Realising M-Payments: modelling consumers’ willingness to M-pay using Smart Phones Aidan Duane a *, Philip O’Reilly b and Pavel Andreev c a The School of Business, Department of Accounting and Economics, Waterford Institute of Technology, Waterford City, Ireland; b Department of Accounting, Finance and Information Systems, University College Cork, Cork, Ireland; c Telfer School of Management, University of Ottawa, Ottawa, Canada (Received 25 October 2011; final version received 3 October 2012) It is predicted that significant and ongoing investment in M-Commerce platforms and application development by commercial entities will fundamentally change consumers’ shopping and web browsing behaviours. However, the evolving behaviour of Smart Phone users is somewhat tempered by concerns over M-Payments. If Smart Phones are to reach their full M-Commerce potential, the ability of consumers to transact and pay for products/services through these devices in an easy, safe and reliable manner must be addressed. In response, this paper contributes a theoretical model and empirically tests the model to explore Irish consumers’ perceptions of using Smart Phones to make M- Payments for products/services. The findings present conclusive evidence that trust is the most powerful factor influencing consumers’ willingness to use Smart Phones to make M-Payments. While perceived usefulness and perceived ease of use influence the payment decision, their impact is much lower. Mobile self-efficacy and personal innovativeness have almost no direct impact. The paper concludes that irrespective of individuals’ high levels of personal innovativeness or mobile self-efficacy and irrespective of whether Smart Mobile Media Services are perceived as useful and easy to use, consumers will not make M-Payments, until they are convinced that Smart Phone M-Payment systems are safe and reliable. Keywords: Smart Phones; user behaviour; M-Payments; trust; PLS Introduction The notion that Smart Phones could become valuable and critical business tools for the delivery of M- Commerce products and services has long been touted by academics, professionals and the media (Varshney and Vetter 2002, Bauer et al. 2005, Leppa¨niemi and Karjaluoto 2005, Gao and Ku¨pper 2006, Hsu and Kulviwat 2006). Smart Phones enable the delivery of a wide range of transactional M-Commerce products and services, including highly individualised and location-based Smart Mobile Media Services (SMMS) (O’Reilly and Duane 2010). Smart Mobile Media Services: ‘. . . provide mobile network subscribers with permis- sion and subscription based, dynamically profiled, location, context and task specific, mobile Internet applications, content, products, services and transac- tions for Smart Phones’. (O’Reilly and Duane 2010, p. 197) In particular, location-based SMMS have resulted in substantial changes to consumers’ interactions with retailers via the mobile web, especially when coupled with mobile couponing (Jayasingh and Eze 2009, Goldman 2010). Thus, SMMS are integral to the M- Commerce value chain proposition. Numerous indus- try experts predict that the range and extent of SMMS available through Smart Phones and other Smart Mobile Media Devices will increase significantly over the coming years, as increasing numbers of commercial entities invest in M-Commerce platforms and applica- tions, to satisfy growing consumer demands for fully fledged multichannel retailing (Skeldon 2011). Signifi- cant investment has taken place in recent times on M- Commerce platforms and application development by major global organisations such as, KFC (Higgs 2008), Starbucks (Xu et al. 2010), Microsoft, McDonalds, Coca-Cola and P&G (Wei et al. 2010). Indeed it is significant that WorldNet TPS predicts that M- Commerce will achieve in the next 3 to 4 years, what E-Commerce has achieved in the last 15 years (Enterprise Ireland 2011). When considering the future of M-Commerce and realisation of the potential of Smart Phones, the establishment of standardised, interconnected and widely accepted mobile payment (M-Payment) proce- dures is crucial (Zhong 2009). It is predicted that M- Payments, using mobile devices for digital and physical goods, could exceed $630 billion in 2014 alone (Juniper Research 2010). According to Egger (2001), trust in *Corresponding author. Email: [email protected]Ó 2012 Taylor & Francis Behaviour & Information Technology, 2014 Vol. 33, No. 4, 318–334, http://dx.doi.org/10.1080/0144929X.2012.745608

Transcript

Realising M-Payments: modelling consumers’ willingness to M-pay using Smart Phones

Aidan Duanea*, Philip O’Reillyb and Pavel Andreevc

aThe School of Business, Department of Accounting and Economics, Waterford Institute of Technology, Waterford City, Ireland;bDepartment of Accounting, Finance and Information Systems, University College Cork, Cork, Ireland; cTelfer School of

Management, University of Ottawa, Ottawa, Canada

(Received 25 October 2011; final version received 3 October 2012)

It is predicted that significant and ongoing investment in M-Commerce platforms and application development bycommercial entities will fundamentally change consumers’ shopping and web browsing behaviours. However, theevolving behaviour of Smart Phone users is somewhat tempered by concerns over M-Payments. If Smart Phones areto reach their full M-Commerce potential, the ability of consumers to transact and pay for products/services throughthese devices in an easy, safe and reliable manner must be addressed. In response, this paper contributes a theoreticalmodel and empirically tests the model to explore Irish consumers’ perceptions of using Smart Phones to make M-Payments for products/services. The findings present conclusive evidence that trust is the most powerful factorinfluencing consumers’ willingness to use Smart Phones to make M-Payments. While perceived usefulness andperceived ease of use influence the payment decision, their impact is much lower. Mobile self-efficacy and personalinnovativeness have almost no direct impact. The paper concludes that irrespective of individuals’ high levels ofpersonal innovativeness or mobile self-efficacy and irrespective of whether Smart Mobile Media Services areperceived as useful and easy to use, consumers will not make M-Payments, until they are convinced that SmartPhone M-Payment systems are safe and reliable.

Keywords: Smart Phones; user behaviour; M-Payments; trust; PLS

Introduction

The notion that Smart Phones could become valuableand critical business tools for the delivery of M-Commerce products and services has long been toutedby academics, professionals and the media (Varshneyand Vetter 2002, Bauer et al. 2005, Leppaniemi andKarjaluoto 2005, Gao and Kupper 2006, Hsu andKulviwat 2006). Smart Phones enable the delivery of awide range of transactional M-Commerce productsand services, including highly individualised andlocation-based Smart Mobile Media Services(SMMS) (O’Reilly and Duane 2010). Smart MobileMedia Services:

‘. . . provide mobile network subscribers with permis-sion and subscription based, dynamically profiled,location, context and task specific, mobile Internetapplications, content, products, services and transac-tions for Smart Phones’.

(O’Reilly and Duane 2010, p. 197)

In particular, location-based SMMS have resultedin substantial changes to consumers’ interactions withretailers via the mobile web, especially when coupledwith mobile couponing (Jayasingh and Eze 2009,Goldman 2010). Thus, SMMS are integral to the M-

Commerce value chain proposition. Numerous indus-try experts predict that the range and extent of SMMSavailable through Smart Phones and other SmartMobile Media Devices will increase significantly overthe coming years, as increasing numbers of commercialentities invest in M-Commerce platforms and applica-tions, to satisfy growing consumer demands for fullyfledged multichannel retailing (Skeldon 2011). Signifi-cant investment has taken place in recent times on M-Commerce platforms and application development bymajor global organisations such as, KFC (Higgs 2008),Starbucks (Xu et al. 2010), Microsoft, McDonalds,Coca-Cola and P&G (Wei et al. 2010). Indeed it issignificant that WorldNet TPS predicts that M-Commerce will achieve in the next 3 to 4 years, whatE-Commerce has achieved in the last 15 years(Enterprise Ireland 2011).

When considering the future of M-Commerce andrealisation of the potential of Smart Phones, theestablishment of standardised, interconnected andwidely accepted mobile payment (M-Payment) proce-dures is crucial (Zhong 2009). It is predicted that M-Payments, using mobile devices for digital and physicalgoods, could exceed $630 billion in 2014 alone (JuniperResearch 2010). According to Egger (2001), trust in

Behaviour & Information Technology, 2014Vol. 33, No. 4, 318–334, http://dx.doi.org/10.1080/0144929X.2012.745608

any payment system is influenced by anonymity,security, reliability, the amount of control that usershave and the reputation of the entity that introducesthe system. One must also recognise that the ‘M-Payments Process’ requires specialised M-Paymenthardware and software, a vendor accepting the M-Payment, an M-Payment processing service, legislationand consumer rights governing the M-Payment processand an independent consumer rights advocate regulat-ing the process (Ondrus et al. 2009, Ondrus andLyytinen 2011). This multidimensionality of trust inM-Payments is reflected in the definition of M-Payments adopted for this study. The authors adoptthe definition provided by Dinez et al. (2011) whodefine M-Payments as:

‘payments made or enabled through digital mobilitytechnologies, via handheld devices, with or without theuse of mobile telecommunications networks. Thesepayments are digital financial transactions, althoughnot necessarily linked to financial institutions or banks’(p. 5).

In some countries including Japan, Singapore andKorea, M-Payment services have become establishedand widely used (Schaettgen and Taga 2010). However,in a global context, and particularly in Europe, M-Payments are still in their infancy. In fact, Schierz et al.(2010) report that less than 1% of mobile phone usershave made an M-Payment. Interestingly, severalresearchers (Barutcu 2008, Matthews et al. 2009, Xuet al. 2010, Andreev et al. 2011, Rao 2011) reveal thatwhile consumers have positive attitudes towards mobileadvertising, mobile coupons, mobile social media andmobile media, they do not possess positive attitudestowards mobile shopping, and in particular making M-Payments using Smart Phones. Herein lies the problem:although growth forecasts for M-Payment serviceshave been very positive, the reality on the ground isquite different (Schierz et al. 2010). These studiesindicate that, while consumers are willing to use SmartPhones to engage in M-Commerce transactional tasks,they are reluctant to make an M-Payment. This is verysignificant, as the realisation of the enormous commer-cial potential of Smart Phones for M-Commerce isentirely contingent on consumers’ willingness to makean M-Payment (WMPay) using Smart Phones and, assuch, complete the M-Commerce transactional loop.Thus, the primary question emerging from the extantliterature is that what factors influence consumers’willingness to use a Smart Phone to makeM-Payments?

Review of the literature: state of the art

Few comprehensive attempts have been made alreadyby researchers to answer this question with extant

studies focussing on the broader field of M-Commerce.Kim and Zhang (2009) suggest that, although there canbe numerous factors influencing people’s adoption ofSmart Phone services, such factors are underinvesti-gated in the extant literature. While some M-Com-merce-based adoption studies have been conducted,they have been primarily focussed on mobile market-ing/advertising and mobile banking adoption. Baueret al. (2005) reveal the importance of personalinnovativeness (PI) in the adoption of mobile market-ing. Similarly, Gupta et al. (2011) note that PI has apositive impact on willingness to use mobile location-based services (LBS). Lee et al. (2011) suggest thatmobile self-efficacy (MSE) influences consumers’ adop-tion of mobile advertising. Chen et al. (2011) testedTAM in a study on Smart Phone acceptance andreports that MSE also plays a positive role onperceived ease of use (PEU).

A number of researchers (Siau et al. 2004, Xu andGutierrez 2006, Mallat 2007) suggest that trustpositively influences consumers’ decisions to engagein M-Commerce transactional tasks. Lin and Wang(2006) reveal that trust also has a positive impact onconsumer loyalty and satisfaction towards M-Com-merce. Chung and Kwon (2009) and Lie et al. (2010)suggest that consumers’ perceptions of competence,integrity and ethical commitment in mobile bankingand M-Commerce were also important trust factorsinfluencing adoption decisions. Previously, trust hasbeen identified as a significant determinant in influen-cing consumers’ E-Commerce transactions in severalstudies (e.g. Jarvenpaa et al. 2000, Gefen et al. 2003,Verhagen et al. 2006, Chen and Barnes 2007). Some E-Commerce studies reveal that trust factors such asperceived security control, perceived privacy control(Cheung and Lee 2003, Roca et al. 2008), perceivedintegrity and perceived competence (Cheung and Lee2003) greatly influence a consumers trust in onlinevendors, and thus their adoption decisions. Govern-ance and independent regulation of the online E-Commerce environment are also trust factors thatinfluence adoption according to Cheung and Lee(2003).

Viehland and Yoong Leong (2010) and Dahlberget al. (2007) report that perceived usefulness (PU) andPEU positively impact upon consumer willingness tomake M-Payments at instore electronic points-of-sale.Kim et al. (2010) suggest that consumers’ are willing tomake an M-Payment if they find the system to beuseful for their transaction needs. Schierz et al. (2010)note that ease of use is even more important for M-Payment services, as they compete with establishedpayment services.

Interestingly, few of the previous M-Commercestudies have been conducted in a European context.

Behaviour & Information Technology 319

However, this is largely because European countrieshave been a laggard when compared to Asian countrieswith respect to the adoption of M-Commerce. In fact,M-Payment services have largely failed to entice orconvince European consumers, and several M-Pay-ment companies/initiatives in the EU have alreadybeen abandoned (Dahlberg and Oorni 2007, Mallat2007). Thus, while several M-Commerce adoptionstudies exist in the literature, few of these specificallyfocus on M-Payments, few are European based andnone of these studies are sufficiently comprehensivewith respect to the inclusion of previously established,empirically tested, constructs from both E-Commerceand M-Commerce literature. Gaining a better under-standing of European consumers’ perceptions of usingSmart Phones to make M-Payments is thus required, inorder to develop M-Payment services for successfuladoption by consumers (Dahlberg and Oorni 2007).Dahlberg et al. (2008) state that:

‘[. . .] we believe that more theory based empiricalresearch is needed to enhance the current under-standing of the M-Payment services markets. [. . .] toimprove the quality and relevance of M-Paymentresearch, we also recommend that researchers collectmore empirical data backed by guiding theories’.(Dahlberg et al. 2008 p. 178)

This paper makes a number of contributions toboth theory and practice. Firstly, it contributes aconceptual model for exploring consumer’s percep-tions of M-Payments. It explores variables that hadnot previously been investigated pertaining to theirimpact on consumer’s WMPay. It adopts and com-bines several factors identified and empirically tested inprevious E-Commerce and M-Commerce studies,namely trust, PI, PEU, PU and MSE, in order toinvestigate their impact on Irish consumers’ willingnessto use Smart Phones to make M-Payments. Anunderstanding of these factors can have significantimplications for M-Payment service providers indeveloping more appropriate M-Payment servicesand applications, guiding M-Payment deploymentstrategies and information and marketing campaigns.Furthermore, it informs mobile vendors of how tocreate more positive relationships with consumers inthe M-Commerce environment.

From the perspective of theory development,adding to the existing knowledge in the field of M-Commerce about the factors influencing adoption ofM-Payment systems, especially in a European contextrepresents a significant contribution through enablingresearchers develop richer theoretical models thatbetter explain adoption behaviours. Furthermore,this study serves as an important starting point fromwhich researchers can engage in future comparative

cross-cultural studies of M-Payment adoption inEuropean and non-European markets.

The remainder of this paper is structured asfollows. The next section discusses conceptualisationof the theoretical model and identifies four researchhypotheses. Following this, methodological design anddata analysis is presented. The subsequent sectionpresents the results of the study and the research modelevaluation. The theoretical implications of the findingsand the challenges for practitioners are then discussed,with concluding remarks and study limitations endingthe paper.

Theoretical model conceptualisation and research

hypothesis

M-Payments are a critical enabler of the truecommercial value of the Smart Phone (O’Reilly andDuane 2010, Andreev et al. 2011). Although literatureproposes three fundamental models for handling M-Payments: (1) mobile network operator (MNO) led, (2)bank and financial institution led and (3) third partyled, with numerous variations/combinations of thesebeing possible (Turner 2009); in practice, an acceptedM-Payment model to facilitate the widespread adop-tion of M-Payments still remains elusive. Ultimately,consumers will play a key role in determining the‘winning’ model, as consumer buy-in for any proposedM-Payment model is critical. Thus, the enormouspotential of Smart Phones for M-Commerce is entirelycontingent on consumers’ willingness to make M-Payments using Smart Phones.

However, consumer acceptance, or WMPay, is thegreatest barrier to M-Payment adoption, which is verymuch influenced by their assessment of the riskinvolved (Mallat 2007). Thus, it is of great concernthat there is considerable evidence that users perceivesignificant risks and uncertainty in interacting withvendors through mobile devices (Im et al. 2008).Viehland and Yoong Leong (2010) contend that inorder for M-Payments to succeed, consumers mustperceive them as being useful and easy to use, but mostimportantly, secure and safe to use.

Viehland and Yoong Leong (2010) and Dahlberget al. (2007) report that both PU and PEU,positively impact consumer WMPay at retailpoints-of-sale. Therefore, PEU, PU and perceivedpayment reliability, which incorporate a consumer’sperception of the security and perceived safety ofmaking an M-Payment using a Smart Phone, arethree important issues for consumers if they are toadopt M-Payment services. Chen et al. (2011) testedTAM in their recent study on Smart Phoneacceptance and reveal that MSE also plays a positiverole on PEU.

A. Duane et al.320

Personal innovativeness, or an individual’s will-ingness to try out new technology, also appears to havea significant impact on the adoption of new technol-ogies (Agarwal and Prasad 1998). While Agarwal andPrasad (1998) examined the moderating effects of PIon intention to adopt, Gupta et al. (2011) reveal thatPI has a direct positive impact on willingness to usemobile LBS. Thus, PI may also impact upon anindividual’s WMPay.

Several studies (e.g. Jarvenpaa et al. 2000, Gefenet al. 2003, Verhagen et al. 2006, Chen and Barnes2007) reveal that trust is a significant determinant ininfluencing consumers’ E-Commerce transactions, as alack of trust discourages consumers from making atransaction. More recently, a number of studies (Siauet al. 2004, Xu and Gutierrez 2006, Mallat 2007)indicate that trust is also a significant determinant ofconsumers’ decisions to engage in M-Commercetransactional tasks. Lin and Wang (2006) also foundthat trust has a positive impact on consumer loyaltyand satisfaction towards M-Commerce. Thus, trust isan important component of any model seeking toexplain a consumers’ WMPay.

Thus, having reflected on prior research, this studyexamines the impact of trust (trust), PI, PEU, PU, andMSE, in order to develop a model explainingconsumers’ willingness to use Smart Phones to makeM-Payments. The following discussion describes thedevelopment of the constructs used in this study.

Trust

A user’s feelings of trust towards an online service is animportant determinant in considering its usage (Chauet al. 2007, Roca et al. 2008). Sanchez-Franco andRondan-Cataluna (2011) believe trust is the mostimportant antecedent. Lie et al. (2010) found that trustis crucial in M-Commerce, given the anonymousbuyer–seller interactions and lack of formal contrac-tual agreements, while Varnali and Toker (2009)consider a lack of trust as a major obstacle in theadoption of mobile services. Similarly, Mallat (2007)found that trust in vendors and MNOs is essential toreduce consumers perceived risks of M-Payments.

We therefore present our first hypothesis:

Hypothesis 1: Consumers’ trust positively impactsupon their willingness to make M-Payments usingSmart Phones.

However, trust is a multidimensional construct,studied in a variety of social science disciplines(Bhattacherjee 2002) and with a multitude of defini-tions (Hsu et al. 2007). Thus, Roca et al. (2008) suggestthat, by considering trust as a reflection in different

dimensions, a better understanding of trust as aconstruct can be achieved. Thus, a thorough reviewof the literature reveals seven manifest variables oftrust (Table 1).

Shortcomings in security controls reduce consu-mer’s trust in M-Payment systems and hinder theemergence of these systems (Chou et al. 2004, Dewanand Chen 2005). When online vendors have imple-mented the appropriate security mechanisms, consu-mers perceive online purchasing as being safe (Rocaet al. 2008). Perceived privacy control is also a criticalfactor in consumers’ acceptance of online services, asconsumers are reluctant to share any personal orfinancial information with online vendors because theyfeel that these vendors could use this information forunintended purposes. In order to protect customers’privacy, organisations must protect all the personalinformation, which they collect either directly orindirectly from other organisations (Wu and Tsang2008).

If individuals perceive a vendor to be honest or ofhigh integrity, their intention to use the electronicchannel will be higher (Roca et al. 2008). Roca et al.(2008) suggest individuals will have greater trust in anelectronic channel if they are less concerned aboutunauthorised use of, or illegal access to, their data bythird parties. Privacy policies (Flavian and Guinalıu2006) and Social Media feedback mechanisms (Lor-enzo-Romero et al. 2011) convey signals of onlinevendor integrity. Privacy policies (Chen et al. 2011)and guarantee policies (Chiu et al. 2009), which areassociated with the ethical perception of web vendorsin terms of their ability to handle sensitive consumerinformation and consumers’ rights and interests, play asignificant role in influencing consumer trust.

Yang et al. (2009) reveal higher levels of perceivedethical commitment also increases trust and heavilyinfluences online purchasing decisions. Flavian andGuinalıu (2006) and Sanchez-Franco and Rondan-Cataluna (2011) suggest perceived competence is alsoparticularly important for an online vendor as theyhave to persuade the consumer that, in addition tobeing honest and reliable, they also have the technical,financial and human resources required to completethe transaction successfully.

Consumer trust in vendor compliance with legisla-tion and the existence of an independent regulatoryauthority to protect and regulate transactions and dataare essential to reduce consumers perceived risks ofmaking an M-Payment (Cleff 2007). Regulatory safe-guards promote consumer confidence in engaging inonline transactions, and online vendors should prior-itise their support for regulation (Sanchez-Franco andRondan-Cataluna 2011). It is important that anindependent objective regulator and the government

Behaviour & Information Technology 321

should play central roles in establishing legislation andstandards of service (Cheung and Lee 2003). Onlinevendors can minimise uncertainty by clearly displayingtheir rules and all the necessary legal aspects and sealsof approval (e.g. VeriSign and TRUSTe) (Sanchez-Franco and Rondan-Cataluna 2011).

Personal innovativeness

Agarwal and Prasad (1998) validated a construct forthe domain of information technology called ‘personalinnovativeness in the domain of IT’ (PIIT) forcharacterising technology adoption, which is definedas ‘the willingness of an individual to try out any newinformation technology’. Personal innovativeness isspecific to an individual (Agarwal and Prasad 1998),and it is the same as innate innovativeness, which ispart of an individual’s personality (Im et al. 2003).Innate innovativeness had a positive impact on drivingconsumer acceptance of mobile marketing (Bauer et al.2005), and these first adopters often become a sourceof opinion on innovations for their peers (Barmecha2011). Similarly, Gupta et al. (2011) suggest that PIhad a significant impact on intention to use mobileLBS. In addition, Lu et al. (2005) report that PIIT is animportant stimulus influencing perceptions of wirelessInternet services via mobile technology, and that PITTsignificantly influences both PU and PEU, with thelatter being particularly affected. Thus, in the contextof this study, we propose that:

Hypothesis 2a: Personal innovativeness positivelyimpacts upon consumers’ perceptions of the ease ofuse of a Smart Phone to make an M-Payment.Hypothesis 2b: Personal innovativeness positivelyimpacts upon consumers’ willingness to make M-Payments using Smart Phones.Hypothesis 2c: Personal innovativeness positivelyimpacts upon consumers’ perceptions of the usefulnessof a Smart Phone to make an M-Payment.

Perceived ease of use and perceived usefulness

Ease of use has been documented in the extantliterature as being an imminent acceptance driver ofmobile applications (Schierz et al. 2010). A review ofthe literature revealed a small number of researchersemployed TAM to explore M-Payments. Viehland andYoong Leong (2010) and Dahlberg et al. (2007)examined PU and PEU on consumer willingness touse M-Payment services at retail points-of-sale andreport that most consumers consider M-Payments easyto use and useful. Schierz et al. (2010) note that ease ofuse becomes even more important for M-Paymentservices, which compete with established paymentsolutions, and thus need to provide benefits when it

comes to ease of use. Therefore, one of the mainreasons for the slow diffusion of M-Payments inparticular could be a failure in understanding theperception among consumers of the ease of use ofmaking M-Payments using Smart Phones. Thus,having explored extant literature on PEU and PU,we propose that:

Hypothesis 3a: Perceived ease of use will have apositive effect on consumers’ willingness to use SmartPhones to make M-Payments.Hypothesis 3b: Perceived usefulness will have apositive effect on consumers’ willingness to use SmartPhones to make M-Payments.

Perceived mobile self-efficacy

Self-efficacy refers to one’s belief in what they can dowith the capability or skills they have (Hsu et al. 2011)or in their capability to perform a particular behaviour(Lai 2008). According to Bandura (1994), the natureand scope of perceived self-efficacy undergoes severalchanges as new and emerging competency demandsarise, which require further development of self-efficacyto function successfully. Evidence of this exists in theliterature as measures for perceived self-efficacy haveemerged for computer self-efficacy, Internet self-effi-cacy and, in recent times, MSE. Computer self-efficacymeasures one’s confidence in mastering a new technol-ogy or software with a certain degree of confidence (Lai2008). Internet self-efficacy specifically relates to usageof E-Commerce, as it requires a skill set beyond simplecomputer use (Keith et al. 2011). Young Hoon et al.(2009) note that E-Commerce transaction self-efficacy,as a situation-specific self-efficacy, positively influencesa consumer’s online purchase intention. Evidence ofthis may be emerging in recent M-Commerce literature,as Lee et al. (2011) report that MSE has a significantinfluence on attitude towards consumers’ willingness toadopt mobile advertising. Furthermore, Igbaria andIivari (1995) suggest that computer self-efficacy had a‘strong direct effect on perceived ease of use’ (p. 587),underlining its importance in the decision to usetechnology. Evidence of this also exists in the M-Commerce literature as Chen et al. (2011) tested TAMin their recent study on Smart Phone acceptance andconclude that MSE played a positive role on PEU.However, irrespective of whichever form of technology-related self-efficacy arises in the literature, knowledgeand confidence play an important role (Khorrami-Arani 2001) as do judgments of what one can do withthe skill-set one possesses (Bandura 1994). Thus, in thiscontext, we propose that:

Hypothesis 4a: Mobile self-efficacy positively impactsupon consumers’ PEU in using Smart Phones to makeM-Payments.

A. Duane et al.322

Hypothesis 4b: Mobile self-efficacy positively impactsupon consumers’ willingness to use Smart Phones tomake an M-Payment.

According to Bandura (1986), a self-efficacyinstrument must assess the specific skills needed forperforming an activity. Given that over 300,000 mobileapplications (Apps.) have been developed in the last 3years (MobiThinking 2011), and this study does notexclusively focus on MSE, it is simply not possible atthis time to create a self-efficacy measure capable ofprecisely assessing the specific skills needed to use eachApplication (App). Therefore, the researchers utiliseda grounded approach in this regard, adopting theapproach recommended by Vispoel and Chen (1990)who advised researchers to develop new, or signifi-cantly revise existing, measures for each study of self-efficacy. Thus, a number of indicators of self-efficacywere developed for use in this study through adoptionand extension of extant literature. These items arepresented in the indicator descriptor table (Table 2).

Therefore, through a detailed review of theliterature, four hypotheses emerged, enabling thegeneration of a research model, presented in Figure1, to investigate consumers’ willingness to use SmartPhones to make M-Payments.

Willingness to make an M-Payment

Most measures of willingness to make an electronicpayment, and in some cases an M-Payment (e.g.

Viehland and Yoong Leong 2010), reflect on previousmeasures established in the marketing literature thatsimply measure ‘price sensitivity’. The purpose ofwillingness to make M-Payment in this study is not tostudy price sensitivity with respect to mobile purchasesbut rather consumers’ willingness to use the ‘M-Payment Process’ as previously referred to in theIntroduction section. However, one must recognisethat the M-Payment market is still in its infancy, andno single M-Payment model has emerged as the defacto and may not do so for a considerable period oftime given the lucrative market that exists and thatrival services will continue to compete with each otherand invest significant amounts of money in acquisi-tions and research (Ondrus and Lyytinen 2011). Thus,different mobile vendors adopt different M-Paymentmodels, and consequently consumers currently interactwith multiple M-Payment models and will continue todo so for the foreseeable future.

Ondrus and Lyytinen (2011) suggest that ‘it is stillpremature to conclude any certain scenarios. Theupcoming announcements of the new players willprobably give more insights into the variability offuture scenarios for mobile payments’. Measurementof WMPay in this study embraces this idea and reflectsconsumers’ WMPay using all four current M-Paymentmodels in the marketplace: MNO driven (e.g. O2),third-party driven (e.g. PayPal), credit card companydriven (e.g. Visa) and domestic bank driven (laser debitcard – similar to Maestro) driven. Ondrus et al. (2009)posit ‘that there is a lack of multiperspective researchthat is needed to obtain a holistic view of paymentsystem adoption and evolution. In addition, we need toconduct research that follows more than just oneperspective at a time’. Thus, this research develops anew measure for WMPay to reflect the current state ofresearch. This measure reflects the M-Payment modelsidentified by Ondrus et al. (2009) of M-Maestro,PostFinance and Verified by Visa.

Method

Design

An online survey was developed to operationalise theresearch model. Following an initial iteration of thesurvey as per Hair et al. (2006), the authors pretestedthe survey with Smart Phone ‘experts’ (active SmartPhone owners and users) in order to assess thesemantic content of construct items. The authorsretained those items that best fitted and reflected thedefinitions of the constructs, a process that facilitatedthe refinement and streamlining of the items includedin this survey. In order to minimise non-response bias,we utilised some of the principles purported by Vicenteand Reiss (2010) pertaining to designing web-

Table 1. Trust measures for this study.

Element Literature

Perceived Security Control Chou et al. 2004, Dewan andChen 2005, Roca et al.2008

Perceived Privacy Control Roca et al. 2008, Wu andTsang 2008

Perceived Integrity Cheung and Lee 2003,Flavian and Guinalıu2006, Roca et al. 2008,Lorenzo-Romero et al.2011

Perceived EthicalCommitment

Chiu et al. 2009, Yang et al.2009, Chen et al. 2011,Sanchez-Franco andRondan-Cataluna 2011

Perceived Competence Flavian and Guinalıu 2006,Sanchez-Franco andRondan-Cataluna 2011

Perceived Governance Cheung and Lee 2003, Cleff2007, Sanchez-Franco andRondan-Cataluna 2011

Perceived Independence ofRegulatory Authority

Cheung and Lee 2003, Cleff2007, Sanchez-Franco andRondan-Cataluna 2011

Behaviour & Information Technology 323

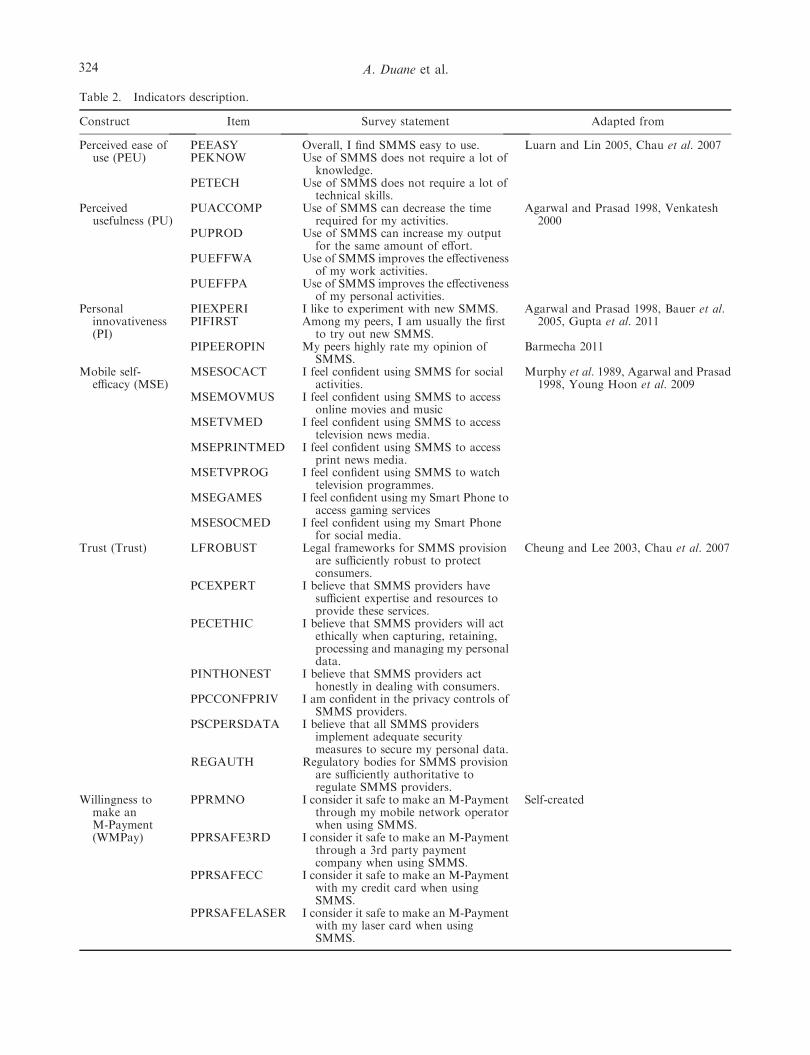

Table 2. Indicators description.

Construct Item Survey statement Adapted from

Perceived ease ofuse (PEU)

PEEASY Overall, I find SMMS easy to use. Luarn and Lin 2005, Chau et al. 2007PEKNOW Use of SMMS does not require a lot of

knowledge.PETECH Use of SMMS does not require a lot of

technical skills.Perceived

usefulness (PU)PUACCOMP Use of SMMS can decrease the time

required for my activities.Agarwal and Prasad 1998, Venkatesh

2000PUPROD Use of SMMS can increase my output

for the same amount of effort.PUEFFWA Use of SMMS improves the effectiveness

of my work activities.PUEFFPA Use of SMMS improves the effectiveness

of my personal activities.Personal

innovativeness(PI)

PIEXPERI I like to experiment with new SMMS. Agarwal and Prasad 1998, Bauer et al.2005, Gupta et al. 2011PIFIRST Among my peers, I am usually the first

to try out new SMMS.PIPEEROPIN My peers highly rate my opinion of

SMMS.Barmecha 2011

Mobile self-efficacy (MSE)

MSESOCACT I feel confident using SMMS for socialactivities.

Murphy et al. 1989, Agarwal and Prasad1998, Young Hoon et al. 2009

MSEMOVMUS I feel confident using SMMS to accessonline movies and music

MSETVMED I feel confident using SMMS to accesstelevision news media.

MSEPRINTMED I feel confident using SMMS to accessprint news media.

MSETVPROG I feel confident using SMMS to watchtelevision programmes.

MSEGAMES I feel confident using my Smart Phone toaccess gaming services

MSESOCMED I feel confident using my Smart Phonefor social media.

Trust (Trust) LFROBUST Legal frameworks for SMMS provisionare sufficiently robust to protectconsumers.

Cheung and Lee 2003, Chau et al. 2007

PCEXPERT I believe that SMMS providers havesufficient expertise and resources toprovide these services.

PECETHIC I believe that SMMS providers will actethically when capturing, retaining,processing and managing my personaldata.

PINTHONEST I believe that SMMS providers acthonestly in dealing with consumers.

PPCCONFPRIV I am confident in the privacy controls ofSMMS providers.

PSCPERSDATA I believe that all SMMS providersimplement adequate securitymeasures to secure my personal data.

PPRMNO I consider it safe to make an M-Paymentthrough my mobile network operatorwhen using SMMS.

Self-created

PPRSAFE3RD I consider it safe to make an M-Paymentthrough a 3rd party paymentcompany when using SMMS.

PPRSAFECC I consider it safe to make an M-Paymentwith my credit card when usingSMMS.

PPRSAFELASER I consider it safe to make an M-Paymentwith my laser card when usingSMMS.

A. Duane et al.324

distributed questionnaires. Through a review andanalysis of the extant literature, they illustrated that,by applying such principles, the risk of non-responsebias is greatly reduced. Therefore, we employed thoseprinciples in this study: screen design layout, avoidedlengthy questions, included an intermittent progressindicator and applied a radio button format. In dealingwith the danger of common method bias, we began byutilising the principles of Podsakoff et al. (2003). Weobtained measures of the predictor and criterionvariables from multiple sources (further, constructreliability tests were conducted [Assessment of mea-surement models section] within the measurement PLSmodels validation). Furthermore, we ensured thequestionnaire was anonymous and avoided the use ofcomplicated and ambiguous wording.

The next phase of this research posted the surveyonline using a web-based survey administration toollocated at www.SurveyMonkey.com. The target popu-lation of users were informed of this survey by postinga survey notification and weblink on an Irish SmartPhone users’ discussion group located at www.Board-s.ie. This online group had 928 members with averagemonthly user activity rates of 42%. Responses werecollected throughout June 2010. Irish Smart Phoneusers were selected as the target population as therehad been no research conducted on M-Payments inIreland to our knowledge, despite Ireland having one

of the largest rates of mobile phone usage in Europeper head of population, with a 117.3% penetration rateas of December 2010 (ComReg 2011). In fact, one outof every two mobile phones sold in Ireland in 2010were Smart Phones (Vodafone-Ireland 2010).

In operationalising the constructs, indicators aris-ing from the literature were either wholly adopted orrevised in order to develop questions for data collec-tion. In addition, the researchers created a number ofnew measures to measure consumers’ WMPay. Table 2presents these indicators, their associated questions andtheir sources in the literature where applicable.

Data analysis

The study employed structural equation modelling, amodel-testing tool, for data analysis and hypothesestesting. Choosing the PLS (SEM) approach, whichuses component-based estimation, is appropriate sinceit allows simultaneous exploration of both the mea-surement and the structural models. In addition, thePLS approach compared to covariance-based SEMallows for testing of the relationships in the model withless restrictive requirements. Another reason forchoosing PLS is that this tool is considered to beappropriate for testing theories at earlier stages ofdevelopment (Fornell and Bookstein 1982) as in thecontext of this study. This technique facilitates theexploration of two models: the measurement (outer)model, relating the measurement variables to theirlatent variables (LVs); and the structural (inner)model, relating the LVs to each other (Chatelin et al.2002, Tenenhaus et al. 2005, Diamantopoulos 2006).

Results

Data statistics

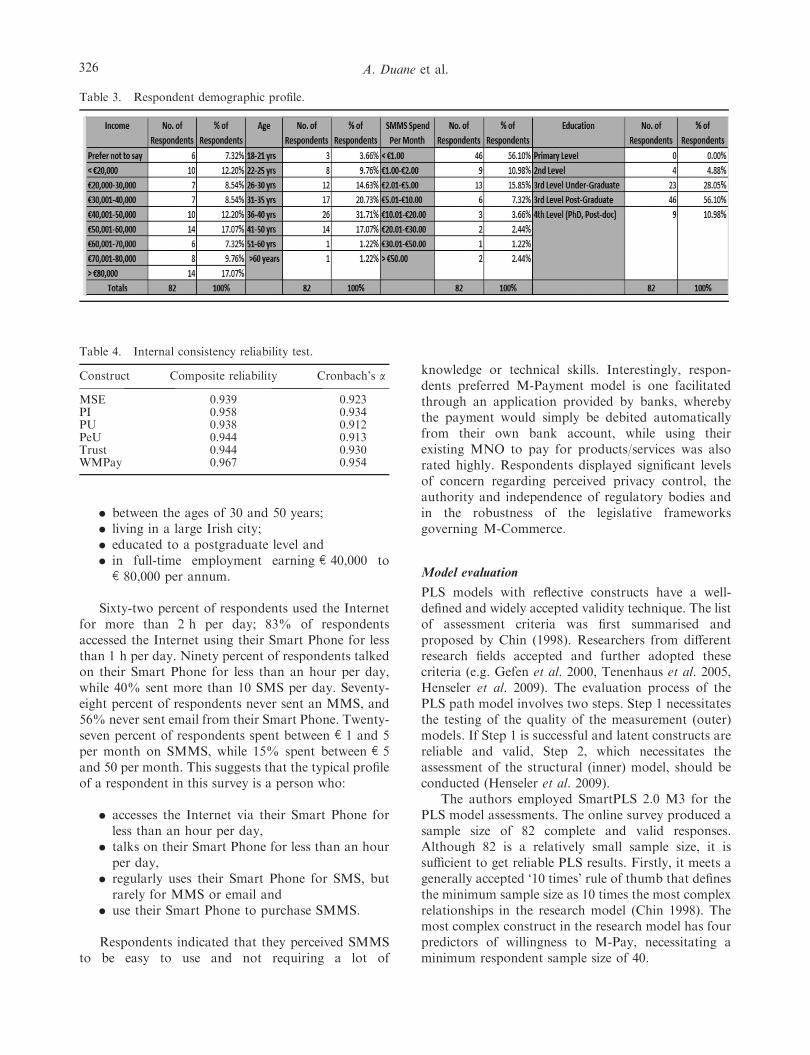

One month after posting the survey notification andweblink to the Irish Smart Phone users’ discussiongroup located at www.Boards.ie, the authors closed thesurvey collection mechanism located at www.Survey-Monkey.com. Analysis of the online survey hosted onSurvey Monkey revealed that 141 of the 928 IrishSmart Phone Users’ online discussion group invited toparticipate in the study had responded. However, only82 of the responses were deemed valid, as 59respondents had failed to complete the entire survey,primarily citing the high number of questions in thesurvey as the reason for abandoning the survey beforecompletion. Despite this, respondents originated from12 of Ireland’s 26 countries including large cities suchas Dublin, Cork and Waterford, which when combinedaccounted for 68% of respondents. As shown in Table3, the demographic attributes of a respondent to thissurvey is a person:

. in full-time employment earning e 40,000 toe 80,000 per annum.

Sixty-two percent of respondents used the Internetfor more than 2 h per day; 83% of respondentsaccessed the Internet using their Smart Phone for lessthan 1 h per day. Ninety percent of respondents talkedon their Smart Phone for less than an hour per day,while 40% sent more than 10 SMS per day. Seventy-eight percent of respondents never sent an MMS, and56% never sent email from their Smart Phone. Twenty-seven percent of respondents spent between e 1 and 5per month on SMMS, while 15% spent between e 5and 50 per month. This suggests that the typical profileof a respondent in this survey is a person who:

. accesses the Internet via their Smart Phone forless than an hour per day,

. talks on their Smart Phone for less than an hourper day,

. regularly uses their Smart Phone for SMS, butrarely for MMS or email and

. use their Smart Phone to purchase SMMS.

Respondents indicated that they perceived SMMSto be easy to use and not requiring a lot of

knowledge or technical skills. Interestingly, respon-dents preferred M-Payment model is one facilitatedthrough an application provided by banks, wherebythe payment would simply be debited automaticallyfrom their own bank account, while using theirexisting MNO to pay for products/services was alsorated highly. Respondents displayed significant levelsof concern regarding perceived privacy control, theauthority and independence of regulatory bodies andin the robustness of the legislative frameworksgoverning M-Commerce.

Model evaluation

PLS models with reflective constructs have a well-defined and widely accepted validity technique. The listof assessment criteria was first summarised andproposed by Chin (1998). Researchers from differentresearch fields accepted and further adopted thesecriteria (e.g. Gefen et al. 2000, Tenenhaus et al. 2005,Henseler et al. 2009). The evaluation process of thePLS path model involves two steps. Step 1 necessitatesthe testing of the quality of the measurement (outer)models. If Step 1 is successful and latent constructs arereliable and valid, Step 2, which necessitates theassessment of the structural (inner) model, should beconducted (Henseler et al. 2009).

The authors employed SmartPLS 2.0 M3 for thePLS model assessments. The online survey produced asample size of 82 complete and valid responses.Although 82 is a relatively small sample size, it issufficient to get reliable PLS results. Firstly, it meets agenerally accepted ‘10 times’ rule of thumb that definesthe minimum sample size as 10 times the most complexrelationships in the research model (Chin 1998). Themost complex construct in the research model has fourpredictors of willingness to M-Pay, necessitating aminimum respondent sample size of 40.

Reliability. The first criterion in the assessment ofmeasurement models is reliability, which traditionallyrefers to internal consistency reliability and indicatorreliability. Internal consistency reliability correspondsto testing either Cronbach’s a, which indicates an

estimation of the reliability assuming that all items areequally reliable or composite reliability, where differentitem loadings are taken into account. Although thosetwo reliability measures differ, either of them may beused. Table 4 shows that both parameters have highvalues (all values are above 0.912), as the requirementvalue is only required to be above 0.7 in the early

Table 5. Construct cross-correlation matrix and AVE analyses.

AVE Construct MSE PI PU PeU Trust WMPay

0.689 MSE 0.8300.883 PI 0.632 0.9400.792 PU 0.395 0.425 0.8900.850 PeU 0.548 0.438 0.363 0.9220.707 Trust 0.380 0.373 0.318 0.363 0.8410.878 WMPay 0.409 0.345 0.412 0.428 0.685 0.937//

Figure 2. PLS results of measurement and structural models.

.Behaviour & Information Technology 327

stages of research and above 0.8–0.9 in the advancedstages (Henseler et al. 2009).

Individual reliability of the indicators relies on theexpectation that LV variance should explain at least50% of the indicator. In other words, loadings ofmanifest variables should not be less than 0.707 (Chin1998, Gefen et al. 2000, Henseler et al. 2009). Figure 2demonstrates that the magnitude of all indicators ishigher than the required value of 0.707. Based on thetwo tests, the authors can conclude that all indicatorsare reliable.

Validity. Convergent validity and discriminant validityexamine the validity of four reflective constructs. Thefirst column in Table 5 shows that the average varianceextracted (AVE) for all constructs is higher than 0.5,which indicates sufficient convergent validity andmeans that each LV explains more than 50% of theirindicator variance on average. Discriminant validityrefers to the appropriate patterns of the interindicators of a construct and other constructs. First,the variance of a construct should be aligned morewith their own indicators than with other constructs.For this purpose, we compared construct cross-correlation and the square root of each construct’sAVE. Table 5 illustrates that all constructs havesufficient discriminant validity since the square root

of each latent construct’s AVE (values on the diagonal)is much larger than the correlation of the specificconstruct with any other reflective construct in ourresearch model.

The authors also tested discriminant validity with across-loading test. Table 6 presents results of the testand demonstrates that an indicator of any specificconstruct has a higher loading on its own constructthan on any other constructs. The results of the testsshow that manifest variables (indicators) presented inthe research model are reliable and valid.

Assessment of the structural model

In assessing the explanatory and predictive power ofthe structural model, the authors employed therecommendations included in extant research (Chin1998, Gefen et al. 2000, Chatelin et al. 2002, Andreevet al. 2009, Henseler et al. 2009).

Explanatory power

Figure 3 presents an overview of the structuralmodel evaluation results. The central criterion forevaluating the structural model is the level ofexplained variance of the dependent construct will-ingness to MPay, for which the R2 was 0.534. Thus,

the model explained 53.4% of the construct’svariance. The variance of the construct was ex-plained at the moderate level consistent with Chin’s(1998) criteria. R2 values of 0.67, 0.33 or 0.19 forendogenous LVs are substantial, moderate or weak,respectively (Chin 1998, p. 323).

In addition, within the research model, MSE andPI explain 31.4% of the PEU variance, while thevariance of PU is explained by PI (18.1%).

The study explored changes in R2 to investigate thesubstantive impact of each independent construct onthe dependent constructs, carrying out the effect sizetechnique by re-running three PLS estimations, ex-cluding in each run, one of the explaining latentconstructs. Table 7 represents a summary of thequantitative results of the effect size test. Chin (1998)proposed to use the effect size f2 of PLS constructs,which similar to Cohen’s implementation for multipleregression might be small (f2 ¼ 0.02), medium(f2¼0.15) and large (f2 ¼ 0.35).

The results of the effect size (Table 7) show thatwhile PEU and PU have small effects (with f2 equals to0.026 and 0.047, respectively), on consumers’ will-ingness to use a Smart Phone to make an M-Payment,Trust has a large effect with magnitude of f2 ¼ 0.545.

Predictive power

Employing the bootstrapping re-sampling technique,using the SmartPLS software, enabled a test for thestatistical significance of the path coefficients. Theevaluation of the structural model shows that all pathcoefficients were highly statistically significant (Figure3). The study found that, Trust (H1 supported withb ¼ 0.569 and p 5 0.001), PU (H3b supported withb ¼ 0.171 and p 5 0.001), and PEU (H3a supportedwith b ¼ 0.136 and p 5 0.001) positively affect con-sumers’ willingness to use a Smart Phone to make anM-Payment.

Personal Innovativeness positively affected bothPEU (H1a supported with b ¼ 0.153 and p 5 0.01),and PU (H1c supported with b ¼ 0.425 and p 50.001).

Mobile self-efficacy positively affected PEU (H4asupported with b ¼ 0.452 and p 5 0.001). However,impacts of both MSE and PI on consumers’ willingnessto use a Smart Phone to make an M-Payment werefound to be statistically insignificant (H2b and H4b arenot supported).

The authors performed the Stone and Geisser Q2

test for the evaluation of the predictive relevance of thestructural model. Chin (1998) stated that Q2 reflects anindex of goodness of reconstruction by model andparameter estimations. A positive Q2 provides evidencethat the omitted observations were well-reconstructedand that predictive relevance is achieved, while anegative Q2 reflects absence of predictive relevance.Table 8 shows that all values of Q2 were greater thanzero, indicating predictive relevance for the endogen-ous constructs of the research model.

Discussion and conclusions

By exploring consumers’ willingness to use SmartPhones to make M-Payments, this paper makes a

number of significant theoretical and practical con-tributions of value to both researchers and practi-tioners. Both of these will now be discussed.

Theoretical contribution

Consumer intention to use Smart Phones for transac-tional services and M-Payment is of scientific andpractical interest. In this study, we sought to extend thetheoretical knowledge of M-Payment adoption, bydeveloping a model explaining consumers’ willingnessto use Smart Phones to make M-Payments. Indeed, thispaper makes a number of theoretical contributions tothe M-Payments literature. Firstly, it contributes aconceptual model for exploring consumer’s perceptionsof M-Payments and in developing same several factorswhich had not been previously been applied to the M-Payments domain were incorporated. The studyadopted and empirically tested a number of constructspreviously recognised in extant literature as beinginfluential in consumers’ decision to adopt mobileadvertising, mobile marketing, LBS, mobile banking,M-Commerce, and E-Commerce in general. Theseconstructs have previously not been used in a singlestudy focussing on the willingness of European con-sumers to use Smart Phones to make M-Payments.Four main hypotheses (divided into a number of sub-hypothesis) were proposed and the results providestrong support for the theoretical predictions. Severalimplications for theory were identified from theseresults.

Viehland and Yoong Leong (2010) state that PEUand trust impact on consumers’ WMPay using a SmartPhone. However, both factors are treated the samewith no differentiation being made between thesefactors. The results from this study extend extantresearch by clearly differentiating between these factorsin terms of impact, illustrating that trust is the criticalfactor in explaining consumers’ WMPay using SmartPhones, while the impact of PEU is significantly less.This is significant as it contradicts the findings ofSchierz et al. (2010), which suggest that ease of use isvery important for M-Payment services, which com-pete with established payment solutions, and thus needto provide benefits when it comes to ease of use. Ourfindings show that although PEU is important, it is notactually a key factor in explaining the slow diffusion ofM-Payments using Smart Phones.

While Lee et al. (2011) found that MSE had asignificant impact on consumers’ willingness to adoptmobile advertising, the results of this study clearlyillustrate that MSE has only a small impact onconsumers’ willingness to use a Smart Phone to makean M-Payment. However, the results show that MSEdoes have a significant impact on PEU. This is

consistent with the findings of Chen et al. (2011).These results may indicate that while consumers areconvinced of the ease of use of SMMS, they stillharbour suspicion and significant concerns aboutmaking an M-Payment using a Smart Phone. Theauthors strongly recommend that future studies shoulddevelop and test more extensive measures of MSE as itrelates to M-Payments, given the vast number ofSMMS available to consumers and the difficulties theirinherent differences pose in measuring MSE in an M-Commerce environment.

Agarwal and Prasad (1998) validated PIIT forcharacterising technology adoption. Previous studiesof the impact of PI on mobile marketing (Bauer et al.2005) and mobile LBS (Gupta et al. 2011) indicatedthat it influences the adoption of both types of SMMS.This study reveals, however, that although PI stronglyinfluences consumers’ perceptions of the usefulness ofa Smart Phone to make an M-Payment, PI has verylittle direct impact on consumers’ willingness to use aSmart Phone to make an M-Payment. Personalinnovativeness also has a small impact on consumer-s’PEU of a Smart Phone to make an M-Payment.Thus, while our study does not reflect the findings ofGupta et al. (2011), further research could consider themoderating effects of PI, similar to Agarwal andPrasad (1998), rather than the direct impact onconsumers’ WMPay. As previously stated, M-Pay-ments are still in their infancy in Europe, and clearlyestablished mechanisms have yet to emerge. Thus,future studies could reflect upon the differentiation ofinnate PI and actual PI by Im et al. (2003) and measureactual adoption of M-Payments.

Implications for practice and future research

Smart Phones present organisations with a significantamount of commercial opportunities. For commer-cial organisations to avail of such opportunities, anunderstanding of consumer’s perceptions of SmartPhones is of paramount importance. Yet, both thepractitioner and academic literature, particularly in aEuropean context, are immature in explainingconsumer adoption of M-Payments using SmartPhones.

The findings of this study present conclusiveevidence that trust is the single most important factorinfluencing consumers’ willingness to use SmartPhones to make M-Payments. Perceived usefulnessand PEU do influence the payment decision, but theyare less important, while MSE and PI have almost noimpact. It is clear then that, irrespective of individuals’displaying high levels of PI, or MSE, and irrespectiveof whether the SMMS is perceived to be useful andeasy to use, consumers will not make M-Payments

A. Duane et al.330

unless they are convinced of the payment reliability ofthe Smart Phone M-Payment system.

Our analysis illustrates that consumer’s perceptionsof privacy controls, legal frameworks and the regula-tion of these frameworks are integral parts of trust inan M-Commerce environment and critical for con-sumers’ willingness to use Smart Phones to make M-Payments. Similar to the study of consumer acceptanceof online services by Roca et al. (2008), perceivedprivacy control emerges in this study as a critical factorin consumers’ willingness to use Smart Phones to makean M-Payment. These findings are very important forpractitioners, and a number of suggestions can bepurported through interpreting our findings. Firstly,commercial entities need to communicate to consumersthat they implement policies and employ the latesttechnologies to protect the privacy and data ofconsumers. For government and commercial entitieswho wish to develop an M-Payment culture, theauthors suggest that these entities review their legalframeworks, with the goal being to ensure that they areadequate to protect consumers. Furthermore, consu-mers’ perception of regulatory bodies having sufficientpowers to take action against service providers who donot adhere to such frameworks is an issue requiringfurther detailed research.

The authors advise that it is possible that PEU maybecome a more important mitigating factor as M-Payment services become more established, and con-sumers’ have a greater choice of which M-Paymentmodel to actually use, because the preferred M-Payment model for Irish consumers is one facilitatedthrough an application provided by banks, wherebythe payment would simply be debited automaticallyfrom their own bank account. Thus, it is possible thatPEU may in future actually influence consumers’choice of which M-Payment model to use, ratherthan their decision to use a Smart Phone to make anM-Payment. The authors therefore recommend that asM-Payment models mature and consumers’ have agreater choice of which M-Payment models to adopt,further studies investigate PEU between the offeringsin more detail.

Although this paper reveals important findings forthe development of theoretical models and practi-tioners alike, nevertheless, there are a number oflimitations to this study. The sample size represents alimitation of the study, with findings based on 82respondents participating in the study. Therefore,further research needs to be conducted to re-examinethe model with a larger sample size. Furthermore, themajority of respondents to this survey were agedbetween 30 and 50 years; thus, future research couldconsider a multigroup analysis to see if the model isinvariantly consistent (e.g. across gender and age

groups). This research also is limited to Smart Phoneconsumers in Ireland, thus a wider European study isrequired. The authors are currently completing furtherresearch to investigate the explanatory power of themodel for different sociodemographic groups and forspecific products/services. Such research may providefurther insight on the impact of PEU on M-Payments.Furthermore, steps are underway to further test themodel in the context of evaluating consumer adoptionof the various M-Payments models available usingSmart Phones.

Note

1. The t-test for each path coefficient was conducted withn71degrees of freedom,where n is a numberof subsamplerepetitions in bootstrapping procedure; 300 repetitionswere chosen resulting in 299 degrees of freedom.

References

Agarwal, R. and Prasad, J., 1998. A conceptual andoperational definition of personal innovativeness in thedomain of information technology. Information SystemsResearch, 9 (2), 204–215.

Andreev, P., Duane, A., and O’Reilly, P., 2011. Conceptua-lising consumer perceptions of contactless m-paymentsthrough smart phones. International Federation forInformation Processing: IFIP WG8.2.

Andreev, P., et al., 2009. Validating formative partial leastsquares (pls) models: methodological review and empiri-cal illustration. ICIS 2009 Proceedings.

Bandura, A., 1986. Social foundations of thought and action: asocial cognitive theory. Englewood Cliffs, NJ: Prentice-Hall.

Bandura, A., ed., 1994. Self-efficacy. Encyclopedia of humanbehavior. New York: Academic Press.

Barmecha, M., 2011. Commerce for the digital consumer.Building tomorrow’s enterprise. InfoSys.

Barutcu, S., 2008. Consumers’ attitudes towards mobilemarketing and mobile commerce in consumer markets.Ege Academic Review, 8 (1), 15–32.

Bauer, H.H., et al., 2005. Driving consumer acceptance ofmobile marketing: a theoretical framework and empiricalstudy. Journal of Electronic Commerce Research, 6 (3),181–192.

Bhattacherjee, A., 2002. Individual trust in online firms: scaledevelopment and initial test. Journal of ManagementInformation Systems, 19 (1), 211–241.

Chatelin, Y.M., Vinzi, V.E., and Tenenhaus, M., 2002. State-of-art on PLS path modeling through the availablesoftware. Les Cahiers de Recherche, 764, Groupe HEC.

Chau, P.Y.K., et al., 2007. Examining customers’ trust inonline vendors and their dropout decisions: an empiricalstudy. Electronic Commerce Research and Applications, 6(2), 171–182.

Chen, K., Chen, J.V., and Yen, D.C., 2011. Dimensions ofself-efficacy in the study of smart phone acceptance.Computer Standards and Interfaces, 33 (4), 422–431.

Chen, Y.H., and Barnes, S., 2007. Initial trust and onlinebuyer behaviour. Industrial Management and DataSystems, 107 (1), 21–36.

Behaviour & Information Technology 331

Cheung, C.M.K. and Lee, M.K.O., 2003. An integrativemodel of consumer trust in internet shopping. ECISProceedings.

Chin, W.W., 1998. The partial least squares approach tostructural equation modeling. In: M.G.E. Mahwah, ed.Modern methods for business research. New Jersey:Lawrence Erlbaum Associates, 295–336.

Chiu, C.-M., et al., 2009. Understanding customers’ loyaltyintentions towards online shopping: an integration oftechnology acceptance model and fairness theory. Beha-viour and Information Technology, 28 (4), 347–360.

Chou, Y., Lee, C., and Chung, J., 2004. Understanding M-commerce payment systems through the analytic hierarchyprocess. Journal of Business Research, 57 (12), 1423–1430.

Chung, N. and Kwon, S.J., 2009. Effect of trust level onmobile banking satisfaction: a multi-group analysis ofinformation system success instruments. Behavior andInformation Technology, 28 (6), 549–562.

Cleff, E.B., 2007. Implementing the legal criteria of mean-ingful consent in the concept of mobile advertising.Computer Law and Security Report, 23 (3), 262–269.

ComReg. (2011. Commission for Communications Regula-tion Quarterly Key Data Report Data as of Q1 2011.Quarterly Key Data Reports. C. f. Communications, 77.

Dahlberg, T., et al., 2008. Past, present and future of mobilepayments research: a literature review. Electronic Com-merce Research and Applications, 7 (2), 165–181.

Dahlberg, T. and Oorni, A., 2007. Understanding changes inconsumer payment habits – do mobile payments andelectronic invoices attract consumers? HICSS, 50.

Dewan, S.G. and Chen, L., 2005. Mobile payment adoptionin the USA: a crossindustry, cross-platform solution.Journal of Information Privacy and Security, 1 (2), 4–28.

Diamantopoulos, A., 2006. The error term in formativemeasurement models: interpretation and modeling im-plications. Journal of Modelling in Management, 1 (1), 7–17.

Dinez, E., Albuquerque, J., and Cernez, A., 2011. Mobilemoney and payment: a literature review based onacademic and practitioner-oriented publications (2001-2011. Proceedings of SIG GlobDev Fourth Annual Work-shop, Shanghai, China.

Egger, F.N., and Abrazhevich, D., 2001. Security & trust:taking care of the human factor [online].Electronic paymentsystems observatory newsletter 9. Available from: http://www.ecommuse.com/en/articles. Accessed 19 July 2012.

Enterprise Ireland. 2011. M-Commerce and M-Payments[online]. Available from: http://www.ebusinesslive.ie/newsletter/Story/4/1828/ob.html/277. Accessed 15 July 2011.

Flavian, C. and Guinalıu, M., 2006. Consumer trust, per-ceived security and privacy policy: three basic elements ofloyalty to a web site. Industrial Management and DataSystems, 106 (5), 601–620.

Fornell, C. and Bookstein, F.L., 1982. Two structuralequation models: LISREL and PLS applied to consumerexit-voice theory. Journal of Marketing Research, 19 (4),440–452.

Gao, J. and Kupper, A., 2006. Emerging technologies formobile commerce. Journal of Theoretical and AppliedElectronic Commerce Research, 1 (2).

Gefen, D., Karahanna, E., and Straub, D.W.2003. Trust andTAM in online shopping: an integrated model. MISQuarterly, 27 (1), 51–90.

Gefen, D., Straub, D.W., and Boudreau, M.-C., 2000.Structural equation modeling and regression: guidelinesfor research and practice. CAIS, 4 (7), 1–70.

Goldman, S.M., 2010. Transformers. Journal of ConsumerMarketing, 27 (5), 469–473.

Gupta, S., Xu, H., and Zhang, X., 2011. Balancing privacyconcerns in the adoption of location-based services: anempirical analysis. International Journal of ElectronicBusiness, 9 (1/2), 118–137.

Hair, J.F., et al., 2006. Multivariate Data Analysis, NewJersey: Prentice Hall.

Henseler, J., Ringle, C.M., and Sinkovics, R.R., 2009. Theuse of partial least squares path modeling in internationalmarketing. Advances in International Marketing, 20, 277–319.

Higgs, B., 2008. Strategy notes: on location. Marketing,(Dec/Jan), 82–82.

Hsu, H.Y.S. and Kulviwat, S., 2006. An integrative frame-work of technology acceptance model and personalisa-tion in mobile commerce. International Journal ofTechnology Marketing, 1 (4), 393–410.

Hsu, M.H., Chang, C.M., and Yen, C.H., 2011. Exploringthe antecedents of trust in virtual communities. Behaviourand Information Technology, 30 (5), 587–601.

Hsu, M.H., et al., 2007. Knowledge sharing behavior invirtual communities: the relationship between trust, self-efficacy, and outcome expectations. International Journalof Human-Computer Studies, 65, 153–169.

Igbaria, M. and Iivari, J., 1995. The effects of self-efficacy oncomputer usage. Omega, 23 (6), 587–605.

Im, I., Kim, Y., and Han, H.J., 2008. The effects of perceivedrisk and technology type on users’ acceptance oftechnologies. Information & Management, 45 (1), 1–9.

Im, S., Bayus, B.L., and Mason, C.H., 2003. An empiricalstudy of innate consumer innovativeness, personal char-acteristics, and new-product adoption behavior. Journalof the Academy of Marketing Science, 31 (1), 61–73.

Jarvenpaa, S.L., Tractinsky, N., and Vitale, M., 2000.Consumer trust in an internet store. Information technol-ogy and management, 1 (1), 45–71.

Jayasingh, S. and Eze, U., 2009. An empirical analysis ofconsumer behavioural intention towards mobile couponsin malaysia. International Journal of Business andInformation, 4 (2), 221–242.

Juniper Research. 2010. Press Release: Mobile PaymentsMarket to Quadruple by 2014, reaching $630bn in value,although still only accounting for around 5% of ecommerceretail sales. Available from: http://juniperresearch.com/viewpressrelease.php?pr¼173. Accessed 5 July 2011.

Keith, M.J., et al., 2011. The role of mobile self-efficacy inthe adoption of location-based applications: an iphoneexperiment. Proceedings of the 44th Hawaii InternationalConference on System Sciences.

Kim, C., Mirusmonov, M., and Lee, I., 2010. An empiricalexamination of factors influencing the intention to usemobile payment. Computers in Human Behavior, 26 (3),310–322.

Kim, Y. and Zhang, P., 2009. Individual users’’ adoption ofsmart phone services. SIGHCI 2009 Proceedings, 19.

Lai, M.L., 2008. Technology readiness, internet self-efficacyand computing experience of professional accountingstudents. Campus-Wide Information Systems, 25 (1), 18–29.

Lee, C.-C., Hsieh, M.-C., and Huang, H.-C., 2011. Theinfluence of mobile self-efficacy on attitude towardsmobile advertising. AISS: Advances in InformationSciences and Service Sciences, 3 (3), 100–108.

Leppaniemi, M. and Karjaluoto, H., 2005. Factors influen-cing consumers’ willingness to accept mobile advertising:a conceptual model. International Journal of MobileCommunications, 3 (3), 197–213.

Lie, T., Fang, W., and Pavlou, P.A., 2010. The triangularrelationship among vendor, user and technology on trust inmobile commerce: a cross cultural comparison [online].Available from: www.ntpu.edu.tw/ads/doc/paper%20lee.doc.

Lin, H.H. and Wang, Y.S., 2006. An examination ofthe determinants of customer loyalty in mobile com-merce contexts. Information & Management, 43 (3), 271–282.

Lorenzo-Romero, C., Constantinides, E., and Alarcon-del-Amo, M.-D.-C., 2011. Consumer adoption of socialnetworking sites: implications for theory and practice.Journal of Research in Interactive Marketing, 5 (2/3).

Lu, J., Yao, J.E., and Yu, C.-S., 2005. Personal innovative-ness, social influences and adoption of wireless Internetservices via mobile technology. Journal of StrategicInformation Systems, 14 (3), 245–268.

Luarn, P. and Lin, H.H., 2005. Toward an understanding ofthe behavioral intention to use mobile banking. Compu-ters in Human Behavior, 21 (6), 873–891.

Mallat, N., 2007. Exploring consumer adoption of mobilepayments – a qualitative study. The Journal of StrategicInformation Systems, 16 (4), 413–432.

Matthews, T., Pierce, J., and Tang, J., 2009. No smart phoneis an island: the impact of places, situations, and otherdevices on smart phone use. Research Report RJ10452,IBM.

MobiThinking. 2011. Global Mobile Statistics 2011 [online].Available from: http://mobithinking.com/stats-corner/global-mobile-statistics-2011-all-quality-mobile-market-ing-research-mobile-web-stats-su. Accessed 5 July 2011.

Murphy,C.A.,Coover,D., andOwen,S.V., 1989.Developmentand validation of the computer self-efficacy scale. Educa-tional and Psychological Measurement, (49), 893–899.

O’Reilly, P. and Duane, A., 2010. Smart Mobile MediaServices (SMMS). The 8th International Conference onadvances in mobile computing and multimedia, Paris,France.

Ondrus, J. and Lyytinen, K., 2011. Mobile payments market:towards another clashof the titans.Proceedings of theTenthInternational Conference of Mobile Business (ICMB).

Ondrus, J., Lyytinen, K., and Pigneur, Y., 2009. Why mobilepayments fail? towards a dynamic and multi-perspectiveexplanation. Proceedings of the 42nd Hawaii InternationalConference on System Sciences, Waikoloa, Hawaii.

Podsakoff, P., et al., 2003. Common method biases inbehavioral research: a critical review of the literature andrecommended remedies. Journal of Applied Psychology,88 (5), 879–903.

Rao, L., 2011. Google Survey: 39 percent of smartphoneowners use their devices in the bathroom [online].Available from: http://techcrunch.com/2011/04/26/goo-gle-survey-39-percent-of-smartphone-owners-use-their-device-in-the-bathroom/. Accessed 2 May 2011.

Roca, J.C., Garcia, J.J., and de la Vega, J.J., 2008. Theimportance of perceived trust, security and privacy inonline trading systems. Information Management &Computer Security, 17 (2), 96–113.

Sanchez-Franco, M. and Rondan-Cataluna, F.J., 2011.Connection between customer emotions and relationshipquality in online music services. Behaviour & InformationTechnology, 29 (6), 633–651.

Schaettgen, N. and Taga, K., 2010. An acronym-free primeron mobile payments [online]. Available from: http://adlittle.nl/uploads/tx_extprism/ADL_PRISM_2_2010_m-payment.pdf. Accessed 5 July 2010.

Schierz, P.G., Schilke, O., and Wirtz, B.W., 2010. Under-standing consumer acceptance of mobile paymentservices: an empirical analysis. Electronic CommerceResearch and Applications, 9 (3), 209–216.

Siau, K., et al., 2004. A qualitative investigation on consumertrust in mobile commerce. International Journal ofElectronic Business, 2 (3), 283–300.

Skeldon, P., 2011. Growing consumer demand for mobileprompts massive investment in new multichannel platformsas retailers look to integrate everything [online]. Availablefrom: http://www.internetretailing.net/2011/06/growing-consumer-demand-for-mobile-prompts-massive -investment-in-new-multichannel-platforms-as-retailers-look-to-integrate-everything/. Accessed 5 July 2011.

Tenenhaus, M., et al., 2005. PLS path modeling. Com-putational Statistics & Data Analysis, 48 (1), 159–205.

Turner, A., 2009. M-payment models: starting to look good,payments cards and mobile. May/June. Available from:http://www.paymentscardsandmobile.com.

Varnali, K. and Toker, A., 2009. Mobile marketing research:the state of the art. International Journal of InformationManagement, 30, 144–151.

Varshney, U. and Vetter, R., 2002. Mobile commerce:framework, applications and networking support.MobileNetworks and Applications, 7 (3), 185–198.

Venkatesh, V., 2000. Determinants of perceived ease of use:integrating control, intrinsic motivation, and emotioninto the technology acceptance model. InformationSystems Research, 11 (4), 342–365.

Verhagen, T., Meents, S., and Tan, Y.H., 2006. Perceivedrisk and trust associated with purchasing at electronicmarketplaces. European Journal of Information Systems,15 (6), 542–555.

Vicente, P. and Reiss, E., 2010. Using questionnaire design tofight nonresponse bias in web surveys. Social ScienceComputer Review, 28, 251–267.

Viehland, D. and Yoong Leong, R.S., 2010. Consu-mer willingness to use and pay for mobile paymentservices. International Journal of Principles and Applica-tions of Information Science and Technology, 3 (1), 34–46.

Vispoel, W.P. and Chen, P., 1990. Measuring self-efficacy:the state of the art. Paper presented at the AmericanEducational Research Association, Boston, MA.

Vodafone-Ireland. 2010. Preliminary results announcementfor the quarter ended 31st December 2010 [online].Available from: http www.vodafone.ie/aboutus/media/press/show/BAU012194.shtml;jsessionid¼2D83NSWpRGTlzZh7LCxCGpytHRgCJ2x6D3Q70hTLyc5gMJYKNt2f!-138711505!2036466758?date¼ThuþFebþ03þ14%3A52%3A00þGMTþ2011. Accessed 20 April 2012.

Wei, R., Xiaoming, H., and Pan, J., 2010. Examining userbehavioral response to SMS ads: implications for theevolution of the mobile phone as a bona-fide medium.Telematics and Informatics, 27 (1) 32–41.

Wu, J.J. and Tsang, A.S.L., 2008. Factors affecting members’trust belief and behaviour intention in virtual commu-nities. Behaviour and Information Technology, 27 (2),115–125.

Xu, G. and Gutierrez, J.A., 2006. An exploratory study ofkiller applications and critical success factors in M-commerce. Journal of Electronic Commerce in Organiza-tions, 4 (3), 63–79.

Xu, H., et al., 2010. The role of push-pull technology inprivacy calculus: the case of location-based services.Journal of Management Information Systems, 26 (3), 137–176.

Yang, M.H., et al., 2009. The effect of perceived ethicalperformance of shopping websites on consumer trust.Journal of Computer Information Systems, 50 (1), 15–24.

Young Hoon, K., Kim, D.J., and Yujong, H., 2009.Exploring online transaction self-efficacy in trust buildingin B2C E-commerce. Journal of Organizational and EndUser Computing, 21 (1), 37–59.

Zhong, J., 2009. A comparison of mobile payment proce-dures in finnish and chinese markets. BLED 2009Proceedings, 37.

A. Duane et al.334

Copyright of Behaviour & Information Technology is the property of Taylor & Francis Ltdand its content may not be copied or emailed to multiple sites or posted to a listserv withoutthe copyright holder's express written permission. However, users may print, download, oremail articles for individual use.