36

Back On Track Reforming rail franchising Nigel Keohane Nida Broughton

Back On Track Reforming rail franchising Nigel Keohane Nida Broughton

SOCIAL MARKET FOUNDATION

2

FIRST PUBLISHED BY The Social Market Foundation, January 2016 11 Tufton Street, London SW1P 3QB Copyright © The Social Market Foundation, 2016 The moral right of the author(s) has been asserted. All rights reserved. Without limiting the rights under copyright reserved above, no part of this publication may be reproduced, stored or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording, or otherwise), without the prior written permission of both the copyright owner and the publisher of this book. THE SOCIAL MARKET FOUNDATION

The Foundation’s main activity is to commission and publish original papers by independent academic and other experts on key topics in the economic and social fields, with a view to stimulating public discussion on the performance of markets and the social framework within which they operate. The Foundation is a registered charity and a company limited by guarantee. It is independent of any political party or group and is funded predominantly through sponsorship of research and public policy debates. The views expressed in this publication are those of the author, and these do not necessarily reflect the views of the sponsors or the Social Market Foundation.

BACK ON TRACK

3

CONTENTS

ABOUT THE AUTHORS .................................... 4

EXECUTIVE SUMMARY ................................... 5

CHAPTER 1 – THE CASE FOR REFORMING RAIL

FRANCHISING ............................................... 9

CHAPTER 2 – REFORMING RAIL

FRANCHISING ............................................. 20

SOCIAL MARKET FOUNDATION

4

ABOUT THE AUTHORS NIGEL KEOHANE Nigel oversees the Social Market Foundation’s research programme as research director and leads the work on public service reform and commissioning, welfare reform and low pay, and pensions and savings. Prior to the SMF, Nigel was head of research at the New Local Government Network think tank, worked in local government and taught history at Queen Mary, University of London. He has a BA and MA in history from Exeter University, and a PhD in political history from Queen Mary. NIDA BROUGHTON Nida joined the Social Market Foundation in May 2012 from the House of Commons, where she was working as an economic adviser to parliamentary committees. Prior to that she worked as an economist at Ofcom, the regulator and competition authority for communications markets. At the Social Market Foundation, Nida is chief economist and leads work on economics and statistics, and has published papers on the public finances, entrepreneurship, skills and housing.

BACK ON TRACK

5

EXECUTIVE SUMMARY Rail transport is hugely important to the social fabric and economic success of the UK, with 1.65 billion passenger journeys made by train between spring 2014 and spring 2015.1 Delivering the best value for money on rail is therefore vitally important for consumers and businesses. As this report shows, there are significant failures in the current rail system – both in terms of its efficiency and in terms of responsiveness to passenger needs. Turning blindly to nationalisation is not the answer. The future rail service requires significant investment, which is better determined by the market than by the shorter-term horizons of politicians and governments. It also needs to benefit fully from the huge technological opportunities that lie ahead – such as smart ticketing and the move to digital traffic management on the tracks. These are best maximised in a market structure that enables and encourages innovation. Looking back to nationalisation would also ignore the significant benefits derived from rail franchising, including huge expansion in the number of passenger journeys and an upward trend in quality over recent decades. For these reasons, this report argues that we should look to radical reform of how we franchise rail services to deliver a more efficient and passenger-orientated system. Failings that need addressing Despite notable improvements in rail performance as well as huge increases in patronage in the last two decades, there remain significant areas where passengers and taxpayers are being let down. In the first place, the efficiency of UK rail lags considerably behind comparators in continental Europe. With fares constrained and fiscal pressure to contain taxpayer subsidy, tackling such inefficiencies has

SOCIAL MARKET FOUNDATION

6

never been more important. Past estimates put the efficiency gap between the UK and continental comparators as high as 40%. As it stands, operators have limited incentives and scope to innovate and to control costs or drive efficiencies because of the high level of specifications in contracts. Such specifications include timetabling, regulation of many fares and the types of improvements to be invested in. Second, despite some notable improvements in service quality in recent decades, customer satisfaction is now flagging on key measures and passengers are being failed on core aspects of the service.

o Levels of dissatisfaction are unacceptably high on several measures: a third of passengers are dissatisfied with ‘the value for money of the price of your ticket’, one in five are unhappy at the amount of room to sit and stand and three in ten are unhappy with how companies deal with delays.

o ‘Overall satisfaction’ has flat-lined and even dipped in recent years. The same is true for satisfaction with punctuality and reliability.

o Satisfaction scores vary markedly between TOCs and some operators are performing far below others.

Reforming rail franchising Chapter 2 argues that radical reforms to rail franchising are needed to ensure that efficiencies are unlocked and so that services are responsive to what passengers want. In particular, operators have too little flexibility and incentive during the life of the contract to encourage necessary quality improvements or cost reductions. To overcome this, the report recommends that:

o The Department for Transport should develop a single measure of overall satisfaction against which it would

BACK ON TRACK

7

score operators. Set this goal, companies would then have the flexibility and incentive to target the aspects of quality or cost of service that affect passenger satisfaction the most. For example, depending on passenger demands, some franchisees could choose to prioritise additional services, punctuality or more comfortable journeys.

o Satisfaction scores would be used to determine rewards

and penalties for train providers during the contract, and in particular to determine whether additional flexibility should be awarded to the train operating company.

o High-performing operators that over-achieved on their

targets would be awarded additional flexibility. Additional flexibilities could include the ability to vary fares as long as total fares remained the same or relaxation in specifications on timetabling. To keep these privileges, operators would have to continue to meet stretching satisfaction targets.

o Poor performing operators would by contrast have to pay

penalty charges for low overall satisfaction scores. Given the limited ability for train operating companies to raise fares, particularly due to price regulation, these penalties would reduce overall profitability.

o New measures should also be introduced to clamp down

on delays and on the failure to pay compensation to passengers. The total paid out by TOCs in compensation in 2014/15 was £25m. However, only one in ten of passengers claim compensation for delayed journeys. These figures suggest that some £1bn of compensation from operators will go unpaid over the course of parliament.

SOCIAL MARKET FOUNDATION

8

As it stands, passengers are often unaware of their rights to claim compensation and find the process too onerous, and operators benefit because of this. Instead, operators should be given a strong incentive to compensate delayed passengers by fining them to the value of all unclaimed compensation payments. This would encourage them to make the processes simpler and to boost take-up of compensation. The money raised by these fines should be distributed as additional reward payments to the operators that over-achieve on overall satisfaction targets.

o The House of Commons Transport Select Committee should institute an ‘Annual hearing into rail performance’. This would be an opportunity to regularly audit whether passenger services have improved over the last twelve months. As a rule, senior representatives from the operators that score worst on overall passenger satisfaction should expect to be called as witnesses. MPs are also likely to want to hear from the Department for Transport, Network Rail and Transport Focus.

BACK ON TRACK

9

CHAPTER 1 – THE CASE FOR REFORMING RAIL FRANCHISING This chapter describes the importance of rail services in the UK, why they require reform and why franchising remains the best way to proceed. There are significant failures currently. First, the efficiency of UK rail lags behind comparators in continental Europe. With continued fiscal pressures limiting government funding for rail, tackling such inefficiencies has never been more important. Second, despite some notable improvements in service quality in recent decades, customer satisfaction is now flagging on many measures and passengers are being failed on core aspects of the service.

Importance of rail Rail transport is a crucial enabler of a successful economy. It is also a principal driver of regional redistribution and helps to sustain rural and remote areas as attractive places to live and work. Delivering the best value for money on rail is therefore vitally important for consumers and businesses. Supporting a fairer deal for taxpayers and commuters, as well as continuing to invest in the railway network, was set out as a key commitment in the 2015 Conservative manifesto.”2

Successes of competition in rail and the franchise system The mid-1990s witnessed the privatisation of British Rail, a vertically integrated, nationally-owned company that operated both the track infrastructure and train services. The Railways Act of 1993 separated out management of the track, rolling stock, delivery of transport to consumers, and regulatory oversight. The aim of the Act was to help provide a source of long-term investment in rail enabling more modernisation, increasing cost efficiency and driving up quality.3 In

SOCIAL MARKET FOUNDATION

10

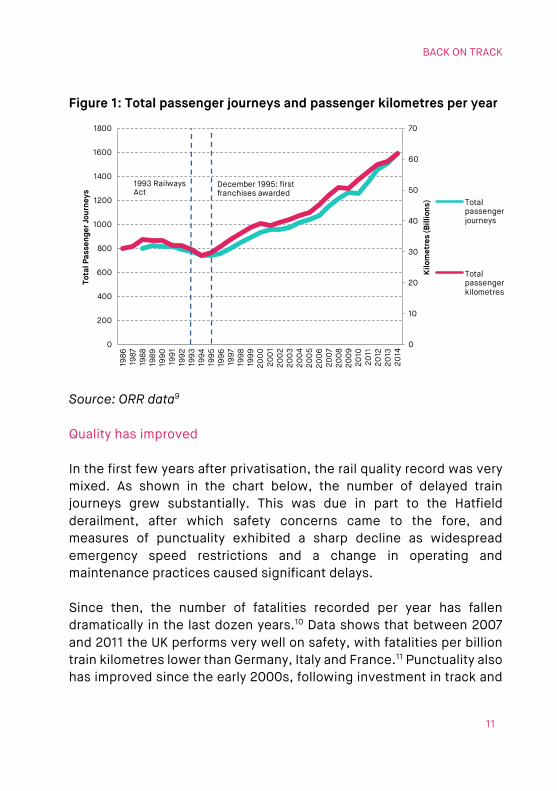

particular, using competitive franchising to deliver rail services via train operating companies (TOCs) was expected to promote efficiency, innovation and investment and reduce the public subsidy by injecting competitive pressure into the market. Across many dimensions, this has been realised, with rail transport seeing substantial improvement over past decades. Growth in passenger numbers Rail has become a more and more important part of the UK’s transport network. At the time of privatisation, many expected continued decline in traffic.4 However, in the mid-1990s, passenger numbers started to climb. The number of journeys taken by train in Britain has grown twice as fast as the growth in GDP, and has been greater than in other European countries.5 Large societal shifts and increased costs associated with car travel alongside lengthening journey times by road (due to congestion and tighter speed limits) and policies designed to discourage car use in favour of more sustainable travel modes, may have induced some road users to travel more by train.6 However, it is notable that increases in passenger numbers occurred alongside privatisation, The separation of infrastructure provider and train operator, together with the competitive pressures imposed by franchising, has provided incentives for operators to focus on passenger needs and preferences, which have led to improvements in rail services in terms of reliability and capacity.7 As many as 345 million additional rail journeys in 2013 have been attributed to the change in the industry model.8 Although exact attribution remains difficult, it is clear that rail has become an even more important part of the economic and social fabric of British life. Patronage is expected to double again by 2030.

BACK ON TRACK

11

Figure 1: Total passenger journeys and passenger kilometres per year

Source: ORR data9 Quality has improved

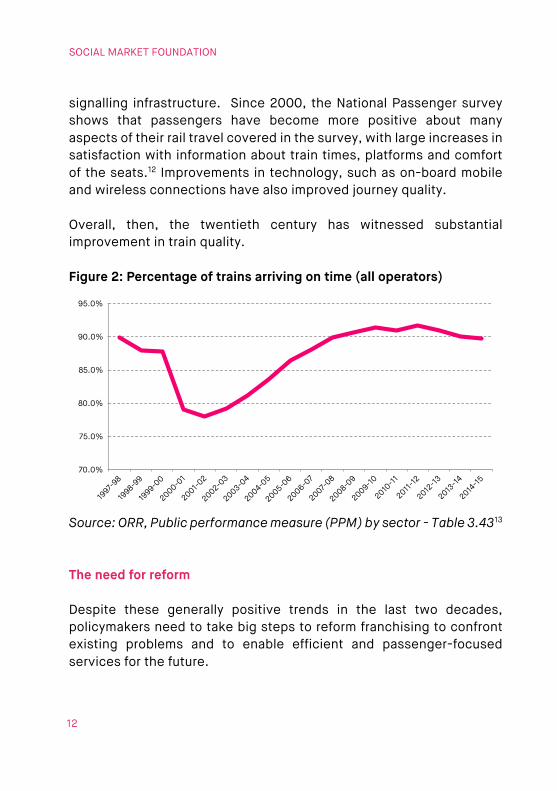

In the first few years after privatisation, the rail quality record was very mixed. As shown in the chart below, the number of delayed train journeys grew substantially. This was due in part to the Hatfield derailment, after which safety concerns came to the fore, and measures of punctuality exhibited a sharp decline as widespread emergency speed restrictions and a change in operating and maintenance practices caused significant delays. Since then, the number of fatalities recorded per year has fallen dramatically in the last dozen years.10 Data shows that between 2007 and 2011 the UK performs very well on safety, with fatalities per billion train kilometres lower than Germany, Italy and France.11 Punctuality also has improved since the early 2000s, following investment in track and

0

10

20

30

40

50

60

70

0

200

400

600

800

1000

1200

1400

1600

180019

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

00

200

120

02

200

320

04

200

520

06

200

720

08

200

920

1020

1120

1220

1320

14

Tota

l Pas

seng

er Jo

urne

ys

Total passenger journeys

Total passenger kilometres

Kilo

met

res

(Bill

ions

)

1993 Railways Act

December 1995: first franchises awarded

SOCIAL MARKET FOUNDATION

12

signalling infrastructure. Since 2000, the National Passenger survey shows that passengers have become more positive about many aspects of their rail travel covered in the survey, with large increases in satisfaction with information about train times, platforms and comfort of the seats.12 Improvements in technology, such as on-board mobile and wireless connections have also improved journey quality. Overall, then, the twentieth century has witnessed substantial improvement in train quality. Figure 2: Percentage of trains arriving on time (all operators)

Source: ORR, Public performance measure (PPM) by sector - Table 3.4313

The need for reform Despite these generally positive trends in the last two decades, policymakers need to take big steps to reform franchising to confront existing problems and to enable efficient and passenger-focused services for the future.

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

BACK ON TRACK

13

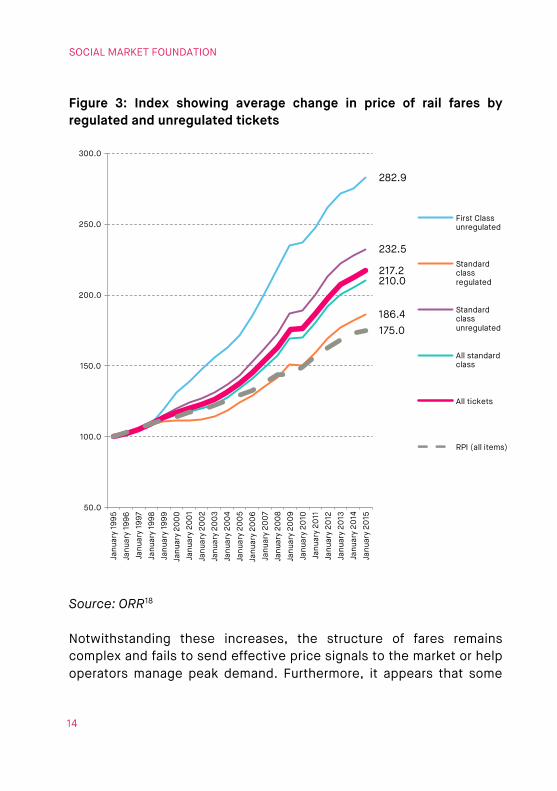

Inefficiencies In the first place, UK rail exhibits much inefficiency. With fares constrained and fiscal pressure to contain taxpayer subsidy, these economic faults must be confronted. Total industry costs have risen significantly since privatisation, and continue to exhibit upward pressure.14 Against the background of a 57% increase in passengers, it might be expected that unit costs would fall, particularly given that the industry has relatively high fixed costs. However, unit costs have remained constant in real terms since 1997.15 The McNulty Review estimated an efficiency gap of as much as 40% between the UK and continental comparators.16 International comparisons suggest that other European countries have obtained significant costs reductions from the competitive tendering of train operations. Making exact comparisons is difficult – the UK may have made different choices in the trade-off between cost and quality and between costs and coverage – but UK rail must find ways to innovate and cut out inefficiencies. Areas that may contribute include: increasing train utilisation, introducing new technologies, improving staff productivity in the passenger sector to match that in the freight sector, better utilisation of the infrastructure and more efficient procurement of rolling stock.17 Therefore, for both the sake of passengers who want to see good value for the fares they pay and for taxpayers who wish to see good value from the subsidies put into the rail system, inefficiencies must be driven out. Overall train fares have experienced above inflation growth, especially in the period 2003 to 2008. Because of this growth, the Government is committed to no real terms increases in fares during the parliament.

SOCIAL MARKET FOUNDATION

14

Figure 3: Index showing average change in price of rail fares by regulated and unregulated tickets

Source: ORR18 Notwithstanding these increases, the structure of fares remains complex and fails to send effective price signals to the market or help operators manage peak demand. Furthermore, it appears that some

282.9

186.4

232.5

210.0217.2

175.0

50.0

100.0

150.0

200.0

250.0

300.0

Janu

ary

1995

Janu

ary

1996

Janu

ary

1997

Janu

ary

1998

Janu

ary

1999

Janu

ary

200

0Ja

nuar

y 20

01

Janu

ary

200

2Ja

nuar

y 20

03

Janu

ary

200

4Ja

nuar

y 20

05

Janu

ary

200

6Ja

nuar

y 20

07

Janu

ary

200

8Ja

nuar

y 20

09

Janu

ary

2010

Janu

ary

2011

Janu

ary

2012

Janu

ary

2013

Janu

ary

2014

Janu

ary

2015

First Class unregulated

Standard class regulated

Standard class unregulated

All standard class

All tickets

RPI (all items)

BACK ON TRACK

15

fares are set below the level which passengers would be prepared to pay.19

Insufficient responsiveness to passengers

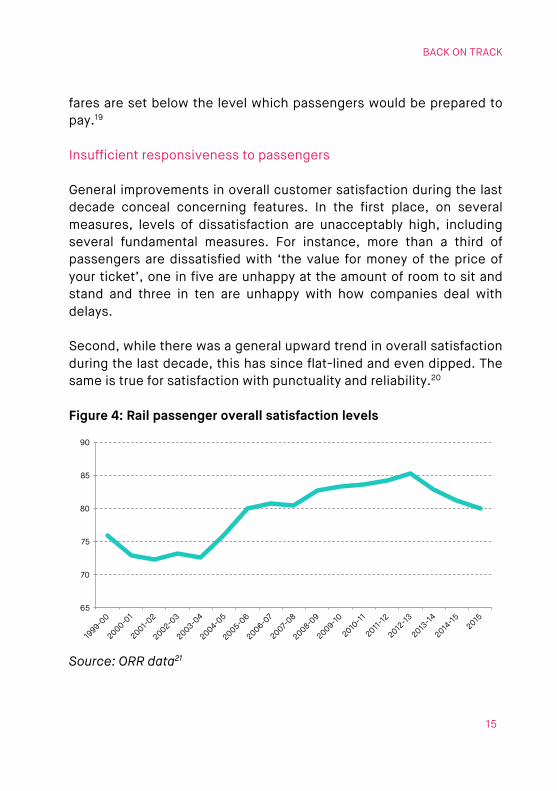

General improvements in overall customer satisfaction during the last decade conceal concerning features. In the first place, on several measures, levels of dissatisfaction are unacceptably high, including several fundamental measures. For instance, more than a third of passengers are dissatisfied with ‘the value for money of the price of your ticket’, one in five are unhappy at the amount of room to sit and stand and three in ten are unhappy with how companies deal with delays. Second, while there was a general upward trend in overall satisfaction during the last decade, this has since flat-lined and even dipped. The same is true for satisfaction with punctuality and reliability.20 Figure 4: Rail passenger overall satisfaction levels

Source: ORR data21

65

70

75

80

85

90

SOCIAL MARKET FOUNDATION

16

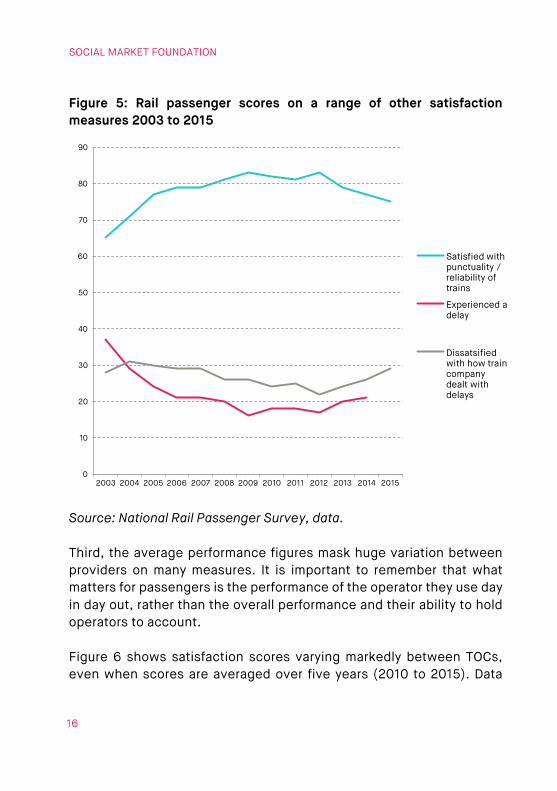

Figure 5: Rail passenger scores on a range of other satisfaction measures 2003 to 2015

Source: National Rail Passenger Survey, data. Third, the average performance figures mask huge variation between providers on many measures. It is important to remember that what matters for passengers is the performance of the operator they use day in day out, rather than the overall performance and their ability to hold operators to account. Figure 6 shows satisfaction scores varying markedly between TOCs, even when scores are averaged over five years (2010 to 2015). Data

0

10

20

30

40

50

60

70

80

90

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Satisfied with punctuality / reliability of trains

Experienced a delay

Dissatsified with how train company dealt with delays

BACK ON TRACK

17

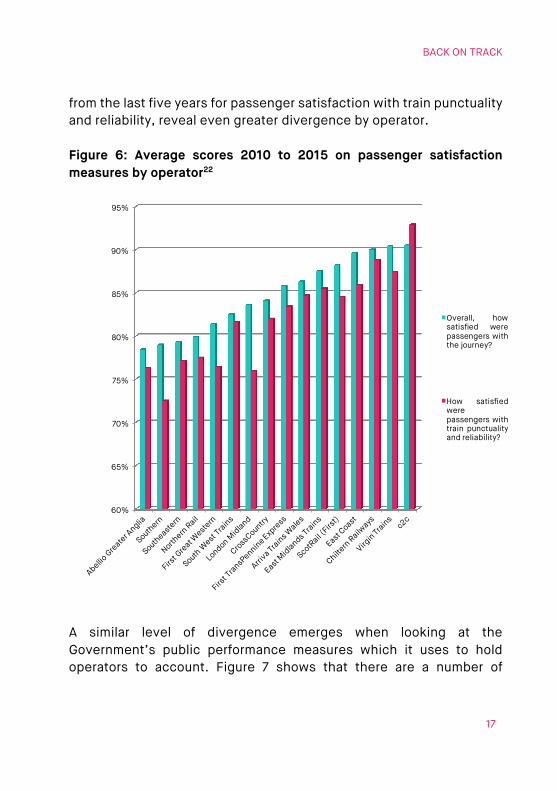

from the last five years for passenger satisfaction with train punctuality and reliability, reveal even greater divergence by operator. Figure 6: Average scores 2010 to 2015 on passenger satisfaction measures by operator22

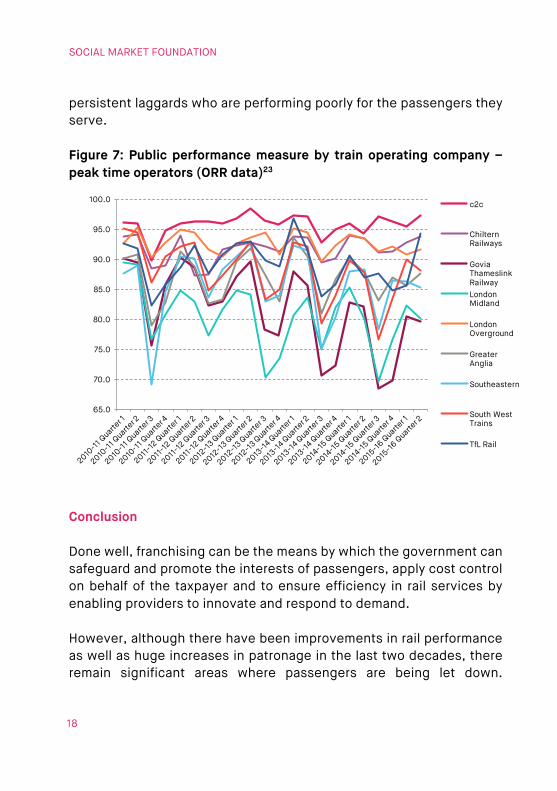

A similar level of divergence emerges when looking at the Government’s public performance measures which it uses to hold operators to account. Figure 7 shows that there are a number of

60%

65%

70%

75%

80%

85%

90%

95%

Overall, howsatisfied werepassengers withthe journey?

How satisfiedwerepassengers withtrain punctualityand reliability?

SOCIAL MARKET FOUNDATION

18

persistent laggards who are performing poorly for the passengers they serve. Figure 7: Public performance measure by train operating company – peak time operators (ORR data)23

Conclusion Done well, franchising can be the means by which the government can safeguard and promote the interests of passengers, apply cost control on behalf of the taxpayer and to ensure efficiency in rail services by enabling providers to innovate and respond to demand. However, although there have been improvements in rail performance as well as huge increases in patronage in the last two decades, there remain significant areas where passengers are being let down.

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0 c2c

Chiltern Railways

Govia Thameslink RailwayLondon Midland

London Overground

Greater Anglia

Southeastern

South West Trains

TfL Rail

BACK ON TRACK

19

Inefficiencies must be unlocked and quality improved – and operators must be freed and incentivised to respond to passenger demand. The hand of passengers must also be strengthened to hold operators to account. The second part of the report describes in more detail how we should seek to reform franchising so that it puts the needs of passengers first. How can we give operators the freedom and incentives to innovate to achieve better outcomes for rail passengers?

SOCIAL MARKET FOUNDATION

20

CHAPTER 2 – REFORMING RAIL FRANCHISING Chapter 1 set out the main problems facing the market for passenger trains. They include a lack of progress on efficiency, insufficient emphasis on consumer needs, and a lack of focus on long-term investment and incentives. How can these problems be resolved? The case for rail franchising A competitive market should – in theory – resolve problems described in Chapter 1. When working well, competition forces companies to improve the services they offer and provide better value for money to attract and retain customers. Decisions are driven by consumer demands, and trade-offs, for example between quality and cost, are driven by what consumers value most. However, in some markets, such as for trains, the potential for this type of competition is limited. It would be highly costly to have a system of competing track and train across the entire network. We therefore have a system whereby – in general – we do not have competing track providers. Instead, access to track is regulated. Limited track reduces the number of competing train providers that can be supported, which means that across much of the network, the right to run trains is franchised out. This results in a model whereby there is competition among bidders for the market, with minimal competition in the market. There are some lines where it is feasible for more than one train operator to run services. Around 1% of passenger services are run by what are known as “open access operators”.24 These direct competitors, or open access operators, use the same track as an existing franchisee to provide passenger services. A recent Competition and Markets Authority study25 has examined the potential for expanding this model, and other options for sharing track that enable additional competition between train providers. In practice,

BACK ON TRACK

21

however, the underlying economics of many routes mean that open access will not be able to provide substantial competitive pressure. Where franchising needs reform and why With limited scope for increasing competition to improve value for money for passengers, we need instead improve the franchising process itself. The lack of direct competition during the contract period means that it is crucial to create within-contract regulations and incentives to deliver value for money for passengers. However, at the moment, these incentives are relativity muted. To overcome the inefficiencies and poor quality measures described in Chapter 1, we need to sharpen these incentives and ensuring there is sufficient flexibility for operators to provide what passengers want. Lack of ability to respond to consumer demand Franchise contracts currently specify a number of details in relation to performance and level of service. Over-specification can limit franchisees’ ability and incentive to deliver better services. Recently, the Government has said it wants to increase flexibility on contracts. However, it still mandates standards of reliability and punctuality that must be achieved; and franchise contracts include service quality commitments in a range of areas, Examples include details of the number of specific services that need to be provided according to a defined timetable, and include commitments such as introducing a specific number of additional carriages, ensuring that bicycles can be transported, and undertaking specific improvement or capacity enhancing work.26 In addition to this, around 45% of fares are regulated in line with inflation.27 These cover commuter fares and the majority of long-distance, off-peak fares.28 These regulated fares can change throughout a franchise period, although changes need to be funded by

SOCIAL MARKET FOUNDATION

22

the Treasury. Currently, Government has committed to maintaining a real terms fares freeze until 2020. In the past, the cap has applied to the total value of regulated fares, which means that train operators could increase some fares by more and some fares by less than this amount. However, in the 2015 Conservative manifesto, it was announced that “train operating companies will not have any flexibility to raise prices”.29 This high level of specification reduces the ability of train companies to react to changing conditions and changing passenger demand. It limits the amount of new innovation that companies can introduce and limits the ability of train companies to make best use of existing capacity, exacerbating overcrowding.30 Varying fares across the rush hour could reduce congestion at the busiest times. For instance, one study has suggested that if the Government focused more on regulating the total fares, and allowing peak fares to rise relative to other fares, this could reduce average peak demand by at least 5% over a five year period, thus reducing investment requirements and saving money.31 Lack of incentive to respond to consumer demand Train operating companies’ lack of ability to improve efficiency and value for money is arguably matched by a lack of incentive, as train companies are insulated from potential risks and rewards. In many previous franchises, Government insulated train operating companies against the risks that are perceived to be outside their control. This includes the performance of the economy, which affects passenger numbers. The insulation worked by providing additional Government support if revenues fell beneath a certain level, in return for a share of revenues if revenues grew above a certain threshold. However, this weakens incentives for train operating companies to attract more passengers. This problem is particularly pertinent to the

BACK ON TRACK

23

UK, where one reason why the rail network lags behind in terms of efficiency is because of the lower level of capacity utilisation.32 The rationale for such risk-sharing is that GDP is an “exogenous” risk outside train companies’ control, which can have a significant effect on passenger demand. Whilst this is true, this is of course the case for many businesses. What is different for rail is that franchise agreements prevent train operating companies from fully adjusting to changes in the economic environment and passenger demand, for example, by changing services.33 If franchise contracts allowed for more flexibility, then train operators would be able to take on more exogenous risk, because they would be better placed to manage and adapt to this risk. The Government’s policy of awarding shorter franchise terms than previously, with initial terms of 7-10 years,34 also reduces the risk of economic growth turning out to be substantially different from forecast. Evidence shows that contracts that limit the amount of risk being taken on whilst including a high degree of specification are not conducive to innovation and efficiency. One study looking at train operating companies in the 2000s found that those placed on management-style contracts oversaw a substantial deterioration in efficiency compared to operators not on such contracts, increasing overall costs. Costs only reduced again once contracts were retendered.35 Such management contracts are only used as a short-term measure, for example, while a new franchise award is being organised, and so are not typical of most franchise contracts. But the study does illustrate that giving train operating companies the ability and incentive to innovate and reduce costs can make a substantial difference to efficiency. How can we provide greater ability and incentive to respond to consumers? To tackle these problems, and focus train providers on delivering greater value for money for passengers, we need to give them the

SOCIAL MARKET FOUNDATION

24

ability and incentive to do so. Currently, franchise contracts specify a range of measures, all designed to capture some aspect of quality of service. This could be simplified by using a single measure such as overall satisfaction. The advantage of doing this would be that train operating companies would have the flexibility to target the aspects of quality of service that affect passenger satisfaction the most. This would reflect what would happen in a competitive market, where, in competing for market share, companies must respond to consumer demands, and decisions are driven by the relative weights consumers place on different aspects of price and quality. The drivers of passenger satisfaction are likely to differ across different franchises. For example, minimising delays is likely to be especially important on commuter-heavy lines and routes that connect to transport hubs such as airports. Comfort and facilities are likely to be of greater importance on routes where most journeys are long-distance. These drivers will also change over time as patterns in travel change. Data on these specific drivers would still need to be collected so that train operating companies could respond adequately, but using a single measure should ensure that companies are able to flexibly change what they do over time to better meet customer needs. For example, depending on passenger demands, some franchisees could choose to prioritise additional services, better punctuality or improving the comfort of journey. Overall, such an approach should lead to greater value for money and greater responsiveness to passengers. In this section, we explore what a simple satisfaction-based framework would look like in practice. We firstly set out how satisfaction targets in contracts could be used, through rewarding firms that do well with additional flexibility, and penalising those that do not. We then discuss what level of flexibility should be provided, and finally discuss additional safeguards to focus train operating companies on delivering value for money.

BACK ON TRACK

25

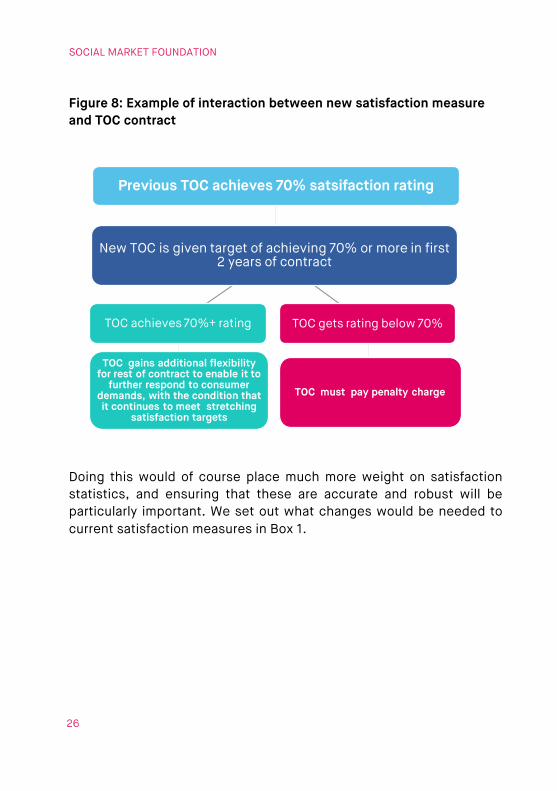

Reward firms that perform well and penalise ones that do not Satisfaction figures would be used to determine rewards and penalties for train providers within contract, and in particular to determine whether additional flexibility should be awarded to the train operating company. Contracts could initially be written to similar levels of specification as currently, but with clauses to reward train operating companies for achieving the same or higher satisfaction levels. For example, new franchise contracts could involve a reward for achieving higher passenger satisfaction than its predecessor line operator part of the way through its contract. By contrast, train operating companies that are not able to hit targets would be penalised. Given the limited ability for train operating companies to raise fares, particularly due to price regulation, these penalties would reduce overall profitability. The reward would be in the form of additional flexibility and freedom from quality and price regulation, subject to satisfaction targets continuing to be met. The aim would be to encourage high performing train providers to take up the option of additional flexibility to help them respond further to consumer demands. Introducing additional flexibility during the contract period rather than at the start could have two key advantages. Firstly, it would make the initial bidding process easier to manage; one difficulty with outcome-based franchise contracts is that it may be harder to compare bids. Granting additional flexibility over time means that the initial contract can be granted on an agreed set of terms. Secondly, it would mean that flexibility is only granted once a TOC has proven itself able to deliver high quality. An example is set out overleaf.

SOCIAL MARKET FOUNDATION

26

Figure 8: Example of interaction between new satisfaction measure and TOC contract

Doing this would of course place much more weight on satisfaction statistics, and ensuring that these are accurate and robust will be particularly important. We set out what changes would be needed to current satisfaction measures in Box 1.

New TOC is given target of achieving 70% or more in first 2 years of contract

Previous TOC achieves 70% satsifaction rating

TOC gets rating below 70%

TOC must pay penalty charge

TOC achieves 70%+ rating

TOC gains additional flexibility for rest of contract to enable it to

further respond to consumer demands, with the condition that it continues to meet stretching

satisfaction targets

BACK ON TRACK

27

Box 1: Measuring satisfaction To ensure that train operators are sufficiently focused on the needs of passengers, whilst stripping out over-specification in contracts, survey data on passenger satisfaction will have to be robust and timely. One of the most important aspects of outcome-based commissioning is the choice of measure. In the case of rail, an obvious measure to use would be passenger satisfaction, as measured by the National Rail Passenger Survey. The specific question is “Overall, how satisfied were passengers with the journey?”. The advantage of this measure is that it is already widely used to measure performance across the rail network and so is widely understood. It is also sufficiently broad to capture a wide definition of quality of service. Other alternatives that could be considered include “Would you recommend the service to a friend or family?”, which is similar to that used to gather patient feedback for the NHS.

However, it would also need to be augmented in the following ways:

1. Robustness: the survey would most likely need to be conducted more regularly than is currently the case (twice a year), so that statistics are timelier. If more weight is placed on this measure, it would also need to sample more passengers: currently the sample sizes for most franchises is 1000-2000 passengers.

2. Factors outside train companies’ control: Some drivers

of satisfaction will be outside the franchisee’s control. For example, franchisees have varying degrees of

SOCIAL MARKET FOUNDATION

28

How much flexibility should be provided? Flexibility would come in the form of removing quality specifications. A further step would be to go beyond stripping out detailed quality specification from contracts, and reduce the extent to which pricing is regulated. Pricing flexibility can help train operating companies better manage demand so as to make most use of existing capacity, as set out

control over the quality of, and facilities available at certain stations. The survey should ideally isolate the drivers of satisfaction that are largely within train companies’ control. In practice, this may mean that the survey has be slightly adapted on a franchise by franchise basis.

3. Inclusion of potential passengers: The main flaw with using a survey based on passengers is that it misses out a group of potential passengers who do not use rail because it does not adequately serve their needs. In fact, this is arguably already a group whose views are missed out under the current system. It is difficult to define who should be included in this group of “potential passengers”. In principle, it should include anyone who may consider rail as a potential travel option. In practice, the simplest approach may be to conduct a general population survey that asks respondents:

• Whether they could use rail for their travel needs; • If they could use rail for their travel needs, but choose

not to do so, what are the reasons for choosing not to travel by rail.

BACK ON TRACK

29

earlier. This could introduce some complexity into the market, but, over time, the development of better connectivity, smart ticketing and consumer-friendly mobile applications could mitigate this. As set out earlier, flexibility in pricing has been restricted, in the main due to concerns about the ability of train companies to raise fares at particular times to very high levels. This may be a legitimate concern if there are particular time slots where passengers are unable to easily switch to alternative times or different transport modes, for example, due to job requirements.36 High prices on commuter routes may be of particular concern, given the potential effect on the wider job market. High prices on these routes are likely to be especially problematic in work areas where housing supply is limited, thereby forcing workers to live further away. In part, greater flexibility in working hours could help commuters vary their working patterns. The last Government introduced a legal right for all employees to request flexible working.37 This is a positive step. Technological developments, such as better mobile and broadband connectivity could also help workers to vary their start and finish times more flexibly. The level of flexibility provided will need to vary by route, and should depend on the margin by which the train operator exceeds its target, and also the level of competition faced by the operator. Where there is competition on routes, flexibility is likely to be particularly useful in helping train operators respond to and compete with these alternative modes of transport. Any potential risk to passengers of providing more flexibility would be reduced due to the competitive pressure: if train operating companies on these routes cannot provide value for money, they will experience a loss in passenger revenues. Greater flexibility should therefore be allowed on these routes. Competition could come from a range of sources. Firstly, competition could come from other transport modes, such as flights, car or bus and coach travel. Long-distance rail is likely to be in competition with

SOCIAL MARKET FOUNDATION

30

domestic airline competition.38 Shorter distance rail is likely to see more competition from the road network.39 Secondly, competition could come from open access operators, although as we set out earlier, the scope for additional competition of this type may be limited. Additional safeguards Compensation and fines As well as being penalised and rewarded based on overall satisfaction levels, train companies should also be held to account by passengers. A direct way for this to occur is for passengers to have easy recourse to claim compensation when trains are late or cancelled and it should be a rule that all passengers who face delays or cancellations are reimbursed fully. Current evidence suggests that this happens all too rarely at the moment. Journeys delayed by 30 minutes or more reflect 6% of all journeys. However, many operators are poor at recompensing the passengers they have failed. In 2015, the largest decline in passenger satisfaction concerned how well train companies dealt with delays (-4 per cent).40 As with other satisfaction measures, there is huge variation between different operators with the best (East Coast, First TransPennine Express and Virgin) seeing six in ten satisfied, whilst the worst (Abellio Greater Anglia, Govia Thameslink, Southeastern and Southern) seeing fewer than 3 in 10 satisfied.41 Research from both the ORR and Transport Focus has shown that passengers in general have low awareness of their rights to claim compensation and how to go about claiming recompense. Nine in ten of those eligible to claim compensation did not claim compensation for the last delay of 30 minutes or more that they experienced.42 This low level of redress means that the value of unclaimed and unpaid compensation is colossal. The total paid out by TOCs in compensation

BACK ON TRACK

31

in 2014/15 was £25m.43 This suggests that passengers are missing out on approximately £225m per year in compensation claims and that some £1bn will go unclaimed from train companies over the course of this parliament. This is bad for individual passengers – who are paying more than they should for poorly-performing rail services and who get no recompense for the inconveniences and costs that come with delays. It is also bad for the rail system overall because operators do not feel the financial pain that should accompany delays and cancellations. The principal reasons given by passengers for not claiming are that they did not even consider it (44%) or believed they were not eligible for recompense (30%). This stems from the lack of profile that compensation is given by operators and the fact that it is not in their interests to be proactive and innovative in terms of how refunds are publicised, claimed and paid. Firms have a clear incentive not to be proactive in such regards. While some operators are experimenting with new compensation channels – such as automatic compensation for delayed trains where the tickets are pre-booked electronically – the overall performance record is lamentable.44 Therefore, claiming needs to be made easier and awareness needs to be raised. In this regard, the move to online claims is to be welcomed as are the Government’s ideas for making the claims and payment process easier.45 The Government hopes that compensation can be paid direct back to customers’ bank accounts or to their travel cards and for a ‘pay as you delay’ scheme, which would see passengers automatically reimbursed for any delays or cancellations. Passenger journeys would be tracked through use of smart travelcards so that companies could identify affected passengers and then transfer refunds electronically to their bank accounts or travelcards. Passengers would be refunded for each minute of delay.46 This is ambitious. However, it is likely to take considerable time to introduce

SOCIAL MARKET FOUNDATION

32

across the network and firms may show little proactive-ness in introducing such schemes, experimenting or ensuring their success. Therefore, more immediate and additional steps should be taken to encourage firms to compensate passengers that are owed refunds. The simplest way to achieve this would be for the Department of Transport to give operators a strong incentive to compensate delayed passengers by fining them to the value of all unclaimed compensation payments. Firms charged high fines under this scheme would have to publicise the fact on their websites and should be named and shamed by the Department of Transport. These steps would give operators a clear incentive to publicise compensation schemes and to make claims and payments as simple as possible through new innovative channels. The money raised by these fines should be distributed by the Department for Transport as additional reward payments to the operators that over-achieve on overall satisfaction. Annual hearing into rail performance The House of Commons Transport Select Committee has carried out important scrutiny of rail passenger services and put forward significant policy recommendations.47 Parliamentary scrutiny can be an important device for accountability and addressing shortfalls in services.48 As a means of increasing accountability on rail performance we recommend that the House of Commons Transport Select Committee should institute an ‘Annual hearing into rail performance’. This would be an opportunity to regularly audit whether passenger services have improved over the last twelve months. As a rule, senior representatives from the operators that score worst on overall passenger satisfaction should expect to be called as witnesses. MPs are also likely to want to

BACK ON TRACK

33

hear from the Department for Transport, Network Rail and Transport Focus. Conclusion Franchise contracts need to be reformed to give train operators greater incentive and ability to provide good value for money. Increasing the flexibility of contracts will mean that operators are better able to do this. We propose:

• Moving towards targeting satisfaction rather than detailed quality specifications.

• Rewarding train operators that perform well on satisfaction measures with additional flexibility.

• Penalising train operators that perform poorly on satisfaction measures with charges.

• Fine train operators the value of all unclaimed compensation payments for delays and cancellations.

• The House of Commons Transport Select Committee should institute an ‘Annual hearing into rail performance’ at which senior representatives from the operators that score worst on overall passenger satisfaction should expect to be called as witnesses.

SOCIAL MARKET FOUNDATION

34

ENDNOTES 1 ORR, Passenger Rail Usage 2014-15 Quarter 4 Statistical Release 2 The Conservative party manifesto 2015, April 2015 3Andrew Bowman, “An illusion of success: the consequences of British rail privatisation, Accounting Forum, Volume 39, Issue 1, March 2015 4Speech by Patrick McLoughlin, Department for Transport, “Rail growth through competition: the success of the UK model”, 2013 5 OXERA (2014) What is the contribution of rail to the UK economy?http://www.oxera.com/getmedia/802a4979-8371-4063-ad24-8a81ed6c8f82/Contribution-of-rail-to-the-UK-economy-140714.pdf.aspx?ext=.pdf 6 Societal changes included increases in female economic activity, migration and numbers of people living alone. Costs of car travel included parking fees, insurance and fuel costs. Increases in fuel costs may account for around a third of the growth in rail patronage - Scott Le Vine, Peter Jones 2012 On the Move: Making sense of car and train travel trends in Britain: http://www.theitc.org.uk/docs/47.pdf 7 These were significant enough to have had an impact at an aggregate level - http://orr.gov.uk/__data/assets/pdf_file/0008/6002/otm-rail-demand-forecasting.pdf ; In London, for example, there have been large investments in the Underground and Overground networks. Underground train mileage increased by 8% (in the context of a fixed network); and National Rail train mileage (London and South East, from 2003) grew by 20%. Transport for London (TfL) reports that at the same time key indicators of service quality have improved, with many indicators of service performance now at ‘best ever’ levels - Scott Le Vine, Peter Jones 2012 On the Move: Making sense of car and train travel trends in Britain: http://www.theitc.org.uk/docs/47.pdf 8 OXERA (2014) What is the contribution of rail to the UK economy?http://www.oxera.com/getmedia/802a4979-8371-4063-ad24-8a81ed6c8f82/Contribution-of-rail-to-the-UK-economy-140714.pdf.aspx?ext=.pdf 9ORR datasets – stats folder 10 See ORR statistics. Key statistics - Passenger safety (p) - Table 5.18. https://dataportal.orr.gov.uk/displayreport/report/html/0a65eb3d-34fc-430f-9d01-4cc429feb0bd 11 UKTI, The UK Rail Industry: A Showcase of Excellence (2014) 12 Matthew Keep, Railway performance and subsidy statistics - Commons Library Standard Note 02199 (2013) http://www.parliament.uk/business/publications/research/briefing-papers/SN02199/railway-performance-and-subsidy-statistics 13 http://dataportal.orr.gov.uk/displayreport/report/html/4cdbe8cc-dc97-4a8e-ae6e-a7fcd5bd268c 14 see Booz & Co – Cost of Railway Outputs, prepared for McNulty (2011) Rail Value For Money Study: http://orr.gov.uk/__data/assets/pdf_file/0009/1710/rail-vfm-summary-report-may11.pdf 15 McNulty (2011) Rail Value For Money Study: http://orr.gov.uk/__data/assets/pdf_file/0009/1710/rail-vfm-summary-report-may11.pdf

BACK ON TRACK

35

16 McNulty, Realising the potential of GB rail – report of the Rail Value For Money Study (2011) 17 McNulty (2011) Rail Value For Money Study: http://orr.gov.uk/__data/assets/pdf_file/0009/1710/rail-vfm-summary-report-may11.pdf; As reported by Passenger Focus in 2009; http://www.publications.parliament.uk/pa/cm201213/cmselect/cmtran/329/329.pdf 18 https://dataportal.orr.gov.uk/displayreport/report/html/920430f4-6a8d-4bb8-9762-2bf89259e346 19 McNulty (2011) Rail Value For Money Study: http://orr.gov.uk/__data/assets/pdf_file/0009/1710/rail-vfm-summary-report-may11.pdf 20 Fiona Preston and Peter Jones, National Rail Passenger Survey Data Analysis On the Move – Supporting Paper 3 (December 2012) 21 https://dataportal.orr.gov.uk/displayreport/report/html/3a49cd46-4de3-472a-b129-e91ff6512d40. Note the source is the Autumn survey except for 2015 where it is the spring survey. 22 Note, Govia Thameslink was not included as there were only 12 months of data. http://data.transportfocus.org.uk/train/nps/question/service-overall/; http://data.transportfocus.org.uk/train/nps/question/service-punctuality/ 23 https://dataportal.orr.gov.uk/displayreport/report/html/3ae82838-402a-4562-b84c-d0f6008a02e0 24 http://orr.gov.uk/__data/assets/pdf_file/0018/1791/open-access-consultation-june-2013.pdf 25 Competition and Markets Authority, Passenger Rail services competition policy project https://www.gov.uk/cma-cases/passenger-rail-services-competition-policy-project 26 See, for example https://www.gov.uk/government/publications/chiltern-railways ; file:///C:/Users/Nida/Downloads/SN01343%20(6).pdf 27 file:///C:/Users/Nida/Downloads/sn01904.pdf 28 https://www.gov.uk/government/policies/expanding-and-improving-the-rail-network 29 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/249001/fares-ticketing-next-steps.pdf 30http://www.publications.parliament.uk/pa/ld201415/ldselect/ldeconaf/134/134.pdf 31 DfT, Rail Fares and Ticketing Review: Initial consultation (2012) 32 ORR Realising the potential of GB Rail 33 Brown review https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/49453/cm-8526.pdf 34 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/211639/brown-government-response.pdf 35 http://www.idep.eco.usi.ch/paper-smith-171421.pdf 36 McNulty Review 37 https://www.gov.uk/flexible-working/overview 38 For example, it has been argued that strong domestic airline competition has reduced growth in long-distance rail https://www.openstarts.units.it/dspace/bitstream/10077/5923/1/White_ET33.pdf

SOCIAL MARKET FOUNDATION

36

39 http://www.networkrail.co.uk/browse%20documents/rus%20documents/route%20utilisation%20strategies/east%20coast%20main%20line/east%20coast%20main%20line%20rus.pdf 40 Transport Focus, National Rail Passenger Survey, Spring 2015 Main Report (2015) 41 Transport Focus, National Rail Passenger Survey, Spring 2015 Main Report (2015). 42 Transport Focus, Understanding rail passengers – delays and compensation (2013) 43 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/455184/toc-compensation-2009-2015.pdf 44 https://www.virgintrains.co.uk/delayrepay/automatic; http://www.independent.co.uk/news/uk/home-news/train-delays-to-trigger-automatic-refunds-but-virgin-trains-attach-strings-to-the-pledge-a6677711.html 45 http://www.telegraph.co.uk/news/uknews/road-and-rail-transport/11808635/Rail-minister-pledges-instant-refunds-for-rail-delays.html 46 http://www.dailymail.co.uk/news/article-2988885/Passengers-cash-train-two-minutes-late-Government-forces-operators-sign-pay-delay-scheme.html 47 House of Commons Transport Select Committee, Investing in the railway (2015), Security on the railway (2014), Rail 2020 (2012) 48 Institute for Government, Select Committees under scrutiny: The impact of parliamentary committee inquiries on government (2015)