31

RDI Workshop: Hedging as a Cooperative and NZX Milk Futures Confidential to Fonterra Co-operative Group May 2016

RDI Workshop: Hedging as a Cooperative

and NZX Milk Futures

Confidential to Fonterra Co-operative Group

May 2016

Page 2 Confidential to Fonterra Co-operative Group

Disclaimer

The information and comments in this presentation are necessarily generalized, are

not intended to be used for specific trading strategies, and do not constitute advice

or a securities recommendation or any offer to buy, sell, subscribe for, any

securities, contracts or any derivative.

Commodity and derivative trading is risky and Fonterra, its officers, employees, and

agents do not warrant its accuracy, adequacy, currency, or that it is suitable for your

intended use. Any examples given are illustrative and are not indicative of future

performance or actual outcomes of particular trading strategies.

Page 3 Confidential to Fonterra Co-operative Group

1. History of Fonterra Risk Management

• Why do we manage risk?

• Whats creates commodity risk for the Co-op?

• How do we manage it?

2. NZX Milk Futures

• The journey, how did we get here?

• The contract

RDI Dairy Risk Management Workshop

Page 4 Confidential to Fonterra Co-operative Group

Agricultural commodity prices exhibit

extreme volatility

WMP 41%

SMP 33%

AMF 35%

Page 5 Confidential to Fonterra Co-operative Group

What creates Commodity Risk within Fonterra

1. Asset footprint

2. Forward contracting

History of Fonterra Risk Management

Page 6 Confidential to Fonterra Co-operative Group

New Zealand

Processing Sites

Page 7 Confidential to Fonterra Co-operative Group

Milk Price Products

AMF

SMP

WMP

Milk Price Products

Non Milk Price Product

Farmer Market

Asset footprint

• Fonterra passes the spot price through to the farmer in the form of Milk Price

• Due to the mix of assets not all sales return Milk Price

Cost of Milk Fonterra Assets

Page 8 Confidential to Fonterra Co-operative Group

Extreme Volatility Impacting on Margins

Page 9 Confidential to Fonterra Co-operative Group

Forward contracting

• Customers require certainty in order to value their COGS when making pricing decisions for end users.

• When Fonterra provides a long dated price for a customer it exposes itself to rising commodity prices.

• Commodity Risk and Trading (CR&T) assume and manage the risk on Fonterra’s behalf.

Buy Sell

(short) (long)

Page 10 Confidential to Fonterra Co-operative Group

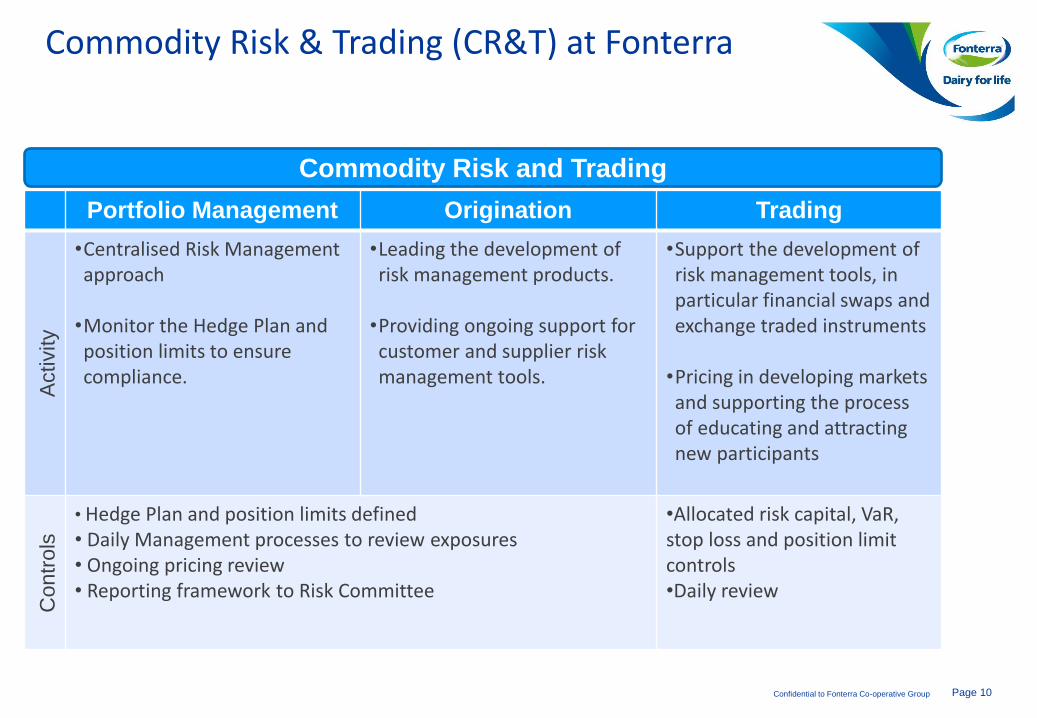

Commodity Risk & Trading (CR&T) at Fonterra

Commodity Risk and Trading

Portfolio Management Origination Trading

Activity

•Centralised Risk Management approach

•Monitor the Hedge Plan and position limits to ensure compliance.

•Leading the development of risk management products.

•Providing ongoing support for customer and supplier risk management tools.

•Support the development of risk management tools, in particular financial swaps and exchange traded instruments

•Pricing in developing markets and supporting the process of educating and attracting new participants

Contr

ols

• Hedge Plan and position limits defined • Daily Management processes to review exposures • Ongoing pricing review • Reporting framework to Risk Committee

•Allocated risk capital, VaR, stop loss and position limit controls •Daily review

Page 11 Confidential to Fonterra Co-operative Group

Convergence of international prices

As the trading of dairy matures we see a convergence of global prices.

Page 12 Confidential to Fonterra Co-operative Group

Risk is managed using exchange traded contracts

• CR&T inherits the portfolio of long dated physical commodity products from Fonterra.

• The financial markets are used, where possible, to offset exposure, lock in margin and reduce risk for Fonterra.

Buy Sell

(short) (long)

Page 13 Confidential to Fonterra Co-operative Group

The CR&T objective is to reduce risk for Fonterra

CR&T Portfolio

Long Fixed Priced

Contracts

GMP

Physical Collars

Derivative Markets

Forward Price Curve

Buy Sell

(short) (long)

Page 14 Confidential to Fonterra Co-operative Group

Strategic commodity stream decisions

Page 15 Confidential to Fonterra Co-operative Group

There are 3 main pricing regions, all have dairy

derivatives and are at different stages of development

International

WMP, SMP,

AMF, butter

SMP, Butter,

Whey

Cheese,

Butter, Whey,

NFDM SMP, Butter

Whey

Page 16 Confidential to Fonterra Co-operative Group

Global Dairy Contract Summary

Exchange Contract Use Settlement Type Settles To Contract Size (mt) Currency Open Interest Lots Traded/Day Months Priced Expected Launch

Class III Milk Hedge Cheese Cash USDA monthly price 90 USD 20,000-40,000 500-1,000 6-24 Established

Nonfat Dry Milk Hedge NFDM/SMP Cash USDA monthly weighted average price 20 USD 5,000-10,000 100-1,000 6-24 Established

Butter Hedge Butter Cash USDA monthly weighted average price 9 USD 3,000-5,000 50-200 6-24 Established

Cheese Hedge Cheese Cash USDA monthly weighted average price 9 USD 10,000-20,000 200-400 6-24 Established

Class IV Milk Hedge NFDM/SMP Cash USDA monthly price 90 USD 2,000-5,000 10-100 6-24 Established

Dry Whey Hedge Whey Cash USDA monthly weighted average price 20 USD 3,000-5,000 50-200 6-24 Established

WMP Hedge WMP/Cheese Cash

GDT - simple average of the two WMP C2 prices for

the month 1 NZD 25,000-30,000 500-3000 6-18 Established

SMP Hedge WMP/NFDM Cash

GDT - simple average of the two SMP C2 prices for

the month 1 NZD 3,000-10,000 100-500 6-18 Established

AMF Hedge AMF Cash

GDT - simple average of the two AMF C2 prices for

the month 1 NZD 500-1,000 20-200 6-18 Established

Butter Hedge Butter Cash

GDT - simple average of the two Butter C2 prices for

the month 1 NZD 500-1,000 20-200 6-18 Established

Milk Futures Hedge Milk Cash TBC 10 NZD N/A N/A N/A 2016

SMP Hedge SMP/NFDM Cash

Indexed simple average of German (33%), France

(33%) & The Netherlands (33%) prices 5 EUR 500-1,000 0-300 6-18 Established

Butter Hedge Butter Cash

Indexed simple average of German (33%), France

(33%) & The Netherlands (33%) prices 5 EUR 0-500 0-100 6-18 Established

Whey Powder Hedge Why Cash

Indexed simple average of German (33%), France

(33%) & The Netherlands (33%) prices 5 EUR 0-500 - 6-18 Established

SMP Hedge SMP/NFDM Physical

Physical delivery to one of the delivery points set

by Euronext 6 EUR 0-100 - 6-18 Established

Whey Powder Hedge Butter Physical

Physical delivery to one of the delivery points set

by Euronext 6 EUR 0-100 - 6-18 Established

Butter Hedge Why Physical

Physical delivery to one of the delivery points set

by Euronext 6 EUR 0-100 - 6-18 Established

CME

NZX

EEX

Euronext

Page 17 Confidential to Fonterra Co-operative Group

The journey to NZX Milk Price Futures

Page 18 Confidential to Fonterra Co-operative Group

Drivers for Risk Tools – Volatility and Uncertainty They are here to stay…

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2 J

ul 2

00

8

4 N

ov

20

08

3 F

eb

20

09

2 J

un

20

09

6 O

ct 2

00

9

2 F

eb

20

10

1 J

un

20

10

15

Sep

20

10

16

No

v 2

01

0

18

Jan

20

11

15

Mar

20

11

17

May

20

11

19

Ju

l 20

11

20

Sep

20

11

15

No

v 2

01

1

17

Jan

20

12

20

Mar

20

12

15

May

20

12

17

Ju

l 20

12

18

Sep

20

12

20

No

v 2

01

2

16

Jan

20

13

19

Mar

20

13

15

May

20

13

16

Ju

l 20

13

17

Sep

20

13

19

No

v 2

01

3

21

Jan

20

14

18

Mar

20

14

20

May

20

14

15

Ju

l 20

14

16

Sep

20

14

18

No

v 2

01

4

20

Jan

20

15

17

Mar

20

15

19

May

20

15

15

Ju

l 20

15

15

Sep

20

15

USD/MT

GDT Trading Event

Dairy Volatility Since 2008

WMP

SMP

AMF

Page 19 Confidential to Fonterra Co-operative Group

What does this volatility look like for NZ farmers? The volatility effect on Fonterra Farmgate Milk Price

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15* 2015/16*

$/KgMS

Dairy Season

Fonterra Farmgate Milk Price

10yr Average FWE

Page 20 Confidential to Fonterra Co-operative Group

Milk Price Futures

Page 21 Confidential to Fonterra Co-operative Group

GDT was the enabler..

• Established by Fonterra in 2008

• Twice monthly auctions

• Helps discover the ‘benchmark price’

• Major volumes transacted

• Hundreds of bidders from more than 80

countries

• Other major global suppliers have joined:

Arla, Murray Goulburn and Dairy Farmers

of America

• www.globaldairytrade.info

Page 22 Confidential to Fonterra Co-operative Group

Page 23 Confidential to Fonterra Co-operative Group

Guaranteed Milk Price

Page 24 Confidential to Fonterra Co-operative Group

What is the Fonterra Farmgate Milk Price?

Page 25 Confidential to Fonterra Co-operative Group

NZX Milk Price Futures Contract and the Fonterra

Farmgate Milk Price

Approximately 85% of NZ farmers supply Fonterra, with some other processors also

hinging their milk price to the final Fonterra Farmgate Milk Price (“Milk Price”)

Because many NZ farmers are paid on this basis, a futures contract settling to the Milk

Price will represent a perfect hedge to the majority of NZ farmers (before allowance for

milk composition).

The Milk Price is already reviewed by the NZ Commerce Commission as required under

the Dairy Industry Restructuring Act (DIRA).

DIRA requires the Milk Price to be at a level that is fair to both farmers and Fonterra’s

competition. For this reason Fonterra’s competitors also understand well how their

businesses interact with the Milk Price.

Both Fonterra and the NZ Commerce Commission already have stringent processes,

guidelines and reporting standards relating to the Milk Price

For the reasons above and others, the NZX Milk Price Futures contract settles to the

final announced Fonterra Farmgate Milk Price.

Page 26 Confidential to Fonterra Co-operative Group

How the Milk Price mechanism works

Page 27 Confidential to Fonterra Co-operative Group

Or…..How the Milk Price mechanism works

Page 28 Confidential to Fonterra Co-operative Group

The Milk Price model

Collects all the Milk that Fonterra would collect ~1.6B KGMS

Manufactures 5 products:

WMP, SMP, BMP AMF and Butter

Sells all of these products on the GDT

Theoretical Revenue

MINUS: Operating Costs (to run a company that collects all the milk makes 5 product and sells it

on GDT)

MINUS: Financing Costs

The MILK PRICE

Real Revenue

from 100s of different products priced and sold via a myriad of different channels and

methods.

MINUS: Operating Costs, to run all of Fonterra

MINUS: COGS, or the cost of the milk

EBIT

MINUS: Interest and Tax

Profit and Dividends

Fonterra Cooperative Group Ltd

Or…..How the Milk Price mechanism works

Page 29 Confidential to Fonterra Co-operative Group

Milk Price vs EBIT Some key points to be aware of

The Milk Price Manual assumes that the notional processor in NZ would choose to

export Reference Commodity Products (RCPs) which are the milk powder streams –

WMP, SMP, Butter, AMF and BMP – in simple terms this is using GDT prices and the

actual Fonterra FX rate. This goes into the Milk Price Revenue.

Any additional revenue made by making non-RCP products or by selling RCPs at prices

above GDT prices goes into Earnings Before Interest and Tax. This is reflected in the

distributable profit (dividend and retained earnings) for the shareholders of Fonterra.

Should the prices of the RCPs increase rapidly, the ability of Fonterra to make profits

over and above those prices can be minimal. In this situation the Fonterra Board of

Directors can choose to review the Milk Price down in order to ensure they remain

profitable. This happened in the 2013/14 season when the final Milk Price was reviewed

downwards from $9.00/kgms to $8.40/kgms.

The Board is highly unlikely to review the Milk Price upwards as that would directly

affect the Co-operative’s profitability.

As a Fonterra farmer supplier, the effect on a hedging position using Milk Price futures if

the price is reviewed down is negligible as their underlying physical exposure is to the

final Milk Price.

Page 30 Confidential to Fonterra Co-operative Group

The contract

Page 31 Confidential to Fonterra Co-operative Group

Thank You