38

Raw material current price trends and impact on the food industry Brian Smith, Data Director Food Matters Live 19 November 2014

Raw material current price trends and impact on the food industry

Brian Smith, Data Director

Food Matters Live

19 November 2014

Content

Setting the scene

Recent trends

Key food raw materials

Key price drivers

Product model price trends – 1, 3, 5 years

Long term food inflation rates

2015 outlook

Volatility and insight

“The price of the commodity may go up, or it may go down,

however,

there is strong potential that the price might stay the same”

Vlad Peksa (1982), Founder of Mintec

“Data and information are not knowledge;

they are like any raw materials,

requiring some intervention and processing to make them useful”

Ron Bennett, St Thomas University Minneapolis

Mintec

Founded in 1982 to “help the supply chain buy better”

Family owned, UK based, global client base.

To provide commodity/raw materials market intelligence, training and support services

Procurement professionals

Retail &

wholesale

Food

manufacturer

Food

service

Core client base

Sample markets and categories covered

Grains and cereals Sugar Meat and livestock Dairy markets

Vegetable oils Oilseeds Meals and proteins Feed materials

Pulses Cocoa Fibres Economic data

Beans Coffee Ingredients Fruit and vegetables

Potatoes Tea Exchange rates Food additives

Solvents Minor metals Electronics Waxes

Industrial Precious metals Engineering Crude drugs

Petrochemicals Foundry ingots Thermosets Essential oils

Crude and fuel Ferrous scrap Recycled resins Fragrances

Gas and coal Non ferrous Plastic Timber

Energy indexes World steel Paper and board Currencies

Fertilisers Noble and bulk Pulp Oleoresins

Gum Metal ores Minerals Freight and shipping

Fibres Textiles Timber Shipping costs

Bulk chemicals Base metals Thermoplastics Rubber

Over 20,000 individual series

Brian Smith Qualifications;

- MBA in Retailing

- BSc (Hons) in Biochemistry

- Diplomas in Health & Safety and Food Hygiene

Experience;

- c25 years commercial and operational experience

- FOOD: producer, manufacturer, wholesale, retail and service industries

- domestic, duty free/travel retail & international markets

- supplier & category management (procurement & trading)

- supply chain and stock management (value chain)

- strategic business development and turnaround (operational excellence)

- brand & trade marketing (vision and value)

- Previously a client of Mintec

Recent headlines

The FAO food price index falls for the sixth consecutive month FAO, 09.10.14

Salmon prices drop as Russian ban hits Grocer 27/9/14

Current rate of UK food inflation

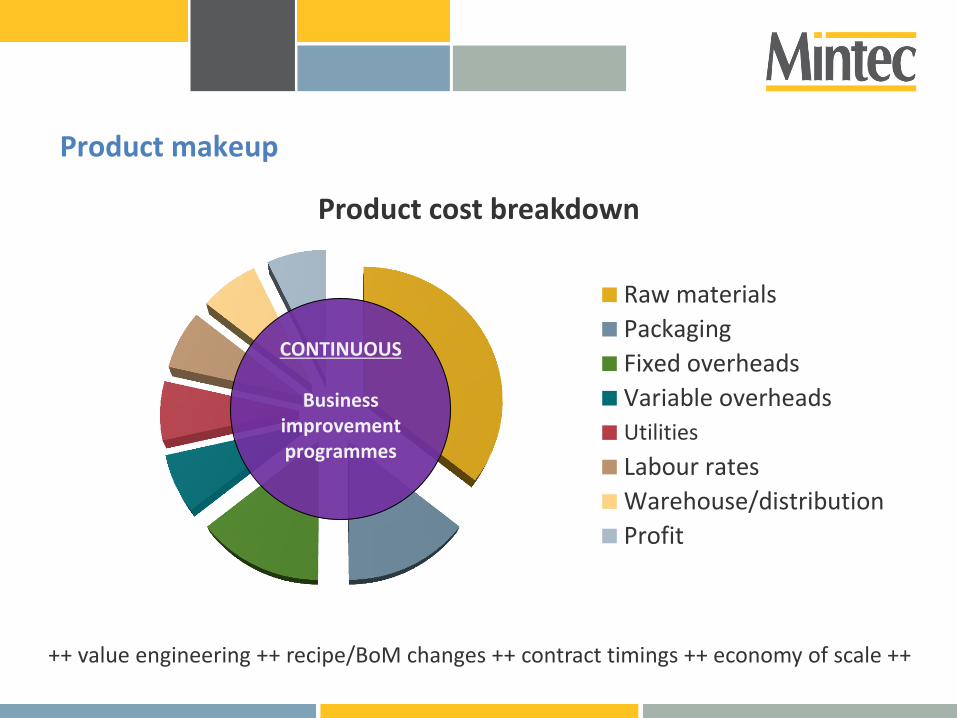

Product makeup

Product cost breakdown

Raw materials

Packaging

Fixed overheads

Variable overheads

Utilities

Labour rates

Warehouse/distribution

Profit

CONTINUOUS

Business improvement programmes

++ value engineering ++ recipe/BoM changes ++ contract timings ++ economy of scale ++

Raw material price changes over the last 12 months Food Non-Food

Pepper IN +74% Sulphur CA +138%

Coffee Arabica ICE NY +58% Nickel LME +30%

Coconut Oil Rotterdam NL +33% Zinc LME +21%

Beef BR +28% LLDPE LME +14%

Cocoa Beans LIFFE +24% Aluminium LME +9%

Cocoa Butter London +21% NBSK Pulp EU +8%

Honey EU +18% PP EU +7%

Eggs NL +16% Tin LME +3%

Wheat Milling LIFFE -7% PVC EU +1%

Durum Wheat IT -10% LDPE EU +1%

Cheddar UK -12% Testliner EU -1%

Sunflower Oil Rotterdam NL -12% Brent Crude Oil London -4%

Beef EU -12% Diesel NW EU -7%

Pigmeat EU -13% Steel Coil EU -8%

Rapeseed Oil Rotterdam NL -14% Kraftliner EU -8%

SMP EU (UK -4%) -17% Natural Gas ICE UK -15%

Butter EU -18% Electricity UK -26%

Whey Powder EU -19% Cotton ICE NY -26%

Cocoa Powder London -36% Electricity EU -30%

Potato Market NL (UK -16%) -69% Natural Gas Bacton -36%

Source: Mintec

September 2014

Key raw materials that make up FAO food price index

Global value of all food raw materials c$5 trillion per annum

Change

%

Change

%

Change

%

Value $'000Production

Metric tonne1 year 5 years 10 years

1 Rice, paddy 186,667,648 722,599,583 -2% -5% N/A

2 Cow's milk, whole, fresh 183,583,111 614,578,723 -27% 42% N/A

3 Cattle, meat 170,272,001 63,031,582 -10% 19% N/A

4 Pig, meat 167,007,794 108,641,257 -25% -4% 17%

5 Chicken, meat 128,199,164 90,001,779 -10% -2% 39%

6 Wheat 84,281,536 701,395,334 -24% 15% 74%

7 Soybeans 65,903,601 262,037,569 -23% 5% 113%

8 Tomatoes 58,223,483 159,347,031 -14% -19% 39%

9 Sugar cane 56,903,836 1,800,377,642 -15% -25% 110%

10 Maize (Corn) 55,478,433 885,289,935 -22% 0% 53%

Top 10 Total 1,156,520,607 5,407,300,435

%age of FAO food price index 64% 68%

2012 FAO Figures

Commodity/raw materialRank

-16% 7% 54%*

Raw material price trend versus UK food inflation

Key drivers – more intense now and here to stay

Geo-political

(and legal)

Raw material fundamentals

Social and environmental

Global volatility

Vulnerable & uncertain

Reliance for trade

Confidence in supply

Risk and conflict

Selected current price drivers impacting food industry

Geo-political/legal

- Growing tensions, sanctions and bans between Russia and EU/US

- Removal of EU milk quota scheme

Environmental/Social

- Favourable and unfavourable climate conditions

- Emerging markets, especially BRIC nations

- Ebola

- Market speculation

Fundamentals

- High ending stocks and consecutive high harvests: grains/oilseeds

- Good stocks and production: crude oil

- Globally tight stock and limited production vs demand: meats

- Demand growing ahead of production: cocoa

Manufacturing PMI

UK: Current PMI = 57.0

Continued growth

Concern that recovery may be losing steam

EU: Current PMI = 52.2

Improvement on recent declining trend

China: Current PMI = 50.4

Improvement on recent declining trend

US: Current PMI = 57.4

Recovery continues, but at slower pace

Unemployment Rate

UK: Down to 6.2%* (below 2m),

30.8m people in work

EU: Rate remains at 11.5%*

China: Stable at 4.1% in September

US: The rate has fallen below 6% for the first time since 2009, reaching 5.9% in September

*August 2014 figures

Key currency movements

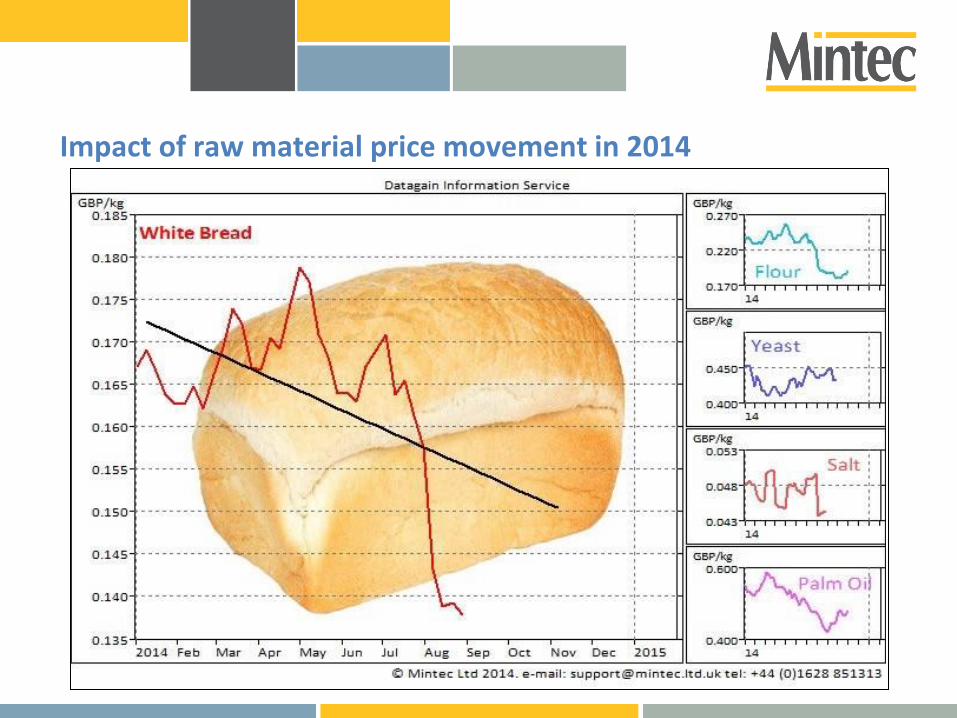

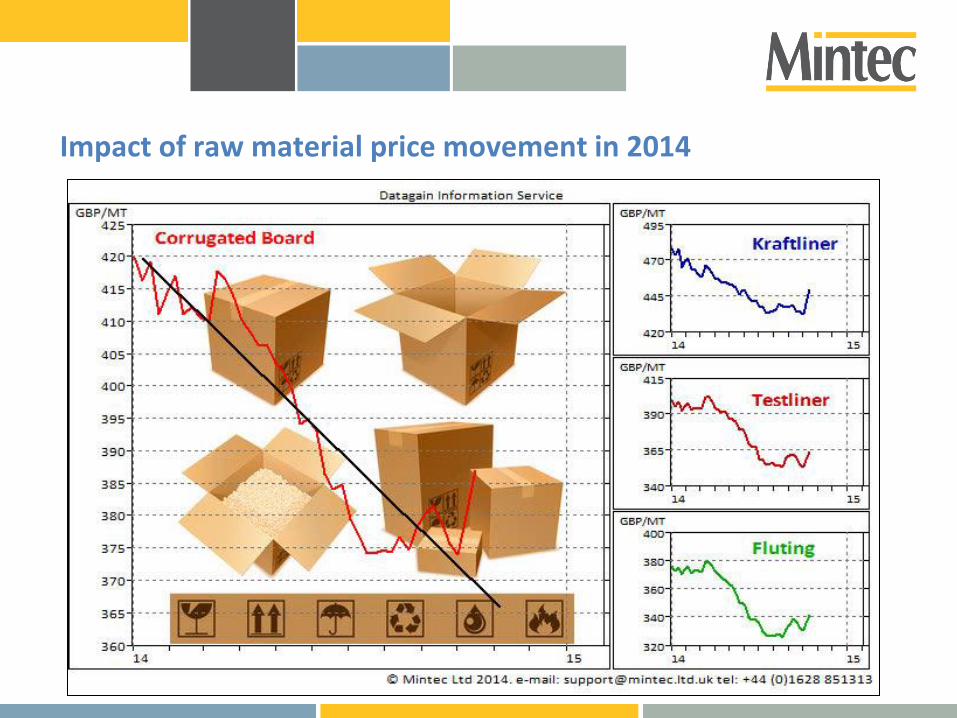

Impact of raw material price movement in 2014

Impact of raw material price movement in 2014

Impact of raw material price movement in 2014

Impact of raw material price movement in 2014

Impact of raw material price movement in 2014

Impact of raw material price movement in 2014

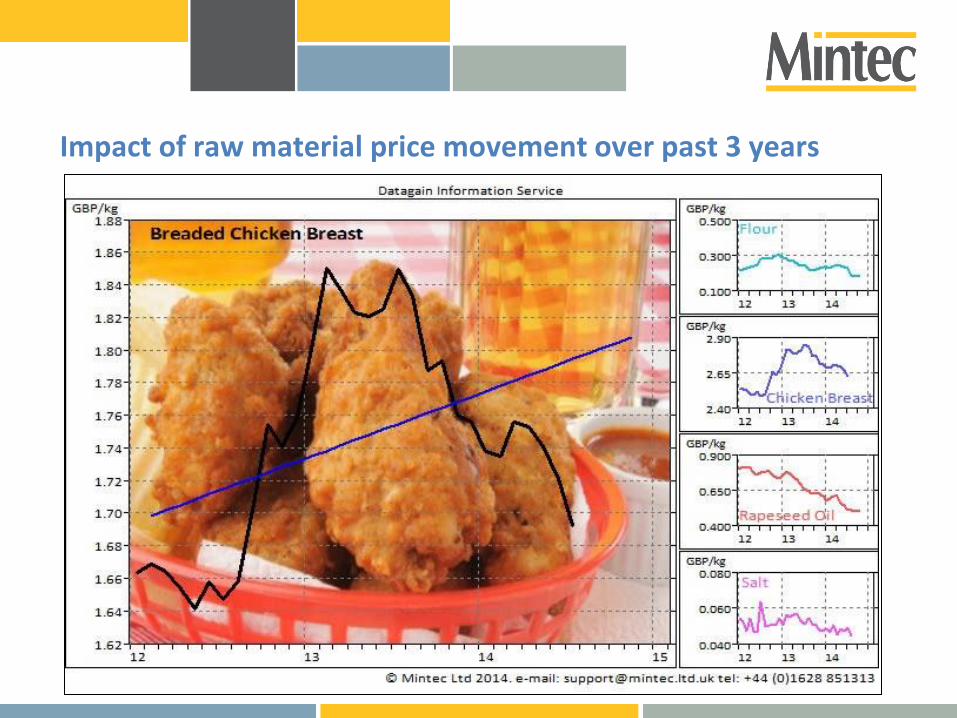

Impact of raw material price movement over past 3 years

Impact of raw material price movement over past 3 years

Impact of raw material price movement over past 3 years

Impact of raw material price movement over past 3 years

Impact of raw material price movement over past 3 years

Impact of raw material price movement over past 3 years

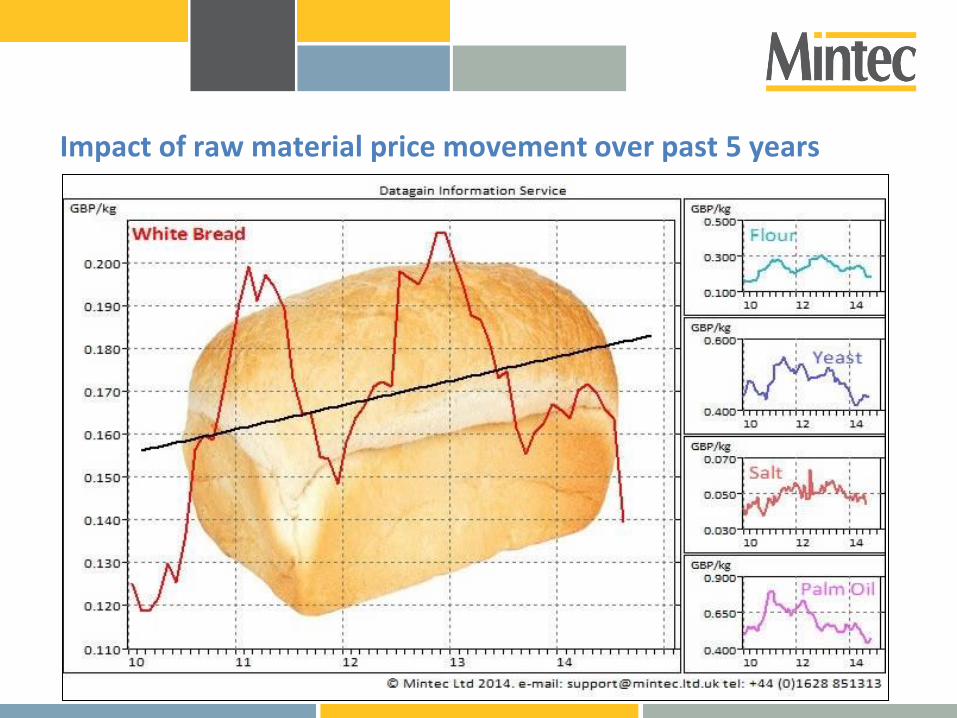

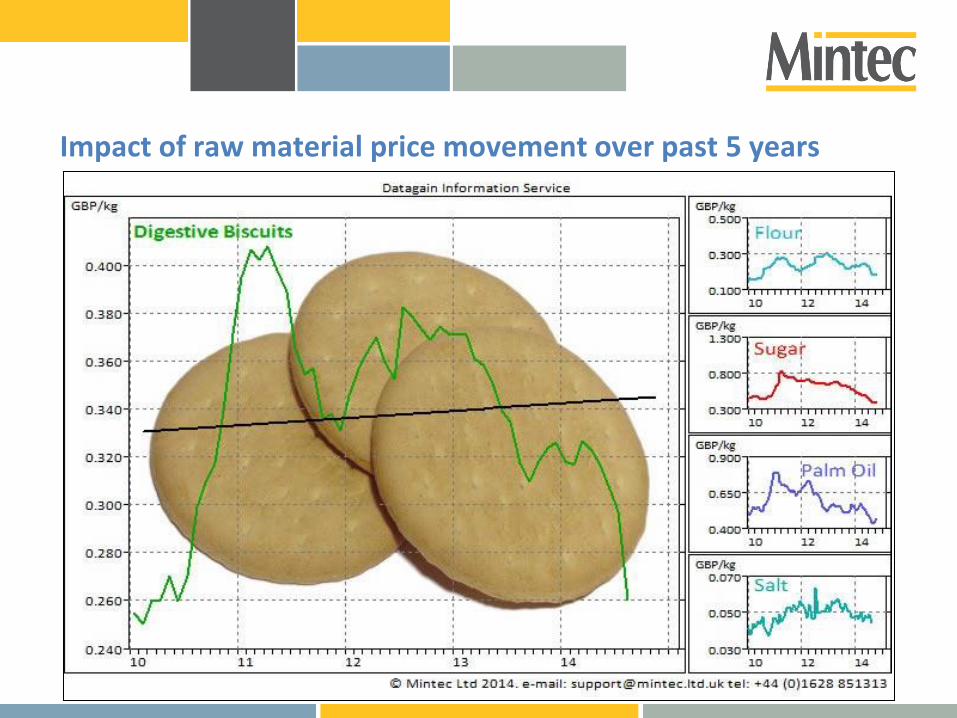

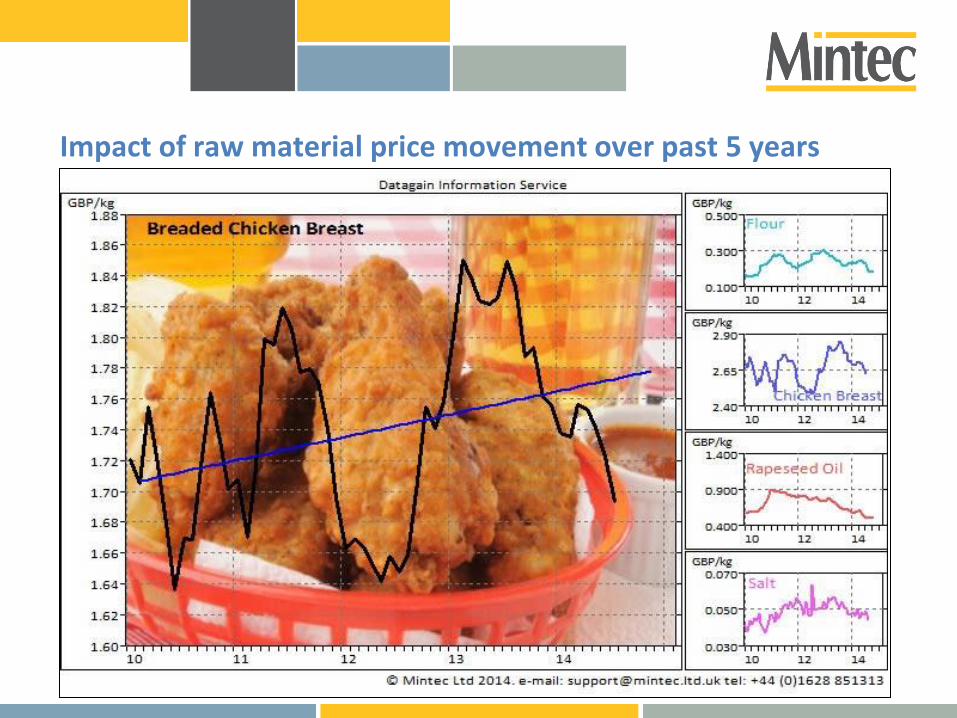

Impact of raw material price movement over past 5 years

Impact of raw material price movement over past 5 years

Impact of raw material price movement over past 5 years

Impact of raw material price movement over past 5 years

Impact of raw material price movement over past 5 years

Impact of raw material price movement over past 5 years

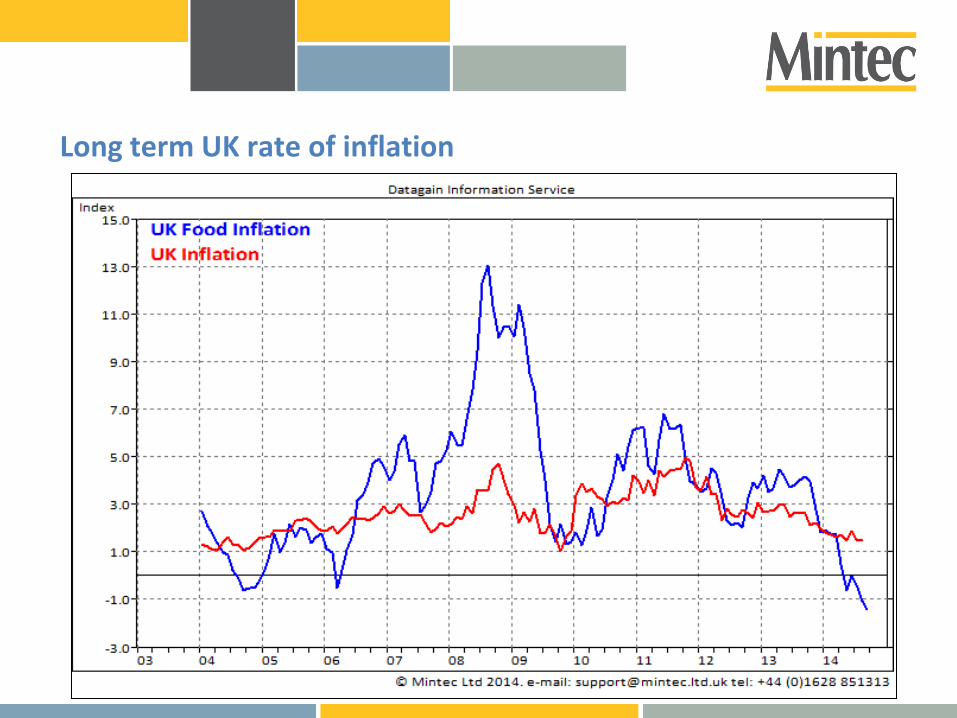

Long term UK rate of inflation

Outlook for 2015

Growth forecasts: EU – 1.5% UK – 2.0% Unemployment: EU – 10.4% UK – 6.5%

Removal of dairy quotas

Low feed costs

Re-distribution of

export markets (due to Russia)

*The Economist

Opportunities

- Crop stocks & size of new harvests

- Russian import ban

- EU legislation changes

Risks

- Speculation and noise in market

- Climate – El-Nino (?)

- Disease – Ebola (?)

Overall an increased volatility due to;

- Climate and disease issues

- Continued rise in global demand

- Russian import ban

Outlook for 2015

Raw material probable price movements

Opportunities in price

- Grains and most edible oils

- Crude oil and energy

- Dairy market

- Potatoes and onions

Marginal movers

- Plastics and paper packaging

- Sugar

Risks to price – requires close monitoring

- Most meats and wild fish

- Cocoa

- Coffee

- Tomatoes and olives (including olive oil)

Mintec-Limited /company/mintec-ltd @MintecLimited

Register on our website for the Mintec Daily News: www.mintecglobal.com/register

Thank you for listening

Come see us on stand 224

www.mintecglobal.com