20

Reinsurance Session 2

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | neil-carson |

| View: | 267 times |

| Download: | 6 times |

Reinsurance

Session 2

Reinsurance

1. Finite Reinsurance2. Life Reinsurance3. Securitization / Alternative Capital

Sources4. Reinsurance Failures

Session 2

Reinsurance

1. Finite Reinsurance

Finite Reinsurance

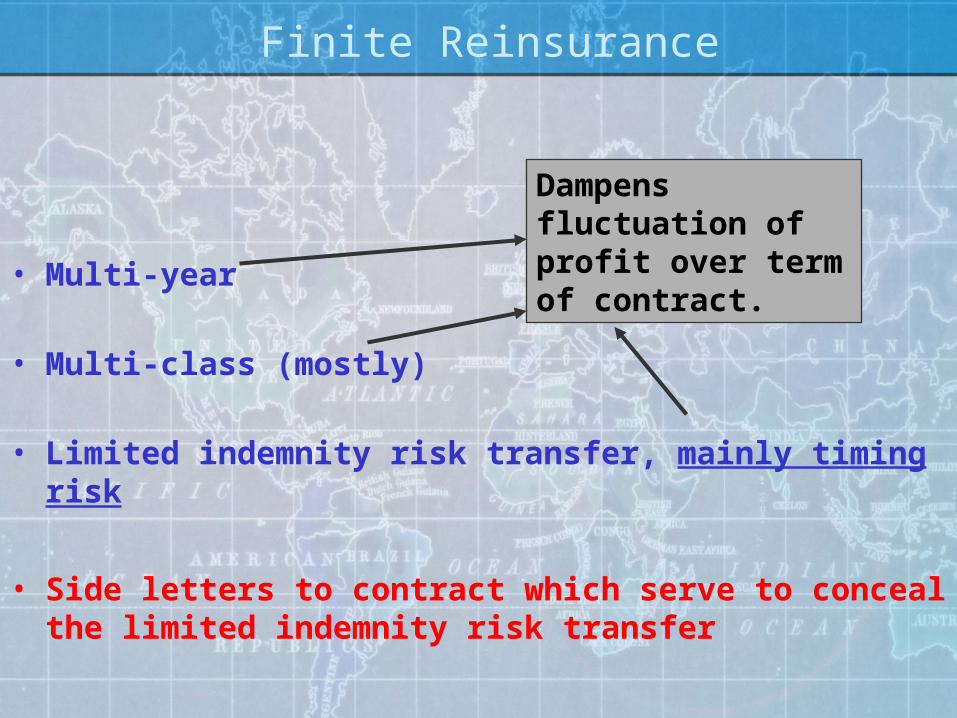

• Multi-year

• Multi-class (mostly)

• Limited indemnity risk transfer, mainly timing risk

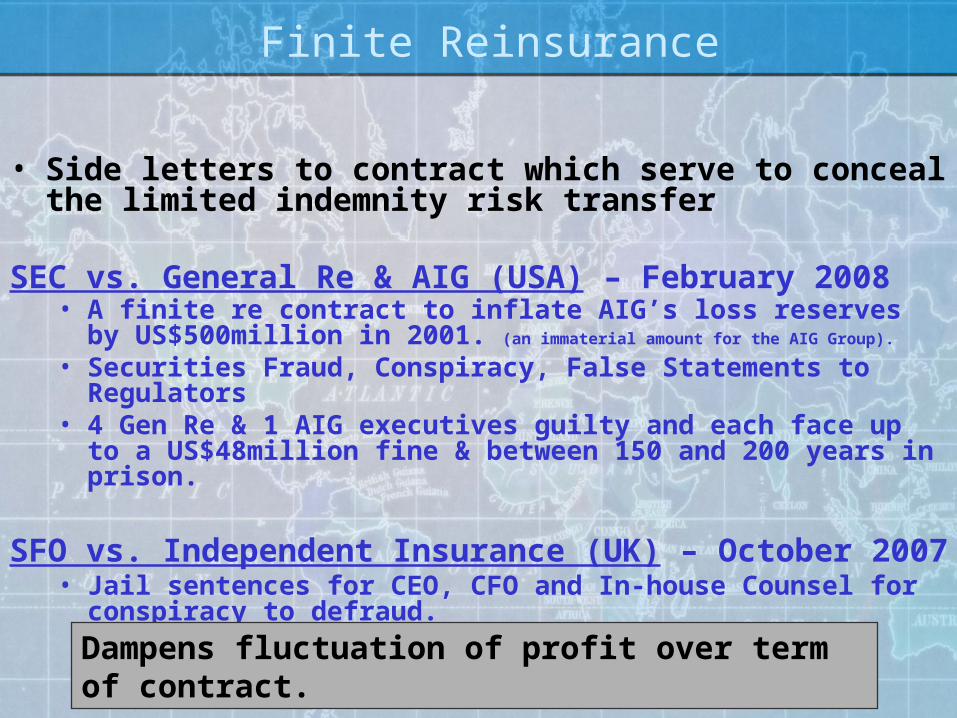

• Side letters to contract which serve to conceal the limited indemnity risk transfer

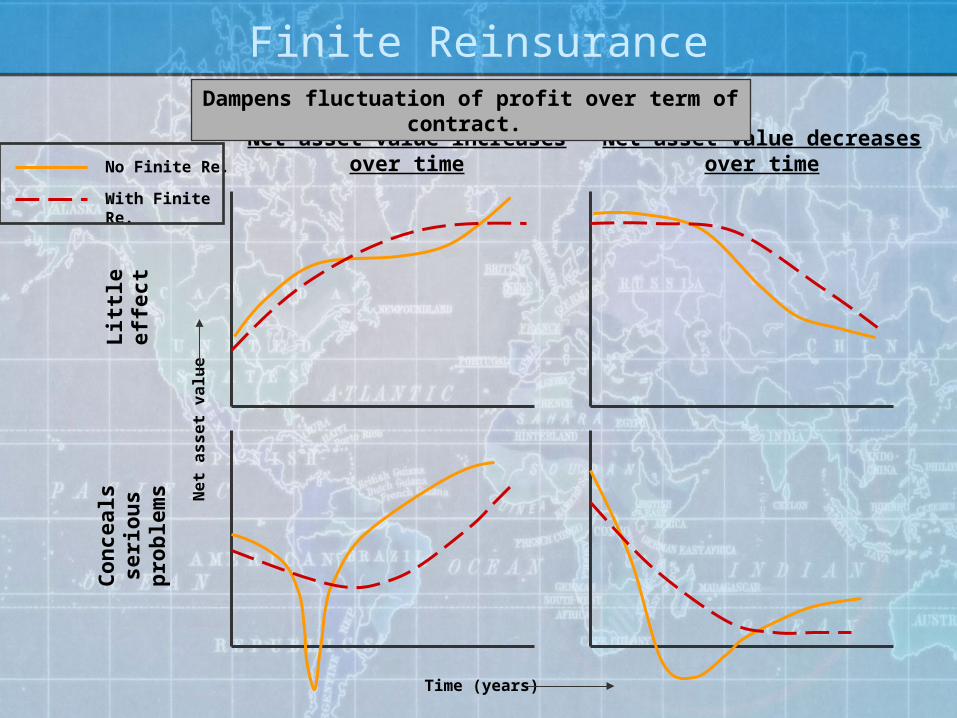

Dampens fluctuation of profit over term of contract.

Finite ReinsuranceWhere would you most likely find Finite Reinsurance?

High level catastrophe XL cover

Low level QS cover

Likely location for Finite Reinsurance

Cover for fairly high claims whose level is predictable over 5-8 years

Finite Reinsurance

Ne

t a

ss

et

va

lue

Time (years)

No Finite Re.

With Finite Re.

Net asset value increases over time

Net asset value decreases over time

Lit

tle

effe

ctC

on

ceal

s se

rio

us

pro

ble

ms

Dampens fluctuation of profit over term of contract.

Finite Reinsurance

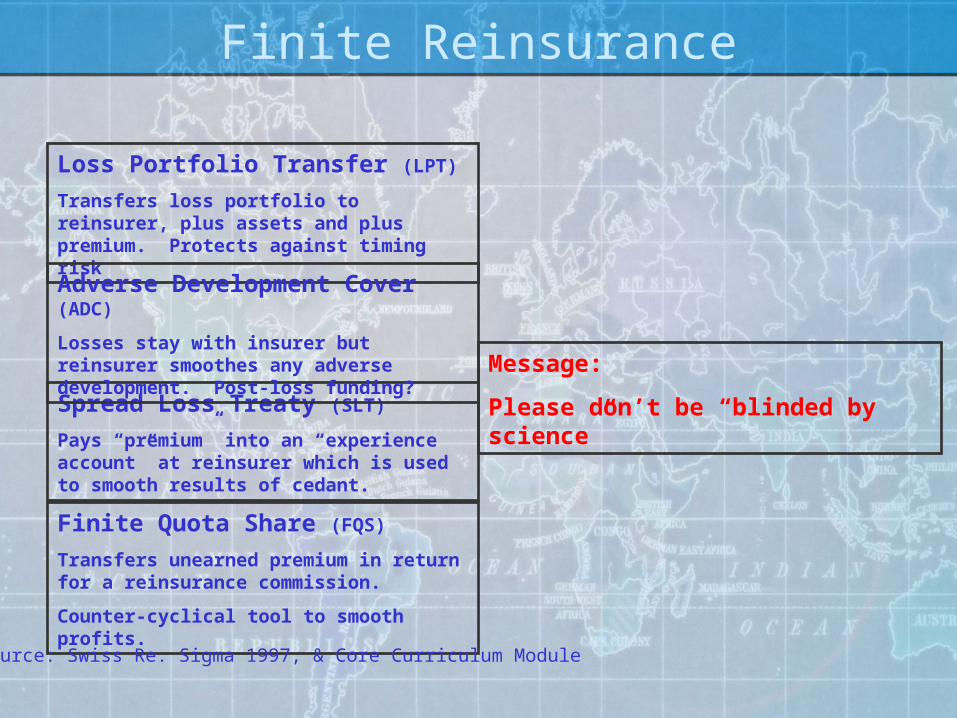

Loss Portfolio Transfer (LPT)

Transfers loss portfolio to reinsurer, plus assets and plus premium. Protects against timing risk

Spread Loss Treaty (SLT)

Pays “premium” into an “experience account” at reinsurer which is used to smooth results of cedant.

Finite Quota Share (FQS)

Transfers unearned premium in return for a reinsurance commission.

Counter-cyclical tool to smooth profits.

Adverse Development Cover (ADC)

Losses stay with insurer but reinsurer smoothes any adverse development. Post-loss funding?

Source: Swiss Re. Sigma 1997, & Core Curriculum Module

Message:

Please don’t be “blinded by science”

Finite Reinsurance

• Side letters to contract which serve to conceal the limited indemnity risk transfer

SEC vs. General Re & AIG (USA) – February 2008• A finite re contract to inflate AIG’s loss reserves by

US$500million in 2001. (an immaterial amount for the AIG Group).

• Securities Fraud, Conspiracy, False Statements to Regulators

• 4 Gen Re & 1 AIG executives guilty and each face up to a US$48million fine & between 150 and 200 years in prison.

SFO vs. Independent Insurance (UK) – October 2007• Jail sentences for CEO, CFO and In-house Counsel for

conspiracy to defraud.

Dampens fluctuation of profit over term of contract.

Reinsurance

2. Life Reinsurance

Life Reinsurance

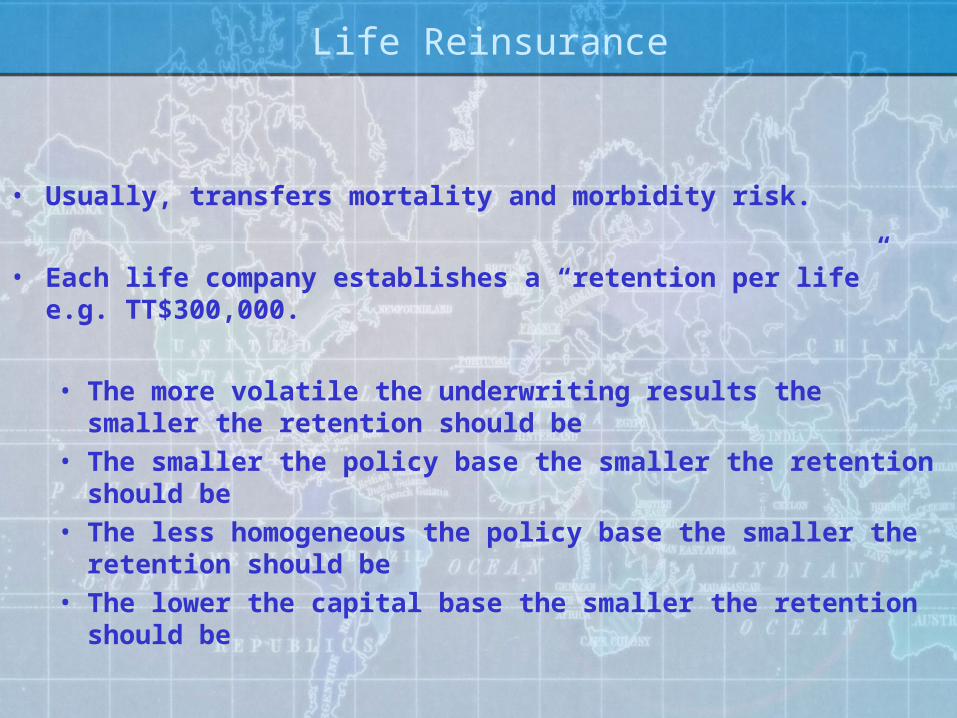

• Usually, transfers mortality and morbidity risk.

• Each life company establishes a “retention per life” e.g. TT$300,000.

• The more volatile the underwriting results the smaller the retention should be

• The smaller the policy base the smaller the retention should be

• The less homogeneous the policy base the smaller the retention should be

• The lower the capital base the smaller the retention should be

Life Reinsurance

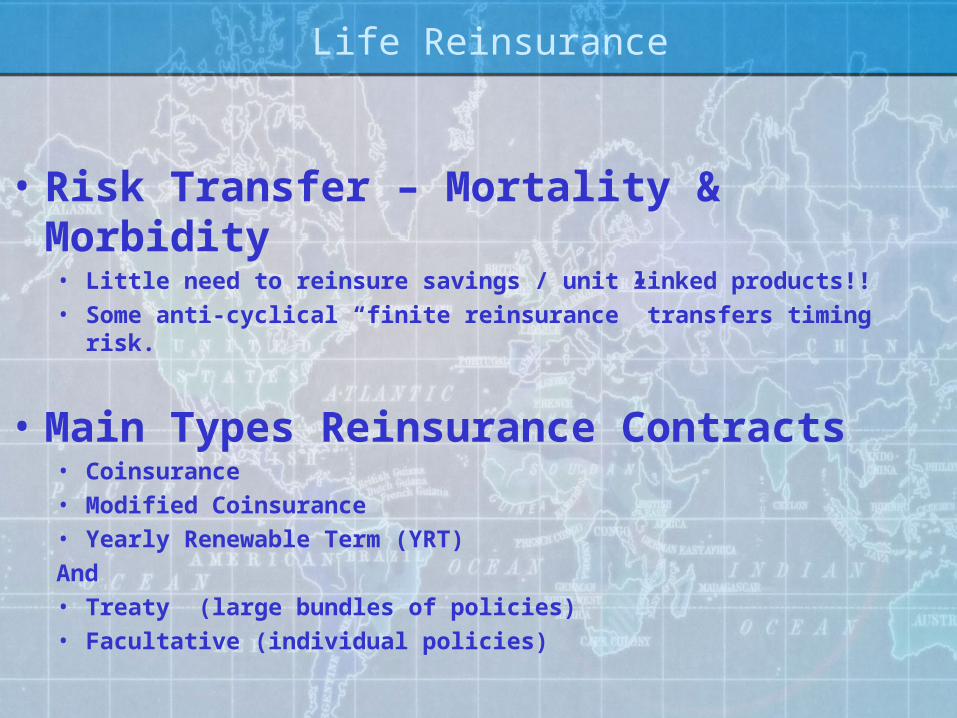

• Risk Transfer – Mortality & Morbidity• Little need to reinsure savings / unit linked products!!• Some anti-cyclical “finite reinsurance” transfers timing risk.

• Main Types Reinsurance Contracts • Coinsurance• Modified Coinsurance• Yearly Renewable Term (YRT)And• Treaty (large bundles of policies)• Facultative (individual policies)

Life Reinsurance -Types of Contract

YRTReinsurer assumes mortality and morbidity risk only, & annual

premiums based on amount at risk. Premiums increase with age of insured. Investment risks and returns remain with primary insurer.

(Quota Share or Excess of Loss)

CoinsuranceReinsurer shares a percentage of business including cash flows and

reserves. Investment risks and returns are shared in proportion to the risk transfer.

Modified CoinsuranceAs above, but ceding company retains assets and reserves and,

therefore, investment risks and returns. Primary insurer pays a fixed rate of interest to reinsurer for the investments it “holds” in relation to the risk transferred.

Reference material:American Council of Life Insurers (ACLI). Reinsurance Treaty Sourcebook http://www.acli.com/ACLI/Issues/GR02-216.htm

Reinsurance

3. Securitization / Alternative Capital Sources

Insurance Securitization

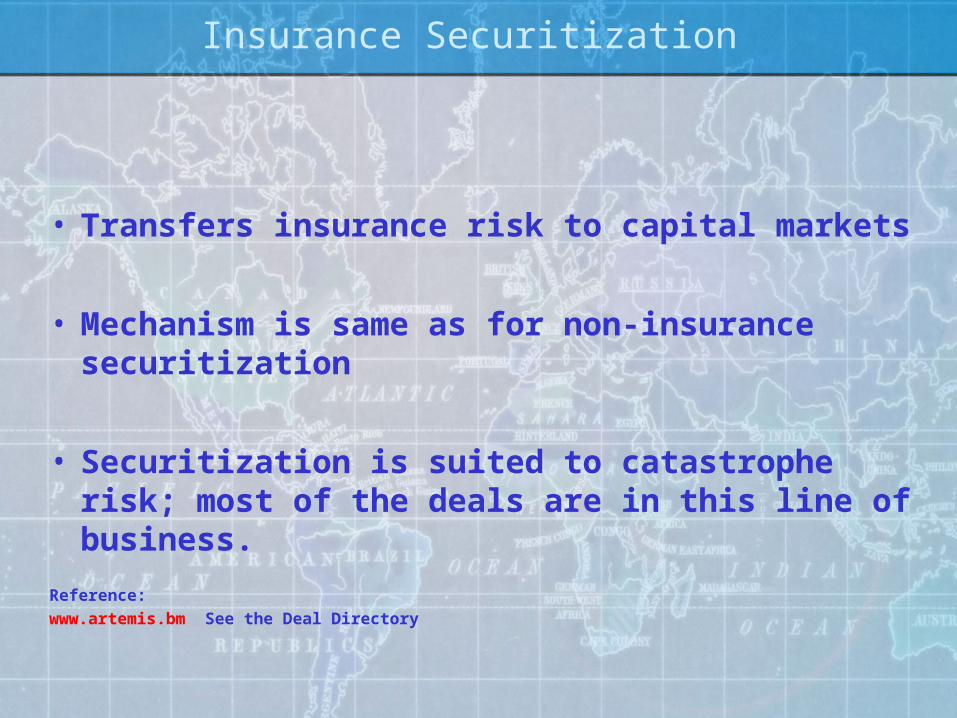

• Transfers insurance risk to capital markets

• Mechanism is same as for non-insurance securitization

• Securitization is suited to catastrophe risk; most of the deals are in this line of business.

Reference:

www.artemis.bm See the Deal Directory

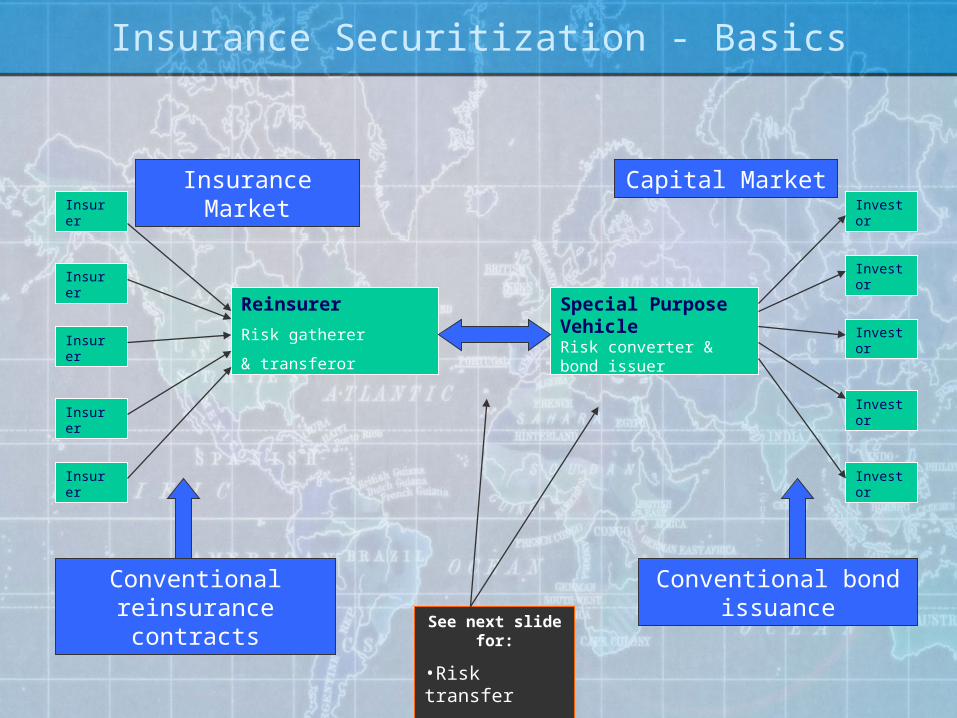

Insurance Securitization - Basics

Insurance Market Capital Market

Reinsurer

Risk gatherer

& transferor

Special Purpose VehicleRisk converter & bond issuer

Insurer

InvestorInsurer

Insurer

Insurer

Insurer

Investor

Investor

Investor

Investor

Conventional reinsurance contracts

Conventional bond issuance

See next slide for:

•Risk transfer

•SPV

Insurance Securitization - Basics

Risk Transfer from Reinsurer to SPV

1. Defined risk is transferred to SPV

2. Reinsurer is reimbursed by triggering a claim:

• Indemnity-based (like a conventional claim)• Not popular with investors

and now uncommon – too much moral hazard

• Parametric trigger• Defined events at defined

locations – quake of specified magnitude in specified location

• Cash flow criterion – variance from pre-agreed cash flow budget

The Special Purpose Vehicle1. Receives funds from

• Transferor – reinsurance premium

• Investors – purchase of bonds

2. If risk transfer claim is triggered, a payment is made to reinsurer.

3. If no payment to reinsurer, then on maturity the bondholders receive all cash in SPV:

• Reinsurance premium• Refund of bond purchase price• Investment income on the above

Risk transfer

SPV

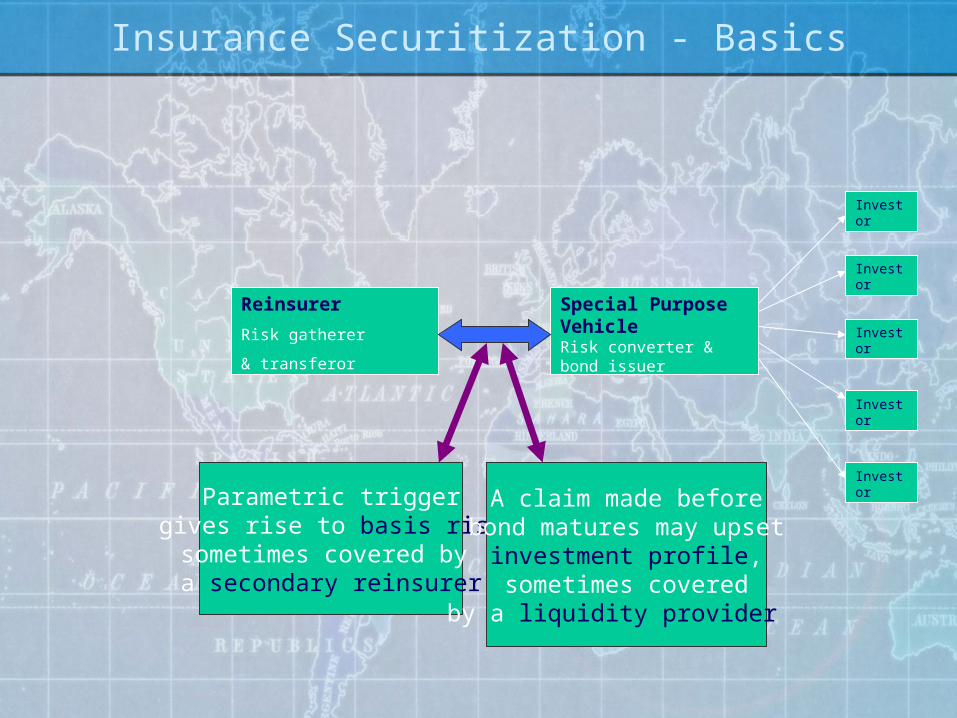

Insurance Securitization - Basics

Reinsurer

Risk gatherer

& transferor

Special Purpose VehicleRisk converter & bond issuer

Investor

Investor

Investor

Investor

Investor

Parametric trigger gives rise to basis risk,sometimes covered by a secondary reinsurer

A claim made beforebond matures may upset

investment profile,sometimes covered

by a liquidity provider

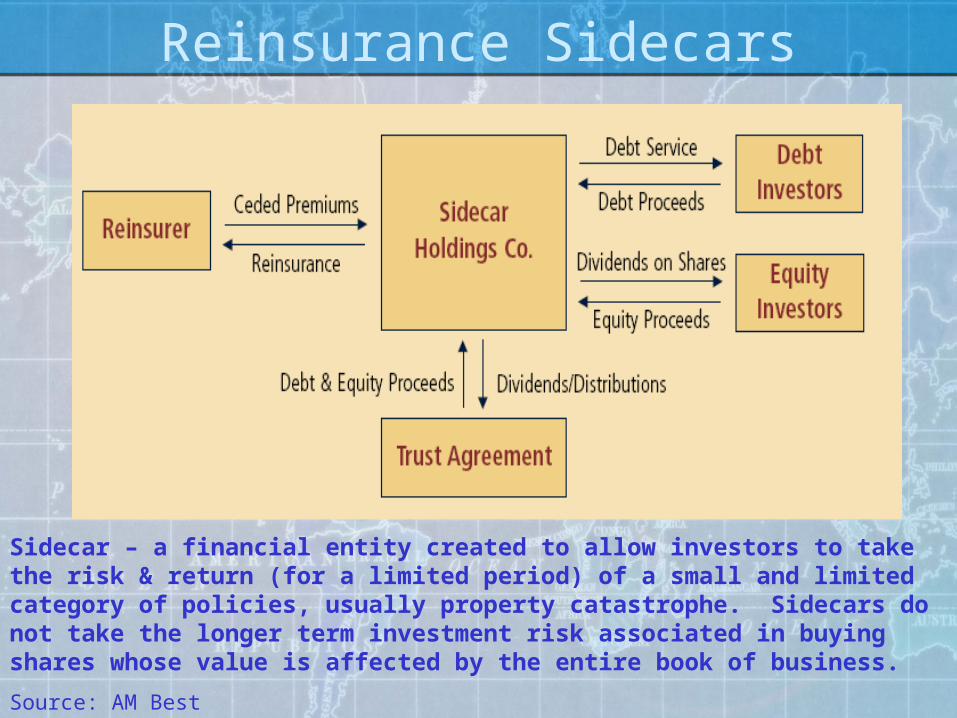

Reinsurance Sidecars

Sidecar – a financial entity created to allow investors to take the risk & return (for a limited period) of a small and limited category of policies, usually property catastrophe. Sidecars do not take the longer term investment risk associated in buying shares whose value is affected by the entire book of business.

Source: AM Best

Reinsurance4. Reinsurance Failures

Insolvency of a reinsurer

BUT, before that happens…..

Cashflow problems in a reinsurer will quickly become the problem of the reinsured

Failure of Reliance National, a large US insurer caused by failure of reinsurers for whom it was fronting – “WORKERS’ COMPENSATION CARVE-OUT”

Even without failures, the biggest & best reinsurers are not immune to problems …..

Munich Re in 2002 … Too heavily invested in equities during a stock market crash.

Munich Re in 2008 … Hurricanes Gustav & Ike in the Caribbean wipe out 3Q profits.

Reinsurance

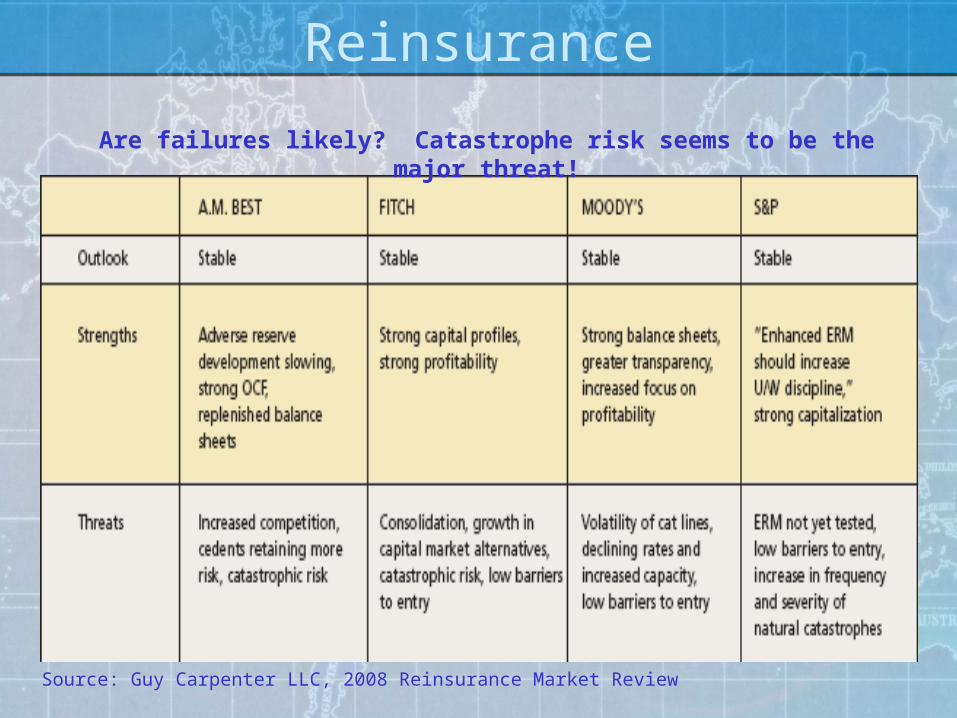

Source: Guy Carpenter LLC, 2008 Reinsurance Market Review

Are failures likely? Catastrophe risk seems to be the major threat!