Ralph C. Lewars Financial Sector Supervision Adviser CARTAC The views expressed in this presentation are entirely my own and do not necessarily reflect the opinion nor the policy of either the IMF or CARTAC.

Transcript

Ralph C. LewarsFinancial Sector Supervision AdviserCARTAC

The views expressed in this presentation are entirely my own and do not necessarily reflect the opinion nor the policy of either the IMF or CARTAC.

Discussion Topics An overview of the work of CARTAC in the region.

…how CARTAC links into the IMF Funding and operation

The Pension Landscape in the Caribbean Social Security Schemes, and Private Pension Plans Systemic Risk and Financial Stability Status of Legislation in the Caribbean Issues and Challenges Reform Options

Measuring Risk and Vulnerabilities Stress Testing Financial Stability Indicators

About CARTAC The Caribbean Regional Technical Assistance Centre

(CARTAC) is one of ten IMF Regional Technical Assistance Centers (RTACs) located around the world in the Pacific, the Caribbean, in Africa, the Middle East, India and Central America.

These Centers were created to: help countries strengthen human and institutional capacity design and implement sound macroeconomic, and financial

sector policies that promote growth and reduce poverty. Became operational in 2001

CARTAC Provides Technical Assistance in Six core areas Macroeconomic Programming and Advice Public Financial Management Tax and Customs Administration Financial Sector Supervision Financial Stability and Crisis Management Real Sector and External Statistics

NB: Since its inception, CARTAC has provided TA to several countries in the region on updating their respective Pension legislation and enhancing supervisory oversight, and developing risk and vulnerability indicators for the sector.

Who Funds CARTAC International donors

The government of Canada through it’s aid office Global Affairs Canada (GAC);

International Monetary Fund (IMF); United Kingdom (DFID); and European Union (EU)

The Government of Barbados finances the costs of office facilities, while the other 20 beneficiary countries make annual contributions to the Centre’s operating expenses.

Other contributors since the inception of CARTAC include Australia (AUSAID), Caribbean Development Bank (CDB), the Inter-American Development Bank (IADB), the United Nations Development Programme (UNDP), Ireland, the United States (USAID), and the World Bank (WB).

How CARTAC operates Regional resource center of the International Monetary

Fund headed by a Centre Coordinator appointed by the IMF

The priorities of CARTAC are approved by a Steering Committee (SC) consisting of representatives of recipient countries, donors and the IMF.

CARTAC, combines on-the-ground capacity building with strategic advice and support from the IMF

All technical assistance (TA) is integrated with the IMF’s lending and surveillance operations, and coordinated with other IMF TA, as well as that of other providers.

All TA is backstopped by IMF, ensuring quality and consistency of policy advice.

The Pension Landscape in the Caribbean

Presenter

Presentation Notes

“Global Pension Matters and Stress Test for Local Pension Plans”. The seminar is aimed at giving an overview of the changes that are occurring around the world that directly/indirectly impact the pension industry and what we can do in Jamaica to mitigate the associated risks or welcome the possible opportunities. Pension reform is a subject of hot debate around the world, driven partly by the increase in public awareness about the need for retirement income planning. Given the challenges associated with public retirement income and social security programs, individuals and governments alike have started to give the retirement income issue increased attention. The recommendations of public and private financial advisors generally involve some form of private retirement savings, be it at the level of the individual or the workplace. The motivation for these common recommendations lies in the considerable projected financial problems of the pay-as-you-go (PAYG) systems, as well as the trend towards DC plans rather than DB plans.

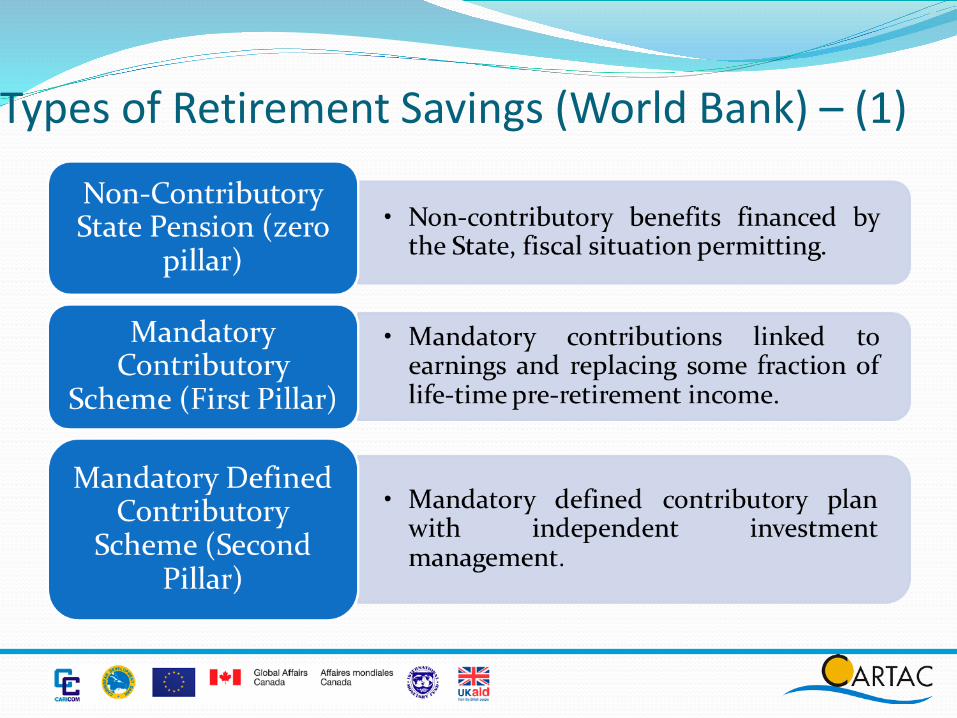

Types of Retirement Savings (World Bank) – (1)

Types of Retirement Savings (World Bank) – (2)

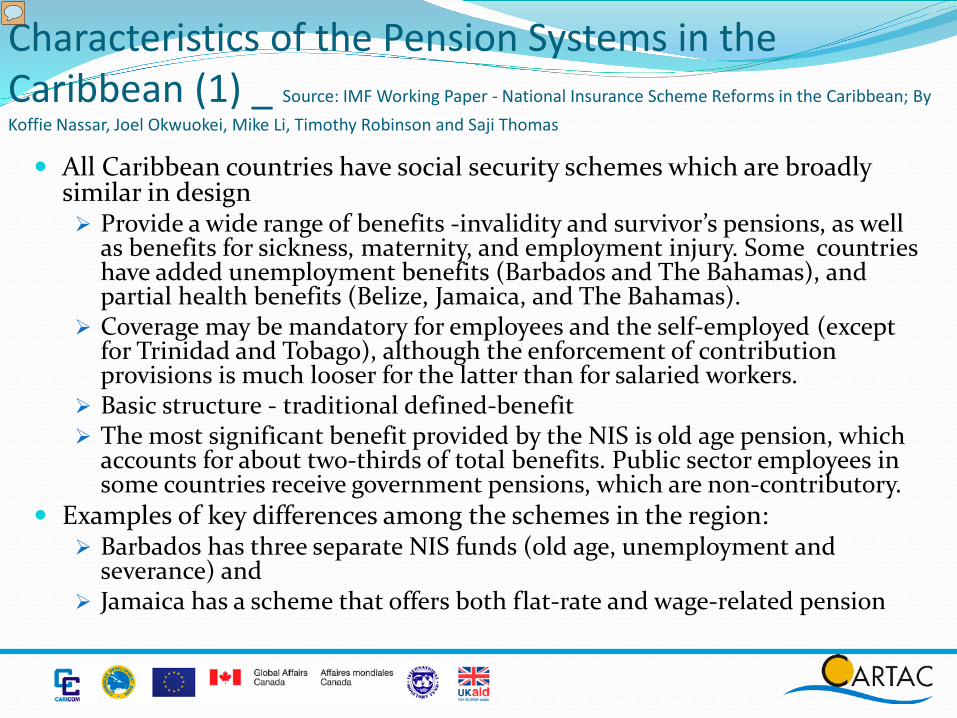

Characteristics of the Pension Systems in the Caribbean (1) _ Source: IMF Working Paper - National Insurance Scheme Reforms in the Caribbean; By Koffie Nassar, Joel Okwuokei, Mike Li, Timothy Robinson and Saji Thomas

All Caribbean countries have social security schemes which are broadly similar in design Provide a wide range of benefits -invalidity and survivor’s pensions, as well

as benefits for sickness, maternity, and employment injury. Some countries have added unemployment benefits (Barbados and The Bahamas), and partial health benefits (Belize, Jamaica, and The Bahamas).

Coverage may be mandatory for employees and the self-employed (except for Trinidad and Tobago), although the enforcement of contribution provisions is much looser for the latter than for salaried workers.

Basic structure - traditional defined-benefit The most significant benefit provided by the NIS is old age pension, which

accounts for about two-thirds of total benefits. Public sector employees in some countries receive government pensions, which are non-contributory.

Examples of key differences among the schemes in the region: Barbados has three separate NIS funds (old age, unemployment and

severance) and Jamaica has a scheme that offers both flat-rate and wage-related pension

Presenter

Presentation Notes

The flat rate portion, which depends on the average number of contributions made by the insured, provides a base income level for the low income earners, while the wage–related portion depends on the actual amount of contributions

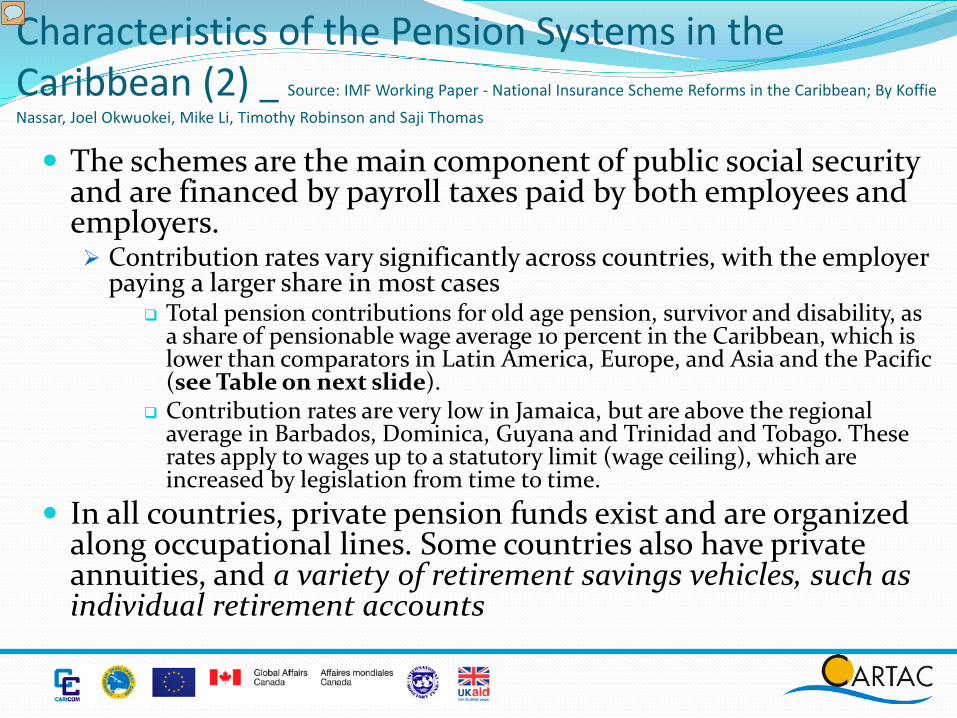

Characteristics of the Pension Systems in the Caribbean (2) _ Source: IMF Working Paper - National Insurance Scheme Reforms in the Caribbean; By Koffie

Nassar, Joel Okwuokei, Mike Li, Timothy Robinson and Saji Thomas

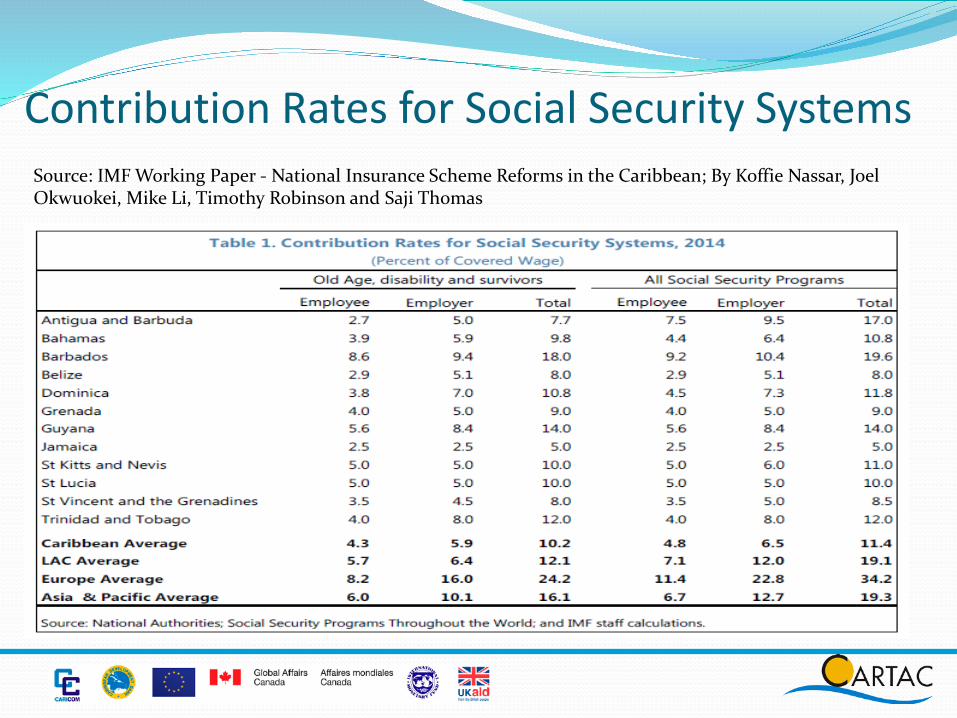

The schemes are the main component of public social security and are financed by payroll taxes paid by both employees and employers. Contribution rates vary significantly across countries, with the employer

paying a larger share in most cases Total pension contributions for old age pension, survivor and disability, as

a share of pensionable wage average 10 percent in the Caribbean, which is lower than comparators in Latin America, Europe, and Asia and the Pacific (see Table on next slide).

Contribution rates are very low in Jamaica, but are above the regional average in Barbados, Dominica, Guyana and Trinidad and Tobago. These rates apply to wages up to a statutory limit (wage ceiling), which are increased by legislation from time to time.

In all countries, private pension funds exist and are organized along occupational lines. Some countries also have private annuities, and a variety of retirement savings vehicles, such as individual retirement accounts

Presenter

Presentation Notes

Thus, a portion of wages of high income earners is excluded from the computation of contributions and does not also count towards benefits

Contribution Rates for Social Security SystemsSource: IMF Working Paper - National Insurance Scheme Reforms in the Caribbean; By Koffie Nassar, Joel Okwuokei, Mike Li, Timothy Robinson and Saji Thomas

Social Security Schemes(NIS) – Reform Options (1)Source: IMF Working Paper - National Insurance Scheme Reforms in the Caribbean; By Koffie Nassar, Joel Okwuokei,

Mike Li, Timothy Robinson and Saji Thomas

Long-term projections point to continuing unfavorable demographic trends and large increases in pension spending

The actuarial deficits calculated as the Present Discount Values (PDVs) of future benefit expenditure minus income over the period 2016-60 at a discount rate of 5 percent, range from 0.7 percent of GDP in Barbados to 92 percent of GDP in Jamaica.

In the absence of reforms, contingent liabilities of several percentage points of GDP could materialize in few countries, putting substantial pressure on public finances

Risks can be mitigated by taking timely reform measures - raising the retirement age; freezing old-age pension benefits; and increasing the contribution rate.

However, the above would not be sufficient to effectively contain actuarial deficits in some countries

Consider measures to improve coverage, with a view to reducing the old age dependency ratio. Improve public information and disclosure Independent oversight and evaluation of social security schemes, and public

sector pension plans, including the publication of actuarial reports (periodically –every 3/5 year?)

Presenter

Presentation Notes

(nb: Barbados is the only country in the Caribbean that has substantially reformed its traditional PAYGO system during the last decades)

Pension Funds – Systemic Risk and Financial Stability (1) There are over 900 private pension plans operating in Trinidad & Tobago,

Barbados and Jamaica with assets of over USD800 Million. Pension assets account for a significant share of total financial assets in some

countries Pension Investments are mainly concentrated in two major asset classes

(government bonds, equities) in the Caribbean Concentration of investment in individual countries (Often the result also

of investment portfolio limits) elevate risk, due to country-specific riskfactors, illiquidity of markets, short maturity of government debt

Though it brings benefit to local capital markets, benefits fromdiversification not fully realized

Can pension funds contribute to systemic risk and financial instability? Pension Plans are one of the largest groups of institutional investors and

can therefore have a significant impact on financial markets Sizeable re-allocations of assets (between fixed income and equities) in

pension plans can also significantly impact financial stability

Presenter

Presentation Notes

Data Limitations: Public disclosure of Prudential and Financial Information on pension plans is quite limited in many countries in the Caribbean region. As in the rest of the world, financial linkages have continued to increase in the Caribbean region. Motivation for financial linkages includes risk diversification, search for higher yield and a desire to increase market share, as well as increased integration in the real sector, including effects from formal arrangements like the CARICOM Single Market and Economy (CSME).

Pension Funds – Systemic Risk and Financial Stability (2); Source: E Philip Davis, 2016 Pension funds may not pose systemic risks in the sense of “a

combination of events that threatens the functioning of the financial system in its entirety” (Beetsma and Vos 2016) Pension funds are typically not leveraged so no multiplier effects in their

profits and losses Average duration of pension fund liabilities 15-20 years so natural long

term investors DB pension funds can be technically insolvent but in many countries

cannot go bankrupt (change parameters such as contributions, indexation, entitlements, to return to solvency gradually). For DC funds assets are the same as liabilities so issue of insolvency usually does not arise, unless there are guarantees

Pension funds are commonly restricted from using derivatives except for hedging

EIOPA stress tests show generally stabilizing influence for financial markets by portfolio rebalancing following sharp price change of a given asset

Presenter

Presentation Notes

• But one important cause for vigilance – trend of imposing similar risk-based solvency requirements on all financial players (Basel III, EU CRD IV, EU Solvency II, and potentially EU Solvency II-like rules for pension funds) plus fair value accounting – this makes sense from a micro perspective, but may carry the danger that the behaviour of all players on the financial markets becomes more similar – especially in reaction to sizable shocks – which may amplify these shocks and have a destabilising effect on financial markets. This way microprudential supervision may create system risks through the backdoor. • Procyclical pattern: – Inadequate surplus build-up in upturn – Fire sales in downturn – Heavy funding needs after downturn

Pension Funds: Transmission Channels – Sources of Feedback Effects on the Macroeconomy

Source: Adopted from S. Nicholls; 2016

Jamaica: Private Pension Plan Investments - March 2017 (J$Bn)

Presenter

Presentation Notes

As per the spreadsheet, what was presented in the slide as “Other” actually comprised: Deposits Commercial Paper Repurchase Agreements (Corporate) Bonds and Debentures Mortgage Loans Other Loans Promissory Notes Lease Other Investments Other Net Assets (Receivables and Payables) Kindly note that the quarterly pension industry statistics can be found on the FSC’s website at this link: http://www.fscjamaica.org/regulated-industries/content-1247.html. The explanation for Deposit Administration Contracts and Pooled Funds is as follows: Deposit Administration Contracts are pension assets held on the balance sheet of insurance companies (that are also licensed to provide pension investment management services). The DA Contract typically offers a guaranteed rate of return, as established by the insurance company. Pooled Funds are broken down into two main subsets: Type I Pooled Funds and Type II Pooled Funds. Type I Pooled Funds are off-balance sheet pooled funds created by licensed pension investment managers, with the sole purpose of investing the assets of more than one pension plan. Only pension plan assets are allowed in Type I Pooled Funds. Type II Pooled Funds are unit trusts, mutual funds and other such collective investment schemes (which are not Type I Pooled Funds).

Private Pension Plans – Regulatory and Supervisory Implications (1); Source: Flavio Marcilio Rabelo Objectives of pension supervision:

Protection of benefits; ensuring adequacy of coverage; and financial stability (Kiel and Bacchas, 2016)

In all countries with private pension systems, the main elements/features of the legislative and regulatory architecture are:

licensing (authorization/registration) criteria; Accounting for pension liabilities governance rules; asset segregation rules; independent custodian; external audit/actuarial review; disclosure requirements; investment limits (“prudent person approach” and the “use of quantitative restrictions”); guarantees; minimum capital and reserves; and regulations on costs and fees.

The relative emphasis given to each of these components depends on the nature of the plan and benefits and also on the development of domestic capital and money markets

The type of benefit structure of pension plans (defined benefit or defined contribution) and form of provision (occupational or personal pension plans) influences the scope of regulation and supervisory oversight:

Defined benefit (DB) plans use a benefit formula based on years or service and salary averages – benefit is guaranteed by the assets allocated in the pension fund.

Key concern – adequacy of funding to finance accrued liabilities (pension promises).

A key objective of regulation and supervisory oversight is to mitigate the insolvency risk of these plans.

In defined contribution (DC) plans, the final benefit depends on the value of the participant’s accumulated account balance. There is no guaranteed benefits. These plans are by definition always fully

funded and the investment risk is entirely borne by the participant. However, due to irregular or small contribution or poor investment returns the

participant may not accumulate a sufficient amount of money to provide for an adequate replacement rate in retirement.

Presenter

Presentation Notes

Most pension plans are set up under a trust with either an institutional trustee or a specified number of individual trustees who are nominated by the members of the plan, in both cases the appointed trustee(s) are responsible for overseeing the administration of the affairs of the plan. The main roles of a pension plan trustee are really to ensure legislative compliance and to ensure that the plan is administered in the best interest of the beneficiaries. They are held to the fiduciary standard of care established at common law for the conduct of trustees, but they must also satisfy the legislative standards and requirements. Trustees are responsible for maintaining proper accounts, establishing a statement of investment policy to be followed by the investment manager, appointing agents such as actuaries, investment managers, accountants and lawyers and monitoring the activities of these agents. They are also responsible for monitoring the financial and actuarial position of the fund or scheme so that appropriate adjustments can be made as needed.

Private Pension Plans – Regulatory and Supervisory Implications (3) DB plans are more difficult to administer than pure DC plans

DB plans need to keep funding levels and solvency at sufficient levels in order to be provide promised benefits at or after retirement

Actuarial calculations/projections required Good ALM expertise required to select the types of investment and the

maturity of the assets to match the projected pension benefits liabilities

In a pure DC plan, it is the individual or plan participants that ultimately ends up bearing both the risk of longevity and the investment risk prior to and after retirement.

In pure DB plans, these risks are generally borne by the employer, the pension fund, or the state (as guarantor). Individuals are theoretically protected against any kind of fluctuation in terms of the underlying returns earned on the pension asset and changes in life expectancy

Presenter

Presentation Notes

Heller (2004) presents an interesting discussion of the risk exposure of governments as a result of explicit and implicit contingent liabilities. One example of the latter derives from the government’s likely inability to stay on the sidelines in the face of a major crisis in the (nonguaranteed) private pensions market. Extreme shocks are however likely to affect individuals even in a pure DB environment as guarantees by the company or the state may become too costly to bear.

Occupational pension plans (defined benefit or defined contribution) are part of a company’s total remuneration package Not a commercial product and are not accessible to the general

public Regulation and supervisory oversight are designed to ensure

that the rules of these plans are clearly stated and that the employer complies abide by the established rules

Personal pension plans are savings vehicle offered mainly by insurance companies to the general publicMostly defined contribution, although some may offer minimum

return guarantee Supervisory oversight is needed to ensure and/or monitor

maintenance of required solvency margins by the sellers of these products

Accounting for Pension Liabilities (1) Accounting for pension liabilities incurred by the public sector -

promised future pension payments under a public PAYG pension system may not/do not completely appear in official government statistics

the reason for this absence of accounting is attributed to: these are promised payments, and may not necessarily be legally enforceable claim on future resources - because they are implicit by nature and they are often easier to renege on

Accounting for private pension plans: the accounting standard known as IAS 19 deals with pension liabilities of companies

Under IAS 19, companies are required to provision for future benefit liabilities. If the plan is based on final salaries, companies have to project the liabilities on the basis of projected wages instead of current wages. Further, assets valuation has to be based on market values and benefit obligations have to be discounted using current market rates for a similar duration as the pension promises, which could lead to volatility in the balance sheet.

Presenter

Presentation Notes

Key to IAS 19 is the concept of “constructive obligation.” This term is meant to precisely go beyond the purely legal aspects of enforceability of claim and considers that companies have to account for claims that represent “an obligation that derives from an enterprise action where: (a) by an established pattern of past practices, published policies, or a sufficiently specific current statement, the enterprise has indicated to other parties that it will accept certain responsibilities; and, (b), as a result, the enterprise has created a valid expectation on the part of other parties that it will discharge these responsibilities.” Pension liabilities are sometimes shifted from a corporation to the government against a compensatory payment, often a lump-sum. By doing so, companies are able to offload their pension liabilities and risks to a government entity. Such a transaction clearly satisfies all characteristics of a purchase of an insurance contract, as it means offloading risk against payment of a “premium.” On the government side, demand for such transaction simply stems from the fact that they can usually book the lump-sum as current income in the yearly budget, while at the same time not having to recognize the implicit pension liability anywhere.

Status of Pension Legislation in the Caribbean – Overview

All countries are committed to the reform of their respective pension system but are at different stages of evolution due to several factors, including other domestic priorities

The absence of legislation (or updated legislation) in some jurisdictions has constrained the authority of the pension regulators/supervisors, and their ability to take corrective actions. For example, pension regulators may not have the power to request that contributions are paid over within a certain time or that plans should fund deficits

Inadequate and/or timely prudential reporting Gaps in registration of pension plans makes it difficult to develop

comprehensive knowledge of the industry

Presenter

Presentation Notes

Although the legislation in Belize was recently passed, the regulator is facing similar challenges. Another challenge for Belize is the fear that pension plans may not register by the timeline given, which would weaken the position of the regulator. Working Group On Pension Reform To Be Established in Jamaica Finance and Public Service Minister, Hon. Audley Shaw, says a Working Group comprising members of the Government and unions representing civil servants is being established to facilitate further discussions on the pension reform programme. Mr. Shaw said the group will explore issues arising in relation to the programme’s administration, with a view to arriving at a consensus at how best these can be addressed. The programme will be anchored on the Pensions (Public Service) Act 2017 and the Constitution (Amendment) (Establishment Fund) (Payment of Pensions) Act 2017 which were passed in the House of Representatives earlier this year, but is still being debated in the Senate. “I am committed, along with State Minister, Hon. Rudyard Spencer, to meet with the unions so that we can explain things more carefully…(and) work together to thrash out whatever concerns they have in terms of the administration of the programme…even after the Bills are passed,” Mr. Shaw said. The Pensions (Public Service) Act 2017 will establish a defined benefit contributory scheme, which will require all pensionable officers to contribute five per cent of salary. It also provides for the establishment of a segregated fund for contributions and gradual increase in the retirement age to 65. The Constitution (Amendment) (Established Fund) (Payment of Pensions) Act 2017 will amend the Constitution to facilitate the payment of pensions, gratuities and allowances out of the pension fund.

Pension Legislation in the Caribbean (1)

Presenter

Presentation Notes

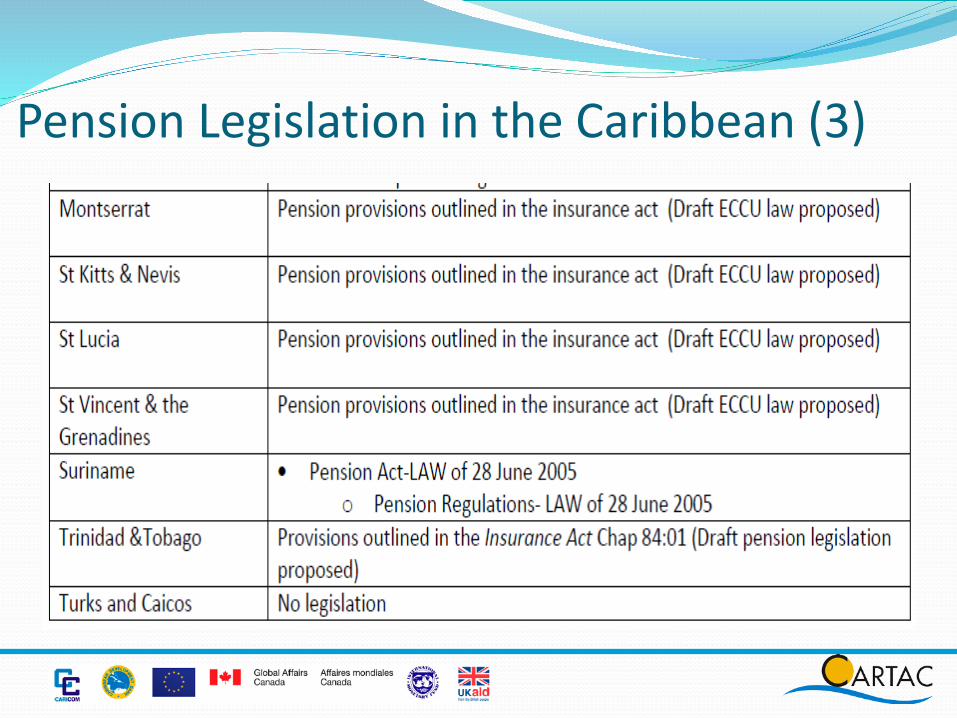

• Barbados, Bermuda, Cayman Islands, Jamaica and Suriname have enacted specific legislation to monitor and supervise the pension industry. • Trinidad and Tobago and the Eastern Caribbean Countries currently operate under pension provisions enacted over decades ago which are outlined in the Insurance Legislation. These countries have proposed legislative reforms. The Eastern Caribbean Countries have proposed a uniform Insurance Bill which includes and expanded Pension legislation and is intended to serve the countries in that region. • The pension legislation in Belize was recently passed. • Bahamas does not have pension legislation in place and have proposed legislative reforms. • Guyana is in the process of drafting separate pension legislation. • Anguilla, Haiti and Turks and Caicos do not have pension legislation in place.

Pension Legislation in the Caribbean (2)

Presenter

Presentation Notes

Working Group On Pension Reform To Be Established in Jamaica Finance and Public Service Minister, Hon. Audley Shaw, says a Working Group comprising members of the Government and unions representing civil servants is being established to facilitate further discussions on the pension reform programme. He made the announcement during Thursday’s (September 14) joint Government of Jamaica/International Monetary Fund (IMF) press conference for the second review under the Precautionary Stand By Agreement, at the Office of the Prime Minister. Mr. Shaw said the group will explore issues arising in relation to the programme’s administration, with a view to arriving at a consensus at how best these can be addressed. The programme will be anchored on the Pensions (Public Service) Act 2017 and the Constitution (Amendment) (Establishment Fund) (Payment of Pensions) Act 2017 which were passed in the House of Representatives earlier this year, but is still being debated in the Senate. “I am committed, along with State Minister, Hon. Rudyard Spencer, to meet with the unions so that we can explain things more carefully…(and) work together to thrash out whatever concerns they have in terms of the administration of the programme…even after the Bills are passed,” Mr. Shaw said. The Pensions (Public Service) Act 2017 will establish a defined benefit contributory scheme, which will require all pensionable officers to contribute five per cent of salary. It also provides for the establishment of a segregated fund for contributions and gradual increase in the retirement age to 65. The Constitution (Amendment) (Established Fund) (Payment of Pensions) Act 2017 will amend the Constitution to facilitate the payment of pensions, gratuities and allowances out of the pension fund. Pension reform, which was prioritized under Jamaica’s four-year Extended Fund Facility that concluded in October 2016, remains a structural benchmark under the three-year successor Precautionary Stand By Arrangement.

Pension Legislation in the Caribbean (3)

Registration, Monitoring and Supervision of Pension Plans in the Caribbean Registration:

Jamaica has registered pension plans, trustees and their agents Barbados, Bermuda, Cayman, Suriname and Trinidad and Tobago have carried out registration of

pension plans The Eastern Caribbean countries of Grenada, St. Vincent & the Grenadines, St. Lucia and Antigua

and Barbuda are in the process of registering pension plans. The other countries either have not commenced registration, despite having the authority to do so

or have no power to register pension plans.

Monitoring and Supervision: Jamaica has adopted the risk based approach to supervision and is using an Early Warning Risk

tool (looks at the frequency and severity of risks, provides an overall score to categorize plans into risk categories) to identify plans at risks in order to take proactive action before those risks crystalize.

Barbados has in place a system to identify plans at risks. Most of the other countries have either not started active supervision of the pension industry or

are using a compliance based approach. Only a few countries conduct onsite examinations of the industry; namely Barbados, Bermuda,

Jamaica, Trinidad & Tobago (limited to Corporate Trustees (banks) and insurance companies) and Suriname.

Presenter

Presentation Notes

Only a few jurisdictions have actively begun the monitoring and supervision of the pension industry.

Key Challenges Funding is a major constraint in advancing the pace of

reform, and objectives/mandate of the pension supervisors in the region

Impacts staff capacity, capabilities Limit ability to develop necessary processes, including prudential

reporting regime required to effectively monitor and supervise In some of the smaller jurisdictions where there is no separate pension

legislation, oversight is provided by supervisors with insurance expertise – continued specialized pension training is required

For those regulators that are at a more advanced stage of pension supervision, a key challenge going forward is to provide the tools and/or training necessary to educate trustees and agents on proper pension management/governance, including managing risks

Presenter

Presentation Notes

Overcome Challenges to Prudential Reporting (power, format, and frequency

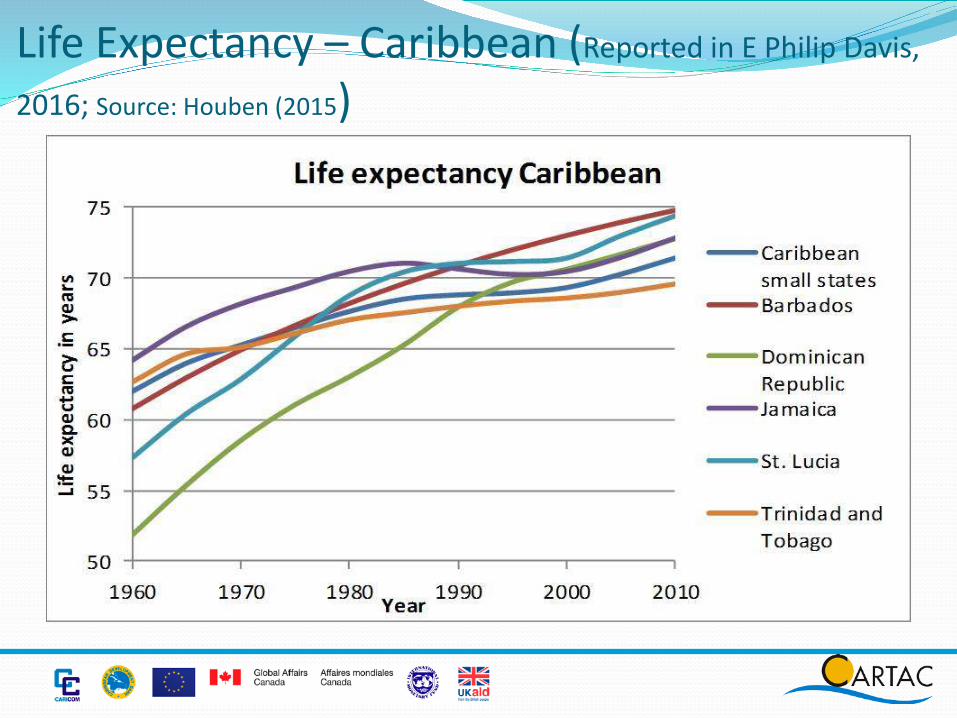

Key Challenges - E Philip Davis, 2016

The pension fund sector in most countries, including the Caribbean face several current and emerging challenges Low nominal and real long term interest rates Lack of long maturity bonds in local markets to match pension

liabilitiesUnderfunding of defined benefit plans (and social security

schemes) A search for yield, driven by pressures to invest in low risk assets Rising longevity (see chart on next slide) Increased preference for and/or conversion of defined benefit

(DB) to defined contribution (DC) plans – beneficiaries may be impacted

Regulatory challenges (accounting standard for DB; regulatory burden/cost; DB guarantees)

Presenter

Presentation Notes

Low long term interest rates Affects DB pension funds as reduces discount rate on liabilities, which are boosted as long rates fall. For DB plans it is the sponsor that has to make larger contributions, unless other parameters are changed. For DC plans the individual finds less assets accumulated for retirement, and increase in annuity prices reducing retirement income. Pressure for regulations on annuity purchase to be eased (e.g. in UK) with risk that pension assets will be dissipated On asset side lower yields raises value of bonds but typically less so than liabilities due to shorter duration. Also reinvestment risk For DC funds low rates reduce the pension that individuals receive from a given contribution rate High and often rising share of bonds in pension assets • The high share has been partly induced by tightening of solvency regulation, as well as concern over volatility of equities • Also affected by valuation method adopted and maturity of funds • It has occurred despite a shift in a number of countries from “portfolio restrictions” to “prudent person” rules for asset allocation which allow greater freedom to invest in capital uncertain assets Offsetting danger of excessive search for yield • Pension funds could seek to invest in risky assets going forward to obtain required rate of return in context of pressures already outlined • Question whether regulations should require greater reserves for riskier portfolios • Some evidence of “search for yield” especially for UK (structured products, private equity, derivatives) Longevity: Raises liabilities of DB plans and reduces the prospective pension of DC

Life Expectancy – Caribbean (Reported in E Philip Davis,

2016; Source: Houben (2015)

DC Plans – Key Policy Challenges (1) - Cass Business School, London, UK 5 March 2013

Dramatic global shift in pensions policy away from public (state) and private employer-sponsored schemes, in which benefits are pre-defined (defined benefit or DB), towards private retirement saving plans, in which benefits depend on the value of accumulated assets (e.g. defined contribution or DC)

Risk is transferred from the state and employers to individuals, including inflation, interest rate, investment and longevity risk.

The transition from DB to DC has been accompanied by a trend towards lower overall contribution rates.

These developments raise very significant concerns about the adequacy and security of future retirement income at a time when longevity is increasing and when the global experience of low returns and high volatility, following the 2008 financial crisis, have reduced public confidence in retirement savings.

DC Plans – Policy Response (2) - Cass Business School, London, UK; March 2013

DC is an integral feature of the private sector pension systems in the United States, United Kingdom, Australia, Chile and New Zealand, among others. However, DC systems might not produce adequate outcomes due to the following factors:

Low contributions Low levels of public confidence and understanding of DC plans Individuals are unable or unwilling to choose appropriate funds Investment strategies offer little or no protection Funds are too volatile in the pre-retirement phase

Public education saving for retirement requires a long-term commitment and also that it

is important to diversify the sources of retirement income implementation of full compulsion or auto-enrolment

DC Plans – Recommended Policy Response (3) - Cass Business School, London, UK; March 2013

OECD research suggests that where the investment period lasts 30-40 years, it is possible for DC systems to produce attractive returns within a low-volatility environment that can help to deliver adequate retirement incomes; provided the design and delivery features are optimal in relation to the overall pension system. These features include: Ensure the design of DC pension plans is internally coherent between the

accumulation and payout phases and with the overall pension system, including a robust investment governance framework that addresses key risks and the uncertainty inherent in saving for retirement;

Encourage high participation rates and adequate contributions (relative to the required outcome) paid over the long-term;

Promote well-designed incentives to save for retirement, particularly where participation and contributions to DC pension plans are voluntary;

Promote low-cost retirement savings instruments; Establish appropriate default investment strategies, but also provide individuals with

a choice of funds with different risk profiles and investment horizons; Encourage annuitization as a protection against longevity risk, including the supply

of annuities and cost-efficient competition in the annuity market; Ensure effective communication and to address financial illiteracy and lack of

awareness.

Conversion from DB to DC – Regulatory Issues (Kiel and Bacchas, 2017)

Conversion from DB to DC – Regulatory Issues (Kiel and Bacchas, 2017) Majority of plans in the Caribbean are not pure DC plans Typical ‘DC plans’

Guaranteed or declared interest; few credit market yield Pension benefits paid from the plan; some may annuitize Investments are not member directed

Measuring Risk and Vulnerabilities

Measuring Risks and Vulnerabilities - Stress Testing Stress testing has only recently been introduced to the pensions sector in

some countries. Practices also vary depending on the type of pension plan supervised (DB/DC/hybrid). How a portfolio will react to certain (extreme) conditions is only partially useful information when it comes to pensions, as the issue is not so much “what will the size of the accumulated pension portfolio be” as “will this deliver an adequate retirement income”

Stress testing in DC plans – process is evolving/very limited experience Stress testing DC pension funds raises the question of what is the objective of the

test, and what is being tested for/“what to stress test the pension fund against”. How to apply stress tests to pure DC pension plans is challenging since DC pension plans do not have any promised benefit or outcome goal.

Stress testing DB pension funds is more popular - DB plans provide a benefit guarantee or promise and must therefore manage their assets closely with regard to their liabilities The objective of stress testing in a DB context is to determine to what extent the assets

may be sufficient to meet future payments, given different risk scenarios.

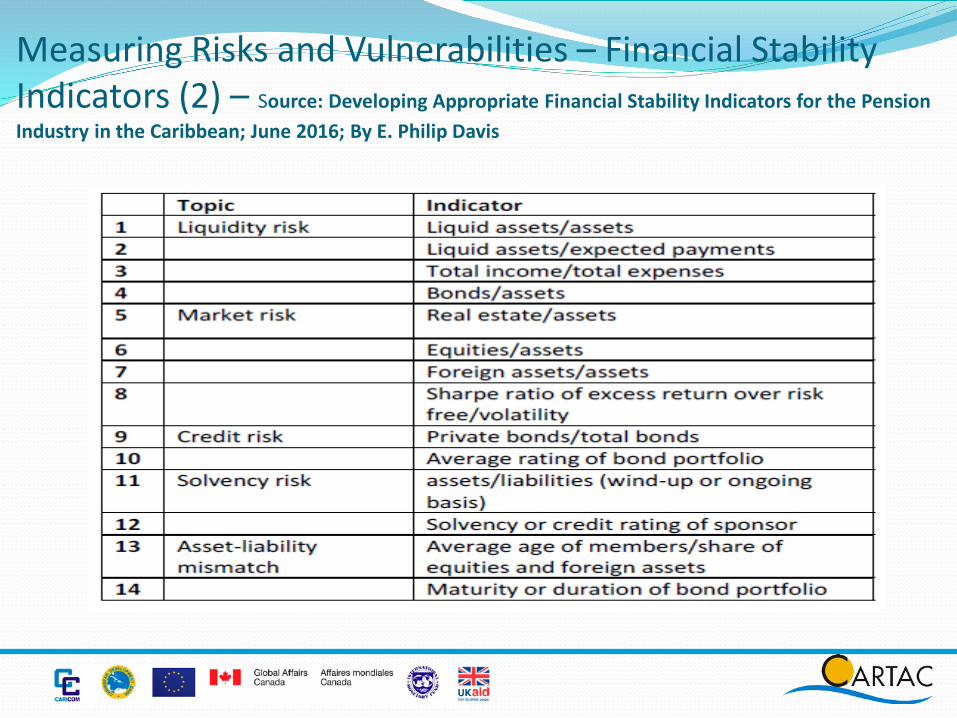

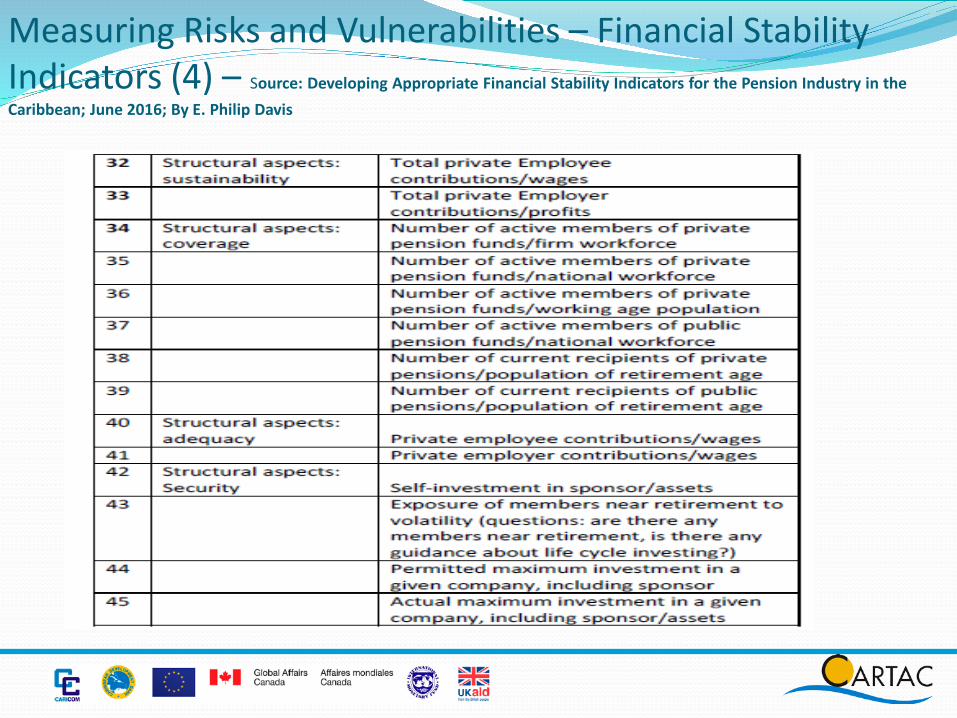

Measuring Risks and Vulnerabilities – Financial Stability Indicators (1) Development of Financial stability indicators for the pension sector is still work in

progress The IMF has suggested compilation of the following four indicators for the

pension sector Liquid assets to estimated pension payments in the next year (Liquidity ratio) Return on Assets (Earnings and Profitability) Pension Fund Assets/Total Financial System Assets Pension Fund Assets/GDP

World Bank consultants - Outcome-based Assessment (OBA) framework for pensions, but this relates more to social security considerations (W. Price, J. Ashcroft and M. Hafeman, Report, IBRD; 2014) Coverage: Maximizing proportion of working age population accumulating retirement income

entitlements. Adequacy: Protecting retirees against severe drops in living standards and poverty by ensuring that they

have accumulated adequate retirement benefits. Sustainability: Delivering promised retirement income without placing burdens that will not be met on

government, employers or workers. Efficiency : How well pension plans transfer contributions to pension income. Security: Minimizing the risk that funds that have been accumulated to provide retirement benefits are

misappropriated.

Measuring Risks and Vulnerabilities – Financial Stability Indicators (2) – Source: Developing Appropriate Financial Stability Indicators for the Pension Industry in the Caribbean; June 2016; By E. Philip Davis

Measuring Risks and Vulnerabilities – Financial Stability Indicators (3) – Source: Developing Appropriate Financial Stability Indicators for the Pension Industry in the Caribbean; June 2016; By E. Philip Davis

Measuring Risks and Vulnerabilities – Financial Stability Indicators (4) – Source: Developing Appropriate Financial Stability Indicators for the Pension Industry in the Caribbean; June 2016; By E. Philip Davis

Measuring Risks and Vulnerabilities – Financial Stability Indicators (5) – Source: Developing Appropriate Financial Stability Indicators for the Pension Industry in the Caribbean; June 2016; By E. Philip Davis

Final Words Since we have touched on some the issues relating to both DB and DC plans, I thought it

might be instructive to conclude by sharing excerpts from an article that was published on May 19, 2017 in the Canadian media on measures being taken by Ontario government (Canada) to implement a new framework for DB pension plans:

“The government will introduce legislation this autumn to implement a new framework for DB pensions that include changes to the going concern funding rules; requiring the funding of a reserve within plans; increasing the guarantee provided under the Pension Benefits Guarantee Fund (PBGF) by 50%; and requiring plans that fall below the 85% funding level to be funded on a solvency basis.

The government is making a variety of other complementary changes designed to improve transparency to plan beneficiaries, enhance income security, set funding rules for benefit improvements and restrict contribution holidays. The government also announced that it will be reviewing the rules governing the wind-up of DB pensions and studying a proposal to establish an agency to administer the pension benefits of wound-up plans.

The reforms are intended to help shore up DB pensions by ensuring that they are funded appropriately and establish a reserve to protect benefits while also giving employers greater flexibility in managing their pension contributions, the province states. - "Everyone deserves a secure retirement”.”

Presenter

Presentation Notes

Proposed public sector pension scheme will require constitutional change Minister of Finance and Planning Dr Peter Phillips, has tabled in Parliament the Pensions (Public Service) Act which seeks to give effect to the proposals for reforming the public sector pension scheme. According to the Bill’s Memorandum of Objects and Reasons, it is seeking to do this by: (1) establishing a defined benefit contributor scheme where all pensionable officers will contribute five per cent of salary; (2) establishment of a segregated fund for the contributions at a time to be determined by the minister; (3) gradually increasing the retirement age to 65 years; (4) and, harmonising the legislation governing public sector pension in a single statute and repealing several enactments which previously dealt with pension. The Bill also seeks to make consequential amendments to the relevant pension provisions in several pieces of legislation. The Bill is also accompanied by a second Bill — short titled the Constitution (Amendment) (established fund) (Payment of Pensions) Act, 2015 — which will seek to amend the Constitution of Jamaica to provide for the payment of the pensions, gratuities and other allowances out of a fund established by law, other than the Consolidated Fund. The second Bill notes that the Constitution only allows for pensions, gratuities and other allowances for public-sector employees to be charged and paid out of the Consolidated Fund (which finances the budget). However, the Pensions (Public Service) Act, 2015 will establish a defined benefit contributory scheme, which contemplates the establishment of a pension fund into which shall be paid all contributions made by pensionable officers and contributions made by the government, as an employer. The Bill seeks to amend the Constitution to provide for the payment of the pensions, gratuities and allowances out of the pension fund so established.

Thank You

References1. Brunton, P. Desmond, and Pietro Masci (Editors); Workable Pension Systems Reforms in the Caribbean; 2005

(Inter-American Development Bank and the Caribbean Development Bank)2. Davis, E Philip; Developing Appropriate Financial Stability Indicators for the Pension Industry in the Caribbean

(Presentation at the CAPS Conference, June 2016)3. E Philip Davis; Trends and Risks in the Global Pension Fund Industry – With Implications for the Caribbean

(Presentation at the CAPS Conference, June 2016)4. E Philip Davis; Evolving Roles for Pension Regulators – Towards Better Control of Risk (2013)5. Kiel, Al, Audia Bacchas and Marcia Tam-Marks; Proposed Prudential Reporting Regime for Pension Plans in

the Caribbean; Caribbean Association of Pension Supervisors, (2016)6. Kiel, Al, and Audia Bacchas; Conversion from DB to DC Pension or Hybrid Plan and its Implications for

Pension Regulators – Caribbean Regulators (2017)7. Nicholls, S; Pension Funds and Financial Stability (2016)8. Rabelo, Flavio Marcilio; Comparative Regulation of Private Pension Plans9. Cass Business School, London, UK; Design and Delivery of Defined Contribution (DC) Pension Schemes -

Policy challenges and recommendations (2013)10. IMF WP WP/07/28 - Public Pension Reform: A Primer; Alain Jousten11. IMF Working Paper (WP/11/29); Stress Tests for Defined Benefit Pension Plans – A Primer; Gregorio Impavido12. IMF WP/16/206; National Insurance Scheme Reforms in the Caribbean; By Koffie Nassar, Joel Okwuokei,

Mike Li, Timothy Robinson and Saji Thomas13. IOPS Working Papers on Effective Pensions Supervision, No.19 - Stress Testing and Scenario Analysis of

Pension Plans; Liviu Ionescu and Juan Yermo, March 201414. OECD Core Principles of Private Pension Regulation (2016)15. World Bank Report No. 47673-LAC; Strengthening Caribbean Pensions - Improving Equity and Sustainability16. World Bank; Issues and Prospects for Non-Financial Defined Contribution (NDC) Schemes (2006)