Red Square MONEY CREATION IN A BANKING SYSTEM WITH A SINGLE MONOPOLY BANK The process of money creation is perhaps the most intriguing aspect of the economic system. It has given rise to the most extraordinary and extravagant theories. Beyond economists, it has attracted the attention of all sorts of people, from majors in the army to Chemistry Nobel Laureates. Still, the process of money creation, as well as the process of money destruction, are highly simple and can be easily understood by all. Money creation, or rather bank deposit creation as we will analyse it here, is no alchemy. It relies mainly on three features of the banking system: the willingness of banks to grant loans, the creditworthiness of borrowers, and the willingness of borrowers to take on loans. Yellow Square The Main Money Creation Channel To understand how money deposits are being created, it is best to start by imagining that the banking system is made up of a single bank, that has a total monopoly on the provision of loans and deposits in the economy, a system that 1982 Nobel Price Laureate John Hicks (1904-1989) called a monocentric banking system. All financial transactions have to transit through this single bank. Every economic agent has an account at this bank. Some agents have a negative account, in which case they have outstanding loans at the bank; other agents have a positive account, in which case they have deposits at the bank. How do new bank deposits get created? There are basically two ways in which deposits get created. Let us start with the most obvious one. Suppose that some individual wishes to purchase some goods or services, but without having the funds to do so. It may be a student who desires to purchase a new car, or an entrepreneur who is keen to hire new workers and increase production, having just received additional orders for his or her product. To go forward with their project, both the student and the entrepreneur have to borrow from the bank. They have to ask for a bank loan. Will the loan be granted? The answer is yes, as long as the borrowers are creditworthy – they are worthy of credit. The word credit comes from the Latin word credere, which means to believe or to trust. Trustworthy people or organizations can get bank credit. How can the borrowers demonstrate their creditworthiness? They may show that their past credit record is impeccable, that they have paid the interest due on their previous loans, and that they have reimbursed past loans. They may indicate that their current income is high compared to the interest payments involved with the loan that they are asking for (such ratios are now generated automatically by bank computer programs, which either flag the customer or tell the loan officer how much can be lent, and at what rate). They may show proof that the goods that they are about to produce have already been ordered by some other firm, and promised to be paid for. They may provide some guarantee – collateral – that the bank can seize in the unlikely case that they will be unable to pay interest and pay back the amounts due. In the case of a loan to purchase a house – a mortgage loan – the collateral is the house being purchased. In the case of a car loan, the collateral is likely to be the car itself. Sometimes the collateral can be financial assets – stocks, corporate bonds, government securities. If all of this is not enough, someone else may back the loan, the mother of the student, in which case she is the creditworthy person prompting the bank to grant the loan.

Transcript

Red SquareMONEY CREATION IN A BANKING SYSTEM WITH A SINGLE MONOPOLY BANK

The process of money creation is perhaps the most intriguing aspect of the economic system. Ithas given rise to the most extraordinary and extravagant theories. Beyond economists, it hasattracted the attention of all sorts of people, from majors in the army to Chemistry NobelLaureates. Still, the process of money creation, as well as the process of money destruction, arehighly simple and can be easily understood by all. Money creation, or rather bank depositcreation as we will analyse it here, is no alchemy. It relies mainly on three features of the bankingsystem: the willingness of banks to grant loans, the creditworthiness of borrowers, and thewillingness of borrowers to take on loans.

Yellow SquareThe Main Money Creation Channel To understand how money deposits are being created, it is best to start by imagining that thebanking system is made up of a single bank, that has a total monopoly on the provision of loansand deposits in the economy, a system that 1982 Nobel Price Laureate John Hicks (1904-1989)called a monocentric banking system. All financial transactions have to transit through this singlebank. Every economic agent has an account at this bank. Some agents have a negative account, inwhich case they have outstanding loans at the bank; other agents have a positive account, inwhich case they have deposits at the bank. How do new bank deposits get created? There arebasically two ways in which deposits get created. Let us start with the most obvious one.

Suppose that some individual wishes to purchase some goods or services, but withouthaving the funds to do so. It may be a student who desires to purchase a new car, or anentrepreneur who is keen to hire new workers and increase production, having just receivedadditional orders for his or her product. To go forward with their project, both the student and theentrepreneur have to borrow from the bank. They have to ask for a bank loan. Will the loan begranted? The answer is yes, as long as the borrowers are creditworthy – they are worthy of credit.The word credit comes from the Latin word credere, which means to believe or to trust.Trustworthy people or organizations can get bank credit.

How can the borrowers demonstrate their creditworthiness? They may show that theirpast credit record is impeccable, that they have paid the interest due on their previous loans, andthat they have reimbursed past loans. They may indicate that their current income is highcompared to the interest payments involved with the loan that they are asking for (such ratios arenow generated automatically by bank computer programs, which either flag the customer or tellthe loan officer how much can be lent, and at what rate). They may show proof that the goodsthat they are about to produce have already been ordered by some other firm, and promised to bepaid for. They may provide some guarantee – collateral – that the bank can seize in the unlikelycase that they will be unable to pay interest and pay back the amounts due. In the case of a loan topurchase a house – a mortgage loan – the collateral is the house being purchased. In the case of acar loan, the collateral is likely to be the car itself. Sometimes the collateral can be financialassets – stocks, corporate bonds, government securities. If all of this is not enough, someone elsemay back the loan, the mother of the student, in which case she is the creditworthy personprompting the bank to grant the loan.

SIDEBARCreditworthiness is at the core of the bank lending system. It can be demonstrated by providingcollateral, or by demonstrating the ability to face the loan obligations.Collateral is property (car, house, inventories, government securities) that is pledged by theborrower as guarantee for the repayment of a loan.

So let us suppose that indeed the borrower is creditworthy. What happens next? Theanswer to this query is simple. A bank loan gets created ex nihilo – out of nothing – at the strokeof a pen; or rather, in our modern world, the bank loan gets created by punching a key on thecomputer. Simultaneously, as the bank loan gets created, a new bank deposit also gets created.

Let us suppose that on January 2, 2008, a creditworthy borrower is being granted a newloan of $40,000 (for quite a nice car!). The effects on Bank-a-mythica, who holds a monopoly onbanking services, are shown in Table 3. The bank now has $40,000 more in loans on the assetside of its balance sheet, but simultaneously, on the liability side, there is an increase of $40,000in the bank deposits. The minute the loan has been granted, the car purchaser gets credited with amoney deposit of $40,000. This is money that the bank now owes to the car purchaser. This iswhy it is on the liability side of the bank. Tables such as this one, which shows changes inbalance sheets rather than the balance sheets themselves, will help us follow the process ofmoney creation and destruction.

Table 3Changes in the Balance sheet of Bank-a-mythica, January 2, 2008

Assets Liabilities and Net Worth

Loans to car purchaser +$40,000 Deposits of car purchaser +$40,000

There is nothing more to money creation. Since chequable bank deposits are part of M1, the moststrictly defined money aggregate as we saw on page 234, Table 3 has shown how most money

gets created in the modern world.

{IN RED} For money creation to occur, all we need is the willingness of a bank to lend and acreditworthy borrower who is willing to borrow. {END Of RED INK}

BoxLines of credit

The money-creating process can be made even more efficient when banks grant lines of credit(also called overdrafts) to their customers. As Keynes explained in 1930 in his Treatise on

Money, an overdraft is “an arrangement with the bank that an account may be in debit at any timeup to an amount not exceeding an agreed figure, interest being paid not on the agreed maximum

debit, but on the actual average debit”. There may be a fee for this line of credit.Take the case of our car purchaser. She may have already negotiated an agreement with the bank,entitling her to borrow up to a certain maximum amount, say $100,000, depending on her annual

income and her existing net wealth. The bank client can then draw on her line of credit whenevershe wants, up to the indicated limit. For instance, in the present case, assuming a $100,000 line of

credit, she would draw $40,000 to pay for her new car, paying interest on that amount (theutilized portion of the credit line). The remaining $60,000 would constitute the unused portion of

the line of credit. Because this part of the credit line is not used, no interest is charged on theremaining $60,000. However, if the car purchaser were to need to borrow some additional

amounts, say $5000 for new kitchen major appliances, she would not need to go back to the bankloan officer to obtain yet another loan. All she needs to do is draw on an additional $5,000 off the

unused portion of her existing credit line.Many businesses have these lines of credit. It gives them flexibility in handling payments to

workers and suppliers, because businesses usually sell their ware after they have been producedand paid for, so that businesses need bank advances. Lines of credit have now been generalizedto individuals, thus also providing them with more flexibility when their expenses, for whatever

reason, run (temporarily!) at a faster pace than their income. {END OF BOX}

What then happens next? Suppose that the car is being purchased the next day, on January 3 .rd

The purchaser goes to the car dealer, most likely with a certified cheque in hand, and after havinggiven the cheque and signed all the papers, she drives off with the car. The car dealer deposits the

cheque, still at Bank-a-mythica, since we assumed that this was the one and only bank of thecountry. The balance sheet of Bank-a-mythica will show the changes indicated in Table 4.

Table 4Changes in the Balance sheet of Bank-a-mythica, January 3, 2008

Assets Liabilities and Net Worth

Deposits of car purchaser -$40,000Deposits of car dealer +$40,000

By combining Tables 3 and 4, we arrive at Table 5, which summarizes the bank’s overalltransactions for those two days. The car purchaser still owes $40,000 to the bank, but all the

money deposits are now in the account of the car dealer.

Table 5Changes in the Balance sheet of Bank-a-mythica, January 2-3, 2008

Assets Liabilities and Net Worth

Loans to car purchaser +$40,000 Deposits of car dealer +$40,000

As we pointed out in page 239, all of our balance sheet tables, such as Table 2 or 5, mustbalance. In all such tables, which are called T-accounts, the two sides of the ledger must carryequal total amounts. This balance is required because changes in assets and liabilities must beequal if the balance sheet is to balance both before and after the transactions.

But Table 5 is unlikely to be the end of the story. Although the car dealer may be quitehappy to be loaded with a $40,000 bank deposit, it is most likely that the car dealer was forcedhimself to take a loan when the car was initially brought into the dealership. Indeed, the cardealer usually holds a large inventory of cars, the cost of which has to be financed by bank loans.So it is most likely that the car dealer will use the proceeds of his sale to diminish the amount ofhis outstanding loans at Bank-a-mythica. Thus, the following change, as shown in Table 6, islikely to appear on the bank’s balance sheet.

Table 5Changes in the Balance sheet of Bank-a-mythica, January 4, 2008

Assets Liabilities and Net Worth

Loans to car dealer -$40,000 Deposits of car dealer -$40,000

The car dealer uses his newly acquired deposits to pay back the bank. The money gets destroyed!When borrowers reimburse their loans, money gets destroyed. At the end of the week, adding

Tables 3, 4, and 5, we obtain Table 6. In the end, despite all the action, there has been no changein the stock of money deposits. But the composition of the balance sheet of the bank haschanged, with car purchasers owing more funds to the bank, while car dealers owe less.

Table 6Changes in the Balance sheet of Bank-a-mythica, January 2-5, 2008

Assets Liabilities and Net WorthLoans to car purchaser +$40,000Loans to car dealer -$40,000Total No change No change

Yellow SquareA Subsidiary Money Creation Channel

We said in the previous section that there were two main channels of money creation. The firstone is through banks granting new loans. The second channel is tied to changes in the

composition of financial portfolios. Money is not the only financial asset that agents can hold.People can hold banknotes (about which more will be said later), chequable and non-chequablebank deposits – these assets being defined as M1 money stock – as well as chequable deposits

from other financial institutions, certificates of deposits, stock market shares, mutual fund shares,bonds, etc. Money is being created when non-financial economic agents, such as manufacturingcorporations or households, transform some of their non-monetary assets into deposits that aredefined as being money (M1, M1+, M2, M2+, etc.). This can occur either because these non-

financial agents decide to hold a greater proportion of their financial wealth in the form ofdeposits, or when banks wish to hold a bigger proportion of their assets in the form of securitiesrather than in the form of outstanding loans. For this kind of money creation to occur, there has

to be a double coincidence of wants: on the one hand, non-financial agents wish to hold moredeposits; and on the other hand, banks wish to hold more assets beyond loans.

Table 7 shows how such a creation of money would occur. The non-financial agent, here ToyManufacturer, sells securities (for instance, government bills that it holds) and gets bank depositsin exchange; Bank-a-mythica purchases the government bills, and credits the sale proceeds to thedeposit account of Toy Manufacturer. We may call this the portfolio-change process. The non-

financial agent is no richer than it was before – its wealth does not change, only the compositionof its wealth has changed – but note that the size of the balance sheet of the banking system hasnow risen by $1000. Both the assets and the liabilities of Bank-a-mythica have risen by $1000.

Of course the portfolio-change process may operate in reverse gear. Manufacturer Toymay be unhappy about the interest rate it is getting on its bank deposits at Bank-a-mythica. It maybe want to hold more of its financial assets in the form of securities, which may be slightly lessconvenient but which carry a slightly higher rate of return than the interest rate on moneydeposits. In this case, Manufacturer Toy may offer to buy securities at a price that will induceBank-a-mythica to sell them. Money, therefore, gets destroyed. The deposits of ManufacturerToy diminish by $1000, while its holdings of securities rise by $1000, and the size of the balancesheet of Bank-a-mythica diminishes by $1000.

In the rest of this chapter, we will concern ourselves with the first of these two moneycreating channels. From a macroeconomic point of view, the lending channel by which moneygets created is a more interesting one as it generally involves changes in income, sales andproduction., which is usually not the case of the portfolio-change process.

Yellow Square

The Limits to Money Creation

One of the most striking feature of the money-creation process, especially through the lendingchannel, is that there seems to be no limit to the creation of money. In a sense this is true. Thecreation of money is not limited by some scarce resource such as the amount of gold that bankshave accumulated in their vaults. It is sometimes argued that this was the case in the past, and itmay have been, although economic historians argue with each other about that, but it is certainlynot the case in modern banking systems. Nowadays banks are free to lend as much as they want.This is certainly true of our monopoly bank, but as we shall see in the next section, it is also trueeven in the general case, when there are several competing banks.

Take first the case of our monocentric banking system. What could its restrictions onlending be? The amount that the monopoly bank can lend is only limited by the three crucialfeatures of the banking system that we identified earlier: the willingness of the bank to grantloans, the creditworthiness of borrowers, and the willingness of borrowers to take on loans.

As in all economic transactions, both partners to the transaction need to be willing toengage in the transaction. For a loan to be granted, and for bank deposits to be created as aconsequence of this new loan, both the bank and the borrower have to be willing to go aheadwith this operation. Why would economic agents refuse loans that they are being offered? Thereason is that they may be unwilling to get into debt and pay interest on this debt. They may alsosee no reason to spend more, or they may be scared of going bankrupt if they borrow too much orborrow any more. Thus borrowers, on their own, may willingly put limits on the amounts theywant to borrow. By borrowing too much, they are afraid that they may lose their entire wealth ora large part thereof. This is sometimes called the borrower’s risk.

Why would a monopoly bank be unwilling to lend? For exactly symmetric reasons. Thebank may fear that some of its clients may be unable to reimburse their loans or make the interestpayments that are due. This is the lender’s risk. If too many of the borrowers of the bank are inthis situation, the bank may become insolvent and may be closed down, as we will explain in ashort time. This is why the bank is on the look for creditworthy customers. Unless the bank isreally pessimistic about future prospects, for instance, fearing an economic recession in the nearfuture, thus being reluctant to increase the size of its balance sheet, the bank is always looking fornew creditworthy borrowers, or willing to increase the size of loans granted to previouscreditworthy borrowers.

But why is the bank looking for creditworthy borrowers and not just any kind ofborrower? Why does the bank fear customers who do not make their interest payments orreimburse their loans? First, as pointed out in page 237, banks are in the business of makingprofits. Besides service fees, banks make their profits on the difference between: their revenues– the interest payments that they receive on their assets (on their loans and the securities that theyhold) and their costs – the interest payments that they have to make on their liabilities (essentiallyon the deposits that people hold at the bank) plus the costs of operating a bank (the salaries ofclerks and loan officers, rentals, the costs of running the automatic teller machines, etc.). Ifborrowers don’t fulfill their interest payment obligations, banks will make losses, not profits.

Bad loans have a second, less obvious, implications. Suppose the bank, by mistake,makes a loan of $200,000 to a non-creditworthy person, and that this person turns out to be acrook. Instead of building a prosperous business with the borrowed money, the crook spends itall in bars, cars, and casinos. At the end of the year, the bank manager wakes up and finds out

about all this. The borrower has defaulted on the loan and has vanished; the collateral that hadbeen offered to get the loan is worthless. There is no way the loan can be recovered. It has to beconsidered as a “bad loan”, and thus must be entirely “written off”. While this is an extreme case,small businesses regularly go bankrupt (as sometimes do large corporations), because of poorplanning, bad luck, or changing economic conditions. Their banks can only recover a portion ofthe loans that they granted. The rest has to be written off.

How will the accountants of the bank take care of this? Table 8 shows how a $200,000bad loan is written off. Since the loan is now worth nothing, it must be removed from the assetsof the bank on its balance sheet. A minus $200,000 entry will thus need to be recorded into thechanges of the balance sheet. But a T-account must always balance by definition. What otherchange must we make for the balance sheet to balance? The answer is to be found in the bank’scapital. The bank has suffered a $200,000 capital loss, which must be subtracted from the bank’sown funds.

Table 8Writing-off a bad loan, Changes in the Balance sheet of Bank-a-mythica

Assets Liabilities and Net WorthAssets LiabilitiesSecurities no change Chequable deposits no changeLoans outstanding -$200,000Total -$200,000 Net Worth

Bank’s capital -$200,000Total -$200,000

Table 9Balance sheet of Bank-a-mythica, December 31, 2007, after accounting for bad loan

Assets Liabilities and Net WorthAssets LiabilitiesCurrency $100,000 Chequable deposits $5,000,000Securities $1,000,000Loans outstanding $4,200,000 Net WorthTotal $5,300,000 Bank’s capital $300,000

Total $5,300,000

The new balance sheet of Bank-a-mythica, once the loan loss has been taken into properaccount, will thus look like Table 9, with Table 9 being the sum of Table 2, before the loss wasrecorded, and Table 8, which records the change induced by the loss. In Table 9, compared toTable 2, Bank-a-mythica has a smaller net worth, but this net worth is still positive, standing at$300,000. Although Bank-a-mythica is not in as good a shape as it appeared in Table 2, it is stillsolvent. In other words, despite the bad loan, the bank’s capital is still positive, as its assets arestill larger than its liabilities. The bank could still face a string of bad loans. Nonetheless, mostlikely, the bank would be concerned about the decline in its own funds and would make an effort

to increase its capital (for instance by issuing new shares), or by being more prudent in its futuredealings and in the choice of its borrowers. SidebarA solvent bank is a bank that has positive net worth. The bank’s capital is positive, so that itsassets are larger than its liabilities. An insolvent bank has negative net worth.

Suppose however that more borrowers have defaulted on their loans, for instance becausetheir businesses did much more poorly than what was predicted in the marketing plan. Supposethat $900,000 worth of loans turned out to be bad loans that year. $900,000 worth of loans mustthus be subtracted from the asset side of the balance sheet of Bank-a-mythica, as shown in Table10, and $900,000 must be subtracted from the bank’s capital. But wait! The own funds of thebank, the bank’s capital, were only $500,000. What happens now? The net worth of the bankbecomes negative, standing at -$400,000. The bank is insolvent. Its liabilities – the deposits ofits customers – are not covered by enough assets (the sum of the securities and loans). The bankmust go under and declare bankruptcy, or its assets and liabilities have to be taken over by someother bank.

To try to avoid such bank failures, there are minimum requirements that are appliedworld-wide regarding the size of bank capital relative to the value of assets (especially the valueof risky loans). These requirements are known as capital adequacy requirements, and theirgeneralization to banks of many countries has been spearheaded by the Bank for InternationalSettlements (BIS), an international organization located in Basel, Switzerland.

Table 10Balance sheet of Bank-a-mythica, December 31, 2007, after accounting for huge bad loans

Assets Liabilities and Net WorthAssets LiabilitiesCurrency $100,000 Chequable deposits $5,000,000Securities $1,000,000Loans outstanding $4,200,000 - $900,000 = $3,500,000

Net Worth

Bank’s capital $500,000 - $900,000= -$400,000

Total $4,500,000 Total $4,500,000

The lesson to be drawn from this is that Bank-a-mythica faces no limit as to the amountof loans it can make, and therefore to the amount of money it can create, save for its own fear ofmaking losses and failing. What limits the creation of money is the number of creditworthyborrowers and the willingness of these potential borrowers to borrow. If no one is willing to gointo debt, no new loan will be granted and bank deposits will not grow. As the saying goes, youcan bring a horse to water, but you cannot force it to drink!

It should also be clear that monetary relations are based on conventions – on customs.The definition of a creditworthy borrower will not be the same in all time and space. Someone

classified as a creditworthy person today in Canada may not have been in the past or in someother country. For instance, criteria to obtain mortgage loans are now much less stringent thanthey were in the past. Also, different banks may have different opinions with regard to thecreditworthiness of the same person. Since we are talking about different banks, this is a goodtime to consider the limits of money creation when several banks are operating within themonetary system.

BoxBank Failures

Thousands of American banks failed during the Great Depression, as they became insolventwhen the value of their assets plummeted with the downfall in economic activity, with otherbanks refusing to make transactions with them when insolvency was suspected, and with thesebanks often being subjected to bank runs. The surviving banks became overly cautious during theGreat Depression, denying loan demands and recalling loans that had been previously made. Thismade the recession even worse, as producers lacked the financial means to produce, thusreducing production and paid wages. As wages received diminished, household consumption alsofell. In addition, when banks went under, depositors lost the money that they had in these banks,further reducing consumption and hence economic activity.

In Canada, not a single bank failed during the Great Depression. Still, in Canada aselsewhere, many bank loans to companies and entrepreneurs must have turned bad, becomingworthless as these companies and individuals went bankrupt. Most probably, some Canadianbanks, as many other surviving banks in the rest of the world, were insolvent then – a point thatwas made by Keynes himself in 1931. But as long as nobody takes notice, or as long as everyoneturns a blind eye, the bank can continue to operate. This shows once more that monetary systemsrely on trust and conventions.

By contrast, as was mentioned earlier and listed in Table 1, in 1985 two Alberta-basedbanks failed – the Canadian Commercial Bank and the Northland Bank, causing a bank run on atleast three other small Canadian banks. The big recession of 1981-1982, the slowdown in the oiland gas sectors, and the concomitant large increase in interest rates are sometimes blamed forthese two failures, as the two Alberta banks were heavily involved in the regional real estatemarket in Western Canada. The Estey Commission, which, as noted on page 238 was set up bythe Canadian federal government to investigate the causes of the failures, concluded that bankmanagement pursued imprudent lending policies and bizarre banking procedures, along withmisleading financial statements. Indeed, the failures of these two Canadian banks show somesimilarities with the Savings and Loans (S&L) debacle in the United States, also in the 1980s.S&L institutions were financial institutions similar to our credit unions or Caisses populaires.The cause of the failure of S&Ls is well-documented. Besides difficulties caused by a mismatchbetween short-term liabilities and short-term assets at a time of rising interest rates, evidence offraud and insider abuse, tied in particular to real estate swindles, has been uncovered, leading toconvictions of fraud and racketeering.

Regulation and bank supervision is needed, not only to restrict overly enthusiasticbankers, but also to create an environment where financial fraud is more difficult, just likebanknotes issued by the Bank of Canada are made in such a way that they are difficult toreproduce, to avoid counterfeiting. {End of Box}

Red SquareMONEY CREATION IN A BANKING SYSTEM WITH SEVERAL BANKS

We have seen that loans made to individuals or corporations, and hence money creation, dependon trust. The same is true of the relations between banks. Whenever they engage in transactionswith each other, banks must trust each other, otherwise the banking system would grind to a halt,or the banks which are not trusted by the other banks would quickly be unable to operate andtheir clients would suffer great inconvenience. Well-functioning banking systems haveinstitutions that allow banks to make their transactions with each other with great confidence. InCanada, transactions between banks are regulated through the Payment Clearing and SettlementAct, which was proclaimed in 1996, and through the by-law of the Canadian PaymentsAssociation. The Bank of Canada is a key player in this institutional setup, in particular itoversees the payment system, but its role will be mainly discussed in the next chapter.

As is the case for individuals, the transactions between banks are closely monitored withthe help of credit ratios. These ratios depend on the amount of collateral that each bank is willingto provide to the LVTS, and on the amount of bilateral credit limits that participants grant to eachother. The purpose of these controls is to insure that the troubles of one bank will not snowballinto other banks running into trouble – the issue of systemic risk. Collateral and trust, orcreditworthiness, are thus the kingpin of a monetary system. Sidebar:There is systemic risk in a payment system when the failure of one bank to meet its obligationscould lead to the failure of other banks to meet their obligations, thus jeopardizing thefunctioning of the entire payment system.

Yellow SquareThe Canadian Clearing and Settlement System

To understand the functioning of a banking system with multiple banks – a polycentric bankingsystem as Hicks would call it – let us go back to a situation which is very similar to that of ourinitial example. Let us suppose that a Chevrolet car dealer must now pay for an allotment of carsthat was sent to him by the car producing company. Suppose that in order to do so the car dealermust draw on his line of credit (See the earlier Box, “Lines of Credit”), for an amount of$400,000, thus increasing the amounts borrowed from his bank, say the Bank of Montreal, by anamount of $400,000, and ordering his bank to pay this amount to GM Canada. Let us supposethat GM Canada does business with another bank, say, the Toronto Dominion Bank.

SidebarA line of credit is an arrangement with the bank that allows someone to borrow freely up to anamount not exceeding an agreed figure, interest being paid not on the agreed maximum, but onthe actual average loan.

Because the amount involved is large, the payment will go through an electronic-onlypayment system (instead of a paper payment system, such as is the case with ordinary cheques).In Canada, this electronic-only wire system is called the large-value transfer system (LVTS). Ithas been operating since 1999. This is a clearing and settlement system, in which banks and afew other participants in the LVTS, such as the Fédération des caisses Desjardins and moreimportantly the Bank of Canada, clear their payments and settle their accounts. About 90 percentof the value of bank payments go through the LVTS. From now on, the participants to the LVTS,save the Bank of Canada, will simply be referred to as “banks”.

SIDEBARClearing is the continuous daily process by which banks exchange and deposit payment itemsfor their clients, and determine the net amounts owed to each. Settlement is the end-of-day procedure by which banks use borrowing and deposit facilities atthe Bank of Canada to fulfill their net obligations to all other banks.

Before any large transaction goes through between two banks (before it clears), acomputerized system verifies that the debit position of the paying bank is not too large. Once thecontrols within the system are all satisfied, the transaction clears and the payment is irrevocable.It cannot be reversed. If a bank were to fail by the end of the day, before final settlement, thecollateral pledged by the failing bank or the collateral pledged to the LVTS by the remainingbanks would be enough to cover any amount due by the failing bank. In our car dealer example,as soon as the $400,000 payment from the Bank of Montreal to the Toronto Dominion bank iscleared, a $400,000 amount is deposited in the bank account of the car producer, GM Canada,and that payment is final. It cannot be revoked.

Thus a loan is initially granted by the Bank of Montreal, with deposit money createdtherein, but the deposit eventually ends up in an account at the Toronto Dominion Bank. Howwill all this be entered in the balance sheets of the two banks at the moment that the transfer tothe account of GM Canada occurs? Let us look at Table 11.

Table 11The money creation channel with two different banks: Intraday Changes in balance sheets

Bank of Montreal Toronto Dominion Bank (TD)Assets Liabilities Assets LiabilitiesLoans to Chevrolet cardealer +$400,000

LVTS balances +$400,000

Deposits of GMCanada+$400,000

LVTS balances-$400,000

LVTS Assets Liabilities and Net Worth

Balances of Toronto Dominion Bank +$400,000Balances of Bank of Montreal

-$400,000

The trick to understand what is going on is to remember that all balance sheets mustbalance. If the Bank of Montreal has made more loans than it has collected deposits, and if theToronto Dominion Bank has collected more deposits than it has made loans, as is the case in ourinstance illustrated by Table 11, there has to be some adjustment mechanism that will make theT-accounts balance.

The Chevrolet car dealer has ordered his bank to transfer $400,000 of his newly acquiredmoney to the deposit account of GM Canada at the Toronto Dominion Bank. Now, as shown inthe bottom part of Table 11, once the transfer is recorded through the LVTS, the Bank ofMontreal owes this $400,000 amount to the clearing system – it is said to have a negative LVTSbalance or to have a debit LVTS position – while the Toronto Dominion Bank is said to hold apositive LVTS balance or to have a credit LVTS position. The system owes the TorontoDominion Bank $400,000.

SIDEBARThe LVTS balance of a bank is the multilateral clearing position that the bank has accumulatedwithin the large-value transfer system in the course of the day. When the bank is in a net creditposition, the balances are positive; when the bank is in a net debit position, the balances arenegative.

Things may change quite rapidly however. During the same day, it may be that GMCanada has to pay its suppliers, producers of metals or plastics, several of whom may be holdingaccounts at the Bank of Montreal. In that event, payments will have to flow from the TorontoDominion Bank towards the Bank of Montreal, and the positive LVTS balances of the TorontoDominion Bank may get reduced close to zero, or may even become negative. And as furtherpayment orders come in during the day, there will be further changes to the net position of eachof bank. These changes can be quite large, so that each morning each participant decides how biga bilateral credit line it grants to each of the other participants, on the basis of their creditassessment. In addition, a central computer calculates the position of each participant on apayment-by-payment basis, so that each bank is aware of its overall position and that of everyother bank. The net amount that each participating financial institution is permitted to owe issubject to bilateral and multilateral limits. Various whistles go off when one bank goes too far ina negative position. In that case, the bank with the excessive negative position will have to waittill it receives transfers from the other banks before it can go ahead with the payments ordered byits depositors .

BoxGross Flows of Payments and Net Balances in the Large-Value Transfer SystemThe Canadian LVTS is unique among clearing and settlement systems in the world, and is highlycost efficient. In other countries, to insure payment finality, large-value payments involve animmediate transfer of funds on the settlement accounts of banks, on the books of the centralbank. But each clearer must hold central bank deposits that are sufficiently large to cover anypossible outgoing payment. In Canada, settlement only occurs at the end of the day, on a

multilateral basis, but payment finality is guaranteed as soon as the payment is being accepted bythe system and thus clears, thanks to the collateral arrangements mentioned above.

The following numerical example may help to explain how the main Canadian clearingand settlement system – the LVTS – works. Suppose the following transactions occur betweenthree banks that participate in the LVTS during the day (the numbers are not unreasonable, giventhat on average, in 2006, no less than $166 billion worth of payments did transit through theLVTS every day – about one ninth of Canada’s annual GDP!)

The Bank of Montreal (BMO) makes payments of $30 billion to depositors of the TorontoDominion Bank (TDB).The Bank of Montreal (BMO) makes payments of $30 billion to depositors of the CanadianImperial Bank of Commerce (CIBC).The Toronto Dominion Bank makes payments of $22 billion to depositors of the Bank ofMontreal.The Toronto Dominion Bank makes payments of $20 billion to depositors of the CanadianImperial Bank of Commerce.The Canadian Imperial Bank of Commerce makes payments of $40 billion to depositors ofthe Bank of Montreal.The Canadian Imperial Bank of Commerce makes payments of $18 billion to depositors ofthe Toronto Dominion Bank.

The following table sums up these transactions and their implications with regards to thesettlement balances of the three banks.

Although there have been transactions reaching a total gross amount of $150 billion, the netamounts involved are much smaller, with the Bank of Montreal being left with $2 billion ofpositive LVTS balances. In other words, the Bank of Montreal is here in a net credit LVTSposition. The Toronto Dominion Bank has a LVTS positive balance of $6 billion, while theCanadian Imperial Bank of Commerce holds the difference, a $8 billion negative LVTSbalance (a net debit LVTS position). It would be easy to build other examples where the totalamount of positive balances is even smaller, despite actual daily transactions being of a largersize. Thus the size of positive LVTS balances is only very indirectly related to the amount ofmonetary transactions or the volume of economic activity. It is a random number thatdepends on the relative size of incoming and outgoing payments for each LVTS participant.{END OF BOX}

But suppose now that we have reached the end of the day, and that the situation is thatdescribed by Table 11, with the Bank of Montreal still being in a $400,000 debit LVTS position(a negative LVTS balance). Can such a situation last? As we will see in the next chapter, in asense it could. But there are economic incentives for this situation to be reversed. The banks thathave positive LVTS balances will usually lend them to the banks that have negative balances!This will occur on a segment of the overnight market – the interbank market – where banksmake loans to each other. In the present case, at the end of the day, the Toronto Dominion Bankcan grant a one-night loan of $400,000 at the overnight rate of interest to the Bank of Montreal.This generates a LVTS credit (positive) flow of $400,000 for the Bank of Montreal, and anegative LVTS flow of $400,000 for the Toronto Dominion Bank, as shown in Table 12, thusallowing both banks to bring their LVTS balances to zero (when Tables 11 and 12 are added).The end result for the balance sheet of each bank is shown in Table 13. SIDEBARThe interbank market is the financial market where banks lend and borrow surplus fundsbetween themselves for one night.The overnight market is the financial market where banks and other financial marketparticipants (investment dealers, pension funds, large corporations, trust companies, theGovernment of Canada) lend and borrow surplus funds for one night. The overnight market hasthree components, one of which is the interbank market.

Table 12The Toronto Dominion Bank Grants an Overnight Loan to the Bank of Montreal: Changein LVTS balances

LVTS Assets Liabilities and Net Worth

Balances of Toronto Dominion Bank -$400,000Balances of Bank of Montreal +$400,000

Table 13The Money Creation Channel with two Different Banks: Overnight Changes in balanceSheets

Bank of Montreal (BMO) Toronto Dominion Bank (TD)Assets Liabilities Assets LiabilitiesLoans to Chevrolet cardealer +$400,000

Funds borrowed fromTD +$400,000

Advances made toBank of Montreal+400,000

Deposits of GMCanada+$400,000

LVTS balances$0

LVTS balances$0

Once again we can draw lessons from this example. First, it is clear that the polycentricbanking system relies on trust and creditworthiness. Banks have to be sufficiently confident inother banks and in the clearing and settlement system to accept that other LVTS participants runtemporary negative balance positions during the day, and to grant overnight loans to banks thatend the day with a deficit LVTS position. Indeed, as we noted earlier, institutions have been setup so that transactions can be carried with very little risk. In addition, as long as all bankinginstitutions are “moving in step”, granting loans and collecting deposits at approximately thesame pace, the situation of a polycentric banking system is not very much different from amonocentric one, because on average, over a period of weeks, the positive and negative positionswill compensate each other for each bank, although they will not on an hour per hour basis.

When some banks are growing faster than others, with their loans growing faster thanthose of other banks, things are more complicated, as these fast-growing banks will show netdebit LVTS positions systematically, unless they find other means to compensate for thediscrepancy between loans and deposits. In the United States, New York City bankssystematically run deficit clearing positions, and so do some banks in Europe. There are basicallytwo ways through which banks that run systematic clearing deficits avoid borrowing extensivelyfrom other banks. First, they can offer certificates of deposits, at attractive interest rates, that arepurchased by the banks or other financial market institutions that have surplus funds. This iscalled liability management. This often involves another segment of the overnight market – themarket for overnight wholesale deposits. Second, once they have granted new loans, they can sellbunches of loans to banks or financial institutions that are in a surplus position. This is aninstance of securitisation, whereby a loan is transformed into a financial vehicle that can be sold,just like a security.

SIDEBAR

Liability management is the process through which banks attempt to obtain funds, for instanceby offering certificates of deposits at attractive interest rates, and hence attracting wholesaledeposits.Securitisation is the process through which illiquid financial assets – assets that cannot be soldeasily, such as mortgages – are transformed into marketable instruments – financial assets thatcan easily be sold and purchased.

At this stage it should be clear that, in a modern monetary system such as the Canadianone, nothing, besides the prudence of bankers and the self-restraint of borrowers, limits thecreation of credit and that of money. This feature of our monetary system, the fact that thecreation of money is essentially endogenous, has advantages. It provides flexibility to themonetary system: monetary units get easily created when the economy is expanding and there is aneed for additional units of money for production and transaction purposes. However, as for mostthings, there is a downside to this flexibility.

In all likelihood, when the economic perspectives are bad, bankers and their customerswill tend to be extra prudent. However, when economic perspectives look good, both bankersand their clients may become overly enthusiastic. Demand for credit may quickly rise andbankers are likely to grant new loans at an accelerating pace, attributing creditworthy status tonearly all income earners. With loans increasing, so will the stock of money. On the basis of

supply and demand analysis, one could then argue that this process ought to lead to rising interestrates – the cost of loans – and that this would then somewhat restrain the demand for loans andthe growth of the money supply. But what happens is that both the demand for and the supply ofloans increase in tandem, as bankers are just too happy to finance the expenditures that theircustomers desire. Hence, with demand and supply growing together, under these circumstancesthere is no inherent market force pushing interest rates upwards.

If such a process persists, at some stage the rising demand for credit and money willoutpace the growth of potential output. An inflationary gap will appear, and the inflation ratewill start rising. In addition, as has happened in the past, speculative bubbles may erupt, leadingto fast-rising prices in the stock market or in the real estate market which may further disrupt theeconomy. Some outside intervention is necessary.

THE BANK OF CANADA: MONETARY POLICY IMPLEMENTATION

Monetary policy can be conceptually divided into two components: monetary policy strategyand monetary policy implementation. Monetary policy strategy is closely tied to monetarymacroeconomics. It deals with the macroeconomic goals of the central bank, for instanceachieving a target inflation rate or a given growth rate of economic activity, and how best toachieve them, especially when goals may be conflicting over the short run. It also deals with themonetary stance and the transmission mechanism of monetary policy – the decision to change thevalue of some monetary variable under the control of the central bank and how this change willimpact the macroeconomic objectives. In other words, monetary policy strategy depends on themacroeconomic model that lies behind the actions of the central bank.

SIDEBAR: Monetary policy strategy is the decision that the central bank takes about somemonetary variable that constitutes its operational target, for instance a short-term rate of interestthat it can control, with the view of influencing or achieving some macroeconomic outcome ortarget, for instance a certain rate of inflation.

Monetary policy implementation is the set of rules, instruments and day-to-day actionsthat allow the central bank to implement its operational target.

By contrast monetary policy implementation deals with the day-to-day, or even the hour-per-hour, operations of the central bank. We can say that it corresponds to the nitty-gritty aspectsof monetary policy. Monetary policy implementation is made up of two elements – theoperational target and the operational instruments – both of which must be under the control ofthe central bank if monetary policy implementation is to be successful. Today, there is a wideconsensus among central bankers that the operational target ought to be a short-term interest rate.In Canada, this operational target is the overnight interest rate on collateralized transactions.This is the rate of interest that arises from the overnight market, which we already encountered inChapter 12 when discussing the clearing and settlement system of Canadian banking. It is the rateat which banks and other financial market participants lend and borrow from each other for onenight, using or searching for surplus funds fully secured by acceptable collateral. The operationaltarget of the Bank of Canada is thus the target overnight interest rate.

SIDEBAR: The overnight interest rate is the interest rate that banks and other financial marketparticipants pay and receive when they borrow and lend surplus funds from each other for oneday, in particular when banks borrow and lend LVTS balances from one another.

The target overnight interest rate is the operational target of the Bank of Canada; it isthe overnight rate that the central bank would like to see realized.

In what follows we examine the operational framework – the technical instruments thatallow the Bank of Canada to achieve its operational target. In other words, we first deal withmonetary policy implementation. Monetary policy strategy – the choice of the value taken by theoperational target – will be studied once we know how the central bank implements its decisions.

Yellow Square

The Corridor System

How the operational target gets implemented in the Canadian monetary system is a simple story.Unless there are special circumstances, the Bank of Canada makes an announcement eight timesa year, in the early morning at specific dates, as to what its target overnight interest rate will beuntil the next announcement. Et voilà!

The Bank of Canada accompanies its new rate announcement with an explanation of itsdecision to decrease, increase or keep constant the target overnight rate (See the Box “Bank ofCanada Press Release”). These justifications have more to do with monetary policy strategy, andhence they will be dealt with later. In the meantime what must be noted is that the targetovernight rate is accompanied by an operating band, which is made up of two additional interestrates that stand below and above the target overnight rate. These two rates are respectively theinterest rate on deposits at the central bank and the interest rate on advances made by theBank of Canada to the banks that participate in the Large Value Transfer System (the LVTS, aswe called it in Chapter 12). This latter rate is also called the Bank rate. These two interest ratesthus determine the operating band. This band looks like a corridor – a channel or a tunnel – thusleading this operating framework to be called the corridor system, as shown in Figure 1.

SIDEBARThe Bank rate is the interest rate charged to banks that still have negative LVTS balances at theend of the day, and hence that must take advances (borrow funds) for one night from the Bank ofCanada in order to settle with the LVTS.The interest rate on deposits at the central bank is the rate of interest that banks get on theirdeposits at the Bank of Canada as a result of the operation of the LVTS. Banks with positiveLVTS balances must deposit them in their account at the Bank of Canada when settlement occursat the end of the day.The operating band is the zone of overnight rates comprised between the Bank rate and theinterest rate on bank deposits at the central bank.The corridor system is the operating framework adopted by the Bank of Canada which forcesthe overnight interest rate to remain within the operating band and close to the midpoint of theband, as defined by the target overnight rate.

Figure 1

The Target Overnight Interest Rate with its Operating Band

Figure 1 illustrates the case where the target overnight rate of interest is 4.25 percent. As aresult, the Bank rate is set at 4.50 percent, since the Bank rate is always set at one quarter of onepercent (or 25 basis points, as financial market specialists say) above the target overnight rate.Symmetrically, the interest rate on deposits at the Bank of Canada is set at 25 basis points belowthe target overnight rate. As a result, the operating band is 50 basis points wide.

The Bank of Canada thus acts as a price-fixer with respect to the short-term interest rate.It constrains the values that the overnight interest rate can take by setting both a floor and aceiling to the values that can be taken by the overnight interest rate. The Bank of Canadapromises to take as a deposit, paid at a 4 percent rate, any amount of positive LVTS balancesheld by an individual bank; and it promises to grant advances, at a 4.5 percent cost, to anyindividual bank that has negative LVTS balances (provided the bank has adequate collateral).The overnight rate can, in theory, take any value within the operating band, the range of which isgiven by the grey area in Figure 1. But it cannot get outside this band. It is constrained within acorridor. Why is this so? Why does the Bank of Canada have the power to influence so much the

overnight rate? The essential reason for this is that in Canada, as in virtually all countries, allpayments must eventually settle on the books of the central bank, here the Bank of Canada.

{In RED} Recall from Chapter 12 that payments go through two steps: first they are cleared,then they are settled. The main clearing system is the Large-Value Transfer System (LVTS).Clearing is the daily process by which banks exchange and deposit payment items for theirclients, and determine the net amounts owed to each. Settlement is the procedure by which banksuse claims on the Bank of Canada to fulfill their net obligations to all other banks at the end ofthe day.

The Bank of Canada is the settlement agent of the LVTS. Banks need to settle with the LVTS atthe end of the day, and they must do so on the books of the Bank of Canada. The Bank of Canadaprovides settlement accounts to LVTS participants; it provides funds to those that need to covertheir settlement obligations (those that have negative LVTS balances at the end of the day); and ittransfers claims on itself for those banks ending the day with positive LVTS balances. {End ofRed}

Suppose, as was the case in the example of Table 11 in Chapter 12 which we partlyreproduce here as the top of Table 1, that the Bank of Montreal has a net debit LVTS position(negative LVTS balances) by the end of the day. How much is it willing to pay other banks toborrow balances from them and bring its LVTS balance position back to zero? Clearly it is notwilling to pay an interest rate higher than 4.50 percent since this is the rate that the Bank ofCanada will charge to banks with negative LVTS balances. If all other banks were offering tocharge more than 4.50 percent to lend LVTS balances, the Bank of Montreal would turn downthese offers and would simply take an advance from the Bank of Canada at the Bank rate of 4.50percent.

Now, what about the banks that have positive LVTS balances? What is their reasoning?Suppose, as shown in the top part of Table 1, that the Toronto Dominion Bank has a net creditLVTS position. What is the minimum interest rate that will induce the TD Bank to lend itsbalances to other banks (thus also bringing its LVTS balance position back to zero)? Clearly, itneeds to get paid more than 4.00 percent, since this is the rate that it would get anyway if it wereto leave its LVTS balances as a deposit at the Bank of Canada. If no deal can be struck betweenthe Bank of Montreal and the Toronto Dominion Bank, then the balance sheet of the Bank ofCanada will be as shown in Table 2. The Toronto Dominion Bank will be granted a claim on theBank of Canada – its LVTS balances will be brought down to zero and transformed into anovernight deposit at the Bank of Canada; as to the Bank of Montreal, it will have to borrow$400,000 from the Bank of Canada to bring its LVTS balances back to zero.

Table 1Balance Positions of Banks in the LVTS

Intra-day LVTS, Before SettlementAssets Liabilities and Net Worth

Balances of Toronto Dominion Bank +$400,000

Balances of Bank of Montreal -$400,000

End-of-day LVTS, After SettlementAssets Liabilities and Net Worth

Balances of Toronto Dominion Bank +$0Balances of Bank of Montreal +$0

Table 2Balance Sheet of Bank of Canada, with no Deal Struck Between Banks

Bank of CanadaAssets Liabilities and Net WorthAdvance to the Bank of Montreal, at 4.50 percent +$400,000

Deposits of Toronto Dominion Bank, at 4.00 percent +$400,000

The overnight interest rate, that will arise out of the negotiations between potentiallenders and borrowers of overnight funds will thus have to be somewhere between 4.00 and 4.50percent. Indeed, unless there are some unusual circumstances, the realized overnight rate willturn out to be very close to the middle of the operating band, at the target overnight rate – in thecase of Figure 1 it will stand at 4.25 percent, or very close to it, say at 4.23 or 4.24, or perhaps4.26 percent. There are essentially two reasons for this. First, the banks know that the Bank ofCanada wishes the overnight rate to be around 4.25, and that it will intervene if the actual ratekeeps drifting away from the target rate. Secondly, competition should bring the overnightinterest rate near the middle of the operating band, because at that point the opportunity gain ofthe lenders and that of the borrowers are precisely the same, being equal to 25 basis points forboth groups of participants to the overnight market.

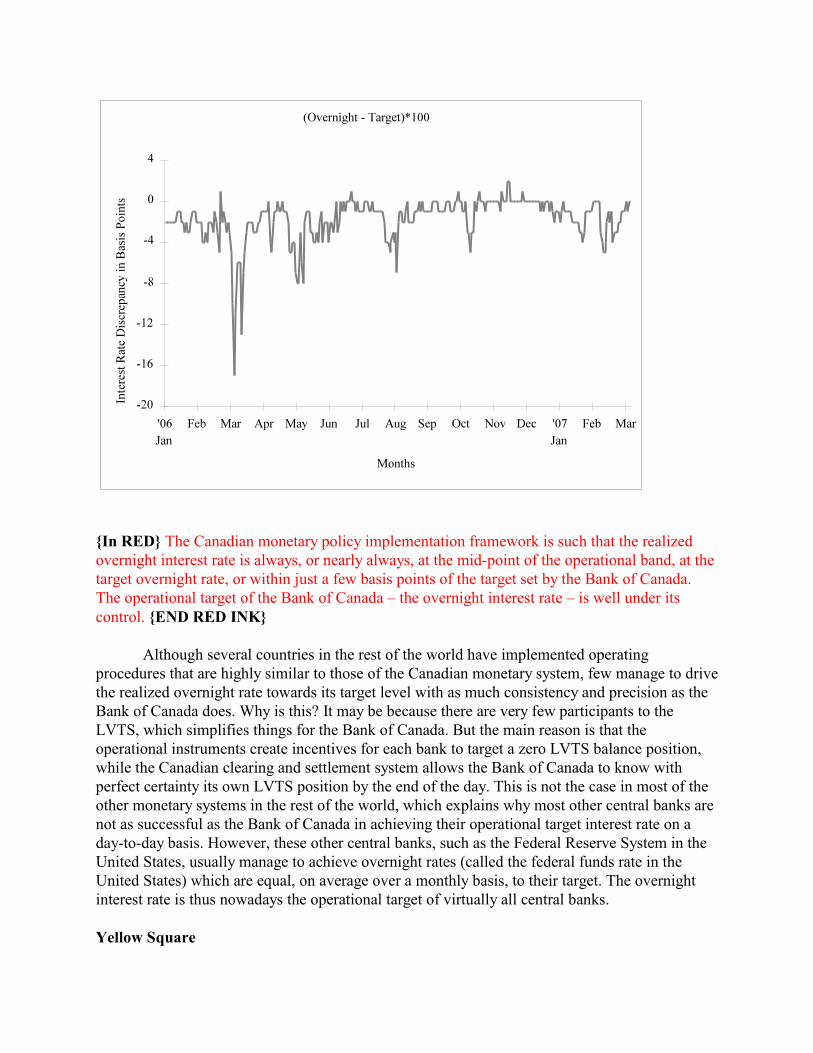

Figure 2 shows the evolution of the daily differences between the actual overnight rateand the target overnight rate since 2006, expressed in basis points. Obviously, except for a fewhiccups, the actual rate is equal, or nearly equal, to the target rate. On average, throughout 2006for instance, the actual rate was 2 basis points lower than the target rate (the discrepancy wasnegative on average).

Figure 2:The Actual Overnight Interest Rate Versus the Target Overnight Interest Rate in Canada, 2006-2007Source: Statistics Canada, series v39079 and v39050Note: Difference is in basis points (A 100 basis point difference equals an interest rate differenceof 1 percent: 4.30 percent versus 4.25 percent is 5 basis points)

{In RED} The Canadian monetary policy implementation framework is such that the realizedovernight interest rate is always, or nearly always, at the mid-point of the operational band, at thetarget overnight rate, or within just a few basis points of the target set by the Bank of Canada.The operational target of the Bank of Canada – the overnight interest rate – is well under itscontrol. {END RED INK}

Although several countries in the rest of the world have implemented operatingprocedures that are highly similar to those of the Canadian monetary system, few manage to drivethe realized overnight rate towards its target level with as much consistency and precision as theBank of Canada does. Why is this? It may be because there are very few participants to theLVTS, which simplifies things for the Bank of Canada. But the main reason is that theoperational instruments create incentives for each bank to target a zero LVTS balance position,while the Canadian clearing and settlement system allows the Bank of Canada to know withperfect certainty its own LVTS position by the end of the day. This is not the case in most of theother monetary systems in the rest of the world, which explains why most other central banks arenot as successful as the Bank of Canada in achieving their operational target interest rate on aday-to-day basis. However, these other central banks, such as the Federal Reserve System in theUnited States, usually manage to achieve overnight rates (called the federal funds rate in theUnited States) which are equal, on average over a monthly basis, to their target. The overnightinterest rate is thus nowadays the operational target of virtually all central banks.

Yellow Square

Government Deposit Shifting

As long as LVTS transactions only involve banks, and not the public sector, whenever a bank isin a deficit position, i.e., whenever it has negative LVTS balances, there is another bank, or agroup of other banks, that has an identical surplus position, i.e., positive LVTS balances, asdescribed by Table 1. In other words, under the above condition, the net overall amount of LVTSbalances held by banks – the sum of positive and negative LVTS balances of each bank – is zeroat all times.

Things are entirely different when payment transactions involve the federal governmentor the central bank. This will be the case when the federal government pays its employees, whenit collects taxes, when the Bank of Canada purchases or sells foreign currencies on foreignexchange markets on behalf of government, when it provides banks with currency, or when itundertakes transactions in government securities with banks or dealers. In all these instances, onebank may be in a LVTS deficit position without any other bank being in a surplus position; orone bank may be in a LVTS surplus position, with none of the other banks being in a deficitposition. In this case, the net overall amount of LVTS balances held by banks – the amount ofsettlement balances as they are called at the Bank of Canada – will be different from zero.Sidebar: Settlement balances are the net aggregate amount of LVTS balances held by banks, that is thesum of positive and negative LVTS balances of each bank.

Why do monetary transactions involving the federal government or the central bankdisrupt the symmetric behaviour of positive and negative LVTS balances? To examine thepeculiarity of federal government transactions, let us suppose that we are around the end of April,when taxpayers are sending in their tax returns with their tax payment. Take the example of awealthy taxpayer who has to send in an additional $60,000 in federal tax, assuming that it goesthrough the LVTS. Table 3 summarizes what happens in the payment system.

Table 3The Impact of Federal Government Collecting Tax Revenues on Intraday Changes inBalance Sheets

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTSbalances-$60,000

Deposits oftaxpayer-$60,000

Balances of BMO$-60,000

Deposits ofCanadiangovernment+$60,000

Balances ofBofC$+60,000

LVTSbalances+$60,000

We assume here that the wealthy taxpayer is a customer of the Bank of Montreal. TheBank of Canada is the fiscal agent of the Canadian government; in other words the Bank ofCanada handles the payments of the federal government. When the taxpayer orders the Bank ofMontreal to make the $60,000 payment, the account of the federal government at the Bank of

Canada gets credited with $60,000 while the LVTS balances of the Bank of Montreal getdiminished by $60,000. The net aggregate amount of LVTS balances held by banks thusdiminishes. Payments to the federal government thus constitute a drain on settlement balances. Ifnothing else occurs, the Bank of Montreal will be looking in vain for a counterparty in its effortsto borrow funds in the overnight market since no bank has compensatory positive LVTSbalances. This will tend to push the overnight rate above the target overnight rate, towards theBank rate, since some banks, here the Bank of Montreal, will be forced to borrow from the Bankof Canada at the Bank rate. The target overnight rate would not be achieved.

What can the Bank of Canada do to avoid such a situation? The Bank of Canada mustpursue neutralizing operations that will neutralize the impact of government transactions onsettlement balances. In other words, the Bank of Canada will take measures to bring back to zerothe amount of settlement balances. The actions taken to modify settlement balances are describedas settlement-balance management, or in short cash setting.

SIDEBAR:Cash setting, or settlement-balance management, is the action that the Bank of Canada takes tobring back the supply of settlement balances to their desired level, usually zero. Cash setting isusually carried by shifting government deposits between the central bank and banks.

In the present case, the Bank of Canada shifts Canadian government deposits back to thebanks. Suppose that it does so, with $60,000 worth of government deposits being shifted to thegovernment account at the Bank of Montreal, as shown in Table 4. In reality the deposits areauctioned off, with the banks offering the highest rate getting the government deposits. Supposethat in this case, the Bank of Montreal acquires $60,000 worth of LVTS balances when theauction is completed. Adding Tables 3 and 4, we obtain Table 5, which shows that the system isback to a situation with a zero amount of settlement balances. The payment flows have beenentirely neutralized.

Table 4The Impact of a Shift of Government Deposits into Banks on Intraday Changes in BalanceSheets

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTSbalances+$60,000

Deposits ofgovernment +$60,000

Balances of BMO$+60,000

Deposits ofCanadiangovernment-$60,000

Balances ofBofC$-60,000

LVTSbalances-$60,000

Table 5The Neutralizing Impact of a shift of Government Deposits into Banks Following a Federal

Government Revenue Inflow

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTSbalances$0

Deposits oftaxpayer - $60,000

Balances of BMO$0

Deposits ofCanadiangovernment$0

Deposits ofgovernment +$60,000

Balances ofBofC$0

LVTSbalances$0

The process is quite similar when banks need additional banknotes issued by the Bank ofCanada – so they can feed their automatic teller machines and respond to the demand of theircustomers who wish to hold and make use of more banknotes. Withdrawals of banknotes fromthe central bank are made as needed by the banks. In other words, whenever the demand forbanknotes rises, more banknotes are being supplied by the Bank of Canada. Banks receive thebanknotes and are debited with negative LVTS balances. These are then neutralized at the end ofthe day by shifting the appropriate amount of government deposits from the central bank to thebanks.

We may now examine, more quickly, what happens when the federal government makesa payment, for instance when it pays for the report of a private-sector economist on the futurecompetitiveness of the Canadian economy. This time the bank winds up with positive LVTSbalances as a result of the government payment, as shown in Table 6. If the public sector and thebank of Canada engaged in no further transactions, the Bank of Montreal would be forced todeposit its LVTS balances at the Bank of Canada, and the actual overnight rate would tend to falltowards the rate on deposits at the central bank. To stop this, the Bank of Canada must bring theamount of settlement balances back to zero. Once again, it will do so by shifting the deposits ofthe federal government, but this time from its accounts at banks towards its account at the centralbank, as shown in Table 7. As a result, as can be seen in Table 8 (which adds Tables 6 and 7),2

the federal government payment transaction is neutralized, with the net amount of settlementbalances in the system being brought back to zero. In all likelihood, the actual overnight rate willbe close to the target.

Footnote 2: In reality, the Bank of Canada will auction an amount of government deposits that issmaller than the amount maturing on that day (and hence returning to the government account atthe Bank of Canada, formally called the Receiver General balances).

Table 6The Impact of Federal Government Expenditures on Intraday Changes in Balance Sheets

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTS Deposits of Balances of Deposits of

balances+$60,000

economist+$60,000

BMO$+60,000

Canadiangovernment-$60,000

Balances ofBofC$-60,000

LVTSbalances-$60,000

Table 7The Impact of Shifting Government Deposits from Banks to the Central Bank on IntradayChanges in Balance Sheets

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTSbalances-$60,000

Deposits ofgovernment -$60,000

Balances of BMO-$60,000

Deposits ofCanadiangovernment+$60,000

Balances ofBofC+$60,000

LVTSbalances+$60,000

Table 8The Neutralizing impact of a Shift of Government Deposits into the Account at the CentralBank Following a Federal Government Expenditure Outflow

Bank of Montreal (BMO) LVTS Bank of Canada (BofC)Assets Liabilities Assets Liabilities Assets LiabilitiesLVTSbalances$0

Deposits ofeconomist + $60,000

Balances of BMO$0

Deposits ofCanadiangovernment$0

Deposits ofgovernment -$60,000

Balances ofBofC$0

LVTSbalances$0

{In RED} When the federal government receives a payment (taxes), the banking system as awhole is put in a negative settlement balance position; when the federal government makes apayment (expenditures), the banking system as a whole is put in a positive settlement balanceposition.

To neutralize the effects of financial payments received by the federal government, theBank of Canada shifts government deposits from the central bank to banks; to neutralize the

effects of financial payments made by the federal government, the Bank of Canada shiftsgovernment deposits from banks to the central bank. {END of RED}

The Bank of Canada transfers government deposits twice a day. It does so first in theearly morning, when most of the bank payments through the LVTS are made. It does it again latein the afternoon, after all bank payments involving the federal government have been made.When this second adjustment is being carried, the Bank of Canada knows with certainty howmuch settlement balances there are in the system. The Bank of Canada is thus able to calculatethe exact amount of government deposits that need to be shifted to achieve a zero amount of netsettlement balances, as occurred in our examples of Tables 5 and 8. Unless there are someunusual circumstances, the amount of government deposits being auctioned will be such that theamount of settlement balances is indeed zero by the end of the day. In other words, the Bank ofCanada normally targets a zero amount of settlement balances.

{IN RED} Under normal circumstances, the net amount of settlement balances in the system iszero at the end of the day. The amounts of positive LVTS balances held by some banks areexactly equal to the amounts of negative LVTS balances held by the other banks. {END of RED}

Thus, despite the existence of government payment transactions, the situation by the endof the day is exactly the one that was described in Chapter 12, in Table 11. Thus any bank with anet debit LVTS position that needs to borrow funds to settle its position is aware that there is atleast one other bank with an offsetting net credit LVTS position, which is a potential lender ofLVTS balances. These banks will meet on the overnight market and the rate of interest on whichthey will agree to borrow or lend will be the overnight interest rate. All bank payments involvinga client come to a close at 6:00 pm, with banks being given an additional half hour to interact onelast time on the overnight market, lending their remaining positive balances or borrowing fromother banks when they are in a debit LVTS position. Hence each individual bank is able to bringits LVTS balances to zero, thus avoiding having to take overnight advances from the central bankat the Bank rate or avoiding depositing its positive LVTS balances for the night at the Bank ofCanada, as was described in the example of Table 13 of Chapter 12.

It follows that, whatever the size of GDP or the size of daily transactions, under normalcircumstances, bank deposits at the Bank of Canada are zero or very close to zero, whileadvances by the Bank of Canada are also zero or next to zero. This can be verified with a look atFigures 3 and 4, which show the evolution of overnight bank deposits at the central bank andovernight advances taken by banks at the Bank of Canada. The magnitude of these deposits andadvances, a few dozen million dollars on average with a few spikes in the hundreds of millions,is dwarfed by the size of daily transactions through the LVTS – more than $165 billions, and thesize of monetary aggregates such as M2 – over $750 billions! These few dozen millions arepeanuts when measured by the scale of the Canadian monetary system, and hence can beconsidered as being virtually equal to zero. Actually, to “grease” the wheels of the paymentsystem, the Bank of Canada purposefully targets an amount of $25 million in positive settlementbalances as of 2007. A banking officer that lets this amount as an overnight deposit at the Bankof Canada, instead of lending it in the interbank market, foregoes about $175 in interest!

Figure 3:

Bank Deposits at the Bank of CanadaSource: Statistics Canada, series v36629, weekly series

Figure 4:Bank of Canada Advances to BanksSource: Statistics Canada, series v36634, weekly series

What would be abnormal or unusual circumstances? A well-known instance occurredwhen the World Trade Centre in the financial centre of New York was subjected to two airplaneattacks on September 11, 2001. The Bank of Canada, along with other central banks, made itclear that it would alleviate any fear of financial disruption by providing the monetary systemwith the additional liquidity that was being demanded by the banks and other financialinstitutions. For more than a week, the Bank of Canada set settlement balances at levels ofseveral hundreds of million dollars. This was done with appropriate government deposit shiftingactions. These settlement balances were then gradually brought back to zero. Technical factorshave also forced occasionally the Bank of Canada to set settlement balances at negative levels in2006 and 2007.

In other words, the Canadian monetary system is such that the overall demand forsettlement balances is usually zero, so that the Bank of Canada sets the supply of settlementbalances to zero in normal circumstances. In the case of 9/11, there was a temporary largedemand for settlement balances, which induced the Bank of Canada to set the supply ofsettlement balances much above zero, equal to this overall demand, so as to keep the overnightinterest rate on target. In addition, we have already pointed out that currency is provided to thebanks on demand. Thus, if we designate the sum of currency and bank deposits at the centralbank by the term base money, we can say that there is a horizontal supply of base money, at thetarget overnight interest rate. Whenever the demand for base money increases, so does the supplyof base money. This is illustrated in Figure 5, under the standard assumption that the demand forbase money is downward sloping (the interest rate being a measure of the opportunity cost ofholding coins or banknotes – the higher the interest rate, the less base money one wishes to hold).

0 0 1 1If there is a shift in the demand for base money, from D D to D D , the supply of base moneywill accommodate at the target overnight interest rate.

Sidebar: Base money is made up of two components of the liability side of the balance sheet of the centralbank: currency and deposits at the central bank (which used to be called bank reserves).

Figure 5The Demand for and the Supply of Base Money

BoxThe Evolution of the Canadian Monetary System

The Canadian monetary system that we describe in this chapter is relatively new. It was fullyimplemented only in February 1999, when the Large Value Transfer System became operational. As pointed out in Chapter 12, page 238, prior to 1994, Canadian banks were under a legalrequirement to hold deposits at the Bank of Canada that were not remunerated, called reserves.

These reserves had to be a certain percentage of the deposits held by the public in banks.Reserves had a dual role: in theory they provided banks with the means to face a bank run; inpractice they were said to help the control of monetary aggregates.

Discussions on the possibility of implementing Canadian monetary policy with highlyreduced reserves and even no reserves at all started in September 1987. A first step towards thisprocess was implemented in 1991, when restrictions on the frequency and size of Bank ofCanada advances to banks (with the appropriate collateral) were lifted. Compulsory reserverequirements were also progressively phased out over a three year period, until they werecompletely eliminated in mid-1994. The focus of monetary policy moved away from theTreasury bill rate – the interest rate on short-term (mainly 90-day) government securities –towards the overnight rate. The 50 basis points operating band for the overnight rate of Figure 1was put in place in 1994, and in 1996 the Bank rate was disconnected from the Treasury bill rate,and set instead at the upper end of the operating band, to provide more clarity as to the intentionsof the Bank.

A second round of discussions took place in 1995, when the present system, dealing withelectronic large-value payments, was designed. As noted above, the LVTS was implemented in1999. An official target overnight rate was put in place, as the rate to be found at the midpoint ofthe operating band, thus completing the corridor system that had been started in 1994. Andfinally, in late 2000, the Bank of Canada moved to a system whereby possible changes in thetarget overnight rate are announced at eight annual preset dates, the so-called fixedannouncement dates.

Nearly identical corridor systems with no reserve requirements exist in New Zealand,Australia, England and Sweden, but not yet in the United States or in the European MonetarySystem with its European Central Bank. {End of Box}