SKYCITY Entertainment Group Limited Federal House 86 Federal Street PO Box 6443 Wellesley Street Auckland New Zealand Telephone +64 (0)9 363 6141 Facsimile +64 (0)9 363 6140 www.skycitygroup.co.nz 18 October 2013 Listed Company Relations NZX Limited Level 2, NZX Centre 11 Cable Street WELLINGTON RE: SKYCITY ENTERTAINMENT GROUP LIMITED (SKC) ANNUAL MEETING OF SHAREHOLDERS Please find attached the following prepared announcements that will be delivered at the company’s annual meeting of shareholders to be held at 10.00am today: (a) Chairman’s Address; and (b) Chief Executive Officer’s Presentation. Copies of these announcements will be available from SKYCITY’s website later today. Yours faithfully Peter Treacy Company Secretary

Transcript

SKYCITY Entertainment Group Limited Federal House 86 Federal Street PO Box 6443 Wellesley Street Auckland New Zealand

18 October 2013 Listed Company Relations NZX Limited Level 2, NZX Centre 11 Cable Street WELLINGTON RE: SKYCITY ENTERTAINMENT GROUP LIMITED (SKC)

ANNUAL MEETING OF SHAREHOLDERS Please find attached the following prepared announcements that will be delivered at the company’s annual meeting of shareholders to be held at 10.00am today: (a) Chairman’s Address; and (b) Chief Executive Officer’s Presentation. Copies of these announcements will be available from SKYCITY’s website later today. Yours faithfully Peter Treacy Company Secretary

Chairman’s Address: Chris Moller Moving now to my chairman’s address for 2013. It is my pleasure to review SKYCITY’s annual result with you, our shareholders and capital note holders, as Chairman for the first time. I am certainly appreciative of the fact that I took up the role of Chairman having already served on the Board for 4 years because, ladies and gentlemen, 2012/13 has been a very busy year in this Company’s proud history. If you are a believer in “to do” lists, as I am, then this was a year in which a number of significant tasks, or more accurately, milestones were knocked off. And the Board is in no doubt that those initiatives have set SKYCITY up for the future. We successfully consolidated our long-term partnerships with governments on both sides of the Tasman by negotiating agreements for our two major projects in Auckland and Adelaide. After years of negotiations, we sold our interest in the Christchurch Casino to Skyline and in exchange purchased the remaining 40 percent share in the Queenstown Casino from them that we did not already own. We also acquired the Wharf Casino in Queenstown from Lasseters meaning that we now have a consolidated and integrated presence in one of New Zealand’s iconic tourism destinations. In Darwin we opened our new 40 million Australian dollar Lagoon resort, which this month won the “Best Redeveloped Hotel” award in the Australian Hotel Association’s National Awards for Excellence. And our International Business performed strongly, with turnover growing from 4.4 billion dollars to 5.7 billion dollars, an increase of 29%, proving that the investments that we have made in that business over the past few years were appropriately founded and well timed.

2012/13 was a year in which we did a lot and yet, putting aside the strong returns from Rugby World Cup 2011 in the previous year, the intensity of planning for tomorrow did not distract the business from continuing to deliver good results for shareholders this year. It is no mean feat to meet expectations in the present whilst, at the same time, readying the business for what the Board believes will prove to be generational changes for the future. And yet if you look at most of the financial metrics we report on, that has been achieved. Granted, reported net profit after tax was down on last year. But there were a number of mitigating factors. As I said, we didn’t have the benefit of the Rugby World Cup 2011 this year. Selling our interest in Christchurch Casino meant that the net profit after tax generated by that business was not included in our second half results. And the Australian dollar lost ground this year, which all but offset the strong operating performance gains we made across the Tasman, particularly in Darwin, when the results were converted to New Zealand dollars. Nevertheless, our base business remains strong. And perhaps the best indicator of that is that if the result is adjusted for these three factors, normalised net profit after tax for the year would have increased by 2.6 percent. This is not to ponder on what might have been but rather to endeavour to assure you that we are working hard to achieve earnings growth at the same time as we future proof and reposition the business. The upward revision of our dividend policy, the reactivation of the Dividend Reinvestment Plan and this year’s total payout of 20 cents per share in dividends

are clear signals that we are committed to delivering shareholders competitive returns. Also, over the last financial year, the SKYCITY share price reached new 5 years highs of 4 dollars 50 in New Zealand and 3 dollars 80 in Australia. As Rod McGeoch observed last year in his address to you, the assets that we developed for the Rugby World Cup have continued to draw in the crowds. And those attractions are now generating new opportunities. We are committed to the cities we are part of. And that commitment expresses itself in long term plans and in ideas that are sometimes years ahead of their time. Here in Auckland we have continued to develop Federal Street as the culinary destination centre of the city. Cast your mind back just a few years and the area was little more than a right-of-way. Today, we have world-class chefs offering amazing and diverse food at everything from street level to more than 50 stories up. That in turn has dramatically changed the profile of visitors to the area. And those influxes of diners, players and visitors are generating new jobs and new business for us and for others. With the New Zealand International Convention Centre, we will have the opportunity to further consolidate and add to the attractiveness of both our front and back yards. That investment will significantly increase the foot traffic year round, bringing the critical mass we need to endorse the SKYCITY precinct as the city’s entertainment hub. And it will stimulate economic growth in Auckland and across New Zealand.

It will also enable us to compete meaningfully for a share of the world’s large-scale conferences, exhibitions and events. Our investments in Queenstown are of a much smaller scale but they are equally focused on our future. Having venues in Queenstown enables us, not just to align our VIP offerings nationally, but also to offer distinctly New Zealand gaming experiences to our high roller visitors with experiences such as wineries, skiing, golf, fishing and adventure sports that they simply cannot get in Macau, Singapore or Australia. Again, our reinvigorated presence in Queenstown will serve ourselves and the economy well. It is good for local operators, for Queenstown’s own regional economy and for the country because it gives lucrative tourism visitors great reasons to come to New Zealand and to stay longer. Across the Tasman, the city of Adelaide is on the cusp of an extraordinary transformation. And again, through careful planning, we are at the epicentre of the transformation as five billion dollars is spent around us on developments along the Torrens River bank and the Adelaide Oval that will redefine and rejuvenate the inner city. Our proposed new 6-star boutique hotel, VIP gaming and signature restaurants will, in similar manner to Auckland, put our distinctive stamp on an integrated entertainment complex that both Adelaide and you, our shareholders, will be truly proud of. These investments are big calls, ladies and gentlemen. But the casino industry is a highly competitive business where customers are competed for globally.

And, in truth, most initiatives that seek to secure and grow the future of the business appear challenging at first. Our investments in Darwin and in our International Business may well have appeared ambitious to some at the time. And yet now, the feedback we are getting from that resort, from the awards we are winning and the strong growth that we continue to enjoy in our International Business, show that well-timed, focussed investments based on customer need and clear differentiation from competing offerings will generate attractive earnings streams. Our successes in procuring the agreements in Auckland and Adelaide this year are testament to the fact that, not only do we have a crucial role to play in the redevelopment and marketing of cities, but that we have the trust and the confidence of governments. As I have said, we want to grow the cities we are part of. And we will do so with gusto providing that you, our shareholders, are rewarded with the prospect of satisfactory returns. However no business can afford to downplay or ignore its social responsibilities. It too is a crucial part of our commitment to the places we do business in. It is also critical to maintaining strong and healthy relationships with government. As an entertainment provider, we are scrutinised more harshly than most regarding our commitment to care for our customers, employees and communities. Our Corporate Social Responsibility programme and our commitment to care is how we earn our social licence to operate. I cannot emphasise strongly enough how seriously this matter is taken by both the Board and SKYCITY management.

Indeed we have a Corporate Social Responsibility Committee, chaired by Director Peter Cullinane, which reports directly to the Board. We have also worked steadfastly, since our inception 19 years ago, to develop a host responsibility programme that leads the world. And, despite the naysayers, we are very proud of it and what it has achieved. This is of course my first opportunity as Chairman to thank Nigel Morrison and his Executive Management team for the good work that they do. Once again, Nigel has led the company through a year where much needed to be achieved and resolved. Indeed, not to put too fine a point on it, Nigel and the team, have in my opinion, nailed it. The challenges of getting the Auckland and Adelaide projects across the line with satisfactory potential returns for shareholders and resolving the Christchurch and Queenstown ownership issues should not be underestimated. And Nigel and the team deserve great credit for these accomplishments. On behalf of the Board I would also like to thank and acknowledge all the staff, who work tirelessly right across our business every day to entertain and serve our customers. I also wish to thank my fellow Directors for their acumen and dedication in steering us through a very full 12 months. As we look ahead, the pace shows no signs of slowing and the challenges of achieving growth have not diminished. We will continue to look for ways to secure our future and to gain efficiencies where we can. We will invest in our offerings to maximise competitiveness and returns.

And we will embark on designing and planning bold new ventures here in Auckland and in Adelaide with our government partners, without losing focus on our existing core businesses. As we do so, we will do everything we can to deliver you acceptable returns.

18/10/2013

1

SKYCITYEntertainmentGroup Limited

Annual Meeting18 October 2013

Chi f E i ’ Chief Executive’s Annual Meeting Address 18 October 2013

For illustrative purposes, converting Normalised NPAT to A$, FY13 Normalised NPAT would be A$119.2m vs FY12 A$108.5m, up 9.9%For illustrative purposes, converting Annual Dividend cps to A$, FY13 AUD17.5 cps vs FY12 AUD13.0 cps up 34.6%NZD/AUD cross‐rate ‐ FY13 converted at the 13th August 2013 rate of 0.8746 and FY12 converted at the 15th August 2012 rate of 0.7675

Revenue and EBITDA growth of 13.2% and 9.5% respectively in Darwin, following the opening of Lagoon Resort and Horizon Villas

IB Revenues grew from A$0.3m in FY12 to A$7.5m in FY13

Adelaide maintained a focus on costs and increased normalised EBITDA margin to 23 6% (FY12: 22 8%)

FY13 Result Overview – Highlights

Adelaide maintained a focus on costs and increased normalised EBITDA margin to 23.6% (FY12: 22.8%)

Auckland had reasonable revenue growth in:

F&B Revenues (+5.0%, excl RWC impact) from success of Federal Street

Hotels and Conventions, with revenue growth of 10.7% in 2H13

Tables Revenue growth in Auckland (+3.4%)

Group International Business performed well, with 29.5% turnover growth for the year, to $5.7 billion

S i f 6 i G i ( G l i $ ) l i i ll

6

Strong win rate of 1.64% in Group IB in 2H13 (2H13 Group Actual win $45.9m) resulting in overall win rate at theoretical for the full year (1.35%)

In Auckland: IB gaming revenues now represent around 15% of total gaming revenues, compared to 5% in FY10

2H13 win rate of 1.9% resulted in Actual win of $36.9m, being some $10m in excess of the theoretical win, and 100% higher than Actual win in 2H12 ($18.3m)

18/10/2013

4

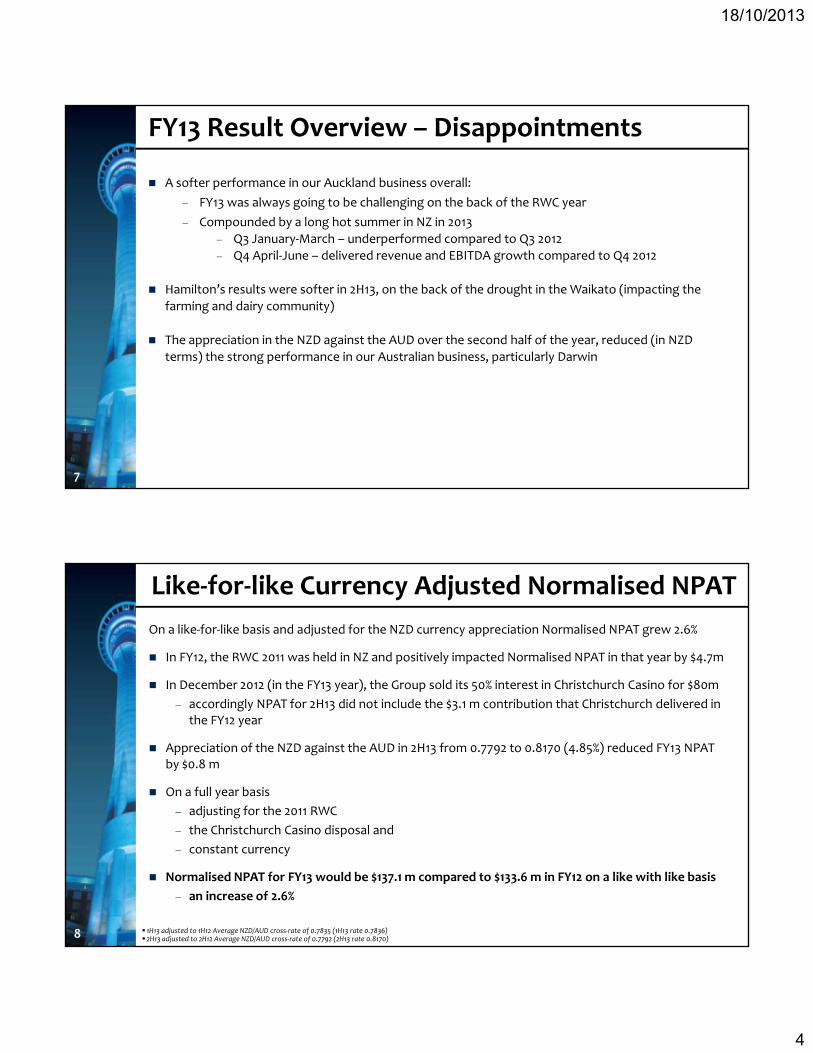

A softer performance in our Auckland business overall:

FY13 was always going to be challenging on the back of the RWC year

Compounded by a long hot summer in NZ in 2013

FY13 Result Overview – Disappointments

Q3 January‐March – underperformed compared to Q3 2012

Q4 April‐June – delivered revenue and EBITDA growth compared to Q4 2012

Hamilton’s results were softer in 2H13, on the back of the drought in the Waikato (impacting the

farming and dairy community)

The appreciation in the NZD against the AUD over the second half of the year, reduced (in NZD

terms) the strong performance in our Australian business, particularly Darwin

7

) g p , p y

On a like‐for‐like basis and adjusted for the NZD currency appreciation Normalised NPAT grew 2.6%

In FY12, the RWC 2011 was held in NZ and positively impacted Normalised NPAT in that year by $4.7m

In December 2012 (in the FY13 year), the Group sold its 50% interest in Christchurch Casino for $80m

Like‐for‐like Currency Adjusted Normalised NPAT

( 3 y ), p 5

accordingly NPAT for 2H13 did not include the $3.1 m contribution that Christchurch delivered in the FY12 year

Appreciation of the NZD against the AUD in 2H13 from 0.7792 to 0.8170 (4.85%) reduced FY13 NPAT by $0.8 m

On a full year basis

adjusting for the 2011 RWC

8 1H13 adjusted to 1H12 Average NZD/AUD cross‐rate of 0.7835 (1H13 rate 0.7836) 2H13 adjusted to 2H12 Average NZD/AUD cross‐rate of 0.7792 (2H13 rate 0.8170)

the Christchurch Casino disposal and

constant currency

Normalised NPAT for FY13 would be $137.1 m compared to $133.6 m in FY12 on a like with like basis

an increase of 2.6%

18/10/2013

5

FY13 FY12 Movement

Interim 10.0 cps 9.0 cps 1.0 cps 11.1%

Final 10.0 cps 8.0 cps 2.0 cps 25.0%

Total Dividends 20.0 cps 17.0 cps 3.0 cps 17.6%

Increased Dividends

The final dividend of 10.0 cents per share increases the total dividend for the full year to 20.0 cents per share. This represents a 3.0 cps increase on FY12 (+17.6%)

The final dividend of 10 cents per share represents a 25% increase on the FY12 final dividend of 8 cents

based on a share price of $4.10, this is an annual gross dividend yield of 6.3% to NZ shareholders

The dividend is calculated in accordance with the previously announced policy of:

an annual dividend of not less than 20 cents per share and

9

an annual dividend of not less than 20 cents per share, and

a dividend payout representing not less than 80% of Annual Normalised NPAT

The Dividend Reinvestment Plan was re‐activated for the FY13 final dividend without any discount. This was taken up by shareholders holding 21% of the shares in the company

SKYCITY is committed to retaining this dividend policy for shareholders, subject to maintaining our investment grade credit rating and giving priority to funding major strategic projects

Agreement with the New Zealand Government on the $402 million New Zealand International Convention Centre (“NZICC”)

Licence certainty to 2048

Tax certainty expansion regulatory concessions

Other Key Highlights in 2013

Tax certainty, expansion, regulatory concessions

Agreement with the South Australian Government

Licence exclusivity until 2035

Tax certainty, expansion, regulatory concessions

Christchurch Disposal

Sold 50% stake in Christchurch Casino for $80m

10

Sold 50% stake in Christchurch Casino for $80m

Queenstown acquisitions

Acquired remaining 40% stake in SKYCITY Queenstown for $5m

Wharf Casino acquired from Lassetters for $5m

18/10/2013

6

T l Sh h ld Total Shareholder Return (TSR)

11

Total Gross Performance Relative to NZX‐50Last 2 Years

50%

60%

+44%

10%

20%

30%

40%

Total R

eturn +33%

12

-10%

0%

SKYCITY (NZX listing) NZX50

Data as at 11 Oct‐13. Assumes dividends are reinvested in equivalent amount of shares as at the ex‐dividend date. Rebased to SKC at the beginning of the periodSource: Capital IQ

18/10/2013

7

Total Gross Performance Relative to ASX‐200Last 2 Years

50%

60%

+49%

10%

20%

30%

40%

Total R

eturn

+36%

13

-10%

0%

SKYCITY (ASX Listing) ASX200

Data as at 11 Oct‐13. Assumes dividends are reinvested in equivalent amount of shares as at the ex‐dividend date. Rebased to SKC at the beginning of the period Source: Capital IQ

K A hiKey Achievements‐ NZICC Agreement‐ Adelaide Agreements

14

18/10/2013

8

Signed the $402m NZICC Agreement with the NZ Government on 5 July 2013 – subject to the enabling legislation passing through Parliament – expected this calendar year

This follows extensive public scrutiny and consultation:

Auditor‐General report on Government’s bid process – cleared

The NZICC Agreement and Next Steps

Auditor‐General report on Government s bid process – cleared

Select committee process including public hearings

Parliamentary debate and questions to Ministers

Architect, design and other consultant appointments are well advanced – will be announced after legislation passing

Focus for 2014 will be:

proposed designs for consultation

15

proposed designs for consultation

building works contract let

2015 – construction starts – creation of 1,000 jobs

Target completion date: September 2017

Full details of the NZICC Agreement were announced on 6 July 2013

SKYCITY will invest A$350m to transform the Adelaide Casino into a world‐class integrated

entertainment complex as part of the new entertainment precinct on the banks of the River

Torrens

The Adelaide Transformation

Will include:

Adelaide’s first 6 star boutique hotel

celebrity and signature restaurants

high‐quality local and interstate premium gaming rooms

world‐class VIP gaming experiences with ‘Horizon’ international suites with adjoining private

gaming salons

16

SKYCITY’s investment will create much needed jobs and economic growth for South Australia

and complement the redeveloped Adelaide Oval and the new and expanded Adelaide

Convention Centre

18/10/2013

9

Following the agreement reached with SA Government on December 2012 and the subsequent

passing of the enabling legislation in August 2013, final agreements were signed last Friday in

Adelaide with the Premier Hon. Jay Weatherill and Deputy Premier Hon. John Rau, (new Approved

Licensing Agreement and a new Casino Duty Agreement)

What Adelaide Agreement means for SKYCITY

These create certainty and capacity for SKYCITY to compete and grow:

extension of exclusive SA licence for a further 20 years out to 2035

of which 15 may be convertible to automated table games (300 stations)

ticket in ticket out (TITO) in Premium gaming rooms

card based cashless gaming throughout

This enables us to compete against our peers in Australia for the first time on a level playing field attracting the interstate and international markets

SKYCITY’s new Adelaide Development

18 Artists impression

18/10/2013

10

Net debt at 30 September 2013 is $598m. Available committed, undrawn bank facilities total $380m

Extension of the $200m syndicated bank facility from June 2016 to October 2018

At 30 September 2013, average debt maturity is 4.5 years (similar levels to 30 September 2012)

f f f

Well Funded for Future Growth

Currently only $56m of the $150m Capital Notes are issued, leaving $94m in Treasury Stock for future issue

SKYCITY holds a Standard and Poor’s Investment grade rating of BBB‐ (Stable outlook)

Existing available funding facilities total $474m (being undrawn bank facilities and Treasury Stock)

19

H R ibiliHost Responsibility

20

18/10/2013

11

SKYCITY is committed to providing a safe environment for anyone who comes to work, stay or be

entertained at SKYCITY

The SKYCITY Board and Senior Management take our host responsibility obligations very seriously.

P t C lli h i C t S i l R ibilit B d b itt

SKYCITY’s Host Responsibility

Peter Cullinane chairs our Corporate Social Responsibility Board sub‐committee

SKYCITY Auckland has the most comprehensive host responsibility programme in NZ and it is

considered world‐leading by experts

We spend more than $5m annually in Auckland on customer care and host responsibility

It is central to what we do every day and we invest significant resources into ensuring our

venues are as safe as possible for all our customers

21

venues are as safe as possible for all our customers

Latest Ministry of Health research shows the prevalence rate for problem gambling has declined

from 0.4 per cent to 0.3 per cent of the population compared to:

smoking at 20 per cent, and

hazardous drinking at nearly 18 per cent

The Facts

g y p

Department of Internal Affairs figures show as at 30 June 2013, New Zealand had a total of 20,360

gaming machines:

17,534, or 86 per cent, of these are in these in pubs and clubs across New Zealand

only 2,826 or 14 per cent were located in casinos

Latest Ministry of Health intervention client data shows that the majority of problem gambling

22

related presentations to counselling agencies relate to the following:

56% gaming machines in pub and club gambling venues

12% lotteries

9% racing

8% casino gaming machines across New Zealand

18/10/2013

12

“Collectively the responsible gambling measures provided in both Australia and New Zealand are more rigorous than anything offered in the United States, The United Kingdom and Asia”. “SKYCITY’s programme would be considered of a higher standard than what is offered in other casinos in Australia”.

SKYCITY is World Leading – Expert opinions

Associate Professor Dr Paul Delfabbro, University of Adelaide

Submission to New Zealand Gambling Commission 2013

“Dr Delfabbro’s report makes it clear that New Zealand is leading the world in this area and both the current HRP and revised HRP approved in this decision are products of an evaluation process which is thorough and independent”.

New Zealand Gambling Commission, GC21/13, 2013

23

“No other casino in the world has introduced facial recognition technology, electronic monitoring and ‘pre‐commitment’ to time and/or expenditure limits together. It is ground‐breaking and could raise the bar across all gambling settings and forms”.

Professor Max Abbott, AUT University, Media Release 25‐06‐2013

The new host responsibility initiatives being introduced by

SKYCITY, under the NZICC Agreement include:

doubling the number of full‐time Host Responsibility staff

in Auckland, providing dedicated Host Responsibility staff

New Host Responsibility Measures

, p g p y

onsite at all times, 24/7

introducing predictive modelling technology which

analyses player data to help identify customers most at

risk from gambling harm

continuing to roll out SKYCITY’s Pre‐commitment

Programme allowing every gaming machine customer to

set both the time and the amount they wish to spend over

24

y p

a given period

trial the use of further measures, including facial

recognition technology, to identify and prevent barred

problem gamblers from gaining entry to the Auckland

casino

Artists impression

18/10/2013

13

SKYCITY d h SKYCITY and the Community

25

SKYCITY is a major contributor to the local and national

economies and New Zealand and Australian Tourism

We employ more than 6,500 employees across New Zealand

and Australia

SKYCITY’s Economic and Tourism Contribution

and Australia

Our 4,000 New Zealand staff earn salaries and wages of

approximately $150m each year

The largest private sector employer in the Auckland CBD,

employing 3,500 Aucklanders

Taxes payable of over $160m to central government in FY13

26

The biggest ratepayer in the Auckland CBD – $4.3m for FY13

Bringing new award winning restaurants to Auckland – The Grill,

The Depot – and now The Sugar Club, The Federal Deli, Masu

Our International Business earned Tourism Export Income for

New Zealand this year of $55.0m up from $16.5m 3 years ago

18/10/2013

14

In addition to the SKYCITY Community Trusts funding in

Auckland, Hamilton and Queenstown which has provided

more than $37.2m in funding to thousands of community

groups and programmes, we also directly provide support to

SKYCITY – Key Charity Partnerships

g p p g y p pp

a range of key charities, including:

Variety the Children’s Charity – new Variety of Chefs

event

Leukaemia Blood Cancer NZ – raised $800,000 this year

through fundraising events at SKYCITY

Kidz First Children’s Hospital – Christmas Party

27

Prostate Cancer Foundation

NZ Breast Cancer Foundation

Auckland RSA – Poppy Partnership – new for 2013

A Focus on Trans‐Tasman Competitions

SKYCITY Breakers – three peat champions 2012/13 –

renewed sponsorship for a further 3 more years

SKYCITY – Key Community Sponsorships

Vodafone Warriors – renewed sponsorship for a

further 2 more years

X Factor NZ – highest rating programme in TV3 history –

1 million+ viewers each show

2013 Adelaide Casino Adelaide Cup

28

18/10/2013

15

O h A hi Other Achievements and Developments

29

SKYCITY Grand Hotel has won 2 significant industry

awards:

World Travel Awards 2013 New Zealand’s Leading

Business Hotel

SKYCITY Grand Hotel – Awards & Refurbishment

Business Hotel

Trip Advisor – Certificate of Excellence 2013

SKYCITY Grand Hotel refurbishment of Premium Luxury

Rooms underway

first 5 floors to be completed mid‐April

30

18/10/2013

16

Our Federal St Dining Precinct continues to be successful:

The Grill by Sean Connolly – two chef’s hats at Cuisine Magazine’s Good Food Awards 2013

Depot – awarded Metro magazine’s Best Casual Bistro

Federal Street Dining Precinct

Depot – awarded Metro magazine s Best Casual Bistro 2013, won one chef’s hat at Cuisine Magazine’s Good Food Awards 2013

Three new restaurants opened with celebrity chefs in past 3 months

Federal Street shared space – $10m co‐investment with A kl d C il

31

Auckland Council

The Sugar Club – opened August 2013

32

18/10/2013

17

Federal Delicatessen – opened September 2013

33

Masu – opened October 2013

34

18/10/2013

18

SKYCITY Darwin’s Lagoon Resort won

Australia’s Best Redeveloped Hotel in

SKYCITY Darwin

Australian Hotels Association (AHA)

Awards for Excellence 2013

35

T di d Trading and Operations Update

36

18/10/2013

19

New Zealand

Auckland revenues of $145.9m are up 3.8% ($5.3m), due to: modest growth in core local gaming revenues, non‐gaming revenues being flat, but continued strong

International Business revenue growth

The softness experienced in 2H13 in Hamilton has continued into 1H14, with revenues down $2.4m

Year to Date Trading – Overview

p 3 4, $ 4

Queenstown has started the year strongly, both in local and International Business revenues, up over 70%

Total NZ Revenues of $165.2m are up 2.9% ($4.7m), reflecting the Auckland result as above

Australia

Total Australian revenues of A$90.3m are flat on prior year, with growth in Darwin being offset by some softness in Adelaide

Darwin continues to benefit from investment in the Lagoon Resort and improved gaming facilities

Adelaide visitation is soft compared to prior year, as a number of the main railway lines at the train station

37

adjacent to the property remain closed for electrification – expect to re‐open by December 2013

Group Overall

For the period 1 July 2013 to 13 October 2013, Group Normalised Revenues on a constant currency basis are up 1.7% from $276.5m to $281.2m however, taking the significant $12.5m movement in NZ$/A$ (0.78 to 0.87) into account

Normalised Revenues at actual currency are down 2.8%, from $276.5m to $268.7m

YTD Group Revenue to 13th October (incl Gaming GST)

New Zealand Casinos

■ Auckland 145.9 140.6 5.3 3.8%

■ Hamilton 14.7 17.2 (2.4) (14.2%)

FY14 FY131 Jul - 13 Oct Movement

1 Jul - 13 Oct 1 Jul - 13 Oct

$m $m $m %

■ Queenstown 4.2 2.4 1.9 78.4%

■ Other 0.4 0.3 0.0 4.8%

Total New Zealand 165.2 160.5 4.7 2.9%

Australian Casinos

■ Adelaide (A$) 46.6 48.4 (1.8) (3.7%)

■ Darwin (A$) 43.7 41.9 1.8 4.3%

Total Australia (A$) 90.3 90.3 0.0 0.0%

Total Australia at LY fx rate 0.7809 (NZ$) 116.0 116.0 0.0 0.0%

Normalised Revenue at constant currency (NZ$) 281.2 276.5 4.7 1.7%

38 In constant currency section FY14 1 Jul – 13 Oct adjusted to LY fx rate of 0.7809 Current actual YTD FY14 fx rate of 0.8720

Exchange rate impact at CY fx rate 0.8720 (12.5) (12.5)

Normalised Revenue at actual currency (NZ$) 268.7 276.5 (7.8) (2.8%)

Adjust International Business to actual win rate 3.3 (11.3) 14.6

Christchurch - 1.8 (1.8)

Reported Revenue at actual currency (NZ$) 271.9 267.0 5.0 1.9%

Normalised Revenue in AUD at actual currency (A$) 234.2 215.3 18.8 8.7%

18/10/2013

20

F d O l k Focus and Outlook for FY14

39

New Zealand

Focus on growing Auckland’s hospitality, tourism and gaming business through revenue initiatives and improved cost management

Continue to grow our International gaming Business, both VIP tables and EGMs

Awaiting Parliament’s decision on the NZICC Bill anticipated by December 2013 Appoint design and project

Focus for FY14

Awaiting Parliament s decision on the NZICC Bill, anticipated by December 2013. Appoint design and project management teams, progress design works

Australia

Adelaide – with the passing of the enabling legislation in July, and having now executed the new ALA and CDA agreements with the SA Government, commence interim capex works to activate VIP product and tax rate concessions in the second half of FY2014

Darwin – continue to drive revenue growth from new gaming, hotel and conventions/events facilities

40

International Business

With our new Executive VP International, Craig Ashton, continue to grow International Business in Auckland, further activate “Horizon” in Queenstown and drive growth in our new “Horizon” Salons in Darwin

Other

Continue to stay abreast of regional casino developments and opportunities that may lead to shareholder accretive opportunities and transactions

18/10/2013

21

Management expects to continue to deliver revenue growth in the underlying business

Currently, the most significant factors that will continue to impact the FY14 result are:

negative foreign currency translation effect of the strong NZD versus AUD: currently NZ$/A$ 0 882 versus 0 800 in FY13 (a 10 25% negative impact on AUD earnings

Outlook for FY14

currently NZ$/A$ 0.882, versus 0.800 in FY13 (a 10.25% negative impact on AUD earnings translated into NZD)

macro economic conditions in New Zealand, which are showing some (but not consistent) positive signs

continued challenging economic conditions in Australia, in particular in South Australia

Adelaide Casino trading improvement once the agreed reforms become effective in 2H14 –now likely to have minimal EBITDA impact in FY14 due to timing of reforms, capex and new systems implementation

41

ongoing positive momentum and growth in the International Business

Management will release 1H14 results on 12 February 2014, at which time further guidance on the FY14 result will be provided

All information included in this presentation is provided as at 18 October 2013.

Reconciliation of Reported Revenue to Normalised Revenue

Gaming Revenue figures reflect gaming win (inclusive of gaming GST). This facilitates Australasian comparisons and is consistent with the treatment adopted by major Australian casinos

Disclaimer

Non‐gaming Revenues are net of GST

Total Revenues are gaming win plus Non‐gaming Revenues

Reported revenue reflects actual International Business win rate while normalised revenue shows International Business at the theoretical win rate of 1.35%.

Normalisation adjustments have been calculated in a consistent manner with prior periods.

The presentation includes a number of forward‐looking statements. Forward looking statements, by their nature, involve inherent risks and uncertainties. Many of those risks and uncertainties are matters which are beyond SKYCITY’s control and could cause actual results to differ from those predicted. Variations could either be materially positive or materially

42

ff f p y p ynegative.

This presentation has not taken into account any particular investor’s investment objectives or other circumstances. Investors are encouraged to make an independent assessment of SKYCITY.