25

Nazis, Fakes, Taxes by Ralph E. Lerner RalphELerner.com [email protected] 590 Madison Ave, New York, NY, 10022 (212) 521-4437 http://www.RalphELerner.com/

| Date post: | 17-Jul-2015 |

| Category: |

Art & Photos |

| Upload: | ralph-lerner |

| View: | 123 times |

| Download: | 0 times |

Nazis, Fakes, Taxes

by

Ralph E. LernerRalphELerner.com

590 Madison Ave, New York, NY, 10022

(212) 521-4437

http://www.RalphELerner.com/

Edgar Degas,

LANDSCAPE WITH SMOKE STACKS

Pastel over monotype, ca. 1890-93http://www.RalphELerner.com

/

STATUTE OF LIMITATIONS - TITLE

§ 2-275

1 - prompt filing of suits

2 - protection for a defendant after period of repose -

evidence can be lost or destroyed with passage of time

3 - promotion of free trade

An action for breach of any contract for sale must be commenced

within four years after the cause of action has accrued.

http://www.RalphELerner.com/

DISCOVERY RULEGregory Erisoty v. Jacqueline Rizik

An owner’s cause of action does not

accrue until he discovers or by

exercise of reasonable diligence

and intelligence should have

discovered, facts which form the

basis of a cause of action

Corrado Giaquinto

Winter

http://www.RalphELerner.com/

DEMAND REFUSAL RULEDeWeerth v. Baldinger

An owner’s obligation to make a

demand without unreasonable

delay includes an obligation to use

due diligence to locate the stolen

property

Claude Monet

Champs de Ble a Vetheuil

1879

http://www.RalphELerner.com/

Guggenheim v. Lubell

An owner has no obligation to use

due diligence to locate his

stolen property - whether it

was unreasonable not to do

more is an issue of fact

relevant to the defense of

laches

The Cattle Dealer

(Le Marchand de Bestiaux)

Marc Chagall

1912

http://www.RalphELerner.com/

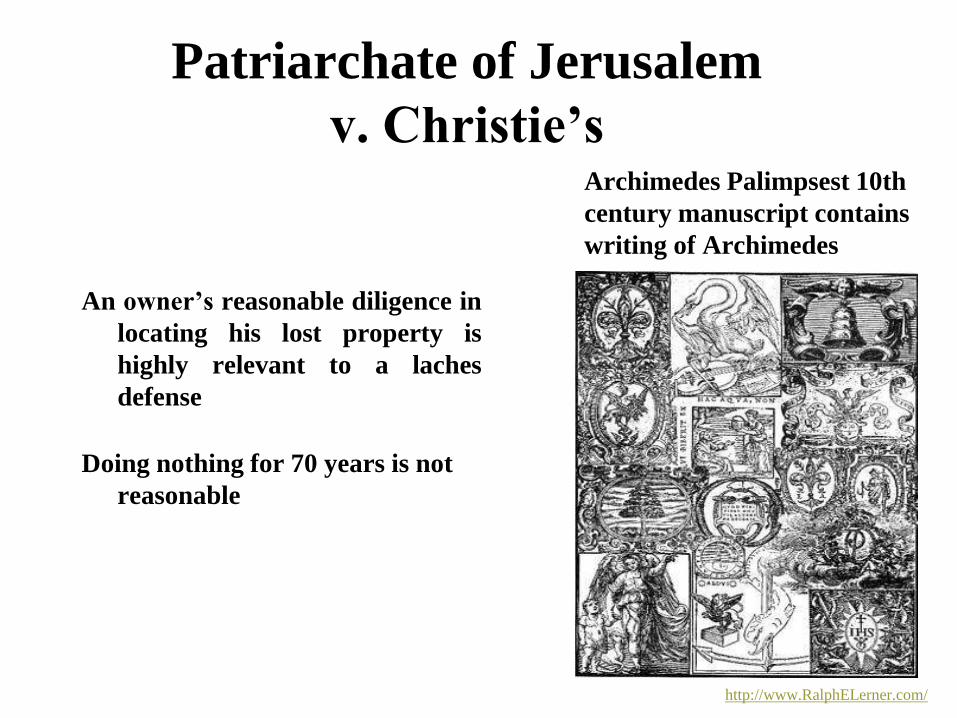

Patriarchate of Jerusalem

v. Christie’s

An owner’s reasonable diligence in

locating his lost property is

highly relevant to a laches

defense

Doing nothing for 70 years is not

reasonable

Archimedes Palimpsest 10th

century manuscript contains

writing of Archimedes

http://www.RalphELerner.com/

STATUTE OF LIMITATIONS -

AUTHENTICITYRosen v. Spanierman

Four year statute of limitations

applies.

A warranty of authenticity does not

extend to future performance of

the goods.

Lack of knowledge of the breach is not

a defense.

The Misses Wertheimer

John Singer Sargeant

http://www.RalphELerner.com/

BALOG v. CENTER ART GALLERY

Hawaii

In the case of artwork which is certified authentic by an expert in the field

or a merchant dealing in goods of that type, such a certification of

authenticity constitutes an explicit Warranty of future performance

sufficient to toll the U.C.C.’s statute of limitations - but only in

Hawaii http://www.RalphELerner.com/

DAMAGES - BREACH WARRANTY TITLEMenzel v. List

1932 - Menzel Purchases for $150

1941 - Painting taken by Nazis

1941-1955 - Location not known

1955 - Perls purchases from dealer

in Paris for $2,800

1955 - Perls sells to List for $4,000

1962 - Menzel say “Give it back”

1966 - Jury for Menzel - value now

$22,500

Jacob’s Ladder

Marc ChagallMeasure of damages $22,500

http://www.RalphELerner.com/

DAMAGES - FRAUD

Nacht v. Sotheby’s

1981 - Nacht purchases for

$23,815

1996 - Nacht discovers it is

not authentic - if it was

authentic value

$225,000

Measure of damages $23,815 Francis Picabia

Josias

1930

http://www.RalphELerner.com/

Edgar Degas,

LANDSCAPE WITH SMOKE STACKS

Pastel over monotype, ca. 1890-93http://www.RalphELerner.com/

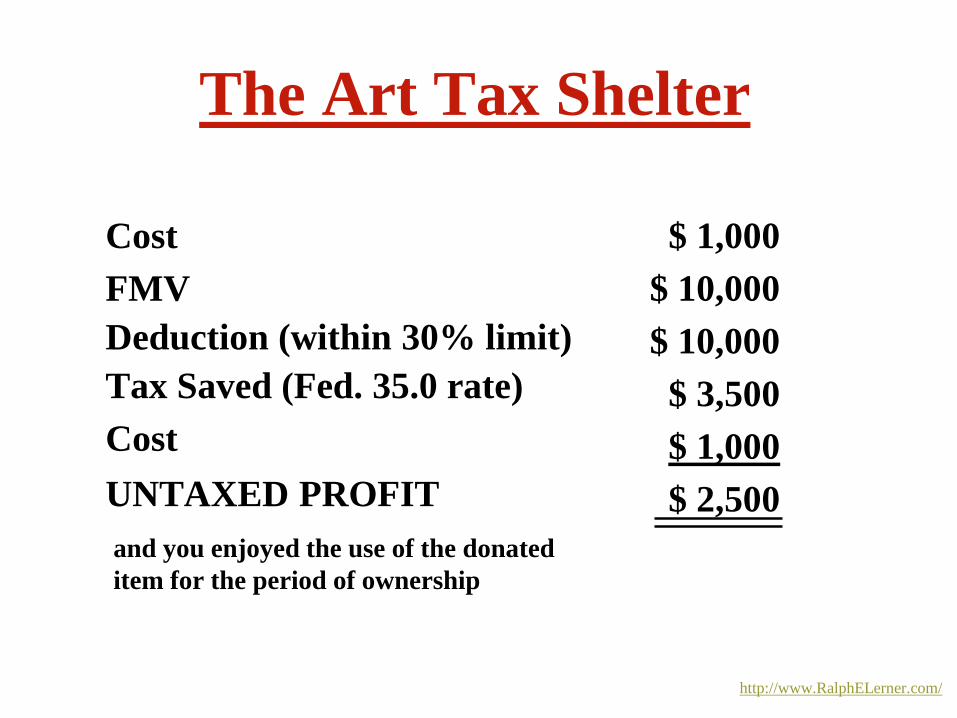

Cost

FMV

Deduction (within 30% limit)

Tax Saved (Fed. 35.0 rate)

Cost

UNTAXED PROFIT

$ 1,000

$ 10,000

$ 10,000

$ 3,500

$ 1,000

$ 2,500

and you enjoyed the use of the donated

item for the period of ownership

The Art Tax Shelter

http://www.RalphELerner.com/

The Four Questions

1. What type of donee organization - public charity

or private foundation?

http://www.RalphELerner.com/

1. What type of donee organization - public charity or

private foundation?

2. What type of property - ordinary income type

property or long-term capital gain type property?

The Four Questions

http://www.RalphELerner.com/

1. What type of donee organization - public charity or

private foundation?

2. What type of property - ordinary income type

property or long-term capital gain type property?

3. Have you satisfied the related-use rule?

The Four Questions

http://www.RalphELerner.com/

1. What type of donee organization - public charity or

private foundation?

2. What type of property - ordinary income type

property or long-term capital gain type property?

3. Have you satisfied the related-use rule?

4. Have you obtained a qualified appraisal by a

qualified appraiser?

The Four Questions

http://www.RalphELerner.com/

FUTURE INTEREST RULE

Section 170(a)(3) - There is no charitable deduction for a

gift of a future interest in tangible personal property

until there is no intervening interest in, right of

possession of, or enjoyment of the property held by the

donor, spouse or certain related individuals.http://www.RalphELerner.com/

FRACTIONAL INTEREST

Winokur v. Commissioner

Women of Warhol

Marilyn, Liz & Jackie

http://www.RalphELerner.com/

FAIR MARKET VALUE

Hypothetical Willing Buyer/

Hypothetical Willing Seller

http://www.RalphELerner.com/

Quedlinburg Treasures

Fair Market Value is determined in the retail market in

which the item is most commonly sold to the public.http://www.RalphELerner.com/

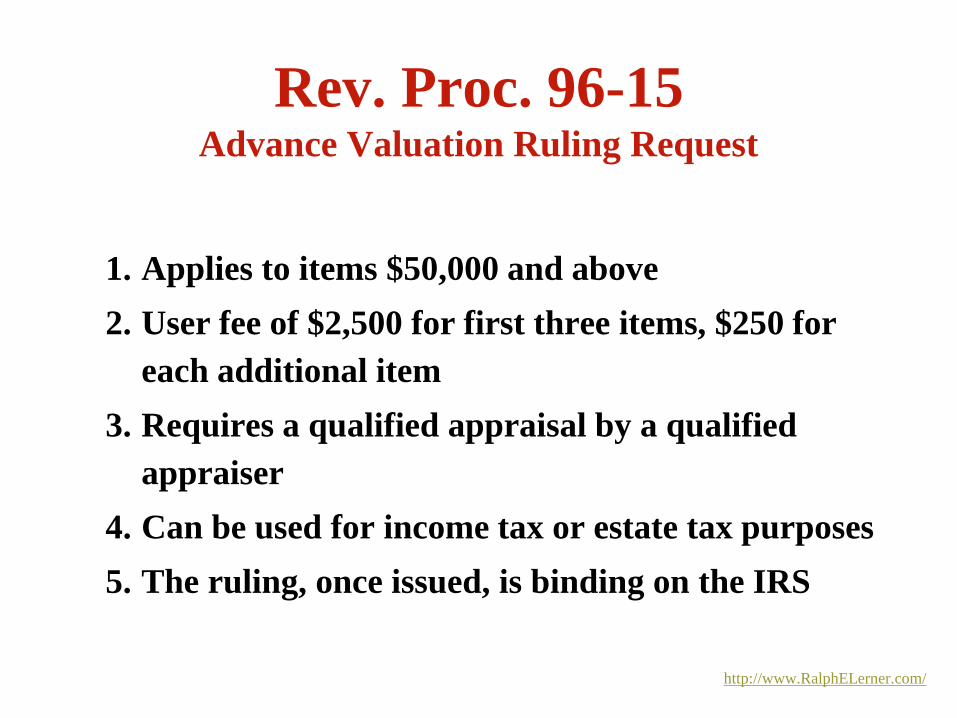

Rev. Proc. 96-15Advance Valuation Ruling Request

1. Applies to items $50,000 and above

2. User fee of $2,500 for first three items, $250 for

each additional item

3. Requires a qualified appraisal by a qualified

appraiser

4. Can be used for income tax or estate tax purposes

5. The ruling, once issued, is binding on the IRS

http://www.RalphELerner.com/

ROTHKO

Avoid Conflicts of Interest

Duty of Loyalty

An executor must care and manage the assets and affairs of the estate

as would prudent persons of discretion and intelligence accented by

“not honesty alone” but by the punctilio of an honor the most sensitive.http://www.RalphELerner.com

/