44

Re-imagining Personal Banking Driving Behavioral Change via Mobile Mohamed Khalil Director of Product, Data & Partnerships [email protected]

Re-imagining Personal Banking Driving Behavioral Change via Mobile

Mohamed Khalil

Director of Product, Data & Partnerships

Technology Impacts Behaviors

DATA

Storage

Retrieval

Transmission

COMPUTATION

Processing

Analysis

Insight

DECISIONING

Context

Choices

Action

New Ways to Stay Fit

New Ways to Get Around

New Ways to Find Love

There’s Almost Always an App for That

When was the last time you couldn’t…

…find your way?

…name a song?

…check on a flight?

…get the best price?

…choose a restaurant?

…etc.

But What about Banking?

What is the behavior change we’re trying to drive?

Eliminating Coupons?

Eliminating Wallets?

“Just paid our taxi with

Paypass… and didn’t have to

pull out my wallet. Loved it!

@Ryan Caldwell

Eliminating POS?

ELIMINATING FRICTION?

What kind of change?

In a perfect world you would

• buy everything at a discount

• without a physical wallet/purse

• and without having to check out

“I really wish it were easier

for me to spend my money.”

No one. Ever.

Millennials Aren’t Impressed

And They Don’t Expect to Be

Tough financial times for Millennials in the US

Average debt $45,000

Avg. credit cards 3

Unemployment 12.4%

Live with their parents 24%

Don’t pay bills on time 42%

No cash savings 70%

So What is the real Need?

Can it work the other way?

There are currently no other bank, payment, or personal financial

management experiences out there that are positioned in this way.

What we will do…

Transform the retail bank account

into a primary financial app

customers engage with 3-5x daily

What customers will say…

“Moven makes managing my money

as easy as spending it. It helps me

make smarter spending decisions

and motivates me to save.”

Moven is Re-Imagining Personal Banking

Our Business Model

Changing the Business Model of Basic Banking

Traditional Banking Model The Moven Difference

Revenue driven by punitive fees Revenue driven by added value service

High fixed costs (branches, checks, legacy

systems) makes customers unprofitable

Mobile-centric platform (just an app)

dramatically reduces cost to serve, highly

scalable

Convenience and Rate Insight and Control

$250 or more cost per acquisition $25 or less cost per acquisition

Technological laggards with mobile and

social technologies

Mobile-first design, direct social integration,

gamification and payments focus

Saddled with legacy customer base Targeting next gen customers

Moven is Re-Thinking the Bank Business Model

The Phone as Your Account

The “Bank” Account The Mobile Account

Switch banks because

we’re better!

• Rate, Rate, Rate

• More Branches

• Lower Fees

Download the app and

spend smarter!

• Spend Smarter

• Save More

• Live Better

1 2 3

Download the app, use debit card or

contactless sticker

Get instant feedback with every purchase

Track spending across all accounts

Send money easily with social integration

4

The Phone as Your Account

Bank Partner and

BIN Sponsorship

Customer Experience and

Money Management Platform

Customer

Payment

Processor

Network

Partner

Technology

Partners

Biometrics, etc

Bill pay

Future:

How Moven Works Today

Play Games to Build Confidence …still behind the curtain for now

Go Behind the Curtain

Context

(insights)

Control

(choices)

Advice

(wisdom)

Mobile Drives New Behavioral Patterns

Action

(fulfillment)

The Old Way of Getting Around

Context:

Where Am I

Control:

What Can I Do

Advice:

What Should I Do

The New Way of Getting Around

Action

How do I do It

Understanding the Driver

“A crucial fact is that the

human brain is basically a

mammalian brain with a

larger cortex. This means

human behavior will

generally be a compromise

between… animal emotions

and instincts, and… human

deliberation and foresight.”

C. Camerer (Cal Tech), G. Loewenstein (Carnegie-Mellon), D. Prelic (MIT), 2004, Neuroeconomics: Why

economics needs brains. Scandinavian Journal of Economics, 106(3), 555-579.

“We are all just monkeys with money…”

– Tom Waits

Rational Thought

Immediate Rewards

The limbic system is dopaminergic, meaning it responds to

reward-motivated behavior and stimuli.

The Biological Basis of the Human Behavior

Short Run Self Long Run Self

Plans, prepares and optimizes for

long term utility and happiness

A series of sequential selves

all focused on the immediate

“Our theory proposes that many sorts of decision problems should

be viewed as a game between a sequence of short-run impulsive

selves and a long-run patient self.”

Drew Fudenburg (Harvard U.) and David K. Levine (Washington U.), 2006, A dual-self model of impulse control.

American Economic Review, 96(5), 1449-1476.

Dual Self Model of Decision Making

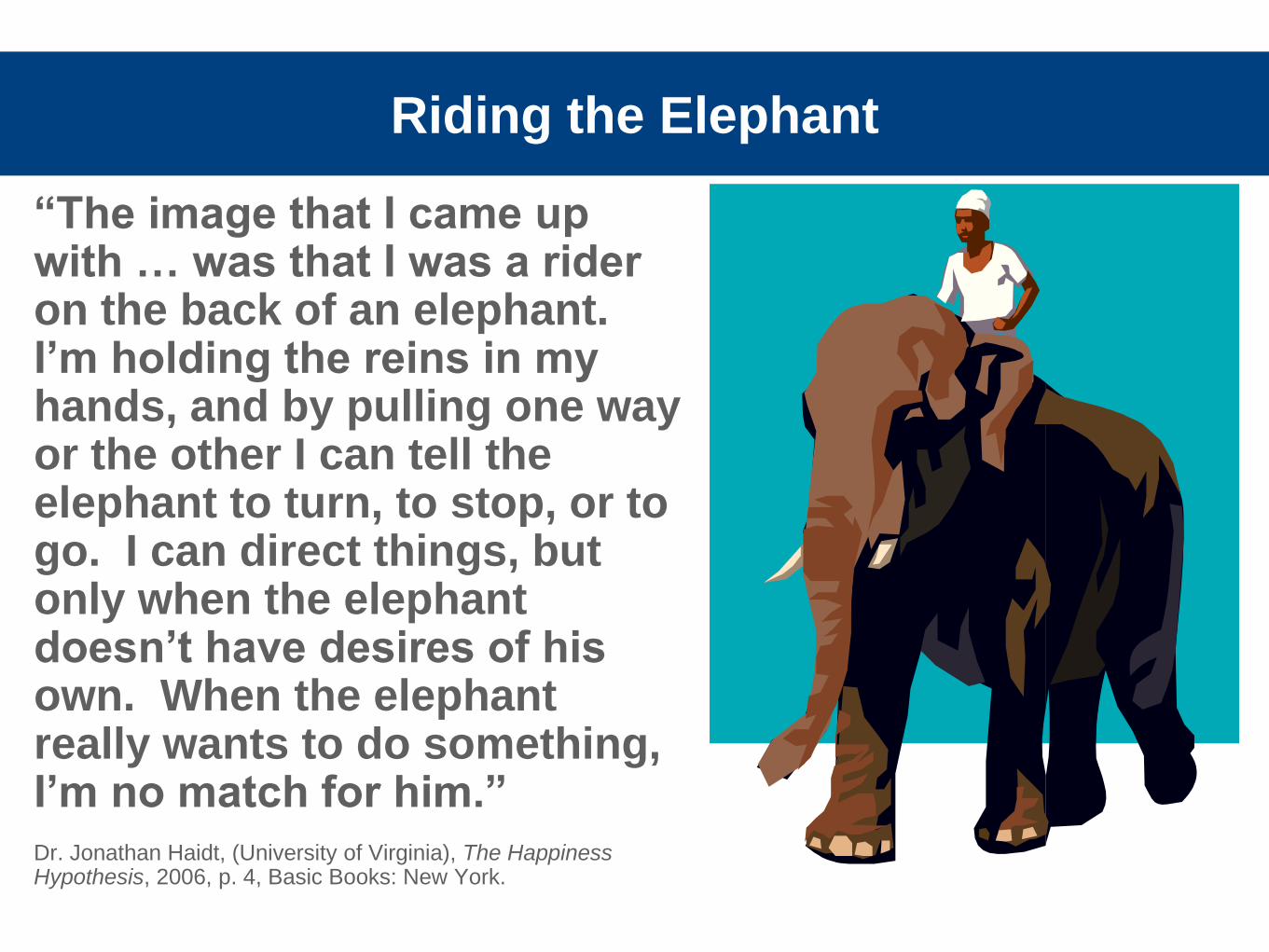

“The image that I came up with … was that I was a rider on the back of an elephant. I’m holding the reins in my hands, and by pulling one way or the other I can tell the elephant to turn, to stop, or to go. I can direct things, but only when the elephant doesn’t have desires of his own. When the elephant really wants to do something, I’m no match for him.” Dr. Jonathan Haidt, (University of Virginia), The Happiness Hypothesis, 2006, p. 4, Basic Books: New York.

Riding the Elephant

Context:

Where Am I

Control:

What Can I Do

Advice:

What Should I Do

So How Do You Design for Success?

Action:

How do I do It

CONTEXT: Where Am I?

EFFORTLESS

MEANINGFUL

•Data Collection

•Transaction Categorization

•Right Level of Insight

• Individual, Peer & Benchmark

CONTEXT: Where Am I?

AND ABOVE ALL

SIMPLE

CONTROL: What Can I Do?

PERSPECTIVE

EMOTIVE

•Short Term vs. Long Term

•Alter Perceptions of Time

•Social Commitments & Life Events

•Make Marginal Decisions Emotional

NOTE: The rider may be compelled by logic or emotion, the elephant,

however, is purely emotional. To engage the elephant, the imagery of

future goals must evoke emotion.

CONTROL: What Can I Do?

AND MUST BE

PREDICTIVE!

ADVICE: What Should I Do?

TRANSPARENT

ALIGNED

•Clarify True Cost of Action

•Highlight Tradeoffs Required

•Offers, Discounts & Rewards

• Product & Merchant Recommendations

ADVICE: What Should I Do?

AND ALWAYS

TRUSTWORTHY

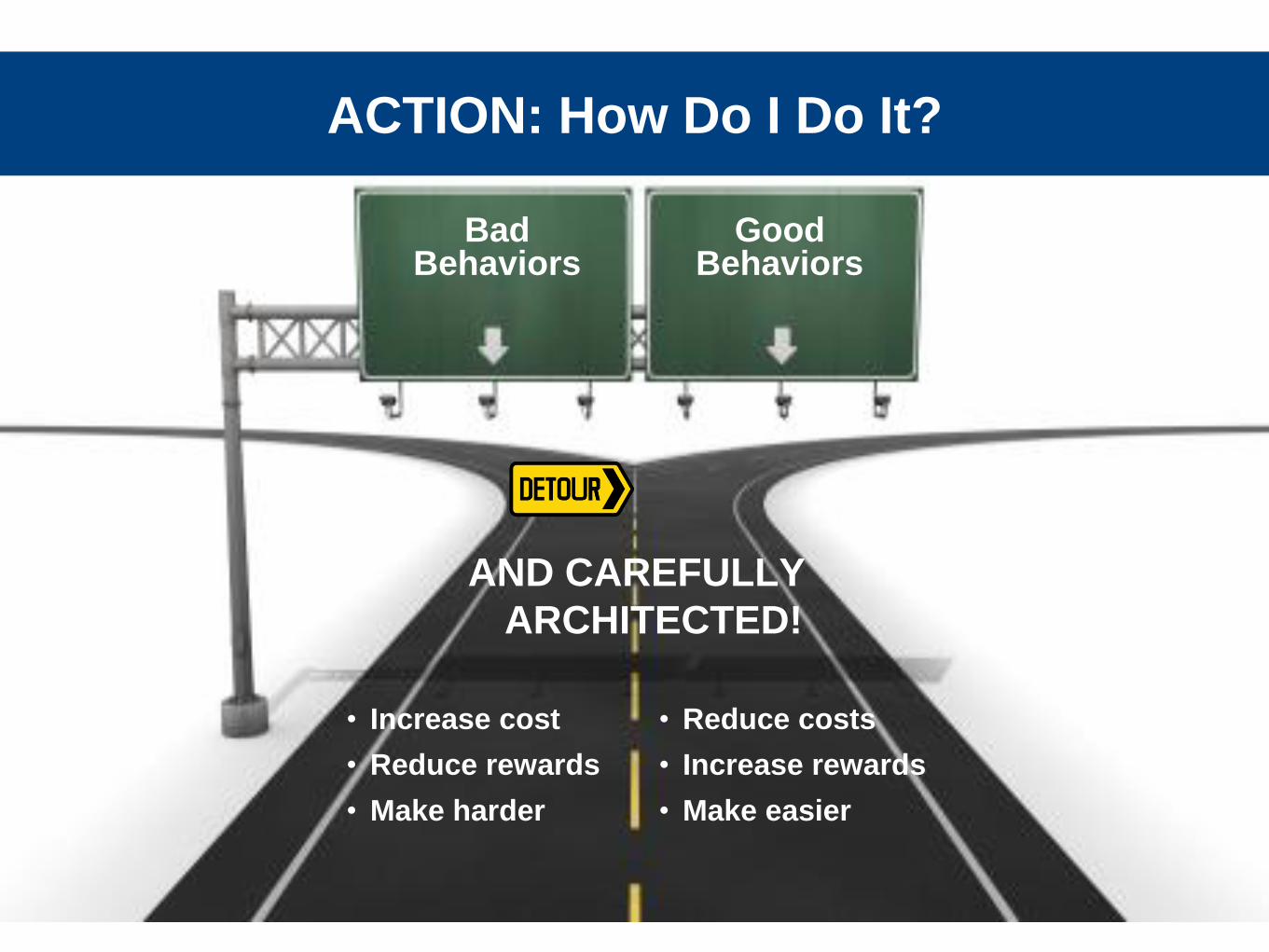

ACTION: How Do I Do It?

FRICTIONLESS

SOCIAL

•Moment of Pause

•Or Instantly Actionable

•Status & Achievements

•Goals & Milestones

Engagement should accommodate

different states of social

transparency.

Pre-Commit to Fewer Temptations

Bad Behaviors

Good Behaviors

• Increase cost

• Reduce rewards

• Make harder

• Reduce costs

• Increase rewards

• Make easier

ACTION: How Do I Do It?

AND CAREFULLY

ARCHITECTED!

Mobile is the Opportunity to Differentiate

Mobile enables differentiated experiences that

• Directly address a segment’s financial concerns

• Create an eco-system of lifestyle solutions

• Establish an ongoing dialogue with the user

Mobile measures success based on users

• Feeling empowered to behave effectively

• Actually improving their finances or lifestyle

• Trusting the provider by accepting the advice

The Journey’s Just Begun

Thank You!

Mohamed Khalil

Director of Product, Data & Partnerships

@getMoven @mikhalil