This article was downloaded by: [University of Sussex Library] On: 06 September 2013, At: 19:21 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK New Political Economy Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/cnpe20 Recasting the Sovereign Wealth Fund Debate: Trust, Legitimacy, and Governance Ashby Monk a a School of Geography and Environment, University of Oxford, South Parks Road, Oxford, UK, OXI 3QY Published online: 10 Nov 2009. To cite this article: Ashby Monk (2009) Recasting the Sovereign Wealth Fund Debate: Trust, Legitimacy, and Governance, New Political Economy, 14:4, 451-468, DOI: 10.1080/13563460903287280 To link to this article: http://dx.doi.org/10.1080/13563460903287280 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms- and-conditions

Transcript

This article was downloaded by: [University of Sussex Library]On: 06 September 2013, At: 19:21Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

New Political EconomyPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/cnpe20

Recasting the Sovereign WealthFund Debate: Trust, Legitimacy, andGovernanceAshby Monk aa School of Geography and Environment, University of Oxford,South Parks Road, Oxford, UK, OXI 3QYPublished online: 10 Nov 2009.

To cite this article: Ashby Monk (2009) Recasting the Sovereign Wealth Fund Debate:Trust, Legitimacy, and Governance, New Political Economy, 14:4, 451-468, DOI:10.1080/13563460903287280

To link to this article: http://dx.doi.org/10.1080/13563460903287280

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Recasting the Sovereign Wealth FundDebate: Trust, Legitimacy, andGovernance

ASHBY MONK

Benjamin J. Cohen argued over two decades ago that ‘high finance can no longer bekept separate from high politics’ (Cohen 1986: 3). This has never been truer than in theera of Sovereign Wealth Funds (SWF). Though difficult to define in precise terms,SWFs are government-owned investment funds operating in private financialmarkets. Spurred on by yawning global trade imbalances and a commodity priceboom, they have roughly $3–4 trillion under management, which is more assetsthan the global hedge fund industry (Devlin and Brummitt 2007). Forecasts suggestthis number could approach $10 trillion by 2015 (Jen and Andreopoulos 2008). More-over, despite the deteriorating economic and financial crisis, Maslakovic (2009)found that SWFs’ assets under management increased by 18 per cent in 2008. Inlarge part, this increase was due to the creation of new SWFs (rather than from thefunds’ investment returns). Indeed, while some SWFs have been around fordecades, 28 of the 48 SWFs identified by the US Government AccountabilityOffice were created since 2000 (GAO 2008); 12 alone have been established since2005 (Kimmett 2008). These SWFs appear to be investing their capital in private,risky assets with considerable focus on the financial sector (Beck and Fidora 2008).

The addition of long-term, stable investors to the current, tumultuous economicenvironment (in particular the financial sector) might have been welcomed bysome. However, many view the rapid growth of SWFs as a source of concern,1

primarily because SWFs are seen to represent a permanent re-direction in invest-ment flows and a shift in the dominant sources of financial capital. Heretofore,global finance was dominated by Anglo-American financial institutions (Clark2000). As Gieve (2008: 1) notes, ‘currently, capital is flowing ‘uphill’ from emer-ging to mature economies’. SWFs imply a redistribution of financial and politicalcapital throughout the world. Understandably, this loss of power has left some inthe West uncomfortable. In addition, by blurring the line between finance andpolitics, many worry that SWFs will be used illegitimately to advance political,as opposed to commercial, agendas (Schumer 2008). Some view SWFs as thesource of a new ‘state financial capitalism’ (Lyons 2007). Others simply wonder

New Political Economy, Vol. 14, No. 4, December 2009

Ashby Monk, School of Geography and Environment, University of Oxford, South Parks Road,

Oxford, OXI 3QY, UK.

ISSN 1356-3467 print; ISSN 1469-9923 online/09/040451-18 # 2009 Taylor & Francis

DOI: 10.1080/13563460903287280

New Political Economy, Vol. 14, No. 4, December 2009

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

what the introduction of public investors into private markets will do for efficiency(Gieve 2008). Some also see SWF investments as potentially hiding attempts byforeign governments to obtain technology and expertise to benefit national strategicinterests (European Commission 2008). In all cases, SWFs are a new source ofpolitical intrigue and concern; the Wall Street Journal even called them ‘. . . oneof the hottest topics in global financial markets’ (Galani and Nixon 2008). To besure, SWFs are changing the economic and political landscape.2

While concerns about emerging market investors are not new (see Moorsteen1975),3 SWFs do appear to have attracted special attention from policy makers(Weiss 2008). Significantly, these concerns have resulted in new policy proposalsfor dealing with SWFs. These proposals are at various stages of consideration andimplementation (see Figure 1). For example, the US has created a SWF taskforceto consider its options. Australia and Germany have implemented new rules target-ing SWFs. In addition, the International Working Group of Sovereign Wealth Funds(IWG) has developed a series of voluntary ‘generally accepted principles and prac-tices’ (known as GAPP or the ‘Santiago Principles’). These principles are an attemptto alleviate Western concerns about SWFs. In particular the principles aim to staveoff further protectionism and quiet those who would assert the states’ ‘power to giveor withhold access to its internal market’ (Strange 1991: 246). In essence, the San-tiago Principles seek to align the investment behaviour of SWFs with recipientcountry norms, which SWFs hope will obviate the need to deal with these fundsoutside of current regulatory frameworks.

The stakes are high for SWFs, as any new protectionist policies in the West willhave a significant impact on their ability to invest in these jurisdictions. Indeed,recent research by Deutsche Bank shows that an overwhelming majority ofSWF investments target North America and Europe.4 Clearly, any new policiesin these regions designed to constrain inward SWF investment will limitthese funds’ ability to implement their strategies. This tension underscores the

FIGURE 1. Examples of Current SWF Policies.

Ashby Monk

452

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

importance of understanding the Western concern vis-a-vis SWFs; it is thusprecisely the focus of this article.

Three main themes emerge within the current SWF debate. First, confusionamong policy makers and analysts as to what actually constitutes a SWF is wide-spread. This makes any thoughtful discussion about these institutions difficult.Second, SWFs are widely perceived to be lacking in ‘good governance’ practices,at least by Western analysts (see Ambachtsheer 2008; Clark and Urwin 2008;Truman 2008). Indeed, viewed in relation to Western financial institutions,many of which are guided by fiduciary duty to a specified individual beneficiary,there is a strong case for clear governance deficiencies in SWFs (Barroso 2008).Third, a lack of ‘trust’ between SWFs and investment recipient countries isevident. In many cases, this distrust stems from a contradiction in the normsbetween those countries that sponsor SWFs and the investment recipient countries.For example, nine of the 10 largest SWFs come from countries lacking full demo-cratic rights (Davis 2008). Government sponsorship of SWFs therefore becomesall the more problematic.

The objective of this article is to explore and analyse these three themes.I resolve any remaining confusion about SWFs and advance the ongoing construc-tive debate about the appropriateness of these funds’ operations in Western privatemarkets. Specifically, this article seeks to explain why some policymakers arereacting to SWFs with concern and, furthermore, why policy proposals to alleviateconcerns are largely focused on instilling ‘good governance’ practices withinthese institutions. Moreover, this article’s theoretical contribution is a conceptual-isation of the interplay between organisational legitimacy and institutionalgovernance. Indeed, I illustrate that achieving trust among SWFs and recipientcountries is in fact first a function of legitimacy, which is in turn a function ofgovernance.

With this in mind, this article proceeds as follows. Section one synthesisesexisting information and develops a definition for a SWF. This process helps toshow the source of concern surrounding SWFs. Next, I evaluate the notion of insti-tutional trust, as it is frequently cited by policy makers as a major problem. I con-clude that while ‘trust’ is an issue, legitimacy is the more pressing problem.Section three builds on this finding, conceptualising the relationship betweenlegitimacy and governance. In order to ground these conceptualisations in empiri-cal fact, I offer two cases studies in section four. One case illustrates the reactionof US policy makers to the China Investment Corporation (CIC). This case isbased on numerous elite interviews in Washington DC. The second casefocuses on the Santiago Principles, which represent a set of practices and prin-ciples geared towards building mutual trust. These cases confirm the importanceof governance in the notion of legitimacy. Section five then offers practical impli-cations of these empirical and conceptual findings.

The paper then concludes that SWFs can achieve legitimacy in Western juris-dictions by aligning their governance practices with their target operating environ-ment’s expectations for these practices. This is an important finding, as it suggeststhat SWFs are not illegitimate institutions. Rather, their practices simply need tobe changed so as to meet Western norms and expectations (if they hope to operatein these jurisdictions). This is significant, as SWFs are likely to be important

Recasting the Sovereign Wealth Fund Debate

453

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

players in the global economy for some time. As insurers of last resort for manycountries facing economic turmoil, SWFs may see a surge in assets coming out ofthis crisis in the same way central banks saw a surge in foreign exchange reservescoming out of the 1997 crisis.

Defining terms: SWF

On a mid-summer visit to Russia, US Treasury Secretary Henry Paulson toldPrime Minister Vladimir Putin that he had had a productive discussion withRussian Finance Minister Alexei Kudrin about the country’s SWF. Putinresponded by saying, ‘since we do not have a sovereign wealth fund yet, youare confusing us with someone else’, to which Paulson replied, ‘we can discusswhat you have called the various funds but we very much welcome your invest-ment’.5 This brief exchange is illustrative of the confusion surrounding SWFs:while Paulson was correct – Russia’s National Wealth Fund is considered bymany to be a SWF – Putin’s response is also justifiable. A widely accepted defi-nition of what exactly constitutes a SWF has been elusive.

However, defining the term SWF is extremely important. If these funds are athreat, we must be able to specifically point to the factors underpinning thisthreat. Without a proper definition, certain financial institutions could be caughtup in a protectionist backlash against SWFs unnecessarily. Moreover, variableand changing definitions adds to the confusion surrounding these funds, makingconstructive dialogue difficult. Using a detailed review of existing literatures,this section seeks to come to a consensus definition on what constitutes a SWF.This exercise will shed light on why SWFs inspire fear in some quarters.

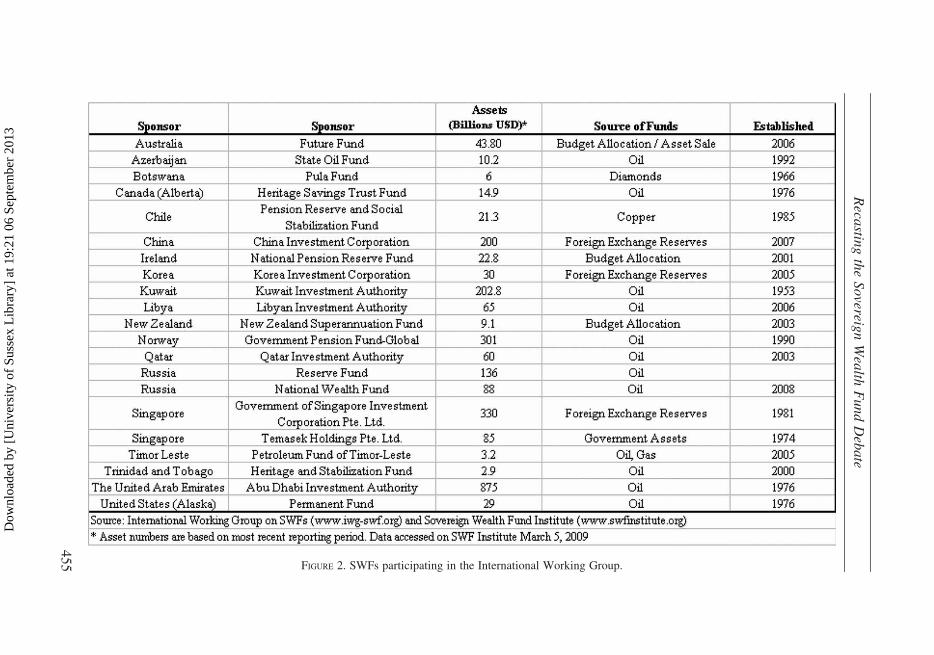

Andrew Rozanov first coined the term ‘sovereign wealth fund’ in 2005. Henoted that SWFs were ‘neither traditional public pension funds nor reserveassets supporting currencies, but a different type of entity altogether’ (Rozanov2005: 52). Rozanav was right; SWFs are different. However, three years onfrom his article, there is still no consensus as to how SWFs differ from otherpublic investment funds and how they should be defined. In fact, Rozanov recentlynoted that SWFs ‘. . . differ in size, age, structure, funding sources, governance,policy objectives, risk/return profiles, investment horizons, eligible assetclasses and instruments, not to mention levels of transparency and accessibility’(2008: 15). Indeed, according to a recent survey conducted by the InternationalWorking Group on Sovereign Wealth Funds (IWG), most of the funds surveyed(20 in total) were funded out of mineral royalties (primarily oil). However,some were funded from fiscal surpluses, foreign exchange reserves, borrowingsfrom the market and even divestment proceeds (IWG 2008). Moreover, therewas a straight 50-50 split among SWFs that were separate legal entities andthose that were not. Finally, the funds themselves cited various objectives, includ-ing fiscal stabilisation, general savings for future generations and coveringexpected future pension expenditures (see Figure 2).

Undoubtedly, this degree of divergence in fundamental characteristics has beenthe source of so much confusion. As such, coming to an acceptable definition willbe difficult. There is a fine line between making any definition too general (andincluding all public investment funds) and making it too specific (and eliminating

Ashby Monk

454

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

FIGURE 2. SWFs participating in the International Working Group.

Reca

stingtheSovereig

nWealth

FundDebate

45

5

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

some funds that deserve the SWF label). For example, limiting the SWF definition(as the US Treasury does) to those funds that receive their capital from foreignexchange reserves would eliminate well-established SWFs, such as Singapore’sTemasek (Nugee 2008).

The logical question is, then, are there any commonalities among SWFs thatcould serve as the basis of a SWF definition? Three characteristics emergewithin the existing research as crucial:

1) Ownership: Governments, both central and sub-national, own and, to varyingdegrees, control SWFs. Control can be exerted either directly or indirectlythrough the appointment of the SWF board.

2) Liabilities: One point of agreement illustrated by the IWG’s recent survey ofSWFs is that these SWFs ‘have no direct liabilities’ (IWG 2008: 15). This isperhaps a surprising point of agreement, as certain SWFs do have liabilities,such as sterilisation debt or some deferred contractual liability to transfermoney out of the SWF and into the general budget or a social securitysystem (Rozanov 2008). However, the point is that SWFs have no outside(non-governmental) liabilities. For those funds that do have a liability, it is typi-cally intra-governmental, i.e. one arm of the government owes another armof the government money. For example, the SWF might owe the ministry offinance, the central bank or even the social security system money. However,SWFs have no external creditor, which means the assets are not encumberedby the property rights of outside, non-governmental owners. In short, SWFliabilities (if they have any) are part of the broader national balance sheet.

3) Beneficiary: Despite certain explicit goals (e.g. filling a future PAYG pensiongap), SWFs are managed according to the interests and objectives of thegovernment/sovereign. As the accounting distinction underpinning point 2above suggests, the ultimate beneficiary of a SWF is not a specific individual.Rather, the beneficiary is either the government itself, the country’s citizenry inabstract, the tax payer generally or is simply left unidentified. This objectivefunction alters the strategic choices made by the funds’ managers, as thenotion of fiduciary duty, which disciplines the investment practices ofWestern financial institutions like pension funds, does not apply.

These three characteristics suggest the following technical definition:

SWFs are government-owned and controlled (directly orindirectly) investment funds that have no outside beneficiaries orliabilities (beyond the government or the citizenry in abstract)and that invest their assets, either in the short or long term,according to the interests and objectives of the sovereign sponsor.6

This concise definition is suitable for three reasons. First, given the heterogeneousnature of the SWF population, the definition does not use specific sources ofcapital (such as commodities or foreign exchange reserves) or legal status as adefining characteristic. The IWG’s survey illustrates that generalities in thisregard are necessary.7

Ashby Monk

456

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

Second, the definition makes no mention of accountability, transparency orgovernance. While some funds, such as the Canada Pension Plan InvestmentBoard, have tried to differentiate themselves from SWFs on the grounds thatthey have higher than average levels of transparency, accountability and govern-ance (Bisch 2008), such distinctions seem to suggest that the term ‘sovereignwealth fund’ is tantamount to unaccountable, non-transparent or poorly gov-erned.8 This is an error because it raises the following issue: as SWFs becomemore transparent, accountable or better governed, will they ‘graduate’ frombeing a SWF?9 Consider briefly a different type of financial institution: arecentral banks with perfect governance practices and central banks with deficientgovernance practices all still central banks? The obvious answer is yes; thesame principle should hold true for SWFs.

Finally, this definition underscores the vulnerability of SWFs to politicalinfluence because the assets are: 1) owned by the government; 2) owed back tothe government (instead of an outside beneficiary); 3) unconstrained by non-governmental property rights or fiduciary duty to any individual beneficiaries;and 4) invested in accordance with the government’s interests.

So, defining the term SWF is important, as it helps to explain why Westernpolicy makers are concerned about these funds. Indeed, if the sponsoring govern-ment is non-democratic, autocratic or communist (and many are) SWFs will face adifficult time reassuring democratic and capitalist investment-receiving countries.Specifically, the inherent vulnerability of these funds to political influence meansthat they will have difficulty convincing others that their motivations are purelycommercial. It is for this reason that some believe transparent and verifiablegood governance practices will immunise SWF investment decisions from politicsand establish trust despite difficult circumstances.

Trust or legitimacy?

Because distrust by policy makers in the activities of SWFs could lead to greatervigilance in monitoring and protectionist sentiments (see Levi and Stoker 2000),which could in turn result in restricted access to key financial markets (see Tuckerand Hendrickson 2004), the stakes are high to establish trust. One initiative thatseeks to do just that is the Santiago Principles, developed by the IWG with thesupport of the International Monetary Fund (IMF). According to Mr. Hamadal-Suwaidi of the Abu Dhabi Investment Authority and Co-Chair of the IWG,the Santiago Principles are specifically designed to establish ‘trust’ betweenSWFs and recipient countries. This was echoed by David Murray of Australia’sFuture Fund, the Chair of the IWG’s Drafting group, who noted, ‘. . . we had toestablish trust in recipient countries that the activities of sovereign wealth fundswere all based on an economic orientation.’10 This point was echoed by theentire leadership of the IWG: ‘It is about collectively doing everything in ourpower to ensure that trust lies at the heart of everything we do . . .’ (Al-Suwaidi2008).11 This perspective is also shared by the investment-receiving countries.For example, according to Joaquin Almunia, the European Commissioner forEconomic and Monetary Affairs, ‘The principles and practices of the GAPPamount to a global public good that can help foster trust and confidence between

Recasting the Sovereign Wealth Fund Debate

457

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

sovereign wealth funds, their originating countries, and the recipient countries.This is what we need in these turbulent times: a strong commitment to enhancemutual trust . . .’. 12 Finally, Kathryn Gordon of the Organisation for EconomicCooperation and Development (OECD) noted that their project and the IWG’sproject are ‘. . . flip sides of the coin in the trust-building process’.13

Evidently, ‘trust’ is an important stepping stone for SWFs’ integration into theglobal financial system; distrust is a problem that requires the attention of SWFsand policy makers alike. But is trust the primary issue? As illustrated above, SWFsclearly inspire concern and in some cases suspicion in the West. However, arethese stakeholders and policy makers correct in labeling distrust as the primaryhurdle? ‘Trust’ may in fact not be the appropriate label for what SWFs are lacking.

The notion of trust reflects someone’s belief that an institution is performing inaccordance with their normative expectations (Kaina 2008). As such, embedded inthis notion of trust is a performance; for SWFs, a performance could be a specificinvestment or asset allocation decision. These performances either conform to anormative expectation and create trust or contradict a normative expectation andcreate distrust. So, the question then arises of whether SWFs inspire concernamong policy makers due to undesirable past performances (i.e. investments).The answer is no; past SWF investments are not the issue. There are few if anyexamples of SWF investments that clearly indicate a breach of trust due to politi-cally motivated investing. So, the concerns voiced by policy makers are largelyunjustified if SWFs are being evaluated according to their track record.

Rather, much of the debate about SWFs is based on codes of conduct and thegeneral appropriateness of these funds. Indeed, the current debate revolvesaround SWF principles and practices, which refer to the established norms andmethods for operations and behaviour, rather than performances. In short,SWFs inspire fear within certain Western policy makers because SWF principlesand practices do not conform to their expectations. Therefore, trust is an inap-propriate label for what SWFs are lacking. A more appropriate label is legitimacy.While this may seem a semantic argument, like the definitional argument above, ithas important implications for solutions and policies.

Legitimacy is a fundamental concept within philosophy, political science, organ-isational sociology and even management theory (see Weber 1978; Weatherford1992; Suchman 1995; Hurd 1999; Pauly 1997; Zimmerman and Zeitz 2002). It hasbeen described as the acceptance of an organisation by its environment (Dowlingand Pfeffer 1975; Suchman 1995; Kostova and Zaheer 1999), and as the localbelief that an organisation is authorised (legally and morally) to operate in acertain place (see Tucker and Hendrickson 2004). In this sense, legitimacy is aconstraint. As Massey (2001: 157) notes, ‘an illegitimate status demands that theorganization respond, or else organizational failure could result’. According toZimmerman and Zeitz (2002: 416), ‘. . . legitimacy is a relationship between thepractices and utterances of the organization and those that are contained within,approved of, and enforced by the social system in which the organization exists’.

Legitimacy is a subjective quality that is defined by a certain actor’s perceptionof an institution’s practices and principles. Specifically, being legitimate meansthat the organisational procedures, structures and principles align with thevalues, norms and expectations of the society in the environment in which

Ashby Monk

458

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

the organisation seeks legitimacy. For SWFs, gaining legitimacy is synonymouswith gaining access to operate and invest in a given country or market.

Trust is not the same as legitimacy. Trust develops when a legitimate institutionacts in accordance with its predetermined rules. So, labeling the problem facedby SWFs as ‘distrust’ implies that SWFs have already performed in a way thatcontradicts Western norms and expectations, which is empirically false. Conver-sely, labeling the problem ‘legitimacy’ suggests that – while SWFs may not haveinvested improperly to date – the principles and practices that underpin theseinstitutions should be the focus of concern. Indeed, legitimacy is not aboutnorms of performance (as is the case with trust). Rather, it is about the normsof principles and practices underpinning the institution and the reflection ofthese principles and practices within the target operating environment. In thisconceptualisation, the expectations of the target environment for the norms ofoperation (principles and practices) are crucial to establish first legitimacy andthen trust.

In short, SWFs interested in establishing trust must first resolve their crisisof legitimacy. Indeed, the ‘trust’ policy makers are seeking to achieve with theSantiago Principles is a function of legitimacy: ‘In this way, institutional legiti-macy becomes a precondition of institutional trust because beliefs of institutionallegitimacy define specific behavioral expectations of how representatives of thoseinstitutions are supposed to act, as well as the benchmarks for the trustworthinessof these representatives’ (Kaina 2008: 514–515).

Legitimacy and governance

SWFs provide a useful test case for examining the interplay between legitimacyand governance. Indeed, as is made clear in the case studies below, both areinter-related. This paper defines governance in financial institutions as theprocedures, policies, structures and decision-making norms underpinning oper-ations and investments (see Clark and Urwin 2008).14 Governance is an impor-tant resources for financial institutions, as it provides the tools to protect againstoutside (political) influence, stem fraud and corruption, maintain accountabilityand transparency, manage new and existing financial risks, and supervise newand existing stakeholders (Monk in press). In sum, governance ensures thatan organisation is operating in accordance with the values and norms ofsociety. A well-governed financial institution inspires confidence amongststakeholders.

As Stoker (1998) suggests, governance and legitimacy are intertwined. TakeSuchman’s (1995) notion of ‘moral legitimacy’ as an example of the similaritiesbetween these two concepts. He views legitimation as a process necessitating anevaluation of techniques, procedures, categories and structures. Correspondingly,Perrow (1970) argues that an organisation’s ‘method of operation’ is crucial inestablishing legitimacy. Dowling and Pfeffer (1975) and Suchman (1995) alsosuggest that legitimacy can be achieved by changing internal practices to reflectthe local expectations and norms.

A simple model of the relationship between legitimacy and governance is asfollows: organisational legitimacy depends on how closely the quality of a specific

Recasting the Sovereign Wealth Fund Debate

459

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

organisation’s institutional governance, which refers specifically to the pro-cedures, policies, structures and decision-making norms underpinning the organ-isation, aligns with the environmental/societal expectations of, and norms for,these governance practices. At a certain degree of alignment, legitimacy will begranted by the target’s society.

This implies that geography is an important factor in legitimacy: on the onehand, governance is specific to the institution; on the other hand, norms of govern-ance are specific to the place. As a result, achieving legitimacy depends wherelegitimacy is sought (and where the organisation is coming from). SWFs are aperfect example of the importance of geography in this process, as many SWFscome from countries with principles that conflict with the target country’s prin-ciples. For example, Jose Manuel Barroso (2008), President of the European Com-mission, noted that SWFs do not meet the standards set by local financialinstitutions, which demand rigid governance structures and disclosure. So, govern-ance is a mechanism to achieve legitimacy at the level of the organisation, even if,politically, the sponsor and the target are misaligned. This point underscores therole of politics in this process. Nonetheless, this article focuses on how theSWF might overcome the political principles underpinning their institution toachieve organisational legitimacy in foreign jurisdictions.

Case studies

The cases discussed in this section further illustrate that legitimacy, not trust, is atthe heart of the SWF debate. Indeed, the first case shows that policy makers inWashington DC are primarily concerned with the China Investment Corporation’s(CIC) principles and practices (rather than any specific investments). Moreover,the second case shows that the Generally Accepted Principles and Practices(GAPP) are based on aligning SWF principles and practices with Westernnorms. Both cases reinforce how stronger legitimacy could resolve concernsassociated with SWFs. Moreover, these cases confirm the importance of govern-ance in achieving legitimacy.

A) CIC. During field work in Washington DC, the author interviewed seniorstaff and policy makers from the US House of Representatives, US Senate, theUS Department of State, the US-China Economic and Security Review Commis-sion, the World Bank, the Chinese Embassy, and the Singaporean Embassy, aswell as staff from think tanks and media outlets interested in the topic ofSWFs. The goal was to understand better the Western fears associated withcertain SWFs. Specifically, through close-dialogue interview methodologies(Clark 1998), we sought to uncover the factors driving US policy makers’concerns about the CIC.15

The CIC officially commenced operations on 27 September 2007 with an initialallotment of $200 billion. It is described as ‘a semi-independent, quasi-govern-mental investment firm established by the Chinese government to invest aportion of the nation’s foreign exchange reserves’ (Martin 2008a: 5). Accordingto Chinese officials, the purpose of the CIC is to improve the rate of return onChina’s foreign exchange reserves and soak up some of the country’s excessliquidity (Martin 2008a).

Ashby Monk

460

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

This specific fund engenders concern in the US for the following reasons. First, ithas the potential to become the world’s largest SWF – China is adding $500 billionto its foreign assets every year (Setser 2008a; 2008b). Second, it reports directly toChina’s State Council, an idiosyncratic reporting structure within China’s stateapparatus that puts the fund under direct supervision of Chinese leadership. Inaddition, four board members come from the Ministry of Finance, two from thePeople’s Bank of China, two from the National Development and Reform Commis-sion, one comes from the Ministry of Commerce and the final member comes fromthe national pension fund (Martin 2008b). This ‘internal structure almost assuresthat its investment decisions will be far more politicized than the management ofChina’s formal reserves by the central bank. All parts of China’s bureaucracyare represented on its board . . . many decisions likely will need to be made bythe top level of China’s government, not by the CIC’ (Setser 2008a: 12–13).Third, the articles of association have not been made public, so the mandatedobjectives, structure and constitution are still unknown (Chance 2008). Finally,while the CIC’s rhetoric about its future operations and investment policies arepositive, its governance (i.e. investment decision making) have been raised aspotentially lacking (even in Chinese sources: see Monk et al. 2008).

Concerns associated with the CIC have little to do with past investments, sinceit has only been in existence for little more than a year. Rather, it is the potentialfuture behaviour and the principles underpinning this organisation that causeconcern among interviewees. Given this, it is not surprising that the overarchingtheme in our interviews with US policy makers can be summed up in one question:‘What are the CIC’s intentions?’.

The difficulty in answering this question is precisely why legitimacy is at thecore of the concerns about the CIC. The opaque nature of the fund compoundsconcerns stemming from its affiliation with (what was frequently referred to ininterviews as) an authoritarian and communist regime. Indeed, many US policy-makers wondered aloud whether the CIC would be used (even decades fromnow) to achieve Chinese political objectives. This fear seemed to be associatedwith a much broader fear about China and its motivations. Even in interviewswith Chinese nationals, it was agreed that concerns about the CIC were basedon general fears about China’s emerging economic power. More generally, theCIC creates disquietude in large part because of its sponsor and the principlesof operation that many associated with this sponsor. Indeed, one senior Senatestaffer went so far as to say, ‘What happens when you unleash communists intofree market capitalism?’. Clearly, apprehensions are based on principles ratherthan explicit investment performances. As such, the CIC will need to establishlegitimacy in the US before it can have trust. Given the underlying politicalfactors at play, this is a tall order.

Nevertheless, further evaluation of the interview evidence reveals anothercrucial point. Interviewees explicitly and implicitly claimed that the lack oftransparent and verifiably good governance was a key problem for them.Indeed, when asked what they would like to learn about the CIC, the policymakers all eventually referred to the fund’s decision-making process, governanceand investment strategy. Moreover, they indicated that if these characteristicsmet their expectations, their concerns would dissipate. In short, if an adequate

Recasting the Sovereign Wealth Fund Debate

461

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

governance structure were implemented – one that ensured immunisation of poli-tics from investment decision making and that the CIC was operating in accord-ance with their norms (and not what these individuals perceived to be Chinesenorms) – these same policy makers so concerned about the CIC indicated thatthey would change their views and grant legitimacy.

This leads to an interesting conclusion: in the absence of ‘good governance’, theCIC is tainted by China’s broader principles (as perceived in the United States).However, with the application of good governance, the CIC would be evaluatedon its own merits and could potentially be viewed as ‘legitimate’ and ‘trust-worthy’. However, Monk et al. (2008) illustrate that this is unlikely in the shortterm. The CIC still has an unresolved mission and character. Due to the fund’srelative youth, it has not yet had the opportunity to establish the governance pro-tocols that could establish legitimacy in Washington DC (and elsewhere). Thus, itis not that this SWF is illegitimate; a more appropriate interpretation is that theCIC does not yet have the governance practices to ensure that political criteriado not influence the investment decision.16 If this were implemented, legitimacywould be attainable.

B) GAPP. In the case above, legitimacy appears possible even when some ofthe principles underpinning the institution (that is, the sponsoring government’spolitics) are in conflict with the target environment. The key to overcoming thisappears to be governance practices that meet the target’s expectations; specifi-cally, it calls for practices that ensure politics are immunised from SWF invest-ment decisions. The Santiago Principles reinforce this point.

The IWG was set up at a meeting of SWFs at the IMF during 30 April–1 May2008. The meeting’s purpose was to create a forum to resolve any national SWFconcerns at an international level. The IWG’s mandate was to identify a frame-work of generally accepted principles and practices that reflect appropriategovernance, accountability and investment practices of all SWFs. So, while theIWG’s leadership says its primary goal is establishing trust, its proposals are infact targeting legitimacy.

The Santiago Principles have several goals. First, they ask SWFs to meet localrecipient regulatory requirements. Second, they ask SWFs to make certain publicdisclosures in a variety of areas. Third, the principles seek to ensure stable finan-cial markets and avoid any protectionist policies targeting SWFs. Fourth, the prin-ciples try to instill transparent and sound governance structures, which will bedesigned to ensure that SWFs invest on the basis of economic and risk andreturn considerations. In short, the goals aspire to align SWF internal practicesand principles with Western expectations and norms.

The Santiago Principles thus provide more evidence of the importance of insti-tutional governance in organisational legitimacy. Indeed, since much of theconcern is rooted in a fear that governments will seek to advance politicalagendas via their SWF, GAPP have several specific governance principles todeal with this concern:

. GAPP 6: The operational management of the SWF should be independent.Moreover, there should be a clear distinction between the owner/governingbody and those individuals responsible for the actual management of the SWF.

Ashby Monk

462

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

. GAPP 7: The owner’s role within the SWF is to determine the general objec-tives and ensure proper oversight.

. GAPP 9: The operational management of the SWF should act in the interest ofthe SWF. This is designed to ensure that owners do not place undue pressure onSWFs. In a sense, this is an attempt to introduce a sense of fiduciary duty withinthe SWF.

. GAPP 16: SWFs should disclose their governance structure. This will give out-siders a better sense of what the SWF seeks to accomplish. Moreover, this willverify to outsiders that SWF operations are managed separately from the owner(i.e. government).

. GAPP 19: If a situation arises in which the SWF will invest based on non-finan-cial criteria (such as to address social, environmental or other factors), thesefactors need to be publicly disclosed and explained.

. GAPP 20: The SWF should not take advantage of privileged – or insider –information known to the sponsoring government so as to ensure fair compe-tition with private financial institutions.

While the Santiago Principles are voluntary – and their implementation subjectto home country laws – their makeup suggests that governance is an importantcomponent in overcoming legitimacy. Indeed, these principles seek to alignSWF principles and practices with Western normative expectations.

Implications

The empirical and conceptual findings presented here raise one final question:what are the practical implications? To begin, mutual trust between SWFs andrecipient countries is a function of legitimacy, which in turn depends on govern-ance. Given this, governance is going to be very important for SWFs, as any fundperceived to be illegitimate in a jurisdiction will eventually see its access to thatjurisdiction constrained (Tucker and Hendrickson 2004). Indeed, legitimacy is fre-quently linked with organisational survival in academic research (Massey 2001).Nevertheless, policy makers and commentators can only advise SWFs on govern-ance practices when SWFs operate abroad. However, once SWFs decide they wantto operate within a Western jurisdiction, the Western policy makers can makecertain explicit demands. With this in mind, the literature on governance andlegitimacy suggests that SWFs have three generic paths available to them (seeDowling and Pfeffer 1975; and Suchman 1995) to avoid these protectionistpolicies: avoidance, lobbying and adaptation.

First, SWFs can simply avoid jurisdictions whose norms and expectations con-flict with their governance practices. Rather than bend internal governance practicesto the norms within certain environments, some SWFs may operate in regions wheretheir current governance practices have already secured legitimacy. For example,the Chairman of the CIC indicated that he would avoid investing in markets,such as Europe, that did not make him feel welcome (see Lewis 2008). Neverthe-less, this option seems unlikely, as the EU and US are markets of such scale thatthey cannot be reasonably bypassed by any well-diversified financial institutions.

Recasting the Sovereign Wealth Fund Debate

463

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

Second, SWFs can try to alter the target environment’s perspective on whatconstitutes legitimacy (Suchman 1995). This would require changing the localdefinitions in such a way that existing SWF practices and principles weredeemed acceptable. In short, instead of aligning the SWFs governance to thetarget environment’s expectations, this would align the target environment’sexpectations to the SWFs’ governance. While this may seem daunting, manySWFs have hired lobbyists and public relations specialists specifically toattempt this process (see Lerer 2008). Indeed, rhetoric, or the art of persuasion,is a crucial aspect of achieving legitimacy (Suddaby and Greenwood 2005).Nevertheless, changing local perceptions would be extremely difficult.

Finally, SWFs can adapt their governance to the target environment’s expec-tations. Indeed, much of this paper has been leading to this option, as this is theapproach adopted by the IWG via the Santiago Principles and suggested by USpolicy makers vis-a-vis the CIC. Nevertheless, the success of this path requirescommunication and transparency, as the target environments need to be convincedand assured that the SWF in question is changing so as to ‘fit in’.

Conclusion

This article has two main objectives. First, it seeks to resolve any remainingconfusion about what actually constitutes a SWF. Condensing the available litera-ture, this paper offers a precise definition: SWFs are government-owned and-controlled (directly or indirectly) investment funds that have no outside benefici-aries or liabilities (beyond the government or the citizenry in abstract) and thatinvest their assets, either in the short or long term, according to the interestsand objectives of the sovereign sponsor. These characteristics leave some poli-ticians in the West uncomfortable, as they render SWFs vulnerable to politicalinfluence. Coming to an acceptable definition was an important exercise, as ithelped to explain why Western policy makers are concerned about SWFs. Onceestablished, evaluating this concern was the second objective of this article.

While many policy makers cited ‘trust’ as their primary issue, I argue to labelthe problem more accurately as legitimacy. Indeed, SWFs are not (yet) worrisomebecause of an established and conclusive track record of politically orientedinvesting. Rather, they are a subject of concern due to the principles and practicesunderpinning the institution, suggesting that SWFs are facing first and foremost acrisis of legitimacy. Before trust can be achieved, SWFs must first engage in aprocess of legitimation. For some, this will be a difficult task: if the sponsoringgovernment is non-democratic, autocratic or communist, SWFs’ assurances ofcommercial motives will be crucial. Put another way, where the SWF sponsor’sprinciples and practices are in conflict with the target environment’s principlesand practices, the SWF seeking legitimacy in the target environment will needto demonstrate that its internal principles and practices break with the sponsorand align with the target. Based on the evidence discussed in this paper, the keyto achieving this is governance.

Viewed in relation to traditional Western financial institutions, such as pensionfunds, mutual funds and endowments, with governance standards that includenotions such as fiduciary duty, accountability and transparency, SWFs come up

Ashby Monk

464

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

short. It still remains unclear to whom many SWFs are accountable and how theirinternal processes and structures discipline investment decisions in relation tofund performance and political interests (see Clark 2007, 2008; Monk, forthcom-ing). Moreover, due to their government ownership, SWFs may be held to a higherstandard of governance than other types of funds. So this deficiency in governanceis at the heart of the SWF crisis of legitimacy. Specifically, there remains wide-spread concern that SWFs are not currently capable of immunising investmentdecisions from political interference (Ambachtsheer 2008).17

However, this redirection of the debate has two important implications. First,the definitional characteristics inherent to a SWF are not the basis of Westernconcern; it is instead the practices and principles that are driving the illegiti-macy (and distrust). Second, this crisis of legitimacy can be overcomethrough a change in these internal governance practices. Indeed, some SWFswith good governance practices, such as Norway’s SWF, have already inte-grated into global financial markets and are widely perceived as legitimateand trustworthy. I acknowledge the burden on Norway’s SWF is less than forChina’s SWFs due to political factors. Nonetheless, even China’s SWF can,according to US politicians, achieve legitimacy through verifiably good govern-ance practices.

As a result, the case of SWFs is useful in demonstrating the power of good gov-ernance in achieving organisational legitimacy. These funds, which in manyinstances have sponsoring governments with political and cultural norms that con-flict with the norms in the West, can still achieve legitimacy through governancepractices that seek to eliminate politics from investment decision making. This is arelatively straightforward process of organisational change and reform; thisappears to be one of the primary objectives of the Santiago Principles. Achievinglegitimacy will be important for those SWFs that remain interested in investing inthe West. Without legitimacy, an organisation’s freedom to operate in certainplaces and spaces is threatened; achieving legitimacy and avoiding illegitimacyis thus essential to all organisations (Dowling and Pfeffer 1995; Tucker andHendrickson 2004). As Jackman (1993: 40) notes, ‘. . . institutions can only besuccessful to the extent that they are generally regarded as legitimate’. Indeed,some countries have already tried to restrict market access to SWFs in someway in order to eliminate a perceived ‘SWF threat’.

In sum, this article suggests that at a certain threshold of alignment betweenthe governance practices of the SWF and the expectations and norms of govern-ance practices embedded in the target environment, organisational legitimacyshould be granted. Once organisational legitimacy is in place, institutional trustwill follow (provided there is no corruption). The sheer size of these funds andtheir status as long-term, stable investors means that every effort should bemade to help these funds achieve this. Indeed, despite the global economiccrisis, SWFs continued to grow in 2008 and expectations dictate a SWF resur-gence coming out of the crisis. So, it is in the interest of all parties to cometo a mutually accommodating solution to this current crisis of legitimacy, asSWFs have the potential to affect the global economy in the 21st century tothe same extent that funded occupational pension plans had in the 20th century(see Clark 2000).

Recasting the Sovereign Wealth Fund Debate

465

Dow

nloa

ded

by [

Uni

vers

ity o

f Su

ssex

Lib

rary

] at

19:

21 0

6 Se

ptem

ber

2013

Notes

1. An important caveat is necessary. While this paper focuses on the current problems facing SWFs in the West,

it does not make the argument that SWFs are inherently threatening. Quite the contrary, I simply make the

observation that in certain places, policy makers perceive SWFs to be a threat (for whatever reason). In fact,

there are many who question the credibility of those even discussing protectionist policies. As Warren Buffet

noted: ‘Our trade equation guarantees massive foreign investment in the US. When we force-feed $2 billion

daily to the rest of the world, they must invest in something here’ (cited in Hamilton 2008).

2. It is not only the politicians who are concerned with the politics of SWFs. A recent survey conducted by

Public Strategies, Inc. of 1,000 registered voters in the United States further demonstrates SWFs’ problems:

66% of respondents felt that allowing foreign governments to buy stakes in US companies could compromise

national security.

3. As Stutzel (1981) shows, there has been an uneasy relationship between resource rich countries and the

countries that receive their capital in the form of investment for some time. Also, Cohen (1986) noted the

US perception in the 1970s that large concentrations of assets in the hands of ‘Arab governments’ might

be a national security threat.

4. See ‘SWF and foreign investment policies – an update’. October 2008. Available from: http://www.dbresearch.

com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000232851.pdf [Accessed 1 October 2009].

5. See http://www.reuters.com/article/marketsNews/idUSL3028241920080630.

6. This definition consciously excludes any reference to ‘foreign assets’, as many SWFs begin as domestically

oriented funds and grow to include foreign assets, such as Temasek. My view is that the definition should

include these funds from their inception rather than when they decide to invest overseas.

7. Nevertheless, as the liabilities section above implies, sources still do have a role in this definition. Indeed, if

the money comes from within or without the government has implications for the categorisation.

8. Rather, I would argue that the Canada Pension Plan is not a SWF because the government has no claims to the

assets in the plan, the assets are contributed by employees and employers, it receives no general tax revenues,

and, by law, it is not managed according to the interests of the sponsor but to maximise investment returns for

beneficiaries.

9. SWFs have been set up in response to the accumulation of wealth, while other types of funds are set up for

the purpose of wealth accumulation. This differentiation has led Ambachtsheer (2008) to refer to SWFs as

‘accidental financial tourists’. While it is true that some SWFs were thrust onto the global stage before

they had a chance to set up the appropriate governance mechanisms, this is not how SWFs should be

categorised – it simply helps to explain current practice.

10. See http://www.iwg-swf.org/tr/swftr0802.htm.

11. See www.iwg-swf.org/tr/swftr0802.htm.

12. See http://www.iwg-swf.org/pr/swfpr0808.htm.

13. See http://oxfordswfproject.com/2008/11/06/qa-with-kathryn-gordon-senior-economist-at-the-oecd/.

14. It should be noted that this is a liberal democratic perspective on ‘good governance’.

15. Due to the extreme sensitivity of the issues, all individuals have been anonymised and, moreover, some of the

insights garnered during interviews are not attributed at all – this is necessary in order to protect sources

given the small community of experts and practitioners focused on SWFs.

16. It should be noted that political interference in the decision making of any public financial institution is

perceived as inappropriate in the West. For example, political influence over US public pension funds has

been deemed illegitimate (Romano 1993).

17. This fear is perhaps justified, as international capital flows cannot help but be of a political nature (see Keynes

1933, cited in Gilson and Milhaupt 2008).

References

Al-Suwaidi, H. (2008), ‘IWG Press Briefing’. Available online http://www.iwg-swf.org/tr/swftr0802.htm

[Accessed 1 October 2009].

Ambachtsheer, K. (2008), ‘Sovereign Wealth Funds: Friends or Foes?’ The Ambachtsheer Letter, 264, pp. 1–4.

Barroso, J.M. (2008), Sovereign Wealth Funds: No European Legislation But Rather A Common Approach. Oslo,

Norway: European Commission. Available from: http://ec.europa.eu/commission_barroso/president/

pdf/statement_20080225_02_en.pdf [Accessed 1 October 2009].

Beck, R. and Fidora, M. (2008), The Impact of Sovereign Wealth Funds on Global Financial Market, European

Central Bank Occasional Paper Series, No 91.

Bisch, D. (2008), ‘Identity Crisis’, Benefits Canada, 32 (2), pp. 70–1.

Chance, C. (2008), ‘China’s Sovereign Wealth Fund Takes Shape’, Asian Investor, 22 February. Available from:

http://www.asianinvestor.net/article.aspx?CIID¼103599 [Accessed 1 October 2009]..

Clark, G.L. (1998), ‘Stylized Facts and Close Dialogue: Methodology in Economic Geography’, Annals of the

Association of American Geographers, 88 (1), pp. 73–87.

Clark, G.L. (2000), Pension Fund Capitalism (Oxford: Oxford University Press).

Clark, G.L. (2007), ‘Expertise and Representation in Financial Institutions: UK Legislation on Pension Fund

Governance and US Regulation of the Mutual Fund Industry’, Twenty-First Century Society, 2 (1), pp. 1–23.

Clark, G.L. (2008), ‘Governing Finance: Global Imperatives and the Challenge of Reconciling Community

Representation with Expertise’, Economic Geography, 84 (3), pp. 281–302.

Clark, G.L. and Urwin, R. (2008), ‘Best-Practice Pension Fund Governance’, Journal of Asset Management,

9 (1), pp. 12–21.

Cohen, B.J. and Council on Foreign Relations (1986), In Whose Interest?: International Banking and American

Foreign Policy (New Haven, London: Yale University Press).

Davis, B. (2008), State Funds May Not Bolster Freedoms, The Wall Street Journal, 11 February, A2.

Devlin, W. and Brummitt, B. (2007), ‘A Few Sovereigns More: The Rise of Sovereign Wealth Funds’, Australian

Treasury Economic Roundup, Spring, pp. 119–36.

Dowling, J. and Pfeffer, J. (1975), ‘Organizational Legitimacy – Social Values and Organizational Behavior’,

Pacific Sociological Review, 18 (1), pp. 122–36.

European Commission (2008), ‘A Common European approach to Sovereign Wealth Funds’, Communication

from the Commission to the European Parliament, The Council, The European Economic and Social

Committee and the Committee of the Regions, COM(2008) 115 provisional EN.

Galani, U. and Nixon, S. (2008), ‘Don’t Fear the Sovereigns’, The Wall Street Journal, 26 January, p. B18.

Gieve, J. (2008). Speech by Sir John Gieve, Deputy Governor of the Bank of England, Sovereign Wealth

Management Conference, London, 14 March.

Gilson, R.J. and Milhaupt, C.J. (2008), ‘Sovereign Wealth Funds and Corporate Governance’, Stanford Law and

Economics, Working paper No. 355.

Government Accountability Office (2008), Sovereign Wealth Funds: Publicly Available Data on Sizes and

Investments for Some Funds Are Limited, United States Government Accountability Office, GAO-08-946.

Hamilton, J. (2008), Buffett Blames US Policy for Rise of Sovereign Wealth Funds, Bloomberg.com, March 3.

Available from: www.bloomberg.com [Accessed 1 October 2009].

Hurd, I. (1999), ‘Legitimacy and Authority in International Politics’, International Organization, 53 (2),

pp. 379–408.

IWG (2008), ‘Current Institutional and Operational Practices’. Available online http://www.iwg-swf.org/pubs/eng/swfsurvey.pdf [Accessed 1 October 2009].

Jackman, R.W. (1993), Power Without Force: The Political Capacity of Nation States (Ann Arbor, MI: The

University of Michigan Press).

Jen, S. and Andreopoulos, S. (2008), ‘SWFs: Growth Tempered – US$10 Trillion by 1015’, Global Economic

Forum, 10 November. Available from: http://www.morganstanley.com/views/gef/archive/2008/20081110-Mon.html#anchor7146 [Accessed 1 October 2009].

Kaina, V. (2008), ‘Legitimacy, Trust and Procedural Fairness: Remarks on Marcia Grimes’, Study’, European

Journal of Political Research, 47, pp. 510–21.

Keynes, J.M. (1933), ‘National Self-Sufficiency’, Yale Review, 22, p. 755.

Kimmitt, R.M. (2008), ‘Public Footprints in Private Markets: Sovereign Wealth Funds and the World Economy’,

Foreign Affairs, January/February, pp. 119–30.

Kostova, T. and Zaheer, S. (1999), ‘Organizational legitimacy under conditions of complexity: The Case of the

Multinational Enterprise’, Academy of Management Review, 24 (1), pp. 64–81.

Lerer, L. (2008), ‘Businesses Plot Strategy to Protect Wealth Funds’, The Politico, 4 March.

Lewis, L. (2008), ‘Big-spending Chinese Eye Up Japan’s Energy “Champion” in $10bn drive for investment’,

Times Online: Banking & Finance, 23 February. Available from: http://business.timesonline.co.uk/tol/business/industry_sectors/banking_and_finance/article3419006.atece [Accessed 1 October 2009].

Levi, M. and Stoker, L. (2000), ‘Political Trust and Trustworthiness’, Annual Review of Political Science, 3,