Strategic Management Journal Strat. Mgmt. J., 35: 550–565 (2014) Published online EarlyView 15 May 2013 in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.2105 Received 26 May 2011 ; Final revision received 28 November 2012 RECIPROCITY AND R&D SEARCH: APPLYING THE BEHAVIORAL THEORY OF THE FIRM TO A COMMUNITARIAN CONTEXT JONATHAN P. O’BRIEN 1 and PARTHIBAN DAVID 2 * 1 Lally School of Management & Technology, Rensselaer Polytechnic Institute, Troy, New York, U.S.A. 2 Kogod School of Business, American University, Washington, District of Columbia, U.S.A. We propose that the behavioral theory of the firm perspective on R&D search requires modification when applied to “communitarian” cultures such as Japan because reciprocity and embeddedness can influence the search decision. When performance exceeds aspirations, communitarian-oriented firms are more inclined to use their privileged position to help their less fortunate stakeholders by engaging in additional R&D search that should yield greater payoffs for these stakeholders in the future. Our results indicate that while Japanese firms engage in “problemistic” search in a manner similar to what has been found in other contexts, they respond differently when performance exceeds expectations. We find that as performance rises above aspirations, communitarian-oriented firms raise R&D search to a greater extent than do firms that lack a communitarian orientation. Copyright 2013 John Wiley & Sons, Ltd. INTRODUCTION For industrial corporations, R&D investments con- stitute a search for solutions that can help build core competencies, exploit growth opportunities, and gain the competitive advantage necessary to obtain higher returns (Franko, 1989; Lengnick- Hall, 1992). A seminal contribution of the behav- ioral theory of the firm resides in explaining how “organizations respond to performance feedback by changing ... strategic behaviors” such as R&D (Greve, 2003a, 2003b: 147). Greve (2003b) notes several examples of firms such as General Motors and Intel that engaged in extensive R&D search in Keywords: behavioral theory of the firm; corporate governance; ownership structure; Japan; varieties of capitalism *Correspondence to: Parthiban David, Kogod School of Busi- ness, American University, 4400 Massachusetts Avenue, NW, Washington, DC 20016, U.S.A. E-mail: parthiban.david@ american.edu Copyright 2013 John Wiley & Sons, Ltd. response to performance shortfalls. More recently, in discussing the importance of R&D at Ford, CEO Alan Mulally asserted that “[w]e have never backed off, even through this entire recession. We actually have increased investment in our new vehicles during the toughest of times” (Langlois, 2012). Considerable empirical work has built on the behavioral theory of the firm to help illumi- nate our understanding of the behavioral deter- minants of R&D search (for reviews, see Argote and Greve, 2007; Greve, 2003b). Further, the behavioral theory of the firm (Cyert and March, 1963) has also been applied to firm R&D invest- ments in numerous countries, such as the United States (Chen, 2008; Chen and Miller, 2007), Japan (Greve, 2003a), India (Vissa, Greve, and Chen, 2010), and Italy (Antonelli, 1989). While most research studies employing the behavioral theory of the firm have posited a uni- versal model, cross-country institutional differ- ences can impact search and hence warrant

Published online EarlyView 15 May 2013 in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.2105

Received 26 May 2011 ; Final revision received 28 November 2012

RECIPROCITY AND R&D SEARCH: APPLYINGTHE BEHAVIORAL THEORY OF THE FIRMTO A COMMUNITARIAN CONTEXT

JONATHAN P. O’BRIEN1 and PARTHIBAN DAVID2*1 Lally School of Management & Technology, Rensselaer Polytechnic Institute, Troy,New York, U.S.A.2 Kogod School of Business, American University, Washington, District of Columbia,U.S.A.

We propose that the behavioral theory of the firm perspective on R&D search requiresmodification when applied to “communitarian” cultures such as Japan because reciprocityand embeddedness can influence the search decision. When performance exceeds aspirations,communitarian-oriented firms are more inclined to use their privileged position to help their lessfortunate stakeholders by engaging in additional R&D search that should yield greater payoffsfor these stakeholders in the future. Our results indicate that while Japanese firms engage in“problemistic” search in a manner similar to what has been found in other contexts, they responddifferently when performance exceeds expectations. We find that as performance rises aboveaspirations, communitarian-oriented firms raise R&D search to a greater extent than do firmsthat lack a communitarian orientation. Copyright 2013 John Wiley & Sons, Ltd.

INTRODUCTION

For industrial corporations, R&D investments con-stitute a search for solutions that can help buildcore competencies, exploit growth opportunities,and gain the competitive advantage necessary toobtain higher returns (Franko, 1989; Lengnick-Hall, 1992). A seminal contribution of the behav-ioral theory of the firm resides in explaining how“organizations respond to performance feedbackby changing . . . strategic behaviors” such as R&D(Greve, 2003a, 2003b: 147). Greve (2003b) notesseveral examples of firms such as General Motorsand Intel that engaged in extensive R&D search in

Keywords: behavioral theory of the firm; corporategovernance; ownership structure; Japan; varieties ofcapitalism*Correspondence to: Parthiban David, Kogod School of Busi-ness, American University, 4400 Massachusetts Avenue, NW,Washington, DC 20016, U.S.A. E-mail: [email protected]

Copyright 2013 John Wiley & Sons, Ltd.

response to performance shortfalls. More recently,in discussing the importance of R&D at Ford,CEO Alan Mulally asserted that “[w]e have neverbacked off, even through this entire recession. Weactually have increased investment in our newvehicles during the toughest of times” (Langlois,2012). Considerable empirical work has built onthe behavioral theory of the firm to help illumi-nate our understanding of the behavioral deter-minants of R&D search (for reviews, see Argoteand Greve, 2007; Greve, 2003b). Further, thebehavioral theory of the firm (Cyert and March,1963) has also been applied to firm R&D invest-ments in numerous countries, such as the UnitedStates (Chen, 2008; Chen and Miller, 2007), Japan(Greve, 2003a), India (Vissa, Greve, and Chen,2010), and Italy (Antonelli, 1989).

While most research studies employing thebehavioral theory of the firm have posited a uni-versal model, cross-country institutional differ-ences can impact search and hence warrant

Reciprocity and R&D Search 551

consideration. Greve’s study of Japanese firmsrecommended that “cultural and institutional dif-ferences may cause differences, and investigationof such issues should be encouraged” (2003a:697). Similarly, Vissa et al.’s study of Indian busi-ness groups also called for “research examiningwhether problemistic search is affected by howthe focal organization is embedded in an organi-zational and environmental context” (2010: 696).The current paper builds on these suggestions todevelop and test a theory that explains why the cul-tural and institutional differences in Japan warrantan extension to the behavioral theory of the firmexplanations of search.1

Firm search behaviors arise from bargainingamong salient stakeholder groups (Cyert andMarch, 1963). While such behavior may be appli-cable in most, if not all, contexts, cultural andinstitutional norms may shape how these variousstakeholder groups interact. The behavioral theoryof the firm was developed by scholars workingin the North American tradition (e.g., Cyert andMarch, 1963). In the United States, managers tendto adopt a “contractarian” orientation and treatthe firm as a nexus of contracts among variousstakeholders that transact at arm’s length. How-ever, managers in other countries are subject todifferent cultural and institutional contexts, andtherefore could manage relationships with stake-holders in very different ways. In Japan, managerstend to adopt a more “communitarian” orientation,wherein stakeholders are embedded in social andcultural ties, and exchanges are guided by norms ofreciprocity (Allen and Gale, 2000; Bradley et al.,1999; Dore, 2000). We submit that, although theextant research literature on the behavioral theoryof the firm purports to be universal, it implic-itly assumes that managers adopt a contractarianperspective, and hence it ignores how a firm’scultural and institutional context might shape theexchanges among various stakeholders (Hall andSoskice, 2001). Specifically, we maintain that thebehavioral theory of the firm does not fully accountfor how reciprocity and embeddedness may influ-ence strategic responses to performance feedback.In effect, our study is an attempt to contextual-ize R&D search behaviors across national borders(O’Brien and David, 2009; Tsui, 2004).

1 Although Greve’s (2003a) study of Japanese shipbuilding firmsfound results consistent with a universal behavioral theory ofthe firm model, we explore subtle, yet important, institutionaldifferences in a more broad-based sample of Japanese firms.

Japan provides a particularly useful settingto examine such institutional differences. WhileJapanese firms generally tend to be more com-munitarian than U.S. firms (Bradley et al., 1999),there is considerable variation among Japanesefirms. Over the past two decades, Japanese firmshave experienced a change in ownership struc-ture resulting in a “clash of capitalisms” (Ahmad-jian and Robbins, 2005) between traditional “rela-tional” owners (i.e., domestic corporations andfinancial institutions) that support a communitar-ian orientation, and “transactional” owners (mostlyfinancial institutions from the United States andthe U.K.) that espouse a more contractarian ori-entation (David et al., 2010). As search is shapedby the preferences of powerful coalitions in thefirm (Cyert and March, 1963), a firm’s owner-ship structure (i.e., the balance of relational versustransactional owners) can influence the extent towhich the firm’s managers are subjected to com-munitarian versus contractarian pressures, which inturn influences how they respond to performancefeedback.

According to the behavioral theory of the firm,performance in excess of aspirations signals theresolution of obstacles to fulfilling the contrac-tual obligations to stakeholders, which inducesmanagers to shift their scarce attention to otherissues and either maintain or possibly even reduceR&D search (Cyert and March, 1963). We theorizethat this behavior holds in a contractarian setting,but not in a communitarian setting, where obli-gations to stakeholders transcend contractual pro-visions and include considerations of reciprocityand embeddedness (Gerlach, 1992; Kester, 1991).Accordingly, when performance is strong, commu-nitarian firms are obliged to use their privilegedposition to “pay back” their network of stakehold-ers (e.g., buyers, suppliers, employees, and banks)by helping less fortunate members (Lincoln, Ger-lach, and Ahmadjian, 1996) via quantity and priceadjustments or other generous terms. Moreover,we maintain that the firm may also elect to “payforward” its network of stakeholders by engagingin additional R&D search that should yield growthopportunities that will benefit these stakeholders inthe future.

The results of our empirical analysis cor-roborate our developed theory. We find thatJapanese firms generally tend to increase R&Das performance rises further above the aspirationlevel, and that communitarian-oriented relational

owners are more supportive of this pay-forwardeffect than are contractarian-oriented transactionalowners. Our results reveal an overall V-shapedrelationship between R&D search and performancerelative to aspirations, with R&D spending risingas both performance shortfalls and performancesurpluses increase relative to aspirations. This find-ing is in contrast to the uniform negative asso-ciation predicted by traditional behavioral theory(Antonelli, 1989; Chen, 2008; Chen and Miller,2007; Greve, 2003a).

THEORY AND HYPOTHESES

The behavioral theory of the firm and R&Dsearch

Neoclassical economics posits that strategic invest-ments in R&D are guided by a rational calculus offinancial returns. When managers identify invest-ment opportunities that offer expected returns inexcess of an appropriately risk-adjusted cost ofcapital, they should adopt all such projects andonly those projects. Accordingly, R&D would sim-ply be an expense that is incurred in the present inthe expectation of a financial return in the future.While this model may describe what organiza-tions should do in order to maximize the wealthof shareholders, even some prominent economicscholars acknowledge that significant deviationsfrom optimality can occur due to factors such asbounded rationality (Williamson, 1985), financialconstraints (Myers and Majluf, 1984), and agencyproblems (Jensen and Meckling, 1976).

The behavioral theory of the firm offers a valu-able complementary lens for explaining and pre-dicting the investment decision by elucidating howthose decisions are actually made in practice byboundedly rational managers navigating a com-plex business landscape (Cyert and March, 1963).According to a behavioral perspective, managersdevelop aspirational performance levels for theirfirms based on historical firm performance andthe observed performance of their peers (i.e., theirreference group). Performance below aspirationindicates potential problems in attaining long-termgoals and hence triggers a “problemistic” searchfor solutions to close the gap (Cyert and March,1963). According to this perspective, R&D mayserve not so much as an investment with a clearcalculated return, but rather as a mechanism tosearch for new directions through more innovative

products, services, and processes that will enablethe firm to either raise prices or to reduce costs,thus closing the performance gap.

The behavioral perspective differs from eco-nomic perspectives not only in terms of whenR&D spending is increased, but also in terms ofwhen it is decreased. Instead of basing the searchdecision on maximization, whereby a search con-tinues until an optimal solution is found, man-agers “satisfice” and continue searching only untila solution is found that is “good enough” interms of exceeding the aspirational performancecriteria. Performance exceeding aspirations indi-cates the resolution of problems and precludes theneed for problemistic search. Thus, the behavioraltheory of the firm generally predicts a uniformnegative relationship between R&D investmentand performance relative to aspiration regardlessof whether firms perform above or below theiraspiration level. While the slack accumulationfrom performance in excess of aspirations mayyield higher search, after controlling for slack, anoverall negative association between performancerelative to aspirations and R&D search is typi-cally found (Chen, 2008; Chen and Miller, 2007).Behavioral research has examined various alter-native models of how search responds to perfor-mance levels below and above aspiration level(e.g., categorical, constant-slope, and changing-slope models; see Greve, 1998), and has con-cluded that “performance should show a nearlylinear relationship with R&D intensity” (Greve,2003a: 691).

U.S. versus Japanese contexts: implicationsof reciprocity and embeddedness

Corporations around the world encompass stake-holders such as shareholders, lenders, customers,suppliers, and employees. Yet, considerableresearch has noted cross-country differences inhow firms relate to stakeholders, with the UnitedStates and Japan presented as examples of polarextremes (Allen and Gale, 2000; Dore, 2000).While a variety of labels have been used todescribe this difference, we find the contractarianversus communitarian approach (Bradley et al.,1999) to be especially helpful in understanding theimplications for the behavioral theory of the firm.A contractarian view treats corporations as a nexusof contracts, both explicit and implicit, amongvarious stakeholder claimants operating at arm’s

length (Alchian and Demsetz, 1972; Jensen andMeckling, 1976) wherein most stakeholders arefixed claimants who are promised a contractuallyspecified payoff, while shareholders are viewedas the sole residual claimants in a completecontracting model. In such a model, managersmaximize the value of the firm by negotiating thecontracts with fixed claimants so as to maximizethe shareholders’ residual payment. Those holdingthis contractarian view claim that this “nexusof contracts” view generally reflects the actualexchange relationships among stakeholders in U.S.corporations.

In contrast, a communitarian perspective viewsorganizations not as a nexus of contracts amongstakeholders transacting at arm’s length, but asa nexus of relationships among stakeholders thatare embedded in a social context (Bradley et al.,1999). Managers’ roles are defined not narrowlyas maximizing shareholder value, but broadly asharmonizing the interests of various stakeholders,and typically in an incomplete contracting setting.Exchanges with stakeholders are guided not just bycontracts but also by norms of reciprocity (Lincoln,Gerlach, and Takahashi, 1992), whereby obliga-tions are not prescribed by contract but representa more general obligation to give something inreturn for what is received (Uzzi, 1996). Hence,parties provide help to each other and trust, withouta contractual requirement to do so, in an equi-table return of help at some future undefined date(Gouldner, 1960).

Two important differences between communi-tarian and contractarian models are worth not-ing. First, reciprocity in a communitarian settingrequires a long-term orientation, as the return offavors may occur well in the future. Contractar-ian relationships can persist for the long term,but there is no commitment to continuity. Hence,parties either periodically renegotiate their con-tracts or go their separate ways and find newexchange partners. In a communitarian setting,parties are committed to finding ways to makethings work out so that stakeholder relationshipscan be safeguarded for the long term. Second,with respect to value appropriation, the contrac-tarian setting allows for the possibility of con-siderable inequality in the distribution of wealthdue to differences in bargaining power. In con-trast, a communitarian logic promotes “ex postdistributive fairness” (Bradley et al., 1999: 44) anda more egalitarian distribution of wealth as the

managers of the firm act as trustees for a variety ofstakeholders.

Japanese managers tend to adopt a communi-tarian view (Bradley et al., 1999), and a compar-ison of business practices in Japan vis-a-vis theUnited States provides a vivid contrast betweenthe contractarian emphasis on arm’s length trans-actions and the communitarian reliance on trans-actions embedded in social and cultural ties. Incomparison to U.S. firms, Japanese firms developmuch closer and longer-term relationships with asmaller set of core suppliers (Dyer, 2000). U.S.firms tend to have a dispersed ownership structuredominated by short-term investors (Porter, 1992),while much of the equity of Japanese firms is heldby long-term owners that are also often customersor suppliers of the firm (Sheard, 1994). While mostdebt for U.S. firms is publicly traded arm’s lengthbonds, most of the debt of Japanese firms is frombanks with whom firms have close relationships(David, O’Brien, and Yoshikawa, 2008; Hoshiand Kashyap, 2001). Finally, pay disparity maybe an order of magnitude higher in U.S. versusJapanese firms (see Anderson et al., 2010; Jilani,2011).

In communitarian contexts, norms of reciprocityoften guide economic exchanges (Lincoln et al.,1992). For example, long-term supplier relation-ships are not explicitly contractual, yet core stake-holders make firm-specific investments in Japanesecorporations (Williamson, 1991), trusting that thefirm will safeguard these investments. Such long-term relationships are facilitated by the willingnessto provide help to each other and by the trust in anequitable return of the help at some future unde-fined date (Gouldner, 1960). Lincoln et al. (1992:566) note that “[t]he norm of reciprocity . . . hasparticular force in Japan where the stress on per-sonal, trusting, and long-term exchange relationsencourages mutual obligation to a degree uncom-mon in the United States” and is a “core valuepattern in Japanese culture.”

Empirical research has shown that the normof reciprocity is especially evident in exchangesinvolving firms with very high and very lowperformance. Dore notes that the reciprocity normin Japan requires that “the losses of the bad timesand the gains of the good times should be shared”(2000: 65). Thus, poor performers are recipients ofassistance and high performers are the providersof such assistance (Lincoln et al., 1996). Whenfirms perform poorly, lenders provide funds on

generous terms, employees accept short-term wageadjustments, and long-term suppliers and buyersmake quantity and price adjustments to help thefirm tide over its problems (Lincoln et al., 1996).While such assistance is costly in the immediateterm, firms trust that their exchange partners willreciprocate should they require assistance in thefuture, which helps to sustain the longevity of thecollective group of embedded stakeholders.

Although the research of Lincoln et al. (1996)focused on firms that were members of a keiretsu ,2

Gedajlovic and Shapiro show that this norm ofreciprocity applies much more broadly, stating:“our study indicates that traditional norms ofmutual assistance (Dore, 2000) and risk reduction(Nakatani, 1984) extend beyond formal networksto Japan’s broader enterprise system” (2002:573). Furthermore, extensive case study evidenceprovides detailed accounts of how Japanese firmsfacing adversity are helped in their recovery bytheir network of embedded ties (Gerlach, 1992;Hoshi and Kashyap, 2001). Finally, althoughJapan’s economic downturn in the 1990s hasinduced some erosion in traditional practices,its economy remains much more communitarianthan the contractarian U.S. model (Yoshikawa andRasheed, 2009).

Implications of reciprocity and embeddednessfor the behavioral theory of the firm

While the behavioral theory of the firm has beenfound to be robust and broadly applicable, it wasdeveloped and most often tested in a contrac-tarian context. We submit that there are subtle,yet consequential, differences in communitariancontexts. From a contractarian perspective, failureto attain the aspiration level indicates problemsin meeting the contractual obligations to prior-ity claimants, which spurs search until solutionsare found and aspirations are met. Performancein excess of aspiration level indicates that con-tractual goals have been achieved, so the impetusfor search abates and managers shift their scarceattention to other issues. From a communitarianperspective, however, considerations of reciprocitymay come into play and impact managerial atten-tion and search behavior. Specifically, we maintain

2 Name given to Japanese corporate groupings where firms haveclose mutual business and financial relationships.

that performance in excess of aspiration level trig-gers attention to reciprocity concerns, which leadsto increased, not decreased, search.

Performance below aspiration level and R&Dsearch

In a communitarian context, the problemisticsearch described by the behavioral theory ofthe firm should be reinforced by the norms ofreciprocity. As performance declines, stakeholdersmay get involved in helping the firm tide overproblems in the hope of fostering long-termsurvival and growth. The norm of reciprocityspurs them to rally around the troubled firm:lenders provide funds on generous terms; employ-ees may accept short-term wage adjustments;and long-term suppliers and customers are morewilling to make quantity and price adjustmentsto assist the firm (Lincoln et al., 1996). Theseconcessions should help the firm fund the searchfor solutions to the current problems. Thus, inaccordance with the problemistic search behaviorpredicted by the behavioral theory of the firmand shown in multiple empirical studies, R&Dintensity should increase as performance dropsfurther below the aspiration level. Thus, as abaseline hypothesis, we posit:

According to the behavioral theory of the firm,performance in excess of aspirations signals thesuccessful resolution of problems and thus dimin-ishes the need for search. From a contractarianperspective, aspirations are set from bargainingamong various stakeholders. Meeting aspirationsindicates that the contractual obligations to vari-ous stakeholders have also been met, and hencethere is less of a need to search for solutionswhen aspirations are exceeded. With the dimin-ished need for problemistic search, R&D searchshould decline, and thus the hypothesized nega-tive relationship with R&D search prevails evenwhen performance exceeds aspirations (Greve,2003b).

The situation is different, however, in a commu-nitarian context. While performance in excess of

aspirations does indeed signal success in meetingthe immediate needs of stakeholders, reciprocityconsiderations remain. Just as stakeholders areobligated to help the firm when performance islow, the firm is obligated to reciprocate by payingback (or perhaps even paying forward) its networkof stakeholders when performance is high. Priorresearch by Lincoln et al. (1996) has shown thathigh performing firms pay back poorly performingaffiliated firms through more favorable prices forbuyers and suppliers, and favorable interest rateson loans. We propose that in addition to payingback affiliated firms, reciprocity can spur firmsto pay forward their stakeholders by investing inR&D to generate future growth opportunities.

Performance in excess of aspirations may signalthat the firm has valuable resources and/or capa-bilities, finding new applications which can helpensure the long-term viability of the network ofstakeholders. R&D search can lead to new prod-ucts, services, or markets that not only yield addi-tional business opportunities for the firm’s buyers,suppliers, and banks, but also generate firm growththat provides enhanced job security and additionalcareer advancement opportunities for employees.Japanese firms tend to reinvest more in their oper-ations for the long term (Porter, 1992) in order togrow the firm and benefit the network of stake-holders (Kester, 1991). R&D search can consti-tute a long-term investment in generating highervalue for stakeholders in the future. Accordingly,we predict that, in communitarian contexts, perfor-mance above aspirations causes managers to shifttheir attention to reciprocity and hence pay forwardits stakeholders by searching for future growthopportunities.3

Hypothesis 2: In communitarian contexts, R&Dintensity increases when performance increasesabove the aspiration level .

Ownership structure and implicationsfor search

Although they tend to be more communitarian thanU.S. firms (Bradley et al., 1999), Japanese firms

3 In contractarian settings, firms often return excess cash toshareholders or pay their executives high compensation as anincentive for maximizing shareholder value. In communitariansettings, however, managers should generally be inclined to moreequitably distribute the wealth by searching for ways to sustainthe enterprise over the long haul.

vary in the extent to which managers are subjectto communitarian versus contractarian pressures.The firm’s goals are shaped by the demands ofpowerful coalitions in the firm (Cyert and March,1963), and the firm’s owners are often powerfulstakeholders. In the past two decades, Japanesecorporations have faced a “clash of capitalisms”(Ahmadjian and Robbins, 2005) between the tra-ditional domestic relational owners that supporta communitarian orientation, and foreign transac-tional owners that espouse a more contractarianorientation (David et al., 2010). Firms vary in theirextent of relational and transactional ownership,and therefore in the extent to which managers facecommunitarian versus contractarian pressures.

Whether owners espouse a contractarian or acommunitarian orientation is shaped by the extentto which they have embedded ties with the firm.Relational owners in Japan are large domesticbanks, insurance companies, and other corpora-tions that have business relationships with thefirm beyond mere shareholdings, and are there-fore more likely to have embedded ties with thefirm (Ahmadjian and Robbins, 2005; David et al.,2010). These relational owners are stakeholdersin multiple ways. In addition to owning shares,domestic banks and insurance companies provideloans and other financial services, while domes-tic corporations are often customers or suppliersof the firm. Relational owners have direct eco-nomic incentives to favor a stakeholder orienta-tion because investments that serve to perpetuateand grow the firm can yield returns to relationalowners through ancillary business relationships.Furthermore, relational ownership stakes tend tobe committed for the long term, sold off onlyin extraordinary circumstances, and often heldreciprocally (Sheard, 1994). Hence, these own-ers are inclined to help the firm when problemsarise, with the assistance effort often coordinatedthrough the main banks (Sheard, 1994). This long-term commitment by a broad community of stake-holders helps engender trust in the reciprocityof the network, thus fostering a communitarianorientation.

Transactional owners, in contrast, tend to beforeign institutional investors, mostly from theUnited States and the U.K. (Ahmadjian and Rob-bins, 2005; David et al., 2010). These ownerslack other business relationships with the firm,and hence can benefit only from shareholderprofits. Having only arm’s length relationships

with the firm, transactional owners make no long-term commitment to hold the shares. Nevertheless,they gain influence through the “threat of exit.” Ifdissatisfied, transactional owners can readily selloff their shares, thereby impairing the stock priceand exposing the firm to a higher cost of capi-tal and an accentuated threat of hostile takeover.Thus, managers are responsive to the preferencesof transactional owners, and recent research hasshown that foreign institutional investors (i.e.,transactional owners) influence firms across theworld to make changes to their governance mech-anisms to favor a more contractarian orientation(Aggarwal et al., 2011).

Considerable empirical work has shown differ-ences in relational and transactional owners’ orien-tation towards stakeholders. Relational ownershipplays a key role in fostering reciprocity and theredistribution of resources from firms with highprofits to those with low profits (Gedajlovic andShapiro, 2002; Lincoln et al., 1996). Hence, theimpact of relational ownership is “conditioned onthe prior performance of the firm: Weaker firmsdo better, but stronger firms do worse,” (Lincolnet al., 1996: 73). Relational owners are also morelikely to favor lifetime employment and higheremployee wages, while transactional owners aremore likely to favor layoffs and lower wages,especially in poorly performing firms (Ahmad-jian and Robbins, 2005; Ahmadjian and Robinson,2001; Yoshikawa, Phan, and David, 2005). Fur-ther, relational owners generally emphasize growththat benefits stakeholders by encouraging long-term investments, such as R&D (Lee and O’Neill,2003), while transactional owners tend to onlyfavor R&D if it yields profitable growth opportu-nities for shareholders (David et al., 2006). Whilenormative questions about the role of transactionalowners are debatable, the research evidence showsthat transactional owners do indeed impact firmstrategy.

The presence of two types of owners withconflicting interests provides an opportunity tocontrast the outcomes predicted by the behav-ioral theory of the firm, which has traditionallybeen applied in a contractarian context, and theoutcomes predicted by our modified versionapplied in a communitarian context. Generally,we expect that higher levels of transactionalownership should pressure managers to adopta more contractarian perspective and hence tomaximize shareholder value, while higher levels

of relational ownership should help foster a morecommunitarian orientation that favors a broaderset of stakeholders.

As noted in Hypothesis 1, both communitar-ian and contractarian perspectives predict higherR&D search when performance falls below aspira-tions. For performance below aspiration, we havenoted that the traditional logic of the behavioraltheory of the firm rooted in a contractarian con-text predicts a negative association between per-formance relative to aspiration and R&D search,as firms step up search to solve underlying per-formance problems. In addition to this prob-lemistic imperative, we noted that a communi-tarian orientation provides additional support asthe broader network of stakeholders make con-cessions in order to assist the struggling firm,enabling the firm to be more capable of fundingR&D search during troubled times. Accordingly,we expect that communitarian-oriented relationalowners should strengthen this negative associa-tion to a greater extent than contractarian-orientedtransactional owners.

Hypothesis 3: When performance decreases belowthe aspiration level, R&D intensity increasesto a greater extent with relational than withtransactional ownership.

We have noted that the traditional logic of thebehavioral theory of the firm for a contractariancontext predicts that R&D intensity will benegatively associated with performance aboveaspiration. However, we have also explained whythe opposite prediction would happen in a com-munitarian context. Instead of conforming to theexpectations of shareholders and cutting back onR&D search because the attainment of aspirationallevels obviates the need for problemistic search,communitarian-oriented managers respond tosuperior performance by searching for the growthopportunities that will yield future benefits for thebroader network of stakeholders. Communitarian-oriented relational owners should produce a morepositive (or less negative) association betweenR&D and performance above aspiration than docontractarian-oriented transactional owners.

Hypothesis 4: When performance increases abovethe aspiration level, R&D intensity increasesto a greater extent with relational than withtransactional ownership.

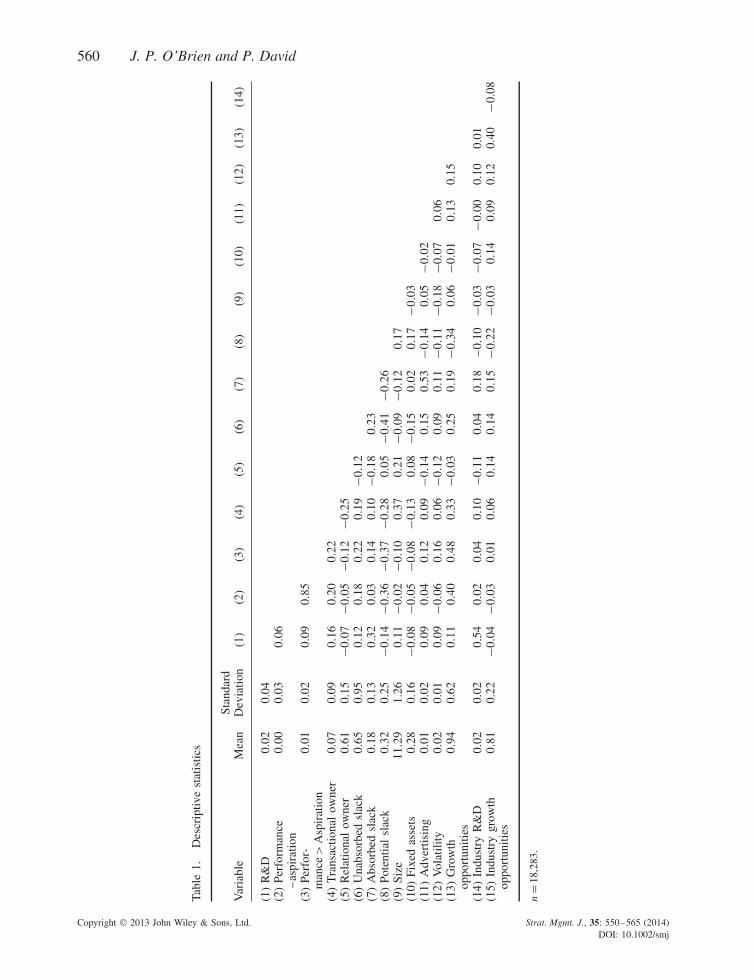

We constructed our sample from the Pacific-BasinCapital Markets (PACAP) Database for Japanesefirms. We began with all 24,556 observationslisted in the database for the years 1992 to 2004.As small firms may be effectively locked outof the foreign securities markets (Anderson andMakhija, 1999), we deleted 1,748 observationsthat had book value of equity of less than 3billion yen. We also deleted 712 observationsin the highly regulated financial, utilities, andcommunications industries. Further, to reduceendogeneity concerns, we lagged the independentvariables by one year so that R&D spending overthe course of a year is modeled as a functionof the ownership structure at the end of theprevious year. Lagging the independent variablesreduced the sample to 19,766 observations. Withoccasional missing variables (mostly pertaining tomarket value data), the final sample encompassed2,123 firms and 18,283 firm/year observations. Allvariables were obtained from the PACAP database,with the exception of R&D and advertisingexpenses, which were merged in from NikkeiEconomic Electronic Database Systems (NEEDS).

Variables

Our dependent variable, R&D intensity, is calcu-lated as total research and development expendi-tures divided by total sales. Although other formsof search occur in organizations, R&D is a criticalform of organizational search that can serve as auseful proxy for how total search in an organiza-tion is adjusted in response to changes in perfor-mance (Greve, 2003a).

The primary independent variables of interestrelate to performance relative to aspirations, andownership structure. To measure performance rel-ative to aspirations, we first constructed measuresof both firm performance and aspiration level. Asnoted by Greve, performance feedback comes from“rough measures of overall performance that willtell a manager that something is amiss, but notexactly what. The overall profitability of an orga-nization would be such a measure” (2003b: 7).Most prior behavioral theory of the firm researchhas typically utilized return on assets (ROA) asa performance aspiration (Greve, 2003b). It is a

particularly salient metric as it is tracked, reported,and serves as a common basis for comparisonamong firms. Further, ROA is highly relevantto meeting the needs of the broader stakeholdergroup because low profitability signals potentialproblems in meeting the needs of the variousstakeholder claimants. Research on reciprocity inJapanese companies also posits that ROA is anappropriate performance measure (Gedajlovic andShapiro, 2002; Lincoln et al., 1996).

We use the firm’s ROA to measure perfor-mance in a given year (Greve, 2003a; Iyer andMiller, 2008). ROA was calculated as operat-ing income divided by total firm assets. Wethen constructed a proxy for aspiration level thatwas based on both historical firm performanceand social aspirations. Similar to Greve (2003a),we measured the historical firm aspiration levelwith a weighted average of past performance.Specifically, historical aspiration (HA) was calcu-lated as: HAt = 0.7(ROAt−1) + 0.2(ROAt−2) + 0.1(ROAt−3). Results were nearly identical if weweighted recent performance more heavily or ifwe simply used the previous year’s performance asa proxy. We calculated the social aspiration (SA)level as the average ROA of all other firms (i.e.,excluding the focal firm) operating in the focalfirm’s industry. Following Greve (2003a), our finalmeasure of aspiration level (AL) was constructedas: AL = 0.8 × SA + 0.2 × HA. Social aspirationsare based on performance of other firms in theindustry that are likely to be competitors and there-fore salient in shaping aspirations.

Next, we subtracted the aspiration level fromthe firm’s actual ROA to construct the variablePerformance—Aspiration . To assess if the slopeof the relationship between R&D and perfor-mance relative to aspirations is different for per-formance above and below the aspiration level,we conduct a spline regression (Greene, 2003:121). Specifically, we constructed a second vari-able, Performance > Aspiration , which was equalto ROA—AL if ROA > AL and zero otherwise.Using inflection points slightly above or below theAL tended to reduce model fit, thus indicating theappropriateness of setting the inflection point atROA = AL.

Transactional and relational ownership areassessed as the total percentage of all outstandingshares held by each type of owner. Hence, largervalues should equate to more power and moreinfluence for each type of owner. We followed

prior research and measured transactionalownership as the total number of shares ownedby foreigners divided by total shares outstanding,and relational ownership as the total number ofshares owned by Japanese financial institutionsand other Japanese business corporations dividedby total shares outstanding (David et al., 2010).While foreign owners can include owners fromvarious countries, some of which might espousea more communitarian perspective, prior researchhas noted that a majority of foreign owners inJapan are portfolio investors from United Statesand the U.K., countries with a more contrac-tarian perspective (David et al., 2010). Further,research on foreign owners of Japanese companies(Ahmadjian and Robbins, 2005; Ahmadjian andRobinson, 2001; David et al., 2006, 2010) aswell as foreign owners of firms in a variety ofother countries (Aggarwal et al., 2011) has shownthat foreign owners, in the aggregate, tend to actin ways that are consistent with a contractarianperspective. Similarly, while our measure ofrelational owners includes both financial andnonfinancial firms, prior research has shown thatboth these types of owners act in ways thatare consistent with a communitarian perspective(Gedajlovic and Shapiro, 2002), and most researchon Japanese corporations has tended to combineboth groups as a measure of relational ownership(David et al., 2010; Lincoln et al., 1996).

We also controlled for numerous other factorsthat could influence current R&D spending. Inpractice, managers generally set R&D budgetsby adjusting the previous year’s budget up ordown, thus we include as a control the variablelag-R&D . We also control for several forms ofslack. It is especially important to control for slackbecause slack-based search is an alternate form ofsearch discussed in both the behavioral theory ofthe firm and in agency theory. According to thebehavioral theory of the firm, when performanceexceeds aspirations, firms may add to slack,or when performance drops below aspirations,firms may deplete slack. The availability of slackresources can facilitate experimentation and search(Greve, 2003b). According to agency theory, thepresence of slack resources could induce agencyproblems by allowing managers to wastefullypursue pet projects even in the absence of growthopportunities (Jensen, 1986), a problem that maybe particularly acute in Japan (O’Brien andDavid, 2009). Unabsorbed slack is measured as

cash and marketable securities divided by currentliabilities (Greve, 2003a; Kim, Kim, and Lee,2008), absorbed slack is the ratio of selling andadministrative expenses to sales (Greve, 2003a),and potential slack is the ratio of total long-term debt to total assets (Bromiley, 1991). Othercontrols include size, the natural log of total firmassets; fixed assets , net fixed assets to total assets;advertising , the ratio of advertising expensesto sales; and earnings volatility , the standarddeviation of ROA over the previous five years.We also proxy for the firm’s growth opportunitieswith its market-to-book ratio, which is calculatedas the sum of the book value of debt plus marketvalue of equity divided by total assets.

We also included two industry level controlvariables. For each industry, industry R&D andindustry growth opportunities represent the medianvalue of the corresponding firm level variable forall firms for which that industry is their primaryindustry. Finally, several of the variables (namelyR&D, ROA, unabsorbed slack, growth opportu-nities , and advertising) contained some extremeoutliers. Rather than exclude those observations,we Winsorized those distributions at the top andbottom 0.5th percentiles. After the Winsorizing,analysis of Cook’s D statistics indicated that nooutliers had a significant impact on the models.

Analysis

Conducting our analysis presented several criticalmethodological considerations. First, unobservedheterogeneity is a concern because our data containmultiple observations per firm. Therefore, weincorporate fixed firm effects into all our models.Fixed effects were deemed superior to randomeffects because Hausman tests indicated that therewas a significant (p < 0.01) systematic differencein the coefficients from random effects modelsversus fixed effects models. Second, our model isdynamic because we include as a control variablethe lag of the dependent variable. However,including the lag of the dependent variable in astandard fixed effects regression model will inducebias. Hence, we employ Bruno’s (2005) correctedleast squares dummy variable approach to correctfor this bias.

Finally, endogeneity is also a potential con-cern. Endogeneity is a form of omitted variablesbias, which occurs when a model excludes oneor more variables that significantly influences the

dependent variable and is correlated with one ormore of the independent variables. While tech-niques such as two-stage instrumental variablesregressions can be employed to eliminate thisbias and hence yield improved estimates of theeffect of an endogenous variable on a depen-dent variable, these techniques are also less effi-cient because they tend to produce much largerstandard errors (see Chapter 15 of Wooldridge,2003). Hence, even if a variable is theoreticallyendogenous, it is preferable to not model it asendogenous unless tests indicate that it induces astatistical problem. Further, our approach mini-mizes the potential endogeneity problem becauselagging all independent variables helps ensure thatthe model does not use independent variables thatwere determined simultaneously with the depen-dent variable, while including firm fixed effectshelps control for time-invariant omitted variables,and including the lag of the dependent variable as apredictor helps to control for omitted variables thatchange slowly over time. Nonetheless, we createdinstruments4 for the potentially endogenous vari-ables (i.e., unabsorbed slack, transactional owner-ship, and relational ownership) and conducted theDavidson-MacKinnon test of exogeneity, whichindicated that endogeneity was not a problem inany of the models we report.

RESULTS

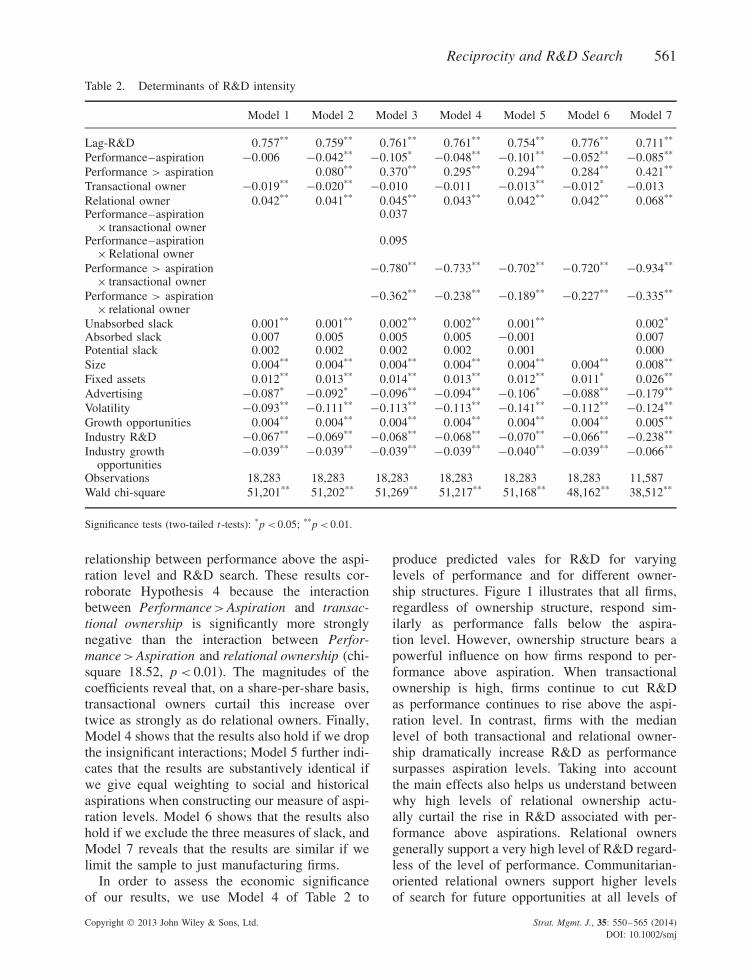

Descriptive statistics of our sample are providedin Table 1, while the results of our statisti-cal analyses are given in Table 2. Model 1 ofTable 2 presents a base model, which suggeststhat performance relative to aspirations is notrelated to R&D search. However, because thismodel only specifies a linear relationship betweenR&D and performance relative to aspirations, itmay fail to detect a nonlinear “kinked” relation-ship. Model 2 of Table 2 incorporates the splinespecification and reveals that performance rela-tive to aspirations does indeed have a significantimpact on R&D, albeit a different effect depend-ing on whether performance is above or below

4 Although the appropriate instruments varied somewhat frommodel to model, we generally found that either industry averagevalues for the variables in question or lags of those variablesserved as valid instruments (i.e., they were strongly related tothe potentially endogenous variable but not strongly related tothe dependent variable).

aspirations. The significant negative coefficient forPerformance—Aspiration shows that as perfor-mance falls further and further below the aspirationlevel, R&D expenditures increase, thus supportingHypothesis 1.

The significant positive coefficient on Perfor-mance > Aspiration reveals the relationship is dif-ferent when performance exceeds aspirations. Ifthe coefficient was of the same magnitude but ofopposite valence, it would suggest that the rela-tionship between R&D search and performancerelative to aspirations flattens out when perfor-mance exceeds aspirations. However, the coeffi-cient for Performance > Aspiration is almost twiceas large as the absolute value of the coefficient forPerformance—Aspiration , suggesting that R&Dexpenditures rise as performance rises furtherabove aspirations, hence making an almost per-fect V-shape at the aspiration level. A Wald testconfirms that the linear combination of the twocoefficients is significantly greater than zero (chi-square = 5.98, p < 0.05), revealing that the slope isindeed significantly greater than zero when perfor-mance exceeds aspirations and hence supportingHypothesis 2.

Although we did not hypothesize main effectsfor transactional and relational ownership, thesignificant negative coefficient for transactionalownership and the significant positive coefficientfor relational ownership are consistent with ourtheoretical arguments. In terms of the controlvariables, it is noteworthy that neither absorbedslack nor potential slack influenced R&D search,but unabsorbed slack had a strong positive effect.Consistent with theory, this finding suggests thatthose forms of slack are not as easily accessible asunabsorbed slack.

Model 3 of Table 2 adds in the interac-tions between ownership structure (i.e., extentof relational and transactional ownership) andperformance above and below aspirations. Theresults reveal that neither transactional ownershipnor relational ownership impact how managersalter organizational search behavior in responseto performance shortfalls. Thus, we fail to findsupport for Hypothesis 3. Curiously, ownershipstructure does impact how performance aboveaspiration influences search behavior. The nega-tive interactions of Performance > Aspiration withboth relational ownership and transactional own-ership reveal that both types of owners tendto use their influence to curtail the positive

relationship between performance above the aspi-ration level and R&D search. These results cor-roborate Hypothesis 4 because the interactionbetween Performance > Aspiration and transac-tional ownership is significantly more stronglynegative than the interaction between Perfor-mance > Aspiration and relational ownership (chi-square 18.52, p < 0.01). The magnitudes of thecoefficients reveal that, on a share-per-share basis,transactional owners curtail this increase overtwice as strongly as do relational owners. Finally,Model 4 shows that the results also hold if we dropthe insignificant interactions; Model 5 further indi-cates that the results are substantively identical ifwe give equal weighting to social and historicalaspirations when constructing our measure of aspi-ration levels. Model 6 shows that the results alsohold if we exclude the three measures of slack, andModel 7 reveals that the results are similar if welimit the sample to just manufacturing firms.

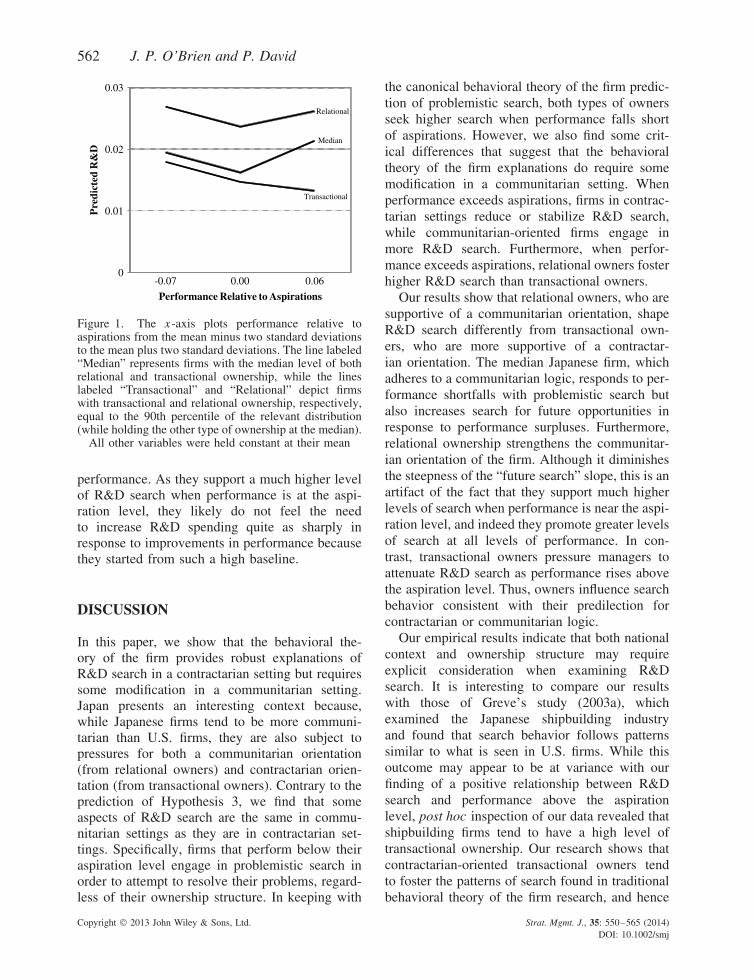

In order to assess the economic significanceof our results, we use Model 4 of Table 2 to

produce predicted vales for R&D for varyinglevels of performance and for different owner-ship structures. Figure 1 illustrates that all firms,regardless of ownership structure, respond sim-ilarly as performance falls below the aspira-tion level. However, ownership structure bears apowerful influence on how firms respond to per-formance above aspiration. When transactionalownership is high, firms continue to cut R&Das performance continues to rise above the aspi-ration level. In contrast, firms with the medianlevel of both transactional and relational owner-ship dramatically increase R&D as performancesurpasses aspiration levels. Taking into accountthe main effects also helps us understand betweenwhy high levels of relational ownership actu-ally curtail the rise in R&D associated with per-formance above aspirations. Relational ownersgenerally support a very high level of R&D regard-less of the level of performance. Communitarian-oriented relational owners support higher levelsof search for future opportunities at all levels of

Figure 1. The x -axis plots performance relative toaspirations from the mean minus two standard deviationsto the mean plus two standard deviations. The line labeled“Median” represents firms with the median level of bothrelational and transactional ownership, while the lineslabeled “Transactional” and “Relational” depict firmswith transactional and relational ownership, respectively,equal to the 90th percentile of the relevant distribution(while holding the other type of ownership at the median).

All other variables were held constant at their mean

performance. As they support a much higher levelof R&D search when performance is at the aspi-ration level, they likely do not feel the needto increase R&D spending quite as sharply inresponse to improvements in performance becausethey started from such a high baseline.

DISCUSSION

In this paper, we show that the behavioral the-ory of the firm provides robust explanations ofR&D search in a contractarian setting but requiressome modification in a communitarian setting.Japan presents an interesting context because,while Japanese firms tend to be more communi-tarian than U.S. firms, they are also subject topressures for both a communitarian orientation(from relational owners) and contractarian orien-tation (from transactional owners). Contrary to theprediction of Hypothesis 3, we find that someaspects of R&D search are the same in commu-nitarian settings as they are in contractarian set-tings. Specifically, firms that perform below theiraspiration level engage in problemistic search inorder to attempt to resolve their problems, regard-less of their ownership structure. In keeping with

the canonical behavioral theory of the firm predic-tion of problemistic search, both types of ownersseek higher search when performance falls shortof aspirations. However, we also find some crit-ical differences that suggest that the behavioraltheory of the firm explanations do require somemodification in a communitarian setting. Whenperformance exceeds aspirations, firms in contrac-tarian settings reduce or stabilize R&D search,while communitarian-oriented firms engage inmore R&D search. Furthermore, when perfor-mance exceeds aspirations, relational owners fosterhigher R&D search than transactional owners.

Our results show that relational owners, who aresupportive of a communitarian orientation, shapeR&D search differently from transactional own-ers, who are more supportive of a contractar-ian orientation. The median Japanese firm, whichadheres to a communitarian logic, responds to per-formance shortfalls with problemistic search butalso increases search for future opportunities inresponse to performance surpluses. Furthermore,relational ownership strengthens the communitar-ian orientation of the firm. Although it diminishesthe steepness of the “future search” slope, this is anartifact of the fact that they support much higherlevels of search when performance is near the aspi-ration level, and indeed they promote greater levelsof search at all levels of performance. In con-trast, transactional owners pressure managers toattenuate R&D search as performance rises abovethe aspiration level. Thus, owners influence searchbehavior consistent with their predilection forcontractarian or communitarian logic.

Our empirical results indicate that both nationalcontext and ownership structure may requireexplicit consideration when examining R&Dsearch. It is interesting to compare our resultswith those of Greve’s study (2003a), whichexamined the Japanese shipbuilding industryand found that search behavior follows patternssimilar to what is seen in U.S. firms. While thisoutcome may appear to be at variance with ourfinding of a positive relationship between R&Dsearch and performance above the aspirationlevel, post hoc inspection of our data revealed thatshipbuilding firms tend to have a high level oftransactional ownership. Our research shows thatcontractarian-oriented transactional owners tendto foster the patterns of search found in traditionalbehavioral theory of the firm research, and hence

the firms Greve (2003a) studied likely conform tothe “Transactional” line depicted in Figure 1.

Our research also suggests that there is stillmuch work to be done in exploring the institu-tional and contextual boundaries of managementtheories. We have maintained that the behavioraltheory of the firm is implicitly based on a con-tractarian context, and that extending the theory toaccount for a more communitarian context yieldsa more general understanding. Like the behavioraltheory of the firm, many management theorieshave been developed in a U.S. context and arelikely to be shaped by contractarian considerations.For example, agency theory may need some refine-ment when applied to different institutional con-texts (Hoskisson et al., 2000; Wright et al., 2005).

While we would expect that most manage-ment theories can be generalized relatively read-ily across developed capitalist economies, moreresearch on which theories may need to be mod-ified and under what conditions is warranted. Amore explicit consideration of cross-country insti-tutional differences should help to extend ourunderstanding of other management theories aswell.

It is also important to point out several impor-tant limitations of our study. First, althoughwe theorized about important differences acrossnational contexts, our empirical sample was lim-ited to Japanese corporations. Cross-country stud-ies would be useful in corroborating our resultsand verifying its generalizability across nationalcontexts. Across countries, the extent of a com-munitarian versus a contractarian logic is shapedby culture as well as institutional rules (Hall andSoskice, 2001). Thus, firms in countries such asGermany, which is believed to have a more com-munitarian logic, should engage in search behav-iors similar to what we note for Japan. By con-trast, firms in countries such as the U.K., which isbelieved to have a more contractarian logic, shouldengage in search behaviors similar to what priorresearch notes for U.S. firms.

A second limitation of our study is that we havetreated all foreign owners of Japanese firms ashomogenous and espousing a contractarian logic.While we believe that this is a reasonable gener-alization because foreign ownership is dominatedby U.S. and U.K. institutional investors who lackancillary business ties to the firm, there could wellbe some instances in which foreign investors havea close, strategic relationship with the firm. Thus,

more research examining variation among foreignowners is needed. A third limitation of our studyis that we do not consider the role of other ownerssuch as family owners. Family ownership repre-sents a distinct ownership category that is hardto characterize as either relational or transactional.Family owners tend to have a large proportionof their own wealth invested in a firm, muchlarger than foreign owners or domestic corpora-tions and institutional investors. Unlike relationalowners that own long-term shares in other firms,family ownership tends to be dedicated to the focalfirm, and therefore not as prone to reciprocal obli-gations to the network of embedded firms. Also,unlike transactional owners that can readily exittheir stake, family owners are in for the long term.Future research would benefit from an expansionof the scope of the study to other kinds of owners.A fourth limitation of our study is that we focusedsolely on the propensity for ownership structure toshift the dominant logic between contractarian andcommunitarian. However, more research on otherfactors that may pressure managers to be morecontractarian versus communitarian could signif-icantly enhance our understanding of the determi-nants of search behavior. Finally, while our theoryassumes that R&D can serve as a mechanism forgenerating the future growth opportunities that willbenefit stakeholders, more research is needed toassess the subtle mechanisms by which firms payback and pay forward their broader network ofstakeholders in the short run and in the long run.

In conclusion, we have shown that, although thebehavioral theory of the firm provides a robustexplanation of R&D search behavior, there maybe subtle, yet important, differences across insti-tutional contexts. Specifically, managers in com-munitarian contexts such as Japan may prioritizethe demands of the various stakeholder groupsdifferently than do managers in more contractar-ian cultures. Furthermore, we also show that notonly do different types of owners place divergentpressures on managers, but that the preferencesof these owners may even supersede the culturalpredispositions of a firm’s managers.

ACKNOWLEDGEMENTS

We thank Associate Editor Joe Mahoney, twoanonymous reviewers, Wei-Ru Chen, and DineshIyer for their helpful comments.

Aggarwal R, Erel I, Ferreira M, Matos P. 2011. Doesgovernance travel around the world? Evidence frominstitutional investors. Journal of Financial Economics100: 154–181.

Ahmadjian CL, Robinson P. 2001. Safety in numbers:downsizing and deinstitutionalization of permanentemployment in Japan. Administrative Science Quar-terly 46: 622–654.

Ahmadjian CL, Robbins GE. 2005. A clash of capital-ism: foreign shareholders and corporate restructuringin 1990s Japan. American Sociological Review 70:451–471.

Alchian AA, Demsetz H. 1972. Production, informationcosts, and economic organization. American EconomicReview 62: 775–795.

Allen F, Gale D. 2000. Comparing Financial Systems .MIT Press: Cambridge, MA.

Anderson S, Collins C, Pizzigati S, Shih K. 2010.Executive excess 2010: CEO pay and the greatrecession. Available at: http://www.ips-dc.org/reports/executive_excess_2010 (accessed 06 November2011).

Anderson CW, Makhija AK. 1999. Deregulation, dis-intermediation, and agency costs of debt: Evidencefrom Japan. Journal of Financial Economics 51:309–339.

Antonelli C. 1989. A failure-inducement model ofresearch and development expenditure: Italian evi-dence from the early 1980s. Journal of EconomicBehavior and Organization 12: 159–180.

Argote L, Greve HR. 2007. A behavioral theory of thefirm—40 years and counting: introduction and impact.Organization Science 18: 337–349.

Bradley M, Schipani CA, Sundaram AK, Walsh JP. 1999.The purposes and accountability of the corporationin contemporary society: corporate governance at acrossroads. Law and Contemporary Problems 62(3):9–86.

Bromiley P. 1991. Testing a causal model of corporaterisk taking and performance. Academy of ManagementJournal 34: 37–59.

Bruno GSF. 2005. Approximating the bias of the LSDVestimator for dynamic unbalanced panel data models.Economic Letters 87: 361–366.

Chen WR, Miller KD. 2007. Situational and institutionaldeterminants of firms’ R&D search intensity. StrategicManagement Journal 28: 369–381.

Cyert RM, March JG. 1963. A Behavioral Theory of theFirm . Prentice Hall: Englewood Cliffs, NJ.

David P, O’Brien JP, Yoshikawa T. 2008. The implica-tions of debt heterogeneity for R&D investment andfirm performance. Academy of Management Journal51: 165–181.

David P, O’Brien JP, Yoshikawa T, Delios A. 2010.Do shareholders or stakeholders appropriate the rentsfrom corporate diversification? The influence of

ownership structure. Academy of Management Journal53: 636–654.

David P, Yoshikawa T, Chari M, Rasheed A. 2006. Strate-gic investments in Japanese corporations: do foreignportfolio owners foster underinvestment or appropriateinvestment? Strategic Management Journal 27:591–600.

Dore R. 2000. Stock Market Capitalism: Welfare Capital-ism . Oxford University Press: New York.

Greve HR. 2003a. A behavioral theory of R&D expen-ditures and innovations: evidence from shipbuilding.Academy of Management Journal 46: 685–702.

Greve HR. 2003b. Organizational Learning from Perfor-mance Feedback: A Behavioral Perspective on Innova-tion and Change. Cambridge University Press: Cam-bridge, UK.

Hall P, Soskice D. 2001. Varieties of Capitalism: TheInstitutional Foundations of Comparative Advantage.Oxford University Press: Oxford, UK.

Hoshi T, Kashyap A. 2001. Corporate Financing andGovernance in Japan . MIT Press: Cambridge, MA.

Hoskisson RE, Eden L, Lau CM, Wright M. 2000. Strat-egy in emerging economies. Academy of ManagementJournal 43: 249–267.

Iyer DN, Miller KD. 2008. Performance feedback,slack, and the timing of acquisitions. Academy ofManagement Journal 51: 808–822.

Jensen MC. 1986. Agency costs of free cash flows,corporate finance, and takeovers. American EconomicReview 76: 323–329.

Jensen MC, Meckling WH. 1976. Theory of thefirm: managerial behavior, agency costs, and own-ership structure. Journal of Financial Economics 3:305–360.

Jilani Z. 2011. Average Japanese CEO earns one-sixth as much as American CEOs. Available at:http://thinkprogress.org/politics/2010/07/08/106536/japanese-ceo-american-sixth/ (accessed 06 October2011).

Kester WC. 1991. Japanese Takeovers: The GlobalContest for Corporate Control . Harvard BusinessSchool Press: Boston, MA.

Kim H, Kim H, Lee PM. 2008. Ownership structureand the relationship between financial slack and R&Dinvestments: evidence from Korean firms. Organiza-tion Science 19: 404–418.

Langlois S. 2012. CEO says Ford won’t back off R&Dspending. Available at: http://articles.marketwatch.com/2012-03-06/markets/31125505_1_ceo-alan-mulally-r-d-spending-ford-motor (accessed 23 Nov-ember 2012).

Lee PM, O’Neill HM. 2003. Ownership structuresand R&D investments of U.S. and Japanese firms:agency and stewardship perspectives. Academy ofManagement Journal 46: 212–225.

Lengnick-Hall CA. 1992. Innovation and competitiveadvantage: What we know and what we need to learn.Journal of Management 18: 399–429.

Lincoln JR, Gerlach M, Ahmadjian CL. 1996. Keiretsunetworks and corporate performance in Japan. Amer-ican Sociological Review 61: 67–88.

Lincoln JR, Gerlach M, Takahashi P. 1992. Keiretsunetworks in the Japanese economy: a dyad analysisof intercorporate ties. American Sociological Review57: 561–585.

Myers SC, Majluf NS. 1984. Corporate financing andinvestment decisions when firms have information thatinvestors do not. Journal of Financial Economics 13:187–221.

Nakatani I. 1984. The economic role of financialcorporate grouping. In The Economic Analysis of theJapanese Firm , Aoki M (ed). Elsevier: North Holland,Amsterdam, The Netherlands; 227–258.

O’Brien J, David P. 2009. Firm growth and type of debt:the paradox of discretion. Industrial and CorporateChange 19: 51–80.

Porter ME. 1992. Capital disadvantage, America’s failingcapital investment system. Harvard Business Review70(5): 65–82.

Sheard P. 1994. Interlocking shareholdings and corporategovernance. In The Japanese Firm: The Sources ofCompetitive Strength , Aoki M, Dore R (eds). OxfordUniversity Press: Oxford, UK; 310–349.

Tsui AS. 2004. Contributing to global managementknowledge: a case study for high quality indigenousresearch. Asia Pacific Journal of Management 21:491–513.

Uzzi B. 1996. The sources and consequences of embed-dedness for the economic performance of organi-zations: the network effect. American SociologicalReview 61: 674–698.

Vissa B, Greve HR, Chen WR. 2010. Business groupaffiliation and firm search behavior in India: respon-siveness and focus of attention. Organization Science21: 696–712.

Williamson OE. 1985. The Economic Institutions of Cap-italism: Firms, Markets, and Relational Contracting .Free Press: New York.

Wooldridge JM. 2003. Introductory Econometrics . South-Western: Mason, OH.

Wright M, Filatotchev I, Hoskisson R, Peng MW. 2005.Strategy research in emerging economies: challengingthe conventional wisdom. Journal of ManagementStudies 42: 1–33.

Yoshikawa T, Phan PH, David P. 2005. The impactof ownership structure on wage intensity inJapanese corporations. Journal of Management 31:278–300.

Yoshikawa T, Rasheed AA. 2009. Convergence ofcorporate governance: critical review and futuredirections. Corporate Governance an InternationalReview 17: 388–404.