Page 1

REALE ESTATE MARKET IN CHINA:

HOUSING REFORM AND AFFORDABILITY

BY

XIE YUFEI

STUDENT NO. 12050652

A PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE DEGREE OF

BACHELOR OF SOCIAL SCIENCE (HONOURS) DEGREE IN CHINA STUDIES

ECONOMICS CONCENTRATION

HONG KONG BAPTIST UNIVERSITY

APRIL 2015

Page 2

2

HONG KONG BAPTIST UNIVERSITY

April 2015

We hereby recommend that the Project by Mr. XIE YUFEI entitled “Real estate market

in China: housing reform and affordability” be accepted in partial fulfillment of the

requirements for the Bachelor of Social Sciences (Honours) Degree in China studies in

Economics.

____________________ _____________________

Dr. Chan Hing Lin

Project Supervisor Second Examiner

Page 3

3

Acknowledgements

I would like to thank my supervisor Dr. Chan Hing Lin for guiding me through the

entire study. Thanks are also due to my family and friends for their meticulous care

and kindly encouragement.

___________________________________

Student’s signature

China Studies Degree Course

(Economics Concentration)

Hong Kong Baptist University

Date: ____________________________

Page 4

4

Table of Contents

1. Introduction................................................................................................................ 5

2. Housing Market Development in China.................................................................... 6

2.1 Chinese Housing Market before Economic Reform......................................... 6

2.2 Chinese Housing Market after Economic Reform............................................ 8

2.2.1 The First Stage (1979-1991)................................................................. 8

2.2.2 The Second Stage (1992-1997)...........................................................10

2.2.3 The Third Stage (1998-now) ............................................................. 15

3. Housing Affordability Issue..................................................................................... 18

3.1 Housing Finance Market for Individuals........................................................ 18

3.1.1 Housing Provident Fund System........................................................ 18

3.1.2 Commercial bank mortgage loan........................................................ 21

3.2 Evidence of the Rapidly Increasing Price of the Residential Housing........... 22

3.3 Reasons for the Skyrocket up of the Housing Price........................................ 23

3.4 Housing Price-to-Income Ratio Analysis....................................................... 29

3.5 Harms Caused by High Housing Price........................................................... 35

4. Major Findings and Conclusion............................................................................... 39

5. Appendix.................................................................................................................. 41

5.1 Figures............................................................................................................. 41

5.2 Tables.............................................................................................................. 43

6. References................................................................................................................ 52

Page 5

5

1. Introduction

China's housing market plays a very important role in the Chinese economy. In

recent years, the boom in real estate market surprised both the Chinese government and

the Chinese citizens. On one hand, the rapid development in housing market drives the

economy going forward, providing better residential properties to the people. On the

other hand, the affordability issue becomes a major concern by the policy makers. The

first part of this article will review the development of the Chinese real estate market

from 1949 to present. The second part of the paper will be given a detailed discussion

about the housing affordability issue.

Page 6

6

2. Housing Market Development in China

Since the founding of the New China, the housing market has always been one

of the major policy concerns to the Chinese government. The development of the real

estate market experienced two major periods. The watershed was in 1978, when the

market-oriented economic reform took place. As China was transformed from a

centrally planned economy to a market economy, the social welfare function of housing

slowly disappeared, and the nature of the housing resources gradually changed from

public goods to commodities. The Chinese government set up a lot of experimental

areas to initiate the new policies and laws, and implement the new governance to the

whole nation. The real estate market was fully privatized in 1998, marking a milestone

in the history of housing development.

2.1 Chinese Housing Market before Economic Reform

The Chinese Communist Party (CCP) came to power in 1949. In the first 30

years of the country's founding, the Chinese economy was centrally planned. Under

socialism, the work unit system (dan wei zhi) was established in the urban areas as the

principal methods of social mobilization and social control. Each work unit was

Page 7

7

strongly associated with its workers in the sense that almost everything people depend

on for a living was provided by the work unit system. Housing was one of the social

welfares that was created and distributed directly by work units to its employees. There

was no market for properties since urban land was totally owned by the state, and the

government controlled all the transactions of the lands. Thus, citizens did not buy their

housing in the market but apply for it in their work units. Work units then distributed the

housing resources according to the seniority and merits of the applicants. This process

increased the inequality among citizens since the standard of housing distribution was

not well established (Liu & Wang, 1999). Housing was not a commodity but public

goods and services, which were embedded in the social welfare system. Because of the

nature of the housing resources and its allocation process, the government invested huge

amount of money for 30 years with no return. For the housing owners, the rent was as

low as about 1 per cent of the employers' income, which was too low to cover the

maintenance cost, resulting in an increasing number of decrepit houses (Liu & Wang,

1999). Meanwhile, the government had to face the increasing financial burden. In late

1970s, the supply of housing was in severe shortage with huge amount of land being

Page 8

8

misused or left unused. People tried to apply for as many land as possible, since land

use was actually free of charge with no time limit in usage. The chaos in the housing

market created many problems. Because of the heavy financial burden, the

infrastructure constructions such as transportation, telecommunication, and water

supply and drainage was left underdeveloped in city areas, lowered the living conditions

of urban residents (Man, 2011). The result indicates that the government was not able to

supply cheap and well-built housing for its citizens in the long run. The housing market

needed changes urgently.

2.2 Chinese Housing Market after Economic Reform

1978 is a critical year for Chinese economy. Deng Xiaoping launched the

market-oriented economic reform, which brought dramatic changes to the country's

economy in every aspect. Since then, the real estate market gradually formed with the

commercialization of housing development, allocation, distribution, exchange and

maintenance. The process of the housing market reform can be separated into three

stages.

2.2.1 The First Stage (1979-1991)

Page 9

9

In 1979, the central government selected 5 pilot cities to do the initial housing

reform experiment by selling newly built public housing to residents at the construction

cost. In 1980, the central government passed the proposal, which allows private housing

ownership, building and purchasing. Transactions were allowed for both newly

constructed housing and existing ones. In the same year, Shenzhen acted as the first

special economic zone to implement the time limit of land use period with the

imposition of land use fees (Liu & Wang 1999). Guangdong provincial government

classified the land in Shenzhen into different grades, each with a certain standard of

charging (Chai, 2008). The positive result led to the imitations of another several pilot

zones including Guangzhou and Fushun in the following years, indicating a nationwide

commercialization of urban housing system (Liu & Wang, 1999). In 1984, the Chinese

government classified the real estate industry as an independent industry in the official

document titled Economic Industrial Classification Codes and Standards (Chai, 2008).

Since then, the foundation of the real estate market was established.

In addition to imposing fees on the use of land, the paid transfer of the right to

land use was further allowed in 1988 due to the amendment of the constitution and the

Page 10

10

Land Management Law. The experiments were undertaken in Shenzhen, Shanghai and

Guangzhou, where the rights to state-owned land use were traded between the

government and both the domestic and foreign real estate developers in forms of auction,

bidding and agreement (Liu & Wang, 1999). Cities such as Zhuhai and Xiamen

followed the trend, starting transfer the right to land use. They also made specific laws

in order to bring order to the right transferring market (Chai, 2008).

In September 1988, the State Council imposed the experimental urban land use

tax. All corporates and individuals who involve in the use of state-owned lands should

pay the tax. Some additional regulations related to the housing market were issued by

the State Council in 1990, forming the legal basis and framework of future reform (Chai,

2008). However, in 1989, the political environment in China was highly unstable. The

economic development in China was negatively affected by some social movements and

its side effects. The housing market also cooled down in 1989 and 1990 compare to the

previous years.

2.2.2 The Second Stage (1992-1997)

Page 11

11

The second stage of the evolution is from 1992 to 1997. In this era, the

economic downturn recovered rapidly as the social and political environment became

more stable. Although work unit still partially participated in the construction and

distribution process of housing to their employees, the commercializing of property

market was regarded as the main trend of the real estate market development. Overall,

the development was overheated at first, and then became more steadily after 1994.

In 1992, Deng Xiaoping's famous Southern Tour Speech accelerated the

development of the Chinese housing market. According to Deng, China would continue

to open its economy, and the real estate market was one of the major focuses in the

tertiary industry. His speech brought a turning point to the Chinese housing market. As

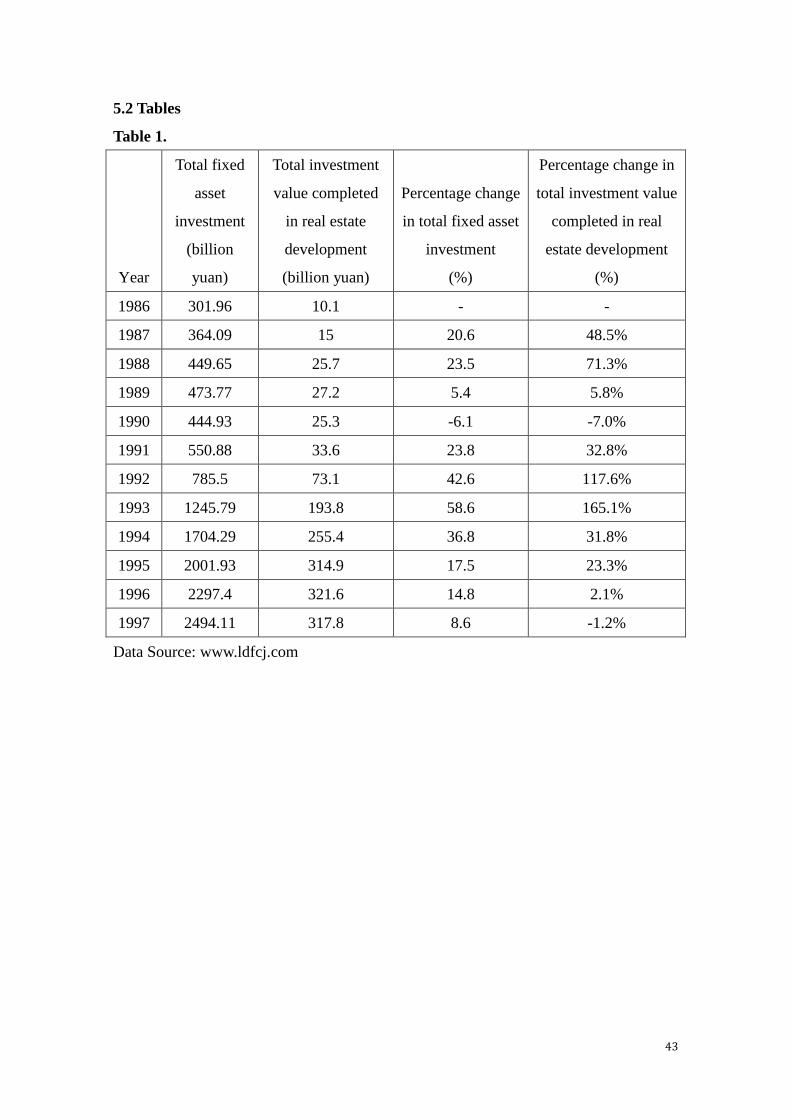

refer to Table 1, the average investment value in housing development was 22.8 billion

yuan from 1986 to 1991. Only three years after Deng's announcement, the figure

skyrocketed to 314.9 billion yuan in 1995, which was 15 times larger than that of 1991.

The annual growth rate of the housing investment was 117.6 per cent in 1992 and

reached its peak at 165.1 per cent in the following year. Compare to the annual growth

rate of total fixed asset investment in the same period, the housing sector outperformed

Page 12

12

with a huge gap. The changes in total investment value completed in real estate

development for year 1986 to 1997 is illustrated in Figure 1. A huge jump in investment

value can be easily observed during 1991 to 1995. The trend both before and after the

over-heating period is relatively steady. To better observe the abnormal development

speed of the housing market, another comparison between the year on year changes of

the total investment completed in real estate industry and the total fixed asset

investment is plotted in Figure 2. The red line, which represents the property market, is

significantly higher than the blue line between 1992 and 1994.

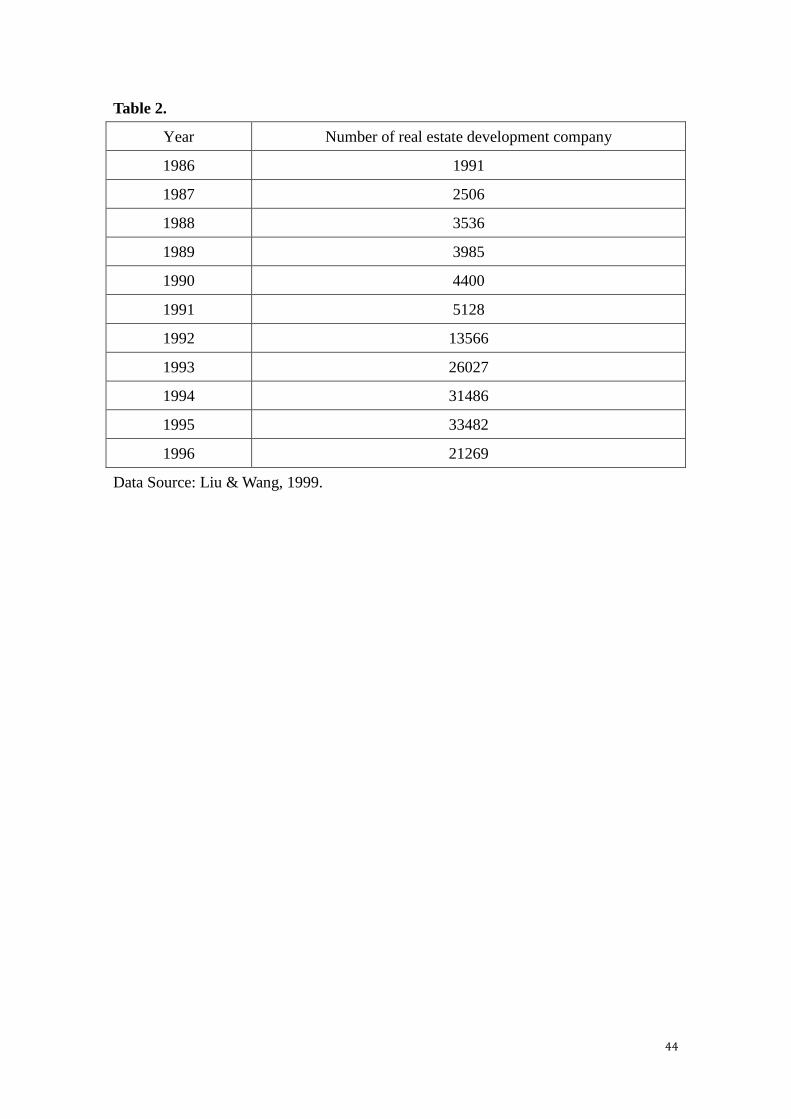

In addition to the investment heat, the number of company involving in

property development also increased dramatically. According to Wang and Liu (1999),

there were only 5128 real estate developers at the end of 1991 in China. However, more

than 8000 housing development companies were established within one year. In 1994, a

total of 31486 corporations were in the housing market across the nation. The detailed

number of real estate development company is listed in Table 2.

The evidences above clearly show a sign of overheats in China's housing

market after 1992. It is a result of both the long absence of the Chinese housing market

Page 13

13

and the further implementation of the opening reform. In practice, the rapid growth

brought some negative externalities. First, the abnormal boom in housing market

created housing bubbles. No economy could grow as fast as Chinese property market,

which means the allocation of capital was highly biased towards real estate industry.

Thus, there was an increase in the demand of construction materials like Steel, cement

and wood, resulting in higher prices of the materials. The rapid changes in prices would

further influence the demand and supply of many other commodities, making the

economy unbalanced. Second, because they are appeared overnight, most of the real

estate companies were small in size and poor in management. They allocated separately

along the coastal areas, resulting in diseconomies of scale. In order to generate higher

profit, those companies focused on the development of commercial buildings instead of

residential properties. However, the demand in office buildings was not aligned with the

supply, foreshadowing a high housing vacancy rate in the future (Wang & Liu, 1999).

Third, the behavior in the real estate market was highly irregular. The booming of the

market did not company with a sound regulatory mechanism. Many property

development companies did not focus on the needs of the society but keen on

Page 14

14

speculation. In some cases, developers did not aim to conduct construction on the land

in the first place. They simply want to resale the land to gain easy profit. Speculations

largely raised the price of housing, making the real estate market very unhealthy. The

revenue generated in the property market went mainly to the developers' hands while

affordability problem rose among coastal areas (Chai, 2008).

After 1994, the Chinese government tried to control the development of the

housing market by strengthening the macroeconomic regulations. As shown in Figure 2,

both the total investment in fixed asset and in real estate development cooled down. In

1994, 1996 and 1997, the annual growth rate of completed housing investment was

lower than that of the total investment in fixed asset, which means the real estate section

had changed from an overheating industry to a relatively normal or unpopular one. In

1997, the value of completed investment in real estate development was recorded a

negative growth of 1.2 per cent. Overall, the Chinese housing market had a relatively

stable development after 1994 till 1997.

In conclusion, the real estate market was gradually formed during the second

stage of the housing market reform. The Chinese government accumulated some

Page 15

15

experience in the housing regulation and governance, and was able to make the market

environment healthier. In people's mind, the essence of housing has been transforming

from public goods and social welfare distributed among urban employees, to

commodities that can be purchased and exchanged in the market.

2.2.3 The Third Stage (1998-now)

The third stage of the housing reform began with the total abandonment of

work unit housing distribution system in 1998. According to the State Council

Document No. 23, employers were only allowed to provide relevant subsidies to their

newly employed workers but direct involvement in the construction and allocation of

housing resources were no longer permitted. Selected middle- and low-income urban

residents could live in subsidized or public rental housing, while high-income families

should relied on mortgage financing to purchase private housing in the market (Man,

2011). Since then, the real estate market in China was fully commercialized.

In addition to the determination of the central government to form a market-driven

real estate market, the other reason for the Chinese government to speed up the housing

reform is to "foster a new point of economic growth. The idea was first proposed by

Page 16

16

Premier Zhu Rongji in June 1996, who further emphasized the residential housing

market to be the major focus point (Chai, 2008).

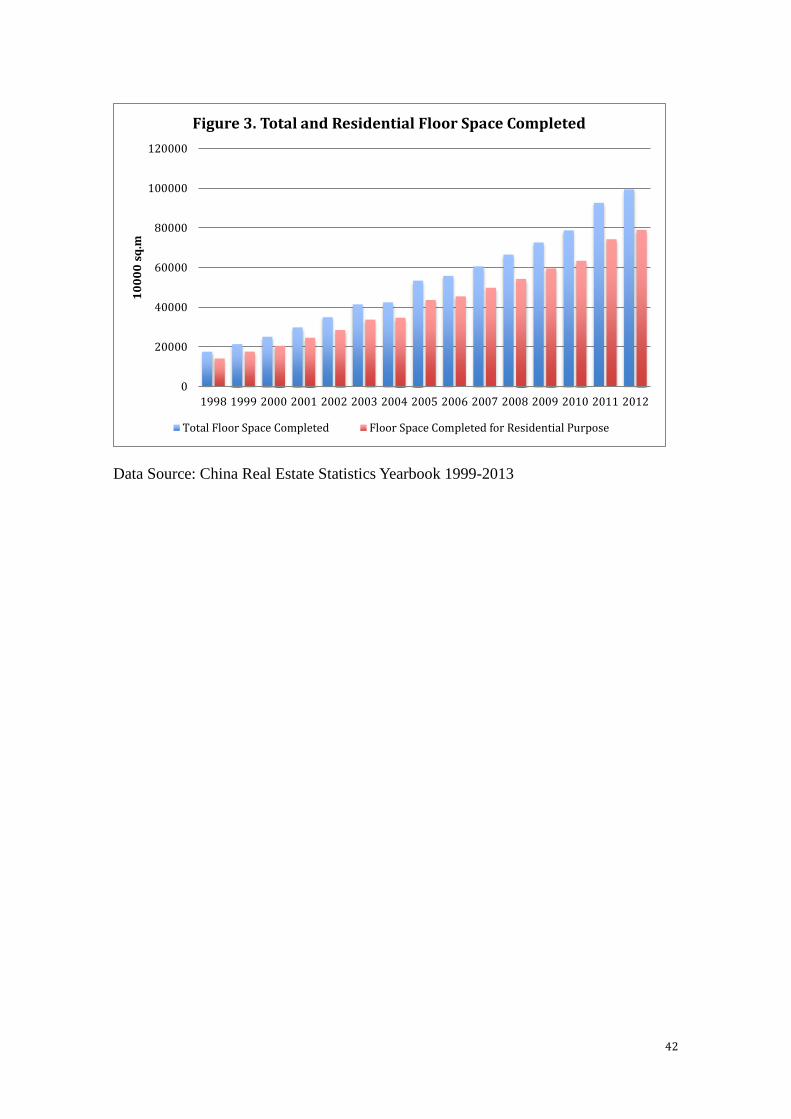

Following the government's strategy, the majority of housing construction in this

era is for residential purpose. Table 3 listed the relationship between the total real estate

development and housing construction completed for residential purpose. From 1998,

the residential housing dominated the whole real estate market. The ratio of residential

housing floor space completed has been at a very steady 80 per cent of total property

construction. The government also advocated the purchase of the new homes by

deducting several taxes charged when purchasing new estates and selling the old ones

(Chai, 2008). Due to the policy support, the figure of residential floor space completed

recoded a 13.3 per cent average annual growth rate between 1998 and 2012. A closer

look of the relationship is illustrated in Figure 3. The housing market had been

developing in a steady speed. On the other hand, the sales of residential housing had

also been increasing since 1998. Due to data limitations, Table 4 lists the sales data of

residential housing from 1998 to 2004. Each year, Chinese people buy more residential

housing than before. The sale in 2004 was 2.6 times of the number in 1998. Compare to

Page 17

17

the situation before the economic reform, urban and rural households see huge

improvement of their living conditions due to this mass provision of private housing.

The housing market in China experienced dramatic changes in the past 60 years.

The Chinese government successfully set up a privatized real estate market through its

housing market reform. The living conditions of the citizens improved a lot, and the

government no longer bears heavy burdens caused by housing resources provision. In

many sense, the housing market reform is successful.

Page 18

18

3. Housing Affordability Issue

The boom in Chinese housing market is like the two sides of a coin. On one

hand, the construction of the housing drives the economy moving forward. Urbanization

creates a lot of job opportunities for the migrant workers. The expansions in

constructions stimulate the domestic demand. On the other hand, real estate and

residential housing prices have been increasing for nearly 10 years. Many of the middle-

to low-income families are not able to afford a decent home, driving down their sense of

happiness. The second part of this article will first introduce the housing finance system

for individuals, and then discuss the evidence and reasons for the rapid increasing

housing price. Next, an evaluation of the housing affordability will be conducted by

calculating housing price-to-income ratios in 31 provinces. Finally, the article will

analyze the harms done by the high housing price.

3.1 Housing Finance Market for Individuals

3.1.1 Housing Provident Fund System

Based on Singapore's experience, housing provident fund system was set up by

Shanghai provincial government in May 1991. With the good results in Shanghai, the

Page 19

19

State Council announced the nationwide implementation of the housing provident fund

(HPF) system in China on November 23, 1994. In 1997, President Jiang Zemin

emphasized on improving the housing provident fund system during the 15th People's

Congress, making the HPF the core of policy housing finance system. Since then, the

housing provident fund was regarded as the main policy tool to enhance housing

affordability for Chinese citizens (Liu & Wang, 1999).

HPF refers to the long-term housing savings scheme deposited by the state

organs, state-owned enterprises, foreign-invested enterprises, collectively owned

enterprises, private enterprises, and other township and village enterprises, institutions

and the in-service workers. The scheme is mandatory, and all the corporates and

individuals must save into the HPF account in order to fulfill the law obligation. The

payment of HPF is on a monthly basis. The amount each worker should deposit into the

HPF account is calculated as the individual housing provident fund deposit ratio times

his or her previous year's average monthly wage. The amount each institution should

deposit into the worker's HPF account is calculated as the housing provident fund

deposit ratio of the institution times the worker's average monthly wage of last year.

Page 20

20

According to the law, both ratios should not be lower than 5 per cent (Lu, Li, & Mi,

2013). Thus, the HPF account is contributed by both the employers and the employees,

and all the money in the account belongs to the worker. Employees contributing to the

fund are eligible in provident mortgage loans applications. If the workers leave the

office or retire, the fund will be fully returned to the workers (Burell, 2006).

The housing provident fund system was set up to increase the portion of

property consumption embedded in the worker's wages in order to improve the

purchasing power when people buy the properties. However, the system has several

problems.

First, the HPF coverage is relatively low. According to Lu, Li, & Mi (2013),

about 70 per cent of the in-service workers and employees participate in the scheme all

over China in 2008. First-tier cities have better coverage rate than second- and third-tier

cities. For example, the HPF coverage rate in Beijing was nearly 100 per cent in 2010,

while in some undeveloped areas the rate was lower than 50 per cent. The reason is that

the law does not force self-employed workers and freelancers to deposit into the HPF

when they were included in the scheme in 2005. Many private and foreign enterprises

Page 21

21

also avoid contributing to the HPF, and some enterprises are unable to make regular

payments due to their financial weakness (Burell, 2006). HPF is also irrelevant to the

people who are unemployed or marginally employed, and they are actually the people

who need financial assistant the most.

Second, the value of the housing provident fund is hard to preserve. If one

chooses not to use the fund to apply for HPF loan or rant a property, the only other way

of using the money is to invest in treasury bonds. Either keep the money in the account

or buy government bonds, the real return of the fund is very low when considering the

inflation in China.

Third, HPF is not effectively used. In the end of 2011, only 65 per cent of the

fund is used to be part of the HPF loans (Lu, Li, & Mi, 2013). In other words, huge

amount of money were not used in proper ways by the citizens. Since the funds are not

allowed to pay for the down payment of the housing, people who cannot afford the

down payment will not be able to apply for mortgage loans and use the money in the

HPF account. As the funds stand idle, people do not benefit from the HPF scheme.

3.1.2 Commercial bank mortgage loan

Page 22

22

Another way Chinese citizens can use to finance their home purchase is

through commercial bank mortgage loan. Mortgage is the most popular type of housing

finance around the world. In China, it also plays the most significant role as more than

90% of mortgage loan is used for home purchasing (Gu, 2005).

The framework of mortgage lending for housing finance was set up in May

1998. The People's Bank of China issued the Regulations for Managing Individual

Housing Mortgage Loans (ge ren zhu fang dai kuan guan li ban fa) to all the Chinese

banks. The document stated the requirements about the eligibility of borrowers, down

payments, mortgage interest rates, loan terms, mortgage insurance, and application

procedures (Tang, Liu, & Wong, 2006).

3.2 Evidence of the Rapidly Increasing Price of the Residential Housing

In the case of China, the affordability issue is highly concerned by the officials

in central government, who tries to stabilize the macroeconomic environment. Although

the average disposable income among Chinese citizens has been increasing due to the

rapid economic growth in the past 37 years, people also witnessed a continuous rise in

housing price. The recent data extracted from China Statistical Yearbook 2014 showed

Page 23

23

the residential housing price in 2013 was 5850 yuan per square meter, which was 7 per

cent more than that of 2012. In big cities like Shanghai, the price increased more sharply.

The average residential housing price in Shanghai was already at a very high level of

13870 yuan per square meter in 2012, ranking number two in China right after Beijing.

In 2013, the average price further increased by 16.7 per cent, to 16192 yuan per square

meter. At national level, the price of residential properties increased by almost 200 per

cent from 1998 to 2012, as shown in Table 5. Among these 15 years, four was recorded

with annual growth rates of more than 10 per cent each. In 2009, the increase in housing

price was as high as 24.7 per cent. In summary, the residential housing experienced a

long period of high-speed price increase.

3.3 Reasons for the Skyrocket up of the Housing Price

There are several reasons caused the dramatic increase in residential housing

price.

First, rapid urbanization and fast expansion of urban population formed strong

demand over the residential housing market. Due to the former strategy in Mao

Zedong's era, the country experienced a rapid population growth. According to the

Page 24

24

census conducted in 1953, China has a total population of 582 million. However, in the

most recent census conducted in 2010, the total population in China was nearly 1.4

billion. In terms of urban areas, the population has increased very sharply. According to

the data of the World Bank, in 1980, there were only 191.4 million people, or 19 per

cent of the total population lived in the urban areas in China. By 2000, it had increased

to 459.1 million, or 36.22% of the total population. In 2013, more than half of the

Mainland Chinese lived in the cities.

Due to the rapid economic growth and the relaxation in hukou system in the

1990s, a considerable amount of people entered the cities as migrant workers. Those

workers were officially categorized as agricultural residents in the hukou system, but

work in urban areas for a living. In 2012, there were more than 262 million migrant

workers all over China. The number was 9 million more than the previous year's record.

Migrant workers serve in factories or service industries. Since they come from rural

areas, they need places to settle down near their work places. A report published by

McKinsey & Company in 2008 forecasted that more than 900 million people would be

living in urban areas in year 2025, occupying 66 per cent of total population. There

Page 25

25

would also be 23 cities, and each of them has a population of more than 5 million.

Among them, 8 cities would be called megacities with more than 10 million populations.

They also forecast that the total population in Chinese urban areas would achieve 1

billion in 2030.1 The huge increase in urban population unavoidably brought equally or

even stronger demand for residential housing, which in turn drives the housing price

higher.

Second, Chinese citizens regard real estate as a major way of investment. In

China, the deposit rate is rather low. However, the cost of living has been increasing

overtime. Many people need to do some investment to keep the value of the money they

earned. Among many channels of investment, like the stock and bond market, the real

estate market is a very attractive one. Housing, unlike stock or bond, is a fixed asset. It

is also different from common goods, which will most likely depreciate from the

moment they were bought by the consumers. By investing in the real estate market, one

can rent the property out, or sell it when the price becomes higher. Thus, the risk of the

investment is nearly zero as long as the housing bubble does not burst. People who have

surplus of funds looking for a proper investment opportunity are willing to put their

1中國城市人口 2030 年將超 10 億. (n.d.). Retrieved from http://www.china.com.cn/aboutchina/zhuanti/zgrk/2008-04/18/content_14975434.htm

Page 26

26

money in the projects with higher return but lower risk. The real estate market seems to

be an appropriate choice for them since the price has been increasing sharply over the

years and it does not seem to be highly risky considering a strong government doing the

backup. Because the growing in housing price is considerably strong, people expect it to

keep increasing in the future. As a result, more and more people invest their money into

the real estate market. Another group of people who do not have a surplus of fund also

try to buy properties. In most of the cases, they buy the home not for themselves but for

their children. They afraid a higher property price would cause higher unaffordability

issues in the future. The excessive investment demand together with rigid needs finally

makes the housing price higher, which in turn stimulates both of the demand to be

increased again.

Third, local governments depend on the property market to generate tax

income in order to help local finance. In 1994, China conducted the tax reform. Before

the reform, there were complaints about local government keeping too much of the tax

revenue while the central government keeping too little. At that time, local governments

were required to remit a fixed amount of money to the central government for several

Page 27

27

years. Because of the rapid economic growth and high inflation rate, the central

government's share of tax revenue would certainly decrease overtime. The 1994 tax

reform aimed to enlarge the portion that central government could share in the tax

system. Value-added tax was created to replace some multiple-rated turnover taxes,

which was considered inefficient. A new tax-sharing system was adopted by the policy

makers, making clear the tax revenue sharing between central and local government.

The central government was able to get as much as 75 per cent of the value-added tax

and all consumption tax, with some transfers and rebates back to local government. In

other words, the local governments could no longer keep large amount of tax revenues

as before. However, the expenditure side of the local government was not changed

much. Local governments were responsible for about the same level of social welfare

provision, infrastructure construction, educational investment, and so on. Thus, there

was a mismatch in local expenditure and income. Under this circumstance, local

governments could either reduce their expenditures or find new ways to finance their

fiscal budgets to avoid issuing huge amount of local government debt.

Page 28

28

It turns out that the local governments rely on their real estate markets very

much. From 2000 to 2009, the nationwide land transfer income recorded a 49 per cent

increase, soaring from 29.258 billion to 1.594 trillion. The ratio of land income to total

income of the local governments increased from less than 10 per cent to 49 percent (An

2011). The heavy burdens bore by local governments creates incentives to the local

officials to develop real estate market. With the governments' backup, property

developers tried to deliberately make the housing price higher. In some cases, real estate

companies spread information containing the huge demand and the shortage of supply

in the market, which was in fact not true. At the same time, they held the housing

resources and sell them slowly. Take Hangzhou for instance, there were 3500 acres of

land provided by the local government for housing constructions in 2003. The amount

was considered to be enough at that time. However, lots of lands were left unused.

Some buildings were not on sale even after the construction has finished already.

Housing developers acted as monopolies to control the supply of housing at a low level.

Then they spread the information to distort the market. After successfully fooled the

Page 29

29

consumers, they began to sell the properties slowly and step by step at higher price.2

The aftermath of this kind of action was naturally an unusual increase in property price.

3.4 Housing Price-to-Income Ratio Analysis

Among many research methods, the most commonly used one is the housing

price-to-income ratio (PIR). According to United Nations Human Settlements

Programme (UN-HABITAT), the housing price-to-income ratio is "the ratio of median

free-market price of a dwelling unit and the median annual household income".3 In

other words, a higher PIR indicates higher housing price relative to the household's

income and lower affordability of housing in a chosen region within a certain period of

time. Under the standard of UN-HABITAT, a ratio of 3 to 5 is considered reasonable. In

detail, the measurement of housing affordability is divided into four categories: If PIR is

under 3, the housing is rated as "Affordable"; if PIR is between 3.1 to 4.0, the housing is

then "Moderately Unaffordable"; if the PIR is between 4.1 to 5.0, the housing is

considered as "Seriously Unaffordable"; and if PIR is equal or larger than 5.1, the

housing is "Severely Unaffordable".

2 Price level catch up Paris, heated Hangzhou housing market. (2003, November 22). People Daily [Beijing].

3 Urban indicators. (n.d.). Retrieved from http://ww2.unhabitat.org/programmes/guo/guo_guide.asp#ind3

Page 30

30

Although the housing price-to-income ratio seems to be both easy to

understand and calculate, some difficulties exist when applying it to the case of China.

First, the measurement of housing price is different between China and western

countries. Foreign countries set the price of housing to each individual unit according to

its condition, location, and many other terms. The record of housing transactions is

relatively easy to be collected by the government. In China, the housing price is defined

as the product of the price per square meter and the total floor area of the property.

Second, the definition of the PIR is using median number of both housing price

and family income. In China, the National Bureau of Statistics only publishes the

average number of the two items in each of the China Statistical Yearbook. Thus,

applying PIR to China is not applicable simply because of the lack of appropriate data.

Chinese scholars always use the average value as the alternative way to

calculate PIR in order to accommodate the situations in China. Base on the research

conducted by Zhang (2011), the using of average number is actually quite acceptable.

As stated in his article, in terms of housing price, the median number is about 72 per

cent of the average, while the median number of household's disposable income is about

Page 31

31

75 per cent of the average. Because the two ratios are close to each other, calculating

PIR using average number should also be close to the PIR calculated by median

number.

As mentioned above, the international definition of PIR is the ratio of the

median price of each unit sold in a particular area to the median annual household

disposable income. In China, due to the limitation of data, average numbers are used

instead of median number. Thus, PIR in China is calculated as the ratio of average price

per unit of housing and the average annual household disposable income, within a

particular region. In practice, the first number can be obtained by using average housing

price per square meter multiply by average floor space sold; the second number can be

obtained by using per capita disposable income multiply by average number of people

per household. The average floor space sold is not listed as an item in the China

Statistical Yearbook. However, it can be calculated by using total floor space sold

divided by total units sold. The number of average people per household is standardized

to 2.87.4

4 Wang, W. (2013). Wo men jiu jing que bu que zhu fang. Retrieved from

http://paper.people.com.cn/rmwz/html/2013-08/01/content_1295181.htm

Page 32

32

The following paragraph will analyze the affordability in Chinese housing

market among 31 provinces in 2012. The data are obtained from China Statistical

Yearbook 2013 and China Real Estate Statistics Yearbook 2013. Table 6-1 to 6-3

concludes the PIRs in different provinces in 2012. The minimum and maximum value

of the housing price-to-income ratio are 5.8 and 15.9, respectively. It is noticeable that

even the minimum value of PIR goes beyond the normal or satisfactory range of PIR

according to UN-HABITAT, indicating a severely unaffordable housing price all over

China. The maximum value is observed in Beijing, whose housing price is about 16

times of the average annual household disposable income. Besides Beijing, another 4

provinces and municipalities have PIRs greater than 10. Zhejiang ranks the second place

as the most unaffordable housing in China with a PIR of 12.7. Hainan, Shanghai, and

Fujian follow Zhejiang, ranking number 3 to number 5 most unaffordable housing in

China. These five provinces are where the highest housing prices can be found all

around China. They are also categorized into the coastal areas of China, making the

eastern China records an average 10.5 housing price-to-income ratio.5 Thus, citizens

5 The eastern coastal area of China contains Beijing, Tianjin, Hebei, Shanghai, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong and Hainan.

Page 33

33

living in coastal China are facing extremely unaffordable housings nowadays. By

looking into the price-to-income ratio for Central China, the average value of PIR in

2012 is 7.6.6 It is still a very large number, but much lower than that of the eastern part

of China. Among the six provinces in central China, the difference in PIR is small

compare to the 10 provinces in the coastal region. That means the housing market in

central China has a relatively balanced development. The western part of China is less

developed, and the PIR in western China is relatively low with 7.2 on average.7

Surprisingly, the lowest average housing price-to-income ratio is observed in the

northeast China.8 The PIR in Heilongjiang, Jilin and Liaoning are 6.3, 5.9 and 6.4,

respectively, all below 7. According to the calculation, residential housings in China are

highly unaffordable. By separating the 31 provinces into 4 parts, it can be conclude that

the housing market in China developed unevenly. The coastal areas are more developed

than inland areas, making the affordability issue more severe.

Internationally, the housing price-to-income ratio is the most frequently used

index when analyzing the housing affordability issues. However, one should notice that

6 The central China contains Shanxi, Anhui, Jiangxi, Henan, Hubei and Hunan. 7 The western China contains Inner Mongolia, Guangxi, Chongqing, Sichuan, Guizhou, Yunnan, Tibet, Shaanxi, Gansu, Qinghai, Ningxia and Xinjiang. 8 The northeast China contains Heilongjiang, Jilin and Liaoning.

Page 34

34

using PIR as a benchmark to measure the housing affordability in China has some

limitations.

First, each province is large in size and developed unevenly. The housing price

within a certain province may vary in a wide range, so as the household disposable

income. The housing price-to-income ratio may not be at the same level of accuracy

when applying to different provinces.

Second, Chinese citizens have explicit and implicit income. Both incomes were

used to do the consumption and investment, including purchasing real estate properties.

The statistics only include the explicit incomes since the implicit ones are not easy to

calculate. However, implicit income should not be ignored due to its large size.

According to Wang (2013), Chinese residents' implicit incomes in 2011 were 6.2 trillion

yuan, accounting for 12% of GDP. In addition, high- and middle-to-high-income

households held most of the implicit incomes. Thus, the price-to-income ratio may not

be so accurate in the sense that the disposable income is only a part of household's

actual income, and the affordability issue may not be as severe as indicated by PIR.

Page 35

35

Third, parents in China will usually finance their children for purchasing a

property. Due to the one child policy, Chinese parents tend to pay all their attention to

their only child. When a newly married couple buying a new home, it is not only the

couple themselves paying for the house. Both the bride's and the bridegroom's parents

will also partially pay for the house. In fact, the property is purchased by three families,

instead of one. As a result, using one household's disposable income may not be

appropriate in some cases, and the housing affordability issue is overstated.

In summary, the housing price-to-income ratio is a way to evaluate the housing

affordability in China. However, one should notice that the PIR couldn’t fully reflect the

real capacity of the Chinese families to pay for their urban properties due to its

limitations. The housing affordability issue may not be as severe as the PIR indicates.

Despite of the limitations observed in data and the PIR model, the very high PIR gives

no doubt about a highly unaffordable residential housing in China, especially in some

big cities such as Beijing and Shanghai.

3.5 Harms Caused by High Housing Price

Page 36

36

Housing is a life necessity since everyone needs a place to live. The price of

housing is highly relevant to the wellbeing of the people and the economic development.

As mentioned above, high housing price in China causes affordability issues, which in

turn downgrades the citizens' standard of living and. Besides, the Chinese economy is

also negatively influenced by the highly unaffordable housing prices in several aspects.

For citizens, a small change in housing price always means a big change in

their sense of happiness. Since properties are already highly unaffordable, people need

to save for several years in order to pay for the down payment. After the purchasing of

the house, the mortgage payment will become the major burden of a typical family in

the following 10 to 30 years. High housing price contributes a lot to a high cost of living

for the citizens. The more people spend on their properties, the less they consume on

other goods and services. In other words, people's ability to consume will be lower as

the housing price goes up. As people reduce their expenditures on other goods and

services, their wellbeing will also be decreased. Besides consumption, young people

may tend to invest less in their education, reducing opportunities for personal

development. What's more, due to the high property price in central city, many people

Page 37

37

choose to locate their homes in suburbs, where the housing prices are relatively lower.

The decisions add extra pressures to the city's transportation net, which in turn causes

environmental problems, resulting in crowded roads and poor air quality. All of the

above reduce people's standard of living and their sense of happiness.

For the economy, high housing price causes more problems. Since people

consume less on other goods and services besides housing, the overall domestic demand

drops. The reduction in demand negatively affects the secondary and tertiary industries,

which are the major contributors to the Chinese economy nowadays. As young people

pay less attention to their education, the accumulation of human capital will also be

slower. In the long run, low human capital will result in poorer quality of the economic

development. High housing price also distorts the investors' behaviors. In recent years,

many real estate speculators groups deliberately drove the housing price up in several

big cities. Their behaviors created huge housing bubbles and weakened the risk

tolerance ability of the society. People who need a place to live will not be able to afford

the housing in those cities, bringing unstable factors to the society. In some other cities,

the housing development companies over produce residential housings because of the

Page 38

38

rapid increasing price. However, the demand for residential housing is mismatched with

the supply, and the result of the excess supply of housing is high vacancy rate. In recent

years, ghost city becomes a phenomenon. Those cities are always well built with high

quality residential and office buildings. Each of the ghost cities has a very promising

original plan, however, none of them turns out to be successful. In daytime, no human

activities can be seen in the cities. At night, it becomes completely dark with no

artificial light. Therefore, they are called "ghost cities".9 In addition to the high vacancy

rate, the high housing price also increases the cost to corporates. Companies do

profit-making business. The higher cost in production will eventually transfer to the

consumers. The rapid increase in price may bring inflation pressure to the economy,

which shrinks people's wealth. In conclusion, unreasonably high housing price makes

the economy unhealthy and dangerous.

9 2014 中國鬼城你知多少. (n.d.). Retrieved from http://mall.fang.com/mall/201403/zgxgcpd.html

Page 39

39

4. Major Findings and Conclusion

The Chinese housing market has experience dramatic changes since the

foundation of the New China. Before 1978, housing was considered a social welfare,

which is constructed and distributed by the work unit. The housing market did not exist,

and the government bore heavy burden on the financing of urban housing. After the

market-orientated economic reform, the housing market also started the reform. The

Chinese government adopted the gradualism methodology when conducting the reform,

and the real estate market slowly privatized. New laws as well as taxations were

implemented step by step. After Deng's Southern Tour Speech in 1992, the Chinese

housing market overheated, and cooled down in 1997. After the first two stages of

development, the real estate market back to a steady growing trend. With the total

abandonment of welfare housing system in 1998, the Chinese housing market fully

commercialized. Residential housing dominated the construction of fix assets, and

Chinese people saw a big jump in terms of the standard of living. However, the

development in the real estate market brought many problems. The major concern for

the Chinese people and policy makers is the housing affordability issue.

Page 40

40

Housing price has been increasing for the last 15 years. Nationally, the price

tripled from 1998 to 2012. There are several contributors to the rapid increasing price.

Urbanization and the relaxation in hukou system brought strong demand for residential

housing. Chinese citizens also keen on real estate investment, driving the demand even

higher. The local governments rely on the housing market to finance their expenditures

since the 1994 tax reform. Irregular behaviors of the housing speculation groups also

force the housing price to go up in many cities. By conducting the housing

price-to-income analysis, it can be conclude that the residential housing in China is

highly unaffordable under international standards. In first-tier cities like Beijing and

Shanghai, the unaffordability is more severe. Housing as an important part of the

economy, highly related to people's stand of living. Heavy burden caused by high

housing price will squeeze people's consumption on other goods and services, lower

domestic demand. It may also affect the citizen's individual development, and influence

the human capital accumulation. Therefore, the abnormal high housing price in China

will finally cause negative effects to the Chinese economy in the long run.

Page 41

41

5. Appendix

5.1 Figures

Data Source: www.ldfcj.com

Data Source: www.ldfcj.com

0

50

100

150

200

250

300

350

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Bil

lio

n Y

ua

n

Figure 1. Total Investment Value Completed in Real Estate Development

-50.0%

0.0%

50.0%

100.0%

150.0%

200.0%

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Figure 2. Growth Rate of Total Fixed Asset Investment and Total Investment Completed in Real Estate Development

Total fixed asset investment

Total Investment Completed in Real Estate Development

Page 42

42

Data Source: China Real Estate Statistics Yearbook 1999-2013

0

20000

40000

60000

80000

100000

120000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

10

00

0 s

q.m

Figure 3. Total and Residential Floor Space Completed

Total Floor Space Completed Floor Space Completed for Residential Purpose

Page 43

43

5.2 Tables

Table 1.

Year

Total fixed

asset

investment

(billion

yuan)

Total investment

value completed

in real estate

development

(billion yuan)

Percentage change

in total fixed asset

investment

(%)

Percentage change in

total investment value

completed in real

estate development

(%)

1986 301.96 10.1 - -

1987 364.09 15 20.6 48.5%

1988 449.65 25.7 23.5 71.3%

1989 473.77 27.2 5.4 5.8%

1990 444.93 25.3 -6.1 -7.0%

1991 550.88 33.6 23.8 32.8%

1992 785.5 73.1 42.6 117.6%

1993 1245.79 193.8 58.6 165.1%

1994 1704.29 255.4 36.8 31.8%

1995 2001.93 314.9 17.5 23.3%

1996 2297.4 321.6 14.8 2.1%

1997 2494.11 317.8 8.6 -1.2%

Data Source: www.ldfcj.com

Page 44

44

Table 2.

Year Number of real estate development company

1986 1991

1987 2506

1988 3536

1989 3985

1990 4400

1991 5128

1992 13566

1993 26027

1994 31486

1995 33482

1996 21269

Data Source: Liu & Wang, 1999.

Page 45

45

Table 3.

Year

Total floor space completed

(10,000 square meters)

Residential floor space

completed

(10,000 square meters)

Proportion

(%)

1998 17566.6 14125.7 80.4

1999 21410.8 17640.7 82.4

2000 25104.9 20603.3 82.1

2001 29867.4 24625.4 82.4

2002 34975.8 28524.7 81.6

2003 41464.1 33774.6 81.5

2004 42464.9 34677.2 81.7

2005 53417 43682.9 81.8

2006 55830.9 45471.8 81.4

2007 60606.7 49831.3 82.2

2008 66544.8 54334.1 81.7

2009 72677.4 59628.7 82.0

2010 78743.9 63443.1 80.6

2011 92619.9 74319.1 80.2

2012 99425 79043.2 79.5%

Data Source: China Real Estate Statistics Yearbook 1999-2013

Page 46

46

Table 4.

Year

Commercial

housing sold

(10000 square

meters)

Residential

housing sold

(10000 square

meters)

Percentage change

in commercial

housing sales

(%)

Percentage change

in residential

housing sales

(%)

1998 12185.33 10827.08 - -

1999 14556.53 12997.87 19.5% 20.0%

2000 18637.13 16570.28 28.0% 27.5%

2001 22411.9 19938.75 20.3% 20.3%

2002 26808.29 23702.31 19.6% 18.9%

2003 33717.63 29778.85 25.8% 25.6%

2004 38231.64 33819.89 13.4% 13.6%

Data Source: China Real Estate Statistics Yearbook 1999-2005

Page 47

47

Table 5.

Year

National average residential housing

price (yuan per square meter)

Percentage change

(%)

1998 1854 -

1999 1857 0.2

2000 1948 4.9

2001 2017 3.5

2002 2092 3.7

2003 2197 5.0

2004 2608 18.7

2005 2937 12.6

2006 3119 6.2

2007 3645 16.9

2008 3576 -1.9

2009 4459 24.7

2010 4725 6.0

2011 4993 5.7

2012 5430 8.8

Data Source: China Real Estate Statistics Yearbook 1999-2013

Page 48

48

Table 6-1

Province

Average housing price

per square meter (yuan

per square meter)

Total floor space sold

(residential) (square meter) Units sold

Beijing 16553 14833746 147153

Tianjin 8010 15114032 153686

Hebei 4142 46224637 444959

Shanxi 3691 13904422 122431

Inner Mongolia 3656 21042187 198073

Liaoning 4717 76553988 840520

Jilin 3875 21594307 245525

Heilongjiang 3726 32262165 373563

Shanghai 13870 15926284 164759

Jiangsu 6432 79233670 705029

Zhejiang 10680 33162270 282224

Anhui 4495 42754287 418989

Fujian 8366 27419567 249314

Jiangxi 4381 21258981 189254

Shandong 4557 77458724 714514

Henan 3511 54555010 489310

Hubei 4668 36200951 340340

Hunan 3670 46640816 400490

Guangdong 7668 71576276 644541

Guangxi 3910 25469557 235237

Hainan 7811 8983484 97242

Chongqing 4805 41051083 438391

Sichuan 4959 56793338 573537

Guizhou 3695 20023965 190506

Yunnan 3861 27896760 239631

Tibet 2982 206486 1830

Shaanxi 4803 25308411 245420

Gansu 3376 8933551 88808

Page 49

49

Qinghai 3692 2468539 22913

Ningxia 3621 7075675 66329

Xinjiang 3594 12747965 121906

Data Source: China Statistical Yearbook 2013 and China Real Estate Statistics Yearbook

2013.

Table 6-2

Province

Average floor space sold

(square meter)

Average housing price

(yuan per unit)

Beijing 100.8 1668623.8

Tianjin 98.3 787732.1

Hebei 103.9 430292.3

Shanxi 113.6 419184.9

Inner Mongolia 106.2 388393.3

Liaoning 91.1 429621.1

Jilin 88.0 340812.3

Heilongjiang 86.4 321790.0

Shanghai 96.7 1340731.4

Jiangsu 112.4 722851.1

Zhejiang 117.5 1254936.0

Anhui 102.0 458676.8

Fujian 110.0 920093.1

Jiangxi 112.3 492119.6

Shandong 108.4 494013.3

Henan 111.5 391454.6

Hubei 106.4 496521.2

Hunan 116.5 427405.9

Guangdong 111.0 851531.4

Guangxi 108.3 423343.1

Page 50

50

Hainan 92.4 721601.7

Chongqing 93.6 449941.8

Sichuan 99.0 491054.9

Guizhou 105.1 388379.1

Yunnan 116.4 449480.2

Tibet 112.8 336470.6

Shaanxi 103.1 495299.1

Gansu 100.6 339605.3

Qinghai 107.7 397758.7

Ningxia 106.7 386271.8

Xinjiang 104.6 375832.1

Data Source: China Statistical Yearbook 2013 and China Real Estate Statistics Yearbook

2013.

Table 6-3

Province

Per capita disposable

income (yuan)

Annual household disposable

income (yuan) PIR

Beijing 36468.8 104665.3 15.9

Tianjin 29626.4 85027.8 9.3

Hebei 20543.4 58959.7 7.3

Shanxi 20411.7 58581.6 7.2

Inner Mongolia 23150.3 66441.2 5.8

Liaoning 23222.7 66649.1 6.4

Jilin 20208.0 57997.1 5.9

Heilongjiang 17759.8 50970.5 6.3

Shanghai 40188.3 115340.5 11.6

Jiangsu 29677.0 85172.9 8.5

Zhejiang 34550.3 99159.4 12.7

Anhui 21024.2 60339.5 7.6

Page 51

51

Fujian 28055.2 80518.5 11.4

Jiangxi 19860.4 56999.2 8.6

Shandong 25755.2 73917.4 6.7

Henan 20442.6 58670.3 6.7

Hubei 20839.6 59809.6 8.3

Hunan 21318.8 61184.8 7.0

Guangdong 30226.7 86750.7 9.8

Guangxi 21242.8 60966.8 6.9

Hainan 20917.7 60033.8 12.0

Chongqing 22968.1 65918.6 6.8

Sichuan 20307.0 58281.1 8.4

Guizhou 18700.5 53670.5 7.2

Yunnan 21074.5 60483.8 7.4

Tibet 18028.3 51741.3 6.5

Shaanxi 20733.9 59506.2 8.3

Gansu 17156.9 49240.3 6.9

Qinghai 17566.3 50415.2 7.9

Ningxia 19831.4 56916.1 6.8

Xinjiang 17920.7 51432.4 7.3

Data Source: China Statistical Yearbook 2013 and China Real Estate Statistics Yearbook

2013.

Page 52

52

6. References

Burrell, M. (2006). China's housing provident fund: its success and limitations. Housing

Finance International, 20(3), 38-49. Retrieved from

http://search.proquest.com/docview/216195740?accountid=11440

Chai, Q. (2008, September 26). Wo guo fang di chan zhi du gai ge yu shi chang fa zhan

de li cheng. Retrieved from

http://theory.people.com.cn/GB/49154/49155/8108609.html

Gu, G. W. (2005). The empirical study of the price mechanism in the Chinese housing

market. Retrieved from

https://kobra.bibliothek.uni-kassel.de/handle/urn:nbn:de:hebis:34-2884

Liu, Z., & Wang, Y. (1999). Zhongguo fang di chan shi chang. Wuhan: Hubei ren min

chu ban she.

Lu, J., Li, Y., & Mi, Y. (2013). Study on the development situation and strategy of

China's housing accumulation fund system. Journal of Graduate School of

Chinese Academy of Social Sciences, 1(193).

Man, Y. J. (2011). Housing policy and housing markets: trends, patterns, and

affordability. In China's housing reform and outcomes (pp. 3-18). Cambridge,

MA: Lincoln Institute of Land Policy.

National Bureau of Statistics of China. (2011, June 13). Dong xi zhong bu he dong bei

di qu hua fen fang fa. Retrieved from

http://www.stats.gov.cn/ztjc/zthd/sjtjr/dejtjkfr/tjkp/201106/t20110613_71947.ht

m

Price level catch up Paris, heated Hangzhou housing market. (2003, November 22).

People Daily [Beijing].

Page 53

53

Tang, B., Liu, S., & Wong, S. (2006). Housing Mortgage and Housing Transaction in

China: Bridging the Missing Links.

Urban indicators. (n.d.). Retrieved from

http://ww2.unhabitat.org/programmes/guo/guo_guide.asp#ind3

Urban population (% of total). (n.d.). Retrieved from

http://data.worldbank.org/indicator/SP.URB.TOTL.IN.ZS?page=6

Wang, W. (2013). Wo men jiu jing que bu que zhu fang. Retrieved from

http://paper.people.com.cn/rmwz/html/2013-08/01/content_1295181.htm

Wang, X. (2013, September 28). Implicit income accounts for about 12% of GDP and is

still expanding. Retrieved from

http://finance.sina.com.cn/zl/china/20130928/005816875784.shtml

Wo guo fang di chan zhou qi fen xi yu yu ce. (n.d.). Retrieved from

http://www.ldfcj.com/rock_news_view.asp?ArticleID=17852

Zhang, Q. (2011). The origin, calculation and application of housing price to income

ratio: an analysis based on literature. Finance & Trade Economics, 12(2011).

中國城市人口 2030 年將超 10 億. (n.d.). Retrieved from

http://www.china.com.cn/aboutchina/zhuanti/zgrk/2008-04/18/content_1497543

4.htm

2014 中國鬼城你知多少. (n.d.). Retrieved from

http://mall.fang.com/mall/201403/zgxgcpd.html

安體富,竇欣,. 論土地財政與房地產市場調控[J]. 地方財政研究,2011,(2).

陳春霞,. 論我國高房價的危害、成因及對策[J]. 特區經濟,2012,(1).

Page 54

54

傅東平,. 高房價及其對中國經濟的影響研究[J]. 特區經濟,2010,(8).

黃萬成,. 個人住房貸款政策對房地產市場的影響研究[J]. 價值工程,2014,(21).

李超,匡耀求,. 人口集聚過程中的我國房價收入比[J]. 學術研究,2013,(2).

李智,. 我國住房公積金制度發展概況、存在的問題及改革建議[J]. 經濟視角(上旬

刊),2014,(3).

錢楓林,鄧予蘭,. 我國商業銀行個人住房貸款風險的分析及防範[J]. 科學經濟社

會,2011,(1).

夏剛,. 房價收入比來源、用途及局限性[J]. 經濟研究導刊,2009,(27).

張運峰,劉曉星,黃鶯,. 美國房價收入比的經濟解釋及對我國的啓示[J]. 南京財經大

學學報,2011,(5).