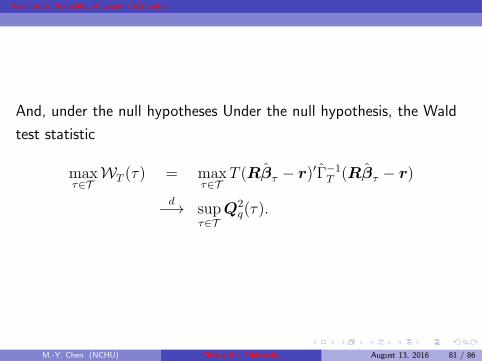

And, under the null hypotheses Under the null hypothesis, the Wald

test statistic

maxτ∈T

WT (τ) = maxτ∈T

T (Rβτ − r)′Γ−1T (Rβτ − r)

d−→ supτ∈T

Q2q(τ).

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 81 / 86

Page 97

Asymptotic Normality of Quantile Estimator

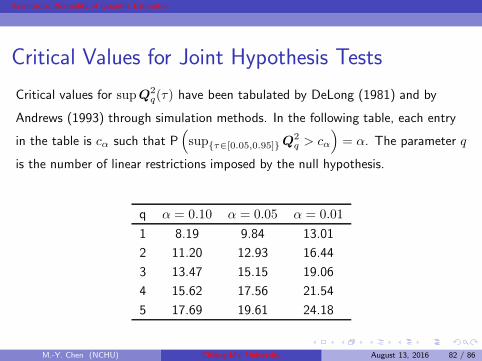

Critical Values for Joint Hypothesis Tests

Critical values for supQ2q(τ) have been tabulated by DeLong (1981) and by

Andrews (1993) through simulation methods. In the following table, each entry

in the table is cα such that P(

supτ∈[0.05,0.95]Q2q > cα

)

= α. The parameter q

is the number of linear restrictions imposed by the null hypothesis.

q α = 0.10 α = 0.05 α = 0.01

1 8.19 9.84 13.01

2 11.20 12.93 16.44

3 13.47 15.15 19.06

4 15.62 17.56 21.54

5 17.69 19.61 24.18

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 82 / 86

Page 98

Asymptotic Normality of Quantile Estimator

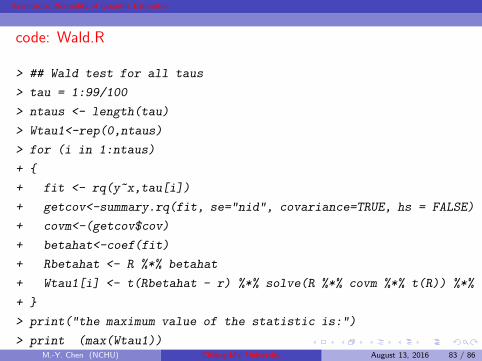

code: Wald.R

> ## Wald test for all taus

> tau = 1:99/100

> ntaus <- length(tau)

> Wtau1<-rep(0,ntaus)

> for (i in 1:ntaus)

+

+ fit <- rq(y~x,tau[i])

+ getcov<-summary.rq(fit, se="nid", covariance=TRUE, hs = FALSE)

+ covm<-(getcov$cov)

+ betahat<-coef(fit)

+ Rbetahat <- R %*% betahat

+ Wtau1[i] <- t(Rbetahat - r) %*% solve(R %*% covm %*% t(R)) %*% (Rbetahat

+

> print("the maximum value of the statistic is:")

> print (max(Wtau1))M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 83 / 86

Page 99

Asymptotic Normality of Quantile Estimator

Average Treatment Effect (ATE)

Evaluating the impact of a treatment (program, policy, intervention).

Let D be the binary indicator of treatment and X be covariates.

Y1(Y0) is the potential outcome when an agent is (is not)

exposed to the treatment.

The observed outcome is Y = DY1 + (1−D)Y0.

We observe only one potential outcome (Y1i or Y0i) and hence can not

identify the individual treatment effect, Y1i − Y0i . We may estimate the

ATE: E(Y1 − Y0).

Under conditional independence: (Y1, Y0)⊥D|X ,

E(Y |D = 1, X)− E(Y |D = 0, X) = E(Y1 − Y0|X),

so that the ATE is E(Y1 − Y0) = E[E(Y1 − Y0|X)].

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 83 / 86

Page 100

Asymptotic Normality of Quantile Estimator

Using the sammpe counterpart of

E(Y |D = 1, X)−E(Y |D = 0, X), we have

ATE =1

n

n∑

i=1

[E(Yi|Di = 1, Xi)− E(Yi|Di = 0, Xi)].

For the dummy-variable regression:

Yi = α +Diγ +X ′iβ + ei, i = 1, . . . , n,

the LS estimate of γ is ATE.

Other estimators: Kernel matching, nearest neighbor matching,

propensity score matching (based on p(x) = P (D = 1|X = x)),

etc.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 84 / 86

Page 101

Asymptotic Normality of Quantile Estimator

Quantile Treatment Effect (QTE)

Let F0 and F1 be the distributions of control and treatment responses. Let

(η) be the“horizontal shift” from F0 to F1: F0(η) = F1(η +(η)).

Then, (η) = F−11 (F0(η))− η, and the τth QTE is, for F0(η) = τ ,

QTE(τ) = F−11 (τ) − F−1

0 (τ) = qY1(τ) − qY0(τ),

the difference between the quantiles of two distributions.

The quantile regression:

Yi = α+Diγ +X ′iβ + ei,

the resulting QR estimate γ(τ) is the estimated τth QTE.

Other: A weighting estimator based on the propensity score.

M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 85 / 86

Page 102

Asymptotic Normality of Quantile Estimator

Difference in Differences

To identify the“true” treatment effect, the potential change due to time

(other factors) must be excluded first.

Define the following dummy variables:Di,at = Di,t ×Di,a.

Di,t = 1 if the ith individual receives the treatment;

Di,a = 1 if the ith individual is in the post-program period;

Model: Yi = α+ α1Di,t + α2Di,a + α3Di,at +Xiβ + ei.

For the treatment group in pre- and post-program periods, the

time effect is α2 + α3.

For the control group in pre- and post-program periods, the

time effect is α2.

The treatment effect is the difference between these two effects:

α3.M.-Y. Chen (NCHU) Chiang-Mai University August 13, 2016 86 / 86