RealOptionsDecisionFrameworkforResearchandDevelopment:ACaseStudyonaSmall

CanadianHigh-TechnologyStart-Up

by

SallyJamalMattar

Thisthesisissubmittedinpartialfulfillmentoftherequirementsforthedegreeof

MasterofScience

in

EngineeringManagement

DepartmentofMechanicalEngineeringUniversityofAlberta

©SallyMattar,2017

ii

Abstract

ResearchandDevelopment(R&D)projectscanbeboth innovativeandhighlyuncertain.Allowing

for managerial flexibility and adopting real options methods and incorporating technology

readiness level scales to assess the maturity of technologies progressing through development

stages,canhelpmanagershedgetheunforeseenrisksthatariseduringthesestages.Managerscan

makedecisionsthatavoidthedownsideandcapturetheupsideoftheserisks.Thismethodologyis

adecision-making framework forresearchorganizations,wherepotentialvaluesofdecisionsand

projects across aportfolio canbe evaluated.Theproposed framework analyzes the risks as they

progressthroughthetechnologyreadinesslevelscale,andenablesR&Dmanagementtoplayactive

roles in project evaluations and justify continued spending on risky, long term projects that are

expectedtobeofhighfuturevalue,anareawheretraditionalvaluationmethodsfallshort.Acase

studyon a small Canadian technology start-up is used todiscuss the importanceof adopting the

proposedmethodology.

iii

Preface

ThisthesisisoriginalworkbySallyMattar.Thecasestudy,whichispartofChapter4ofthethesis

received research ethics approval from the University of Alberta Research Ethics Board, Project

Name“Realoptionsanalysisapplication”,Pro0073487,July20,2017.Thisworkwasnotpublished

anywhereelseanddoesnotcontaincollaborativework.

iv

Acknowledgements

IwouldliketothankmysupervisorDr.LipsettforgivingmetheopportunitytocompleteaMasters

inEngineeringManagement.Iamgratefulforallhissupportandguidancethroughoutthecourseof

mydegreeandIhaveenjoyedworkingwithhimimmensely.Itwasalwaysapleasuretochatwith

himandhealwayshadsomethingintelligentandinterestingtosay.Hewasacontinuoussupport

andwithouthim,thisprojectcouldnothavebeencompleted.

Iwould also like to thankDr. Lianne Lefsrud. Ever since taking her class in the Fall semester of

2016,shehasbeenaninspirationandrolemodel,andIaspiretobe likeheroneday.Shealways

offered support and gave valuable advice when needed. She also provided guidance on the

structureandorganizationofthisthesisandIamverygratefulforallherhelp.

v

TableofContents

Abstract.....................................................................................................................................................................................iiPreface......................................................................................................................................................................................iiiAcknowledgements.............................................................................................................................................................ivTableofContents..................................................................................................................................................................vListofFigures.....................................................................................................................................................................viiiListofTables..........................................................................................................................................................................ixChapter1Introduction.......................................................................................................................................................11.1ThesisMotivation&BusinessCase.......................................................................................................................11.2ObjectiveofThesis........................................................................................................................................................21.3ThesisStructure.............................................................................................................................................................4Chapter2ReviewoftheLiterature...............................................................................................................................52.1R&DandTechnologyDevelopment......................................................................................................................52.1.1R&DandTechnologyDevelopment...................................................................................................................62.1.2ExamplesofTechnologyDevelopmentModels.........................................................................................102.1.3TechnologyPush–MarketPull........................................................................................................................132.1.4CapabilitiesofaFirm............................................................................................................................................142.2TechnologicalMaturity............................................................................................................................................142.2.1TechnologyReadinessLevelsOverview.......................................................................................................142.2.2TRLs:CharacteristicsatEachLevel................................................................................................................162.2.3OtherTRAToolsandTechniques....................................................................................................................222.2.4LimitationsofTRLs................................................................................................................................................232.3TechnologyRiskManagement..............................................................................................................................242.3.1RisksinR&D&TechnologyDevelopment...................................................................................................242.3.2RiskManagementinR&D...................................................................................................................................302.3.3RiskManagementTools&Techniques.........................................................................................................312.4FinancialValuationMethods.................................................................................................................................332.4.1TraditionalValuationMethods.........................................................................................................................332.4.2FinancialOptionsTheoryOverview...............................................................................................................362.4.3Black-ScholesModel..............................................................................................................................................372.4.4BinomialModel........................................................................................................................................................382.5RealOptionsValuation.............................................................................................................................................412.5.1IntroductiontoRealOptions:ValueasaDecision-MakingTool........................................................41

vi

2.5.2RealOptionsValuation:FinancialOptionsvs.RealOptions................................................................432.5.3TypesofRealOptions...........................................................................................................................................452.6RealOptionsAnalysis...............................................................................................................................................482.6.1ApplyingRealOptions:TheSteps....................................................................................................................482.6.2Monte-CarloSimulations.....................................................................................................................................502.6.3RealOptionsinIndustry......................................................................................................................................51Chapter3DevelopmentoftheROADecisionFramework...............................................................................543.1FrameworkMethodology.......................................................................................................................................543.2Phase1:CollectionofData&InitialPlanning................................................................................................563.3Phase2:TechDevelopmentStages-gates&TRLAssessment................................................................573.4RisksinTechnologyDevelopment......................................................................................................................623.5Phase3:RealOptionsAnalysis.............................................................................................................................693.5.1Base-CaseDiscountedCashFlow&SensitivityAnalysis......................................................................693.5.2Monte-CarloSimulation.......................................................................................................................................703.5.3RealOptionsProblemFraming&OptionValuation................................................................................72Chapter4ApplicationtoCaseStudy:CopperstoneTechnologies................................................................764.1Phase1:DataCollection&Background...........................................................................................................764.1.1CompanyBackground:CopperstoneTechnologies.................................................................................774.1.2InterviewwithBusinessDevelopmentManager......................................................................................784.1.3InformationfromRelevantSources...............................................................................................................794.2Phase2:CurrentTRLandCriticalRisks...........................................................................................................804.2.1ARCurrentTechnologicalMaturity................................................................................................................814.2.2CriticalRiskFactors...............................................................................................................................................834.3Phase3:ROAApplication.......................................................................................................................................864.3.1ROAProblemSet-up..............................................................................................................................................864.3.2Base-caseDCF..........................................................................................................................................................874.3.3SensitivityAnalysis&Monte-CarloSimulation.........................................................................................894.3.4ROValuationatTRL4...........................................................................................................................................924.3.5ROValuationatTRL6...........................................................................................................................................974.3.6SensitivityAnalysisforExercisedOption..................................................................................................1084.3.7OtherCaseStudyConsiderations..................................................................................................................1094.4.NationalResearchCouncilofCanadaCaseStudy.....................................................................................1104.4.1NRCCaseBackground........................................................................................................................................110

vii

4.4.2RecommendationsforFutureNRCPortfolios..........................................................................................111Chapter5Conclusion.....................................................................................................................................................1135.1Conclusion...................................................................................................................................................................1135.2FrameworkLimitations.........................................................................................................................................1165.3RecommendationsforFutureResearch.........................................................................................................117References...........................................................................................................................................................................119Appendix1SupportingInformationforLiteratureReview..........................................................................1291.1DefinitionsofTRLs..................................................................................................................................................1291.2GOARiskAssessment.............................................................................................................................................1311.3PotentialRisksinR&D...........................................................................................................................................132Appendix2CaseStudySupportingInformation................................................................................................1342.1CopperstoneTeamBios.........................................................................................................................................1342.2ActivitiesTimeline...................................................................................................................................................1362.3CopperstoneTechnologiesFinancials.............................................................................................................1372.4SampleofInterviewQuestionswithBusinessDevelopmentManager............................................1372.5SummaryfromRelevantThesisDocument..................................................................................................138Appendix3RealOptionsAnalysisSupportingCalculations.........................................................................1403.1Base-CaseDCF...........................................................................................................................................................1403.2SensitivityAnalysis..................................................................................................................................................1413.3BuildingCapabilitiesOptionValuation...........................................................................................................1443.4MarketPivotOptionValuation...........................................................................................................................1453.5MonitoringServicesOptionValuation............................................................................................................1463.6SalesOptionValuation...........................................................................................................................................1473.7LicensingOptionValuation..................................................................................................................................148Appendix4EthicsApproval........................................................................................................................................149

viii

ListofFigures

Figure1.EREStagesofDevelopmentModel..............................................................................................................11

Figure2.DoD'sTechnologyStagesofDevelopment..............................................................................................11

Figure3.LeeandGartner’s.DevelopmentModel.....................................................................................................12

Figure4.Tritleetal.StagesofDevelopment..............................................................................................................13

Figure5.Technology-Push&Market-Pull....................................................................................................................13

Figure.6DoDTRAProcess.................................................................................................................................................21

Figure7.TechnologyRiskAcrossTRLsforHighTechnologies.........................................................................27

Figure8.3x3ProbabilityImpactMatrix.......................................................................................................................32

Figure9.GenericBinomialLattice..................................................................................................................................39

Figure10.ThestructureofRealOptions....................................................................................................................42

Figure11.FrameworkSetup.............................................................................................................................................56

Figure12.StagesofTechnologyDevelopmentAgainstTRLs.............................................................................57

Figure13.FrameworkSetupofStage-gates&RealOptions...............................................................................60

Figure14.GenericSADTModel........................................................................................................................................61

Figure15.CriticalRiskFactorsforR&D.......................................................................................................................62

Figure16.CriticalRiskFactorsDuringStagesofDevelopment.........................................................................64

Figure17.Riskprofileofmajorrisksduringtechnologydevelopment.........................................................66

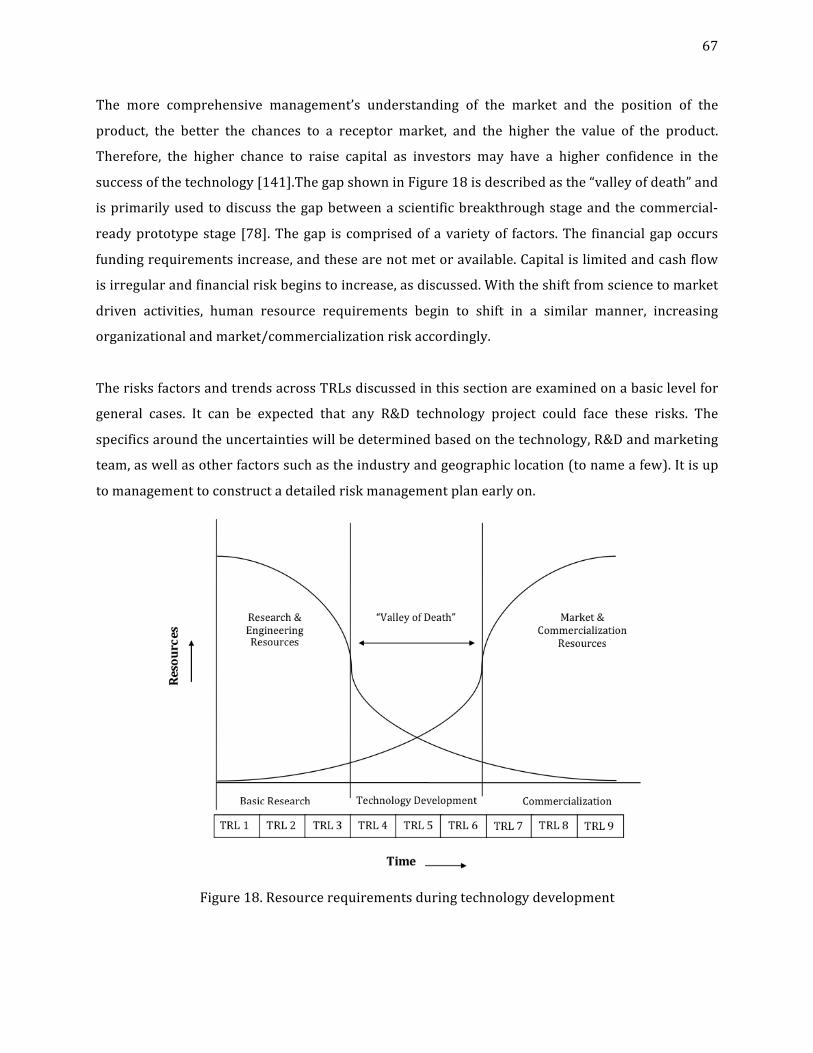

Figure18.Resourcerequirementsduringtechnologydevelopment..............................................................67

Figure19.PossibleRealOptionsConsideredatTRL4..........................................................................................68

Figure20.Monte-CarloStochasticUncertaintyModeling....................................................................................71

Figure21.BinomialLatticeExample.............................................................................................................................73

Figure22.CSTCurrentTRLPositioning.......................................................................................................................81

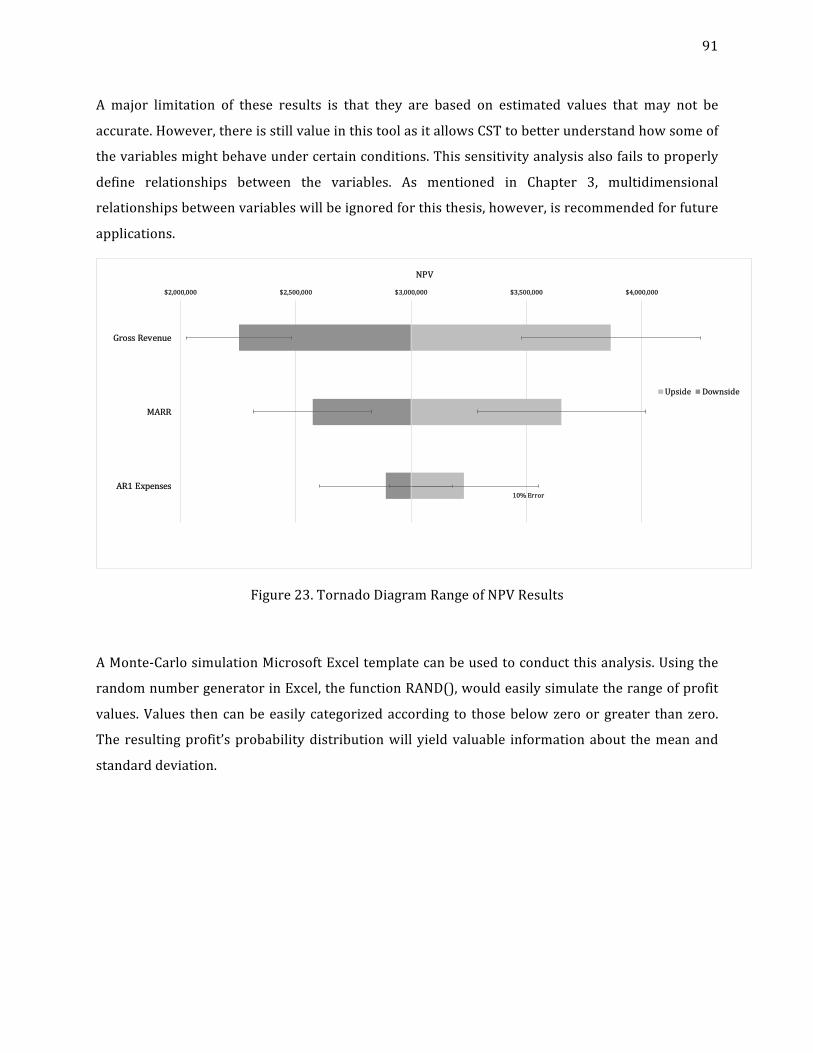

Figure23.TornadoDiagramRangeofNPVResults................................................................................................91

Figure24.DecisionTreeatTRL4...................................................................................................................................93

ix

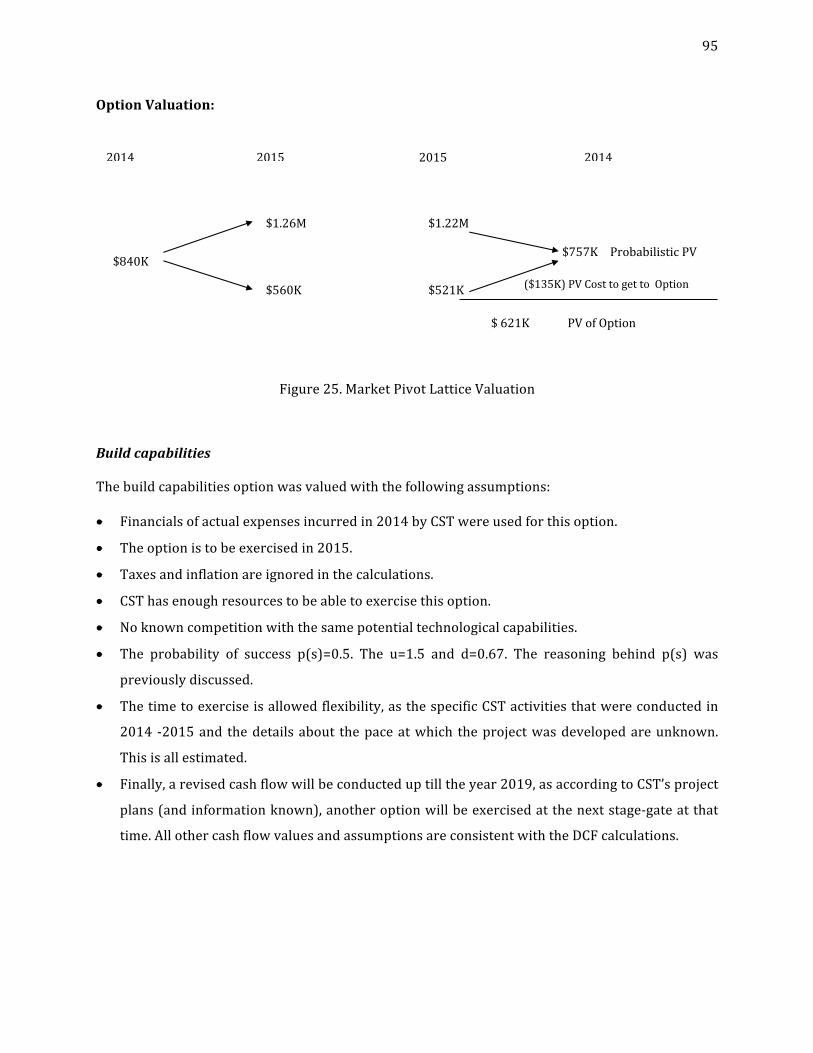

Figure25.MarketPivotLatticeValuation...................................................................................................................95

Figure26.BuildCapabilitiesLatticeValuation..........................................................................................................96

Figure27.DecisionTreeatTRL6.................................................................................................................................100

Figure28.MonitoringLatticeValuation.....................................................................................................................102

Figure29.LicensingLatticeValuation........................................................................................................................104

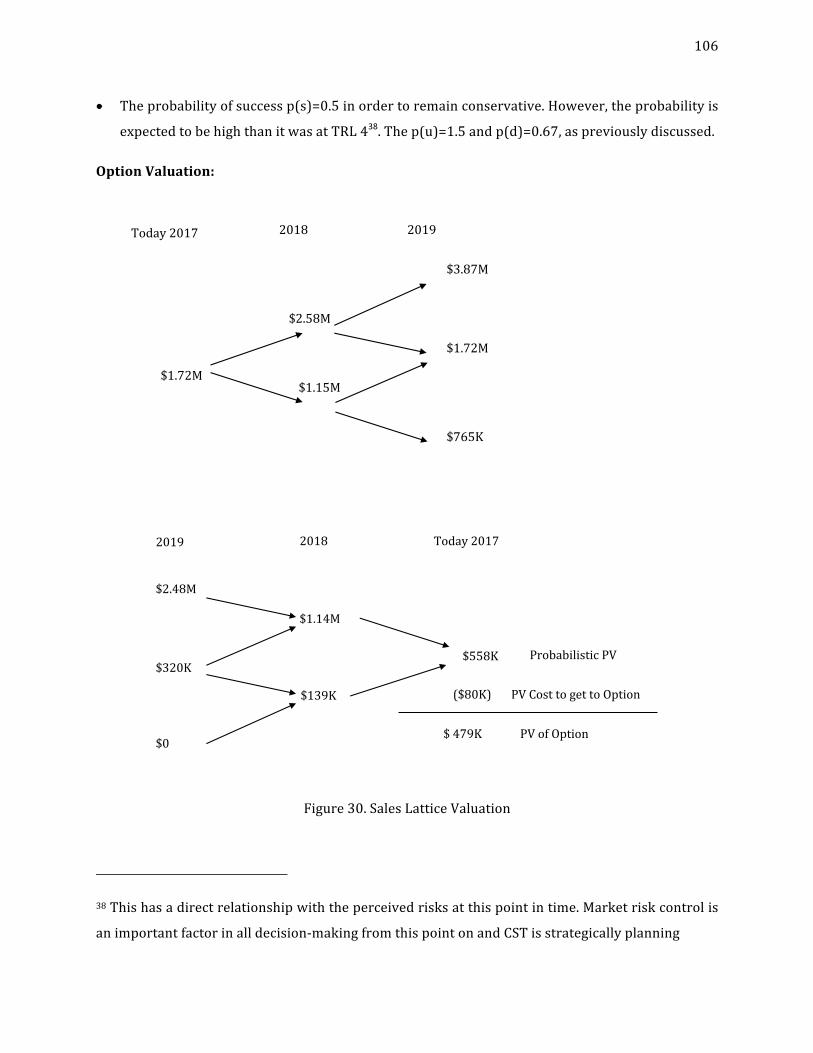

Figure30.SalesLatticeValuation..................................................................................................................................106

Figure31.PotentialRisks.................................................................................................................................................132

ListofTables

Table1.NASATechnologyReadinessLevels............................................................................................................15

Table2.R&D3LevelsandDescriptionsandTNVandDescriptions..................................................................20

Table3.MajorR&DRisksinLiterature.........................................................................................................................25

Table4.DCFAssumptionsvsDCFrealities.................................................................................................................34

Table5.FinancialOptionsvs.RealOptions................................................................................................................43

Table6.RisksandOptionsTypes....................................................................................................................................47

Table7.ExampleofPossibleEffectsRiskonProfit.................................................................................................85

Table8.Base-caseDCFResults.........................................................................................................................................87

Table9.DCFSensitivityAnalysisResults.....................................................................................................................90

Table10.SummaryofCommercializationOptionsProsandCons...................................................................98

Table11.TRLSoftwareDefinitions..............................................................................................................................129

Table12.TRLHardwareDefinitions............................................................................................................................130

Table13.GOATRASteps...................................................................................................................................................131

1

Chapter1Introduction

1.1ThesisMotivation&BusinessCase

There is a lack of simple tools that can be used to guide and value decision-making processes

associated with technology development, and provide managers with the flexibility to make

decisionsthatcancaptureopportunitiesduringatechnologyorresearchanddevelopment(R&D)

project.Thereisaneedforastreamlinedmethodologythatcanaiddecision-makersindevelopinga

setof rubricswhereacommonunderstandingofhowcritical riskelementscan influenceproject

success for technology andR&Dprojects at different stages. Themethods need to be adapted in

ordertomodelhowexpendituresatearlystagesofR&DcanleadtodiscoveriesthatbenefitCanada.

Researchers,managers,anddecision-makers inR&Dandtechnologyorganizationsarechallenged

withhow to evaluate thepotential business benefits of early stageprojects and assess the value

that these technologies will bring to the firm compared to the costs associated with their

development[1].R&Dandtechnologyprojectsneedtoolsthatmanagerisksandallowmanagersto

make decisions accordingly as conditions change and information is gained [2]. This is the

motivationbehindtheresearchconductedforthisthesisasthereisacurrentgapwherethereare

missing tools that reflect thedynamicnatureofR&Dandcanbeapplied for these longandrisky

projects. The work conducted during this research will work to fill those gaps by developing a

decision-frameworkthatutilizesastructuredapproachtotechnologydevelopmentandevaluation.

Understandingthepotentialvalueofatechnologyisusefulformanagersthatarechoosingbetween

projects and trying to understand the benefit of committing financial and human resources to a

project, and for the researchers that try to structure these projects tomaximize the value of the

potential technology [3]. R&D and technology projects can be long and unpredictable making it

challengingformanagerstoforecasttheeffortrequiredtodevelopthesenewtechnologies[4]and

their likelihood of success once pursued. These uncertainties may lead to high risks and could

result inproject failures [5].The currentlyusedvaluationmethods suchasdiscounted cash flow

(DCF)andnetpresentvalue(NPV)arenotsufficienttoolstousefortheseprojects.

2

These traditional methods assume there is only one possible route to achieve project goals or

targetsandplacemanagersinpassiverolesthatassumethatinitialpredictionsmadeandresource

commitmentsestablished,cannotbechangedevenifconditionsrequirethemtodoso[6].Thislack

ofmanagerial flexibility couldundervalueaproject [7] suchasR&Dor technologydevelopments

thathave longerhorizonsanddonothave immediatepayoffs.Organizationsmayoverlook these

projectsas theymayhavenegativenetpresentvalues [8],neglecting thepotential futurebenefit

and the opportunity to grow [9]. In addition, organizations who rely exclusively on financial

methods to assess projects are less successful at developing new products than those that also

consideredqualitativeaspects[3].Thesetraditionalapproachesusestandardinvestmentdecision-

makingthatsolelydependsonprofitcreationwhichisnotusefulforR&Dfirmswhoseultimategoal

maynotbetocreateprofit[10].Forexample,somegoalsmaybetocreateaproductimprovethe

environment,asopposedtomarketandselltothegeneralpublic.

For these reasons discussed, a methodology must be developed to overcome these gaps in

technology development management and valuation. The details behind the proposed approach

andresearchobjectivesarediscussedinthefollowingsection.

1.2ObjectiveofThesis

The objective of this research is to develop a framework that allowsmanagers, researchers, and

decision-makers to exercise flexibility through decision-making and value their technology

investments.Theframeworkwillcombinethetechnologyreadinesslevelscale(TRL)andastage-

gate approach thatwill be the logical pointswhere a project’s activities, requirements and risks

changeandshouldbereassessed.Thiswillsupportdecision-makingthroughaconsistentmethod

thatwillassessatechnology’smaturityandprogress.Theframeworkwillutilizearealoptions(RO)

approach by recommending a small number of options to be placed along the TRL scale where

managerial decisions can be evaluated through real options analysis (ROA) and encourage

management to make evidence-based decisions for technology development and project

continuation.

3

TheapplicationofTRLsandtheROmethodcanenablemoreconsistentdiscussionsonhowrisks

changefromonephaseofaprojecttoanother,andthecomparativevalueofdifferentdecisions,or

differentprojectsacrossaportfolio.Thisapproachcanbevaluablefororganizationsasitcanhelp

exploreopportunitiesandjustifyspendingonlongerandriskierprojectswithpotentiallyveryhigh

futurevaluestoCanada.

“Realoptions”,anextensionoffinancialoptiontheory,referstoadecisionpertainingtoatangible

asset as opposed to stock. It refers to the ability of managers to exercise flexibility through

decisions such as growth, delay, or abandonment of a project as technology, financial,market or

other conditions change [11]. This active decision-makingmethod can improve the likelihood of

scientific success and the positive commercial benefit to Canada. Real options will allow

organizations to establish key decision points during R&D stages for projects across a research

program. It is a structured analysis method for determining success factors as a technology

progresses through the development stages, and the comparative influence of making early

investmentsinR&Dactivitiesthatmitigatetechnicalandcommercialrisk.

ByincorporatingTRLsintoadecision-framework,thiscansupportthesedecision-makingprocess

duringdevelopmentandimplementation[12].Itisanapproachthatworkstoreduceriskthrough

proof-of-concept and system success [13]. Furthermore, incorporating real optionsmethods into

this framework can provide researchers and managers with a tool that allows them to better

understand risk.Realoptions canmakeup forwhat traditionalmethods lack,which isproviding

flexibility. It allowsmanagers to alter the course of uncertain projects by incorporating strategic

options,thatincreasetheoverallvalueoftheproject[9].ROcanbethoughtofasguidesthatallow

managerstomakedecisionsatdifferentstagesoftheproject,suchas,whetheraprojectshouldbe

continued or terminated [9]. The sequence of decision-making during these projects allows for

justifieddecisionsofwhentoundertakeanopportunity[14].

4

The framework will be applied to a small Canadian high-technology start-up that is currently

developingautonomousrovers (AR).TheseARsallowaccess to tailingsponds thatareotherwise

inaccessible using the current measuring equipment. The case study will examine current

technological maturity using the TRL scale and the proposed stage-gate approach and identify

critical risks that would threaten progress and the ability for the start-up to meet their

organizationalandprojectgoals.Thebehaviourofthesecriticalrisksandhowtheyareexpectedto

developandtheireffectsonprojectgoalswillbediscussed.ROwillthenbeappliedtovaluearange

ofpotentialdecisionsatkeystagesoftheproject.Theseoptionswillbecomparedanddiscussed.

Thestudywillalsobrieflyintroducegeneralconceptsrelatedtoapplyingthisframeworktoalarge

government research organization’s portfolio. Framework limitations and application challenges

willbeconsideredandrecommendationsforfutureresearchwillbediscussed.

1.3ThesisStructure

This thesis is organized into five chapters. Following the introduction, Chapter 2 is a literature

review that introduces and discusses relevant topics to R&D and technology development,

technology readiness levels and assessment methodologies, real options theory and application,

andframeworksusedinvariousindustries.Chapter3establishestheproposedframeworkandthe

approach behind how it can be applied to assess decisions and value options. The framework is

then applied to a case study in Chapter 4, and potential application to a government research

organization’sportfolio isalsoexamined.Theanalysisandresultsarediscussed.Toconclude the

work, Chapter 5 provides a summary and discusses the limitations of the framework and

recommendationsforfutureresearch.

5

Chapter2ReviewoftheLiterature

This chapter reviews the main topics related to the development of the real options decision

frameworkthatwillbedescribedinChapter3.

GeneralconceptsoftechnologydevelopmentandR&Darediscussed,alongwiththecommonstages

of development discussed in the literature. This conceptualization acts as the baseline for

discussing technology readiness levels (TRL), where general activities, common assessment

methodologies, challenges and applications in industry are outlined. Common risks in R&D and

technologyprojectsarethendefinedwithillustrativeexamples.ThissectionisaprimerforChapter

3,astheseriskswillthenbemappedalongthedevelopmentstagesandTRLscale.

Risk management concepts and tools used in the R&D context are reviewed. Finally, valuation

methodsarediscussed.Traditionalvaluationmethodsandfinancialoptiontheoriesareintroduced.

Real option types, application and industry use are discussed. The steps and important

considerationsforapplyingrealoptionswillbeexamined,withadditionaldetailprovidedduringits

applicationinChapter3andChapter4.

2.1R&DandTechnologyDevelopment

R&D and technology projects deliver a combination of new knowledge, new technology or

capability, or a platform of technologies [15]. Technology R&D efforts should improve the

performanceandreliabilityofatechnologyandthuscontributetooverall technologymaturation,

whileinvestmentsmadeateachstageshouldresultinrisksbeingreduced[16].

Organizational, portfolio and project goals must be properly prioritized in R&D programs [17].

ProperresourceallocationiscriticalinR&Ddecision-making,wheremanagersmustbalancemany

organizational short-term and long-term goals that may be weighted differently by different

stakeholders [17]. Firms need to be able to work effectively within financial and resource

constraints[18].Short-termandlong-termgoalsbothalsoneedtobeconsideredaccordingly[17].

6

The need to problem solve and quickly adapt to changing conditions in high-technology R&D is

magnifiedbythepresenceofunforeseenrisksassociatedwithtechnologyintegration,performance

levels, schedule andproject budgets [19]. Tools that help assess the impacts of projects and any

overlapwithotherprojectsincludeportfolioanalysis1anddevelopmentstage-gates[18].Stage-gate

methodsemploygateswherethetechnologyisassessedagainstasetofcriteriaanda“continue/go

orstop/kill”decisionismade[15].Stage-gatesanddevelopmentmodelsarediscussedin2.1.1and

2.1.2.

R&Dandtechnologyprojectsareoftencompromisedwhen inappropriatetoolsandprocesses(or

financial criteria) are applied tomanage them [15]. Examples of such tools are discussed in 2.4.

Because of the uniqueness of such projects, applying traditional methods to manage innovative

projectsmaycauseharm,asitcouldresultinterminatingahigh-profitpotentialproject[15].

2.1.1R&DandTechnologyDevelopment

Developinganewtechnologymayposehighriskstoanorganizationastheycarryalargeamountof

technical uncertainty and other unknowns [15]. Uncertainties in R&D are expected as these

projects have intensive activities associated with knowledge discovery, problem-solving,

overcoming failure, dealing with change and making breakthroughs [19]. New technology

developmentsareunpredictable,and it is–bydefinition - impossible toschedulea technological

breakthrough,whichmakesithardtoestimatefutureefforts[4].

R&D projects are separated into development phases, and milestones are set as a method to

determine and control project progress [20]. These phases behave as checkpoints where

organizationalorprojectgoalsarerealizedandprogress isassessed[17].A lackofspecificstage-

gatedecisionpointswithpre-setcriteriaresults in incorrectproductconcepts,wastedresources,

technologyfailureandexcessivespending[21].

1Portfolioanalysisreferstotheprocessesthatinvolveassessingandaddressingtheuncertainties

inprojects,allocatingandbalancingresourcesamongprojectswhilemeetingorganizationalgoals.

7

At theearlystagesof theproject, there isnoconcreteevidenceorknowledgeabout thepotential

successofatechnology[22],theprobabilityoftechnicalsuccessmaybequitelowastechnological

capability has not yet been recognized [23][15]. However, as a technology progresses andmore

information isobtained, theestimateofsuccessbegins to improve[22].Manyorganizationshave

implemented requirements for their R&D and high-technology projects, where specific business

plans and commercialization options are laid-out however, the challenge managers face when

dealingwiththeselongandhighlyuncertainprojects,istheirinabilitytocorrectlycompletesome

of the requirements of these processes [15]. For example, envisioning themarket landscape and

conducting a market and competitor analysis is difficult for a technology that is still at the

fundamentalresearchstage,andhasnotyetbeenfullydefined[15].

DuringtheconceptualphasesofR&D,theremaybeachangeinprojectdirectionastechnologyand

marketinformationbecomesapparent,itisimportantformanagerstohavetheflexibilitytomake

these changes2 [17]. Fundamental research phases may be heavily relying on studies, technical

literature, preliminary lab studies, economical valuations and patent surveys [18]. The applied

phaseofR&Dtypicallyinvolveslaboratoryworkthataimsatrefiningthetechnology’sfeatures,and

initialassessmentoffeasibilityandpotentialmarketforproductsandservicesembodyingthenew

technology.Thetechnologyshouldnowhaveaspecificpotentialapplicationorpurpose[18].These

early phases develop concepts and ideas, where pattern recognition3 and future scenario

development isvaluable [17]. It is important to identify technologies thatare feasibleandhavea

potentialformarketacceptance[24].

2This is thevalue in realoptions.Realoptionsaredefined in2.4. It allows thesedecisions tobe

estimatedandconsideredfromaspectsrelatedtotime,costs,resourcerequirements,etc.

3 Pattern recognition is the skill needed to be able to spot trends in data (if any) or projects.

Recognizingpatternsand trendanalysisgohand-in-hand, andmanagers canutilize suchskills to

improveprojectplanningandresourceallocationiftheychooseto.

8

During the technologydevelopmentphase, the focusbecomesondesign,prototyping,and testing

[18][14]. The ultimate goal during the technology development phase is to eventually be able to

deliveraproduct toauser [25].At thispoint, the technologymusthaveproven toaddeconomic

value [12].Thepilot testingof technologywouldhavemoved from laboratory to operational (or

relatively operational) environment [26]. This is also where scale-up activities may begin (and

continue into the next phase). During the process of scale-up, new information about risks is

realized [26].The scale-upactivities are separated intobatch sizes,where smaller sizes canbea

proof-of concept, and the larger batches test for the effects of larger scalemanufacturing on the

quality or viability of the technology [26]. There is also an inherent process that occurs during

development,which is the “technology transfer”.This iswhere thedevelopmentprocesschanges

fromtechnologyandsciencecreationtoproductcreation.Furthermore,thereisatransitionwhere

the project is transferred from scientific personnel to the commercialization andmarket experts

[27].Therefore, it is important formanagement toensure that functionalgroupsworkefficiently

withoneanother[27],andkeepabalanceoftheteamandindividualresponsibilities[17].

The decision to commercialize is usually made when uncertainties from the R&D stages are

resolved [14]. The commercializationwarrants a shift in tasks as the organization is involved in

market positioning and competition [24]. This phase may involve activities that involve

manufacturing, process and product launches done through marketing [14]. During the

commercializationphase,issuessuchasthecostofgoodssold(COGS),thesizeofmarketandsale

pricemaybecriticalissues[17].Commercializationofnewtechnologiescouldincludelicensingor

donating intellectual property that is not active (i.e. dormant) [9]. The commercialization phase

bringsnew technologies to themarket and can includeactivities suchasmanufacturing, refining

thetechnologyanddistributiontocustomers[25].Thelackofcommercialskillsandashortageof

financeswillpreventanorganizationfrombeingabletomoveforwardwithnewtechnologies[28].

CooperandKleinschmidt[21]discusstheresultsfromtheirresearchwheretheyfoundthatmany

companies dive far into later stages of development without any consideration for

commercialization, only to realize later their expectations of themarket are incorrect [21]. This

brings up an important concept that should be discussed, technology-push and market-pull

technologies.Thisisdiscussedin2.1.3.

9

ActivitiesinthestagesofdevelopmentarespecifictotheprojectbutCohenetal.[29]discussnine

dimensions for basic gate decision criteria that are the framework for identifying issues. The

criteria remain the same but the details evolve as a technology progresses from one gate to

another4.Thesedimensionsforbasicgatecriteriaareasfollows[29]:

• Strategicfit:businessstrategiesandneeds

• Marketandcustomer:potentialbreadthofthetechnologyinthemarket

• Businessincentivesandrisks:keyissuesanduncertainties

• Technicalfeasibilityandrisks:scienceandtechnologyuncertainties

• Competitiveadvantage:technologyorbusinessbenefitsoverthecompetition

• Killervariables:thatcompletelystopaproject

• Legalandregulatorycompliance:health,safety,environmentaloroperationalintegrity

• Criticalfactorsforsuccess

• Plantoproceed:planstoachievegoals,milestonesandtargetdatesforthenextgate.

Hoegletal.[30]discusstheimportanceofteamdynamics(andcoordination)duringallthephases

of development and emphasize that proper team dynamics in the early conceptual phases of

developmentcanultimatelyhavemajoreffectsonperformanceinthelaterstagesofdevelopment

[30].During thedifferent stagesof theproject,managers canexpect tohavedifferent views that

overall influence the project. Criteria for decision making should be integrated within all

developmentalphases[18].Managersordecision-makerscanbethoughtofasgate-keepersduring

aprojectwheretheycanstopprojectsthatarenotproducingaccordingtosetstandards,butmust

alsobeabletospotpotential innewideas,andmakechangesduringtheprojecttocapturethese

opportunities[29].

Metricsmustbesetbymanagementearly-on inorder forprogressevaluationtobecompletedat

each stage. As the project progresses from conceptual stages all the way to commercialization,

informationandevaluationmetricschange[17].

4 For example, for research, initially thequestion askedmaybewhether the research is feasible.

Stagesaftermaybecomeaboutwhethertheconceptsinvestigatedarefeasible.

10

It isalso importanttonotethatR&Dorganizationsmaynotbecorporateenvironmentsandtheir

goal may not be to maximize revenue5[10]. It is important to note that the nature of available

informationchangesduringtechnologydevelopment.Intheinitialstages,datacanbeexpectedto

be of the qualitative nature,while in the later stages of commercialization,managers can expect

morequantitativeinformation[17].

Terminationphases areoftennot included inR&Dprojects, however, reasons for terminationor

failure of a project should be considered6 as it could improve and drive the decision-making

processesinaproject[17].Figure4illustrateshowtheterminationphaserelatestootherstagesof

developmentandhowitfitswithinamodel.

2.1.2ExamplesofTechnologyDevelopmentModels

Another common tool used by organizations is the stage-gate development method where the

technology is assessed against a set of criteria and decisions aremade at each gate [15]. Exxon

Research andEngineering (ERE)7 Companyuses a stage-gate systemwhereR&D activities begin

with fundamental research, applied research development, validation, and concludes with a

commercializationstage[29].EREthenaddedthreenewresearchgatesthatprecedethestandard

stage-gateprocessdiscussed.Thisadditionincludedidentifyingopportunitiesandenablingscience

andideagrowth[29].Kelmetal.[24]emphasizethatregardlessofthedifferencesinthetheoretical

developmentmodelsinindustry,andthespecificsbehindeachphase,thereisanoverallconsensus

thattheearlystagesofatechnologydevelopedareheavilyinvolvedintechnicalinnovation,while

thelaterphasesarefocusedoncommercialization[24].

5Anorganizationmayhaveitsownideaofmetricsofsuccess.Forexample,anot-for-profitcould

aimtoonlywanttohavepositivesocietalimpactinthepublic.

6Thisiscanbedonethroughriskassessments.

7ThishasnowbecomeExxon-Mobil(EMRE)

11

Figure1.EREStagesofDevelopmentModel[Adaptedfrom[29]]

StageAshowninFigure1iswherebusinessmanagersandresearchersbegintotrytoestablisha

businesscaseandcompetitiveedgeforthepotentialtechnology,throughadetailedplanthatsets

technical and scientific variables. The plan includes resource requirements as well as plans of

action of how these deliverables can be met [29]. Stage B is where the plan from Stage A is

executed,andissuesrelatedtoscientificprocessandleadstobusinessopportunitiesareidentified

[29].

Usingthegate-processisastructuredmethodtoassessresearchprogressandallowsfordecisions

tomade in a timelymannerwhile tracking project progress fromboth a science and technology

aspect,aswellascommercializationaspect[29].Atthegateofeachstage,risksanduncertainties

andotherdriving factors shouldbediscussedandcommunicatedwithkeypersonnel [17].There

are many versions of technology development models in literature that have been adapted for

differentpurposesandindustries[17][29][31][32].

Figure2.DoD'sTechnologyStagesofDevelopment[Adaptedfrom[33]]

ConceptRefining

TechnologyDevelopment

SystemDevelopment&Demonstration

Production&Deployment

OperationsandSupport

DecisionMilestones

A B C

12

Figure2demonstratesthetechnologydevelopmentmodelusedbytheUSDepartmentofDefense

(DoD). Their model is comprised of five stages: concept refinement, technology development,

systemdevelopmentanddemonstration,productionanddeployment,andoperationsandsupport

[34][35]. The model identifies three major milestones as logical stops where technology

opportunitiescanbecaptured[34].This isshownattechnologyreadinesslevel(TRL)4,6,and7,

andOlechowskietal.suggestthatmappingTRLstostagesofdevelopmentisausefulpractice[36].

They argue that it allows expectations to be clear and consistent for all projects [36]. Concepts

related to technology readiness levels will be discussed in Section 2.2. The Milestone Decision

Authority(MDA)workswithstakeholdersinordertoassesswhetherthereisenoughinformation

at eachphase, beforemoving on to the next [34]. A projectmay start at any stage of themodel,

however, it is still a requirement that itmeet the entrance requirement of anyupcomingphases

[34].

LeeandGartner[25]discussedstagesoftechnologydevelopmentinasimplifiedmodelillustrated

inFigure3.Thereisonlyonephaseofresearchasopposedtotheclassicbasicandappliedresearch

phases and three major gates. This model does not view development as a linear sequential

process, instead, it is an iterativeprocess that responds to themarket andcompetition [25].The

potentialofwhetheratechnologicalbreakthroughhasanycommercialviabilityisdoneatthefirst

stagewiththehelpofamarketspecialist[25].

Figure3.LeeandGartner’s.DevelopmentModel[Adaptedfrom[25]]

TechnologyDevelopment

BasicResearch

TechnologyCommercialization Marketand

IndustryGo/NoGo Go/NoGo Go/NoGo

13

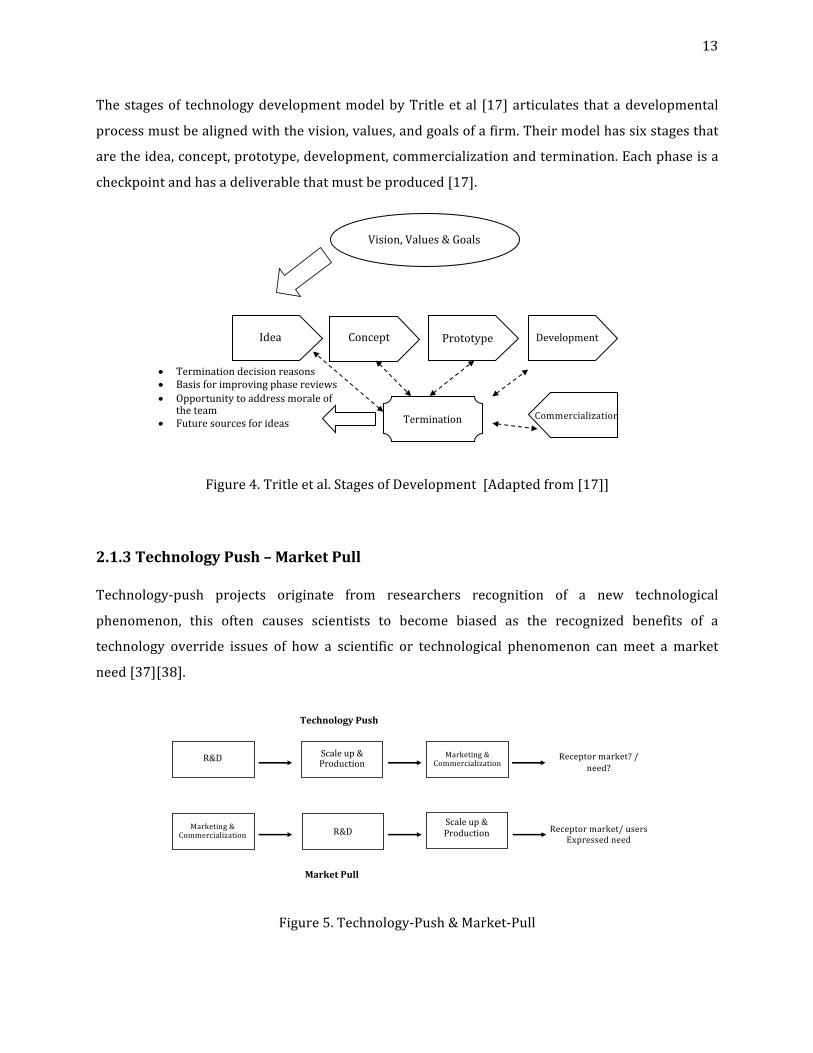

Thestagesof technologydevelopmentmodelbyTritleetal [17]articulates thatadevelopmental

processmustbealignedwiththevision,values,andgoalsofafirm.Theirmodelhassixstagesthat

aretheidea,concept,prototype,development,commercializationandtermination.Eachphaseisa

checkpointandhasadeliverablethatmustbeproduced[17].

Figure4.Tritleetal.StagesofDevelopment[Adaptedfrom[17]]

2.1.3TechnologyPush–MarketPull

Technology-push projects originate from researchers recognition of a new technological

phenomenon, this often causes scientists to become biased as the recognized benefits of a

technology override issues of how a scientific or technological phenomenon canmeet a market

need[37][38].

Figure5.Technology-Push&Market-Pull

Vision,Values&Goals

Idea Concept Prototype Development

CommercializationTermination

• Terminationdecisionreasons• Basisforimprovingphasereviews• Opportunitytoaddressmoraleof

theteam• Futuresourcesforideas

Receptormarket?/need?

R&D Scaleup&Production

Marketing&Commercialization

Marketing&Commercialization R&D

Scaleup&Production

Receptormarket/users

Expressedneed

TechnologyPush

MarketPull

14

Thepossibilitiesofthesetechnologiesareover-hypedinordertosecureinitialcapitalinvestment,

butoftenthereisnoidentifiedcustomeroruserneed[39].Wheatcraftarguesthatthetechnology-

pushapproachishighrisk,andprefersmanagersandresearchersadoptthemarket-pullapproach

[39].Technologiesdevelopedwiththemarket-pullordemand-pullapproachdefinedtheirproducts

features with a market of end users in mind [40]. Market conditions create opportunities for

technologies to satisfy unmet market needs [41]. Management’s attitude, in general, has an

influenceoninnovationwithinanorganizationandtheapproachtakenastheyhaveacriticalrole

indecision-making[38].

2.1.4CapabilitiesofaFirm

Capabilitiesofafirmhavealargeinfluenceonthefinancialcapital,technicalexpertiseandresource

requirements(andavailability)[38].Dynamiccapabilitiesisatopicthathasgainedpopularityover

theyears[42].Tosummarize,itistheabilityofanorganizationtointegrate,buildandreconfigure

theircompetenciesinreactiontofast-pacedanddynamicsenvironments[43].Anin-depthreview

ofthistopicisoutsidethescopeoftheresearch.

2.2TechnologicalMaturity

2.2.1TechnologyReadinessLevelsOverview

Thetechnologyreadiness level (TRL)scalewas firstdevelopedbyNASA in theearly1970’s [36].

The purpose of this scale was to set a standard, and provide a consistentmeasurement system

managers could use to assess technological maturity [16]. This can be validated through

demonstrationsthatincreaseinfidelity,andinrealisticoperatingenvironments[44][16].TheTRL

scale allows researchers and managers the opportunity to improve risk management,

communicationoftechnologydevelopmentprogress,andtheirdeliverables[45].Theoriginalscale

developed consisted of seven levels andwas later upgraded to nine levels in the 1980’s, where

NASA then published definitions of each level and their activities [44][46]. By 1999, the U.S

DepartmentofDefense(DoD)hadadoptedthisscalefortheirprogramsandsystems[47][46].The

scalewas then expandedby theDoD to allow the applicability of TRLs to softwaredevelopment

projects [48]. The terms “readiness” and “maturity” describe the developmental progress of

technologyandhavebeenusedinterchangeablyintheliterature[34].

15

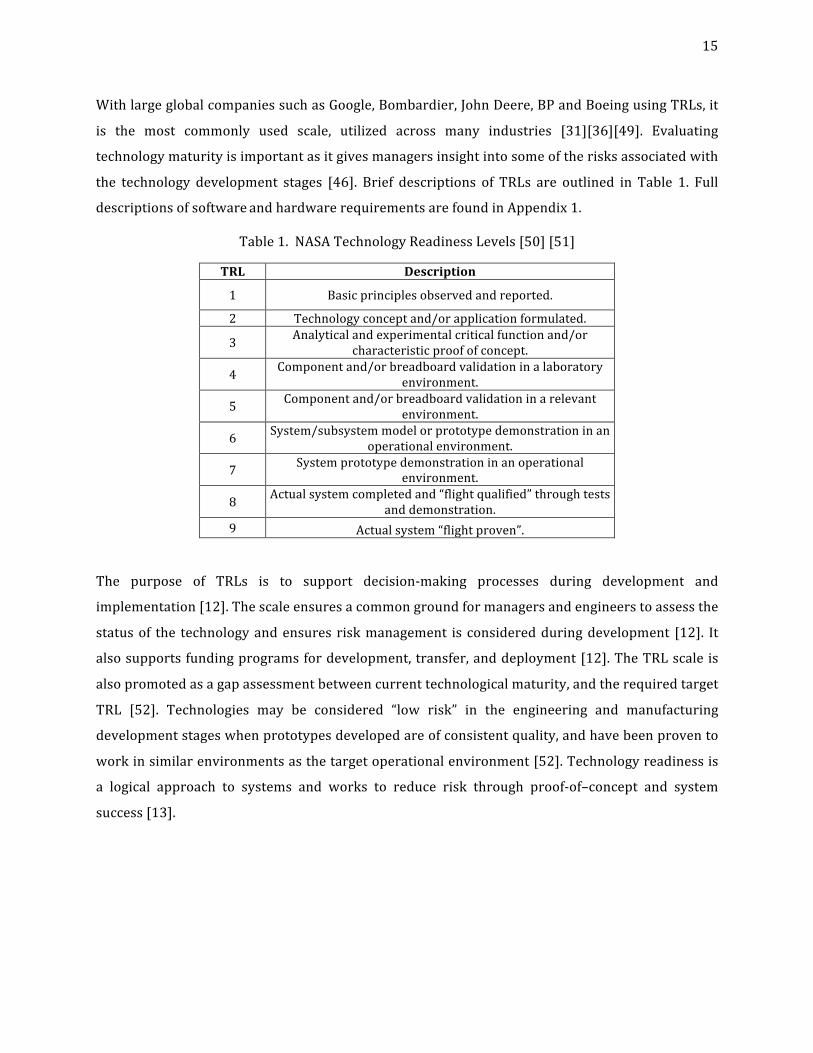

WithlargeglobalcompaniessuchasGoogle,Bombardier,JohnDeere,BPandBoeingusingTRLs,it

is the most commonly used scale, utilized across many industries [31][36][49]. Evaluating

technologymaturityisimportantasitgivesmanagersinsightintosomeoftherisksassociatedwith

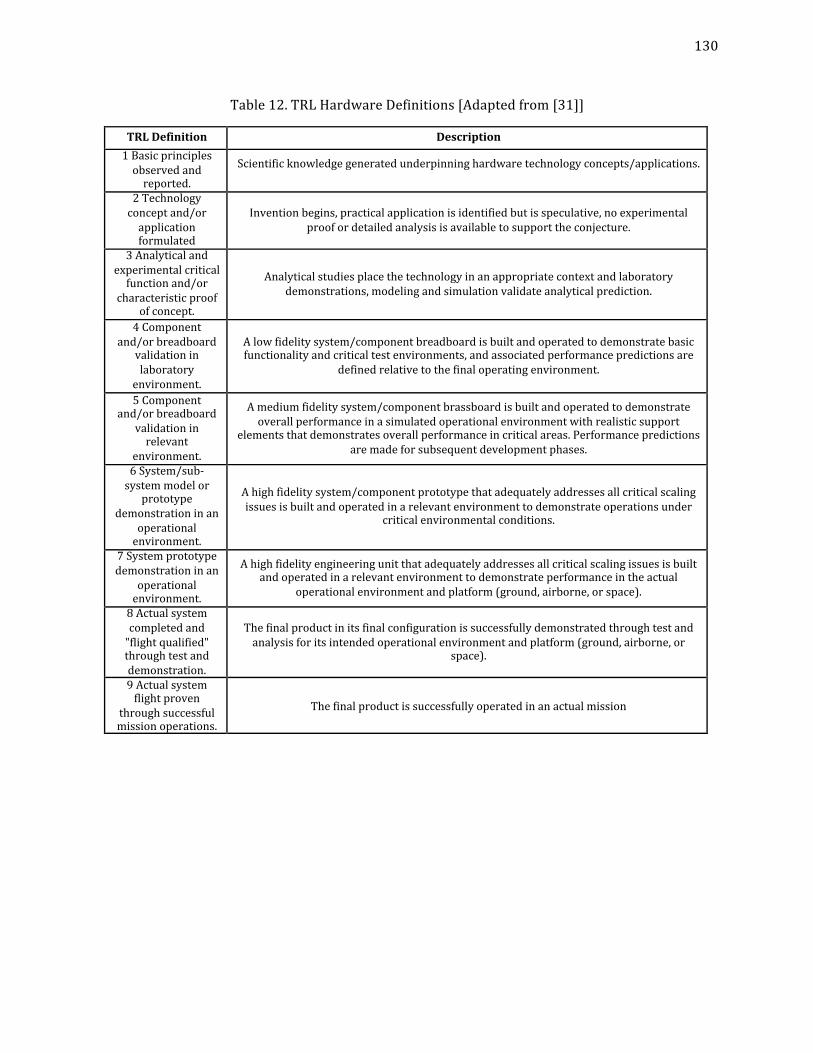

the technology development stages [46]. Brief descriptions of TRLs are outlined in Table 1. Full

descriptionsofsoftwareandhardwarerequirementsarefoundinAppendix1.

Table1.NASATechnologyReadinessLevels[50][51]

TRL Description

1 Basicprinciplesobservedandreported.

2 Technologyconceptand/orapplicationformulated.

3 Analyticalandexperimentalcriticalfunctionand/orcharacteristicproofofconcept.

4 Componentand/orbreadboardvalidationinalaboratoryenvironment.

5 Componentand/orbreadboardvalidationinarelevantenvironment.

6 System/subsystemmodelorprototypedemonstrationinanoperationalenvironment.

7 Systemprototypedemonstrationinanoperationalenvironment.

8 Actualsystemcompletedand“flightqualified”throughtestsanddemonstration.

9 Actualsystem“flightproven”.

The purpose of TRLs is to support decision-making processes during development and

implementation[12].Thescaleensuresacommongroundformanagersandengineerstoassessthe

statusof the technologyandensures riskmanagement is consideredduringdevelopment [12]. It

alsosupportsfundingprogramsfordevelopment,transfer,anddeployment[12].TheTRLscaleis

alsopromotedasagapassessmentbetweencurrenttechnologicalmaturity,andtherequiredtarget

TRL [52]. Technologies may be considered “low risk” in the engineering and manufacturing

developmentstageswhenprototypesdevelopedareofconsistentquality,andhavebeenprovento

workinsimilarenvironmentsasthetargetoperationalenvironment[52].Technologyreadinessis

a logical approach to systems and works to reduce risk through proof-of–concept and system

success[13].

16

2.2.2TRLs:CharacteristicsatEachLevel

As shown in Table 1, TRL 1 is the lowest level of maturity where activities might include

fundamental research and studying basic properties [30]. The costs during this level could vary

dependingontherigoroftheresearch[44].Theserelatedcostsarecompletelydependentonthe

scientific area of the research conducted and resources required (i.e. white board vs. super

computers)[53].TRL1isacommonlevelforuniversitiesandresearchorganizations[54][53].TRL

2 is where the practical application of a technology is identified, but without any experimental

prooforproperanalysistosupporttheclaim[39].Thecostswillstillberelativelyonthesamescale

asTRL1.AnyorganizationmaybeatTRL2,however,itiscommonforuniversities,entrepreneurs,

andsmallbusinessestobeinthisTRL[53].

AtTRL3,appliedresearchanddevelopmentbeginswherethetechnologyisputintocontext.This

levelcombinesanalyticalandexperimental(couldbelaboratory)methodologiestoproveconcepts.

Thespecificsbehindapproachesusedarespecifictothetechnologyandresearchers’discretion.For

software,proofofalgorithmisnecessary,whilehardwarewillrequirephysicalvalidation.Similar

to the previous TRLs, costs in TRL 3 can be expected to be unique to the technology being

developed [44][53], and because of the increase in costs, it can be expected that some kind of

funding would be attained at this point. This could be private sponsorship or government-type

funding.AttheselowTRLs(1to3),thetechnologicalriskishighwhichmeansthatleadtimesare

increasedandfundingopportunitiesmaybescarce.OftentechnologiesatTRL1-3mayfallintothe

technology-pushcategoryclassification,especiallyduringtheprocesseswhereknowledgeisgained

withoutanyspecificapplication[39].Duringtheseearlystages,managersshouldbegintoconsider

how the technology or processmay be interrelated and the potential risk and other parameters

needed for future development [26]. In TRL 4, low-fidelity validation is required and should be

developedinawaythatisconsistentwiththerequirementsofthepotentialsystemapplication,and

beabletosupporttheconceptsinpreviousTRLs.Theelementsofatechnologymustbeintegrated

to determine that theywill all operate with one another and achieve target performance at the

levelsofacomponent.Mankins[53]ranksTRL4costsasmoderate[44],andhedescribesthecost

requirementstobe“severaltimesgreater”[53]thanthepreviouslevels.AtTRL4,theuncertainty

isexpectedtohavedecreasedslightlywiththeproofofconceptandlaboratoryvalidation,whichis

argued to provide greater chances of securing funding sources [53]. TRLs 3-4 should identify

activitiesthatproveconceptsatalaboratoryscale,thatarealsorisk-reducing[26].

17

TRL 5 requires that elements of a technology be integrated into a component, sub-system or

system-level.Thismaymeanthatmoretechnologiescouldbe involved inthedemonstration.The

fidelityofthecomponenttestedinthislevelincreasesgreatly.CostsforR&DincurredinTRL5are

describedasmoderatetohigh[44],wheretheyaretwo(ormore)timesgreaterthanthatinTRL4

[44].TheactivitiescompletedinthisTRLaremostlikelydonebyR&Dorganizationswithaccessto

corporate laboratories. Therefore, it is expected that funding required increases due to these

increasedcosts[55].AtTRL6,theprototypesystemistestedinarelevantoperationalenvironment

andprovensuccessful.At thispoint,maturation isdrivenby instillingconfidence inmanagement

(inthetechnology’sfuturedeployment),ratherthantheR&D.Demonstrationmaybeofthesystem

applicationandanyothertechnologiesthatcouldbeintegrated.CostsinTRL6areexpectedtobe

highdue to intensive demonstrations of the technology [44]. Almost always, there is a source of

fundingwhetherfromthegovernmentorindustry.Pilot-scaletestingactivitiesinTRLs5-6address

risksandexposefurtherinformationabouttheconcept,andfurtherreducethem[26].Thecostsare

describedtobe“twoormoretimes”lessthantheinvestmentrequiredinTRL7[55].

LevelsbeyondTRL6aremajormaturationsteps.InTRL7,theprototypeshouldbecloseto,orat

the operational scale necessary, with the demonstrations occurring in the relevant operational

environments[44].Thepurposeofthislevelistoensuresystemengineering,aswellastodevelop

management confidence in concepts related to the market. Costs associated with TRL 7 are

describedas“veryhigh”[44].Dependingonthescaleandfidelityofthesystem,thiscouldbealarge

amount of the ultimate system cost, thus would always require formal sponsorship. TRL 8

representstheendofrealsystemdevelopmentformostelements[55].Thislevelmayincludenew

technologiesbeingintegratedintothesystem.CostsinTRL8arespecifictotherequirementsofthe

systemandareclassifiedas“veryhigh”withthemagnitudeofcostsbeing5-10timesgreater(this

isbecauseoffull-scalesystemdevelopment)[44]thanallthepreviousTRLscombined,andagain,

wouldexpectformalfunding.TRL9isthefinallevelwherethesystemisdeployed,andthefixingof

systembugsandglitchesbegins.AtTRLs7-9,researchersandmanagersshouldbeabletoassess

customer acceptance and real-world impact as the new product is introduced (or about to be

introduced) intothemarket[26].Thisalsoassumesthatcustomers’acceptanceofthetechnology

willbepositive,therefore,itisimportantthatthebusinesscaseisreviewedduringthistime[26].

18

It is important to note that reducing risk across TRLs is not done linearly in terms of cost [56].

Mankins[53]notedthatthecosttoincreasefromTRL5toTRL6ismorethan4timesthecostsof

the previous levels, and progressing to TRL 7 comes with even greater costs. He refers to

progression past TRL 6 as “the valley of death” [53][56] and discusses the struggle between

scientistsandmanagers.Withanynewtechnology,reducingriskisapriorityformanagerssothat

projectbudget andproject schedules arenot affected,while the scientists justwant tomaximize

theiradvancesanddiscoveries[56].MoreonthiswillbediscussedinChapter3.

2.2.2TRLAssessmentMethodologies

A technology readiness assessment (TRA) is the process of assessing the maturity level of a

technology [31]. This process relies on information during the technology development stages.

However, theU.SGovernmentAccountabilityOffice(GOA)suggests thatperformingaTRAbefore

developmentbeginsprovidesvaluableinformationformanagement[31].Mankins[16]statesthat

animportantpointduringdevelopmentiswhenmanagementmustdecideonwhethertechnologies

neededaspartofasystemhaveallcollectivelyreachedthetargetmaturity,risk,andperformance

levelforprogress[16].TheassessmentofTRLscanbeconductedattimesthatmanagementdeems

necessary,asaTRAneedstobespecificinthecontextofthetechnologyandtheaudiencethatwill

useit[31].TheabilitytoconductathoroughTRAwillultimatelydependontheavailabilityofdata,

reports,andaccuracyofitall[31].Inthecaseofnewtechnologydevelopments,scopeisnotalways

availableorunderstood[31].

Because theTRLscalemay lackobjectivityandrely toomuchon tacitknowledge,somematurity

assessmentmodelsandmethodshavebeendevelopedtotacklethisissue[34].Thesemodelshave

notonlybeenusedtoassessmaturity,buttoalsoassessriskssomanagementcanbetteranticipate

theminlaterstages[44][16].

19

Mankins [44] recommends that a general model to assess a technology should include five

categories:

1. Abasicresearchphasewheregoalsandtargetsareidentified.

2. An applied or focused research phase where a specific technology is considered for specific

applications.

3. Technologydevelopmentandprototypingforeveryidentifiedapplication(priortofullsystem

development).

4. Fullsystemscale-upandtesting.

5. Technologylaunchandoperations.

Mankinsalsosuggeststhatanassessmentshouldpossessthefollowingcharacteristics[16]:

• Clarity: cleardecision-making criteria todetermine risksand readiness.Criteria shouldallow

forindependentevaluationandverification.

• Transparency: technology risk assessment should be formal and consensus based, where all

participantseasilyunderstandtheassessmentprocessesandresults.

• Crispness:decisionsmadeduringtheassessmentshouldbetimelyanduptoprogrambudget

planningrequirements.

• Usefulinprogramadvocacy:processesusedduringtheassessmentshouldhavethebasicsfor

advocacyofaresult.

The model Mankins [16] introduces is an integrated technology readiness and risk assessment

framework (TRRA). This is a quantitative approach [34].He argues thatTRLs fail to address the

difficulty inR&Dprogress,andtheeffortrequiredtomovefromaTRLtothenextwithinasetof

criteriaorrequirements. ThismodelbuildsonanotherpaperbyMankins[57]anddescribes the

“research and development degree of difficulty” (R&D3) as a measure of the difficulty that is

expected during the process of maturation for a technology [55]. The purpose of this is to

supplementTRLmetrics[57].Itdeterminestheprobabilityofsuccess(orfailure)foragivensetof

technologyrequirementsatdifferentstagesofdevelopment [16].TheR&D3consistsof five levels

thataredescribedinTable2.The integratedassessmentmethoddevelopedincorporatesanother

dimension, “the technologyneedvalue” (TNV) [16].TheTNV isaweighting factor that isapplied

relative to the assessment of the importance of technological development (shown in Table 2)

[16][55].

20

Theapproachassessestheprobabilityofsuccess, identifiesthegapbetweenthecurrentTRLand

targetlevelanditsR&Deffort,andthenutilizestheTNVtoassesstheimportanceoftheprogram.

The factors are then applied into a technology riskmatrix that assess the technology on amore

coherentbasis[16].

Table2.R&D3LevelsandDescriptions[57]andTNVandDescriptions[16].

R&D3 Description TNV WeightingFactor

Description

R&D3–I

Averylowdegreeofdifficultyisanticipatedinachievingresearchanddevelopmentobjectivesforthis

technology.ProbabilityofSuccessin“Normal”R&DEffort99%

TNV1

40% Technologyeffortisnotcriticalatthistimetothesuccessoftheprogram.Advancesto

beachievedareusefulforsomecostimprovementshowever,theinformationprovidedisnotneededfordecisionsuntil

thefarterm

R&D3–II Amoderatedegreeofdifficultyshould

beanticipatedinachievingR&Dobjectivesforthistechnology.

ProbabilityofSuccessin“Normal”R&DEffort90%

TNV2

60% Technologyeffortisusefultothesuccessoftheprogram.Advancestobeachieved

wouldmeaningfullyimprovecostand/orperformancehowever,theinformationprovidedisnotneededfordecisionsuntil

themidtofarterm

R&D3–III Ahighdegreeofdifficultyanticipatedin

achievingR&Dobjectivesforthistechnology.ProbabilityofSuccessin

“Normal”R&DEffort80%

TNV3

80% Technologyeffortisimportanttothesuccessoftheprogram.Advancestobeachievedareimportantforperformanceand/orcostobjectivesandtheinformationprovidedisneededfordecisionsinthenear

tomidterm

R&D3–IV

AveryhighdegreeofdifficultyanticipatedinachievingR&Dobjectives

forthistechnology.ProbabilityofSuccessin“Normal”R&DEffort50%

TNV4

100% Technologyeffortisveryimportanttothesuccessoftheprogram.Advancestobe

achievedareenablingforcostgoalsand/orimportantforperformanceforperformanceobjectivesandinformationprovidedis

highlyvaluableforneartermmanagementdecisions

R&D3–V Thedegreeofdifficultyanticipatedin

achievingR&Dobjectivesforthistechnologyissohighthatafundamentalbreakthroughisrequired.ProbabilityofSuccessin“Normal”R&DEffort20%

TNV5

120% Technologyeffortiscriticallyimportanttothesuccessoftheprogram.Performanceadvancestobeachievedareenablingandtheinformationtobeprovidedisessentialfornear-termmanagementdecisions

21

Azizianetal.[34]discusstheTRAprocessusedbytheDoDfordefenseacquisitionprograms.Itisa

six-stepprocessthat isshowninthe figurebelow.Theprocess isstartedbysettingaschedule in

order for importantmilestones tobemet [34].Theassessment thencontinuesby identifying the

criticalelements8(CTE)acrossaWorkBreakdownStructure,dataisthencollectedandpresented

toanaudience(expertsintechnology)thatisindependentoftheteam[35].Reviewersthenassess

thematurityofCTEsagainstthemetricsthathavebeendecidedonandthenpassedupforapproval

bythechainofcommand[34][35].Ifnotapproved,then,theymayconductanotherTRA[35].

InthecasewhenacomponentisnotatthesameTRLastherestofthetechnologies,theDoDmay

doanyof the following [35]:restructure theprogramso thatonlymature technologiesareused;

delay the program in order to mature the technology; change the program requirements; not

initiatetheprogramandconsideranothersolution.

Figure.6DoDTRAProcess[Adaptedfrom[34]]

8 (CTE) is defined as an element that the system being acquired depends on in order to meet

operationalrequirements[64].

SetSchedule

IdentifyCriticalElements

CoordinateCriticalElements

AssessCriticalElements:PrepareTRA

Coordinate&SubmitTRA

OversightReview

DataCollection

22

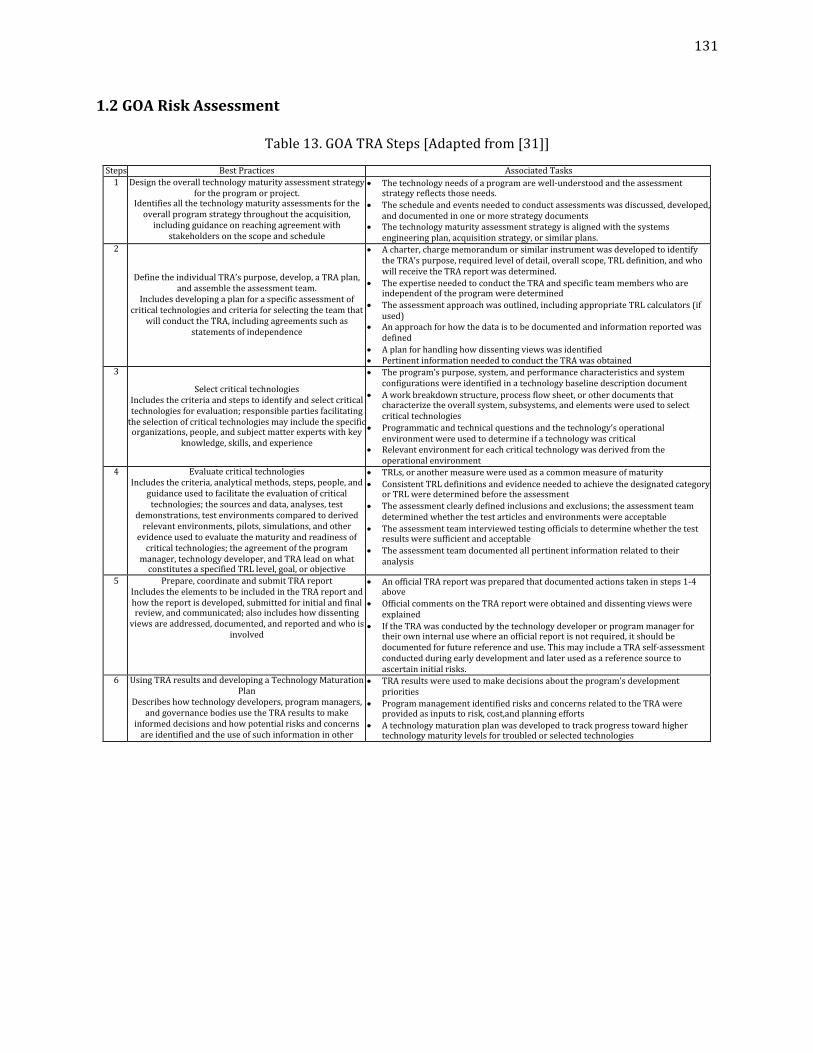

TheU.SGovernmentAccountabilityOffice(GOA)drewuponthetechniquesandpracticesatNASA

and the DoD and produced their own TRA methodology that is often called the “best practice”

[58][31].Thepublished150pageguideoutlinesthesixstepstoimplementingthismethodindetail

[31].Thesestepsaresummarized inAppendix1.Anotherapproach toconductingTRAconsiders

moreholisticmethodstoredrawtheboundariesoftheproblemsandexaminestherateatwhicha

technology can mature, and larger issues related to technology-life cycles9, specifically its

obsolescence.Formoreinformationsee[59].

2.2.3OtherTRAToolsandTechniques

SimilartotheR&D3,therearemanyothermaturityassessmenttoolsthathavebeendevelopedto

work or leverage with the TRL scale and provide insight on different aspects of technology

development[34].Theadvancementdegreeofdifficulty(AD2)isaqualitativemethodthatisargued

tobuildontheR&D3approachandpossesses9 levels that integratetheaspectsofcost,schedule,

and risk [60]. Another qualitative technique developed, is the Manufacturing Readiness Level

(MRL)createdbytheDoD[61].Itisusedtoassessthemanufacturingmaturityofatechnologyona

scale of 1 to 10 [61][62]. This can be applied during system development of a technology and

continuesafterthetechnologyhasbeeninoperationforafewyears[62].

TheSystemReadinessLevel(SRL)isaquantitativeapproachthatmeasurestheindexofmaturity

onasystem-level[63].SRLsareafunctionofTRLs(andtheirmaturities)andareexpressedbased

on the Integration Readiness Levels (IRL) [63]. The IRL scale is a 9-point scale that measures

maturityandtherelationshipbetweentheinterfacesofotherreadiness levelsandcanbeusedto

determinetheriskofintegration(whenusedwithTRLs)[63][34].

9 Technology-life cycle has four stages. It starts at theR&Dphase and ends in the decline phase

wherethetechnologyeventuallybecomesobsolete.

23

Automated tools to measure maturity are also available, where they quantitatively assess the

maturitybasedontheinformationfedbytheuser[34].Themostwell-knownbeingtheTechnology

ReadinessLevelCalculator[58](andMRLcalculator).ThisisaMicrosoftExceltoolthatcalculates

the TRL level as an output at a specific time [58]. The calculator provides no information about

risksor theprobabilityofsuccessbutcangivemanagementageneral ideaabout therisk(as the

assumptionisthehighertheTRL,thelowertheoverallrisk[39]).

2.2.4LimitationsofTRLs

There can be a biaswhen conductingTRLswhere different priorities andmetrics for success or

levelsofacceptableriskcanplayafactorinwhichchoicesaremade.Thisincludesoptimism,which

can affect TRA results. Managers may also be tempted to accept higher risks and immature

technologies in hopes of future performance and stakeholder buy-ins [31]. In the case where a

technology is not developed at every level10, the risks related to skipping these levels should be

assessedagainstthecost[39].TRLsalonearenotsufficientasanentireframeworkfortechnology

and risk management. As discussed, many other complementary methodologies have been

introduced in order to better identify uncertainties during research and development, to take

actionupontheseuncertaintiesandtodeveloplong-termtechnologyopportunitiesbasedonneeds

[45][55]. Some other issues identified in literature include improper assessment of methods to

integrate two technologies, or an individual component of a system and the measurement of

uncertainty during the maturation process [47][46][36]. In addition, the lack of ability to

comparatively assess the alternate TRLs on the entire system [47], and failure to consider

technologyaging(obsolesce)[64].

10Managerscanchoosetoskipalevel;thisiscalledleap-frogging.

24

Finally, a paper published in 2015 by Olechowski et al. [36] identified amajor challenge as the

failuretoalignTRLswithtechnologydevelopmentstage-gates.Theyacknowledgethefactthatthe

aligningispracticedinindustry;however,arguethattherehasbeenlimiteddiscussionaboutthisin

theacademicworld.Theyarguethatthelackofpropermappingdoneinindustryandprocessesof

determining the minimum acceptable TRLs is related to the lack of understanding of the

consequencesofmissedmilestonesandreachingtargetTRLs11.

2.3TechnologyRiskManagement

2.3.1RisksinR&D&TechnologyDevelopment

There is a significant amountof risk that canbeexpectedduringanew technologydevelopment

project[27].ThereisalargeamountofliteraturethatidentifiescommonrisksassociatedwithR&D

andhigh-technologyprojects.However,thereisaweaknessinaligningtheserisksalongthestages

of development for a technology project and identifying trends of how one risk might affect

another.Thissectionhighlightsthemajortypesandcategoriesofrisksonagenerallevel.Chapter3

willapplythetopicssummarizedinthissectionanddiscussitinarelevantcontextthatbuildson

the framework inamanner thatcanbemappedoutalong technologystagesofdevelopmentand

generalcorrelationsofhowrisksmayberelated.Appendix1listsexamplesofpotentialrisksthat

mayariseduringdevelopmentasoutlinedby[65].

Thereisaninherentdifferencebetweenriskanduncertainty.Risksaredescribedasthedegreeof

whichanuncertaintyandlossmayoccurinanevent[32].Thereforeriskisaquantifieduncertainty

andoutcome[66].R&Dprojectsarelabeledas“risky”iftheprobabilityofabadoutcomeishigh,the

ability to control the risks within time and resource constraints is difficult, and if the potential

impact of the consequences is substantial [65]. The high uncertainty in R&D leads to high risks,

which may lead to project failure. Improving R&D probability of success requires managers to

controlrisksduringallstagesoftheproject[5].

11GoogleandJohnDeereweretheexamplesdiscussed.

25

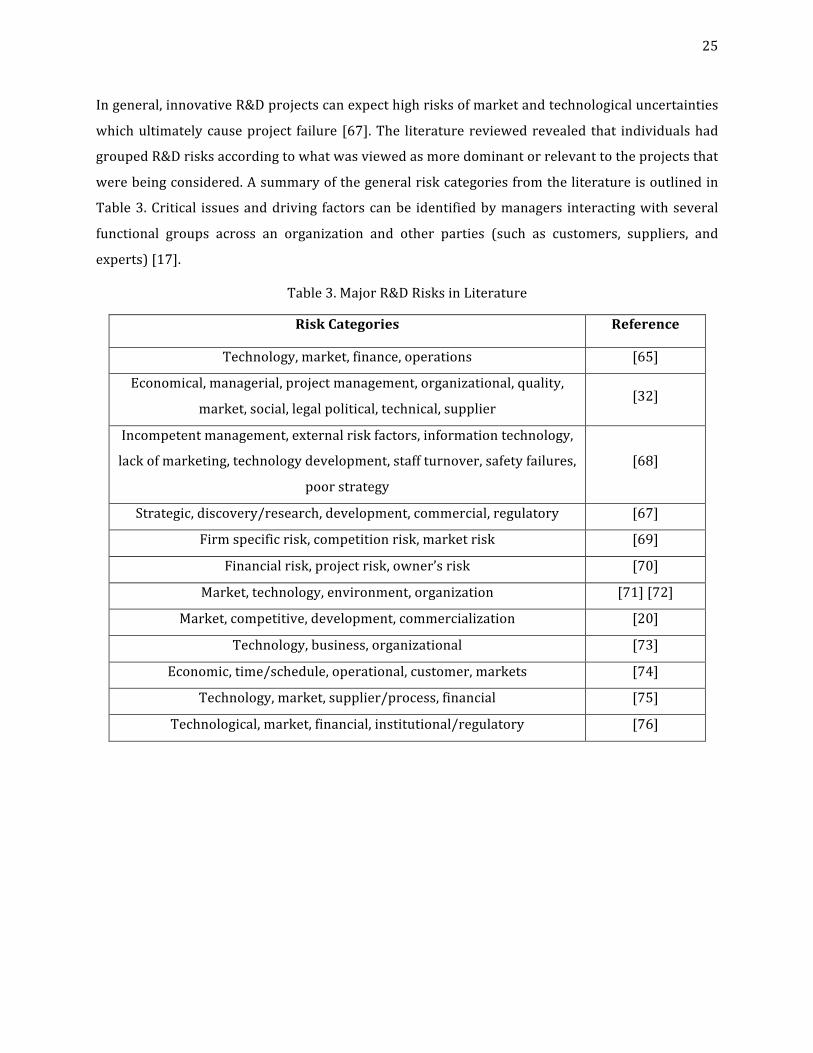

Ingeneral,innovativeR&Dprojectscanexpecthighrisksofmarketandtechnologicaluncertainties

whichultimatelycauseproject failure [67].The literaturereviewedrevealed that individualshad

groupedR&Drisksaccordingtowhatwasviewedasmoredominantorrelevanttotheprojectsthat

werebeingconsidered.Asummaryofthegeneralriskcategoriesfromtheliteratureisoutlinedin

Table3.Critical issuesanddriving factorscanbe identifiedbymanagers interactingwithseveral

functional groups across an organization and other parties (such as customers, suppliers, and

experts)[17].

Table3.MajorR&DRisksinLiterature

RiskCategories Reference

Technology,market,finance,operations [65]

Economical,managerial,projectmanagement,organizational,quality,

market,social,legalpolitical,technical,supplier[32]

Incompetentmanagement,externalriskfactors,informationtechnology,

lackofmarketing,technologydevelopment,staffturnover,safetyfailures,

poorstrategy

[68]

Strategic,discovery/research,development,commercial,regulatory [67]

Firmspecificrisk,competitionrisk,marketrisk [69]

Financialrisk,projectrisk,owner’srisk [70]

Market,technology,environment,organization [71][72]

Market,competitive,development,commercialization [20]

Technology,business,organizational [73]

Economic,time/schedule,operational,customer,markets [74]

Technology,market,supplier/process,financial [75]

Technological,market,financial,institutional/regulatory [76]

26

Technologyriskscanbedescribedasthoserelatedtodesign,platformdevelopment,manufacturing

technology,IP[65],andtechnologylife-cycles[77],whiletechnicalrisksaredefinedasthetechnical

issues that comeupwithnew technologies (suchasglitches) [78].Otherexamplesof technology

riskelements includenotreducingthetechnologytopracticeorfailuretodemonstratefeasibility

[78],ortheabilitytoremainfeasibleleadingtobecomingobsolete[69].Technologyandtechnical

risksareimportantduringtheearlydevelopmentstagesofatechnologyastheyhaveaninfluence

onmilestones and feasibility. ThoseR&D firms that are able topossess technologieswithhigher

capabilitiesgenerallytendtohaveinvestorsthatlookforqualitiessuchasafirm’sabilitytomeet

technologychallenges[24].

Technicaluncertaintiesmaycreatepressureonmanagerstoinvestinordertolowertherisk[79].

Thelogicbehindthisisthatdelayinginvestment(i.e.actionsanddecisionstomitigatetheserisks)

may cause exposure to an increase in competition [79] and delayed market entry

(commercialization) could result in significant failure, as competition that possesses the right

resources may act quicker and enter the market (competitive risk) [69]. However, aggressively

enteringamarket tooearlymayposemanychallenges suchas large increases in costdue to the

infrastructure needed [79]. Another risk could be competition’s response to the new technology

launch, as their actions (releasing similar or better products) could destroy a firm’s competitive

advantage [69]. These competitive risks that could arise are directly related to actions by

competitorswhichcancausevaryinglevelsoflossesinprojectopportunities[69].

Manufacturingtechnologyrisksarealsoimportant,forexample,properscale-up(andthepotential

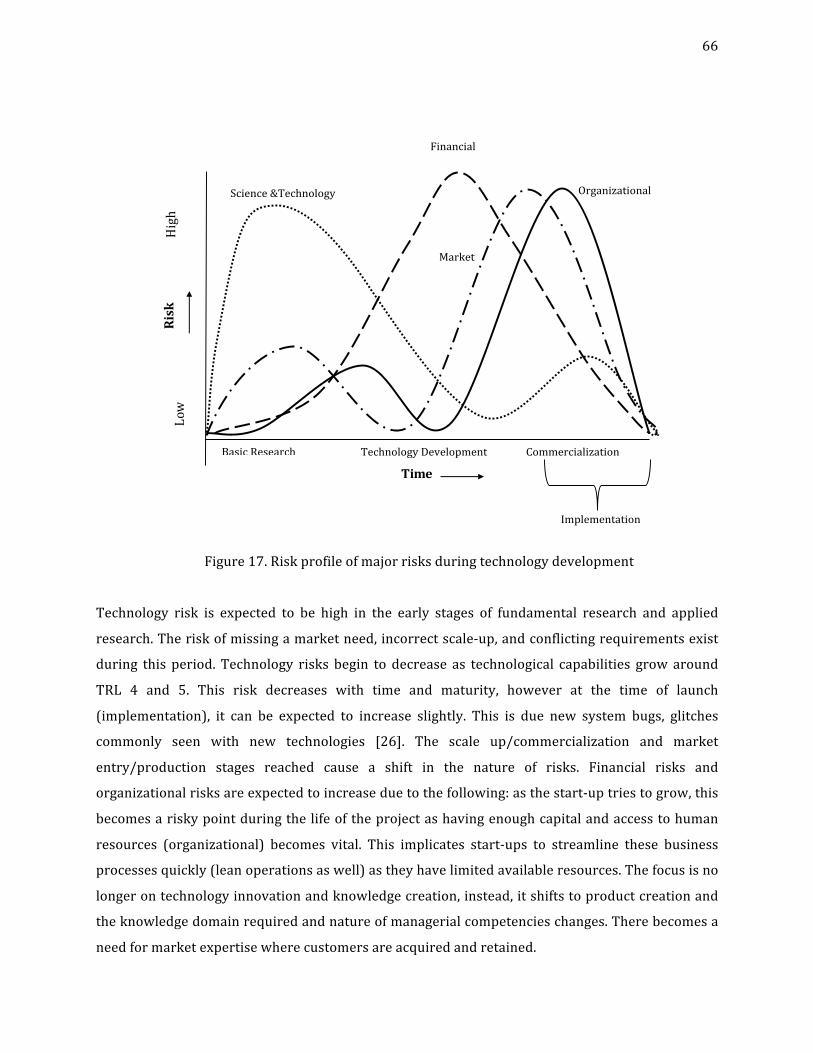

forscale-up)[65]isnecessarytoachievesuccessinlaterstages[65].Figure7illustratesthegeneral

trend for technology risk12 as technologiesmature acrossTRLs, as suggestedbyBatkovsky et al.

[12]. The figure depicts an increase in investment in funding requirements as higher TRLs are

reached.TheactualgrowthtrendasTRLsincrease(i.e.linear,exponential,etc.,)isnotreflectedin

Figure7.

12 The paper [12] only showed a table that outlined the relative qualitative magnitudes of risk

acrosstheTRLs.

27

Figure7.TechnologyRiskAcrossTRLsforHighTechnologies

Market risks can be characterized to be of any or a combination of the following: customer

demands, regulatorychanges thatmay influencedemand,customeracceptanceandadoption, the

effectofcompetitorsstrategiesandtheriseofnewerandcheapertechnologies[65][69].Wangetal.

[20]discussthatwhenhighmarketuncertaintiesarepresent,managersarestillatrisktoproperly

match market requirements, even with managerial flexibility. They advise that organizations

exercise their efforts to obtain reliable information about the market so that the range of their

optionstoreduceuncertaintycanproperlybeassessed[20].Theyalsoemphasizetheimportance

ofmaximizingmarket research capabilities as they argue evenwithwell thought-out technology

planning methodologies, a high market uncertainty will reduce any chances of capturing

opportunities [20] Often, managers are unsure of the market opportunities for a particular

technology [32]. Ifa firmhasaccess todataon thepotentialcustomers, competition,distribution

channels and other market information, then this can contribute to market uncertainty being

loweredoverall[32].

Market risks can be either strategic or operational and although different, there can be overlap

betweenthetwo[76].Operationalriskscanbemanagedbyprojectmanagerswhilestrategicrisks

moreoften thannot, require the involvementofhigherexecutives (suchasaboardofdirectors).

[76].Successfulcommercializationofatechnologyisdependentonthepresenceofamarketneed

andtheabilitytostrategizeaccordingly[80].Propermarketingstrategieswillexplorepositioning

opportunitieswithin themarket and devise action plans to gain a competitive advantage and to

maximizethevalueofaparticulartechnology[80].

TRL1 TRL3TRL2

TRL4 TRL5

TRL6 TRL7 TRL8 TRL9

Increasingcost

Absolutelyhigh

Extreme

lyhig

h

Veryhigh

High

Mediu

m

Low

VeryLow

Technologyrisklevels

28

Thiscalls forsomeonewithmarketingexpertise thatwouldbeable toconduct thisallwithin the

organizational (internal) and external constraints [80]. Formulation of marketing strategies for

early stage technology projects is an important milestone [80]. The concepts behind marketing

which strategies to select and when are outside the scope of this thesis. However, they are

recognizedasanimportantaspectofdevelopmentthatshouldbestudiedandconsidered.

Financeorfinancialrisks13canrefertotherisksassociatedwiththelimitedfinancingavailablefor

development in a project [69][76] and the challenges associated with obtaining funding for a

project[70].Thisisanimportantcategoryofrisk,astheavailabilityoffundingiscriticalincapital