38

R&D AND INNOVATION IN SERVICES : KEY FINDINGS FROM THE QUANTITATIVE ANALYSIS STRAND KNOWINNO-INNOSERV Project Final Conference Paris, 11 December 2012

R&D AND INNOVATION IN SERVICES : KEY FINDINGS FROM THE QUANTITATIVE ANALYSIS STRAND KNOWINNO-INNOSERV Project Final Conference Paris, 11 December 2012

BACKGROUND AND PROJECT DESCRIPTION

Services contribute significantly to GDP growth

Contribution of different sectors to real GDP growth (annualised), 2000-2011*

Source: OECD, STAN database, November 2012. Note: * or most recent available year. Latest available year displayed in parenthesis when different from 2011.

-1

0

1

2

3

4

5

6

SV

K (0

9)

KO

R (1

0)

PO

L (0

8)

ES

T (0

9)

ISR

(08)

C

ZE (0

9)

AU

S (0

6)

GR

C (0

9)

LUX

(09)

IS

L (0

9)

SV

N (1

0)

NZL

(08)

G

BR

(08)

E

SP

(09)

C

AN

(08)

H

UN

(10)

C

HE

(08)

A

UT

ME

X (0

9)

FIN

S

WE

(09)

U

SA

(09)

N

LD (1

0)

NO

R (0

9)

BE

L (0

9)

FRA

D

EU

(10)

P

RT

(06)

D

NK

(10)

IT

A (1

0)

JPN

(09)

Other Manufacturing Community, social, personal svcs Business sector services %

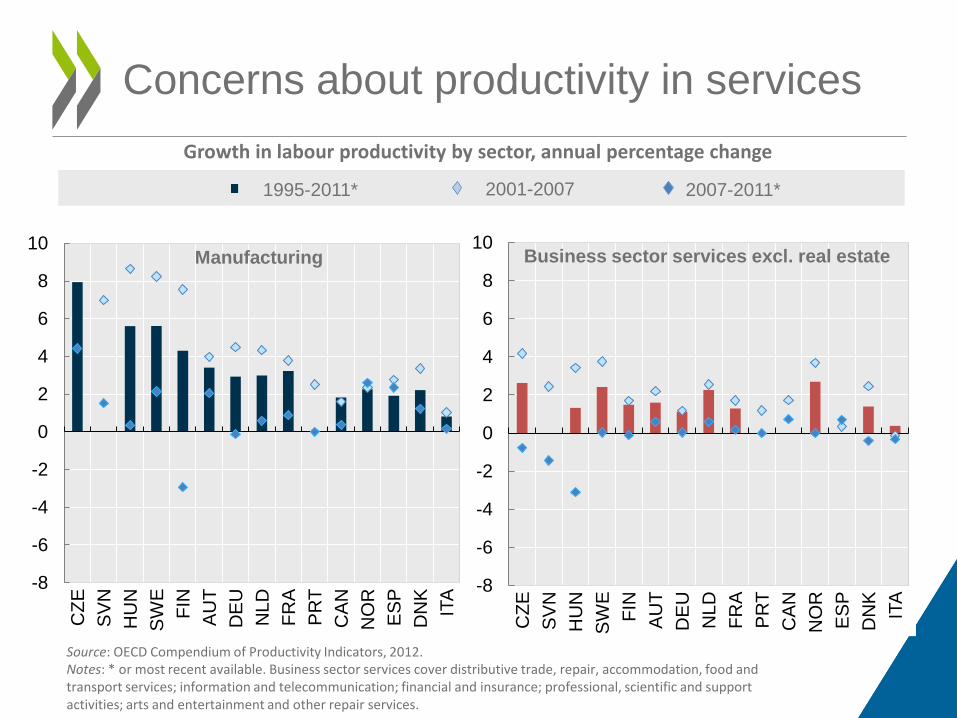

Concerns about productivity in services Growth in labour productivity by sector, annual percentage change

-8

-6

-4

-2

0

2

4

6

8

10

CZE

S

VN

H

UN

S

WE

FI

N

AU

T D

EU

N

LD

FRA

P

RT

CA

N

NO

R

ES

P

DN

K

ITA

-8

-6

-4

-2

0

2

4

6

8

10

CZE

S

VN

H

UN

S

WE

FI

N

AU

T D

EU

N

LD

FRA

P

RT

CA

N

NO

R

ES

P

DN

K

ITA

Manufacturing Business sector services excl. real estate

1995-2011* 2001-2007 2007-2011*

Source: OECD Compendium of Productivity Indicators, 2012. Notes: * or most recent available. Business sector services cover distributive trade, repair, accommodation, food and transport services; information and telecommunication; financial and insurance; professional, scientific and support activities; arts and entertainment and other repair services.

• Review existing data sources and indicators for R&D and innovation in services: assess strengths and weaknesses

• Provide new policy-relevant evidence on the nature of R&D and innovation in services

• Draw lessons for improving the R&D and innovation measurement framework

Project objectives

• Use wide range of firm-level survey data to capture complexity of firms’ competitive strategies

• International coordination for cross-country comparisons: – EU (CIS) and non-EU countries

• Exploit new data linking possibilities (e.g. patents and ORBIS)

• Adopt broader framework of analysis to explore the relation between innovation in service sectors and service innovation

A distinctive methodological approach

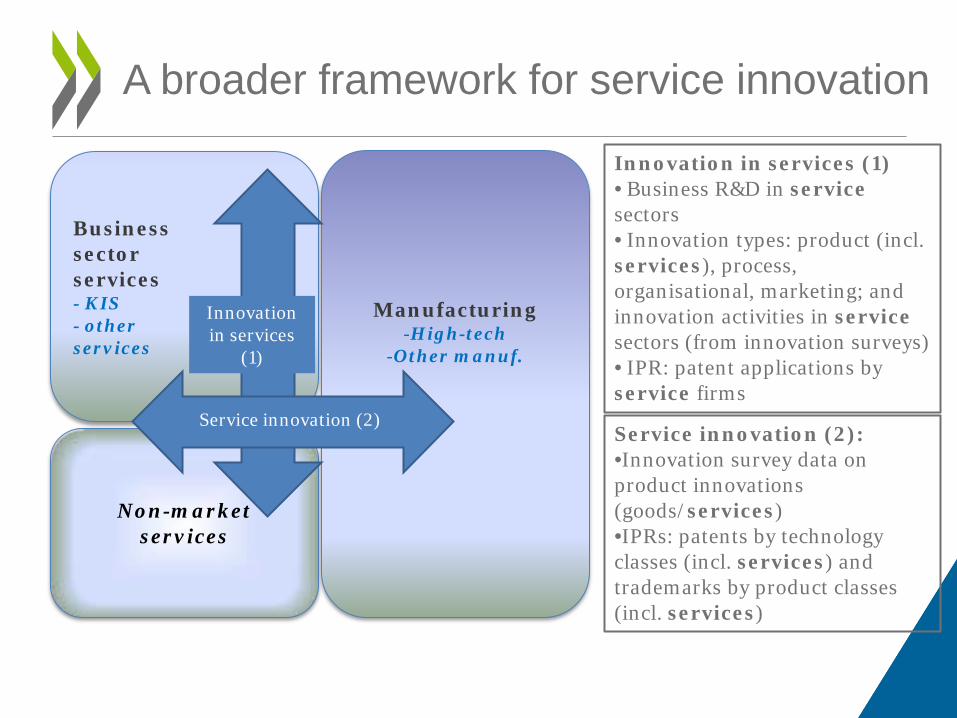

A broader framework for service innovation

Business sector services - KIS - other services

Non-market services

Manufacturing -High-tech

-Other manuf.

Innovation in services

(1)

Service innovation (2)

Innovation in services (1) • Business R&D in service sectors • Innovation types: product (incl. services), process, organisational, marketing; and innovation activities in service sectors (from innovation surveys) • IPR: patent applications by service firms

Service innovation (2): •Innovation survey data on product innovations (goods/services) •IPRs: patents by technology classes (incl. services) and trademarks by product classes (incl. services)

R&D IN SERVICES

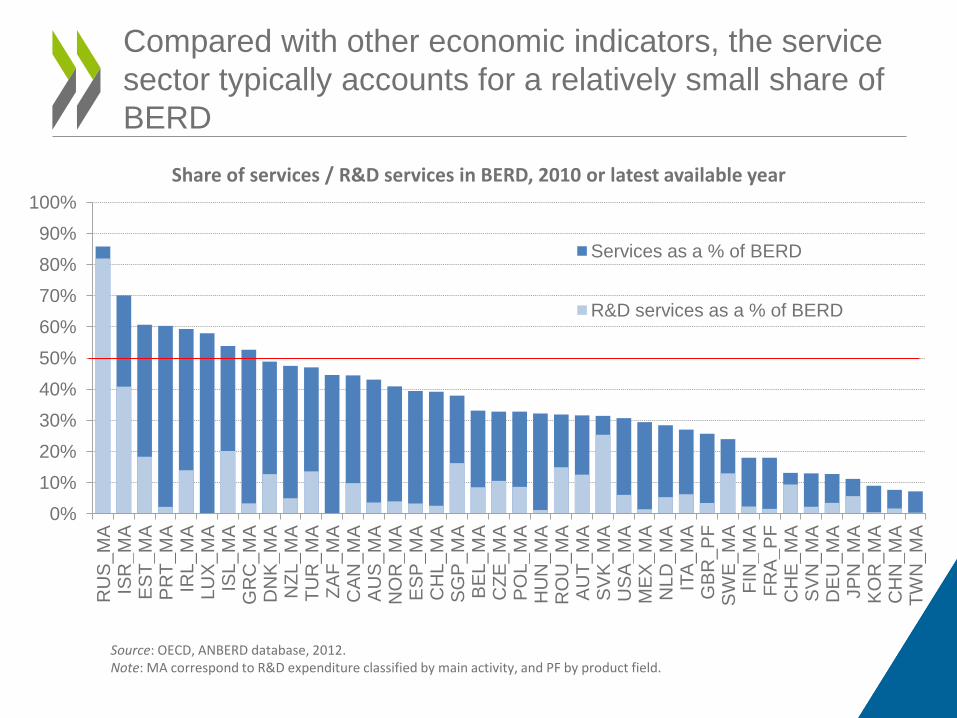

Compared with other economic indicators, the service sector typically accounts for a relatively small share of BERD

Share of services / R&D services in BERD, 2010 or latest available year

Source: OECD, ANBERD database, 2012. Note: MA correspond to R&D expenditure classified by main activity, and PF by product field.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RU

S_M

A

ISR

_MA

E

ST_

MA

P

RT_

MA

IR

L_M

A

LUX

_MA

IS

L_M

A

GR

C_M

A

DN

K_M

A

NZL

_MA

TU

R_M

A

ZAF_

MA

C

AN

_MA

A

US

_MA

N

OR

_MA

E

SP

_MA

CH

L_M

A

SG

P_M

A B

EL_

MA

CZE

_MA

P

OL_

MA

H

UN

_MA

R

OU

_MA

A

UT_

MA

S

VK

_MA

US

A_M

A

ME

X_M

A

NLD

_MA

IT

A_M

A

GB

R_P

F S

WE

_MA

FI

N_M

A

FRA

_PF

CH

E_M

A

SV

N_M

A

DE

U_M

A

JPN

_MA

K

OR

_MA

C

HN

_MA

TW

N_M

A

Services as a % of BERD

R&D services as a % of BERD

-4 -2 0 2 4 6 8

10 12 14 16

FIN

K

OR

A

UT

ES

T JP

N

SV

N

PR

T D

EU

H

UN

C

ZE

AU

S

ES

P

BE

L C

AN

IT

A

ME

X

GR

C

NLD

IR

L P

OL

FRA

S

WE

N

OR

G

BR

Between-sector changes Within changes in non-service sectors Within changes in services Total changes

While the structural shift to less R&D-intensive sectors reduces headline R&D intensity, R&D intensity within services is increasing

Decomposition of R&D intensity changes Basis points, 1995-2009 (or closest year available) yearly average

Source: OECD calculations based on STAN and ANBERD, 2012.

Innovation is broader than R&D, particularly in services…

Share of firms with internal R&D activities among product innovating firms, by broad sector, 2006-2008

0

10

20

30

40

50

60

70

80

90

100

FIN SVN DEU FRA SWE NLD BEL CZE NOR HUN EST AUT ESP PRT SVK IRL ITA AUS

Manufacturing Services %

Source: OECD calculations based on European Commission, Eurostat, 2008 Community Innovation Survey, microdata, 2012 and national innovation surveys from Australia, Austria and Belgium Note: Weighted.

INNOVATION IN THE SERVICE SECTOR… AND SERVICE INNOVATION ACROSS THE ECONOMY

Innovation rates in KIS are close to those in high-tech manufacturing

Share of firms introducing product, process, organisational or marketing innovation by sector category, 2006-2008

0

10

20

30

40

50

60

70

80

90

High-tech manufacturing Other manufacturing

Knowledge-intensive services Other services %

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 and national innovation surveys from Australia, Austria and Belgium. Note: Weighted

0

10

20

30

40

50 Goods

Service

Process Organisational

Marketing High-tech manufacturing Other manufacturing Knowledge-intensive services Other services

%

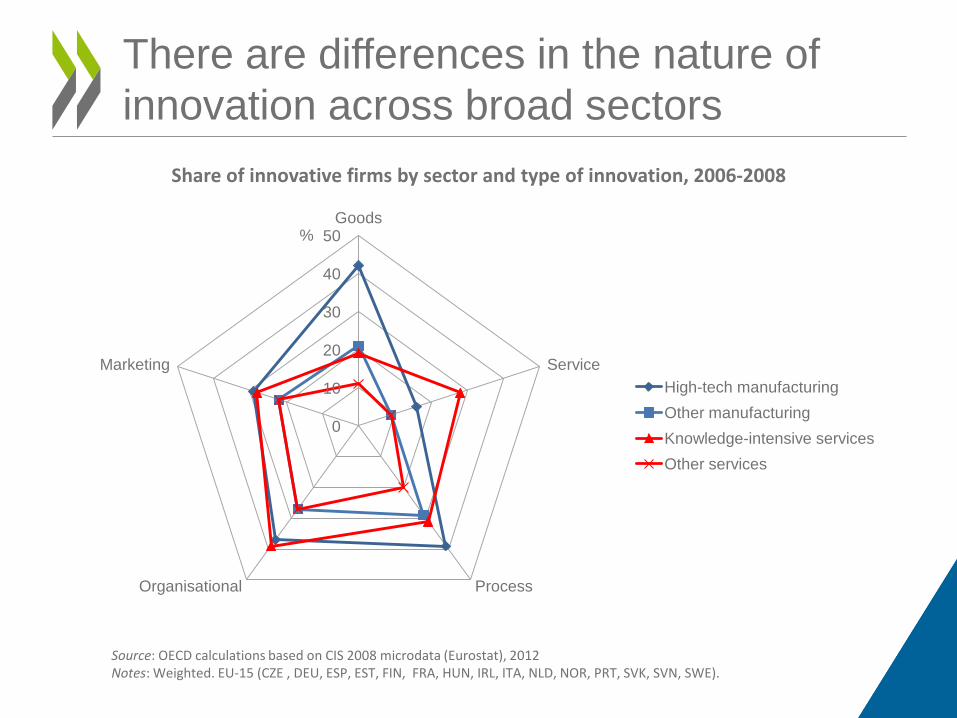

There are differences in the nature of innovation across broad sectors

Share of innovative firms by sector and type of innovation, 2006-2008

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Notes: Weighted. EU-15 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, NLD, NOR, PRT, SVK, SVN, SWE).

Service innovation also takes place in manufacturing and tends to co-occur with goods innovation

Share of product innovating firms that innovate in goods only, in service only or both in goods and in service, by broad sector and country, 2006-2008

0

20

40

60

80

100

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

Man

ufac

turin

g S

ervi

ces

AUS AUT BEL CZE DEU ESP EST FIN FRA HUN IRL ITA NLD NOR PRT SVK SVN SWE

Goods only Goods and service Service only %

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 and national innovation surveys from Australia, Austria and Belgium. Note: Weighted.

Some manufacturing sectors are among the most likely to introduce new services

Sector relative likelihood of innovating by type of innovation, 2006-2008

-1.5 -1

-0.5 0

0.5 1

1.5 ICT services

Scientific and technical services

Finance and insurances

Computer and electrical equipment

Machinery and equipment

Coke, petroleum, chemicals

Manufacturing n.e.c.

Wood, pulp, paper, publishing, printing

Rubber and plastics Wholesale, retail trade Transportation

Pharmaceuticals

Basic metals, metal production

Motor vehicles

Other transport equipment

Textiles, apparel, leather

Food, beverages, tobacco

Goods Service Product or process Organisational Marketing

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Notes: Weighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE). Marginal effect of sector on the probability of innovating, controlling for size, belonging to a group/to a multinational and country - baseline=Food, beverage and tobacco. Sectors are ordered according to their relative likelihood of introducing service innovation.

SERVICE INNOVATION ROLE IN FIRMS’ INNOVATION STRATEGIES

Service innovation plays a central role in the innovation strategies of firms

Multi-dimensional scaling of innovation types and activities, 2006-2008

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Notes : Unweighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE).

good service

methods

logistic

supporting activities

abandoned

ongoing

business practices work responsibilities

external relations

design/packaging promotion

placement pricing

internal R&D

external R&D

capital

external knowledge

training

market introduction

other activities

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

-0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2 technological

product/marketing

process/organisation

non-technological

product innovations process innovations ongoing or abandoned organisational innovations marketing innovations innovation expenditure

Service innovation uniformly co-occurs with multiple types of innovation

0 0.5

1 1.5

2 2.5

3

Pdt- goods

Pdt- service Mkt-

design Mkt-

placement Mkt-

promotion Pcs- methods

Mkt- pricing

Org- work respons…

Org- external …

Org- busines…

Pcs- logistics

Pcs- supporti…

Increase range of goods or services

0 0.5

1 1.5

2 Pdt- goods

Pcs- methods

Mkt- design

Org- busines…

Pcs- supporti…

Org- work responsi…

Mkt- pricing

Pdt- service

Org- external …

Pcs- logistics

Mkt- promotion

Mkt- placement

Replace outdated products or processes

0 0.5

1 1.5

2 2.5 Pdt- goods

Pdt- service

Mkt- placement

Org- external … Mkt-

design Pcs-

methods Mkt-

promotion

Mkt- pricing

Org- work responsi…

Org- busines…

Pcs- logistics

Pcs- supporti…

Enter new markets

0 0.5

1 1.5

2 2.5 Pdt- goods

Mkt- design

Pdt- service

Mkt- placement

Mkt- promotion

Mkt- pricing

Pcs- methods

Org- work responsi…

Org- busines…

Org- external …

Pcs- logistics

Pcs- supporti…

Increase market share

0

0.5

1

1.5

Pcs- methods

Pdt- goods Org-

busines… Pdt-

service Mkt-

design Org- work responsi…

Mkt- promotion

Pcs- logistics

Mkt- pricing

Pcs- supporti…

Mkt- placement

Org- external …

Improve quality of goods or services

0 0.5

1 1.5

2

Pcs- methods

Org- busines…

Pcs- supporti…

Pcs- logistics

Org- work responsi…

Pdt- service

Mkt- pricing

Mkt- design

Org- external …

Mkt- promotion

Mkt- placement

Pdt- goods

Improve flexibility for producing goods or services

Service innovation is related to a wide range of objectives

Relationship between innovation types and various innovation objectives, 2006-2008

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Notes: Unweighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE). Proportional odds ratios obtained from ordered logistic regressions performed on the level of importance (high, medium, low, not relevant) given by firms to different innovation objectives for product (goods or service) or process innovations activities, on the sample of innoactive firms (firms with product or process innovation, or ongoing/abandoned activities for product or process innovation).

THE OPENNESS OF INNOVATION IN SERVICES

When introducing new products or processes, firms in services are more likely to rely on external inputs for development

Share of product and process innovating firms whose innovation was developed by or with others, by sector category, 2006-2008

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Note: Weighted. EU-14 (CZE , DEU, ESP, EST, FIN, FRA, HUN, ITA, NLD, NOR, PRT, SVK, SVN, SWE).

0 5

10 15 20 25 30 35 40 45 50

High-tech manufacturing

Other manufacturing Knowledge-intensive services

Other services

Product innovation Process innovation %

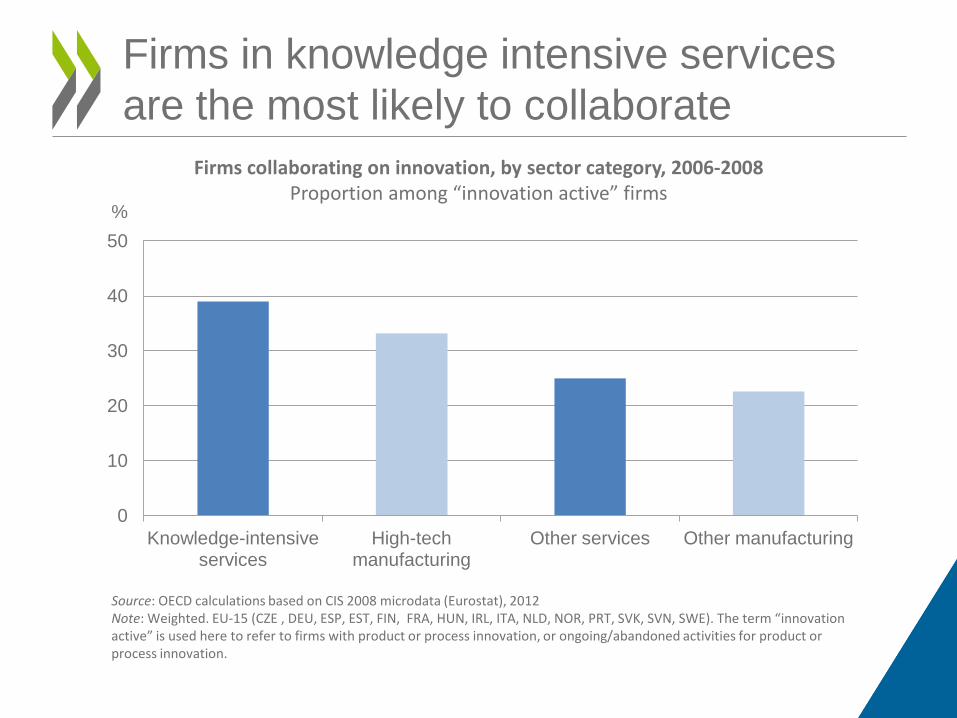

Firms in knowledge intensive services are the most likely to collaborate

Firms collaborating on innovation, by sector category, 2006-2008 Proportion among “innovation active” firms

0

10

20

30

40

50

Knowledge-intensive services

High-tech manufacturing

Other services Other manufacturing

%

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Note: Weighted. EU-15 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, NLD, NOR, PRT, SVK, SVN, SWE). The term “innovation active” is used here to refer to firms with product or process innovation, or ongoing/abandoned activities for product or process innovation.

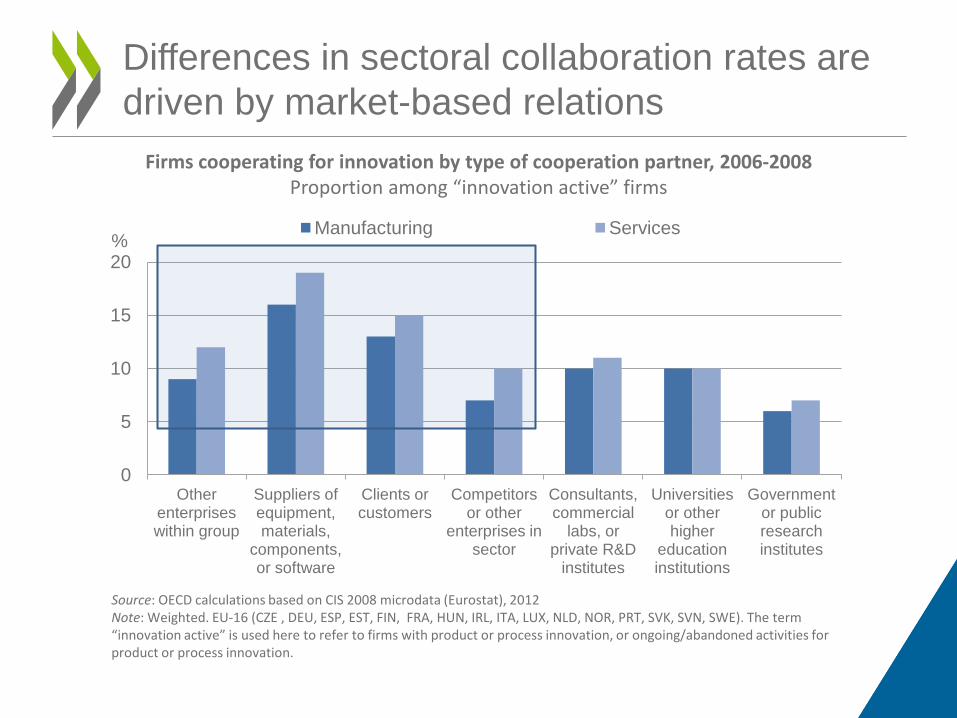

Differences in sectoral collaboration rates are driven by market-based relations

Firms cooperating for innovation by type of cooperation partner, 2006-2008 Proportion among “innovation active” firms

0

5

10

15

20

Other enterprises within group

Suppliers of equipment, materials,

components, or software

Clients or customers

Competitors or other

enterprises in sector

Consultants, commercial

labs, or private R&D

institutes

Universities or other higher

education institutions

Government or public research institutes

Manufacturing Services %

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Note: Weighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE). The term “innovation active” is used here to refer to firms with product or process innovation, or ongoing/abandoned activities for product or process innovation.

IMPACTS OF SERVICE INNOVATION ON PERFORMANCE

Service innovation is positively related to firms’ performance

Effect of different types of innovation on employment growth, 2006-2008

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Note: Weighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE). Marginal effects obtained from OLS regressions performed on firms' employment growth rates between 2006 and 2008 controlling for size, country, and belonging to a domestic/multinational group. All innovation types are introduced jointly in the regression. White bars correspond to non-significant coefficients (at 5 % level).

-0.04

-0.02

0

0.02

0.04

0.06

0.08

Goods Process Service Organisational Marketing

All sample High-tech manufacturing Other manufacturing Knowledge-intensive services Other services

Do service innovation activities also benefit competitors?

Implied “impacts” of various types of innovation by other firms within same sector, 2006-2008

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

Goods innovation spillovers

Service innovation spillovers

Product-process innovation spillovers

Marketing innovation spillovers

Organisational innovation spillovers

Internal R&D activity

spillovers

All sample High-tech manufacturing Other manufacturing

Knowledge-intensive services Other services

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Notes: Weighted. EU-16 (CZE , DEU, ESP, EST, FIN, FRA, HUN, IRL, ITA, LUX, NLD, NOR, PRT, SVK, SVN, SWE). The bars correspond to the marginal effects of “spillovers” on firms' likelihood to introduce the corresponding innovation type or to engage in the corresponding activity. “Spillovers” were calculated as the weighted average share of firms introducing the corresponding innovation type or engaging in the corresponding innovation activity among other firms in the same sector (NACE rev. 2 at 2 digit level). White bars correspond to non-significant coefficients (at 5 % level).

FORMS OF PROTECTION OF SERVICE-BASED INNOVATION

How do service firms protect their innovations?

Share of firms using various intellectual property rights by sector category

Source: OECD calculations based on CIS 2006 microdata (Eurostat), 2012 Note: Weighted. EU-10 (CZE, ESP, EST, GRC, HUN, IRL, LUX, NOR, PRT, SVK). The shares correspond respectively to firms that have applied for a patent, registered an industrial design, registered a trademark or claimed copyright during the three years 2004 to 2006.

0%

2%

4%

6%

8%

10%

12%

14%

16%

High-tech manufacturing

Other manufacturing KIS Other services

Patents Designs Trademarks Copyright

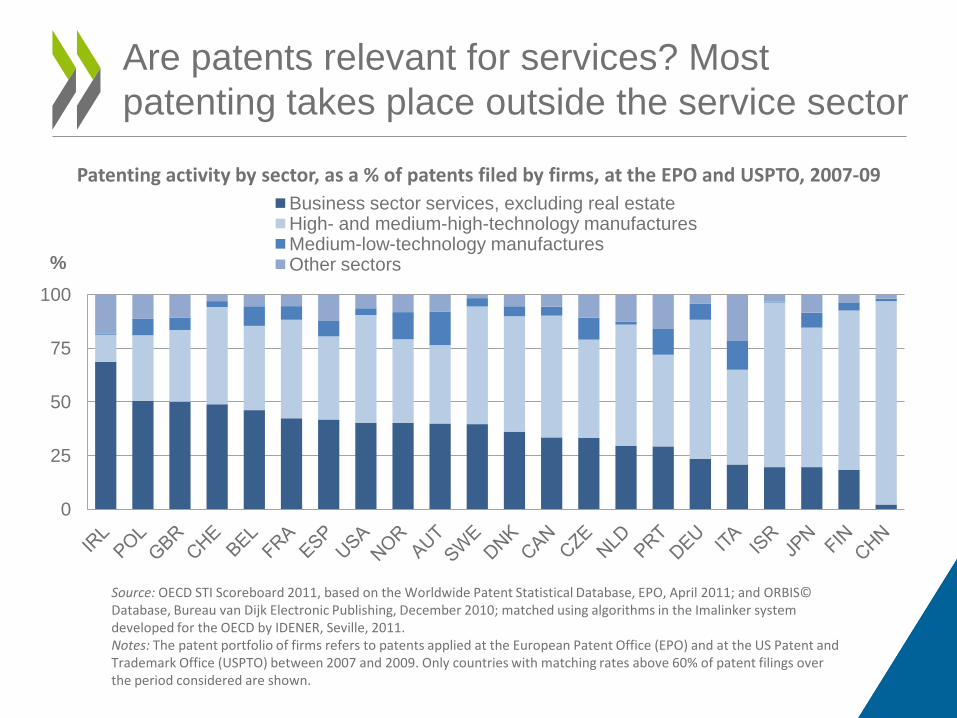

Are patents relevant for services? Most patenting takes place outside the service sector

Patenting activity by sector, as a % of patents filed by firms, at the EPO and USPTO, 2007-09

0

25

50

75

100

%

Business sector services, excluding real estate High- and medium-high-technology manufactures Medium-low-technology manufactures Other sectors

Source: OECD STI Scoreboard 2011, based on the Worldwide Patent Statistical Database, EPO, April 2011; and ORBIS© Database, Bureau van Dijk Electronic Publishing, December 2010; matched using algorithms in the Imalinker system developed for the OECD by IDENER, Seville, 2011. Notes: The patent portfolio of firms refers to patents applied at the European Patent Office (EPO) and at the US Patent and Trademark Office (USPTO) between 2007 and 2009. Only countries with matching rates above 60% of patent filings over the period considered are shown.

Service trademarks are widely used, often in combination with goods

Trademark applications designating goods and/or service classes by country, 2006-2008 As a percentage of trade mark applications at the OHIM and USPTO

0 10 20 30 40 50 60 70 80 90

100

SV

N

ES

P

SV

K

CZE

LU

X E

ST

FIN

A

UT

GB

R

PO

L N

OR

E

U27

N

LD

IRL

HU

N

DE

U

US

A

BE

L G

RC

O

EC

D

DN

K

RU

S

PR

T SW

E

FRA

IN

D

CA

N

ISL

BR

A

CH

E

ITA

A

US

N

ZL

ME

X TU

R

ZAF

ISR

K

OR

B

RIIC

S

CH

L JP

N

CH

N

IDN

Goods only Goods and services Service only %

Source: OECD calculations based on United States Patent and Trademark Office Bulk Downloads: Trademark Application Text hosted by Google cloud (http://www.google.com/googlebooks/uspto-trademarks.html), and OHIM Community Trademark Database; CTM Download, 2011.

BARRIERS TO SERVICE INNOVATION AND PUBLIC SUPPORT

Relative to high tech manufacturing, firms in service sector tend to report fewer or similar obstacles to innovation

Relative likelihood of reporting hampering factors as important by sector, 2004-2006

-0.5 -0.4 -0.3 -0.2 -0.1

0 0.1 0.2 0.3

Lack of funds within enterprise

Lack of finance from outside

Innovation costs too high

Lack of qualified personnel

Lack of information on technology

Lack of information on markets

Difficulty in finding cooperation partners

Market dominated by established enterprises

Uncertain demand for innovation

No need due to prior innovation

No need because of no demand for innovation

High-tech manufacturing Other manufacturing KIS Other services

Source:: OECD calculations based on CIS 2006 microdata (Eurostat), 2012 Note: Weighted. EU-11 (CZE, ESP, EST, GRC, HUN, IRL, LUX, NOR, PRT, SVK, SWE). Marginal effect of belonging to each sector category on the probability to consider each hampering factor as of medium or high importance, obtained from probit model regressions run on each hampering factor. Baseline=High-tech manufacturing.

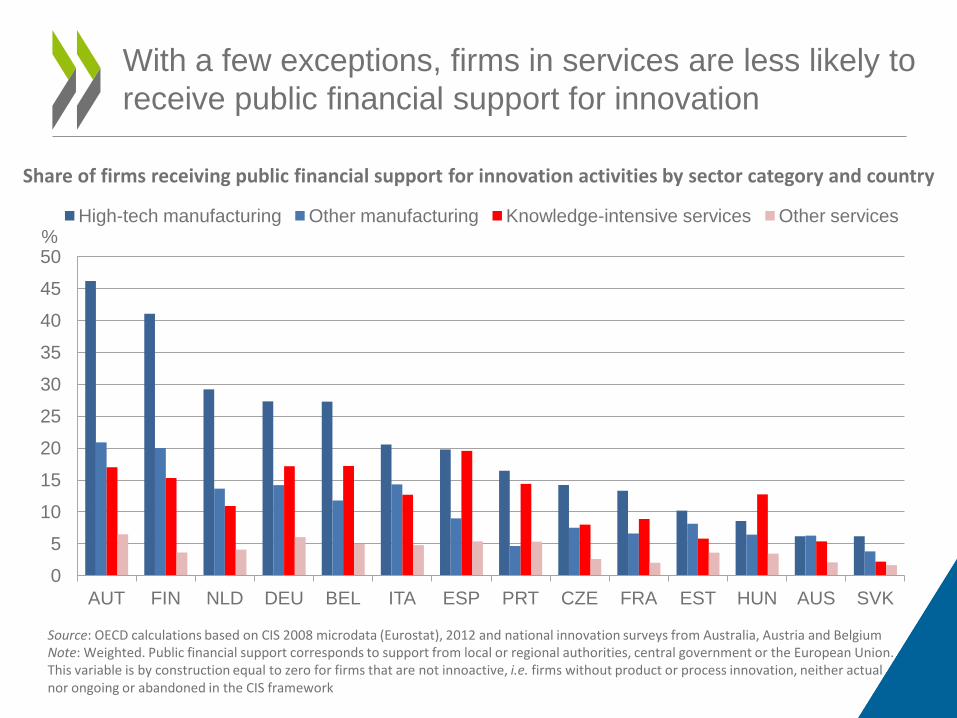

With a few exceptions, firms in services are less likely to receive public financial support for innovation

Share of firms receiving public financial support for innovation activities by sector category and country

0

5

10

15

20

25

30

35

40

45

50

AUT FIN NLD DEU BEL ITA ESP PRT CZE FRA EST HUN AUS SVK

High-tech manufacturing Other manufacturing Knowledge-intensive services Other services %

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 and national innovation surveys from Australia, Austria and Belgium Note: Weighted. Public financial support corresponds to support from local or regional authorities, central government or the European Union. This variable is by construction equal to zero for firms that are not innoactive, i.e. firms without product or process innovation, neither actual nor ongoing or abandoned in the CIS framework

The sectoral public funding for innovation gap has narrowed slightly over time in most countries

Relative likelihood of manufacturing firms to receive public financial support compared to services in 2004-2006 and 2008-2010

Source: OECD calculations based on Eurobase CIS 2010 and CIS 2006 microdata (Eurostat), 2012 Notes: Unweighted. The points represent the ratio of the share of innoactive firms receiving public financial support in manufacturing to those in services in the corresponding countries and years. Innoactive firms are those with product or process innovation, or ongoing/abandoned activities for product or process innovation.

BEL CZE

DEU EST

ESP

LUX

HUN

NLD

POL PRT

SVK

0

1

2

3

4

5

0 1 2 3 4 5

2008

-201

0

2004-2006

The sectoral distribution of R&D tax incentives resembles that of business R&D spending

Proportion of services in BERD and R&D tax incentives, 2008 (or nearest year)

0

10

20

30

40

50

60

70

GBR CAN FRA USA CZE NDL JPN

Share of services in business R&D, main activity Share of R&D tax incentives to service sector

Source: OECD/NESTI R&D tax incentives questionnaire, MSTI, RDS.

Public support is associated with higher rates of service innovation…

Effect of public support on the propensity of firms to introduce different types of innovations

-0.05

0

0.05

0.1

0.15

0.2

0.25

Product new to market

Product Goods Service Marketing Organisational Product or process

Source: OECD calculations based on CIS 2008 microdata (Eurostat), 2012 Note: Weighted. EU-13 (CZE , DEU, ESP, EST, FIN, FRA, HUN, ITA, LUX, NLD, PRT, SVK, SVN). Marginal effect of support on firms' likelihood to introduce different types of innovation, obtained from probit model regressions controlling for size, country and belonging to a domestic/multinational group. The regressions were run on the sample of innoactive firms, that is firms with product or process innovation, or ongoing/abandoned activities for product or process innovation. White bars correspond to coefficients that are not significant at the 5 % level.

KEY MESSAGES

1. The distinction between R&D and innovation is far more important in services. These two terms are too often confused in the debate.

2. Service innovation is widespread and takes place across all sectors. It has specific features of relevance to policy makers:

– It plays a pivotal role in business innovation strategies. – It is more reliant on external inputs and more collaborative than other types – Innovation relationships are primarily market-based, with suppliers,

customers and firms in same group and market. – Service sector companies use rather different mechanisms to appropriate the

benefits of their innovations

3. Service innovation is positively related to employment and turnover growth, and the evidence appears to be consistent with positive spillovers

4. Service firms do not report higher incidence of barriers to innovation, but the data suggest limited awareness among less knowledge intensive services

5. Service firms less likely to receive public support for innovation, which is mainly oriented towards R&D.

Preliminary conclusions from the analysis