Page 1

© 2013 SteelConsult International Page www.steelconsult.com

1

Realities of Survival for

European Steel – Is there a

future for Steel in Europe?

23 May 2013, London (UK)

Platts 9th Steel Markets Europe Conference 2013

Page 2

© 2013 SteelConsult International Page www.steelconsult.com

2

• The information included in this presentation is supplied as an information source only and on the specific understanding that while

SteelConsult International has made every reasonable effort to compile any information with care and diligence, SteelConsult makes no

statements, representations nor guarantees about the accuracy or completeness of the information or any part of it and that no-one

should seek to rely on the report or any part of it for any purpose.

• SteelConsult International cannot accept and disclaims all responsibility and all liability (including, and without limitation, liability in

negligence) for any costs, damages, expenses or losses incurred from any reference to the report by any party, howsoever arising.

Realities of Survival for European Steel

Disclaimer

Page 3

© 2013 SteelConsult International Page www.steelconsult.com

3

Realities of Survival for European Steel

About SteelConsult International

Services Product Areas Why SteelConsult?

• Strategic Consulting • Steelmaking Raw Materials • Specialised in Iron & Steel

• Market Research • Semis • Expertise & experience

• Economics Analysis • Flat Products • Background in industry

• Customer Satisfaction Surveys • Long Products • Wide contact network

• We know the steel industry

• We know the market

• Extensive databases

• Strong network of senior consultants,

with a background in the industry

Page 4

© 2013 SteelConsult International Page www.steelconsult.com

4

Realities of Survival for European Steel – Contents

Contents

• Realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 5

© 2013 SteelConsult International Page www.steelconsult.com

The global steel industry has done well over the last 10 years, especially compared to the automotive sector. Profitability has fallen sharply in 2012, though remains significantly higher than before the China boom

5

Source: SteelConsult International

0

500

1000

1500

2000

2500

3000

3500

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Global Steel Earnings

Automotive Earnings

Iron Ore Earnings

EBITDA (Index (US$, 2000=100))

2 8

3 6

2 2

2 9

4 2

8 4

9 1

9 8

118

14 0

4 5

8 78 3

6 1

2 3 3 3 4 6

1418

2 2

4 2

2 5

6 6

9 0

6 0

0

20

40

60

80

100

120

140

160

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Global Steel Earnings (Top-70)

Iron Ore Earnings (Top-9)

EBITDA (bln US$)

Top-70 publicly listed mills

(65% of global steel output)

Top-9 publicly listed iron

ore mining companies

(45% of global iron ore

output, 75% of seaborne

trade)

Top-12 Automotive OEMs

(90% of global car output)

Realities of Survival for European Steel – Realities

2,068

170

129

Page 6

© 2013 SteelConsult International Page www.steelconsult.com

Realities of Survival for European Steel – Realities

However, EU steel mills have been hit hard since 2008, with profitability down by 80% in 2012 from the pre-crisis peak reached in 2008

Source: SteelConsult International

EBITDA main listed steel companies Europe (bn €)

4

7

4 4

6

12

13

16

18 18

2

7

3

8

0

2

4

6

8

10

12

14

16

18

20

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

6

0

20

40

60

80

100

120

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Global Steel EU Steel

EBITDA (Index (US$, 2008=100))

2008 pre-crisis peak

Page 7

© 2013 SteelConsult International Page www.steelconsult.com

7

Source: SteelConsult analysis

Notes: *YTD **Incl. net energy credit

Operational production cost/t slab, EU mill, US$/t

75 76 80 90117

174196 203

364

266

357

526

408 409

17 15

36

3131

67

73

29

33

27

24 23

41 47 5060

65

6266

76

75

81

81

89

79 81

2514

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Other operational production costs**

Freight raw materials

Raw materials

Realities of Survival for European Steel – Realities

Slab production costs in 2012 and 2013 are still at one of the highest levels ever. EU mills find themselves squeezed by weak fundamentals in their local sales markets, whilst competing in persistently tight global markets for their raw materials

Page 8

© 2013 SteelConsult International Page www.steelconsult.com

8

0

50

100

150

200

250

'67'68'69'70'71'72'73'74'75'76'77'78'79'80'81'82'83'84'85'86'87'88'89'90'91'92'93'94'95'96'97'98'99'00'01'02'03'04'05'06'07'08'09'10'11'12'13'14'15'16'17'18'19'20

Europe (excl. Turkey)

Source: WSA, SteelConsult

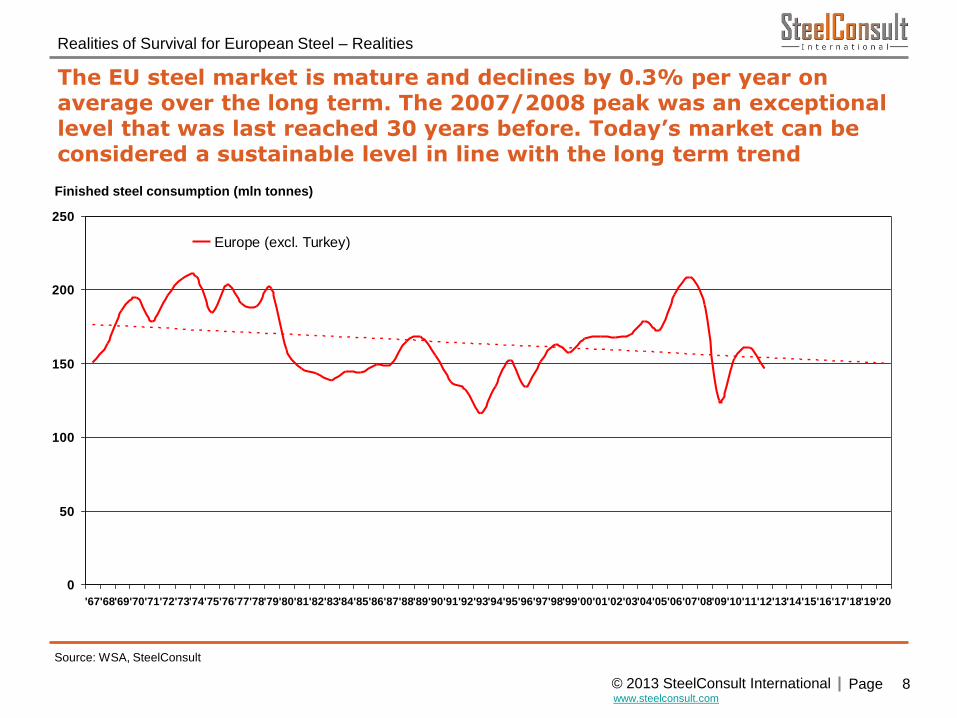

Realities of Survival for European Steel – Realities

The EU steel market is mature and declines by 0.3% per year on average over the long term. The 2007/2008 peak was an exceptional level that was last reached 30 years before. Today’s market can be considered a sustainable level in line with the long term trend

Finished steel consumption (mln tonnes)

Page 9

© 2013 SteelConsult International Page www.steelconsult.com

9

Data: WSA, SteelConsult

Steel output by country/region (mln tonnes)

Realities of Survival for European Steel – Realities

Steel production is moving from the Atlantic region to Asia, which in 2012 produced 66% of global output, compared to only 11% in 1960

37%28%

11%

48%

14%

14%

20%

7%

5%

7%

2%12%

4%

37%

4%

47%

3%1%

0%

20%

40%

60%

80%

100%

120%

1900 1960 2012 2020

Americas Europe CIS Japan

China Other Asia ROW

Europe

Asia

?

Source: Hatch Consulting

Page 10

© 2013 SteelConsult International Page www.steelconsult.com

10

Realities of Survival for European Steel – Realities

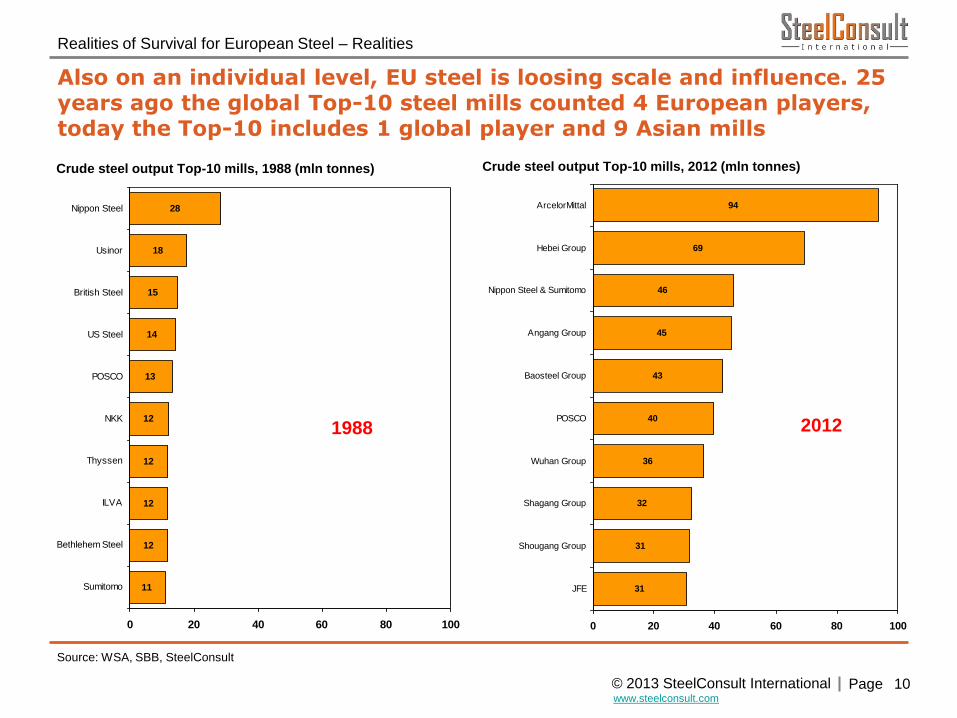

Also on an individual level, EU steel is loosing scale and influence. 25 years ago the global Top-10 steel mills counted 4 European players, today the Top-10 includes 1 global player and 9 Asian mills

Source: WSA, SBB, SteelConsult

11

12

12

12

12

13

14

15

18

28

0 20 40 60 80 100

Sumitomo

Bethlehem Steel

ILVA

Thyssen

NKK

POSCO

US Steel

British Steel

Usinor

Nippon Steel

Crude steel output Top-10 mills, 1988 (mln tonnes)

1988

31

31

36

40

45

69

46

43

32

94

0 20 40 60 80 100

JFE

Shougang Group

Shagang Group

Wuhan Group

POSCO

Baosteel Group

Angang Group

Nippon Steel & Sumitomo

Hebei Group

ArcelorMittal

2012

Crude steel output Top-10 mills, 2012 (mln tonnes)

Page 11

© 2013 SteelConsult International Page www.steelconsult.com

11

Realities of Survival for European Steel – Realities

Europe is indeed the worst performer with regard to market growth...

-1%

1%

4%4% 5%

5%7%

8%

15%

-1%

7%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Europe North

America

East Asia

(excl.

China)

Other

World

Latin

America

CIS Global MENA Turkey India China

Finished steel consumption growth, CAGR 2000-2012

Source: WSA, SteelConsult

Page 12

© 2013 SteelConsult International Page www.steelconsult.com

12

Realities of Survival for European Steel – Realities

Slow growth notwithstanding, the EU is still a major steel market in tonnage terms, about the same as USA + Japan, and larger than the fast growing “BRI” markets (Brazil, Russia and India) combined

131

47 56

202

646

7329 20

146

63

0

100

200

300

400

500

600

700

North

America

Latin

America

Europe CIS East Asia

(excl.

China)

China India Turkey MENA Other

World

Source: WSA, SteelConsult

Finished steel consumption, 2012, m tonnes

Page 13

© 2013 SteelConsult International Page www.steelconsult.com

13

Realities of Survival for European Steel – Contents

Contents

• Realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 14

© 2013 SteelConsult International Page www.steelconsult.com

0

20

40

60

80

100

120

140

160

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A

0

20

40

60

80

100

120

140

160

China

EU

World

14

Realities of Survival for European Steel – Short term outlook

Whilst Chinese steel output has continued to rise firmly post-2008, EU mills are producing at 75% utilization. This roughly suggests 25% overcapacity in Europe, though real overcapacity is significantly lower

Crude steel output, index (May 2008 = 100)

Source: WSA, SteelConsult

2008 2009 2010 2011 2012 2013

Page 15

© 2013 SteelConsult International Page www.steelconsult.com

15

3.3% 3.4%

2.6%

-2.3%

0.4%

4.7% 4.8%

13.7%

1.2%

3.6%

-2.7%

-1.0%

-2.7%

2.6%

0.7%

10.0%

2.2%

2.9%

-1.5%

0.0%

3.0%3.5%

4.0%

10.3%

3.2% 3.3%

0.9%

3.1%3.5% 3.6%

6.7%

9.6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Global USA Eurozone Japan Brazil Russia India China

2011 2012 2013f 2014f

Source: EIU, SteelConsult

BRIC countries Global

Industrial Production growth (%)

Realities of Survival for European Steel – Short term outlook

The ‘decoupling’ of emerging markets persists, though the latter have also seen growth cool down since 2011. The Eurozone is expected to see IP contract by 1.5% in 2013 and only a modest recovery of 0.9% growth in 2014

G3

Page 16

© 2013 SteelConsult International Page www.steelconsult.com

16

Source: Eurostat

Realities of Survival for European Steel – Short term outlook

The EU-27 manufacturing sector shows signs of stabilization, but the construction sector, the largest steel end-use sector, is still dropping sharply

Leading economic indicators EU (Index 2010=100)

80

85

90

95

100

105

110

115

120

125

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Industrial production manufacturing EU-27

Construction production EU-27

2007 2008 2009 2010 2011 2012 2013

Page 17

© 2013 SteelConsult International Page www.steelconsult.com

17

Source: ACEA, SteelConsult

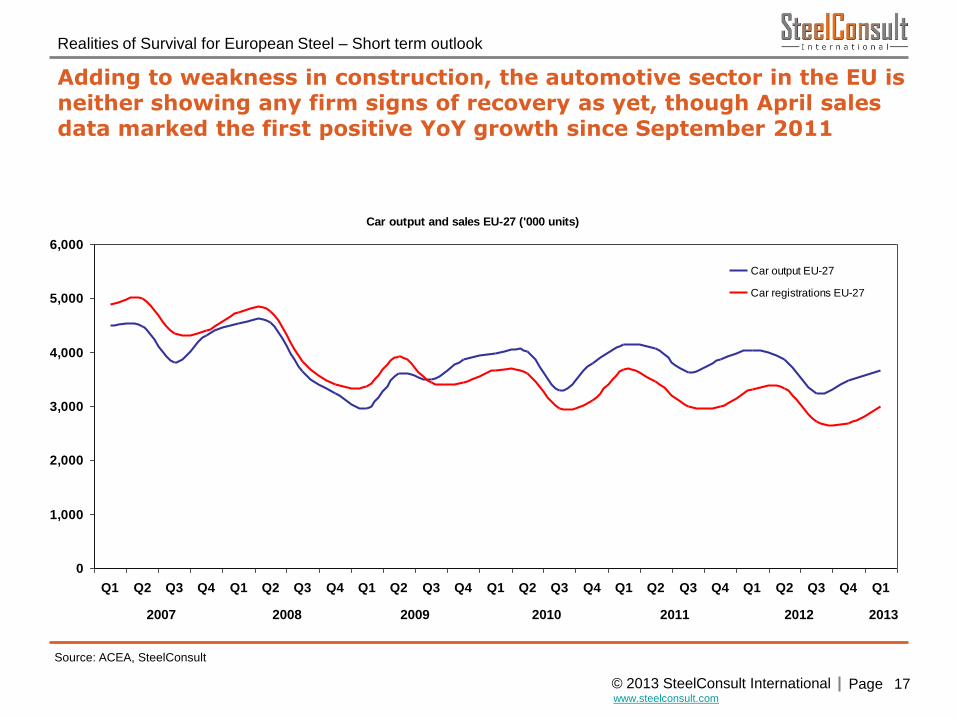

Realities of Survival for European Steel – Short term outlook

Adding to weakness in construction, the automotive sector in the EU is neither showing any firm signs of recovery as yet, though April sales data marked the first positive YoY growth since September 2011

Car output and sales EU-27 ('000 units)

0

1,000

2,000

3,000

4,000

5,000

6,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Car output EU-27

Car registrations EU-27

2007 2008 2009 2010 2011 2012 2013

Page 18

© 2013 SteelConsult International Page www.steelconsult.com

18

Source: Eurostat

Note: Data is seasonally adjusted

Realities of Survival for European Steel – Short term outlook

Looking forward, new building permits are also down in the EU, but, typically, the average for the EU-27 hides large differences in performance between Northern Europe and the South

Leading economic indicators - forward looking

0

20

40

60

80

100

120

140

160

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M

Building permits Germany (Jan. 2007=100)

Building permits Spain (Jan. 2007=100)

2007 2008 2009 2010 2011 2012 2013

Page 19

© 2013 SteelConsult International Page www.steelconsult.com

19

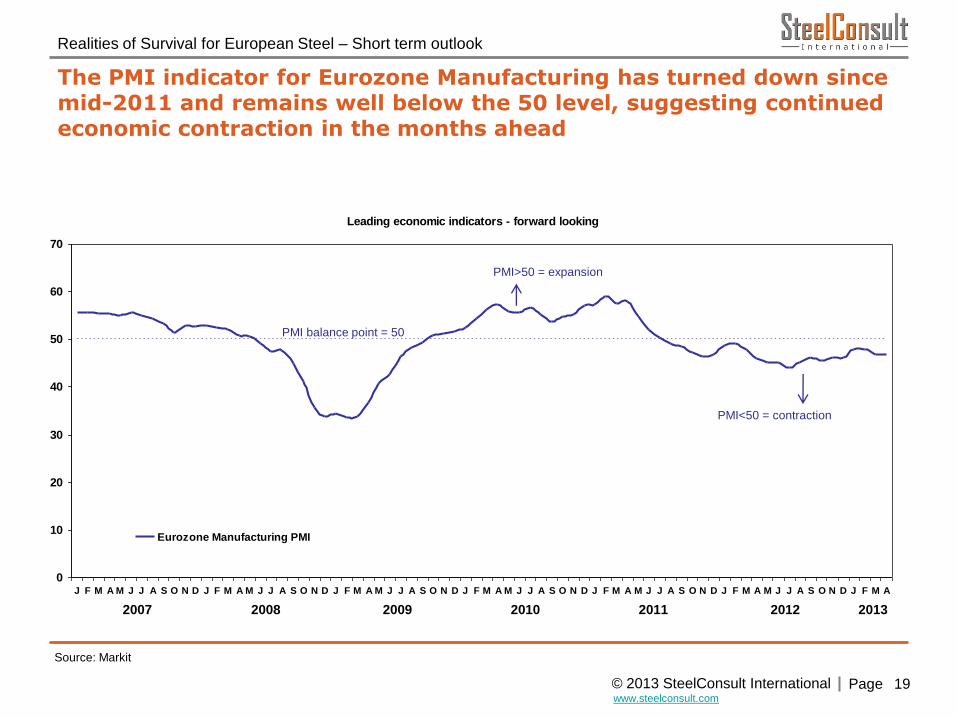

Source: Markit

Realities of Survival for European Steel – Short term outlook

The PMI indicator for Eurozone Manufacturing has turned down since mid-2011 and remains well below the 50 level, suggesting continued economic contraction in the months ahead

Leading economic indicators - forward looking

0

10

20

30

40

50

60

70

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A

Eurozone Manufacturing PMI

2007 2008 2009 2010 2011 2012 2013

PMI>50 = expansion

PMI<50 = contraction

PMI balance point = 50

Page 20

© 2013 SteelConsult International Page www.steelconsult.com

20

Realities of Survival for European Steel – Contents

Contents

• Realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 21

© 2013 SteelConsult International Page www.steelconsult.com

21

Realities of Survival for European Steel – Long term challenges – Imports

China, Russia and Ukraine are the three largest single exporters of steel to the EU

2.9 3.8 3.8 3.62.1 2.9 2.7

1.62.0 1.5 1.6

1.52.2 2.8 1.9

1.1

4.9

9.4

7.0

1.3

3.24.3

2.8

10.2

14.5

16.9

14.1

7.9

7.4

10.1

6.3

2.8

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012

Other

China

Ukraine

Russia

Source: ISSB, SteelConsult

3rd country imports of finished steel into the EU-27 (mln t)

Page 22

© 2013 SteelConsult International Page www.steelconsult.com

22

Source: SteelConsult analysis

Operational production cost/t slab/billet, US$/t, 2012

Realities of Survival for European Steel – Long term challenges – Imports

Chinese steel mills are competitive in their own domestic market, but not sufficiently competitive to be major structural exporters of steel to Europe

408 410 414 408 407347

435

318

24 11 41

47

16

50

2828

28

7

28

5131

27 6872

40

77

11547

16

0

100

200

300

400

500

600

700

800

EU Coastal EU Inland Brazil Ukraine China USA Turkey (scrap

based EAF)

Middle East (DRI

based EAF)

Raw materials Freight raw materials Labour Other operational production costs and energy

Integrated mills EAF mills

Page 23

© 2013 SteelConsult International Page www.steelconsult.com

23

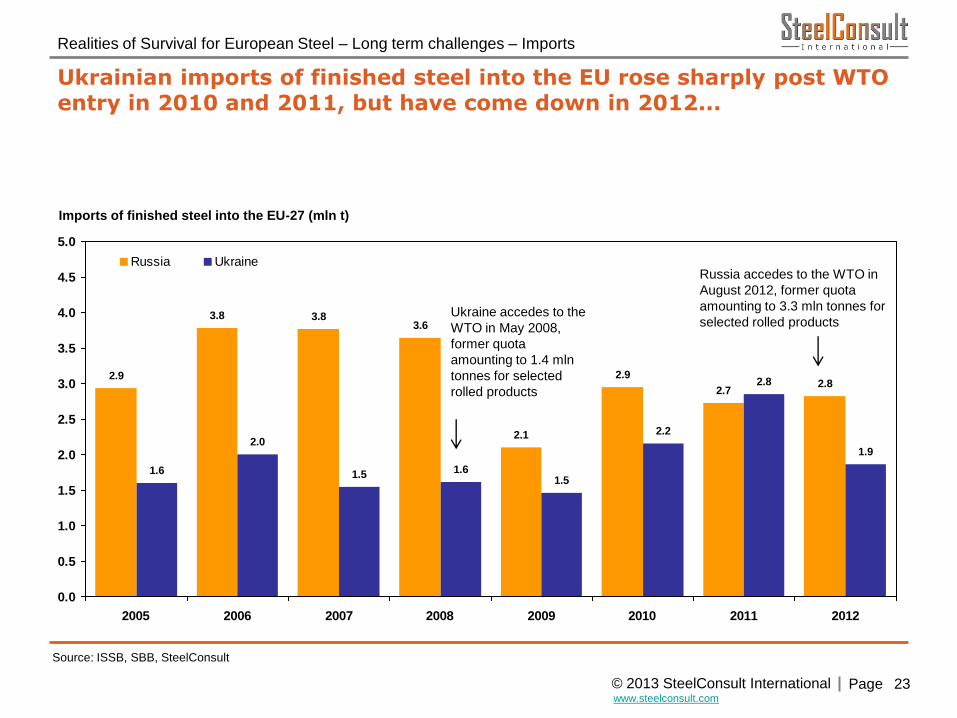

Realities of Survival for European Steel – Long term challenges – Imports

Ukrainian imports of finished steel into the EU rose sharply post WTO entry in 2010 and 2011, but have come down in 2012...

2.9

3.8 3.83.6

2.1

2.9

2.7

1.6

2.0

1.5 1.61.5

2.2

2.8

1.9

2.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2005 2006 2007 2008 2009 2010 2011 2012

Russia Ukraine

Source: ISSB, SBB, SteelConsult

Imports of finished steel into the EU-27 (mln t)

Russia accedes to the WTO in

August 2012, former quota

amounting to 3.3 mln tonnes for

selected rolled products Ukraine accedes to the

WTO in May 2008,

former quota

amounting to 1.4 mln

tonnes for selected

rolled products

Page 24

© 2013 SteelConsult International Page www.steelconsult.com

Imports of finished steel into the EU-27 (kt)

Source: ISSB, SteelConsult

2008 2009 2010 2011 2012 2013

0

50

100

150

200

250

300

350

400

450

500

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F

Russia Ukraine

Realities of Survival for European Steel – Long term challenges – Imports

Russian exports of steel to the EU have so far not significantly increased following the country’s access to the WTO in August 2012, except for an expected temporary peak in Jan/Feb 2013

24

Russia accedes

to the WTO in

August 2012

Ukraine accedes

to the WTO in

May 2008

Page 25

© 2013 SteelConsult International Page www.steelconsult.com

25

Realities of Survival for European Steel – Long term challenges – Imports

Contents

• Some realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 26

© 2013 SteelConsult International Page www.steelconsult.com

26

Realities of Survival for European Steel – Long term challenges – Offshoring

Brazil has seen a number of investment plans for new greenfield slab-for-export plants in the last decade, but the CSA and CSP plants are the only export projects to actually have gone ahead

Source: SteelConsult

Bacabeira:

CSM - 10m tpy

Sepetiba:

CSA (TKS/Vale) - 5m

tpy Itaguai:

CSN – 4.5m tpy

Sao Luis:

Baosteel/Arcelor/

Vale - 5m tpy

Pecem:

CSP

(Dongkuk/POSCO/Vale)

– 3m tpy

Anchieta: CSV

(Baosteel/Vale) – 5m

tpy

Congonhas:

CSN – 4.5m tpy

TMK – 3m tpy

CSN – 4.5m tpy

Anchieta: CSU (Vale)

– 5m tpy

Page 27

© 2013 SteelConsult International Page www.steelconsult.com

27

Realities of Survival for European Steel – Long term challenges – Offshoring

Brazil principally exports its Fe in the shape of ore and not in the shape of processed products. Brazil does not seem to offer a robust business case for investing in greenfield export capacity for supply to the European market

0

50,000

100,000

150,000

200,000

250,000

'80 '81 '82 '83 '84 '85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Semis & finished steel

Pig iron - Fe content

Ore & pellets - Fe content

Source: WSA, IBS

Net exports Brazil (’000 tonnes)

Page 28

© 2013 SteelConsult International Page www.steelconsult.com

28

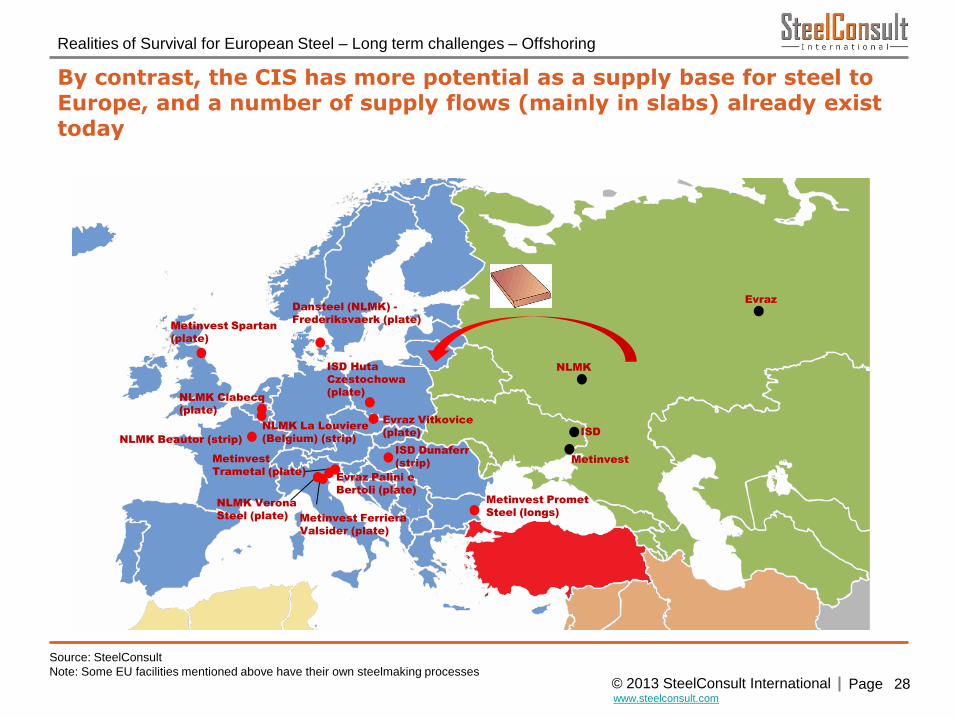

Realities of Survival for European Steel – Long term challenges – Offshoring

By contrast, the CIS has more potential as a supply base for steel to Europe, and a number of supply flows (mainly in slabs) already exist today

Source: SteelConsult

Note: Some EU facilities mentioned above have their own steelmaking processes

Dansteel (NLMK) -

Frederiksvaerk (plate)

NLMK La Louviere

(Belgium) (strip)

NLMK Clabecq

(plate)

ISD Dunaferr

(strip)

Evraz Vitkovice

(plate)

Metinvest

Trametal (plate)

Evraz Palini e

Bertoli (plate)

NLMK Verona

Steel (plate)

NLMK Beautor (strip)

NLMK ISD Huta

Czestochowa

(plate)

Metinvest Spartan

(plate)

Metinvest Ferriera

Valsider (plate)

Metinvest

Evraz

ISD

Metinvest Promet

Steel (longs)

Page 29

© 2013 SteelConsult International Page www.steelconsult.com

29

Realities of Survival for European Steel – Contents

Contents

• Realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 30

© 2013 SteelConsult International Page www.steelconsult.com

16

25

8

-10

-5

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013* 2014* 2015* 2016* 2017* 2018* 2019* 2020*

-10

-5

0

5

10

15

20

25

30

Actual cost

Case 3: High case scenario (EUR60/t CO2 by 2020)

Case 2: Middle case scenario (EUR40/t CO2 by 2020)

Case 1: Low case scenario (EUR20/t CO2 in 2020)

30

Realities of Survival for European Steel – Long term challenges – CO2 emissions costs

CO2 emissions costs are expected to rise to levels of €8-25/t crude steel in Phase III

CO2 emissions costs, average of integrated EU steel mills (€/t crude steel)

Free

Phase I Phase II Phase III

Source: SteelConsult analysis

Note: Indicative only, forecasts are subject to specific assumptions

Page 31

© 2013 SteelConsult International Page www.steelconsult.com

31

Realities of Survival for European Steel – Long term challenges – CO2 emissions costs

These costs would represent 15%-45% of average EBITDA margins of the EU steel industry over the last three years

96

114

132

155

168

19

71

33

64

0

20

40

60

80

100

120

140

160

180

2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: SteelConsult analysis

Average EBITDA margin EU steel industry (€/t crude steel)

Page 32

© 2013 SteelConsult International Page www.steelconsult.com

32

Realities of Survival for European Steel – Contents

Contents

• Some realities for EU steel

• Short term outlook

• Long term challenges:

• Imports

• Offshoring

• CO2 emissions costs

• Conclusions

Page 33

© 2013 SteelConsult International Page www.steelconsult.com

33

Realities of Survival for European Steel – Conclusions

Conclusions (1)

• The EU steel industry is clearly facing challenging times: growth has shifted to other parts of the

world, demand has fallen to a new, structurally lower level, raw materials costs remain high, at

least for now, and the industry is facing overcapacity.

• The outlook is still weak in the near term future in all main steel consuming sectors, though some

early signs of stabilization may have appeared, these will need to materialize further in the coming

months.

• Modest growth can be expected in the coming years, but the market is very unlikely ever to go

back to 2007 levels. The EU market will remain cyclical, but will inevitably decline further over the

long term.

• Is there a future for EU steel? Yes, the EU is still a major market in volume terms, with a high

share of value added, demanding business. Quality, lead times, freight costs, service, delivery

reliability, and price risk all favour locally produced steel.

Page 34

© 2013 SteelConsult International Page www.steelconsult.com

34

Realities of Survival for European Steel – Conclusions

Conclusions (2)

• China is not sufficiently competitive to become a major exporter of steel on a structural basis.

However, European mills may still on occasion be hit by temporary exports of excess steel from

China. Any small imbalance in China will translate to large tonnages hitting the global market. A

10% reduction in capacity utilization in China equals the entire amount of overcapacity in the CIS in

the early nineties, after the collapse of the former Soviet Union, at any point in time.

• Imports of finished steel from Ukraine and Russia may rise at times, but so far the accession of

these two countries to the WTO has not led to excessive increases in exports to the EU.

• For high value added steel products, there is a robust case for shipping the raw materials to and

producing the steel in Europe, rather than shipping large volumes of semis from other parts of the

world.

• The only region that has a potential role to serve as a steel supply base to Europe is the CIS.

• Depending on the development of carbon prices, CO2 emissions costs may translate to a

significant part of EBITDA margins and thus put further pressure on integrated mills, in particular

those with low value added products.

Page 35

© 2013 SteelConsult International Page www.steelconsult.com

35

Realities of Survival for European Steel

Thank you for your attention!

SteelConsult International

Binderij 3-S

1185 ZH Amstelveen

The Netherlands

Tel: +31 20 661 8900

Fax: +31 20 661 8901

Email: [email protected]

www.steelconsult.com