56

January-September 2012 QUARTERLY REPORT 3Q12

| Date post: | 08-Sep-2018 |

| Category: |

Documents |

| Upload: | trinhkhanh |

| View: | 214 times |

| Download: | 0 times |

January-September 2012

QUARTERLY REPORT

3Q12 3Q

12

Contents 2 BBVAGroupHighlights

3 Groupinformation Relevantevents........................................................................................................................................................................................................................................................... 3

Earnings................................................................................................................................................................................................................................................................................6

Balancesheetandbusinessactivity................................................................................................................................................................................................. 13

Capitalbase.....................................................................................................................................................................................................................................................................17

Riskmanagement...................................................................................................................................................................................................................................................19

TheBBVAshare........................................................................................................................................................................................................................................................ 22

Corporateresponsibility................................................................................................................................................................................................................................. 23

24 Businessareas Spain..................................................................................................................................................................................................................................................................................... 26

Eurasia.................................................................................................................................................................................................................................................................................. 31

Mexico..................................................................................................................................................................................................................................................................................35

SouthAmerica...........................................................................................................................................................................................................................................................39

TheUnitedStates...................................................................................................................................................................................................................................................43

CorporateActivities..............................................................................................................................................................................................................................................47

Otherinformation:Corporate&InvestmentBanking...............................................................................................................................................50

January-September2012

QUARTERLYREPORT

2 BBVAGroupHighlights

BBVAGroupHighlights

BBVA Group Highlights (Consolidatedfigures)

30-09-12 ∆% 30-09-11 31-12-11

Balance sheet (million euros)

Totalassets 645,447 10.4 584,438 597,688

Customerlending(gross) 377,383 7.0 352,633 361,310

Depositsfromcustomers 288,709 2.4 282,050 282,173

Othercustomerfunds 160,113 16.7 137,252 144,291

Totalcustomerfunds 448,823 7.0 419,302 426,464

Totalequity 43,750 9.7 39,868 40,058

Income statement (million euros)

Netinterestincome 11,220 16.0 9,676 13,160

Grossincome 17,103 13.6 15,052 20,566

Operatingincome 9,000 16.1 7,753 10,615

Incomebeforetax 2,173 (47.6) 4,145 3,770

Netattributableprofit 1,656 (47.3) 3,143 3,004

Netattributableprofitadjusted(1) 3,345 (3.8) 3,478 4,505

Data per share and share performance ratios

Shareprice(euros) 6.11 (1.1) 6.18 6.68

Marketcapitalization(millioneuros) 32,901 10.3 29,817 32,753

Netattributableprofitpershare(euros) 0.32 (50.3) 0.64 0.62

Netattributableprofitpershareadjusted(euros)(1) 0.63 (11.4) 0.71 0.93

Bookvaluepershare(euros) 8.13 (5.6) 8.61 8.35

P/BV(Price/bookvalue;times) 0.8 0.7 0.8

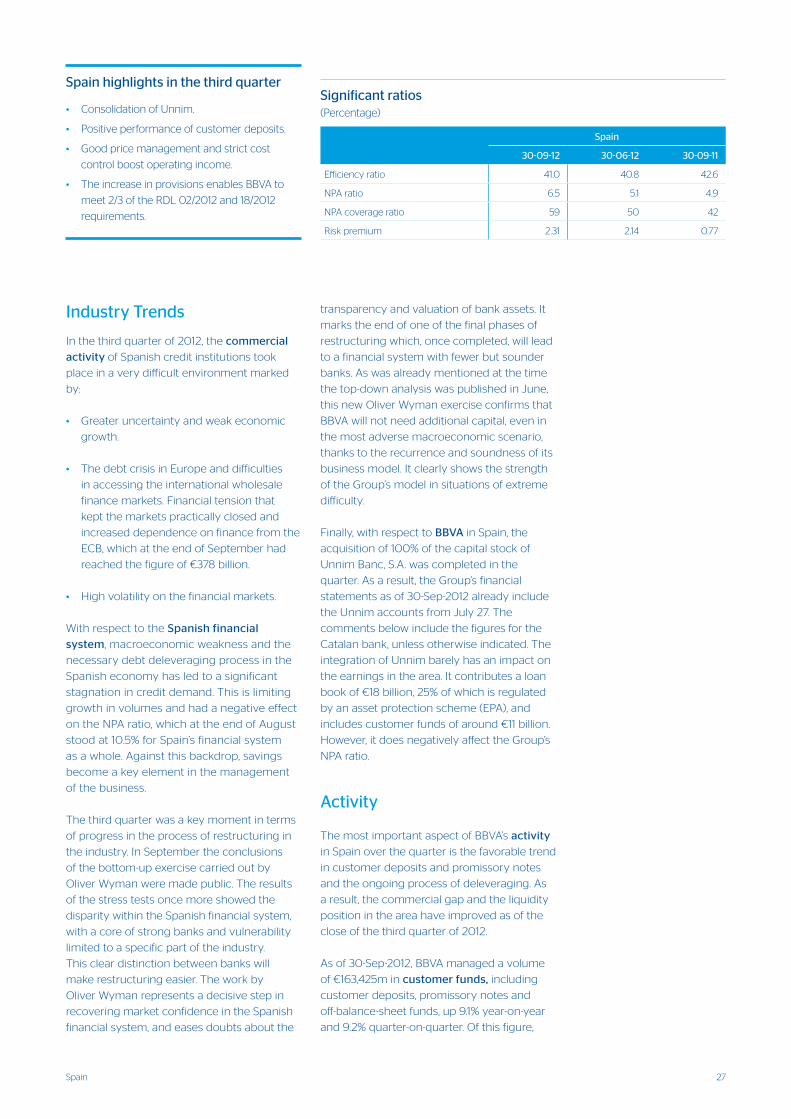

Significant Ratios (%)

ROE(Netattributableprofit/Averageequity) 5.3 11.3 8.0

ROEadjusted(1) 10.7 12.5 11.9

ROTE(Netattributableprofit/Averagetangibleequity) 6.7 15.2 10.7

ROTEadjusted(1) 13.5 16.8 16.0

ROA(Netincome/Averagetotalassets) 0.46 0.83 0.61

ROAadjusted(1) 0.83 0.91 0.88

RORWA(Netincome/Averagerisk-weightedassets) 0.85 1.46 1.08

RORWAadjusted(1) 1.53 1.60 1.55

Efficiencyratio 47.4 48.5 48.4

Riskpremium 1.92 1.10 1.20

NPAratio 4.8 4.1 4.0

NPAcoverageratio 69 60 61

Capital adequacy ratios (%)

Corecapital 10.8 9.1 10.3

TierI 10.8 9.8 10.3

BISRatio 13.3 12.6 12.9

Other information

Numberofshares(millions) 5,382 11.6 4,825 4,903

Numberofshareholders 1,007,410 2.7 981,348 987,277

Numberofemployees(2) 117,475 6.2 110,625 110,645

Numberofbranches(2) 8,072 8.6 7,436 7,457

NumberofATMs(2) 20,181 10.9 18,192 18,794

General note: These quarterly statements have not been audited. The consolidated accounts of the BBVA Group have been drawn up according to the International Financial Reporting Standards (IFRS) adopted by the European Union and in conformity with Bank of Spain Circular 4/2004, together with the changes introduced therein.

(1)In2011,duringthefourthquarter,USgoodwillimparmentcharge.In2011and2012,impairmentchargerelatedtothedeteriorationoftherealestatesectorinSpain.Andinthethirdquarterof2012,impactofUnnimbadwill.

(2)ExcludingGaranti.

3Relevantevents

ThefollowingarethemostimportantfeaturesoftheBBVAGroup’

earningsinthethird quarter of 2012:

1. Intermsofsolvency, BBVAcomfortablypassedOliver

Wyman’sstresstestandcontinuestocomplywiththecapital

recommendationsoftheEuropeanBankingAuthority(EBA).

2. Positiveperformanceofrecurring revenue inallgeographical

regions.

3. ThishasenabledtheGrouptoabsorbagainasignificant

increaseinitsloan-loss provisionsinSpain,inordertocoverthe

ongoingimpairmentofitsrealestateportfoliosandassets.

4. TheGroupcontinuestostrengthenitsliquiditypositionthrough

comprehensivemanagementineachofthegeographicalareas

whereitoperates,whileimprovingitsfinancingstructure.

5. TheUnnimconsolidationonJuly27.

6. Maintenanceofthecurrentdividendpolicy.

Thesepointsarediscussedbelowinmoredetail.

1. BBVAcomfortablypassedOliverWyman’sstress test.

• Theresultsofthestress testconductedbyOliverWymanon

14Spanishbankinggroups(90%ofthebankingsystem)were

publishedonSeptember28th.Itfocusedonananalysisofthe

portfolioofloanstothedomesticprivatesector(including

foreclosedrealestateassets).Thisworkhasbeenadecisive

stepinrestoringmarketconfidenceinthesector.

• Thestudyenjoysahighlevelofcredibility,sincethe

Europeanauthoritieshavemonitoredtheprocessvery

closelyandagreedonthemethodologyused.Inaddition,the

dataprovidedbythebanksandtheBankofSpainhasbeen

reviewedbyexternalauditorsandindependentrealestate

appraisers.

• Thetheoreticalexerciseconsidersastress scenariothat

ismorenegativethantheoneusedinothercountries

(Portugal,IrelandandGreece),andevenmoreseverethan

theoneconductedinJunebytheInternationalMonetary

Fund(IMF)forSpain.

• Themainresults and conclusions are:

– Aggregatecapitalneedsforthefinancialindustryunder

averyadversescenarioamountto€53,700m(including

thetaxeffectandconsideringthemergerprocesses

underway).Therefore,ingeneraltermstherehavebeen

nomajorsurpriseswithrespecttotheresultsofthe

top-downexerciseconductedlastJune(between

€51,000mand€62,000m).Inaddition,theamountiswell

belowthe€100,000mthattheEuropeanUnionhasmade

availabletothesector.

– Eveninthemostadverseandhighlyunlikelyeconomic

scenario,sevenbankinggroups,whichaccountformore

than62%oftheloanportfolioanalyzed,havenocapital

needs.Inshort,thestudyoncemoreshowedthegreat

disparitywithintheSpanishfinancialsystem,withahard

coreofstrongbanksandvulnerabilitylimitedtoaspecific

partoftheindustry.Thiscleardistinctionwillmakeit

easiertospeeduptherestructuringofthesector.

– Asexpected,BBVAisoneofthebanksincludedinthe

groupwithnocapitalneeds.Itcomfortablypassedthe

stresstest,thankstoitsrecurringrevenueandsoundness

ofitsbusinessmodel.

• Infact,fromapracticalpointofview,attheendofthe

thirdquartertheBankcontinuestocomplywiththeEBA’s

recommendations.Asof30-Sep-2012BBVAmaintainedthe

coreratiopostedatthecloseofthefirsthalfoftheyearof

10.8%underBaselII.

2. Recurring revenuecontinuestoincrease,asshownbythe2.6%

growthingrossincomeinthequarter,excludingnettrading

income(NTI)anddividends.Theaverageannualgrowthrateis

14.0%.Themainreasonsforthiscontinuetobe:

• Strongactivityinemergingmarkets.

• Goodmanagementofspreadsinallregions.

• Positiveperformanceoftheinsurancebusiness.

3. TheabovehasenabledtheBanktoabsorbagainasignificant

increaseinloan-loss provisionsaimedatreflectingthe

impairmentofassetsrelatedtotheSpanishrealestatesector.So

farthisyear,theGrouphassetasideprovisionsof€2.9billion(€1.6

billioninthethirdquarter),includingbothloan-lossprovisions

andprovisionsforforeclosedandacquiredassetswithinthe

scopeofRoyalDecree-Laws02/2012and18/2012,thuscomplying

withtwo-thirdsoftheprovisionsrequiredintotalbybothRDL’s.

Aftermakingtheseprovisions,BBVApostedacumulativenet

attributableprofitof€1,656m(€146minthethirdquarter).

4. Comprehensiveliquiditymanagement,whichenablesthe

Grouptomaintainacomfortableposition.Thefollowingisworth

mentioninginthisregard:

• BBVAhassuccessfullycompletedseveralissuesofsenior

debtinEuropeandotherplacementsintheAmericas

(MexicoandPeru,amongothercountries)withasignificant

levelofdemand.

Groupinformation

Relevantevents

4 Groupinformation

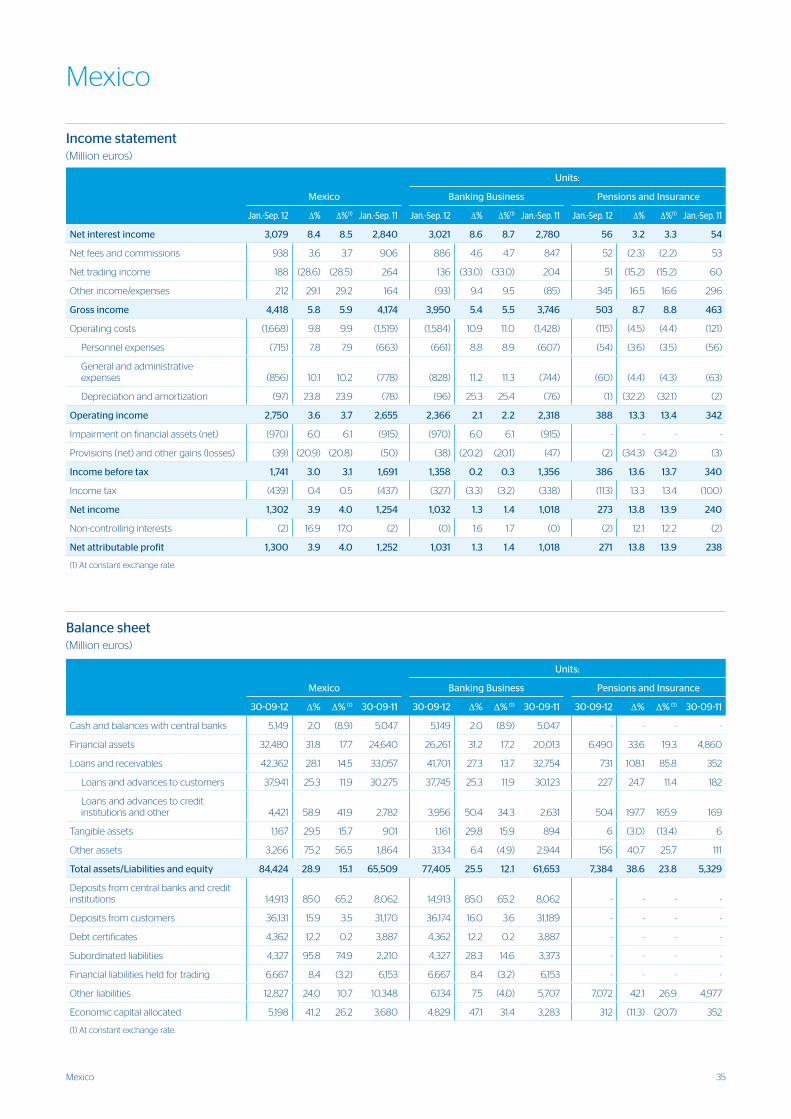

• Mexicomaintainsitssustainedgrowthinactivity,aboveallin

theretailportfolio.Commercialcampaignshavebeenlaunched

thatareboostingconsumerfinance,financeforsmallbusinesses

andthegatheringoflower-costliabilities,suchascurrentand

savingsaccounts.Asaresult,netinterestincomecontinuesto

performwell,andincreased8.5%overthelastyearatconstant

exchangerates.This,combinedwiththepositiveperformance

oftheinsurancebusiness,theyear-on-yearincreaseinoperating

expenses(atlevelssimilartothoseseeninpreviousquarters),

andthestabilityoftheriskpremium,ledtoacumulativenet

attributableprofitof€1,300m(up4.0%year-on-year,alsoat

constantexchangerates).

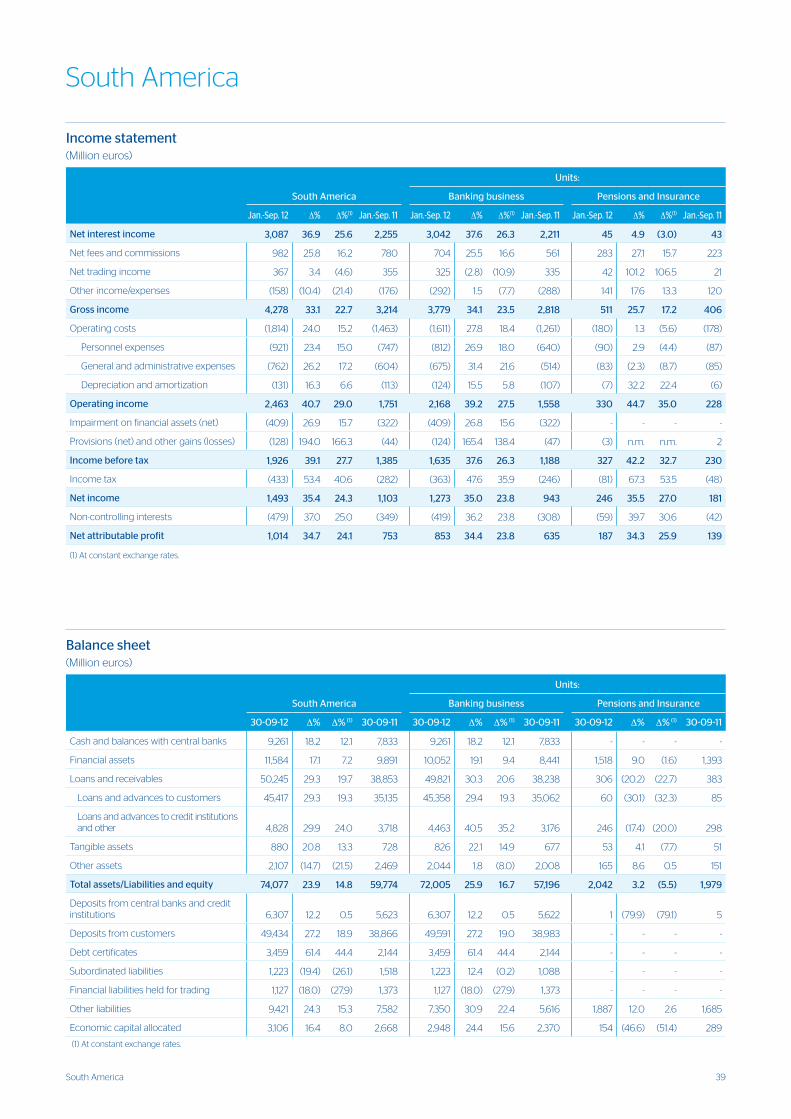

• South America enjoyedonceagainoutstandingperformance

inactivity,customerspreadsandassetquality.Asaresult,

theregionwasabletomaintainitsexpansionandgrowth

planswhilepostinga24.1%year-on-yearincrease(atconstant

exchangerates)incumulativenetattributableprofitto€1,014m.

• The United Statesmaintainsafavorabletrendinactivity,asset

quality,earningsandsolvency,verymuchsupportedonthe

localbusiness.TheloanbookofBBVACompassgrew4.5%

year-on-yearthankstothepositiveperformanceofthetarget

portfolios(residentialmortgagesup20.3%andcommercial

loansup25.5%),whilecustomerfundsincreased9.5%dueto

thegoodperformanceoflow-costfunds.Thedecreaseon

impairmentlossesonfinancialassetshashadaverypositive

impactonearningsandoffsettheflatperformanceofnet

interestincomeinthecurrentenvironmentoflowinterestrates

andarelativelyflatcurve.Asaresult,theareagenerateda

cumulativenetattributableprofitof€341m(up29.3%atconstant

exchangerates).

The economic background

Inthethirdquarterof2012,theworld economycontinuedto

runoutofsteam.Thiswastheresultofweaknessthathasbeen

particularlyclearintheeurozone.Butithasalsobeenapparent

thattheemergingeconomiesinAsiaandLatinAmericaare

notimmunetotheeffectsofthecontinuedfinancialtensionsin

theEuropeandebtmarketsandhavealsobegunamoderate

slowdown.However,theauthoritieshavereactedwiththeadoption

ofnewmonetarypolicymeasures(andinthecaseoftheeuro

zone,institutionalmeasures),whichshouldhelprestoremarket

confidenceintheeurozone.

ThemostrelevantactionshavetakenplaceinEurope. Following

theagreementsreachedattheEuropeansummitlastJune,major

stepshavebeentakentostrengthenthegovernanceofthe

EconomicandMonetaryUnion.Themeasuresadoptedinclude

theimplementationoftheEuropeanStabilityMechanism(ESM)

andprogressintheprocessthatwillleadtothecreationofasingle

Europeanbankingsupervisor.Butthemostdecisivemeasure

hasbeentheannouncementbytheECBofanewprogramfor

unlimitedpurchasesofsovereigndebtofthosecountriesthatopt

toaccessthesefunds,understrictconditionality.Thisinitiative

hascontributedtoeaseconcernsontheriskpremiumsofthe

peripheralcountriesandreducetailrisk.Overall,themeasures

explainedabove,inadditiontothosealreadyadoptedinJune,

representawindowofopportunityforresolvingthefinancialcrisis

• Growthincustomer deposits.Theincreasedproportionof

retaildepositsontheliabilitysideofthebalancesheetin

allthegeographicalareascontinuestoallowtheGroupto

improveitsfinancingstructure.

• ReductionintheCorporate & Investment Banking (CIB)

portfoliosinalldevelopedcountries.

• Improvementinavailablecollateral.

5.Theacquisitionof100%ofthecapitalstockofUnnimBanc,

S.A.wascompletedonJuly27,withaverylimitedimpact

onsolvencyandoncreditandliquidityrisks.Themain

effectsofitsincorporationintotheGroup’sfinancialstatements

are:

• Inclusionofanetworkwith556branchesand3,028

employeesthatmanage€18billionincustomerloansand

€11billionincustomerdeposits(dataasofthecloseof

September2012).

• Noimpactonliquidity,sinceahighpercentageofitsloan

bookiscollateralizableandithasabroadbaseofretail

deposits.

• CreditriskisstrictlylimitedbytheAssetProtectionScheme

(EPA)thatcoversitsmoreproblematicportfolios,andby

itshighNPAcoverageratio.However,itshighNPAratio

significantlyaffectsthatoftheGroup,adding53basispoints

tothefigureforthecloseofthefirsthalfof2012.

• Withrespecttosolvency,theimpactoftheincorporationof

Unnimispracticallyneutralintermsofcorecapital,asthe

increaseinrisk-weightedassetsisoffsetbythegenerationof

badwillfor€320m,andtheexchangeofhybridinstruments

heldbyUnnimretailcustomersforBBVAshares(thelatter

willimpactinOctober).

6. ThelevelofrecurringearningsenablestheGrouptocontinue

withthedividendpolicyapprovedatthelastGeneral

ShareholdersMeeting(AGM).InOctober2012,theamountof

€0.10persharewaspaidunderthe“dividend-option”scheme.

Around80%ofshareholdersoptedtoreceivenewlyissued

BBVAshares,whichoncemoreconfirmsthesuccessofthis

remunerationsystem.

Thefollowingisworthmentioningwithrespecttothebusiness

areas:

• Spain generatedacumulativeoperatingincomeof€2,972m,

6.2%uponthefigure12monthsearlier.Theincreaseininterest

incomeisoutstandingthankstogoodpricemanagement,

andthecontroloveroperatingexpenses.Loan-lossprovisions

haveincreasedsignificantlytooffsetthegradualimpairmentof

realestateportfoliosandassets.Asregardsactivity,themost

relevantaspectcontinuestobethefavorableperformanceof

on-balance-sheetcustomerfunds.

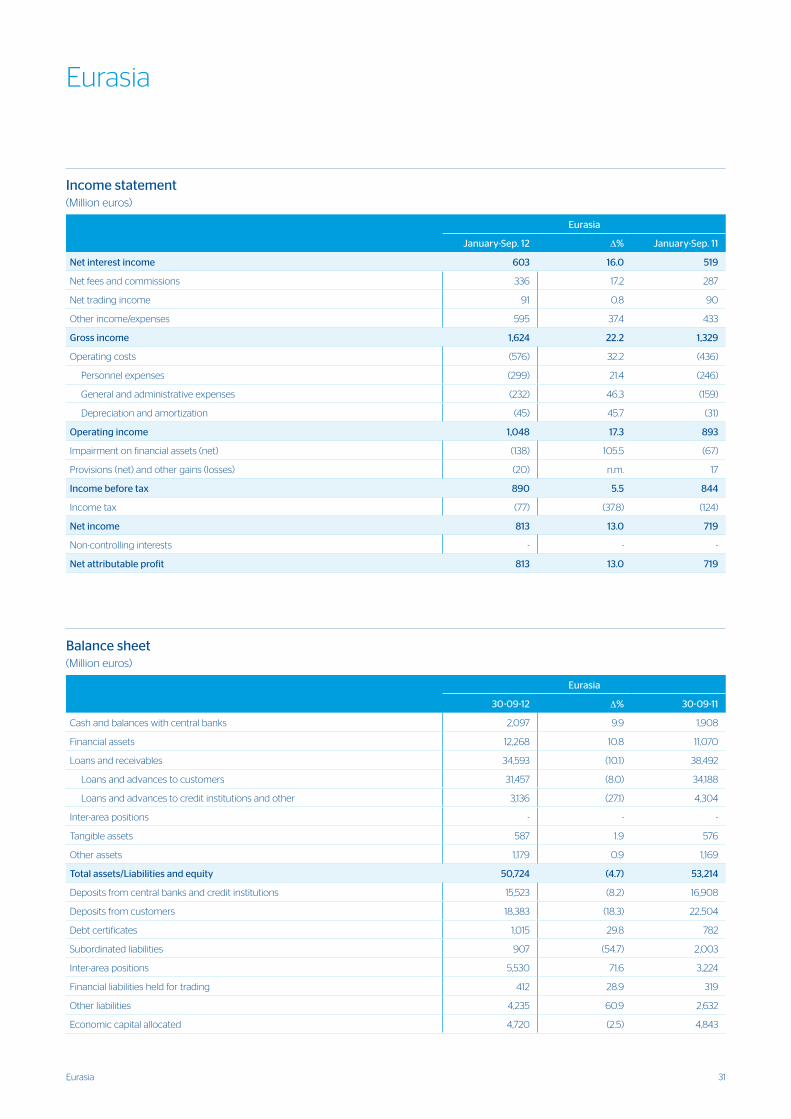

• Eurasia generatedacumulativeprofitof€813m(up13.0%

year-on-year)thankstothegoodperformanceofGarantiand

thegrowingcontributionofthestakeinChinaCiticBank(CNCB).

5Relevantevents

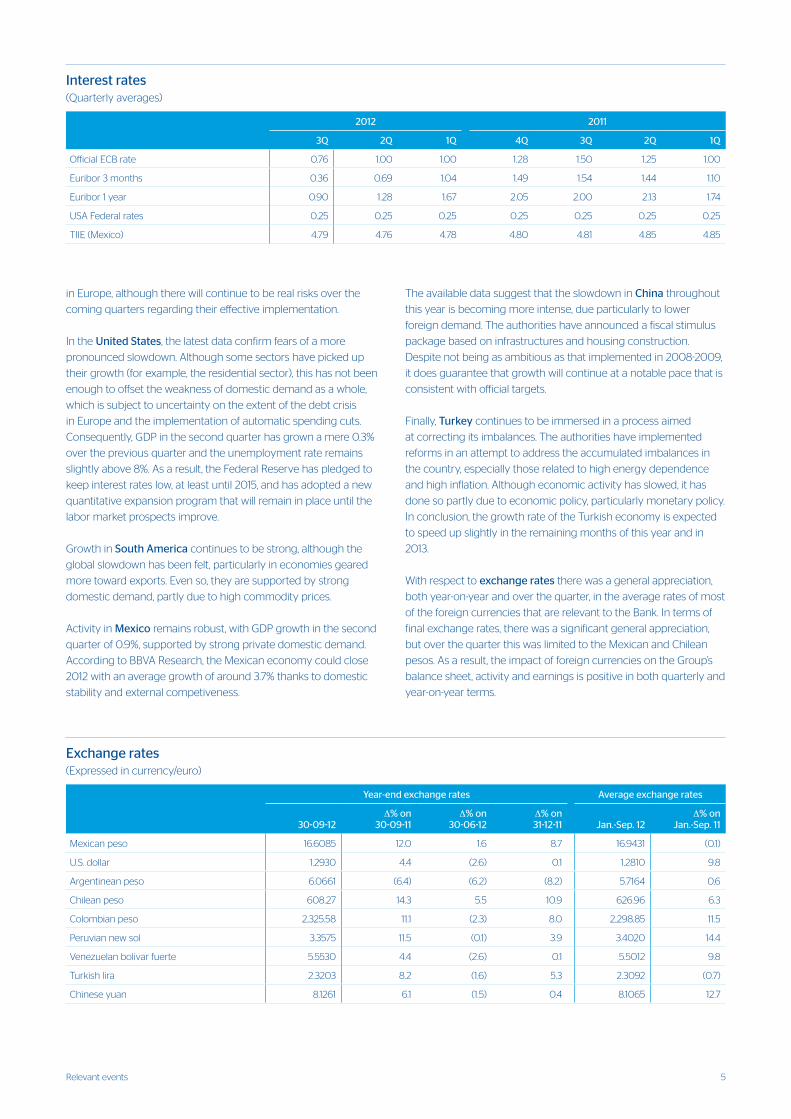

Interest rates (Quarterlyaverages)

2012 2011

3Q 2Q 1Q 4Q 3Q 2Q 1Q

OfficialECBrate 0.76 1.00 1.00 1.28 1.50 1.25 1.00

Euribor3months 0.36 0.69 1.04 1.49 1.54 1.44 1.10

Euribor1year 0.90 1.28 1.67 2.05 2.00 2.13 1.74

USAFederalrates 0.25 0.25 0.25 0.25 0.25 0.25 0.25

TIIE(Mexico) 4.79 4.76 4.78 4.80 4.81 4.85 4.85

TheavailabledatasuggestthattheslowdowninChinathroughout

thisyearisbecomingmoreintense,dueparticularlytolower

foreigndemand.Theauthoritieshaveannouncedafiscalstimulus

packagebasedoninfrastructuresandhousingconstruction.

Despitenotbeingasambitiousasthatimplementedin2008-2009,

itdoesguaranteethatgrowthwillcontinueatanotablepacethatis

consistentwithofficialtargets.

Finally,Turkeycontinuestobeimmersedinaprocessaimed

atcorrectingitsimbalances.Theauthoritieshaveimplemented

reformsinanattempttoaddresstheaccumulatedimbalancesin

thecountry,especiallythoserelatedtohighenergydependence

andhighinflation.Althougheconomicactivityhasslowed,ithas

donesopartlyduetoeconomicpolicy,particularlymonetarypolicy.

Inconclusion,thegrowthrateoftheTurkisheconomyisexpected

tospeedupslightlyintheremainingmonthsofthisyearandin

2013.

Withrespecttoexchange ratestherewasageneralappreciation,

bothyear-on-yearandoverthequarter,intheaverageratesofmost

oftheforeigncurrenciesthatarerelevanttotheBank.Intermsof

finalexchangerates,therewasasignificantgeneralappreciation,

butoverthequarterthiswaslimitedtotheMexicanandChilean

pesos.Asaresult,theimpactofforeigncurrenciesontheGroup’s

balancesheet,activityandearningsispositiveinbothquarterlyand

year-on-yearterms.

inEurope,althoughtherewillcontinuetoberealrisksoverthe

comingquartersregardingtheireffectiveimplementation.

IntheUnited States,thelatestdataconfirmfearsofamore

pronouncedslowdown.Althoughsomesectorshavepickedup

theirgrowth(forexample,theresidentialsector),thishasnotbeen

enoughtooffsettheweaknessofdomesticdemandasawhole,

whichissubjecttouncertaintyontheextentofthedebtcrisis

inEuropeandtheimplementationofautomaticspendingcuts.

Consequently,GDPinthesecondquarterhasgrownamere0.3%

overthepreviousquarterandtheunemploymentrateremains

slightlyabove8%.Asaresult,theFederalReservehaspledgedto

keepinterestrateslow,atleastuntil2015,andhasadoptedanew

quantitativeexpansionprogramthatwillremaininplaceuntilthe

labormarketprospectsimprove.

GrowthinSouth Americacontinuestobestrong,althoughthe

globalslowdownhasbeenfelt,particularlyineconomiesgeared

moretowardexports.Evenso,theyaresupportedbystrong

domesticdemand,partlyduetohighcommodityprices.

ActivityinMexicoremainsrobust,withGDPgrowthinthesecond

quarterof0.9%,supportedbystrongprivatedomesticdemand.

AccordingtoBBVAResearch,theMexicaneconomycouldclose

2012withanaveragegrowthofaround3.7%thankstodomestic

stabilityandexternalcompetiveness.

Exchange rates (Expressedincurrency/euro)

Year-end exchange rates Average exchange rates

30-09-12 ∆% on

30-09-11∆% on

30-06-12 ∆% on31-12-11 Jan.-Sep. 12

∆% on Jan.-Sep. 11

Mexicanpeso 16.6085 12.0 1.6 8.7 16.9431 (0.1)

U.S.dollar 1.2930 4.4 (2.6) 0.1 1.2810 9.8

Argentineanpeso 6.0661 (6.4) (6.2) (8.2) 5.7164 0.6

Chileanpeso 608.27 14.3 5.5 10.9 626.96 6.3

Colombianpeso 2,325.58 11.1 (2.3) 8.0 2,298.85 11.5

Peruviannewsol 3.3575 11.5 (0.1) 3.9 3.4020 14.4

Venezuelanbolivarfuerte 5.5530 4.4 (2.6) 0.1 5.5012 9.8

Turkishlira 2.3203 8.2 (1.6) 5.3 2.3092 (0.7)

Chineseyuan 8.1261 6.1 (1.5) 0.4 8.1065 12.7

6 Groupinformation

TheBBVAGroup’sincomestatementfor

thethird quarter of 2012continuesto

showahighlevelofrecurringrevenue,

whichhasenabledittoabsorbthe

impairmentonassetsrelatedtothereal

estatesectorinSpain.Inaddition,the

incorporationofUnnimhasgenerated

badwillof€320m.

TheGroup’squarterlyprofitstandsat

€146m,whichbringsthecumulative

figurethroughSeptember30,2012to

€1,656m.Excludingthechargeforthe

aforementionedimpairmentofassets

relatedtotherealestatesectorinSpain

andUnnim’sbadwill,theadjustednet

attributableprofitamountsto€971mover

Earnings

Consolidated income statement: quarterly evolution (Millioneuros)

2012 2011

3Q 2Q 1Q 4Q 3Q 2Q 1Q

Net interest income 3,880 3,744 3,597 3,485 3,286 3,215 3,175

Netfeesandcommissions 1,259 1,215 1,216 1,136 1,143 1,167 1,114

Nettradingincome 337 462 367 416 (25) 336 752

Dividendincome 35 311 27 230 50 259 23

Incomebytheequitymethod 172 178 193 207 150 123 121

Otheroperatingincomeandexpenses 13 51 47 42 22 62 79

Gross income 5,697 5,960 5,447 5,515 4,627 5,162 5,263

Operatingcosts (2,831) (2,688) (2,585) (2,652) (2,461) (2,479) (2,359)

Personnelexpenses (1,483) (1,429) (1,379) (1,404) (1,325) (1,306) (1,276)

Generalandadministrativeexpenses (1,086) (1,021) (974) (1,021) (920) (964) (887)

Depreciationandamortization (262) (238) (232) (227) (216) (208) (196)

Operating income 2,866 3,272 2,862 2,863 2,166 2,683 2,904

Impairmentonfinancialassets(net) (2,038) (2,182) (1,085) (1,337) (904) (962) (1,023)

Provisions(net) (197) (99) (131) (182) (94) (83) (150)

Othergains(losses) (561) (311) (222) (1,718) (166) (154) (71)

Income before tax 69 680 1,423 (375) 1,002 1,484 1,659

Incometax 236 (21) (250) 368 (95) (189) (369)

Net income 305 659 1,173 (7) 907 1,295 1,290

Non-controllinginterests (159) (154) (168) (132) (103) (106) (141)

Net attributable profit 146 505 1,005 (139) 804 1,189 1,150

Adjusted(1) (825) (742) (122) (1,166) (173) (82) (80)

Net attributable profit (adjusted) (1) 971 1,247 1,127 1,026 978 1,271 1,229

Basic earnings per share (euros) 0.03 0.10 0.19 (0.03) 0.16 0.24 0.24

Basic earnings per share adjusted (euros) (1) 0.18 0.23 0.22 0.21 0.20 0.26 0.25

(1)In2011,duringthefourthquarter,USgoodwillimparmentcharge.In2011and2012,impairmentchargerelatedtothedeteriorationoftherealestatesectorinSpain.Andinthethirdquarterof2012,impactofUnnimbadwill.

Net attributable profit (1)

(Million euros)

(1) Adjusted.(2) At constant exchange rates: –6.1%.

971971

12471127

1026978

12711229

0

200

400

600

800

1,000

1,200

1,400

1Q 2Q 3Q 4Q 2Q

–3.8% (2)

2011 20121Q

3,478 3,345

971

1,1271,229 1,271

978 1,026

1,247

3Q

7Earnings

throughtherepricingofloansandgreater

contributionfrommortgagefloors.Allthis

againstabackdropoflowervolumes,asa

resultofthenecessarydeleveragingtaking

placeinthecountryandfallinginterestrates.

Overall,thisareageneratedcumulativenet

interestincomeof€3,571m,withariseof

8.0%comparedwiththefigureforthesame

periodin2011.

• Eurasiahaspostedstronggrowthinnet

interestincomeduetotheincorporationof

GarantionMarch22,2011.Likeforlike,this

headinggrew23%atGarantiBankthanks

tostrongactivitywithretailcustomersand

verygoodfiguresfromcustomerspreads,

particularlyduetothereducedcostof

liabilities.However,theCIBbusinessinthe

areashowsa28.3%dropinthislineowingto

fallingvolumes.AsofSeptember2012,the

netinterestincomecontributedbyEurasia

was16.0%higherthaninthesameperiodlast

year,totaling€603m.

thequarter,withacumulativefigurethrough

Septemberof€3,345m.

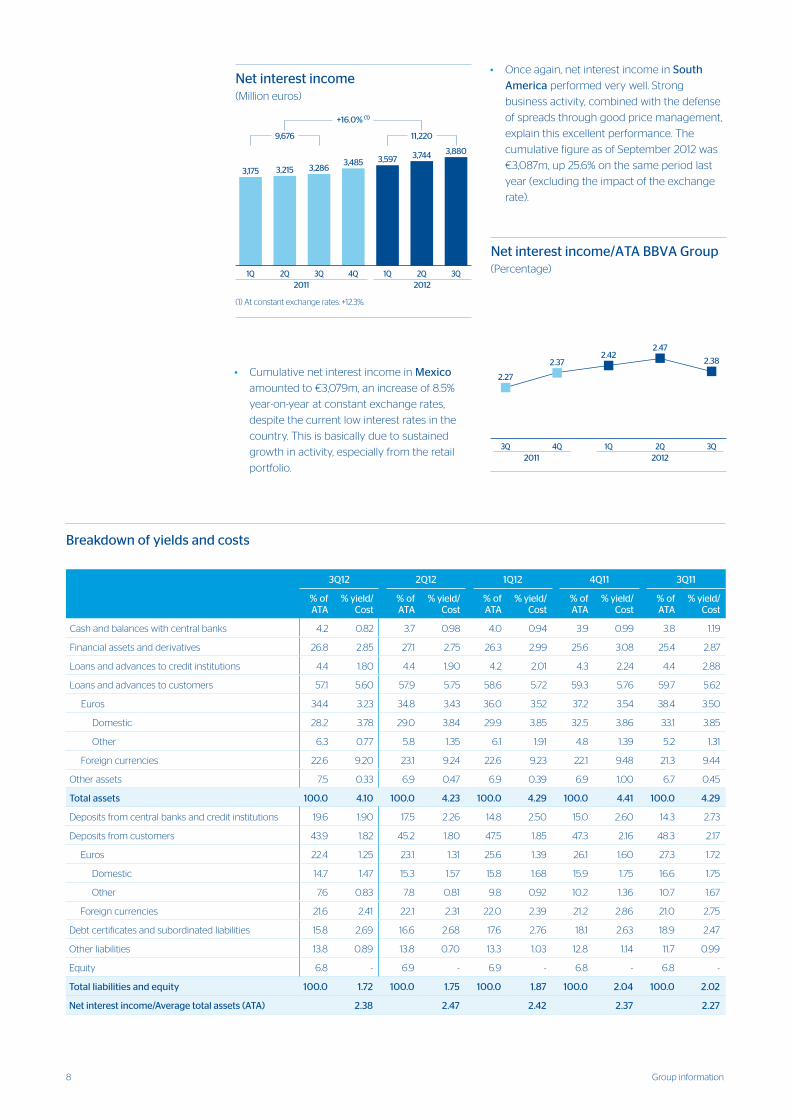

Net interest income

TheBBVAGroup’snet interest income

maintainedthegrowthpathstartedinthe

lastquarterof2010.Ittotaled€3,880minthe

thirdquarterof2012and€11,220mbetween

JanuaryandSeptember,up16.0%

year-on-year.Theincreaseisduetothe

defenseofcustomerspreadsinpractically

allthegeographicalareaswheretheBank

operates,strongactivityinemergingmarkets

andpositivemanagementofstructural

interest-rateriskinanenvironmentmarkedby

lowinterestrates.Bygeographicalarea,the

followingresultsareworthnoting:

• Spainhasrecordedasteadyincreasein

quarterlynetinterestincomesincetheendof

lastyear,thankstogoodpricemanagement

Consolidated income statement (Millioneuros)

January-Sep. 12 ∆%∆% at constant exchange rates January-Sep. 11

Net interest income 11,220 16.0 12.3 9,676

Netfeesandcommissions 3,690 7.8 4.5 3,424

Nettradingincome 1,167 9.8 5.9 1,063

Dividendincome 373 12.2 11.6 332

Incomebytheequitymethod 543 37.9 37.8 394

Otheroperatingincomeandexpenses 112 (31.6) (14.1) 163

Gross income 17,103 13.6 10.5 15,052

Operatingcosts (8,103) 11.0 7.9 (7,299)

Personnelexpenses (4,290) 9.8 6.8 (3,907)

Generalandadministrativeexpenses (3,081) 11.2 8.0 (2,771)

Depreciationandamortization (732) 17.9 13.8 (620)

Operating income 9,000 16.1 13.0 7,753

Impairmentonfinancialassets(net) (5,305) 83.6 80.0 (2,890)

Provisions(net) (427) 30.4 28.1 (328)

Othergains(losses) (1,095) 180.0 179.9 (391)

Income before tax 2,173 (47.6) (49.4) 4,145

Incometax (36) (94.5) (94.8) (652)

Net income 2,137 (38.8) (40.8) 3,492

Non-controllinginterests (481) 37.6 25.4 (349)

Net attributable profit 1,656 (47.3) (48.7) 3,143

Adjusted(1) (1,688) - - (335)

Net attributable profit (adjusted) (1) 3,345 (3.8) (6.1) 3,478

Basic earnings per share (euros) 0.32 0.64

Basic earnings per share adjusted (euros) (1) 0.63 0.71

(1)In2011,duringthefourthquarter,USgoodwillimparmentcharge.In2011and2012,impairmentchargerelatedtothedeteriorationoftherealestatesectorinSpain.Andinthethirdquarterof2012,impactofUnnimbadwill.

8 Groupinformation

Net interest income/ATA BBVA Group(Percentage)

3Q 4Q 3Q2011 2012

2.27

2.372.42

2.47

2.38

2

3

2.27

2.422.37

1Q

2.38

2Q

2.47

• Onceagain,netinterestincomeinSouth

Americaperformedverywell. Strong

businessactivity,combinedwiththedefense

ofspreadsthroughgoodpricemanagement,

explainthisexcellentperformance.The

cumulativefigureasofSeptember2012was

€3,087m,up25.6%onthesameperiodlast

year(excludingtheimpactoftheexchange

rate).

• CumulativenetinterestincomeinMexico

amountedto€3,079m,anincreaseof8.5%

year-on-yearatconstantexchangerates,

despitethecurrentlowinterestratesinthe

country.Thisisbasicallyduetosustained

growthinactivity,especiallyfromtheretail

portfolio.

Breakdown of yields and costs

3Q12 2Q12 1Q12 4Q11 3Q11

% of ATA

% yield/Cost

% of ATA

% yield/Cost

% of ATA

% yield/Cost

% of ATA

% yield/Cost

% of ATA

% yield/Cost

Cashandbalanceswithcentralbanks 4.2 0.82 3.7 0.98 4.0 0.94 3.9 0.99 3.8 1.19

Financialassetsandderivatives 26.8 2.85 27.1 2.75 26.3 2.99 25.6 3.08 25.4 2.87

Loansandadvancestocreditinstitutions 4.4 1.80 4.4 1.90 4.2 2.01 4.3 2.24 4.4 2.88

Loansandadvancestocustomers 57.1 5.60 57.9 5.75 58.6 5.72 59.3 5.76 59.7 5.62

Euros 34.4 3.23 34.8 3.43 36.0 3.52 37.2 3.54 38.4 3.50

Domestic 28.2 3.78 29.0 3.84 29.9 3.85 32.5 3.86 33.1 3.85

Other 6.3 0.77 5.8 1.35 6.1 1.91 4.8 1.39 5.2 1.31

Foreigncurrencies 22.6 9.20 23.1 9.24 22.6 9.23 22.1 9.48 21.3 9.44

Otherassets 7.5 0.33 6.9 0.47 6.9 0.39 6.9 1.00 6.7 0.45

Total assets 100.0 4.10 100.0 4.23 100.0 4.29 100.0 4.41 100.0 4.29

Depositsfromcentralbanksandcreditinstitutions 19.6 1.90 17.5 2.26 14.8 2.50 15.0 2.60 14.3 2.73

Depositsfromcustomers 43.9 1.82 45.2 1.80 47.5 1.85 47.3 2.16 48.3 2.17

Euros 22.4 1.25 23.1 1.31 25.6 1.39 26.1 1.60 27.3 1.72

Domestic 14.7 1.47 15.3 1.57 15.8 1.68 15.9 1.75 16.6 1.75

Other 7.6 0.83 7.8 0.81 9.8 0.92 10.2 1.36 10.7 1.67

Foreigncurrencies 21.6 2.41 22.1 2.31 22.0 2.39 21.2 2.86 21.0 2.75

Debtcertificatesandsubordinatedliabilities 15.8 2.69 16.6 2.68 17.6 2.76 18.1 2.63 18.9 2.47

Otherliabilities 13.8 0.89 13.8 0.70 13.3 1.03 12.8 1.14 11.7 0.99

Equity 6.8 - 6.9 - 6.9 - 6.8 - 6.8 -

Total liabilities and equity 100.0 1.72 100.0 1.75 100.0 1.87 100.0 2.04 100.0 2.02

Net interest income/Average total assets (ATA) 2.38 2.47 2.42 2.37 2.27

Net interest income(Million euros)

38803880374435973485328632153175

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

(1) At constant exchange rates: +12.3%.

1Q 2Q 3Q 4Q 2Q

+16.0% (1)

2011 20121Q

9,676 11,220

3,8803,597

3,175 3,215 3,2863,485

3,744

3Q

9Earnings

€1,167m.NTIwassignificantlyaffectedbya

particularlyweakthirdquarterof2011,when

amidaworseningdebtcrisistherewasan

exceptionallossofassetvalues,inaddition

toreducedbusinessactivityandthelackof

earningsfromportfoliosales.

Revenuefromdividendsamountedto€373m,

12.2%uponthefigure12monthsearlier.This

headingbasicallyincludestheremuneration

fromtheGroup’sstakeinTelefónicaand,toa

lesserextent,thedividendscollectedinthe

GlobalMarketsunit.

Income by the equity method totaled

€543m,up37.9%year-on-year.Practically

allofthisamountcomesfromthestakein

CNCB.

Finally,theother operating income and expenses headingfellby31.6%to€112m.

Thepositiveperformanceoftheinsurance

businessfailedtooffsettheincreased

allocationstothevariousdeposit

guaranteefundsinthecountrieswhereBBVA

operates.

Overall,inthefirstninemonthsof2012the

Groupgeneratedgross incomeof€17,103m,

up13.6%year-on-year,boostedmainlyby

recurringrevenue.Grossincomeexcluding

NTIanddividendsreached€15,564m,up

14.0%overtheprevious12months.This

increaseisparticularlysignificantgiven

thecontextinwhichitwasgenerated.

ItissupportedbytheGroup’sbalanced

geographicaldiversificationbetween

emerginganddevelopedmarkets,andonits

customer-centricbusinessmodel.

• IntheUnited States,netinterestincome

continuedtobenegativelyaffectedbythe

Guarantyrun-off,lowerbusinessvolumein

CIB,write-downsinsecuritiesportfoliosand

thecurrentenvironmentoflowinterestrates

withapracticallyflatcurve.Ontheotherhand,

theincreaseinloanvolumesandthe

year-on-yearreductioninthecostofdeposits

hadapositiveimpact.Asaresult,overthe

quarterthisheadingremainedatthelevelof

previousquarters,totaling€1,285mforthe

year,down3.6%year-on-yearatconstant

exchangerates.

Gross income

TheGroup’sincome from fees and commissionsfortheperiodJanuary-

September2012totaled€3,690m,picking

uptheiryear-on-yeargrowthrateto7.8%

(comparedwith6.6%inthefirsthalfof2012).

Strongactivityinemergingmarketsandthe

greatercontributionofGarantithisyearamply

offsetthenegativeimpactsfromsluggish

activityinSpainandtheregulatorychanges

implementedinsomeoftheareaswherethe

Bankoperates.Bybusinessarea,thisheading

remainedstableintheeurozone.InMexico,

revenuefromcreditcardsandthepensions

businessincreased.InTurkey,strongactivity

practicallyoffsetsnegativeregulatoryeffects.

IntheUnitedStatestheyfell,basicallyas

aresultofregulatorypressures.InSouth

Americatheygrew,inlinewiththestrong

activitymentionedabove.

NTIgeneratedinthefirstninemonthsof

2012increasedby9.8%year-on-yearto

Gross income net of NTI and dividends(Million euros)

53245324518850534869460245664488

0

1,000

2,000

3,000

4,000

5,000

6,000

(1) At constant exchange rates: +12.5%.

1Q 2Q 3Q 4Q 2Q

+14.0% (1)

2011 20121Q

13,657 15,564

5,3245,053

4,488 4,566 4,6024,869

5,188

3Q

Gross income(Million euros)

569756975960

54475515

462751625263

0

1,000

2,000

3,000

4,000

5,000

6,000

(1) At constant exchange rates: +10.5%.

1Q 2Q 3Q 4Q 2Q

+13.6% (1)

2011 20121Q

15,052 17,103

5,6975,4475,263 5,1624,627

5,5155,960

3Q

10 Groupinformation

Operating income

Themostsignificantaspectofoperating

expensescontinuestobetheirstrictcontrol

indevelopedcountriesandtheirgrowth

inemergingareas,inlinewiththefigures

mentionedinpreviousquarters.Inthe

cumulativefigurethroughSeptember2012,

thisheadingtotaled€8,103m,11.0%up

year-on-year,wellbelowtheincreasein

revenue.Asaresult:

• Therewasanimprovementoftheefficiency

ratioonthefigureforthesameperiodin2011

to47.4%attheendofSeptember.

Breakdown of operating costs and efficiency calculation (Millioneuros)

January-Sep. 12 ∆% January-Sep. 11 2011

Personnel expenses 4,290 9.8 3,907 5,311

Wagesandsalaries 3,302 9.9 3,003 4,122

Employeewelfareexpenses 632 11.5 567 758

Trainingexpensesandother 356 5.7 337 431

General and administrative expenses 3,081 11.2 2,771 3,793

Premises 693 9.4 633 849

IT 557 20.4 462 662

Communications 253 13.9 223 299

Advertisingandpublicity 282 4.1 271 378

Corporateexpenses 73 (5.8) 77 106

Otherexpenses 909 9.6 829 1,140

Leviesandtaxes 314 14.1 276 359

Administration costs 7,372 10.4 6,678 9,104

Depreciation and amortization 732 17.9 620 847

Operating costs 8,103 11.0 7,299 9,951

Gross income 17,103 13.6 15,052 20,566

Efficiency ratio (Operating costs/Gross income, in %) 47.4 48.5 48.4

48,5 48,4 47,4

10

15

20

25

30

35

40

45

50

17103

-8103

20566

-9951

15052

-7299-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

15,052

20,56617,103

7,2999,951

8,103

Jan.-Sep.2011

Jan.-Sep.2012

2011

48.5 48.4 47.4

Jan.-Sep.2011

Jan.-Sep.2012

2011

Efficiency

Grossincome

Operatingcost

(Percentage)

Efficiency ratio

(Million euros)

Operating income(Million euros)

28662866

3272

28622863

2166

26832904

0

500

1,000

1,500

2,000

2,500

3,000

3,500

(1) At constant exchange rates: +13.0%.

1Q 2Q 3Q 4Q 2Q

+16.1% (1)

2011 20121Q

7,753 9,000

2,8662,8622,9042,683

2,166

2,863

3,272

3Q

Operating costs(Million euros)

28312831268825852652

246124792359

0

500

1,000

1,500

2,000

2,500

3,000

(1) At constant exchange rates: +7.9%.

1Q 2Q 3Q 4Q 2Q

+11.0% (1)

2011 20121Q

7,299 8,103

2,8312,585

2,359 2,479 2,4612,652 2,688

3Q

11Earnings

Provisions and others

Thestronggenerationofoperatingincome

hasenabledtheGrouptoabsorbasignificant

increaseinitsloan-lossprovisionsinSpainin

ordertocovertheongoingimpairmentofits

realestateportfoliosandassets.Impairment losses on financial assetstoSeptember

totaled€5,305m,up83.6%onthefigure

recorded12monthsearlier.

Provisionsinthesameperiodamountedto

–€427m(–€328m12monthsearlier).They

basicallycoverearlyretirementcostsand,

toalesserextent,transferstoprovisionsfor

contingentliabilities,allocationstopension

fundsandothercommitmentswiththestaff.

Theother gains (losses)headingnearly

tripledbetweenJanuaryandSeptember2012

comparedwiththeamountreportedforthe

sameperiodin2011,atanegative€1,095m.This

headingincludesprovisionsmadeforrealestate

andforeclosedandacquiredassetsinSpainand

thebadwillgeneratedbytheUnnimdeal.

Number of employees (1)

29132 28934

32042

35538 3595039383

30690 30724 31277

12991 12798 12543

2274 2239 2230

sep 2011 dic 2011 sep 20120

20,000

40,000

60,000

80,000

100,000

120,000110,625

September2011

29,132

35,538

30,690

12,991

110,645

December2011

28,934

35,950

30,724

12,798

(1) Excluding Garanti.(2) Including Unnim Group.

117,475

September2012

32,042

39,383

31,277

12,543

Spain (2)

Mexico

South America

The United States

Rest of the world

Impairment losses on financial assets(Million euros)

203820382182

1085

1337

9049621023

0

500

1,000

1,500

2,000

2,500

(1) At constant exchange rates: +80.0%.

1Q 2Q 3Q 4Q 2Q

+83.6% (1)

2011 20121Q

2,890 5,305

2,038

1,0851,023 962 904

1,337

2,182

3Q

Number of branches (1)

3,018,0 3,016,0

3,572,0

1,999,0 1,999,0 2,014,0

1,545,0 1,567,0 1,621,0

745,0 746,0 745,0

129,0 129,0 121,0

sep-11 dic-11 sep-120

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

7,436

September2011

3,018

1,999

1,545

745

7,457

December2011

3,016

1,999

1,567

746

8,072

September2012

3,572

2,014

1,621

744

(1) Excluding Garanti.(2) Including Unnim Group.

Spain (2)

Mexico

South America

The United States

Rest of the world

Number of ATMs (1)

5,258,05,283,0

6,023,0

7,293,07,710,0

7,831,0

4,540,0 4,682,0 5,210,0

1,101,0 1,119,0 1,118,0

sep-11 dic-11 sep-120

5,000

10,000

15,000

20,000

25,00020,181

September2012

6,023

7,831

5,210

1,117

18,192

September2011

5,258

7,293

4,540

1,101

18,794

December2011

5,283

7,710

4,682

1,119

(1) Excluding Garanti.(2) Including Unnim Group.

Spain (2)

Mexico

South America

The United States

• TheBankmaintaineditsleadershippositionin

efficiencyamongitspeergroup.

• Cumulativeoperating incomeamountedto

€9,000m,16.1%uponthefigureforthefirst

ninemonthsof2011.

BBVAclosedSeptemberwith117,475

employees,3,028oftheminUnnim.

ExcludingtheincorporationofUnnim,

thefigureincreasedlastyearby3,822,

mainlyinMexicoandtoalesserextent

inSouthAmerica,andfellintheUnited

StatesandSpain.Thenumberofbranches,

whichstoodat8,072asof30-Sep-2012,

includes556Unnimbranches.Excluding

these,theincreaseisalsoconcentratedin

SouthAmericaandMexico.Finally,ATMs amountedto 20,181,andreflectedthesame

trendasthenumberforemployeesand

branches.Thefigureincludes715Unnim

ATMs,andtheincreasecontinuedtobe

concentratedbasicallyinthecountriesof

LatinAmerica.

12 Groupinformation

Finally,earningspershare(EPS)between

JanuaryandSeptember2012were€0.32

(€0.63adjustedEPS);returnontotalaverage

assets(ROA)0.46%(0.83%adjusted);return

onequity(ROE)5.3%(10.7%adjusted);and

returnonequityexcludinggoodwill(ROTE)

6.7%(13.5%adjusted).

Inconclusion,addingtheprovisionsmadeto

covertheimpairmentoftheassetsrelated

totherealestatesectorinSpain(accounted

bothasimpairmentlossesonfinancialassets

andothergains(losses)),thetotalamount

chargedbyBBVAyeartodatetotals€2.9

billion(€1.6billioninthethirdquarter).

Finally,asinthelastquarter,thelevelof

income taxwaslowforthesamereasons

mentionedthen:revenuewithlowornotax

rate(mainlydividendsandincomebythe

equitymethod)andthegrowingweightof

theearningsfromMexico,SouthAmericaand

Turkey,whereeffectivetaxratesarelow.

Net attributable profit

Thenetattributableprofitforthequarter

was€146m,whilethecumulativefigure

throughSeptemberstandsat€1,656m.

Excludingthechargefortheimpairmenton

theassetsrelatedtotherealestatesector

inSpainandthebadwillgeneratedbythe

incorporationofUnnim,theadjustednet

attributableprofitamountsto€971moverthe

quarter,withayeartodatefigureof€3,345m.

Tosumup,theBBVAGroupcontinuesto

generatesoundearningsdespitethedifficult

environment.

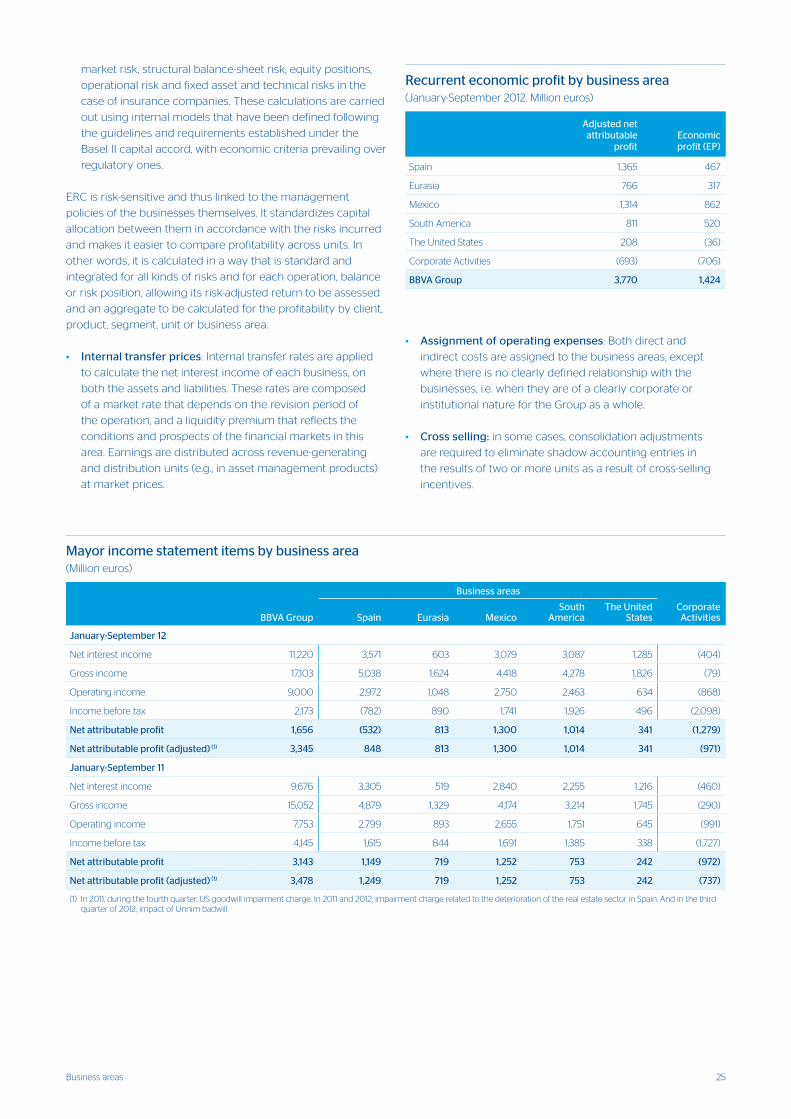

Bybusiness areas,Spainposteda€532m

loss.Excludingthechargefortheimpairment

ofrealestateassets,theareagenerated

cumulativeadjustedearningsthrough

Septemberof€848m.Eurasiagenerated

€813m,Mexico€1,300m,SouthAmerica

€1,014mandtheUnitedStates€341m.

Earnings per share (1)

(Euros)

0.180.18

0.230.220.210.20

0.260.25

0.00

0.05

0.10

0.15

0.20

0.25

0.30

(1) Adjusted.

1Q 2Q 3Q 4Q 2Q

–11.4%

2011 20121Q

0.71 0.63

0.18

0.22

0.25 0.26

0.20 0.210.23

3Q

Loan-loss and real estate provisions (1)

(Million euros)

(1) Includes total loan-loss provisions, and foreclosed and/or asset purchases in Spain.(2) Includes loan-loss provisions and provisions related to foreclosed and asset purchases within the scope of the

Royal Decree-Laws 02/2012 and 18/2012 (RD).

10431136

1404

1276

175 174

1060

1635

0

500

1000

1500

2000

2500

3000

Otherloan-loss

provisions

Provisionswithin thescope ofthe RD (2)

Quarterly average2011

2Q2012

1Q 3Q

1,297

1,123

174

1,236

1,061

175

2,394

1,334

1,060

2,888

1,253

1,635

ROA (1)

(Percentage)

0.91 0.880.83

0.0

1.5

0.91 0.880.83

(1) Adjusted.

January-Sep.2011

2011 January-Sep.2012

ROE (1) and ROTE (1)

(Percentage)

January-Sep.2011

2011 January-Sep.2012

16.816.0

13.512.5

11.910.7

0

10

20

12.511.9

10.7

(1) Adjusted.

ROE

ROTE

16.816.0

13.5

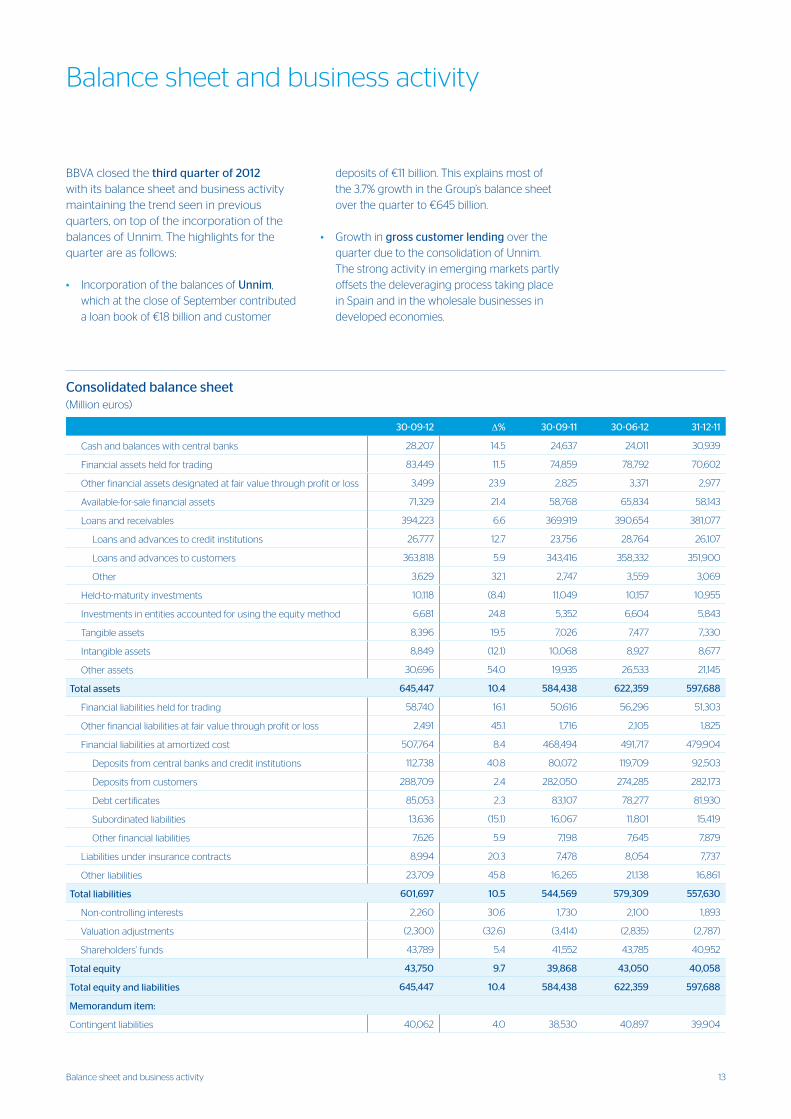

13Balancesheetandbusinessactivity

BBVAclosedthethird quarter of 2012

withitsbalancesheetandbusinessactivity

maintainingthetrendseeninprevious

quarters,ontopoftheincorporationofthe

balancesofUnnim.Thehighlightsforthe

quarterareasfollows:

• IncorporationofthebalancesofUnnim,

whichatthecloseofSeptembercontributed

aloanbookof€18billionandcustomer

depositsof€11billion.Thisexplainsmostof

the3.7%growthintheGroup’sbalancesheet

overthequarterto€645billion.

• Growthingross customer lendingoverthe

quarterduetotheconsolidationofUnnim.

Thestrongactivityinemergingmarketspartly

offsetsthedeleveragingprocesstakingplace

inSpainandinthewholesalebusinessesin

developedeconomies.

Balancesheetandbusinessactivity

Consolidated balance sheet (Millioneuros)

30-09-12 ∆% 30-09-11 30-06-12 31-12-11

Cashandbalanceswithcentralbanks 28,207 14.5 24,637 24,011 30,939

Financialassetsheldfortrading 83,449 11.5 74,859 78,792 70,602

Otherfinancialassetsdesignatedatfairvaluethroughprofitorloss 3,499 23.9 2,825 3,371 2,977

Available-for-salefinancialassets 71,329 21.4 58,768 65,834 58,143

Loansandreceivables 394,223 6.6 369,919 390,654 381,077

Loansandadvancestocreditinstitutions 26,777 12.7 23,756 28,764 26,107

Loansandadvancestocustomers 363,818 5.9 343,416 358,332 351,900

Other 3,629 32.1 2,747 3,559 3,069

Held-to-maturityinvestments 10,118 (8.4) 11,049 10,157 10,955

Investmentsinentitiesaccountedforusingtheequitymethod 6,681 24.8 5,352 6,604 5,843

Tangibleassets 8,396 19.5 7,026 7,477 7,330

Intangibleassets 8,849 (12.1) 10,068 8,927 8,677

Otherassets 30,696 54.0 19,935 26,533 21,145

Total assets 645,447 10.4 584,438 622,359 597,688

Financialliabilitiesheldfortrading 58,740 16.1 50,616 56,296 51,303

Otherfinancialliabilitiesatfairvaluethroughprofitorloss 2,491 45.1 1,716 2,105 1,825

Financialliabilitiesatamortizedcost 507,764 8.4 468,494 491,717 479,904

Depositsfromcentralbanksandcreditinstitutions 112,738 40.8 80,072 119,709 92,503

Depositsfromcustomers 288,709 2.4 282,050 274,285 282,173

Debtcertificates 85,053 2.3 83,107 78,277 81,930

Subordinatedliabilities 13,636 (15.1) 16,067 11,801 15,419

Otherfinancialliabilities 7,626 5.9 7,198 7,645 7,879

Liabilitiesunderinsurancecontracts 8,994 20.3 7,478 8,054 7,737

Otherliabilities 23,709 45.8 16,265 21,138 16,861

Total liabilities 601,697 10.5 544,569 579,309 557,630

Non-controllinginterests 2,260 30.6 1,730 2,100 1,893

Valuationadjustments (2,300) (32.6) (3,414) (2,835) (2,787)

Shareholders’funds 43,789 5.4 41,552 43,785 40,952

Total equity 43,750 9.7 39,868 43,050 40,058

Total equity and liabilities 645,447 10.4 584,438 622,359 597,688

Memorandum item:

Contingentliabilities 40,062 4.0 38,530 40,897 39,904

14 Groupinformation

Customer lending (gross)(Billion euros)

353

September2011

343

September2010

377

September2012

(1) At constant exchange rates: +4.3%.

+7.0% (1)

377

353343

200

250

300

350

400

• Growthinon-balance-sheet customer

funds(customerdepositspluspromissory

notes)mainlyintheretailsegmentinallthe

geographicalareasinwhichBBVAoperates.

• Asaresult,theGroup’sliquidityposition

andfundingstructureimproved.Intheeuro

balancesheet,thecommercialgapwas

reducedby€9.6billionoverthequarter.

Loans and advances to customers

Atthecloseof30-Sep-2012,gross customer lending amountedto€377billion,up7.0%

year-on-yearand2.3%quarter-on-quarter.

ExcludingthebalancesfromUnnim,this

headinggrewmoderatelyovertheyearby

1.8%,butfellby2.6%overthequarter.

Bybusiness areas,thedisparitybetween

emerginganddevelopedcountriesseenin

previousquarterscontinued:

• InSpain, excludingUnnim,theloanbook

shrank(down6.1%year-on-yearanddown

5.5%quarter-on-quarter)inlinewiththe

necessaryprocessofdeleveraginginthe

economy.Includingthebalancesfromthe

Catalanbank,therewasariseof3.2%over

thelast12monthsand3.9%overthequarter.

• InEurasiathisheadingfellby7.7%onthe

figureatthecloseofSeptember2011and

4.6%onthecloseofJune2012,duetothe

reductionofthewholesalecustomer’sloan

portfolio.Retailloansgrewby4.9%overthe

last12monthsandremainatverysimilar

levelsto30-Jun-2012.Notableagainthis

quarterwasthepositiveperformance

ofbalancesfromTurkey,whichwereup

22.8%onthefigureforthesamedatelast

year.

• AttheendofSeptember2012,lendingin

Mexicowasupyear-on-yearby11.5%(up2.2%

Customer lending (Millioneuros)

30-09-12 ∆% 30-09-11 30-06-12 31-12-11

Domestic sector 198,583 3.8 191,330 193,358 192,442

Publicsector 27,614 5.8 26,096 27,501 25,509

Otherdomesticsectors 170,969 3.5 165,234 165,856 166,933

Securedloans 107,100 5.5 101,552 96,546 99,175

Commercialloans 5,176 (12.5) 5,918 5,671 6,620

Financialleases 4,413 (14.3) 5,151 4,542 4,955

Othertermloans 39,074 (7.1) 42,043 39,080 41,863

Creditcarddebtors 1,584 2.7 1,542 1,564 1,616

Otherdemandandmiscellaneousdebtors 2,497 (8.0) 2,713 4,178 2,939

Otherfinancialassets 11,125 76.2 6,314 14,276 9,766

Non-domestic sector 159,167 9.3 145,614 159,385 153,222

Securedloans 63,118 8.4 58,202 63,032 60,655

Otherloans 96,049 9.9 87,413 96,353 92,567

Non-performing loans 19,834 26.4 15,689 16,243 15,647

Domesticsector 15,137 35.7 11,156 11,531 11,042

Non-domesticsector 4,697 3.6 4,533 4,713 4,604

Customer lending (gross) 377,383 7.0 352,633 368,844 361,310

Loan-lossprovisions (13,565) 47.2 (9,217) (10,513) (9,410)

Customer lending (net) 363,818 5.9 343,416 358,332 351,900

15Balancesheetandbusinessactivity

overthequarter),stronglysupportedbythe

retailsegment.

• TherewasalsoasignificantriseinSouth America (up19%year-on-yearand3.9%

quarter-on-quarter).Onceagain,this

growthhasbeenleveragedontheprivate

individualssegment,thankstothepositive

performanceofconsumerlendingand

creditcards.

• Finally,intheUnited States,BBVACompass

isstillpostingsteadygrowthinlending,with

ayear-on-yeargrowthof4.5%(up10.5%

excludingnonperformingloans).Itisworth

notingthatloanstothecommercialand

residentialrealestatesegmentcontinueto

drivegrowthinthebank’slendingactivity.

Tosumup,thedomestic sector continues

tobeimmersedinadeleveragingprocess

andhasgrownasaconsequenceofthe

incorporationoftheUnnimbalances,while

thenon-domestic sectorhasincreasedby

9.3%sincethecloseofSeptember2011.

Non-performing loanstotaled€20billion

asof30-Sep-2012,ariseof26.4%inyear-on-

yeartermsand22.1%sinceJun-30-2012.As

canbeseenintheaccompanyingtablefor

customerlending,thisupwardtrendderives

fromthedomesticsectorandislargelydue

totheincorporationofUnnim,andtoalesser

extenttotheworseningNPAratiosinSpain,in

linewithexistingforecasts.Itisimportantto

highlightthefactthatUnnim’snon-performing

balanceshaveahighcoverageratioand

thattheconstructionrealestateportfolio,

foreclosedassetsandassetspurchasedby

theCatalanbankareguaranteedbyanasset

protectionscheme(EPA)covering80%ofreal

lossesintheseassets.

Customer funds

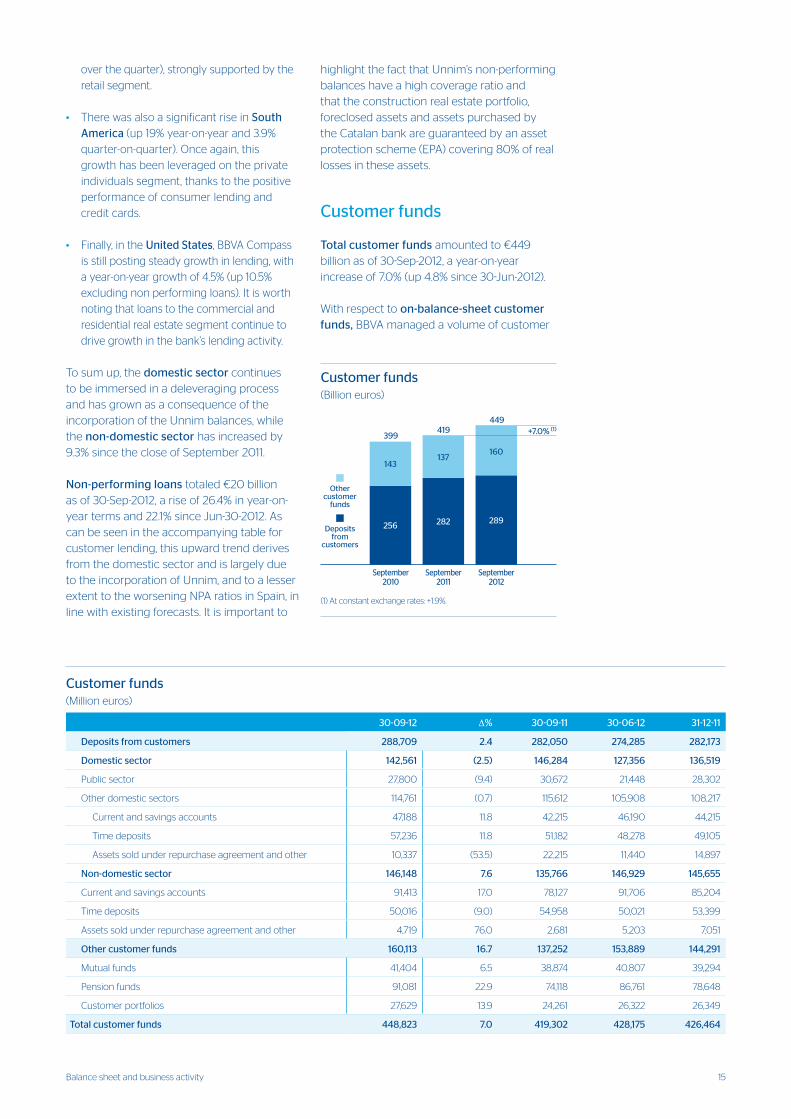

Total customer fundsamountedto€449

billionasof30-Sep-2012,ayear-on-year

increaseof7.0%(up4.8%since30-Jun-2012).

Withrespecttoon-balance-sheet customer funds,BBVAmanagedavolumeofcustomer

Customer funds (Millioneuros)

30-09-12 ∆% 30-09-11 30-06-12 31-12-11

Deposits from customers 288,709 2.4 282,050 274,285 282,173

Domestic sector 142,561 (2.5) 146,284 127,356 136,519

Publicsector 27,800 (9.4) 30,672 21,448 28,302

Otherdomesticsectors 114,761 (0.7) 115,612 105,908 108,217

Currentandsavingsaccounts 47,188 11.8 42,215 46,190 44,215

Timedeposits 57,236 11.8 51,182 48,278 49,105

Assetssoldunderrepurchaseagreementandother 10,337 (53.5) 22,215 11,440 14,897

Non-domestic sector 146,148 7.6 135,766 146,929 145,655

Currentandsavingsaccounts 91,413 17.0 78,127 91,706 85,204

Timedeposits 50,016 (9.0) 54,958 50,021 53,399

Assetssoldunderrepurchaseagreementandother 4,719 76.0 2,681 5,203 7,051

Other customer funds 160,113 16.7 137,252 153,889 144,291

Mutualfunds 41,404 6.5 38,874 40,807 39,294

Pensionfunds 91,081 22.9 74,118 86,761 78,648

Customerportfolios 27,629 13.9 24,261 26,322 26,349

Total customer funds 448,823 7.0 419,302 428,175 426,464

September2011

September2010

September2012

(1) At constant exchange rates: +1.9%.

143135

157

256

282 289

050100150200250300350400450

Customer funds(Billion euros)

Othercustomer

funds

Depositsfrom

customers

419399

449+7.0% (1)

137143

160

282256289

16 Groupinformation

deposits,excludingpromissorynotes,of

€289billionasof30-Sep-2012,up2.4%since

September2011and5.3%on

30-Jun-2012.Ascanbeseeninthe

accompanyingtableshowingcustomerfunds,

therehasbeenasignificantgrowthoverthe

quarterinthedomestic sectorasaresultof

theincorporationofUnnimandthegrowth

incustomerfunds(includingpromissory

notes)overthequarter.Inthenon-domestic sector,volumeshavebeenmaintainedatvery

similarlevelstothecloseofJune2012.The

fallindepositslinkedtowholesalecustomers

hasthusbeenoffsetbythepositivetrendin

balancesfromtheretailsegmentinpractically

allthegeographicalareas,asshownonthe

followingsectionsdedicatedtoeachofthe

Group’sbusinessareas.

Allinall,BBVAmaintainsintactitshigh

capacitytogatherdepositsandthe

capillarityofitscommercialnetwork,asretail

deposits(includingpromissorynotes)grew

inboththedomesticandnon-domestic

sectors.

Off-balance-sheetcustomerfundsclosed

Septemberat€160billion,up16.7%

year-on-yearand4.0%quarter-on-quarter.

Incontrastwithotherquarters,therewasa

slightyear-on-yearincreaseinSpain,dueto

thepositiveperformanceofpensionfunds

andcustomerportfolios.BBVAisthebiggest

pensionfundmanagerinSpainandtheonly

oneofthetopfivetoincreaseitsmarketshare

betweenJune2011andJune2012.Asof

30-Jun-2012,itsmarketsharewas19.1%,81

basispointshigherthanthefigureforthe

previousyear.

Inthenon-domesticsector,assetsunder

managementinmutualfundsandpensions

funds,aswellascustomerportfolios,have

continuedtogrow.

Equity

BBVA’sequityasof30-Sep-2012was

€43,750m,up1.6%quarter-on-quarterand

9.7%year-on-year.Thisismanlyexplained

bythepartialconversionofthemandatory

subordinatedconvertiblebonds,theretained

earningsoftheperiodandtheexchangerate

differences.

Other customer funds (Millioneuros)

30-09-12 ∆% 30-09-11 30-06-12 31-12-11

Spain 50,492 0.5 50,225 48,709 50,399

Mutualfunds 18,987 (6.1) 20,220 18,694 19,598

Pensionfunds 17,695 5.7 16,741 17,192 17,224

Individualpensionplans 10,075 5.0 9,600 9,729 9,930

Corporatepensionfunds 7,620 6.7 7,141 7,463 7,294

Customerportfolios 13,810 4.1 13,265 12,823 13,578

Rest of the world 109,622 26.0 87,027 105,180 93,892

Mutualfundsandinvestmentcompanies 22,417 20.2 18,654 22,113 19,697

Pensionfunds 73,386 27.9 57,377 69,569 61,424

Customerportfolios 13,819 25.7 10,996 13,499 12,771

Other customer funds 160,113 16.7 137,252 153,889 144,291

96.9

December2011

44.2

93.7

September2011

42.2

97.3

March2012

43.6

99.7

June2012

46.2

112.0

September2012

47.2

49.151.2 49.3 48.357.2

7.65.24.4

+19.5%

3.6

42.244.2 43.6 46.2

47.2

51.2 49.1 49.3 48.3

57.2

0.33.6 4.4 5.2 7.6

0

20

40

60

80

100

120

–x.x% (2)

On-balance sheet customer funds. Other domestic sectors (1)

(Billion euros)

(1) Including promissory notes sold by the retail network and excluding repos and other.

Timedeposits

Promissorynotes

Currentand savings

accounts

17Capitalbase

Themostsignificanteventsthatinfluencethe

Group’scapitalbaseinthethird quarter of

2012aresummarizedbelow:

• Asof30-Sep-2012theGroupcontinues

tocomplywiththeEBA’scapital

recommendations.

• Thegenerationofoperatingincome

hasenabledBBVAtoabsorbtheimpact

ofloan-lossprovisionstocoverthe

impairmentofassetsrelatedtothereal

estatesectorinSpain.

• Theincreaseinrisk-weightedassets(RWA),

derivedfromtheincorporationofUnnim

andthegrowthinLatinAmerica,hasbeen

compensatedtoagreatextentbythefall

oflendinginSpainandintheCIBportfolios

ofdevelopedcountries.

• TheimpactoftheincorporationofUnnim

ispracticallyneutralintermsofcorecapital.

Thenegativeeffectinthequarter(10basis

points)willbeoffsetbytheexchangeoffer

forthehybridinstrumentsheldbyUnnim

retailcustomersinthemonthofOctober.

• BBVAcomfortablypassedthestresstest

exerciseconductedbyOliverWyman.

Thisconfirmsonceagainitscapacityto

generatecapitaleveninveryadverse

economicscenarios.

AccordingtoBaselIIcriteria,theGroup’s

capital basestoodat€44,467mattheclose

ofSeptember,up3.8%onthefigurereported

attheendofJune2012,largelyduetothe

increaseinTierIIeligiblecapital.RWAtotaled

€335,203m.Theirincreaseoverthequarteris

basicallyduetotheincorporationofUnnim.

Withrespecttothecomponentsofthecapital

base,theevolutionofthecore capitalwas

veryflat,withaslightincreaseof€150msince

30-Jun-2012to€36,075m.Asaresult,thecore

andTierIratiosasof30-Sep-2012stoodat

10.8%,thesamelevelpostedattheendofthe

firsthalfof2012.

Inthesameperiod,othereligiblecapital

amountedto€1,552m,primarilyduetoBBVA

Bancomer’ssubordinateddebtissue.Asa

Capitalbase

Capital base (BIS II Regulation) (Millioneuros)

30-09-12 30-06-12 31-03-12 31-12-11 30-09-11

Core capital 36,075 35,924 35,290 34,161 29,628

Capital (Tier I) 36,075 35,924 35,290 34,161 32,053

Other eligible capital (Tier II) 8,393 6,841 8,241 8,609 9,067

Capital base 44,467 42,765 43,531 42,770 41,120

Risk-weighted assets 335,203 332,036 329,557 330,771 325,458

BIS ratio (%) 13.3 12.9 13.2 12.9 12.6

Core capital (%) 10.8 10.8 10.7 10.3 9.1

Tier I (%) 10.8 10.8 10.7 10.3 9.8

Tier II (%) 2.5 2.1 2.5 2.6 2.8

18737.0

23355.024929.0

29628.0

36075.0

0

5000

10000

15000

20000

25000

30000

35000

40000

Sep.2008

18,737

Sep.2009

Sep.2010

24,969

Sep.2011

29,628

Sep.2012

36,075

01234567891011121314151617181920

6.48.0 8.2

9.110.8

23,355

+21.8%

Core capital evolution (BIS IIRegulation) (Million euros and percentage)

Corecapital

Corecapital

(%)

18 Groupinformation

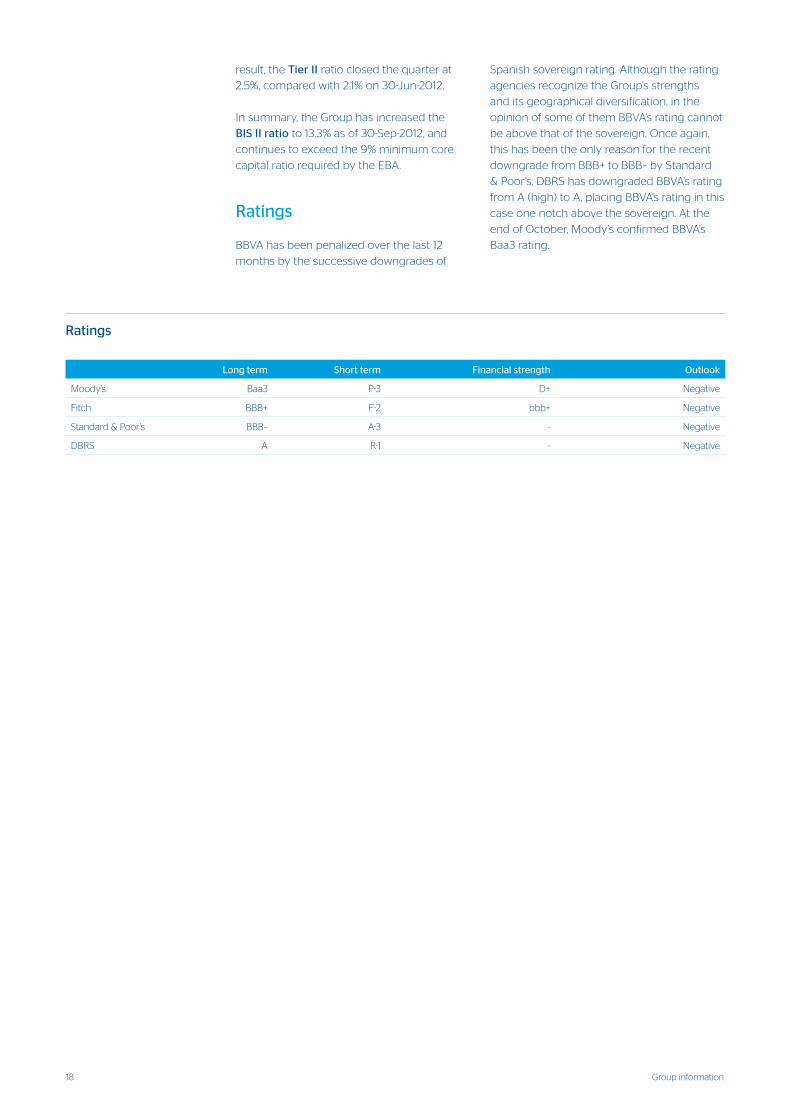

Ratings

Long term Short term Financial strength Outlook

Moody’s Baa3 P-3 D+ Negative

Fitch BBB+ F-2 bbb+ Negative

Standard&Poor’s BBB– A-3 - Negative

DBRS A R-1 - Negative

result,theTier IIratioclosedthequarterat

2.5%,comparedwith2.1%on30-Jun-2012.

Insummary,theGrouphasincreasedthe

BIS II ratioto13.3%asof30-Sep-2012,and

continuestoexceedthe9%minimumcore

capitalratiorequiredbytheEBA.

Ratings

BBVAhasbeenpenalizedoverthelast12

monthsbythesuccessivedowngradesof

Spanishsovereignrating.Althoughtherating

agenciesrecognizetheGroup’sstrengths

anditsgeographicaldiversification,inthe

opinionofsomeofthemBBVA’sratingcannot

beabovethatofthesovereign.Onceagain,

thishasbeentheonlyreasonfortherecent

downgradefromBBB+toBBB–byStandard

&Poor’s.DBRShasdowngradedBBVA’srating

fromA(high)toA,placingBBVA’sratinginthis

caseonenotchabovethesovereign.Atthe

endofOctober,Moody’sconfirmedBBVA’s

Baa3rating.

19Riskmanagement

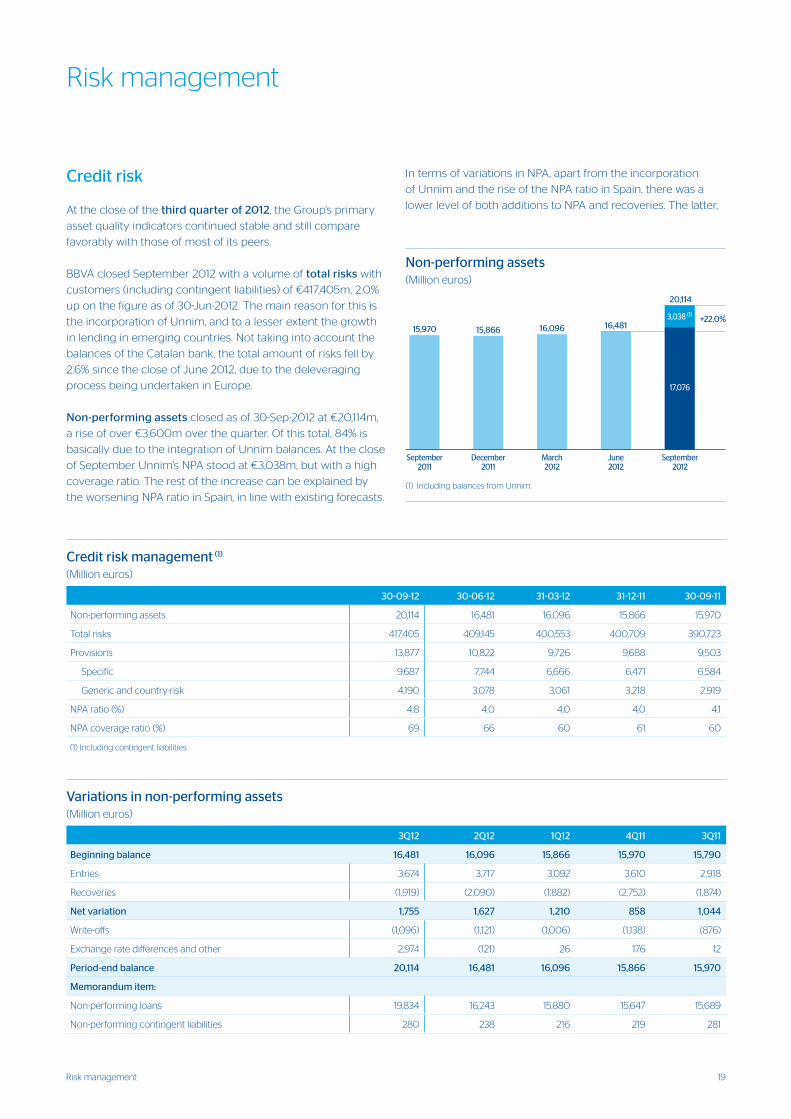

Credit risk

Atthecloseofthethird quarter of 2012,theGroup’sprimary

assetqualityindicatorscontinuedstableandstillcompare

favorablywiththoseofmostofitspeers.

BBVAclosedSeptember2012withavolumeoftotal riskswith

customers(includingcontingentliabilities)of€417,405m,2.0%

uponthefigureasof30-Jun-2012.Themainreasonforthisis

theincorporationofUnnim,andtoalesserextentthegrowth

inlendinginemergingcountries.Nottakingintoaccountthe

balancesoftheCatalanbank,thetotalamountofrisksfellby

2.6%sincethecloseofJune2012,duetothedeleveraging

processbeingundertakeninEurope.

Non-performing assetsclosedasof30-Sep-2012at€20,114m,

ariseofover€3,600moverthequarter.Ofthistotal,84%is

basicallyduetotheintegrationofUnnimbalances.Attheclose

ofSeptemberUnnim’sNPAstoodat€3,038m,butwithahigh

coverageratio.Therestoftheincreasecanbeexplainedby

theworseningNPAratioinSpain,inlinewithexistingforecasts.

IntermsofvariationsinNPA,apartfromtheincorporation

ofUnnimandtheriseoftheNPAratioinSpain,therewasa

lowerlevelofbothadditionstoNPAandrecoveries.Thelatter,

Riskmanagement

Variations in non-performing assets (Millioneuros)

3Q12 2Q12 1Q12 4Q11 3Q11

Beginning balance 16,481 16,096 15,866 15,970 15,790

Entries 3,674 3,717 3,092 3,610 2,918

Recoveries (1,919) (2,090) (1,882) (2,752) (1,874)

Net variation 1,755 1,627 1,210 858 1,044

Write-offs (1,096) (1,121) (1,006) (1,138) (876)

Exchangeratedifferencesandother 2,974 (121) 26 176 12

Period-end balance 20,114 16,481 16,096 15,866 15,970

Memorandum item:

Non-performingloans 19,834 16,243 15,880 15,647 15,689

Non-performingcontingentliabilities 280 238 216 219 281

Credit risk management (1) (Millioneuros)

30-09-12 30-06-12 31-03-12 31-12-11 30-09-11

Non-performingassets 20,114 16,481 16,096 15,866 15,970

Totalrisks 417,405 409,145 400,553 400,709 390,723

Provisions 13,877 10,822 9,726 9,688 9,503

Specific 9,687 7,744 6,666 6,471 6,584

Genericandcountry-risk 4,190 3,078 3,061 3,218 2,919

NPAratio(%) 4.8 4.0 4.0 4.0 4.1

NPAcoverageratio(%) 69 66 60 61 60

(1)Includingcontingentliabilities.

Non-performing assets(Million euros)

20,114

September2012

December2011

15,866

March2012

16,096

September2011

15,970+22.0%

16,481

June2012

(1) Including balances from Unnim.

3,038 (1)

17,076

20 Groupinformation

Asaresult,theGroup’scoverageratiohasimprovedby3.3

percentagepointsto69%.Bybusinessarea,Spain,theUnited

StatesandSouthAmericaincreasedtheirratiosto59%,94%

and142%,respectively,whileMexicoclosedthequarterat107%

andEurasiaat114%.

Exposure to the real estate sector in Spain

Themostimportantpointwithrespecttoexposuretothe

realestatesectorinSpaininthe third quarter of 2012is,as

mentionedearlier,theincreaseinprovisionstocoverthe

additionalimpairmentinthevalueofassetsassociatedwith

therealestateindustryowingtothecountry’sworsening

macroeconomicsituation.Followingtheincreaseinprovisions

forloan-losses,andforforeclosuresandassetspurchases,at

thecloseofthefirstninemonthsof2012theGroupmeets

two-thirdsoftherequirementsimposedbyRoyalDecree-Laws

02/2012and18/2012.

IncludingthefiguresfromUnnim,theGroup’sexposuretothis

sectorincreasesby€2,652m,butwithahighcoverageratio

(48%ofnon-performingplussubstandardloans).Foreclosures

andassetpurchasesamounttoanadditional€3,267m,

althoughtheyalsohaveahighcoverageratio(65%).

however,haveslowedinresponsetoseasonalfactorsaffecting

thisquarter,aboveallinSpain.Theratioofrecoveriesto

additionstoNPAstoodat52.2%.

Asaresult,theGroup’sNPA ratioattheendofSeptember2012

stoodat4.8%,up79basispointsoverthequarter.Ofthisrise,

53basispointsaretheresultoftheaforementionedintegration

ofUnnim.ExcludingtheCatalanbank,theratiowouldbe4.3%,

26pointsmorethanon30-Jun-2012,basicallyasaresultof

thedeteriorationoftheeconomicsituationinSpain,combined

withthefinancialdeleveragingprocessunderwayinthe

country.InMexico,theNPAratioremainsstable(4.1%atthe

endofSeptember),whileithasincreasedinEurasia,although

itcontinuesatverylowlevels(1.7%comparedwith1.4%inthe

previousquarter).IntheUnitedStates,itfellsignificantlyto

2.4%(2.8%asof30-Jun-2012).Finally,theratioinSouthAmerica

droppedslightlyfrom2.3%attheendofJune2012to2.2%at

thecloseofSeptember.

Coverage provisionsforcustomerriskincreasedoverthe

quarterby28.2%to€13,877m,mainlyduetoasignificant

increaseinprovisionsinSpainandtheincorporationofUnnim.

NPA ratio

Coverageratio

NPA and coverage ratios(Percentage)

September2012

December2011

March2012

June2012

September2011

60 61 60

66

4.1 4.0 4.0 4.0

69

4.8

(1) Excluding Unnim.

4.3 (1)

68 (1)

Recoveries over entries to NPA(Percentage)

64.2

76.2

60.956.2

52.2

3Q 4Q 3Q2011 2012

1Q 2Q

26,029,0 30,0

39,0

44,0 43,0

0

20

40

60

Coverage of NPLs and substandar real estatedeveloper’s exposure(Percentage)

September2012

December2011

March2012

June2012

September2011

2629 30

39

44

43 (1)

(1) Excluding Unnim.

Coverage of foreclosures and asset purchases(Percentage)

September2012

December2011

March2012

June2012

September2011

33 34 3436

50

33,0 34,0 34,036,0

50,0

44,0

0

20

40

60

Cobertura de adjudicados y compras (1)

(Porcentaje)

(1) Excluding Unnim.

44 (1)

21Riskmanagement

ItshouldbestressedthattheUnnimdealincludesanasset

protectionscheme(EPA)bywhichtheDepositGuarantee

Fund(FGD)willtakeon80%ofanylossesofapredetermined

assetportfolioforaperiodof10years,aftermakinguseof

existingprovisions.TheriskofincorporatingUnnimportfolios

totheBBVAGroupisthereforeextremelylimited,notonlydue

totheirhighcoverageratio,butalsobecauseoftheexistence

oftheEPA.

Asaresultoftheabove,therehasbeenanincreaseoverthe

quarterofthecoverageofnon-performingandsubstandard

loansoftheBBVAGroupof5percentagepointsto44%,and

thatofforeclosuresandassetpurchaseshasincreasedby14

percentagepointsto50%.

Economic capital

Attributable economic risk capital(ERC)consumption

amountedto€36,181masofthecloseofSeptember,an

increaseof9.2%onthefigurefor30-Jun-2012.

AsistobeexpectedfromBBVA’sprofile,thelargestallocation

toERC(56.8%)relatestocreditriskonportfoliosoriginatedin

theGroup’sbranchnetworkfromitsowncustomerbase.This

amountincreasedoverthequarterby9.6%,basicallydueto

theinclusionofUnnim.

Equityrisk,whichrefersbasicallytotheportfolioofholdings

inindustrialandfinancialcompanies,thestakeinCNCB,

andconsumptionofeconomiccapitalfromgoodwill,has

maintaineditsproportionstableinrelationtototalrisks

(20.0%).

Structuralbalance-sheet risk,originatedfromthe

managementofstructuralinterest-rateriskand

exchange-raterisk,accountsfor7.4%ofERC,andwasup13.3%

overthequarter.

Operational riskincreasedby5.0%inabsoluteterms,although

itreduceditsrelativeweightto5.6%;whilefixed-asset

riskincreasedby7.8%andaccountsfor6.4%oftotalERC

consumption.

Finally,therelativeweightofmarket risk,whichisofless

importancegiventhenatureofthebusinessandBBVA’spolicy

ofminimalproprietarytrading,stoodat2.8%atthecloseof

September.

Coverage of real estate exposure in Spain (Millionofeurosasof30-Sep-12)

Risk amount Provision % Coverage over risk

NPL+Substandard 8,746 3,826 44

NPL 6,842 3,196 47

Substandard 1,904 630 33

Foreclosedrealestateandotherassets 11,679 5,818 50

Fromrealestatedevelopers 8,650 4,648 54

Fromdwellings 2,406 917 38

Other 623 253 41

Subtotal 20,425 9,644 47

Performing 7,473 647 9

Withcollateral 6,850

Finishedproperties 4,082

Constructioninprogress 1,268

Land 1,500

Withoutcollateralandother 623

Real estate exposure 27,898 10,291 37

Memorandum item: BBVA Group excluding Unnim

NPL+Substandard 6,912 2,949 43

Foreclosedrealestateandotherassets 8,412 3,694 44

Subtotal 15,324 6,643 43

Performing 6,655 400 6

Real estate exposure 21,979 7,043 32

22 Groupinformation

TherewasastrongrecoveryintheEuropeanfinancialsectorover

thethird quarter of 2012. Therobustperformanceofperipheral

countrybanksintheequitymarketswasparticularlyoutstanding.

Therewereanumberoffactorsbehindthischange.Themost

importantoftheseincludetheannouncementsofasinglebank

supervisionmechanismintheeurozoneandanewprogramof

ECBsecondarymarketpurchases(OMT),subjecttoaprevious

request.RegardingSpain,aconditionalityagreementhasbeen

establishedtoaidthebankingsectorlinkedtothepublicationof

the“bottom-upstresstest”byOliverWyman.

ThesefactorsresultedinarevaluationoftheEuropean banking sector.TheStoxxBanksindexwentup11.2%inthequarter,

outperformingthegeneralStoxx50equitymarketindex(+5.8%).

Likewise,Spain’sIbex35rose8.5%betweenJuneandSeptember

2012,comparedtoan11.3%fallinthepreviousquarter.

BBVA’s results in the second quarter of 2012werefavorably

receivedbyanalysts.TheyparticularlyvaluedtheBank’sstrong

solvencylevels,assubsequentlyratifiedinOliverWyman’s

“bottom-upstresstest”,whichhighlightedthestrengthofthe

Bank’scapitalpositioneveninanextremelyadversescenario.By

businessarea,theperformanceofrevenueingeneral,andnet

interestincomeinparticular,wasalsowellreceived.InSpain,BBVA

wassetapartbyitssuperiorassetqualitycomparedtoitspeers.

DespiteconsideringthattheSpanishmacroeconomicconditions

willcontinuetoputpressureonthearea’searnings,analysts

consideredthatthestrengthandfavorableperformanceofthe

Group’sbusinessesinothergeographicareaswouldbesufficient

tooffsetthiseffectoverthecomingquarters.EarningsinSouth

Americasurprisedpositively,thankstoitshighrevenuegeneration

capacity.TheUSA,Turkey,Asiaand,toalesserextent,Mexicoalso

producedbetterthanexpectedresults.

Againstthisbackdrop,theBBVA sharegained8.6%overthe

quarterto€6.11pershare,resultinginamarketcapitalization

of€32,901m.Thisrepresentsaprice/bookvalueof0.8,aP/E

of15.6(calculatedontheaverageprofitfor2012estimatedby

theconsensusofBloomberganalysts)andadividendyieldof

6.9%(alsocalculatedaccordingtotheaveragedividendper

shareestimatedbyanalystsfor2012andthesharepriceasof

September30,2012).TheimprovementintheBBVAshareis

inlinewiththatoftheIbex35(+8.5%),butslightlybelowthe

performanceoftheEuropeansectorasawhole(StoxxBanks

+11.2%,andEuroStoxxBanks+12.8%).

Asregardsshareholder remuneration,BBVAmaintainedits

dividendpolicy.OnSeptember14itannouncedthedistributionof

€0.10pershareunderthe“dividendoption”flexibleremuneration

systemagreedattheAGMonMarch16,2012.Thisprogramoffers

shareholderstheoptiontoreceivethedividendinnewlyissued

BBVAsharesorincash.Around80%ofshareholdersoptedto

receivenewlyissuedBBVAshares,whichoncemoreconfirmsthe

sucessofthisnewremunerationsystem.

TheBBVAshare

The BBVA share and share performance ratios

30-09-12 30-06-12

Numberofshareholders 1,007,410 1,044,129

Numberofsharesissued 5,382,108,140 5,382,108,140

Dailyaveragenumberofsharestraded 90,201,068 71,780,925

Dailyaveragetrading(millioneuros) 516 371

Maximumprice(euros) 6.75 5.89

Minimumprice(euros) 4.31 4.52

Closingprice(euros) 6.11 5.63

Bookvaluepershare(euros) 8.13 8.00

Marketcapitalization(millioneuros) 32,901 30,296

Price/Bookvalue(times) 0.8 0.7

PER(Price/Earnings;times) 15.6 8.9

Yield(Dividend/Price;%) 6.9 7.5

Share price index(30-09-11=100)

31-12-11 31-03-1230-09-11 30-06-12 30-09-12

Stoxx 50

BBVA

Europe StoxxBanks

50

60

70

80

90

100

110

120

130

140

50

60

70

80

90

100

110

120

130

140

23Corporateresponsibility

ByrenewingitslistingontheDowJonesSustainability

Index(DJSI),BBVAhasmaintaineditspositionamongthe

leadingcompaniesintermsofsustainabilityatinternational

level.InclusionontheDJSIreflectsthesteadyintegrationof

theenvironmental,socialandcorporategovernance(ESG)

variablesintotheday-to-daymanagementoftheBank.

BBVAhasworkedtointegratetheseaspectsacrossitsvalue

chainforyears,fromproductdesign,advertisingandsales

toriskmanagement.BBVA’sfullratingintheanalysiscarried

outbytheSAMagencyforDJSIisavailableontheGroup’s

CorporateResponsibilitywebsite,www.bancaparatodos.com.

Belowarethecorporateresponsibilitymilestonesforthe

third quarter of 2012:

Financial InclusionBBVABancomerwillpromoteaccesstobankingfor1.5

millionusersthroughthe Dinero móvil(Mobilemoney)

initiative,whichenablespeopletosendmoneytoothers

inanypartofthecountrythroughtheelectronicbanking

channeloftheirchoice.Theaimoftheprojectistomake

iteasierforcustomerstoaccesslow-costbankingservices

thataresecure,approachable,accessible,time-savingand

convenient.

Financial LiteracyFiguresforthethirdValores de futuro(Futurevalues)

campaignwerepublishedinJuly.Itclosedattheendofthe

schoolyearwitharound800,000participantsinSpain.In

Mexico,BBVABancomerhasreachedanagreementwiththe

NationalAdultEducationInstitute(INEA)tofosterfinancial

literacyinthecountry,andhasincludedworkshopsdealing

withsavingandcreditintotheINEAfamilyfinancemodule

aspartofadulteducation.Ithasalsoincludedtwonew

workshopstosupporttheMexicanSMEsector.

Responsible BankingCustomer-Centric Approach. Throughits“Blue

BBVA”program,BBVAhasgivenyounguniversitystudents

anumberofexclusiveadvantagesandservicestofinance

theirstudies.Thisprogramisspecificallytargetedatyoung

adultsandreflectstheBank’sstrategyofofferinginnovative

productsthatmeetthespecificneedsofdifferentcustomer

segments.

Environment. BBVAColombiahasjoinedthe“Green

Protocol”,anagreementunderwrittenbythefinancialsector

topromotesustainabledevelopmentinthecountry.Through

thisagreementtheBankcommitsvoluntarilytoimplement

policiesandpracticesthatcanberecognizedasamodelin

termsofenvironmentalresponsibility.Inadditiontothis,the

BBVAFoundationhasawardedits“BiodiversityConservation”

prizetoWWFSpainforitskeyinnovativeactionsinvarious

areasofconservation.

Community InvolvementThewinnerofBBVA’s4thINTEGRAAwardwastheCatalan

cooperativeLaFageda.Theawardisworth200,000euros.

Theawardrecognizestheworkofnon-profitorganizations

orself-employedpeoplewhocarryoutprojectsthatbring

peopleintothelabormarketandboostnewinitiativesand

goodpracticesinthisfield.Inaddition,SpainandPortugalhave

launchedthe2ndTerritorios Solidarios(SolidarityTerritories)

program,whichmakes1.8millioneurosavailableforemployees

inSpaintodevelopsupportiveprojectsledbynon-profit

organizations.Finally,theMomentumProject,BBVA’sinitiative

supportingsocialentrepreneurship,waslaunchedinMexico

forthefirsttime.TheaimistoboostSMEsthroughastrategic

alliancewithprestigiousinstitutionssuchastheEGADE

BusinessSchoolandNewVenturesMexico,inpartnershipwith

theInter-AmericanDevelopmentBank(IDB).

BBVA in the Sustainability IndicesBBVAhasaprominentpositioninthemaininternational

sustainabilityindices,withthefollowingweightingattheclose

ofSeptember:

Corporateresponsibility

Formoreinformationandcontactdetails,pleasevisit

www.bancaparatodos.com

Main sustainability indices in which BBVA participates

Weighting (%)

DJSIWorld 0.52

DJSIEurope 1.25

DJSIEurozone 2.66

ASPIEurozoneIndex 2.00

EthibelSustainabilityIndexExcellenceEurope 1.32

EthibelSustainabilityIndexExcellenceGlobal 0.90

MSCIWorldESGIndex 0.36

MSCIWorldexUSAESGIndex 0.75

MSCIEuropeESGIndex 1.31

MSCIEAFEESGIndex 0.85

FTSE4GoodGlobal 0.31

FTSE4GoodGlobal100 0.50

FTSE4GoodEurope 0.74

FTSE4GoodEurope50 1.23

24 Businessareas

Inthissectionwediscussthemoresignificantaspectsofthe

activitiesandearningsoftheGroup’sdifferentbusinessareas,

alongwiththoseofthemainunitswithineach,plusCorporate

Activities.Specifically,wedealwiththeincomestatement,the

balancesheetandthemainratios:efficiency,NPAratio,NPA

coverageratioandriskpremium.

In2012themainchangeinthereporting structureofthe

businessareasoftheBBVAGrouphasbeenthetransfer

totheUnitedStatesoftheassetsandliabilitiesofabranch

inHouston,whichpreviouslybelongedtoMexico(BBVA

Bancomer).Thishasbeendonetakingintoaccountthe

geographicalnatureoftheGroup’sreportingstructure.In

addition,changeshavebeenmadethataffectotherareasand

whichowingtotheirirrelevantnatureneednocomment.

Thus,thecompositionofthebusiness areasin2012isvery

similartothatexistinginthepreviousyear:

• Spain,whichincludes:Theretailnetwork,withthe

segmentsofindividualcustomers,privatebanking,and

smallbusinessesinthedomesticmarket;Corporateand

BusinessBanking(CBB),whichhandlestheneedsofSMEs,

corporations,governmentanddevelopersinthecountry;

Corporate&InvestmentBanking(CIB),whichincludes

activitywithlargecorporationsandmultinationalgroups;

GlobalMarkets(GM),withthetradingflooranddistribution

businessinthedomesticmarket;andotherunits,among

themBBVASegurosandAssetManagement(management

ofmutualandpensionfundsinSpain).