64

Annual Report 2003 Annual Report 2005 Growing Partnerships Worldwide

AnnualReport2003

AnnualReport2005

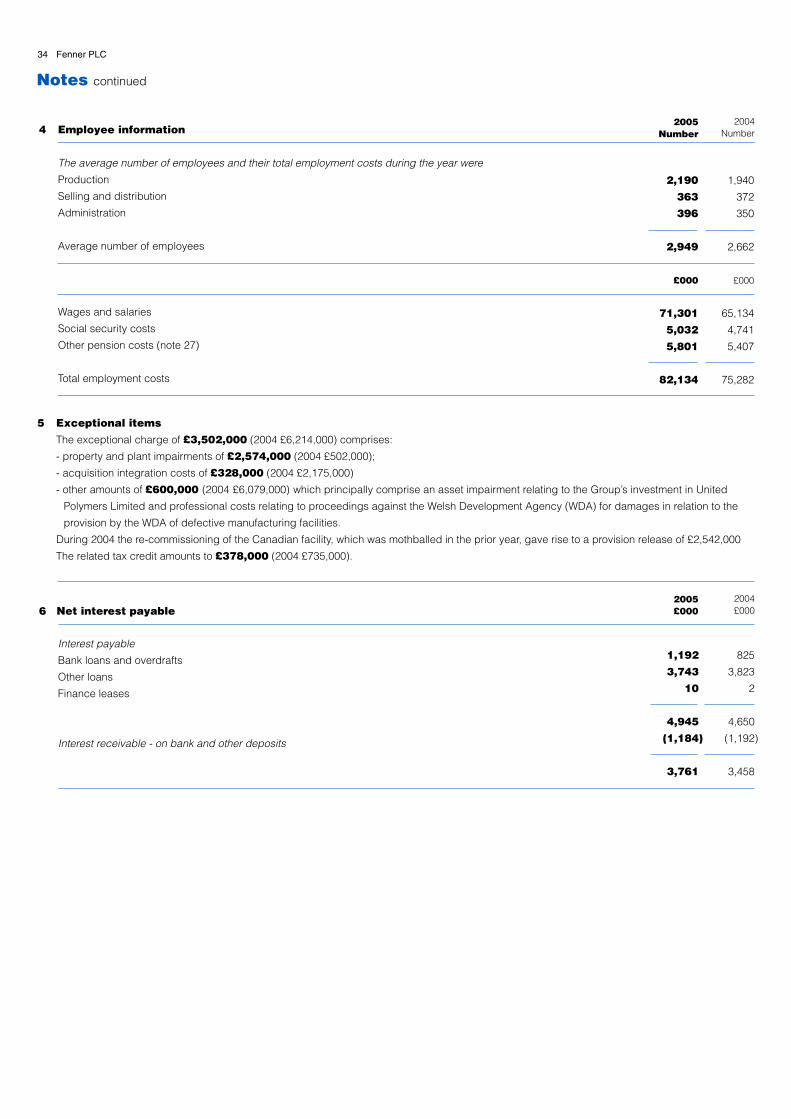

Growing Partnerships WorldwideRegistered office: Hesslewood Country Office Park,Hessle, East Yorkshire HU13 0PW, Telephone 01482 626511 Fax: 01482 626512Registered Number: 329377 www.fenner.com

Fe

nn

er P

LC

Annual R

eport 2005

Fenner is a world leader in reinforced polymertechnology.

Our strategy is to increase market share andtarget new value added product areas. We willcontinue to concentrate on growing thosebusinesses where we already demonstrateleadership through our skills in applications,design, materials technology and dedication tocustomer service as well as by carefully plannedacquisitions.

Advanced Sealing TechnologiesAdvanced Sealing Technologies

CHARLOTTETel: (1) 704 334 5353Fax: (1) 704 334 1733www.scandura.net

Tel: (44) 1482 781234Fax: (44) 1482 785438www.fennerdunlop.com/europe

Tel: (31) 512 585 555Fax: (31) 512 585 511www.fennerdunlop.com/europe

Tel: (86) 21 599 369 89Fax: (86) 21 599 367 34www.fennerdunlop.com/shanghai

Tel: (61) 3 9680 4500Fax: (61) 3 9689 9191www.apexfenner.com.au

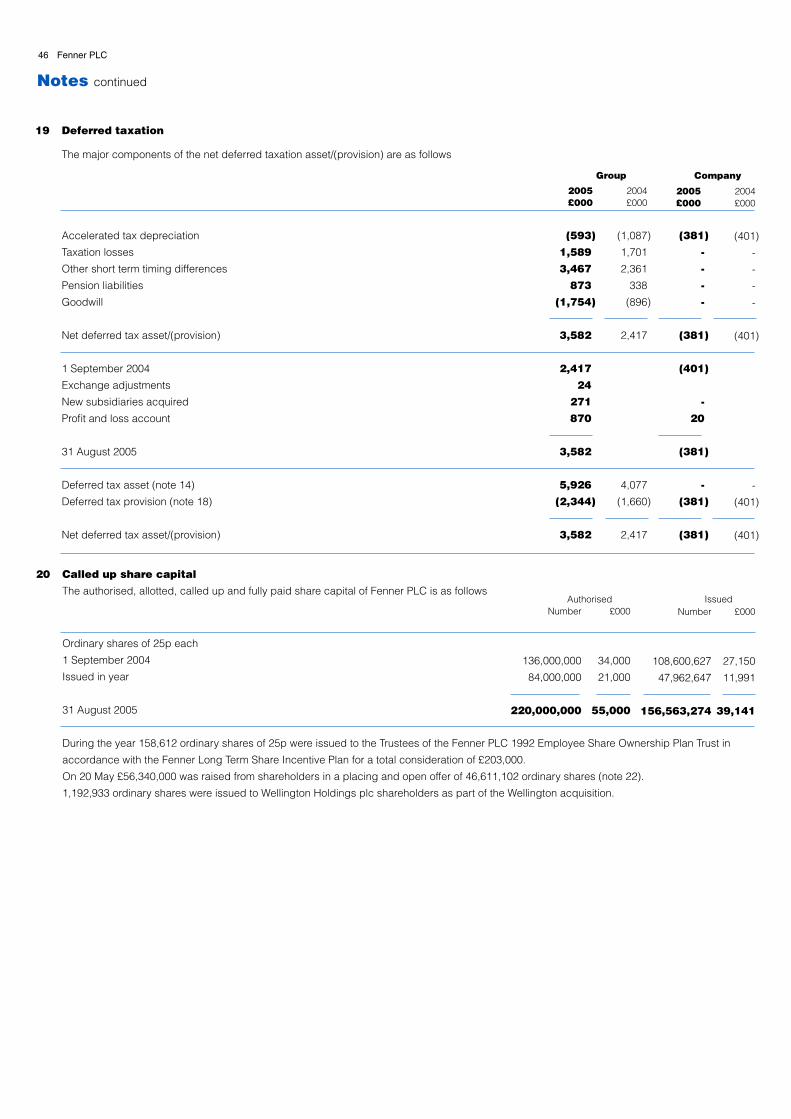

Tel: (44) 1522 781800Fax: (44) 1522 510029www.james-dawson.com

Tel: (44) 113 249 3486Fax: (44) 113 248 9656www.fennerdrives.com

Tel: (44) 20 8941 2244Fax: (44) 20 8783 1669www.hallite.com

Tel: (49) 40 73 47 480Fax: (49) 40 73 47 48 49www.hallite.de

Tel: (27) 11 974 1902Fax: (27) 11 974 1900www.fenner.co.za

Tel: (27) 11 828 8950Fax: (27) 11 822 2013www. ksbpumps.co.za

ATLANTATel: (1) 404 294 5272Fax: (1) 404 296 5165www.gaduck.com

Tel: (1) 717 665 2421Fax: (1) 717 665 2649www.fennerdrives.com

DETROITTel: 248 362 0170Fax: 248 362 4246www.hallite.com

HOUSTONTel: 281 446 6662Fax: 281 446 7034www.cdipolytek.com

Advanced Sealing Technologies

JamesD wsonaPANTONE 28060% TINT 280

Tel: (86) 21 599 369 89Fax: (86) 21 599 367 34www.james-dawson.com

JamesD wsonaPANTONE 28060% TINT 280

C O N V E Y O R B E L T I N G E U R O P E

C O N V E Y O R B E L T I N G E U R O P E

Tel: (91) 452 2464201Fax: (91) 452 2464204

C O N V E Y O R B E L T I N G A M E R I C A S

C O N V E Y O R B E L T I N G A U S T R A L I A

C O N V E Y O R B E L T I N G

C O N V E Y O R B E L T I N G

Tel: (1) 705 645 4431Fax: (1) 705 645 3112www.scandura.net

C O N V E Y O R B E L T I N G A M E R I C A S

AnnualReport2003

AnnualReport2005

Growing Partnerships WorldwideRegistered office: Hesslewood Country Office Park,Hessle, East Yorkshire HU13 0PW, Telephone 01482 626511 Fax: 01482 626512Registered Number: 329377 www.fenner.com

Fe

nn

er P

LC

Annual R

eport 2005

Fenner is a world leader in reinforced polymertechnology.

Our strategy is to increase market share andtarget new value added product areas. We willcontinue to concentrate on growing thosebusinesses where we already demonstrateleadership through our skills in applications,design, materials technology and dedication tocustomer service as well as by carefully plannedacquisitions.

Advanced Sealing TechnologiesAdvanced Sealing Technologies

CHARLOTTETel: (1) 704 334 5353Fax: (1) 704 334 1733www.scandura.net

Tel: (44) 1482 781234Fax: (44) 1482 785438www.fennerdunlop.com/europe

Tel: (31) 512 585 555Fax: (31) 512 585 511www.fennerdunlop.com/europe

Tel: (86) 21 599 369 89Fax: (86) 21 599 367 34www.fennerdunlop.com/shanghai

Tel: (61) 3 9680 4500Fax: (61) 3 9689 9191www.apexfenner.com.au

Tel: (44) 1522 781800Fax: (44) 1522 510029www.james-dawson.com

Tel: (44) 113 249 3486Fax: (44) 113 248 9656www.fennerdrives.com

Tel: (44) 20 8941 2244Fax: (44) 20 8783 1669www.hallite.com

Tel: (49) 40 73 47 480Fax: (49) 40 73 47 48 49www.hallite.de

Tel: (27) 11 974 1902Fax: (27) 11 974 1900www.fenner.co.za

Tel: (27) 11 828 8950Fax: (27) 11 822 2013www. ksbpumps.co.za

ATLANTATel: (1) 404 294 5272Fax: (1) 404 296 5165www.gaduck.com

Tel: (1) 717 665 2421Fax: (1) 717 665 2649www.fennerdrives.com

DETROITTel: 248 362 0170Fax: 248 362 4246www.hallite.com

HOUSTONTel: 281 446 6662Fax: 281 446 7034www.cdipolytek.com

Advanced Sealing Technologies

JamesD wsonaPANTONE 28060% TINT 280

Tel: (86) 21 599 369 89Fax: (86) 21 599 367 34www.james-dawson.com

JamesD wsonaPANTONE 28060% TINT 280

C O N V E Y O R B E L T I N G E U R O P E

C O N V E Y O R B E L T I N G E U R O P E

Tel: (91) 452 2464201Fax: (91) 452 2464204

C O N V E Y O R B E L T I N G A M E R I C A S

C O N V E Y O R B E L T I N G A U S T R A L I A

C O N V E Y O R B E L T I N G

C O N V E Y O R B E L T I N G

Tel: (1) 705 645 4431Fax: (1) 705 645 3112www.scandura.net

C O N V E Y O R B E L T I N G A M E R I C A S

AustraliaCONVEYOR BELTING

n Melbourne, AustraliaOver 20 stockholding branchesPrincipal products: Rubber ply beltsTechnical rubber products Conveyor services

n Sydney, AustraliaPrincipal products: Solid-woven PVC belts Conveyor services

ChinaCONVEYOR BELTING

n Shanghai, ChinaPrincipal products: Solid-woven PVC belts Nitrile covered PVC belts

PRECISION POLYMERS

n Shanghai, ChinaPrincipal products: Silicone hoses

IndiaCONVEYOR BELTING

n Madurai, IndiaPrincipal product: Solid-woven PVC belts

Southern AfricaCONVEYOR BELTING

n Johannesburg, South AfricaPrincipal products: Solid-woven PVC belts Nitrile covered PVC beltsRubber compound

KSB PUMPS

JamesD wsonaPANTONE 28060% TINT 280

n Johannesburg, South AfricaEight branchesPrincipal product: Centrifugal pumps

C O N V E Y O R B E L T I N G A U S T R A L I A

C O N V E Y O R B E L T I N G

C O N V E Y O R B E L T I N G

Key:-Conveyor BeltingManufacturing facilitiesSales/service branches

Precision PolymersManufacturing facilitiesSales/service branches

Advanced SealingTechnologiesManufacturing facilitySales/service branches

PumpsManufacturing facilitySales/service branches

North America

n Atlanta, GeorgiaPrincipal products: Rubber ply beltsLightweight rubber belts

n Bracebridge, OntarioPrincipal products: Steel cord belts Rubber ply belts

n Charlotte, North CarolinaPrincipal product: Lightweight PVC belts

n Port Clinton, OhioPrincipal product: Rubber ply belts

n Toledo, OhioPrincipal products: Rubber ply belts Special profile belts

n Tlalnepantla, MexicoPrincipal product: Rubber ply belts

ADVANCED SEALS

n Detroit, MichiganPrincipal product: Hallite Dynamic Seals

n Houston, TexasPrincipal product: CDI Polytek Seals

EuropePRECISION POLYMERS

n Lincoln, UKPrincipal products: Precision beltsSilicone hosesIndustrial ductingIndustrial rubberproducts

n Poynton, UKPrincipal products: Silicone hoses

n Leeds, UKPrincipal products: Detachable link beltsExtruded belting

North AmericaPRECISION POLYMERS

n Manheim, PennsylvaniaPrincipal products: Precision beltsDetachable link beltsKeyless bushingsUrethane beltingHigh-tech fabrics

n Wilmington,North CarolinaPrincipal products: Composite pulleys, sprockets & couplingsBelt & chain guidesGuide rail systems

Europe

n Hull, UKPrincipal products: Solid-woven PVC beltsNitrile covered PVC belts

n Drachten, NetherlandsSales/service offices in France, Spain & UKPrincipal products: Rubber ply beltsPassenger conveyorbeltingRubber profiles & sheeting

ADVANCED SEALS

n Hampton, UKPrincipal products: Hallite &CDI Polytek Seals

n Hamburg, GermanyPrincipal product: Hallite Seals

C O N V E Y O R B E L T I N G E U R O P E

JamesD wsonaPANTONE 28060% TINT 280

C O N V E Y O R B E L T I N G A M E R I C A S

CONVEYOR BELTING

CONVEYOR BELTING

Advanced Sealing TechnologiesAdvanced Sealing Technologies

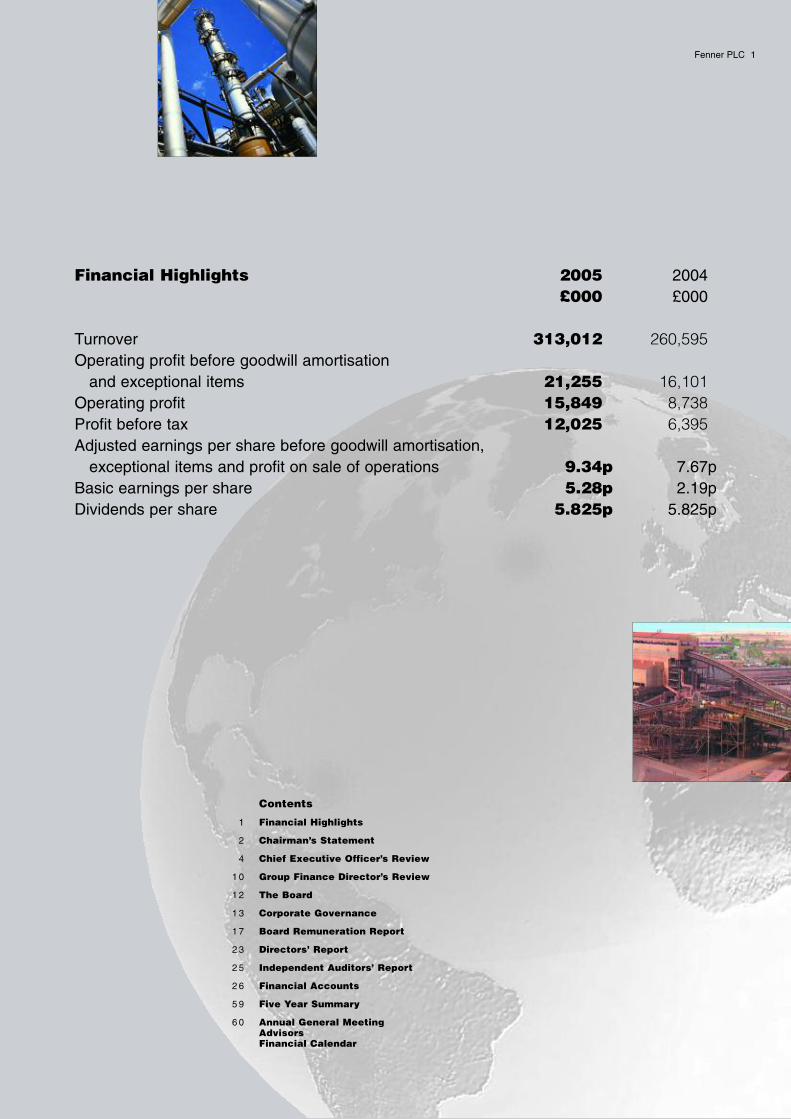

Fenner PLC 1

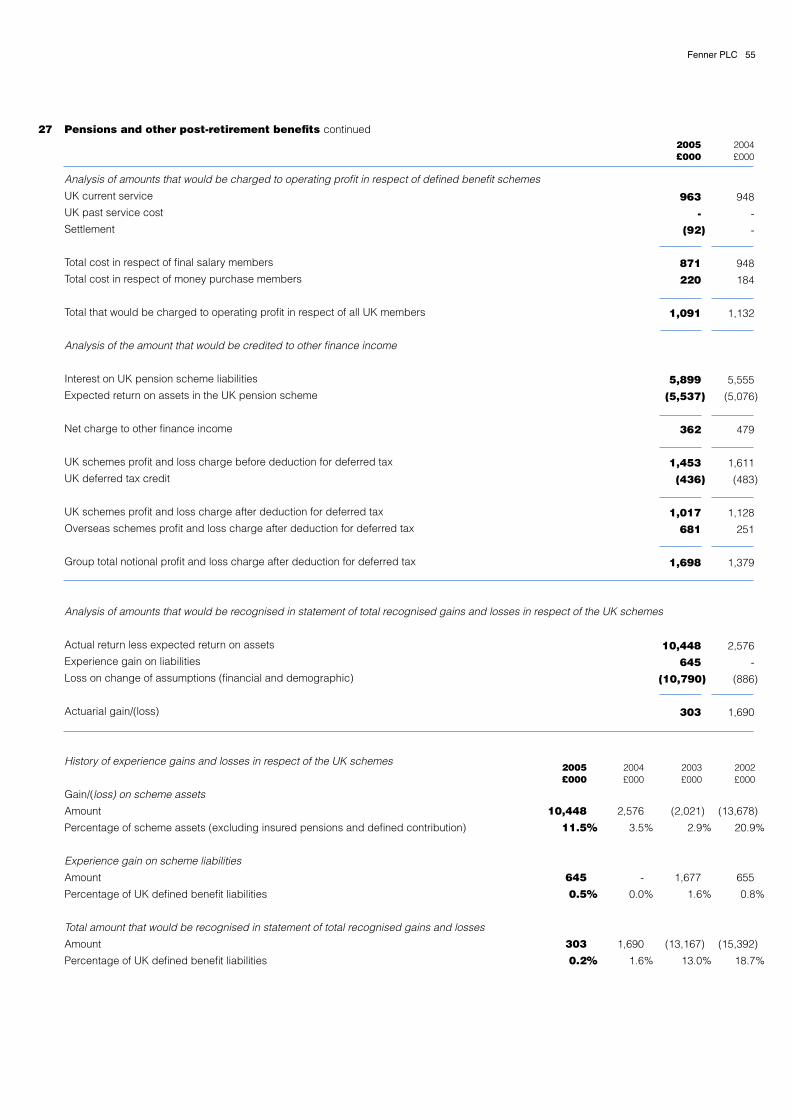

Financial Highlights 2005 2004£000 £000

Turnover 313,012 260,595Operating profit before goodwill amortisation

and exceptional items 21,255 16,101Operating profit 15,849 8,738Profit before tax 12,025 6,395Adjusted earnings per share before goodwill amortisation,

exceptional items and profit on sale of operations 9.34p 7.67pBasic earnings per share 5.28p 2.19pDividends per share 5.825p 5.825p

Contents

1 Financial Highlights

2 Chairman’s Statement

4 Chief Executive Officer’s Review

1 0 Group Finance Director’s Review

1 2 The Board

1 3 Corporate Governance

1 7 Board Remuneration Report

2 3 Directors’ Report

2 5 Independent Auditors’ Report

2 6 Financial Accounts

5 9 Five Year Summary

6 0 Annual General MeetingAdvisorsFinancial Calendar

Chairman’s Statement2 Fenner PLC

Following a solid first half performance, Group profit before tax for the

year increased 88% to £12.0m. We have benefited from an

unprecedented worldwide demand for energy particularly in China.

Our capital expenditure and rationalisation programmes have created

opportunities for productivity improvements throughout our operations.

The acquisition of Wellington Holdings plc (“Wellington”) in May

has provided a valuable addition to our niche precision polymer

businesses. Our strengthened balance sheet leaves us well placed to

exploit these opportunities.

We are encouraged by our

strong start to the year and

by current positive

indications for the future.

Colin CookeChairman

TURNOVER AND

PROFITS

Group turnover increased

20% to £313.0m (2004

£260.6m) which includes £10.8m from the former Wellington businesses acquired on 20 May

2005. Turnover growth in our underlying businesses amounted to 16% reflecting the strong

recovery in the heavyweight belting market driven by global energy demands.

Group operating profit for the year before goodwill amortisation and exceptional items

amounted to £21.3m (2004 £16.1m) including £1.9m from the former Wellington businesses.

After goodwill amortisation and exceptional items, Group operating profit amounted to

£15.8m (2004 £8.7m).

Turnover for the second half year reached £171.7m (2004 £139.8m) generating an

operating profit before goodwill amortisation and exceptional items of £14.7m (2004 £10.6m)

reflecting a strong second half performance characteristic of the markets in which the Group

operates.

Following an improved first half performance, our heavyweight belting businesses made

further progress building on the significant volume recovery particularly in North America.

Despite intense raw material price pressures, profit margins have continued to improve.

The Precision Polymers businesses in both the UK and North America have performed

well, benefiting from a recovery in levels of industrial activity.

The former Wellington businesses outperformed our expectations during the final

quarter of our financial year.

Exceptional items of £3.5m (2004 £6.2m) principally arose from impairment costs,

giving a Group profit before tax of £12.0m (2004 £6.4m). As a result of the much improved

operating performance, Group earnings per share before goodwill amortisation and

exceptional items increased to 9.34p per share (2004 7.67p) and after goodwill amortisation

and exceptional items to 5.28p (2004 2.19p).

Improvementsthroughoutour operations

Fenner PLC 3

DIVIDENDS

The Board recommends a final dividend maintained at 3.85p, which, together with the

interim dividend of 1.975p, represents a total for the year of 5.825p (2004 5.825p). The

underlying dividend cover is 1.6 after adjusting for goodwill amortisation, exceptional items

and the element relating to shares that were only in issue for three months of the year.

CASH RESOURCES AND INVESTMENT

We have raised a net £56.3m from shareholders during the year. £45.7m was invested in the

Wellington acquisition. The balance was applied to reducing our

existing debt levels whilst we examine the opportunities available

for further investment. Net borrowings at the year end amounted

to £33.9m (2004 £39.4m).

PEOPLE

The progress in improving our margin returns is a demonstration of the commitment by all

our employees, whom I thank for their efforts in this regard.

Our AGM in January 2006 will mark the retirement from the Board of Tom Glucklich,

who has been a non-executive director of the Company for over 10 years. I would like to

take this opportunity to thank Tom for his support and intellectual contribution during that

period and to wish him every success for the future.

I am pleased to announce the appointment on 1 November 2005 of David Campbell as

a non-executive director of the Company. David was formerly Chief Executive of British Vita

PLC and following the retirement of Tom Glucklich in January 2006, will chair the Company’s

Remuneration Committee.

OUTLOOK

We have made a strong start to the new year with many of our markets showing continuing,

robust strength. A buoyant energy sector has been a significant factor

in our recent growth and the confidence of our customers in this area is

an encouraging sign. Asian demand has provided the opportunity for

further new developments as the region becomes a more significant

part of the Group. Overall we look forward to another year of healthy

progress as we consolidate the benefits of our acquisition strategy.

Colin Cooke Chairman

“...opportunities...for furtherinvestment.”

“...strong startto the newyear...”

A transformationalyear

Chief Executive Officer’s Review4 Fenner PLC

Fenner Advanced Sealing Technologies service a wide range ofindustries worldwide including mobile hydraulics, industrialprocessing, materials handling, well servicing, forestry, aircraft fuelsystems, oil and gas, earthmoving and mining.

2005 saw a transformation in the Group with the acquisition of

Wellington Holdings plc in May. As a result we have now increased

the high-margin Precision Polymer’s turnover to a third of the Group’s.

We believe this also improves our profit and cash generating ability

and provides a further platform for growth.

Since the acquisition, the Wellington business, now renamed

Fenner Advanced Sealing Technologies, has performed above our

initial expectations and has already started to deliver the synergies

envisaged.

During the year we saw many of our markets strengthen as the combination of Chinese

demand and surging energy prices benefited many of our operations, both directly and

indirectly. These developments have been particularly favourable to our Asia Pacific

businesses, encouraging us to expand further our operations in China with three additional

new major projects in progress, which are detailed below.

ASIA PACIFIC

Our Chinese conveyor belting operation continued to gain momentum with strong sales

growth. As China’s burgeoning economy surged ahead on the strength of its exports and

insatiable demand for energy, coal producers

endeavoured to match the requirements. The

ensuing drive for coal productivity

improvements has proved beneficial for our

heavy duty products, as existing and new

customers realise the value of utilising higher

performance belting. This upward trend has

supported our capital investment to date with

further plant expansion planned to service our broadening customer base in this

increasingly important territory for the Group.

The hose operation in Shanghai received additional investment during the year to

accommodate output levels which are increasing as new business is gained. Slow but

steady progress is being made towards tighter truck emissions

legislation that requires changes to be made to original equipment

manufacturers’ designs, which in turn increases demand for our

products. These positive developments underpin our capital expenditure

programme for the commissioning of a dedicated world-class

manufacturing hose facility capable of meeting market demand.

The acquisition of Wellington Holdings plc brought numerous new

and exciting opportunities to the Group. These included the identification of gaps in their

geographical coverage in locations where we have existing knowledge and expertise. To

exploit these distinctive competencies, plans are underway for further penetration of seals’

markets in China with the construction of a new plant.

Fenner PLC 5

Mark AbrahamsChief Executive Officer

“...dedicatedworld-classmanufacturinghose facility...”

Above: Manufactured at the Fenner Shanghai facility, this Fenaplast conveyor belt is in operation undergroundat the Shenhua Yujialiang mine in Inner Mongolia. Currently, over 100km of Fenner Chinese-manufacturedbelting is running underground and constantly setting new records of service life and coal output.

Production of computer peripherals has progressively migrated to South East Asia in recent

years, and the overwhelming majority of our mini-pitched timing belts are shipped into the

region. Accordingly, our presence has been strengthened in South East Asia to support

existing office equipment accounts and to identify and develop new business opportunities.

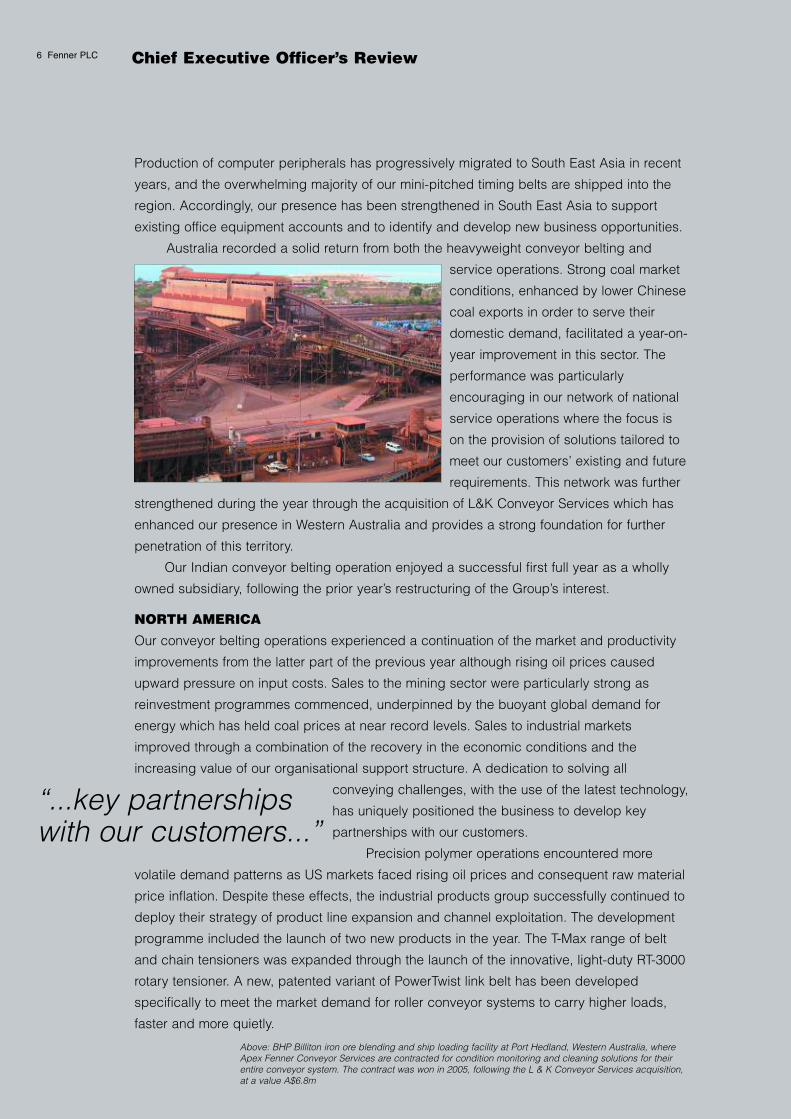

Australia recorded a solid return from both the heavyweight conveyor belting and

service operations. Strong coal market

conditions, enhanced by lower Chinese

coal exports in order to serve their

domestic demand, facilitated a year-on-

year improvement in this sector. The

performance was particularly

encouraging in our network of national

service operations where the focus is

on the provision of solutions tailored to

meet our customers’ existing and future

requirements. This network was further

strengthened during the year through the acquisition of L&K Conveyor Services which has

enhanced our presence in Western Australia and provides a strong foundation for further

penetration of this territory.

Our Indian conveyor belting operation enjoyed a successful first full year as a wholly

owned subsidiary, following the prior year’s restructuring of the Group’s interest.

NORTH AMERICA

Our conveyor belting operations experienced a continuation of the market and productivity

improvements from the latter part of the previous year although rising oil prices caused

upward pressure on input costs. Sales to the mining sector were particularly strong as

reinvestment programmes commenced, underpinned by the buoyant global demand for

energy which has held coal prices at near record levels. Sales to industrial markets

improved through a combination of the recovery in the economic conditions and the

increasing value of our organisational support structure. A dedication to solving all

conveying challenges, with the use of the latest technology,

has uniquely positioned the business to develop key

partnerships with our customers.

Precision polymer operations encountered more

volatile demand patterns as US markets faced rising oil prices and consequent raw material

price inflation. Despite these effects, the industrial products group successfully continued to

deploy their strategy of product line expansion and channel exploitation. The development

programme included the launch of two new products in the year. The T-Max range of belt

and chain tensioners was expanded through the launch of the innovative, light-duty RT-3000

rotary tensioner. A new, patented variant of PowerTwist link belt has been developed

specifically to meet the market demand for roller conveyor systems to carry higher loads,

faster and more quietly.

“...key partnerships with our customers...”

6 Fenner PLC Chief Executive Officer’s Review

Above: BHP Billiton iron ore blending and ship loading facility at Port Hedland, Western Australia, whereApex Fenner Conveyor Services are contracted for condition monitoring and cleaning solutions for theirentire conveyor system. The contract was won in 2005, following the L & K Conveyor Services acquisition,at a value A$6.8m

The markets have responded favourably to both

of these carefully targeted product launches.

These, together with our marketing alliances, have

contributed to incremental sales growth. Market

demand in the office equipment segment was

slow in the first few months of the year, but

recovered considerably in the second half. Our

continuous improvement programme increased

production yields, but nevertheless, capacity was

flexed to meet customer demand for mini-pitch

timing belts. Planning is now well advanced for a

building extension to accommodate an increase in capacity with completion scheduled for

2006.

The newly-acquired seals operations benefited from buoyant energy markets. To

enhance growth further new applications, including the semi conductor processing industry,

were developed. The design of new sealing solutions, such as the patented SigmaSeal is

encouraging. This seal, which is generating interest in new markets, has unique

self-energising and low friction properties suitable to the control valve industry.

EUROPE

The environment for our UK based heavyweight conveyor belting operation became

increasingly difficult during the year with declining demand from both the UK and German

coal industries. Against this, the demand from our worldwide potash customers remained

robust and further penetration of Eastern European, Ukrainian and Russian coal markets was

achieved. Whilst raw material prices increased significantly during the year, sales pricing

action coupled with improved purchasing enabled margins to be maintained.

Weak economic conditions prevailed in most of our major European industrial markets,

which together with the threat from the competition

over an otherwise flat market, led to a difficult year for

our Dutch operation. As a consequence, action to

address the cost base was implemented in the

second half through a reduction in the workforce

whilst overall productivity improvements were

achieved through additional investment in new plant

and systems.

James Dawson at Lincoln built upon the solid

foundations established in recent years to record a

good performance overall. Demand from the speciality vehicle and business machine

markets was generally strong allowing the benefits from recent capital investment

programmes to be realised. Further recognition of the accomplishments of this operation

was gained in the year with the Queen’s Award for Enterprise in International Trade.

Fenner PLC 7

Top: Fenner Drives recently launched a new range of taper edge bands specially developed to meet therequirements of the wallboard industry. These taper edge bands last up to 12 times longer thanconventional PVC bands, reduce downtime and are capable of operation at temperatures up to 64°C.

Bottom: James Dawson are supplying charge air hoses on Volvo Truck vehicles. This business emphasisesthe Global position James Dawson has within the silicone hose supplier base.

8 Fenner PLC Chief Executive Officer’s Review

1 Artist’s impression of thePrecision Polymers facility to bebuilt in the new Industrial Park inJiading, Shanghai. The newfacility will be shared equally byFenner Advanced SealingTechnologies and James Dawson.

2 One of the new sealingdevelopments is the SigmaSealwhich has unique self-energisingand low friction properties suitablefor the control valve industry.

3 At the solid-woven conveyorbelting Centre of TechnicalExcellence based in Hull, thisair-bearing PVC rheometerprovides an understanding of thecomplex viscosity, flow and fusionchanges that take place during heat processing of a belt.

4 The conveyor belting facility in Atlanta has installed two new looms capable of weaving up to 2.2m widths. The looms operate at overtwice the speed of the previous looms and a further 10 are scheduled for commissioning by the end of the current year.

5 James Dawson Managing Director Rodney Barbour receiving the Queen’s Award for Enterprise from Mrs Bridget Carcroft-Eley, HerMajesty’s Lord-Lieutenant of Lincolnshire at the ceremony held at the Lincoln facility.

6 A consignment of solid-woven Fenaplast conveyor belting destined for underground use being loaded at the new Indian facility.

1 2

3

4

5

6

The Poynton (Cheshire) hose facility, which was acquired in February 2004, continued to

perform well. The projected market synergy between Poynton’s EPDM hose and Lincoln’s

silicone hose products is now beginning to be realised and is expected to lead to continued

steady growth of sales of Poynton products.

Fenner Drives Europe, formerly BTL in Leeds, experienced a continuing reduction in

demand from traditional markets, reflecting the general decline in UK manufacturing.

However, this decline was more than offset as programmes of innovative marketing, product

line expansion and increased activity in Europe took effect.

At the end of the year, the UK operations of both James Dawson and Fenner Drives

were restructured. James Dawson now operates exclusively in the world markets for

commercial and speciality vehicles, focusing upon capitalising on recent investments in the

specialist hose business. The industrial rubber and business machine products of James

Dawson have been brought under the responsibility of Fenner Drives Europe.

Sales from our European seals operations exceeded expectations in the period since

acquisition with strong demand from longwall mining

equipment and the oil and gas industry. As we enter the new

year, the planned relocation of the UK operation to a new

facility is progressing satisfactorily. The factory and offices

which are currently under construction at Hampton will

replace the existing network of 1920’s buildings. The benefits of the move will follow the

completion which is scheduled for the second half of 2006.

AFRICA

An increase in demand for energy in South Africa caused a heightened activity in the

region’s coal mining industry and the

commissioning of previously mothballed power

generation plants. This environment enabled the

achievement of a further successful year by our

conveyor belting operation, despite the keen

competition within the local market.

The Group’s other South African operation,

KSB, improved as the year progressed

following softer volumes into agricultural markets

in the early months and higher contract volumes

in the second half-year.

Significant progress has been made during the last year with an increasingly encouraging

trend in performance. As we enter the new financial year we do so with confidence that most

of our businesses are seeing healthy market conditions with opportunities for growth.

Mark Abrahams Chief Executive Officer

Fenner PLC 9

“...seals operationsexceededexpectations...”

Above: Fenner South Africa’s in-house splicing crew out in the fieldsplicing a solid-woven, high abrasion resistant conveyor belt on akey installation feeding coal to Lethabo, one of South Africa’snational power stations.

Group Finance Director’s Review10 Fenner PLC

The Group advanced significantly during the year with the acquisition

of Wellington Holdings plc. Our integration of the business has

progressed satisfactorily and an excellent performance has been

achieved in the initial period of ownership. With the improved

performance of our existing businesses, the overall result is most

encouraging.

OPERATING CASH FLOW

A robust operating profit before goodwill amortisation and exceptional

items of £21.3m (2004 £16.1m) facilitated a healthy operating cash

inflow. Working capital levels did increase with higher stock and debtors which reflected the

increase in trading activity, coupled with tighter credit terms arising from capacity constraints

in our supplier base.

Exceptional items of £3.5m (2004 £6.2m) largely related to property and plant

impairments. Of this amount, £1.0m resulted in a cash outflow in the period.

Overall the Group generated a cash inflow from operations of £21.3m (2004 £14.2m).

ACQUISITIONS AND GOODWILL

During 2005 the Group acquired the entire issued share capital of Wellington Holdings plc

for a consideration of £45.7m (including acquisition expenses) and made two smaller

acquisitions for £0.3m.

Goodwill arising on these transactions amounted to £41.6m.

FUNDING AND RESOURCES

During the year the Company raised £56.3m from shareholders in a placing and open offer

of new ordinary shares. The proceeds were principally used to fund the purchase of

Wellington Holdings plc.

The acquisition necessitated our having to formally anticipate the repayment of the

US$50m Private Placement Note in March 2006. This, together with the continuing capital

expenditure programme and potential for further bolt-on acquisitions, required us to secure a

new £60m five year committed Revolving Credit facility with three leading UK banks. This

has also replaced several uncommitted bank lines and gives us more flexibility for the

Company’s future debt financing options.

The Group’s gross borrowings at 31 August 2005 were £86.0m offset by cash and

deposits of £52.1m, giving net borrowings of £33.9m. Approximately 48% of the gross

borrowings is currently at a fixed interest rate.

PENSIONS

The Group has continued to account for pensions in accordance with SSAP 24. Following the

acquisition of Wellington Holdings plc, the Group has inherited further pension obligations.

The major scheme relates to the UK; a defined benefit arrangement which on 31 March 2000

was closed to new members. Existing members’ pensions continue to be accrued on a final

salary basis for the qualifying service up to 31 March 2000, with eligibility to participate in a

defined contribution scheme thereafter.

In accordance with the principles of FRS 7 “Fair Values in Acquisition Accounting” the deficit

Richard PerryGroup Finance Director

Fenner PLC 11

of £2.1m in this scheme has been included within the provisional fair value of net assets

acquired.

The manner in which pension arrangements are reflected in the Group’s accounts will

change when the substantive requirements of FRS 17 “Retirement Benefits” are adopted

under International Financial Reporting Standards. Note 27b of the accounts gives the

funding position and pension cost in accordance with FRS 17 principles.

TAXATION

The Group’s taxation charge for the year was £4.5m (2004 £3.1m) after offsetting a tax credit

of £0.4m in respect of exceptional items. Before exceptionals and goodwill amortisation, the

tax rate was 28% (2004 29%).

TREASURY POLICY

The Group has a central treasury function which operates in accordance with Board

approved policies. Its principal objective is to minimise financial risk. Where appropriate,

derivative transactions are undertaken to reduce interest rate and currency rate risks arising

from the Group’s operations and sources of finance. No speculative trading is undertaken.

The interest cost arising on borrowings is managed on a net basis through the use,

where appropriate, of swaps to reduce the interest rate risk.

Deposits of funds are made with banks and financial institutions approved by the Board

and within set credit limits. Bank and loan facilities are monitored on a regular basis and

maintained at a level which provides adequate funding for seasonal variations in borrowings

whilst allowing for acquisitions and organic expansion.

The Group’s principal foreign currency exposures arise on the translation of overseas

profits and net assets into sterling, the translation of intra-group lending (principally from the

UK to overseas subsidiaries) and from trading transactions in foreign currencies. The Group

normally only hedges the accounting exposure on the translation of overseas profits to the

extent that such profits are offset by interest charges on foreign currency borrowings.

Where cost effective, overseas net assets are hedged by foreign currency borrowings and

intra-group lending is matched by external borrowings in the same currency. Currency

exposures arising from trading transactions are continually monitored and material

exposures are hedged once cash flows can be identified with sufficient certainty.

During the year the derivatives used by the Group have been forward foreign exchange

contracts, options and interest rate swaps.

INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS)

For accounting periods commencing on or after 1 January 2005 all European listed

companies are required to use IFRS to prepare their consolidated financial statements. For

Fenner this means that the 2006 Interim Report, the 2006 Annual Report and all subsequent

reports including all comparative information will be prepared using IFRS. The Group has

continued its preparatory work to ensure full compliance with these requirements.

Richard Perry Group Finance Director

12 Fenner PLC

COLINCOOKE (65)* a r n

ChairmanJoined the Companyin May 1993 as non-executive Chairman.He is also a non-executive director ofAdvanced FluidConnections plc(formerly known asOystertec plc).

The Board

MARKABRAHAMS (50) n

Chief ExecutiveOfficerAppointed to theBoard as GroupFinance Director in1990, and becameChief ExecutiveOfficer in May 1994.He is also non-executive Chairmanof Inditherm plc.

RICHARDPERRY (55)Group FinanceDirectorAppointed to theBoard in September1994. He is also anon-executivedirector of ScapaGroup plc.

DAVID BUTTFIELD(59)* a r n

Appointed to theBoard in January2003, he is a formerexecutive directorof D S Smith Plc.

THOMASGLUCKLICH (69)* a r n

Appointed to theBoard in August 1995,he was formerly adirector of LazardBros & Co Limited.

DEBRABRADBURY (39)Company SecretaryJoined the Company in2001 and wasappointed CompanySecretary in July 2002.

DAVID CAMPBELL(55)* a r n

Appointed to theBoard in November2005, he wasformerly ChiefExecutive of BritishVita plc.

* Non executive a Audit Committeer Remuneration Committeen Nomination Committee

Fenner PLC 13

The Group is committed to comply with the Principles of Corporate Governance as set out in the 2003 FinancialReporting Council’s Combined Code as incorporated into the FSA Listing Rules (“Combined Code”) and continues torecognise the importance of high standards of corporate governance. This statement explains how the Principles ofCorporate Governance are applied within the Group and areas of non compliance are explained.

Directors & Directors’ IndependenceThe Board usually comprises the non-executive Chairman, two executive directors and two non-executive directors andis responsible to shareholders for the proper management of the Group. Specific matters are reserved for the Board’sconsideration under a formal schedule including Group strategy, reviewing trading performance, considering seniormanagement appointments, formulating policy on key issues including the approval of significant capital expenditure,acquisitions and disposals and reporting to shareholders.

The Board is headed by a non-executive Chairman who was independent upon appointment and whose role is distinctand separate from that of the Chief Executive Officer. The other non-executive directors are also independent. ThomasGlucklich, a non-executive director is the senior independent director of the company and is considered by the Boardto be independent in both character, judgement and contribution despite having served for 10 years. Thomas Glucklichwill be retiring from the Board at the forthcoming AGM. David Campbell was appointed to the Board on 1st November2005 and was independent upon appointment. The Chairman and the non-executive directors are independent ofmanagement and do not have any business relationships which could interfere with the exercise of their judgement.

Biographical details of the directors are set out on page 12.

Non-executive directors receive appropriate briefings on the Group and its operations when they are appointed to theBoard. They are encouraged to visit the Group’s offices and factories whenever the opportunity presents itself, wherethey are briefed on local business operations. All directors have access to the Company Secretary, who is responsiblefor ensuring that Board procedures are followed and that the Group complies with all applicable rules, regulations andobligations governing its operations. A procedure exists for directors to take independent professional advice, at theGroup’s expense, if necessary, in the furtherance of their duties. The Board is provided with timely and appropriateinformation prior to each Board, Committee or General Meeting covering the items on the agenda for such meetings.

The Board is in the process of identifying a suitable and meaningful board evaluation process. The NominationCommittee appraised the requirements of the Board during the year as part of the recruitment process for a new nonexecutive director.

All directors are subject to election by shareholders at the first Annual General Meeting following their appointment andto re-election thereafter at intervals of no more than three years.

The Board has a number of committees consisting of directors and senior executives. Details of their composition andpurpose are outlined below. In addition the Chairman and the non-executive directors meet from time to time withoutthe executive directors being present.

Group ExecutiveThe Executive Committee is chaired by Mark Abrahams. It consists of the two executive directors, the CompanySecretary and five members of the Group’s senior management. The Executive Committee meets at least 6 times a yearand deals with the daily management of the Group through powers delegated to it by the Board.

Audit CommitteeThe Audit Committee comprises the Chairman and the non-executive directors and is chaired by David Buttfield whohas recent and relevant financial experience. Due to the size of the Company and the number of non-executivedirectors, the Board has decided that the Chairman of the Company should remain a member of the Committee.

The terms of reference of the Audit Committee cover all the main points recommended by the Combined Code. Itsprincipal duties are to monitor the integrity of the financial statements, to review the internal controls and riskmanagement systems, to review the work of internal audit and to consider all aspects of the relationship with theexternal auditor. The Committee has the authority to obtain external legal or other professional advice on any matterwithin its terms of reference.

Corporate Governance

There is a policy on the provision of non-audit services by the external auditor. Certain services such as due diligencein relation to acquisitions and disposals, taxation and actuarial advice are permitted but others, for example, internalaudit, information technology and HR consultancy are generally considered inappropriate. Non-audit fees are reportedto the Committee.

The Committee has received and reviewed written confirmation from the external auditor on all relationships that in theirjudgement may bear on its independence. The external auditor has also confirmed that it considers itself independentwithin the meaning of UK regulatory and professional requirements.

Nomination CommitteeThe Nomination Committee, which consists of the Chairman, the non-executive directors and the Group ChiefExecutive Officer, is chaired by Colin Cooke. The duty of the Committee is to make recommendations to the Boardregarding the appointment of new Board members. Given the size of the Board and the Company, it is felt bothappropriate and prudent to have Mark Abrahams on the Committee to work with the Chairman and non-executivedirectors on senior recruitment issues. Written terms of reference were adopted during the year clearly setting out therole and scope of the Committee. There were three meetings during the year to identify and recruit a new non-executivedirector to replace Thomas Glucklich when he retires at the forthcoming AGM. The Committee was assisted bySpencer Stuart Consultants in identifying a short list of candidates who met the profile being sought by the Board.David Campbell was subsequently selected and joined the Board on 1 November 2005.

Remuneration CommitteeThe Remuneration Committee consists of the Chairman and non-executive directors and is chaired by ThomasGlucklich. David Campbell will become the Chairman of the Committee when Thomas Glucklich retires. The GroupChief Executive Officer also attends the meetings by invitation.

The Committee is responsible to the Board for determining the remuneration packages of the executive directors andother senior executives and advises on executive remuneration policy issues. It also approves the granting of shareoptions to employees within the Group and administers the Group’s Long Term Share Incentive Plan (LTIP).

The Remuneration Committee during the year received advice from MM&K Ltd who assisted the Committee inconsideration of matters relating to directors’ incentives and Mercer Human Resource Consulting, who conducted areview of executive directors’ remuneration.

Directors’ remunerationThe Board Remuneration Report is set out on pages 17 to 22.

Relations with shareholdersThe Company encourages regular dialogue with its institutional shareholders and also with private investors at theAnnual General Meeting. Update meetings are held with institutional shareholders following the announcement ofinterim and final results and as requested throughout the year. Similar meetings are held with private client brokers sothat the same information can be disseminated to private investors. Recent analyst presentations are also madeavailable on the www.fenner.com website. The Group website was revised during the year and now providescomprehensive investor relations information for shareholders to view. The website includes the current share price,regulatory announcements, financial performance information, shareholder information and an investor relationscontact address.

Corporate Governancecontinued

14 Fenner PLC

Number of meetings during the yearChairman C I Cooke

Executive directorsM S AbrahamsR J Perry

Non-executive directorsT C GlucklichD F Buttfield

* By invitation

Group Board

109

109

910

Meetings of the BoardAudit

Committee

32

3*3*

33

RemunerationCommittee

55

3*-

55

NominationCommittee

33

3-

33

Fenner PLC 15

Annual General MeetingIn relation to the Company’s Annual General Meeting:

- the proxy count in respect of each resolution is announced after it has been dealt with on a show of hands;- a separate resolution is proposed for each substantially separate issue, including the receipt of the annual

report and accounts;- all executive and non-executive Board members normally attend the Meeting; and- the Notice of the Meeting, the annual report and accounts and any other related papers are normally sent to

shareholders more than one month before the Meeting.

Accountability and auditDirectors’ responsibilities in respect of the financial statementsCompany law requires the directors to prepare financial statements for each financial year which give a true and fairview of the state of affairs of the Company and the Group and of the profit or loss of the Group for that period. Inpreparing those financial statements, the directors are required to:

- select suitable accounting policies and then apply them consistently;- make judgments and estimates that are reasonable and prudent;- state whether applicable accounting standards have been followed, subject to any material departures

disclosed and explained in the financial statements; and- prepare the financial statements on the going concern basis unless it is inappropriate to presume that the

Company and the Group will continue in business.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at anytime the financial position of the Company and the Group and enable them to ensure that the financial statementscomply with the Companies Act 1985. They are also responsible for safeguarding the assets of the Company and theGroup and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The maintenance and integrity of the Fenner PLC website is the responsibility of the directors; the work carried out bythe auditors does not involve consideration of these matters and accordingly, the auditors accept no responsibility forany changes that may have occurred to the financial statements since they were initially presented on the website.Legislation in the UK governing the preparation and dissemination of financial statements may differ from legislation inother jurisdictions.

Going concernAfter making enquiries, the directors have formed a judgment at the time of approving the financial statements thatthere is a reasonable expectation that the Company and Group have adequate resources to continue in operationalexistence for the foreseeable future. For this reason, the directors continue to adopt the going concern basis inpreparing the financial statements.

Internal controlThe Board continues to review the effectiveness of the Group’s system of internal control and evaluates the InternalControl report at least twice a year. This review covers all controls, including operational, financial, compliance and riskmanagement.

As required by the UK Listing Authority, the Group has complied with the Combined Code provisions on internal controlhaving established the procedures necessary to implement the guidance contained in “Guidance for Directors on theCombined Code” issued by the Institute of Chartered Accountants in England and Wales and by reporting inaccordance with that guidance.

The directors are responsible for the Group’s system of internal control which, like any system of internal control, canonly provide reasonable and not absolute assurance against material misstatement or loss.

The directors have reviewed the effectiveness of the system of internal control in operation during the year and up tothe date of approval of the annual report.

Corporate Governancecontinued

16 Fenner PLC

The key procedures within the control structure are:- the identification of major business and insurance risks faced by the Group’s operations, by both the Board and

senior management, and the determination of the most appropriate course of action to deal with these risks;- central review and approval procedures in respect of major areas of risk, such as acquisitions and disposals,

litigation, treasury management, taxation and environmental issues;- a clear management structure with well defined lines of responsibility and the appropriate levels of delegation;- regular review of the Group’s business units by operational and executive management;- a structured process for appraising and authorising capital projects. This process includes clearly defined

authorisation levels. Projects are subject to post investment appraisals;- well established consolidation and reporting systems for both the statutory and monthly management accounts,

with all Board members receiving a monthly statement of the financial results;- comprehensive budgeting systems with an annual budget approved by the Board. Monthly results are reported

against budget and revised forecasts for the year are prepared regularly; and- an internal programme of monitoring visits by the Internal Audit team was agreed with the Audit Committee,

which review the compliance of each business unit with standard internal financial control procedures adopted by the Group.

Compliance with the Combined CodeThe Group has complied with the main provisions of the Combined Code in force during the year ended 31 August2005 that are appropriate for a Group of this size. The Group has sought to explain non-compliance with the Boardevaluation process, the inclusion of the Chief Executive on the nomination committee and the inclusion of the Chairmanon the audit committee and will continue to work towards full compliance with the spirit of the Combined Code.

Board Remuneration Report

The Board presents its report on directors’ remuneration which has been prepared following the provisions ofSchedule B of the Combined Code issued in July 2003 and the provisions of the Directors’ Remuneration ReportRegulations 2002. Details of the Remuneration Committee’s responsibilities are given on page 14.

The parts of this report covering directors’ detailed emoluments, share schemes and pensions are audited.

Members of the remuneration committeeThe members of the remuneration committee during the year were: Thomas Glucklich (Chairman), Colin Cooke andDavid Buttfield

During the year the Remuneration Committee took advice from an independent external source, as noted on page 14.

Remuneration policyExecutive directorsThe Company’s policy on remuneration is to attract, retain and incentivise executives with the experience andnecessary skills to operate and develop the Company’s businesses to their maximum potential, thereby delivering thehighest level of return for shareholders.

Consistent with this policy, benefit packages awarded to executives are intended to be competitive and comprise amix of performance-related and non-performance related remuneration designed to incentivise them, but not to detractfrom the goals of Corporate Governance.

During the year, Mercer Human Resource Consulting was commissioned to produce a report on comparative pay forexecutive directors of companies similar to Fenner. The report confirmed that the pay levels of the executive directorswere not above those of their peers.

The Committee also takes account of the pay levels of senior management of the Fenner Group when establishing theexecutive directors’ remuneration.

It is the Committee’s current intention to continue to reward the executive directors with an annual performance relatedbonus plan, linked to operating profit, earnings per share and cash targets, and a long-term share incentive plan(LTIP). The shares allocated under the LTIP will be awarded to an executive after a period of three years and will bedependent on the comparative performance of the Company’s total shareholder return (TSR) against the TSR ofcompanies comprising the FTSE All Share Engineering and Machinery sector (The Peer Group) over the period fromthe provisional allocation date to the final award date. The Committee considers that TSR, which comprises of inter aliadividend yield and share price movement in comparison with The Peer Group, is the best measure of long termperformance as it aligns the interests of executives with shareholders and recognises market conditions in the Group’sindustrial sector.

The targeted composition of each director’s remuneration is as follows:

Non-performance related Performance related

Mark Abrahams 60% 40%Richard Perry 60% 40%

Chairman and Non-executive directorsThe Chairman and non-executive directors are usually appointed for a fixed three year term.

The remuneration of the non-executive directors is determined by the Board as a whole, having regard to thepackages awarded by other UK listed companies of similar size and complexity.

The non-executive directors do not participate in any of the Group’s bonus, share option or incentive schemes, nor dothey accrue any pension entitlement.

Fenner PLC 17

Board Remuneration Reportcontinued

18 Fenner PLC

Directors’ service contractsThe executive directors have rolling 12 month contracts, in addition the Company has agreed to the payment of aprescribed sum equivalent to 12 months salary and contractual benefits if there is a change of control or termination oftheir contracts by the company other than for cause.

The service contracts do not contain any provision for compensation on early termination other than the notice period,and the provision noted above, however the Committee will seek to mitigate cost to the Company whilst dealing fairlywith each individual case.

The details of the service contracts in relation to the executive directors and letters of appointment in relation to theChairman and non-executive directors, who served as directors during the year are:

Unexpiredterm at Notice

31 August 2005 period

Mark Abrahams - 1 yearRichard Perry - 1 yearColin Cooke* 28 months Fixed TermThomas Glucklich 4 months Fixed TermDavid Buttfield 4 months Fixed Term

* Colin Cooke’s services are provided by way of an agreement between the Company, Steels Management Limited andColin Cooke.

External appointmentsFenner recognises that its executive directors are likely to be invited to become non-executive directors of othercompanies and that such appointments can broaden experience and knowledge, which may benefit Fenner. Thereforeexecutive directors may, subject to approval by the Board and providing there is no conflict of interest, be allowed toaccept appointments as a non-executive director of another company and are normally allowed to retain the fees paidfrom such appointments. In normal circumstances, they may not accept more than one appointment. Currently theChief Executive Officer, Mark Abrahams, is non-executive Chairman of Inditherm plc and retained fees of £35,000 inrelation to Inditherm plc’s year ending 31 December 2004. The Group Finance Director, Richard Perry, was appointedas a non-executive director of Scapa Group plc on 1 June 2005 and will retain the fees.

Remuneration components for executive directorsThe major components of the executive directors’ remuneration are:

Basic annual salary and benefitsThe basic annual salary is subject to an annual review which takes into account the performance of the Group and theindividual and salary trends in comparable companies. In addition, a car allowance, healthcare insurance and otherbenefits are available in line with normal corporate practice.

Annual performance related bonusPerformance related cash bonuses are reviewed annually. Demanding performance targets are set, which must beachieved before the maximum bonus is payable. The confirmed criteria include targets linked to the Group’sperformance in terms of operating profit and earnings per share. The target bonus for achievement of the annualbudget for these measures is 35% of basic annual salary and the maximum potential payment for the annual bonus is60% of basic annual salary, excluding benefits in kind and pension contributions.

Long Term Share Incentive PlanThe Long Term Share Incentive Plan (LTIP) is designed to encourage its participants to deliver sustained long termperformance.

Rewards under the LTIP are linked to the Company’s performance over three year periods (Plan Cycles). As near aspracticable to the start of a Plan Cycle, the Remuneration Committee notifies each participant of the provisionalallocation of ordinary shares which could be distributed to him after the end of the Plan Cycle if the performance targetis met. The performance target is intended to be demanding. The provisional allocation of ordinary shares is based ona percentage (maximum 100%) of the participant’s basic annual salary and the value of the Company’s ordinary sharesat the start of the Plan Cycle.

The performance measurement for each of the Plan Cycles is the Company’s TSR which is compared with the TSR ofThe Peer Group. In the opinion of the Remuneration Committee, the FTSE All Share Engineering and Machinery Index isthe most appropriate index against which the TSR of the Company should be measured because it is an index ofbusinesses similar in nature to Fenner and which represent alternative investment options for our shareholders.

100% of the provisional allocation of ordinary shares may be distributed only if the Company’s performance places itwithin the top 16 per cent of the companies in The Peer Group. Participants will not receive any ordinary shares if theCompany’s ranking is below the median (i.e. the point which divides The Peer Group into two equal halves such that50% of the companies are above this point and 50% are below it). Between these two points there is a piecewise linearrelationship between the number of shares vesting and the percentile ranking of Fenner amongst the Peer Group.There have been no departures from the Company’s policy on awarding benefits under long-term incentive schemesduring the year. In the event that a director resigns, the awards will lapse.

The performance chart below illustrates the Company’s total shareholder return over the past five years compared tothe performance of The Peer Group. In addition to the statutory requirement to plot data over five financial year ends,the graph and table below reflect data for each of the Plan Cycle dates for the LTIP. The Plan Cycle dates are alignedwith the Group’s Preliminary Announcement, which the Remuneration Committee believes are the most appropriatepoints for benchmarking the LTIP. This is because at these dates there is full disclosure of relevant price sensitiveinformation to the market as a whole.

Share optionsSince the creation of the LTIP no options have been granted to the executive directors and they are no longer eligible toparticipate in the Share Option Scheme for new options.

PensionsThe executive directors participate in the defined benefits section of the Fenner Pension Scheme, an Inland Revenueapproved mixed benefits scheme, on the same terms as other senior executives. The Scheme provides for a maximumpension of two-thirds of remuneration at or near retirement age of 62. For both of the executive directors, pensionablesalary and benefits from the Fenner Pension Scheme are restricted by the Inland Revenue earnings cap, consequentlypayments are made to funded unapproved retirement benefit schemes (FURBS) to provide top-up pension benefits inexcess of the Inland Revenue limits.

FTSE All ShareEngineering

& Machinery Index

112100103898676

103109111124146

Fenner

86100111117115107107110150170214

Date

31 August 2000 9 November 2000

31 August 20018 November 2001

31 August 20027 November 2002

31 August 20036 November 2003

31 August 200410 November 2004

31 August 2005

Total Shareholder Return

31/08/00 31/08/01 31/08/02 31/08/03 31/08/04 31/08/05

120

100

80

60

140

160

180

200

220

Fenner FTSE All Share Engineering & Machinery Index

Fenner PLC 19

Board Remuneration Reportcontinued

20 Fenner PLC

Directors’ detailed emoluments

Annual salary, Annual fees or performance Total Total

consultancy Benefits in related emoluments emolumentsservices kind* bonus** 2005 2004

£ £ £ £ £

ExecutiveMark Abrahams 258,742 29,125 129,372 417,239 346,789Richard Perry 162,750 26,820 81,375 270,945 223,073Non-executiveColin Cooke*** 90,100 - - 90,100 90,100Thomas Glucklich 34,000 - - 34,000 27,392David Buttfield 31,000 - - 31,000 24,974

576,592 55,945 210,747 843,284 712,328

*Benefits in kind include the provision of a car allowance and healthcare insurance for both executive directors.**The bonuses will be paid by way of additional Company contributions into the respective funded unapprovedretirement benefit schemes. ***By an agreement between the Company, Steels Management Limited and Colin Cooke dated 24 June 1993, asamended by subsequent supplemental agreements between the same parties the last one being dated 21 December2004, Steels Management Limited agreed to provide the services of Colin Cooke as a non-executive director and Chairman of the Company until the AGM 2008. Steels Management Limited may at any time terminate the agreement bygiving 12 months notice in writing to the Company. In the year ended 31 August 2005 £90,100 (2004 £90,100), includinga £5,100 car allowance, was payable under this agreement. No remuneration was paid directly to Colin Cooke, nor wereany pension contributions paid on his account. The non-executive directors do not participate in any Company pensionscheme, nor do they receive benefits in kind.No director waived emoluments in respect of the year ended 31 August 2005.

Share schemesInterests in share optionsDetails of options held by directors are set out below:

Earliest exercise Expiry Exercise August 2004 Exercised Lapsed August 2005

date date price Number in year in year Number

Mark Abrahams 27 July 1998 26 July 2005 144.00p 73,380 - 73,380 -

Richard Perry 15 November 1997 14 November 2004 132.05p 157,895 - 157,895 -27 July 1998 26 July 2005 144.00p 26,315 - 26,315 -

No options have been granted or exercised during the year. No other directors have been granted share options in theshares in the Company. None of the terms and conditions of the share options was varied during the year. All optionswere granted in respect of qualifying services and all have now lapsed.

The market price of the Company’s shares at the end of the financial year was 145.25p and the range of market pricesduring the year was between 103.9p and 163.0p.

Interests in sharesThe interests of the directors in the 25p ordinary shares of the Company were:

31 August 2005 1 September 2004 Number Number

Mark Abrahams 394,840 360,255Richard Perry 327,032 290,173Colin Cooke 210,408 198,596Thomas Glucklich 1,000 1,000David Buttfield - -

All directors’ interests are beneficially held. There have been no changes in the interests set out above between31 August 2005 and 9 November 2005.

Long-term incentive schemesShares awarded to executive directors under the long-term incentive plan are as follows:

End of Plan Cycle 1 September Provisional Shares Shares 31 August Value & Award

Allocation 2004 allocation awarded lapsed 2005 awarded Determinationdate Number Number Number Number Number £ date

Mark Abrahams7 November 2001 161,296 161,296 38,598 122,698 - 46,318 16 November 20046 November 2002 196,569 200,559 200,559 6 November 20055 November 2003 212,623 216,939 216,939 5 November 200610 November 2004 155,046 155,046 10 November 2007

Richard Perry7 November 2001 104,667 104,667 25,047 79,620 - 30,056 16 November 20046 November 2002 127,390 129,976 129,976 6 November 20055 November 2003 136,925 139,704 139,704 5 November 200610 November 2004 97,524 97,524 10 November 2007

Total of awards in year 63,645 76,374

The number of shares provisionally allocated was adjusted under the rules of the long term incentive plan following theShare Placing and Open Offer.

The performance criteria attached to the shares that were awarded on 16 November 2004 and those provisionallyallocated on 10 November 2004 relate to the Company’s TSR, which is compared with the TSR of The Peer Group.

There have been no variations in the terms and conditions of scheme interests during the year. All awards under long-termincentive plans were in respect of qualifying services.

The Plan Cycle ending on 16 November 2004 was independently evaluated and an award of shares made representing24% of the original award of shares was made on 14 December 2004. The market value (as defined in the Rules of thePlan) of an Ordinary Share of the Company at the beginning of the Plan Cycle was 103.9p, at the end of the Plan Cyclewas 120.00p and the market value used on 16 November 2004 for the new Plan Cycle was 127.7p (125.16p afteradjustment for the Share Placing and Open Offer).

The Performance Graph on page 18 showing TSR gives an indication of whether each LTIP Plan Cycle will achieve theperformance criteria, based upon the share price at 31 August 2005.

Given the nature of the performance calculation, it could be misleading to indicate a likely outcome for future shareawards.

Fenner PLC 21

Signed on behalf of the Board of DirectorsT C Glucklich Chairman of the Remuneration Committee9 November 2005

Additional information as required by the Listing RulesTransfer value of additional accrued benefits

Additional accrued benefits earned in year earned in year less directors’ contributions£ £

Mark Abrahams 2,700 26,400Richard Perry 3,500 36,200

The accrued pension entitlement is the amount that the director would be paid annually on retirement based on serviceto 31 August 2005. The Listing Rules require the increase in this amount to be disclosed excluding inflation. Thebenefits do not allow for any retained benefits which the directors may have relating to previous employment. Thepension benefits exclude any additional pension purchased by additional voluntary contributions.

The increase in the accrued entitlement is the difference between the accrued entitlement at the year end (31 August2005) and the accrued entitlement at the previous year end (31 August 2004).

The pension benefits are based on the directors’ pensionable salaries which are limited to the Inland Revenue earningscap (currently £105,600 per annum).

All transfer values have been calculated on the basis of actuarial advice in accordance with Actuarial Guidance NoteGN11. The transfer values of the accrued entitlement represent the value of assets that the pension scheme wouldneed to transfer to another pension provider on transferring the scheme’s liability in respect of the directors’ pensionbenefits. They do not represent sums payable to individual directors and, therefore, cannot be added meaningfully toannual remuneration.

The transfer value of the increase in accrued benefits, required by the Listing Rules, discloses the current value of theincrease in accrued benefits that the director has earned in the period, whereas the change in his transfer value,required by the Companies Act discloses the absolute increase or decrease in his transfer value and includes thechange in value of the accrued benefits that results from market volatility affecting the transfer value at the beginning ofthe period, as well as the additional value earned in the year.

The Company also makes contributions to funded unapproved retirement benefit schemes (FURBS) in respect of theexecutive directors. The contributions made by the Company, excluding the annual performance related bonus, were:

2005 2004£ £

Mark Abrahams 174,652 170,430Richard Perry 108,229 127,779

PensionsDirectors’ pension entitlementSet out below are details of the pension benefits to which each of the executive directors is entitled.

Accrued Increase in Accrued Transfer Transfer Increase inentitlement accrued entitlement value at value at transfer value31 August entitlement 31 August 31 August 31 August less directors’

2004 over the year 2005 2004 2005 contributions£ £ £ £ £ £

Mark Abrahams 35,900 4,000 39,900 304,200 397,900 93,700Richard Perry 34,000 4,700 38,700 378,200 495,500 109,140

22 Fenner PLC

Board Remuneration Reportcontinued

The directors submit their report and the audited Group accounts for the financial year ended 31 August 2005.

Principal activities and review of businessFenner is a global manufacturer and distributor of conveyor belting and reinforced precision polymer products.

The trading year under review, future prospects and the Group’s research and development activities are covered inthe reports on pages 1 to 11.

Results and dividends £000

Group profit for the year 6,531

DividendsInterim 1.975p per share – payable 2,148Final 3.85p per share – proposed 6,028

8,176

Charitable donationsDuring the year the Group contributed £4,000 (2004 £6,000) to United Kingdom charitable organisations.

Substantial shareholdingsThe register maintained by the Company under Section 211 of the Companies Act 1985 records that on 9 November2005 interested parties with substantial individual interests were as follows:

% ofNumber of issued

Interested party shares capital

Brown, Shipley & Co. Ltd 11,781,965 7.53%Hermes Administration Services Limited 10,223,365 6.53%UBS Global Asset Management Life Limited 8,737,676 5.58%Legal & General Investment Management 5,289,079 3.38%

Directors and their interestsThe names of the directors of the Company who served during any part of the year are shown in the BoardRemuneration Report.

Details of the directors’ beneficial interests in the ordinary shares of the Company, in share options over the ordinary sharecapital of the Company and in the Fenner Long Term Share Incentive Plan are given in the Board Remuneration Report.

Save as disclosed in the Board Remuneration Report:a) no director has any interest (beneficial or non-beneficial) in any share or loan capital of the Company or any of its

subsidiaries;b) no change in the interests of directors has occurred between the end of the financial year and 9 November 2005;

andc) there were no contracts of significance subsisting during or at the end of the financial year in which a director of

the Company was materially interested.

There are no directors retiring by rotation at the forthcoming Annual General Meeting but Thomas Glucklich will retire atthat Meeting after 10 years service. David Buttfield will be recommended for re-election for a new three year term andDavid Campbell will be recommended for election following his appointment to the Board on 1 November 2005.

Directors’ Report

Fenner PLC 23

Supplier payment policyGiven the international nature of the Group’s operations, the Group does not operate a standard code in respect ofpayments to suppliers. Individual operating businesses are responsible for agreeing the terms and conditions underwhich transactions with their suppliers are conducted, including the terms of payment. It is the Group’s policy thatpayments to suppliers are made in accordance with these terms. The average creditor days for the Group during the yearended 31 August 2005 was 52 days (2004 54 days). The Company does not have any trade creditors.

Employment policyThe Group operates worldwide and its employment policies are designed to meet local conditions and requirements butare established on the basis of the best practices in each country. Wherever the Group operates, it encourages theprovision of equal employment opportunities regardless of sex, race, religion or age.

The Group’s policy is to secure good relations between management and all employees, to promote a betterunderstanding of all the issues, both internal and external, that influence the Group’s business performance and toimprove performance and productivity. Formal and informal meetings are used to consult employees and to keep theminformed about the performance of the Group. The practices of consultation and involvement vary from country tocountry according to local customs, legal considerations and the size of the operation. The regular worldwide issue of aGroup newspaper assists the process of communication, as do briefing meetings, information bulletins and meetingswith employee representatives.

The Group continues to recognise its social and statutory duty to employ disabled persons and does all that ispracticable to meet this responsibility. Full and fair consideration is given to the recruitment, training, careerdevelopment and promotion of disabled persons bearing in mind the aptitude and ability of the individual concerned.

If an employee becomes disabled while employed by the Group, wherever possible, he or she will continue to beemployed in the same job. If this action is not practicable or possible then every effort will be made to find suitablealternative employment. In these circumstances retraining would be made available using Group resources as well asby contact with the local disabilities employment adviser.

Environmental policyFenner PLC recognises and accepts that concern for the environment is an integral and fundamental part of theCompany's corporate business strategy.

The Company actively seeks to reduce its impact on the environment to the lowest practical level by ensuring that alloperations and activities within the Group exemplify best contemporary practice in respect of the environment. Anythreat of pollution from the Group’s activities is identified and either eliminated or controlled effectively.

Independent auditorsA resolution to re-appoint PricewaterhouseCoopers LLP as independent auditors to the Company will be proposed at theAnnual General Meeting.

Annual General MeetingAs special business at the forthcoming Annual General Meeting resolutions will be proposed to renew the directors’authority to allot relevant securities, to disapply the statutory pre-emption rights to a limited extent and to make marketpurchases of Ordinary Shares in the Company subject to defined limits. The proposed resolutions and further detailsregarding these proposals are set out in the Chairman’s explanatory letter accompanying the Notice of the AnnualGeneral Meeting.

Signed on behalf of the Board of DirectorsC I Cooke Chairman9 November 2005

Directors’ Reportcontinued

24 Fenner PLC

Independent Auditors' Report to the members of Fenner PLC

We have audited the financial statements which comprise the Group profit and loss account, the balance sheets,Group cash flow statement, the statement of total recognised gains and losses, and the note of historical cost profitsand losses, the reconciliation of movements in shareholders’ funds and the related notes. We have also audited thedisclosures required by part 3 of Schedule 7A to the Companies Act 1985 contained in the Board Remuneration Report(“the auditable part”).

Respective responsibilities of directors and auditorsThe directors’ responsibilities for preparing the annual report and the financial statements in accordance withapplicable United Kingdom law and accounting standards are set out in the statement of directors' responsibilities. Thedirectors are also responsible for preparing the Board Remuneration Report.

Our responsibility is to audit the financial statements and the auditable part of the Board Remuneration Report inaccordance with relevant legal and regulatory requirements and United Kingdom Auditing Standards issued by theAuditing Practices Board. This report, including the opinion, has been prepared for and only for the Company’smembers as a body in accordance with Section 235 of the Companies Act 1985 and for no other purpose. We do not,in giving this opinion, accept or assume responsibility for any other purpose or to any other person to whom this reportis shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

We report to you our opinion as to whether the financial statements give a true and fair view and whether the financialstatements and the auditable part of the Board Remuneration Report have been properly prepared in accordance withthe Companies Act 1985. We also report to you if, in our opinion, the Directors' Report is not consistent with thefinancial statements, if the Company has not kept proper accounting records, if we have not received all the informationand explanations we require for our audit, or if information specified by law or the Listing Rules regarding directors'remuneration and transactions is not disclosed.

We read the other information contained in the annual report and consider the implications for our report if we becomeaware of any apparent misstatements or material inconsistencies with the financial statements. The other informationcomprises the Directors' Report, the financial highlights, the Chairman's Statement, the Chief Executive Officer'sReview, the Group Finance Director's Review, the Corporate Governance statement and the unaudited part of theBoard Remuneration Report

We review whether the Corporate Governance statement reflects the Company's compliance with the nine provisions ofthe 2003 FRC Combined Code specified for our review by the Listing Rules of the Financial Services Authority, and wereport if it does not. We are not required to consider whether the Board's statements on internal control cover all risksand controls, or to form an opinion on the effectiveness of the Company’s or Group's corporate governance proceduresor its risk and control procedures.

Basis of audit opinionWe conducted our audit in accordance with auditing standards issued by the Auditing Practices Board. An auditincludes examination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statementsand the auditable part of the Board Remuneration Report. It also includes an assessment of the significant estimatesand judgements made by the directors in the preparation of the financial statements, and of whether the accountingpolicies are appropriate to the Company and Group’s circumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considerednecessary in order to provide us with sufficient evidence to give reasonable assurance that the financial statementsand the auditable part of the Board Remuneration Report are free from material misstatement, whether caused by fraudor other irregularity or error. In forming our opinion we also evaluated the overall adequacy of the presentation ofinformation in the financial statements.

OpinionIn our opinion: