16

Regulatory issues raised by access upgrade investment: where we are in the UK debate Richard Budd Senior Regulatory, Economist, BT 16 September 2008 [email protected]

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 217 times |

| Download: | 0 times |

Regulatory issues raised by access upgrade investment:

where we are in the UK debate

Richard BuddSenior Regulatory, Economist, BT

16 September 2008

Where we are – July 2008 announcement

• Widespread ADSL2+ will ~ double current speeds (up to 24Mb/s)

• 10 million km fibre already, 120,000 business premises have fibre access

• Announced intention for £1.5bn investment in FTTC and FTTP

• Accessible by up to 10 million homes by 2012 ~ 40Mb/s to 100Mb/s by FY 2012

• All fibre based services from BT will be wholesaled to other ISPs - would be world’s most open super-fast network

Planned peak broadband speeds and coverage by country

Source : OECD Telecommunications Database

Peak service rate CoverageOpen access

100 Mbps (FT)

50 Mbps

20 Mbps (ATT)

40 Mbps (Verizon)

100 Mbps(NTT)

100 Mbps(BT)

17% by 2012 (FT)

26% by 2012

27% by 2010 (ATT)

16% by 2010 (Verizon)

40% by 2009 (NTT)

40% by 2012 (BT)

×

×

×

100 Mbps(KT)

96% by 2009 (KT) ×

Major Govt. funding

High Density Population

×

×

×

×

×

×

×

×

×

Note: All countries have a range of speeds

Commercial drivers

• Virgin Media upgrade• Success of 3G mobile “dongles”• Increasing demand for bandwidth from IPTV• 21CN core upgrade …but consumer “willingness to pay” / take-up

uncertain …extent and form of regulation uncertain

- minimise regulatory risk to investment - no RAB in telecoms; not expecting any price

controls

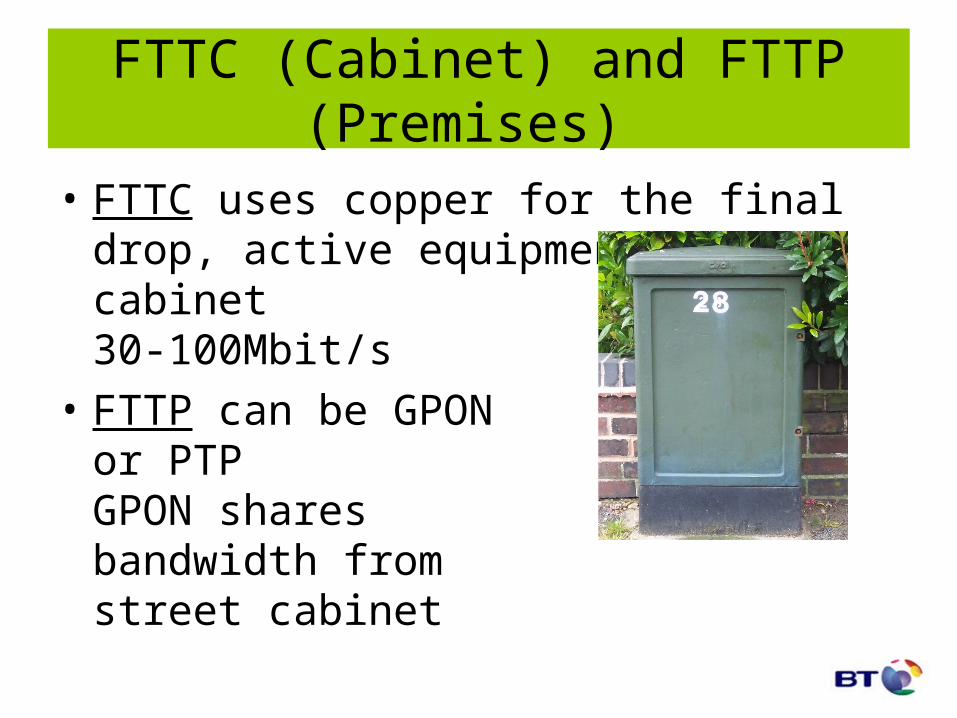

FTTC (Cabinet) and FTTP (Premises)

• FTTC uses copper for the final drop, active equipment in cabinet30-100Mbit/s

• FTTP can be GPON or PTPGPON shares bandwidth from street cabinet

BSG Chairman’s Foreword

•Deployment costs of FTTC nationwide three to four times higher than current gen bband

•FTTP/GPON five times higher again

•FTTP/PTP ~ six times higher than FTTC

Analysys Mason Report for the Broadband Stakeholder Group

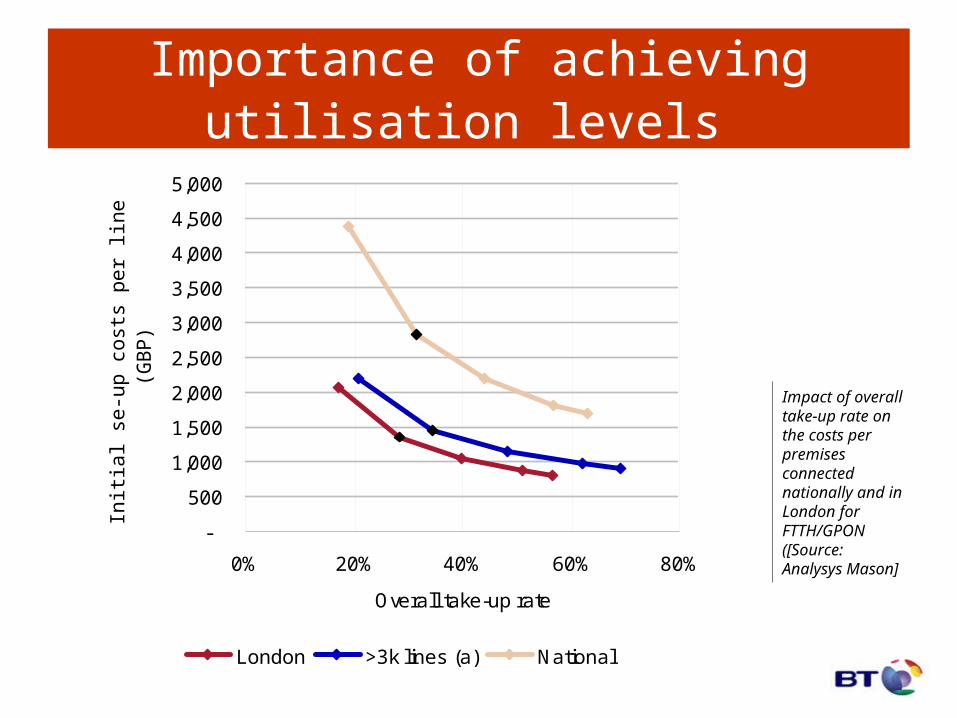

Importance of achieving utilisation levels

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0% 20% 40% 60% 80%

Overall take-up rate

Initi

al s

e-u

p c

ost

s p

er

line

co

nn

ect

ed

(G

BP

)

London >3k lines (a) National

Impact of overall take-up rate on the costs per premises connected nationally and in London for FTTH/GPON ([Source: Analysys Mason]

Regulatory consultations

• Ofcom - Future broadband: policy approach to NGA, September 2007

• Ofcom – NG New Build: Promoting higher speed broadband in new build developments, April 2008

• ‘Future Broadband’ Statement expected mid-September 2008

• Also, European Commission draft Recommendation, mid-September 2008

Future broadband: policy approach to NGA, September 2007, Five Principles

1) Contestability NGA Investment open to all

2) Maximising potential for innovation Focus on competing infrastructure investments

3) Equivalence BT Upstream [Access business] has same products, processes and price for CPs as for BT Downstream

4) Reflecting risk in returnsAnchor product regulation or risk-adjusted returns

5) Regulatory certainty Stability and clarity

2007 Ofcom Consultation - competition can be promoted at many levels and locations through

contestability and innovation

Customer StreetCabinet Local

Exchange

Metro NodeCore Network

Passive Access

Copper or Fibre Fibre

Duct

Fibre

Wavelength

Duct

Sub-loop unbundling

Fibre

Wholesale Access Product

Active LineAccess

Active LineAccess

Active LineAccess

Street cabinet

Local exchange Metro Node Core Network

Copper sub-loop

FibreFibre to the cabinet

Splitter Metro Node Core Network

Fibre

Local exchange

Fibre to the home

Sub-loop unbundling - passive copper line access; appropriate supporting backhaul products

Active line access - high quality, flexible, Ethernet based product; appropriate supporting backhaul

products

Active line access - high quality, flexible, Ethernet based product; appropriate supporting backhaul

products

Two main remedies for market power: sub-loop access and ALA

New build networks - FTTH, no copper access, maybe not BT

• Competition can be promoted by:– Contestability at the point of deployment – Application of appropriate regulations where market

power develops • Consumer protection by ensuring access to

existing services at existing prices • Voice regulation continues, possibly by new

products• Spectre of fragmentation – patchwork of new

build technologies.

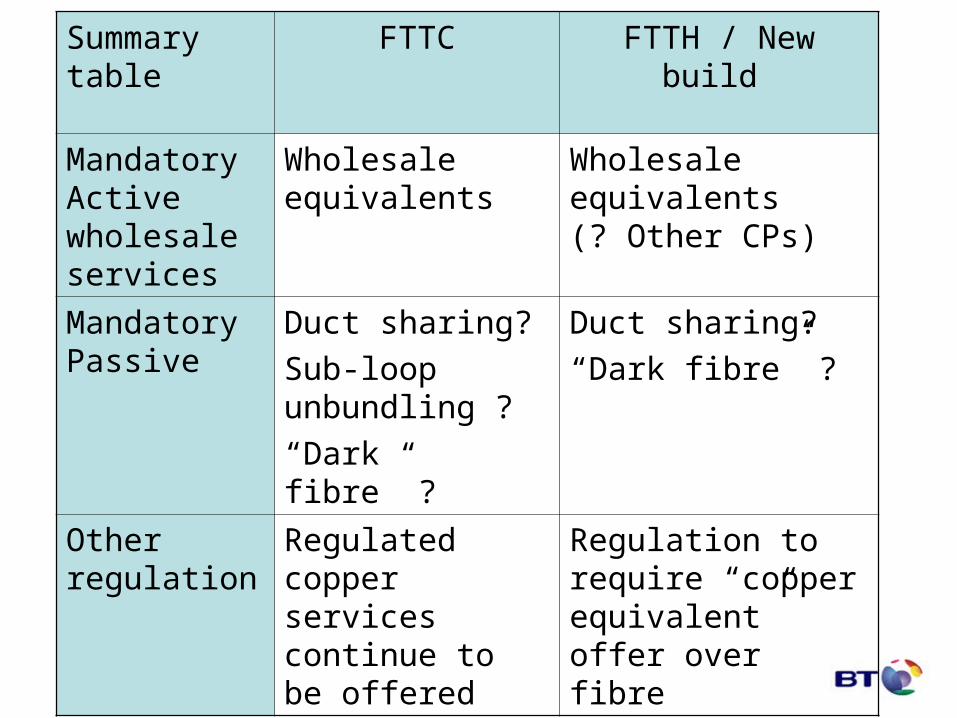

Summary table

FTTC FTTH / New build

Mandatory Active wholesale services

Wholesale equivalents

Wholesale equivalents (? Other CPs)

Mandatory Passive

Duct sharing?

Sub-loop unbundling ?

“Dark fibre” ?

Duct sharing?

“Dark fibre” ?

Other regulation

Regulated copper services continue to be offered

Regulation to require “copper equivalent” offer over fibre

Copper Access Regulation

• Telecommunications Strategic Review (TSR) saw limited prospect for competition to “legacy monopoly access infrastructure”

• Various implications:– WACC de-averaged and lower for access network – Some costs removed from copper access services in

2005 as already met by customers• Wholesale copper access price materially below forward-

looking costs (and at utility return)• Fibre to be priced at a premium to copper• Copper regulation will influence fibre returns

Regulatory certainty …

• 2005 TSR unwound 1990s policy towards competition between current generation access

• Concern over aggressive push on “remedies” upstream of the ALA product after any BT investment?

• Business case has long payback

• City reaction mixedat best