Royal Dutch Shell October 13, 2017 Royal Dutch Shell plc October 13, 2017 Re-shaping Shell, to create a world-class investment case Chemicals Investor Briefing John Abbott – Downstream Director Graham van’t Hoff – EVP Chemicals #makethefuture

Transcript

Royal Dutch Shell October 13, 2017

Royal Dutch Shell plcOctober 13, 2017

Re-shaping Shell, to create a world-class investment caseChemicals Investor BriefingJohn Abbott – Downstream DirectorGraham van’t Hoff – EVP Chemicals

#makethefuture

Royal Dutch Shell October 13, 2017

John AbbottDownstream DirectorRoyal Dutch Shell plc

Royal Dutch Shell October 13, 2017 3

Definitions & cautionary note

Reserves: Our use of the term “reserves” in this presentation means SEC proved oil and gas reserves.

Resources: Our use of the term “resources” in this presentation includes quantities of oil and gas not yet classified as SEC proved oil and gas reserves. Resources are consistent with the Society of Petroleum Engineers (SPE) 2P + 2C definitions.

Discovered and prospective resources: Our use of the term “discovered and prospective resources” are consistent with SPE 2P + 2C + 2U definitions.

Organic: Our use of the term Organic includes SEC proved oil and gas reserves excluding changes resulting from acquisitions, divestments and year-average pricing impact.

Shales: Our use of the term ‘shales’ refers to tight, shale and coal bed methane oil and gas acreage.

Underlying operating cost is defined as operating cost less identified items. A reconciliation can be found in the quarterly results announcement.

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate legal entities. In this release “Shell”, “Shell group” and “Royal Dutch Shell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this release refer to companies over which Royal Dutch Shell plc either directly or indirectly has control. Entities and unincorporated arrangements over which Shell has joint control are generally referred to as “joint ventures” and “joint operations” respectively. Entities over which Shell has significant influence but neither control nor joint control are referred to as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This release contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘goals’’, ‘‘intend’’, ‘‘may’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘plan’’, ‘‘probably’’, ‘‘project’’, ‘‘risks’’, “schedule”, ‘‘seek’’, ‘‘should’’, ‘‘target’’, ‘‘will’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this release, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including regulatory measures addressing climate change; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. No assurance is provided that future dividend payments will match or exceed previous dividend payments. All forward-looking statements contained in this release are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended December 31, 2016 (available at www.shell.com/investor and www.sec.gov ). These risk factors also expressly qualify all forward looking statements contained in this release and should be considered by the reader. Each forward-looking statement speaks only as of the date of this presentation, October 13, 2017. Neither Royal Dutch Shell plc nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this release.

With respect to operating costs synergies indicated, such savings and efficiencies in procurement spend include economies of scale, specification standardisation and operating efficiencies across operating, capital and raw material cost areas.

We may have used certain terms, such as resources, in this release that United States Securities and Exchange Commission (SEC) strictly prohibits us from including in our filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov.

Royal Dutch Shell October 13, 2017 4

Energy challenge

Source: UN Population Fund; UN World population Prospects (2015 revision); World Urbanisation Prospects (2014 revision); IEA, Energy Technology Perspectives 2015; Shell New Lens Scenarios

Growing populationGlobal population will increase from around 7.4 billion today to nearly 10 billion by 2050, with 67% living in cities

Rising demandGlobal energy demand will likely be almost 60% higher in 2060than today, with 2 billion vehicles on the road (800 million today)

Ongoing supplyRenewable energy could triple by 2050, but we will still need large amounts of oil and gas to provide the full range of energy products we need

Mitigating climate changeNet-zero emissions is a potentially achievable societal ambition

Growing global demand for energy as population and living standards increase

Royal Dutch Shell October 13, 2017

Strategy

“Let’s make the future” STRATEGIC

Focus portfolio on resilient positions

Invest in advantaged projects

Value chain integration

OPERATIONAL

Reset cost and capital spending

First class execution projects

and operations

Unrelenting focus on HSSE and

licence to operate

Leader: value + influence

Reducing our carbon

intensity

Shared value with

society

World-class investment case

FCF/share + ROCE growth

Conservative financial

management

5

Royal Dutch Shell October 13, 2017

Strong free cash flow and returns

Driving strategy in multiple time horizons

CONVENTIONALOIL + GAS

CHEMICALS

OIL PRODUCTS

DEEP WATERINTEGRATED GAS

SHALES NEW ENERGIES

Cash engines:today

Growth priorities: 2016+

Future opportunities: 2020+

Competitive + resilient

Funds dividends + balance sheet

FCF + ROACE pathway

Affordable growth in advantaged positions

Material value + upside

Managed exposure

Path to profitability

Cash engines 2020+

Relentless portfolio high-grading

6

Royal Dutch Shell October 13, 2017 7

Downstream Cash engine

Further strengthen our financial performance

Upgrading our portfolio

Returns + free cash flow improvement

Chemicals growth priority

Marketing Refining & Trading Chemicals

Growth priority

Differentiated products

Brand leverage + customer offer

Selective growth

Full integration with trading

Improve retained assets

Reducing refining capacity

Advantaged feedstock from

Upstream and refining

Strong product portfolio with

proprietary technology

Focused growth into

differentiated leading positions

Royal Dutch Shell October 13, 2017

Graham van‘t HoffExecutive Vice President - Chemicals

Royal Dutch Shell October 13, 2017 9

Agenda Chemicals demand

Position of Shell Chemicals within the industry

Shell Chemicals strategy

Execution

Financial performance

Growth projects

Q&A

01

02

03

04

05

06

07

Royal Dutch Shell October 13, 2017 10

Solar impulse:90% of the aircraft’s structure made from chemical technology

Royal Dutch Shell October 13, 2017 11

Chemicals

Growth priority

*Cracker base chemicals (Aromatic derivatives, Ethylene, Propylene and Isobutylene). Source: IHS/Shell analysis

Chemicals demand outlook

Shell produces key petrochemical building blocks

Limited impact of recycling Chemicals enabling CO2

reduction 0

100,000

200,000

300,000

400,000

500,000

2000 2005 2010 2015 2020 2025 2030

N. America S. America Europe Middle East Asia Others

Petrochemicals* demand in kT per annum

Asia 37%

Asia 52%

Royal Dutch Shell October 13, 2017 12

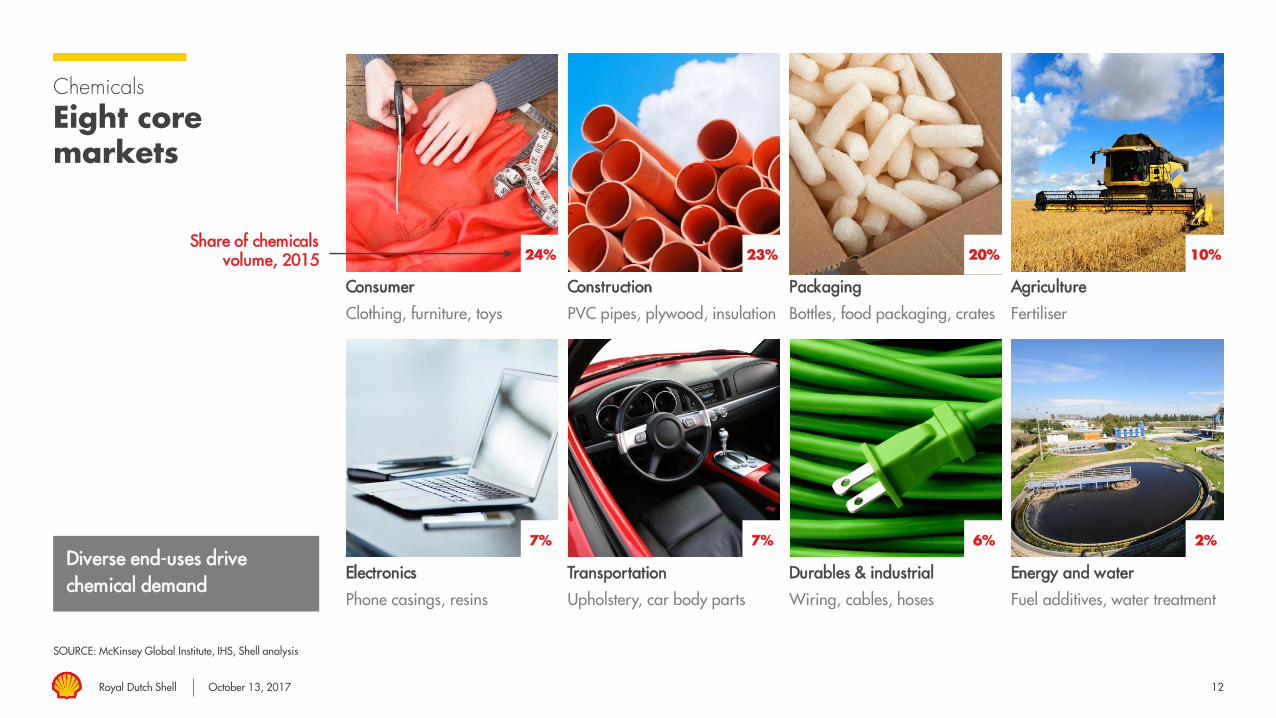

Chemicals

Eight core markets

SOURCE: McKinsey Global Institute, IHS, Shell analysis

Diverse end-uses drive chemical demand

Consumer

Clothing, furniture, toys

Construction

PVC pipes, plywood, insulation

Packaging

Bottles, food packaging, crates

Agriculture

Fertiliser

Electronics

Phone casings, resins

Transportation

Upholstery, car body parts

Durables & industrial

Wiring, cables, hoses

Energy and water

Fuel additives, water treatment

Share of chemicals volume, 2015 24% 23% 20% 10%

7% 7% 6% 2%

Royal Dutch Shell October 13, 2017

ChemicalsGrowth priority

Positioning in the competitive landscape

Access to advantaged feedstock

Process technologies

Big integrated sites

Large scale

Customised solutions

Product-materials innovation

Production close to markets

Medium scale sites

13

BASE CHEMICALS/ SOLUTIONSPERFORMANCE

Pure Chemical Companies

FEED

STO

CKS

CO

NSU

MER

S

INTERMEDIATES

Add Differentiation

Royal Dutch Shell October 13, 2017 14

Chemicals

Value chains

C2

C4

C6

C3

C1Ammonia

Methanol Acetic Acid / VAM

Urea

Ethylene

Propylene

Propylene Oxide

Acrylic Acid Super Absorbents

Butadiene

Butenes Solvents

Benzene

Phenol

Toluene

Xylene

TDI

Paraxylene

Polycarbonate

No Shell participation

Shell participation PTA

INTERMEDIATES

Agriculture

EO/MEG

Alpha olefins HODer Surfactants Consumer

Polyethylene

Polyester

Films

Containers

Packaging

Packaging

Polypropylene

Polyols Polyurethane foam Consumer

Styrene Polystyrene Moulded panels

Consumer

Construction

MDINBZ / aniline

Electronics

Elastomers Automotive

Fibres Consumer

NA

PHTH

A /

HEA

VY

LIQ

UID

S (O

IL) ET

HA

NE

LPGBI

O B

ASE

FEE

D

C8

BASE CHEMICALSFEEDSTOCKS PERFORMANCE END PRODUCTCONVERTER

MET

HA

NE

Royal Dutch Shell October 13, 2017

ChemicalsGrowth priority

Positioning in the competitive landscape

Competitors are actively acquiring or developing differentiation further down the value chains

Source: company reports, Shell analysis

15

FEED

STO

CK

PRODUCTS & MARKETS

Adv

anta

ged

Gen

eric

SolutionsBase Chem/Intermediates

Established Integrated Oil companies

Moving towards specialties

Low cost operatorsIn-market advantage

Active aggregation of technology and position

Royal Dutch Shell October 13, 2017

ChemicalsStrategy Advantaged

Feedstock First Class Footprint Strong Product & Customer Portfolio

Excellence Every Day & HSSE

Access Advantaged Feedstock Monetize With Competitive Advantage

Base chemicals cycles Feedstock portfolio has shifted to

advantaged feed and more gas

Key to robust profitability is keeping a balanced exposure to different regions, feedstocks, markets and therefore, margin sources

Indicative industry margins ($/mT)

67%

33%

53%47%

2007

2016

Liquid

Gas

1990 1996 2002 2008 2014

AdvantagedFeedstock First class footprint

Strong product & customer

portfolio

Excellence every day &

HSSE

Ethane cracker margin USGCNaphtha margin NEANaphtha margin WE

Feedstock disparity

Oil Gas Feed ParityOil Gas Feed Parity

Royal Dutch Shell October 13, 2017

Buenos Aires

Singapore

Scotford

Sarnia

Durban

19

Chemicals

Focused and balanced footprint

China in-market

Small Chemical activities at group refineriesAdvantaged gas feed siteIntegrated Chemical/refinery mega sites/clusters

US Gulf coast

FEP & Stanlow

Moerdijk, Pernis Nanhai

Rheinland

Shell-CNOOC JV –Petrochemical complex

Capacity* is regionally balanced

33

40

27

Portfolio consolidated from 133 locations in 1998 to 15 today

* Base Chemicals Capacity (C2+C3+bz); Portfolio includes Shell operated (12) and non-operated (3)

Americas

Europe

Asia

AdvantagedFeedstock

First class footprint

Strong product & customer

portfolio

Excellence every day &

HSSE

Deer ParkGeismarNorcoMobile

BukomJurong

Royal Dutch Shell October 13, 2017

Chemicals

Market-leading process technologies

Underpinned by high performance proprietary catalysis systems

Shell Chemicals proprietary technology

OMEGA (Monoethyleneglycol)

SMPO (Styrene Monomer/Propylene

Oxide/Polyols)

SHOP (Higher Olefins and Detergent Alcohols)

DPC/PC (Diphenyl carbonate)

Shell has been active in petrochemicals since 1929

Long history of product & technology development

~1,000 customers:

Annual product sales: >17 million tonnes

Long-term contracts and relationships with strong

partners

AdvantagedFeedstock

First class footprint

Strong product & customer

portfolio

Excellence every day &

HSSE

20

Royal Dutch Shell October 13, 2017 21

Chemicals

Operating and safety performance

Downtime as % of capacity

Chemicals plants – unplanned downtime

%

AdvantagedFeedstock

First class footprint

Strong product & customer

portfolio

Excellence every day &

HSSE

0

2

4

6

8

10

12

2012 2013 2014 2015 2016

Unplanned downtime without “big-hits” Unplanned downtime “big-hits” impact

Royal Dutch Shell October 13, 2017 22

Chemicals

Financial and competitive performance

Earnings and ROACE on CCS basis, excluding identified items; Shell ROACE calculations for 2012 has been restated for the impact of IAS 19; source: company reports, Shell analysis

$ billion

Earnings

%

0

5

10

15

20

25

30

13Q1 14Q1 15Q1 16Q1 17Q1

Competitive performance – ROACE 4Q rolling

Ensure robust performance under different market conditions and grow base business