14

Tom Hellman, VP Drilling & Completions March 6, 2017 Raymond James Institutional Investors Conference

Tom Hellman, VP Drilling & Completions

March 6, 2017

Raymond James Institutional Investors Conference

(MAY 2014 – MAY 2016)

Bias for Action

WE BUILT A BRAND NEW COMPANY

2

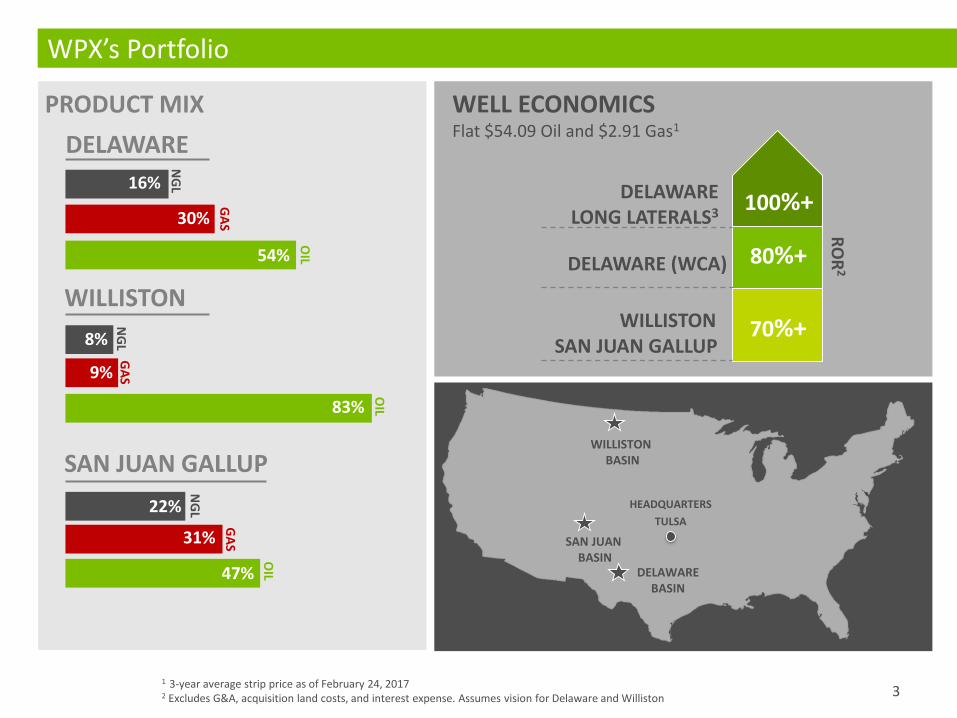

WPX’s Portfolio

DELAWARE

54%

30%

GA

S

OIL 80%+DELAWARE (WCA)

WILLISTONSAN JUAN GALLUP

RO

R2

WELL ECONOMICSFlat $54.09 Oil and $2.91 Gas1

WILLISTON BASIN

DELAWARE BASIN

SAN JUANBASIN

1 3-year average strip price as of February 24, 20172 Excludes G&A, acquisition land costs, and interest expense. Assumes vision for Delaware and Williston

70%+

100%+DELAWARE LONG LATERALS3

HEADQUARTERS

TULSA

NG

L16%

WILLISTON

83%

9%

GA

S

OIL

NG

L8%

SAN JUAN GALLUP

47%

31%

GA

S

NG

L22%

OIL

3

PRODUCT MIX

Panther Acquisition Enhances Sustained Growth Outlook

ASSET QUALITY SUPPORTS RAPID GROWTH ASSET QUALITY SUPPORTS RAPID GROWTH

Assumes 2017 WTI $50Bbl /NYMEX $2.75Mcf and 2018-2020 WTI $55Bbl /NYMEX $3.00Mcf.

OIL

MB

BL/

D

UPDATED PRO FORMA RANGE

► Free cash-flow positive by year-end 2018

► Assumes modest 1-3 rig additions per year

► 30% oil growth in 2017

► 55% oil growth in 2018

4

Panther acquisition enhances growth strategy

0

20

40

60

80

100

120

140

160

2016 2017 2018 2019 2020

$0

$500

$1,000

$1,500

$2,000

$2,500

2016 2017 2018 2019 2020

C A G R : 3 0 % - 4 0 % C A G R : 3 0 % - 4 0 %

MIL

LIO

NS

($)

PREVIOUS FORECAST UPDATED PRO FORMA RANGE PREVIOUS FORECAST

Expanding WPX’s World-Class Delaware Position

5

PANTHER ACQUISITION OVERVIEW

► 18,000+ acres in core of Delaware

► 920 gross locations, including 150+ long lateral locations

► Significant current production of ~6,500 Boe/d (55% oil)

► Maintain Panther’s current 2 rig program

► Valuation primarily supported on 3 zones with upside in 5

additional zones

► Expected to close in late March

N E W M E X I C O

T E X A S

CULBERSON

LEA

EDDY

WARD

REEVES

LOVING

PECOS

WINKLER

WPX OPERATED ACREAGE

PANTHER ACREAGE

SELF-FUNDING DEVELOPMENT

2 rig program funded with operating cashflows

DEEP INVENTORY OF CORE DELAWARE

Resource supports sustained growth

HIGH QUALITY ROCK

Multiple stacked pay intervals with significant upside

ACCRETIVE TO CASHFLOWS AND NAV

Accretive to shareholders 2017 and beyond

BENEFITS

THICK Hydrocarbon Stack Across Entire Acreage Position

A STATE LINE LOG B EAST TYPE LOG C CENTRAL TYPE LOG D SOUTH TYPE LOGN E W M E X I C O

T E X A S

WARD

LEAEDDY

REEVES

LOVING WINKLERA

B

C

D

DE-RISKED

UPSIDE POTENTIAL

De-risked pay section across acreage with

substantial UPSIDE

WPX OPERATED ACREAGE ACQUIRED ACREAGE

6

Delaware Basin: Delineation of the Wolfcamp

N E W M E X I C O

T E X A S

CULBERSON

LEA

EDDY

LOVING

WPX OPERATED ACREAGE

PANTHER ACREAGE

D

D

XY

XY

C-STATE 16-1HIP 30: 1,635 BOE/D (65% OIL)90 DAY CUM: 114,338 BOE

E. PECOS FED COM 22-14HIP 30: 1,736 BOE/D (30% OIL)90 DAY CUM: 139,336 BOE

DELINEATING WOLFCAMP ACROSS POSITION

► WOLFCAMP XY-PECOS STATE 46-6H► Lateral length: ~4,800 ft

► Proppant (#/ft): ~1,750

► Tracking in-line with WCA 1,000 MBOE type curve after 45 days

660’330’

WOLFCAMP B

LOWER WOLFCAMP A

UPPER WOLFCAMP A

WOLFCAMP X/Y

1 MILE

35

0 F

T

CBR SPACING TEST UNDERWAY

► PURPOSE OF TEST

► Validate 16 well U/L Wolfcamp A spacing

► Understand future infrastructure needs

PECOS STATE 46-6HIP 30: 1,780 BOE/D (50% OIL)

D

LINDSAY 16-6HIP 30: 1,434 BOE/D (18% OIL)90 DAY CUM: 119,047 BOE

PECOS STATE 46-5HIP 30: 1,628 BOE/D (22% OIL)

REEVES

7

► Utilized diverter

► Hybrid completion design

► Engineered completions

► WOLFCAMP D-PECOS STATE 46-5H► Lateral length: ~4,850 ft

► Proppant (#/ft): ~2,750

► Currently producing with 3,800 psi flowing tubing pressure (2-17)

► UPDATE ON CBR

► Expected first sales end of March

► 16 day record well spud-to-rig release

► Encouraging DFIT results

► Utilized diverter

► Hybrid completion design

► Engineered completions

Note: Well production data is on a 3-stream basis

Williston Basin: Strong, Consistent Results

1 Spud-to-rig release for a 2-mile lateral2 Public data based on production from wells completed in 2016

Peers include AXA,BURLINGTON RESOURCES,EOG,ERF,HESS,LIBERTY RESOURCE,MRO,NFX,OAS,PETRO-HUNT,QEP,SM,STL,TPLM,WLL,XTO

► 39% oil growth 4Q’16 vs 3Q’16

► 4Q production 28.8 MBOE/d

► Set new drilling record of 11.7 days1

► Completed DUC inventory

► Current total well cost $5.5MM

► 14 wells on 1st sales during 4Q

► 6 Middle Bakken and 8 Three forks wells

8

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

WPX PEER 1 PEER 2 PEER 3 PEER 4 PEER 5 PEER 6 PEER 7 PEER 8 PEER 9

180 DAYS CUM OIL PRODUCTION FOR 2016 NEW WELLS2

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,00090 DAYS CUM OIL PRODUCTION FOR 2016 NEW WELLS2

WPX PEER 1 PEER 2 PEER 3 PEER 4 PEER 5 PEER 6 PEER 7 PEER 8 PEER 9

WILLISTON HIGHLIGHTS

#1 PRODUCERON CUMULATIVE OIL BASIS 90 DAYS/180 DAYS2

San Juan Basin: Continued Strong Well Results

12015 well performance based on 1 mile laterals, 2016 based on average of 7,200’ laterals

CONTINUING TO RAISE THE BAR

► 21% oil growth 4Q’16 vs 3Q’16

► Set new basin record

► Drilled 1.5 mile lateral in 5.8 days

► Strong performance on 6-well pad

► Cumulative 180-day production: +1.0 MMBOE

► Average day: ~1,000 BOE/D per well (70% oil)

► Average lateral length: 7,250 ft.

► Average D&C cost: ~$4.1MM

► Focused on West Lybrook in 2017

► New rig spud first well 12/31/20160

50

100

150

200

250

300

0 20 40 60 80 100 120 140 160 180 200C

um

Pro

du

ctio

n M

BO

E

Days of Production

6-WELL

PAD

2016

GALLUP WELLS

CURRENT

650 MBOE65% IN EUR SINCE 20151

2016 SAN JUAN GALLUP WELLS

INCREASE

9Note: Well production data is on a 3-stream basis

10

Contracted Service Cost Mitigates Potential Inflation

Contracts in Place for 2017

Services Exposed to Spot Market

Note: D&C components based on latest blended AFE (Williston, San Juan, Delaware)

2017 D&C COST BREAKDOWN

of D&C costs are contracted through 2017

► Majority of services exposed to inflation are contracted

► Focused on securing services since 2Q 2016 to prepare

for activity ramp

► Some contracts go through 2018, others have options

to extend past 2017

► ~90% of D&C costs go through Supply Chain Mgmt.

• Sand• Stimulation Services• Drilling Rigs• Tubulars/Wellhead• Cementing Material and Services• Water

• Fluids/Cuttings/Solids Control• Directional Equipment & Services• Chemicals• Other (Completions)• Other (Drilling)

Foundation in Place for Enhancing and Accelerating Value

► POSITIONED

► PRUDENT

► FLEXIBLE

► DISCIPL INED

WILLISTON BASIN

DELAWARE BASIN

SAN JUAN BASIN

HEADQUARTERS: TULSA

11

Disclaimer

The information contained in this summary has been prepared to assist you in making your own evaluation of the Company and does not purport to contain all of the information you may consider important in deciding whether to invest in shares of the Company’s common stock. In all cases, it is your obligation to conduct your own due diligence. All information contained herein, including any estimates or projections, is based upon information provided by the Company. Any estimates or projections with respect to future performance have been provided to assist you in your evaluation but should not be relied upon as an accurate representation of future results. No persons have been authorized to make any representations other than those contained in this summary, and if given or made, such representations should not be considered as authorized.

Certain statements, estimates and financial information contained in this summary constitute forward-looking statements or information. Such forward-looking statements or information involve known and unknown risks and uncertainties that could cause actual events or results to differ materially from the results implied or expressed in such forward-looking statements or information. While presented with numerical specificity, certain forward-looking statements or information are based (1) upon assumptions that are inherently subject to significant business, economic, regulatory, environmental, seasonal, competitive uncertainties, contingencies and risks including, without limitation, the ability to obtain debt and equity financings, capital costs, construction costs, well production performance, operating costs, commodity pricing, differentials, royalty structures, field upgrading technology, and other known and unknown risks, all of which are difficult to predict and many of which are beyond the Company's control, and (2) upon assumptions with respect to future business decisions that are subject to change.

There can be no assurance that the results implied or expressed in such forward-looking statements or information or the underlying assumptions will be realized and that actual results of operations or future events will not be materially different from the results implied or expressed in such forward-looking statements or information. Under no circumstances should the inclusion of the forward-looking statements or information be regarded as a representation, undertaking, warranty or prediction by the Company or any other person with respect to the accuracy thereof or the accuracy of the underlying assumptions, or that the Company will achieve or is likely to achieve any particular results. The forward-looking statements or information are made as of the date hereof and the Company disclaims any intent or obligation to update publicly or to revise any of the forward-looking statements or information, whether as a result of new information, future events or otherwise. Recipients are cautioned that forward-looking statements or information are not guarantees of futureperformance and, accordingly, recipients are expressly cautioned not to put undue reliance on forward-looking statements or information due to the inherent uncertainty therein.

12

Reserves Disclaimer

The SEC requires oil and gas companies, in filings made with the SEC, to disclose proved reserves, which are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible – from a given date forward, from known reservoirs, under existing economic conditions, operating methods, and governmental regulations. The SEC permits the optional disclosure of probable and possible reserves. We have elected to use in this presentation “probable” reserves and “possible” reserves, excluding their valuation. The SEC defines “probable” reserves as “those additional reserves that are less certain to be recovered than proved reserves but which, together with proved reserves, are as likely as not to be recovered.” The SEC defines “possible” reserves as “those additional reserves that are less certain to be recovered than probable reserves.” The Company has applied these definitions in estimating probable and possible reserves. Statements of reserves are only estimates and may not correspond to the ultimate quantities of oil and gas recovered. Any reserve estimates provided in this presentation that are not specifically designated as being estimates of proved reserves may include estimated reserves not necessarily calculated in accordance with, or contemplated by, the SEC’s reserves reporting guidelines. Investors are urged to consider closely the disclosure regarding our business that may be accessed through the SEC’s website at www.sec.gov.

The SEC’s rules prohibit us from filing resource estimates. Our resource estimations include estimates of hydrocarbon quantities for (i) new areas for which we do not have sufficient information to date to classify as proved, probable or even possible reserves, (ii) other areas to take into account the low level of certainty of recovery of the resources and (iii) uneconomic proved, probable or possible reserves. Resource estimates do not take into account the certainty of resource recovery and are therefore not indicative of the expected future recovery and should not be relied upon. Resource estimates might never be recovered and are contingent on exploration success, technical improvements in drilling access, commerciality and other factors.

13

WPX Non-GAAP Disclaimer

This presentation may include certain financial measures, including adjusted EBITDAX (earnings before interest, taxes, depreciation, depletion, amortization and exploration expenses), that are non-GAAP financial measures as defined under the rules of the Securities and Exchange Commission.

This presentation is accompanied by a reconciliation of these non-GAAP financial measures to their nearest GAAP financial measures. Management uses these financial measures because they are widely accepted financial indicators used by investors to compare a company’s performance. Management believes that these measures provide investors an enhanced perspective of the operating performance of the company and aid investor understanding. Management also believes that these non-GAAP measures provide useful information regarding our ability to meet future debt service, capital expenditures and working capital requirements. These non-GAAP financial measures should not be considered in isolation or as substitutes for a measure of performance prepared in accordance with United States generally accepted accounting principles.

14