59

Real Options Mehmet Bozbay Hoksung Yau Laura Goadrich Ping Fong Hsieh Sirisha Sumanth March 8, 2004

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | olivia-couse |

| View: | 216 times |

| Download: | 0 times |

Real Options

Mehmet Bozbay

Hoksung Yau

Laura Goadrich

Ping Fong Hsieh

Sirisha Sumanth

March 8, 2004

Chapter 4: Getting Real About Real Options

Objectives

Overview TerminologyReal options in the Real world

Overvaluing options (Agouron) Exploring options (Cisco) Case study (Nole)

Summary

Issues in Real Options

Advantages: Successfully explains valuation of multiple

companies believed to have substantial real options Explain some of the difference in markets not

accounted by traditional techniques Disadvantage:

Real Options can be miscaluculated/misused and misvalue a company

Provides a method to exemplify market outcomes using nontraditional techniques

Overview: Real Options

Helps investors determine whether a company’s stock is over- or undervalued

Real options considers impact of: Risk New technology New market …

Real-World Examples: Agouron Pharmaceuticals, Cisco, Nole

Terminology

Scope-up options Opportunities to increase variability in product lines Eg. IBM expanding to create graphic cards

Scale-up options Opportunities to expand capacity Eg. Power Packaging took over one plant of General Mills

Learning options Opportunities to acquire companies with the goal of entering

into new businesses Eg. GE taking over Datex-Ohmeda

Equity Stakes Purchasing equity in start-up companies

Real-World Example: Agouron Pharmaceuticals

Kellogg & Charnes (2000) Financial Analysts Journal

Illustrates the problem of valuing a company with real options and how that valuation can differ from the market’s valuation

Background: biotechnology companies known for having high values when their products are in development (no positive cash flow)

Real-World Example: Agouron Pharmaceuticals

Types of real options available Growth option

Expand production if favorable in the market Abandonment option (why choose?)

Viable reasons for abandonment • inhibit share holder loss• scrap failing projects• …

Real-World Example: Agouron Pharmaceuticals

Real World Example: Agouron Pharmaceuticals Valuations of Agouron based on real options differed from

the actual market values of the company’s stock as a particular drug progressed through the development process Discovery Preclinical Clinical trial- phase I Clinical trial- phase II Clinical trial- phase III FDA filing and review

Once the drug hit the market, the drug can vary in quality from Breakthrough - Above Average - Average - Below Average - Dog

Real World Example: Agouron Pharmaceuticals Root cause of differences:

The abandonment of a drug is rarely announced Only one drug made it to phase II and III Potential projects were included in the valuation when they

were not part of the product pipeline Investors were making different assumptions

Political pressure for FDA to approve drugs for HIV-positive patients

Assumed need less than eight years from phase II to launch, but only took two years

Sales were four times expectations in the first year Lesson: real options were not overlooked by the

market, but may have been overvalued

Real-World Example:Cisco Basics

Sell: Networking supplies Scale-up options

Supply network equipment for Internet connectivity

Scope-up options Supplies businesses and individuals

Learning options Integrating voice, video and data in their network

Real-World Example: Cisco Example Traditional discounted cash flow example Market Value (FY 2000): $445.1 billion

Assumptions: Earnings will grow at a rate of 10% annually after 2005 The risk-free rate is 5% The market risk premium is 6% There is no adjustment for earnings after 5 years

Real-World Example: Cisco Evaluation

billionbillionTermValue 800.448

)10.0137.0(

)10.01(093.15$2005

CostOfCapital = riskFreeRateOfInterest + riskPremiumOfMarket * Volatility = 5% + (6% * 1.45) = 13.7%

Real-World Example: Cisco Sensitivity Analysis

DCF = $266.565billion vs. Market Value= $445.1billion Difference: $178.535billion

Sensitivity Analysis Vary constant growth rate of 10% to 11% DCF – MarketValue = $91.061million

Vary cost of capital from 13.7% to 16% Difference: $284.873million

Lesson: Not considering options poorly represents the actual market value.

Real-World Example: Nole Background

Example illustrating valuing an option. Initial start-up costs

capital expenditures $500million investment in working capital $50million

Depreciation & capital expenditures $100million/year

Option 1: Not expand Revenues

Y1 $1billion Y2 $1.2billion Y3 $1.44billionY4 $1.526billion Y5 $1.617billion Y6 $1.715billion

Real-World Example: Nole ChoicesOption 2: Expand in year 3 with $2billion

Annual depreciation $200million Expenditures

Annual capital expenditures year 4, 5, 6 each $100million

No additional capital expenditures Revenues

Y1 $1billion Y2 $1.2billion Y3 $1.44billion

Y4 $1.9billion Y5 $2.47billion Y6 $3.211billion

Real-World Example: Nole Expanding in Y3, init Y0

Real-World Example: Nole Without Expanding in Y3, init Y0

Real-World Example: Nole Value of Expanding Option

Real-World Example: Nole Strategic Value

Real-World Example: Nole Expanding Black-Scholes

Value of option= P x N(d1) – X x e –r x t x N(d2)

= $1,231 x 0.4678 – $2,300 x e-6% x 3 x 0.1718

= $245million

Value of Expansion Option using DCF = -$31million

termValueowueOfCashFlpresentValP

Real-World Example: Nole Volitility

Real-World Example: Nole Variability of Volatility

Increasing volatility

increases cost of capital

decreases value of underlying

decreases value of option

Summary

Agouron showed a large difference between real world valuations and traditional methods.

Cisco illustrated the positive impact of using options.

Nole compared the valuation traditional verses options and clearly expressed the need for options to describe the marketplace.

Chapter 5: Pitfalls and Pratfalls in Real Option

Valuation

Complication from Internal and External Interactions

Interaction between option holders and underlying asset’s value can complicate the analysis of real option.

Inability to Explain Absurd Valuation The options a company has are usually not independent

with each other. Their values are not additive. It’s questionable whether the presence of real options can explain the absurd price that were witnessed in recent years for many Internet stock.

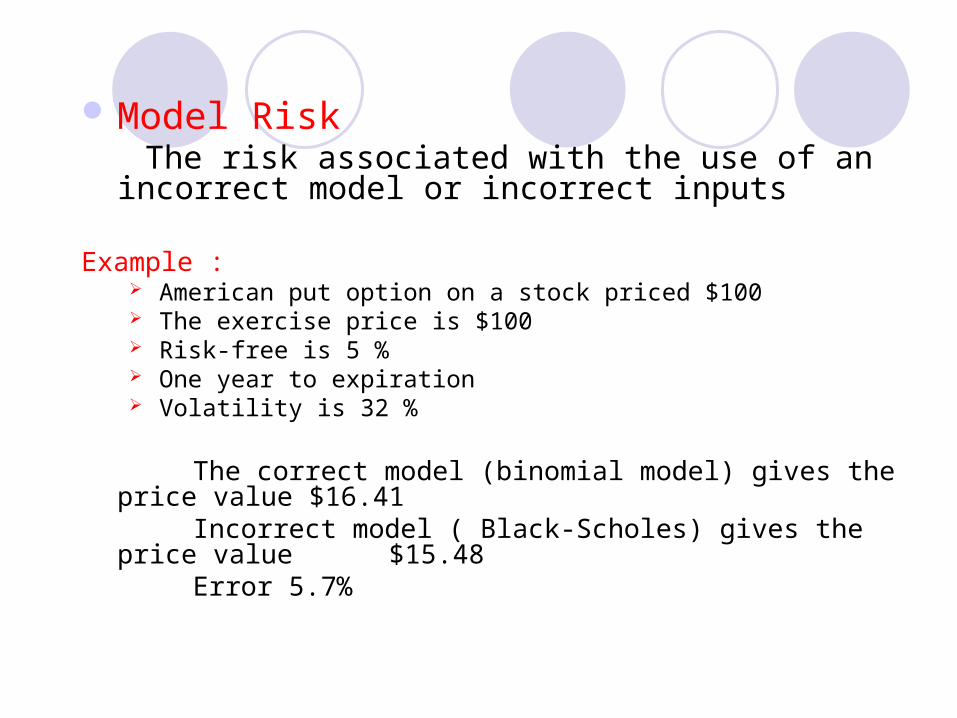

Model Risk The risk associated with the use of an incorrect model

or incorrect inputs

Example : American put option on a stock priced $100 The exercise price is $100 Risk-free is 5 % One year to expiration Volatility is 32 %

The correct model (binomial model) gives the price value $16.41 Incorrect model ( Black-Scholes) gives the price value $15.48 Error 5.7%

Failure to meet Assumption Major Assumptions Lognormality Randomness

Known and constant volatility

Minor Assumptions Known and constant risk-free rate No taxes and transaction costs American-style option

Major Assumptions

Lognormality The rate of return on the underlying asset is lognormally distribution.

Example: A non-dividend –paying stock sells for $100 and moves up to $110 after one

year. The logarithmic return is ln(1.10) = 9.53% The model typically assume the logarithmic return follows a normal

distribution, which means the return itself follows a lognormality distribution

Randomness Prices are randomness to assure that markets are competitiveness that allows

pricing models to work. No one participant can dominate all the others.

Known and constant volatility The volatility in standard option-pricing models is not directly observe and easy

to obtain. Also, the models are sensitive to the volatility.

Minor Assumptions1. Known and constant risk-free rate

Option-pricing models generally assume a known and constant risk-free rate.

2. No taxes and transaction costs

It facilitates the capture of most essential elements of the economic process being modeled.

3. American-style option

The option is the one that can be exercised before

expiration. It offers more flexibility.

Difficulty of Estimating Inputs 1. Market Value of the Underlying Asset Sometimes, the estimating for appropriate discount rate, the life of a

project may be difficult. 2. Exercise Price The amount of money can be received or paid in the future are difficult

to determine.

3. Time to Expiration A company can’t know how long it can keep a project before

abandoning it to claim a salvage value.

4. Volatility The option prices are very sensitive to the estimate of volatility. But it is

very difficult to observe in financial option-pricing application.

5. Risk-Free Rate The value of an option is not so sensitive to estimate of the risk-free

rate.

It is acceptable to obtain an estimate of the risk-free rate by estimating the rate on a default-free zero-coupon security.

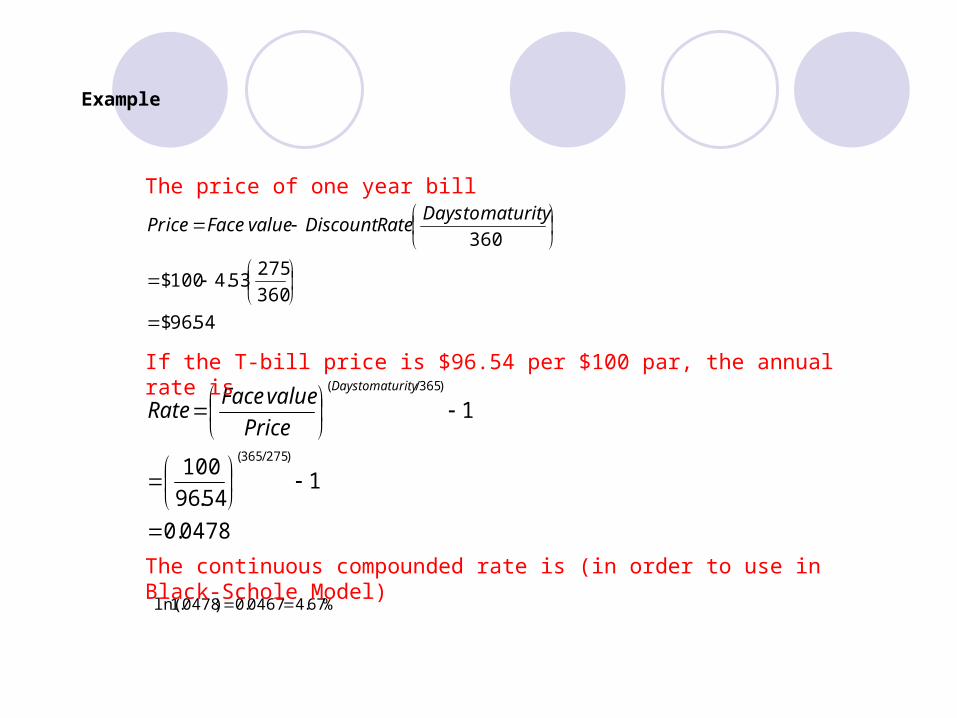

Example

A real option expires in 275 days

Let the bid and ask discount rates on US government zero-coupon bonds (Treasury Bills) for maturity be 4.52% and 4.54%

We spilt the difference and assume a rate of 4.53%

Example

54.96$

360

27553.4100$

360

maturitytoDaysRateDiscountvalueFaceicePr

0478.0

154.96

100

1

)275/365(

)365/(

maturitytoDays

Price

valueFaceRate

%67.40467.0)0478.1ln(

If the T-bill price is $96.54 per $100 par, the annual rate is

The continuous compounded rate is (in order to use in Black-Schole Model)

The price of one year bill

Nontradability of the Underlying Asset

Assumption in the area of real options analysis: underlying asset can be bought and sold in a liquid market.

When using binomial approach, the ability to trade the asset and the option in such a manner that no arbitrage opportunity exists is the glue that binds the models together.

Assumptions of Hedging, Tradability, and Risk Neutral Valuation

r: Risk-free rate (5%) u: Holding period return on the stock if it goes

up ($150) d: Holding period return on the stock if it goes

down ($50) Stock price: $100

55.05.05.1

50.005.11

du

drp

Option price calculation

19.26$05.1

)0($45.0)50($55.0

c

Risk-adjusted discount rate and probability of outcomes

If the probability of up move is 0.6, then Risk-adjusted discount rate k = 0.1.

If k = 0.12, then q=0.62.

k

1

)50)($1()150($100$

Risk-adjusted discount rate and probability of outcomes (cont.) If k is risk-free rate, then

q plays the same role as p in the option-valuation problem. Option-pricing models are often said to use risk neutral valuation.

pq

q

55.005.1

)50)($1()150($100$

Consistency of All Approaches

No one assume investors are risk neutral. Rather, risk neutral valuation is simple and imposes only light demands.

Risk neutral valuation is not a different approach that obtains different numbers from a standard risk-adjusted approach.(Feinstein 1999)

Example

Invest $9 in a project If the outcome is good, invest $18 and begin to

generate $10 a year forever. If the outcome is bad, invest $18 and begin to

generate $3 a year forever. Probability of good outcome is 0.6 and bad

outcome is 0.4 Discount rate is 25%

Example (cont.)

The market value of the project is:

The market value of the project at time 1 is:

12$25.0

3$

or 40$25.0

10$

1

1

B

G

V

V

6$18$12$

or 22$18$40$

1

1

B

G

X

X

Example (cont.) The value of the project at time 0 is:

NPV is

Up factor:

Down factor:

The risk neutral probability is

64.8$25.1

)]6.0$(4.0)22($6.0[0

V

5463.264.8

22$u

6944.064.8$

6$

d

5383.0)6944.0(5463.2(

)6944.0(05.1

p

36.0$9$64.8$

Example (cont.)

Option value $11.28

According to Feinstein’s approach, the overall discount rate is a blend of 25% and 5%. So the weighted discounted rate is:

The correct project value is

$11.28

05.1

)0($4617.0)22($5383.0

0.1704

1)0($4617.0)22($5383.0

)05.1)](0($4.0)22($6.0[

1- )1(

)1]()1([

11

11

BG

BG

w XppX

rXqqXk

1704.01

)0($4.0)22($6.0

Summary

One source of difficulty in applying real options valuation is the assumption may or may not be appropriate in the case of real options (lognormality distribution of the value of the underlying asset, randomness of prices)

The estimation of inputs, such as the volatility of the value of the underlying asset, the exercise price, the time to expiration, is more challenging for real options than for fincial options.

Chapter 6: Empirical Evidence on the Use and Accuracy of

Real Options Valuation

Paddock, Siegel, and Smith (1988) – Option Valuation of Claims on Real Assets: The Case of Offshore Petroleum Leases

Real options model for valuing offshore oil and gas leases in a federal sale of 21 tracts in the Gulf of Mexico.

Real options were not able to explain the bids as well as one might have hoped. Real options theory was not very well-known in 1988. Data provided by the government were not too good

to carry out analysis. Winner’s curse – tendency for the highest bidder to

pay more than fair

Quigg (1993) – Empirical Testing of Real Option-Pricing Models

Market prices of 2,700 land transactions in Seattle during 1976-1979. Market prices reflect a premium for the option to wait

to invest (optimal development) that has a mean value of 6% of the land value.

Supports the belief that investors either use real options models or trade in such a manner that their valuations are consistent with those of real options models.

Berger, Ofek, and Swary (1996) – Investor

Valuation of the Abandonment Option Whether investors price the option to abandon a firm

at its exit value.

This option is priced as an American put, whose value increases with exit value. Significant relationship between a company’s market

value and its estimated exit value, suggesting that investors take the option to exit into account when valuing companies.

The more likely the option will be exercised, the more valuable is the option.

Hayn (1995) – The Information Content of Losses

Hypothesizes that because shareholders have a liquidation option, losses are not expected to perpetuate. They are thus less informative than profits about the firm’s future prospects. The results are consistent with the hypothesis. Investors do not respond to losses to the same

magnitude that they do to profits. Option to liquidate is valued by investors.

Moel and Tufano (2002) – When Are Real Options

Exercised? An Empirical Study of Mine Closings

The flexibility that mining firms have to open and close mines. The overall pattern of closures is well predicted by real

option theory. Closures are influenced by the price and volatility of gold,

firm’s operating costs, proxies for closing costs, and the size of reserves.

Fail to capture aspects of firm-level decision making. Divisions within a firm share a common destiny and

decision about particular units are influenced by the performance of the other parts of the firm.

Clayton and Yermack (1999) – Major League Baseball Player Contracts: An Investigation of the Empirical Properties of Real Options

Contracts negotiated between professional baseball players and teams to investigate the use of real options in a commercial setting.

Baseball contracts feature options in diverse forms, and they found that these options have significant effects on player compensation. As predicted by theory, players receive higher guaranteed

compensation when they allow teams to take options on their future services, and lower salaries when they bargain for options to extend their own contracts.

The apparent value of options decreases as a function of the "spread" between option exercise price and annual salary and increases as a function of the time until exercise.

Howell and Jagle (1997) – Laboratory Evidence on How Managers Intuitively Value Real Growth Options

Asked managers series of questions on growth options from some investment case studies, asked other questions related to their personal situations and the kinds of investment decisions they make in their work. Skilled managerial decision makers agree only approximately with

real option theory. They tend on average to value growth options in an erratic way. Overvaluation seems to be a function of “Industry”, being lowest in

the oil industry, and it is also a function of (Business) “Experience” and “Position” being highest for more senior people.

The result can be interpreted in two ways: This limited sample of managers is not sufficiently knowledgeable

about real options models. Real options models are simply not used in practice. Small sample size is a major limitation of this study (82 managers)

Busby and Pitts (1997) - Real options in practice: an exploratory survey of how finance officers deal with flexibility in capital appraisal

Dissatisfaction with discounted cash flow techniques has lead to a growing literature focusing on the value of managerial flexibility in handling real asset investments, a subject area known as real options.

An exploratory survey of senior finance officers in industrial firms, examining the significance that real options assumed in their investment decisions, whether their firms had established procedures for assessing real options, and whether their intuitions were consistent with what theory prescribes.

There was wide variation between individual decision-makers in their perception of real options.

Few firms have procedures to assess options in advance. Very few decision-makers seemed to be aware of real option research but,

mostly, their intuitions agreed with the qualitative prescriptions of such work.

Chapter 7: Summary and Conclusions

Companies are often highly misvalued in the market Corporate investment decisions are typically made

using standard discounted cash flow (DCF) techniques, which are not equipped to accommodate real options

Discounted cash flow techniques that attempt to capture flexibility are not adequate

The valuation of financial options has benefited from years of study, evolving from the binomial and Black–Scholes models.

A number of limitations and difficulties arise in applying real options

Real options models oftentimes do not meet the assumptions inherent in the models

The estimation of inputs in real options models is particularly challenging

The models are based on the idea that one can trade the underlying asset and the option to form a risk-free hedge or trade a combination of the underlying asset and risk free bonds to replicate the payoffs of the option

Empirical research has provided some, but very limited, support for the real-world applicability of real options models

Thank youThank you