REGULATING GOLD MURABAHAH IN ISLAMIC BANKING Associate Professor Rifki Ismal 5 th International Conference on Islamic Banking and Finance: Risk Management, Regulation and Supervision Islamic Research and Training Institute (IRTI) Islamic Development Bank (IDB) Jordan, 6-8 October 2012 1

Transcript

REGULATING GOLD MURABAHAH IN

ISLAMIC BANKING

Associate Professor Rifki Ismal

5th International Conference on Islamic Banking and Finance:

Risk Management, Regulation and Supervision

Islamic Research and Training Institute (IRTI)

Islamic Development Bank (IDB)

Jordan, 6-8 October 2012

1

2

BACKGROUND: GOLD MURABAHAH

• Gold Murabahah endorsed by DSN is a Murabahah contract

which allows Islamic banks to finance gold trading with a

deferred payment basis.

• In fact, gold Murabahah is a new trend because of: (i) the

world gold price hike, (ii) a liquid asset & tradable in the

market and, (iii) protection wealth from inflation.

• Nevertheless, it may face market risk, liquidity risk, credit

risk, default risk and reputation risk due to market fluctuation

and cause losses to investors. It then affects the

performance of Islamic banks.

• The paper attempts to analyze: (a) the behavior of gold

prices as the most determinant factor for investors to

purchase gold including gold Murabahah and the behavior of

gold investors in purchasing or selling their gold Murabahah.

At the end, it proposes some recommendations to regulate

gold Murabahah contract in the Islamic banking industry.

3

UNDERLYING THEORY

• Expected price of gold and probability of occurrence.

Investors want to know the future price of gold, probability of

occurrence, the behavior of gold prices, and the time to

purchase gold.

• The transactions of gold Murabahah involves on the spot

price of purchasing gold and expected price of gold due to

the volatility gold prices in the market.

E(Vt) = the expected price of gold in the certain period;

rt+1 = the probability of occurrence of the gold price;

Vt = the price of gold in the next period.

The probability of occurrence is determined by constructing

intervals and locating prices in the intervals based on certain

division

ttt VrVE 1)(

4

UNDERLYING THEORY

• In an observed period, the highest price of gold is b and the

lowest one is a. Then, the difference between the highest and

the lowest price of gold or (x) is divided into four intervals of

gold prices.

a b

Interval 1 Interval 2 Interval 3 Interval 4

X

Interval 1:

41

xay

Interval 2:

242

xay

xa

Interval 3:

4

3

23

xay

xa

Interval 4:

4

34

xay

• the probability of occurrence of a gold price in certain interval

is a basis to compute expected price of gold in a certain

period. The formulas of the probability of occurrence per

interval and expected price of gold are written as:

5

UNDERLYING THEORY

4

1

11 t

ty

yr

14

1

11)( V

y

yVE

t

t

Probability of interval 1: Expected price:

Probability of interval 2:

4

1

22 t

ty

yr

Expected price: 24

1

22 )( V

y

yVE

t

t

Probability of interval 3:

4

1

33 t

ty

yr

Expected price:34

1

33 )( V

y

yVE

t

t

Probability of interval 4:

4

1

44 t

ty

yr Expected price:

44

1

44 )( V

y

yVE

t

t

• the risk of gold price volatility is a variance

between actual price of gold and expected price of

gold multiplied by the probability of occurrence.

1)( tttt EVVrVar

V

y

yV

y

yVar

t

t

tt

t

tt 4

1

1

4

1

)(or

EARLY TERMINATION & SIMULATION

• the early termination risk is a risk happening prior to the

maturity date of gold Murabahah contract.

• If Pt = payment price of gold Murabahah, P0 = initial price of

gold, r = Murabahah margin, It = installment of gold

Murabahah, D = down payment, t = tenor of Murabahah, then

0rPPt

T

t

tt

t

DPI

1

• Early termination occurs if (Pt+1) > (Pt).

• Simulation of the maximum limit of gold Murabahah contract:

maximum gold Murabahah financing of Rp250 million and

Rp150 million per debtor.

n

n

np

MN

1

0

0

1

MpNn

n

n

Max or

ntntt npnpnpnpM ...332211

Max early

termination

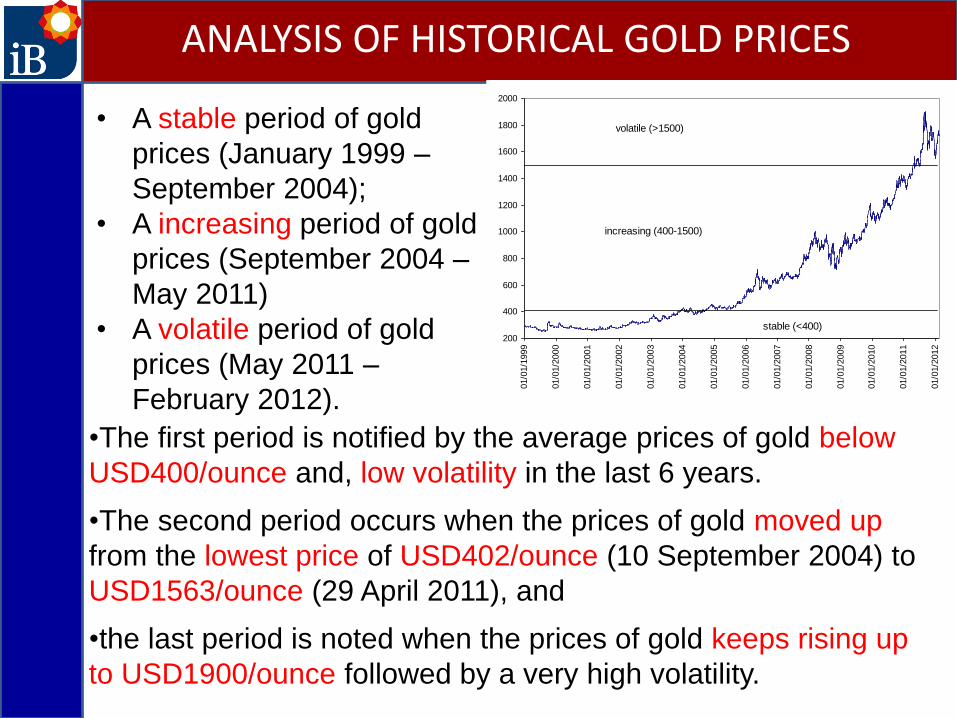

ANALYSIS OF HISTORICAL GOLD PRICES

• A stable period of gold

prices (January 1999 –

September 2004);

• A increasing period of gold

prices (September 2004 –

May 2011)

• A volatile period of gold

prices (May 2011 –

February 2012).

200

400

600

800

1000

1200

1400

1600

1800

2000

01/0

1/1

999

01/0

1/2

000

01/0

1/2

001

01/0

1/2

002

01/0

1/2

003

01/0

1/2

004

01/0

1/2

005

01/0

1/2

006

01/0

1/2

007

01/0

1/2

008

01/0

1/2

009

01/0

1/2

010

01/0

1/2

011

01/0

1/2

012

stable (<400)

increasing (400-1500)

volatile (>1500)

•The first period is notified by the average prices of gold below

USD400/ounce and, low volatility in the last 6 years.

•The second period occurs when the prices of gold moved up

from the lowest price of USD402/ounce (10 September 2004) to

USD1563/ounce (29 April 2011), and

•the last period is noted when the prices of gold keeps rising up

to USD1900/ounce followed by a very high volatility.

ANALYSIS OF PROBABILITY OF OCCURENCE

Stable Prob of Occurrence Increasing Prob of Occurrence Volatile Prob of Occurrence

< 296 0.53 < 693 0.44 < 1591 0.25

296 - 339 0.19 693 - 983 0.30 1591 - 1694 0.34

339 - 383 0.13 983 - 1273 0.16 1694 - 1797 0.32

> 383 0.15 > 1273 0.10 > 1797 0.09

Price Interval Harga and Probability per Period

•in the stable period, the highest probability of occurrence (53%)

was in the prices were below USD296/ounce.

•in the increasing period, (i) when the prices were less than

USD693/ounce (44%), and (ii) if the prices were USD693/ounce

– USD983/ounce (30%).

•in the volatile period, when the prices of gold were between (i)

USD1591/ounce – USD1694/ounce (34%); (ii) USD1694/ounce

– USD1797/ounce (32%) and, (iii) less than USD1591/ounce

(25%).

FINDINGS

•When the prices of gold are stable, the next prices tend to

decrease or stand in the lower position than the existing

one.

•Hence, from the investors (gold Murabahah investors)

point of view, investing funds in gold, when the price is

stable, will not be really profitable.

•When the prices of gold are increasing, the next prices

will go up (maximally 10.78%) or will moderately go down.

•Lastly, when the prices of gold are volatile in the high

position, the next prices will inflate modestly with the

maximum inflation of 3.35%.

ANALYSIS OF THE EXPECTED PRICE OF GOLD

250

270

290

310

330

350

370

390

410

430

01/0

1/1

999

05/0

2/1

999

12/0

3/1

999

16/0

4/1

999

21/0

5/1

999

25/0

6/1

999

30/0

7/1

999

03/0

9/1

999

08/1

0/1

999

12/1

1/1

999

17/1

2/1

999

21/0

1/2

000

25/0

2/2

000

31/0

3/2

000

05/0

5/2

000

09/0

6/2

000

14/0

7/2

000

18/0

8/2

000

22/0

9/2

000

27/1

0/2

000

01/1

2/2

000

05/0

1/2

001

09/0

2/2

001

16/0

3/2

001

20/0

4/2

001

25/0

5/2

001

29/0

6/2

001

03/0

8/2

001

07/0

9/2

001

12/1

0/2

001

16/1

1/2

001

21/1

2/2

001

25/0

1/2

002

01/0

3/2

002

05/0

4/2

002

10/0

5/2

002

14/0

6/2

002

19/0

7/2

002

23/0

8/2

002

27/0

9/2

002

01/1

1/2

002

06/1

2/2

002

10/0

1/2

003

14/0

2/2

003

21/0

3/2

003

25/0

4/2

003

30/0

5/2

003

04/0

7/2

003

08/0

8/2

003

12/0

9/2

003

17/1

0/2

003

21/1

1/2

003

26/1

2/2

003

30/0

1/2

004

05/0

3/2

004

09/0

4/2

004

14/0

5/2

004

18/0

6/2

004

23/0

7/2

004

27/0

8/2

004

40

60

80

100

120

140

160

Actual price (kiri)

Expected price (kanan)

350

550

750

950

1150

1350

1550

10/0

9/2

004

05/1

1/2

004

31/1

2/2

004

25/0

2/2

005

22/0

4/2

005

17/0

6/2

005

12/0

8/2

005

07/1

0/2

005

02/1

2/2

005

27/0

1/2

006

24/0

3/2

006

19/0

5/2

006

14/0

7/2

006

08/0

9/2

006

03/1

1/2

006

29/1

2/2

006

23/0

2/2

007

20/0

4/2

007

15/0

6/2

007

10/0

8/2

007

05/1

0/2

007

30/1

1/2

007

25/0

1/2

008

21/0

3/2

008

16/0

5/2

008

11/0

7/2

008

05/0

9/2

008

31/1

0/2

008

26/1

2/2

008

20/0

2/2

009

17/0

4/2

009

12/0

6/2

009

07/0

8/2

009

02/1

0/2

009

27/1

1/2

009

22/0

1/2

010

19/0

3/2

010

14/0

5/2

010

09/0

7/2

010

03/0

9/2

010

29/1

0/2

010

24/1

2/2

010

18/0

2/2

011

15/0

4/2

011

100

150

200

250

300

Actual price (kiri)

Expected price (kanan)

1450

1500

1550

1600

1650

1700

1750

1800

1850

1900

20/0

5/2

011

27/0

5/2

011

03/0

6/2

011

10/0

6/2

011

17/0

6/2

011

24/0

6/2

011

01/0

7/2

011

08/0

7/2

011

15/0

7/2

011

22/0

7/2

011

29/0

7/2

011

05/0

8/2

011

12/0

8/2

011

19/0

8/2

011

26/0

8/2

011

2-S

ep-1

19-S

ep-1

116-S

ep-1

123-S

ep-1

130-S

ep-1

17-O

ct-1

114-O

ct-1

121-O

ct-1

128-O

ct-1

14-N

ov-1

111-N

ov-1

118-N

ov-1

125-N

ov-1

12-D

ec-1

19-D

ec-1

116-D

ec-1

123-D

ec-1

130-D

ec-1

16-J

an-1

213-J

an-1

220-J

an-1

227-J

an-1

23-F

eb-1

210-F

eb-1

2

150

200

250

300

350

400

450

500

550

600

Actual price (kiri)

Expected price (kanan)

STABLE

PERIOD

INCREASING

PERIOD

VOLATILE

PERIOD

FINDINGS

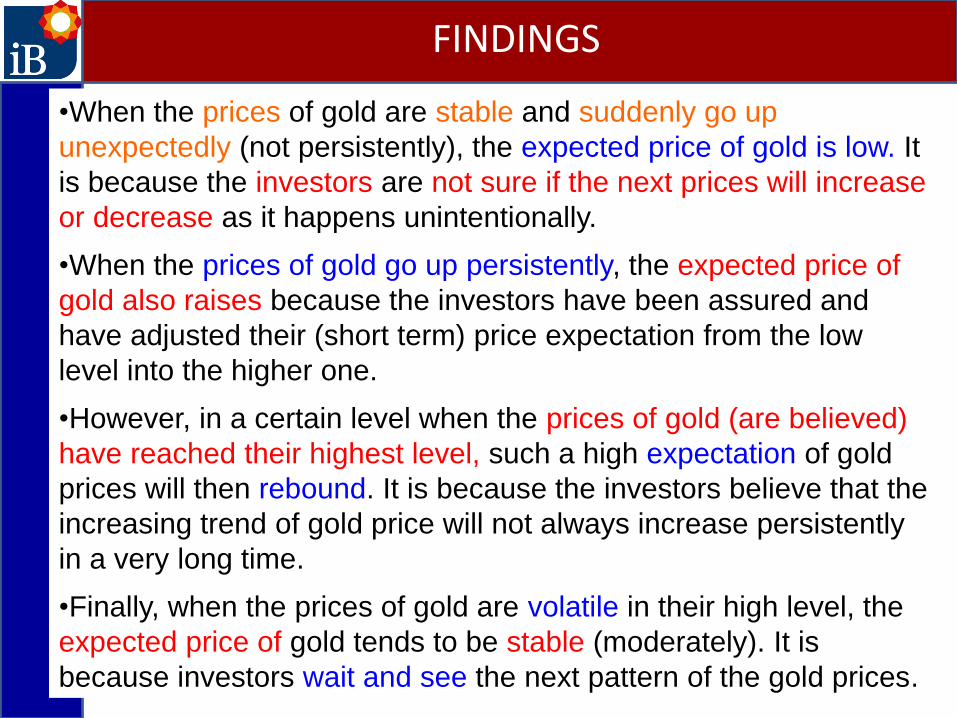

•When the prices of gold are stable and suddenly go up

unexpectedly (not persistently), the expected price of gold is low. It

is because the investors are not sure if the next prices will increase

or decrease as it happens unintentionally.

•When the prices of gold go up persistently, the expected price of

gold also raises because the investors have been assured and

have adjusted their (short term) price expectation from the low

level into the higher one.

•However, in a certain level when the prices of gold (are believed)

have reached their highest level, such a high expectation of gold

prices will then rebound. It is because the investors believe that the

increasing trend of gold price will not always increase persistently

in a very long time.

•Finally, when the prices of gold are volatile in their high level, the

expected price of gold tends to be stable (moderately). It is

because investors wait and see the next pattern of the gold prices.

ANALYSIS OF RISK OF PRICE FLUCTUATION

35

40

45

50

55

60

65

70

75

01/0

1/1

999

12/0

3/1

999

21/0

5/1

999

30/0

7/1

999

08/1

0/1

999

17/1

2/1

999

25/0

2/2

000

05/0

5/2

000

14/0

7/2

000

22/0

9/2

000

01/1

2/2

000

09/0

2/2

001

20/0

4/2

001

29/0

6/2

001

07/0

9/2

001

16/1

1/2

001

25/0

1/2

002

05/0

4/2

002

14/0

6/2

002

23/0

8/2

002

01/1

1/2

002

10/0

1/2

003

21/0

3/2

003

30/0

5/2

003

08/0

8/2

003

17/1

0/2

003

26/1

2/2

003

05/0

3/2

004

14/0

5/2

004

23/0

7/2

004

250

270

290

310

330

350

370

390

410

430

450

Variance (kiri)

Actual price (kanan)

Poly. (Variance (kiri))

90

110

130

150

170

190

210

10/0

9/2

004

19/1

1/2

004

28/0

1/2

005

08/0

4/2

005

17/0

6/2

005

26/0

8/2

005

04/1

1/2

005

13/0

1/2

006

24/0

3/2

006

02/0

6/2

006

11/0

8/2

006

20/1

0/2

006

29/1

2/2

006

09/0

3/2

007

18/0

5/2

007

27/0

7/2

007

05/1

0/2

007

14/1

2/2

007

22/0

2/2

008

02/0

5/2

008

11/0

7/2

008

19/0

9/2

008

28/1

1/2

008

06/0

2/2

009

17/0

4/2

009

26/0

6/2

009

04/0

9/2

009

13/1

1/2

009

22/0

1/2

010

02/0

4/2

010

11/0

6/2

010

20/0

8/2

010

29/1

0/2

010

07/0

1/2

011

18/0

3/2

011

350

550

750

950

1150

1350

1550

Variance (kiri)

Actual price (kanan)

Poly. (Variance (kiri))

140

190

240

290

340

390

20/0

5/2

011

03/0

6/2

011

17/0

6/2

011

01/0

7/2

011

15/0

7/2

011

29/0

7/2

011

12/0

8/2

011

26/0

8/2

011

9-S

ep-1

1

23-S

ep-1

1

7-O

ct-1

1

21-O

ct-1

1

4-N

ov-1

1

18-N

ov-1

1

2-D

ec-1

1

16-D

ec-1

1

30-D

ec-1

1

13-J

an-1

2

27-J

an-1

2

10-F

eb-1

2

1450

1500

1550

1600

1650

1700

1750

1800

1850

1900

1950

Variance (kiri)

Actual price (kanan)

Poly. (Variance (kiri))

STABLE

PERIOD

INCREASING

PERIOD

VOLATILE

PERIOD

FINDINGS

•When the prices of gold are stable, the risk of price

fluctuation remains very low. Even, the increasing of the

gold prices in the modest magnitude will not automatically

increase the risk of price fluctuation.

•However, when the prices of gold inflate persistently, the

risk of price fluctuation goes along such inflation.

•Nevertheless, the risk of price fluctuation will then go

down when such a persistent increase of gold prices has

been maximum (top of the threshold)

•The same as finding in the increasing trend of gold

prices, when the prices are volatile in the high level, the

risk of price fluctuation tend to be stable moderately.

ANALYSIS OF EARLY TERMINATION

0

2

4

6

8

10

12

May-0

1

Nov-0

1

May-0

2

Nov-0

2

May-0

3

Nov-0

3

May-0

4

Nov-0

4

May-0

5

Nov-0

5

May-0

6

Nov-0

6

May-0

7

Nov-0

7

May-0

8

Nov-0

8

May-0

9

Nov-0

9

May-1

0

Nov-1

0

30% Mark up, 1 Y tenor

20% Mark up, 1 Y tenor

Stable period

Increasing periodv

o

l

a

t

i

l

e

p

e

r

i

o

d

0

5

10

15

20

25

Oct-0

0

Apr-0

1

Oct-0

1

Apr-0

2

Oct-0

2

Apr-0

3

Oct-0

3

Apr-0

4

Oct-0

4

Apr-0

5

Oct-0

5

Apr-0

6

Oct-0

6

Apr-0

7

Oct-0

7

Apr-0

8

Oct-0

8

Apr-0

9

Oct-0

9

Apr-1

0

Oct-1

0

20% Mark up, 2 Y tenor

40% Mark up, 2 Y tenor

Stable period

Increasing periodv

o

l

a

t

i

l

e

p

e

r

i

o

d

•Down payment determines the share of investors’ funds to be invested in

gold Murabahah. If the gold Murabahah transactions need to be restricted,

down payment should be raised and vice versa.

•The high Murabahah margin could lower the probability of the investors to

terminate their gold Murabahah contract prior to its maturity date.

•The possibility to have a higher gold price than the current price is higher in

the increasing period of gold prices as indicated previously and in this gold

Murabahah termination assessment.

ANALYSIS OF EARLY TERMINATION

•The longer the tenor of gold Murabahah contract, the higher

the possibility for gold Murabahah investors to unilaterally end

the contract especially when the price of gold is in the

increasing trend.

•When the price of gold tends to go up, the banking regulator

can raise the margin of gold Murabahah or at least set it in an

appropriate level followed by shortening the tenor of gold

Murabahah contract.

•Such strategy may mitigate the frequency of gold Murabahah

termination because the possibility of the new gold price to

exceed its initial price is controlled by Murabahah margin.

•In addition, the advantage of doing termination is minimized by

the short term tenor of gold Murabahah

MAXIMUM TRANSACTION PER PERSON

•The assessment informs that the lesser the maximum amount of gold

Murabahah transaction per investor, the lesser the frequency of gold

Murabahah termination prior to its maturity date.

•Further, the combination of minimizing the limit of the maximum

amount of gold Murabahah per investor and the short tenor of gold

Murabahah contract may limit the frequency of early termination

compared to a higher limit of maximum amount of gold Murabahah

with a long tenor.

0

20

40

60

80

100

120

140

160

Jan-9

9

Jul-99

Jan-0

0

Jul-00

Jan-0

1

Jul-01

Jan-0

2

Jul-02

Jan-0

3

Jul-03

Jan-0

4

Jul-04

Jan-0

5

Jul-05

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Total Number of Early

Termination

0

10

20

30

40

50

60

70

80

90

Jan-9

9

Jul-9

9

Jan-0

0

Jul-0

0

Jan-0

1

Jul-0

1

Jan-0

2

Jul-0

2

Jan-0

3

Jul-0

3

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Total Number of Early

Termination

RECOMMENDATIONS

•The regulation for gold Murabahah transaction should not

be fixed (permanent) but it needs to be reviewed regularly

based on the trend (pattern) of the gold prices.

•The regulation for gold Murabahah contract might be

different in the cases of stable, increasing and volatile

periods of gold prices.

•The key variables to manage gold Murabahah transactions

and mitigate risk of early termination are:

•margin of gold Murabahah contract as it determines the

possibility and frequency of terminating gold Murabahah

contract prior to its maturity date,

•tenor of gold Murabahah contract as it controls the

intention of investors to shortly end the gold

•down payment as it can manage the amount of gold

Murabahah, frequency of transactions and, unilateral

termination of gold Murabahah contract

Associate Prof. Dr. Rifki Ismal is both a

central banker and lecturer. He earned

bachelor degree in economics from University

of Indonesia, master in economics from

University of Michigan, ann arbor (USA) and

PhD in Islamic economics and Finance from Durham

University (England). An Associate Professor in Islamic

Banking and Finance is from the Australian Government