Related Party Transactions By Haihao (Ross) Lu A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Rotman School of Management University of Toronto Ó Copyright by Haihao Lu 2017

Transcript

Related Party Transactions

By

Haihao (Ross) Lu

A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy

Rotman School of Management University of Toronto

Ó Copyright by Haihao Lu 2017

ii

Related Party Transactions

Haihao (Ross) Lu

Doctor of Philosophy

Rotman School of Management University of Toronto

2017

Abstract

Related party transactions (hereafter RPTs) are common business practices. If misused,

however, they can result in significant losses for investors. This study attempts to examine

empirical issues pertaining to RPTs. Specifically, the paper has two goals. The main goal is

related to a 2006 Securities and Exchange Commission (SEC) regulation mandating public

firms to disclose their governance policies on RPTs. I intend to investigate whether firms

change their RPT behaviors in response to this mandated RPT governance disclosure and

whether investors update the implied cost of capital on these RPT behaviors accordingly.

Employing hand-collected RPT data for S&P 1500 firms, I find the initiation of RPT

governance disclosure significantly reduces the occurrence of RPTs, suggesting an ex-post

improvement in RPT governance. This reduction is more pronounced on firms with higher

agency costs. I also find the types of RPTs and the identities of related parties play a role in

the detected disclosure effect, suggesting certain types of RPTS could be more likely to be

used as expropriation. Furthermore, I document that the disclosure of RPT governance

reduces the implied costs of capital premium (ICC) associated with RPTs. Taken together, this

analysis provides initial evidence about the effects of the SEC’s 2006 regulation on RPT

governance disclosures, and shows how the disclosures on RPT governance can enhance firms’

iii

governance on RPT activities and whether investors could recognize the firm behavior change

by reducing firms’ implied cost of capital.

The second goal is to assess whether independent directors’ compensation is

associated with the occurrence of RPTs. Studying independent directors attracts my interest

because they are responsible for reviewing and approving RPTs in most companies. By

decomposing independent directors’ compensation into the market-level component and the

over-compensated component, I show that firms with over-compensated directors or with a

lower portion of equity-based compensation in contrast to cash-based compensation incur

more RPTs. These results suggest that independent directors’ overcompensation reduce

directors’ independence and equity-based compensation aligns directors’ interests with those

of shareholders, consistent with the private benefit theory. This study provides novel evidence

that appropriate directors’ compensation design can better control RPT behaviors.

iv

Acknowledgements

First and foremost, I would like to thank my supervisor, Ole-Kristian Hope, for his

valuable advices and unconditional support during the term of my Ph.D. study. His passion to

research, high standards to work, and excellent professionalism left a profound impact on me

that will keep motivating me for the rest of my life. He never hesitates to offer help and

always pushes me to strive for the next level. I couldn’t achieve what I have done without him.

I am also very much indebted to my mentor, Gus De Franco for his generous help in my

research. Since the very first year, he has encouraged me to discuss any topics with him, no

matter how immature it initially sounds like. I benefit a lot from his patience, kindness and

professional judgment. I would also like to thank the other two committee members, Ping

Zhang and Baohua Xin, for their invaluable suggestions and encouragements in developing

the dissertation. I would especially thank Mark Kohlbeck for donating his time to serve as my

external committee member and providing me with constructive and beneficial comments.

I also want to thank all Rotman professors who helped me during my Ph.D. study,

including Partha Mohanram, Jeff Callen, Gordon Richardson, Hai Lu, Franco Wong, Scott

Liao, Dushyant Vyas, Francesco Bova, Alex Edwards, Daehyun Kim, Aida Wahid and Feng

Chen. I also enjoyed my time with my fellow Ph.D. students Sasan Saiy, Yu Hou, Leila

Peyravan, Wuyang Zhao, Danqi Hu, Barbara Su, Stephanie Cheng, Mahfuz Chy, Muhammad

Azim and Mingyue Zhang.

v

Finally, I am very grateful to my beautiful wife and best friend, Stella Peng, and my

lovely kids, Dennis Lu and Deanna Lu, who supported me wholeheartedly throughout my

journey toward Ph.D. I would also like to acknowledge with great gratitude, the support and

love from my parents, sister, and parents-in-law. Their help and love were essential to my

achievement.

vi

Table of Content

Abstract ........................................................................................................................................... ii

Acknowledgement ……………………………………………………………………………….iv

Table of Contents ............................................................................................................................ v

Introduction .................................................................................................................................... xi

Chapter 1: Economic Consequences of Corporate Governance Disclosure: Evidence from the

2006 SEC Regulation on Related-Party Transactions ................................................................ 1

Table 7 for Chapter 2: Moderator of Director Compensation Effect on RPTs ................. 82

Table 8 for Chapter 2: Director compensation effect on RPTs at firm level .................... 83

Table 9 for Chapter 2: Alternative RPT measurement ..................................................... 84

x

Introduction

Related party transactions are common business practices. If properly used, they can be

beneficial for firms. However, misused related party transactions can cause significant losses for

investors, as in the case of Enron and Adelphia. Even though the transaction amount could be

small, misused RPTs could signal serious governance problem. Given that RPTs represent

potential means for insiders to expropriate wealth from other investors via self-dealing, both the

Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission

(SEC) require detailed disclosure of material RPTs in annual reports and proxy statements. In

2006, the SEC amended its rule and regulation for RPT disclosure, which includes an entirely

new requirement to disclose a description of a company’s policies and procedures for the review,

approval, and ratification of RPTs.

Chapter 1 shows how a 2006 SEC regulation mandating RPT governance disclosure

affects the firm’s RPT behavior and the investors’ risk perception on firm’s RPTs. Before 2006,

only a few firms voluntarily disclosed their RPT governance procedures. After 2006, the RPT

governance disclosure becomes mandatory. I expect this mandatory disclosure of RPT

governance reduce the occurrence of RPTs because it enhances the RPT governance. For firms

that did not have a formal RPT governance policy before the regulation, this mandatory

disclosure requirement would encourage them to establish formal RPT policies to avoid bad

signals to investors. For firms that had an RPT policy but did not disclose before the regulation,

public RPT governance disclosure would enhance the monitoring effects as the disclosure

increases the litigation risk of responsible directors, mitigates the opportunistic behaviors of

insiders, and hence reduces agency problems arising from RPTs. Consistent with my expectation,

xi

I find when firms initiate their RPT governance disclosures following the mandatory requirement,

they significantly reduce their RPT behaviors.

Chapter 1 also examines whether investors alter their risk perceptions on those firm’s

RPT behaviors following the 2006 regulation, using implied cost of capital as risk perception

proxy. I expect this mandatory disclosure will reduce implied cost of capital premium on firms

RPTs as this mandatory disclosure reduces the information asymmetry between investors and

firms and brings better controls on RPTs. I do find affirmative results.

Chapter 2 investigates how independent directors’ compensation can affect firm’s RPT

behaviors. As independent directors are responsible for RPT governance in most U.S. companies,

the way in which they are compensated is likely to affect their incentives to effectively govern

firms’ behaviors. On the one hand, their compensation has to be high enough to attract capable

candidates; on the other hand, over-compensation may impair the independence of directors,

making them more subject to managers’ influences. By decomposing independent directors’

compensation into the market level component and the over-compensated component, I find that

firms with over-compensated directors or with a lower portion of equity-based compensation in

contrast to cash-based compensation incur more RPTs. These results suggest that independent

directors’ overcompensation reduces directors’ independence and equity-based compensation

aligns director interests with those of shareholders.

1

Chapter 1

Economic Consequences of Corporate Governance Disclosure: Evidence from the 2006

SEC Regulation on Related-Party Transactions

1. Introduction

A related-party transaction (hereafter RPT) is a transfer of resources, service, or

obligations between a reporting entity and a related party, which usually refers to executives, the

board of directors, and primary shareholders.1 RPTs can be beneficial to firms’ daily operations

because appropriate RPTs can reduce transaction costs, improve operating efficiency, and share

financial and intangible resources. However, if misused, they can result in significant losses for

investors, as in the case of Enron and Adelphia.2 Even though the transaction amounts could be

small, misused RPTs could signal serious governance problems. Given that RPTs represent

potential means for insiders to expropriate wealth from other investors via self-dealing, both the

Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission

(SEC) require detailed disclosure of material RPTs in annual reports and proxy statements. To

facilitate investors’ assessment of the potential conflict of interests arising from RPTs, the SEC

amended its rules and regulations for RPT disclosure in 2006.3 The revised SEC regulation

includes an entirely new requirement to disclose a description of a company’s policies and

procedures for the review, approval, and ratification of RPTs.

In this paper, I investigate economic consequences of this mandatory RPT governance

disclosure. Specifically, I ask two questions: (1) does the disclosure of firms’ RPT governance

1 Related parties also include their immediate family members. 2For example, the top management team of Enron used special purpose entities to manipulate profit. Adelphia Communications Corp guaranteed related party debts and provided extensive loans to its top executives.3https://www.sec.gov/rules/final/2006/33-8732a.pdf, retrieved on July 25, 2017

2

lead to a lower level of RPT activities? (2) does the disclosure of firms’ RPT governance lead to

a lower implied cost of capital?

Before 2006, only a few firms voluntarily disclosed how they govern their RPTs.4 The

2006 SEC regulation requires that all firms to disclose their RPT review policy, representing an

exogenous increase in RPT governance disclosure. For the convenience of presentation, I define

firms that voluntarily disclosed their RPT governance before the 2006 regulation as “Already-

Disclosed” firms and firms that initiated RPT governance disclosure after the 2006 regulation as

“Newly-Disclosed” firms. Since the Already-Disclosed firms have voluntarily disclosed their

RPT governance prior to 2006, the impact of 2006 regulation on the Already-Disclosed firms, on

average, is expected to be significantly less than that on the Newly-Disclosed firms.

As discussed in Section 2, this study predicts that the mandatory disclosure of RPT

governance leads to a lower level of RPTs and lower cost of capital, both involving real impacts

on firms’ operating activities. This prediction is consistent with the conflict-of-interest view

(Kohlbeck and Mayhew 2010, 2017), which considers RPTs as a potentially harmful form of

expropriating wealth from shareholders. For firms that did not have a formal RPT governance

policy before the regulation, this mandatory disclosure requirement encourages them to establish

a formal policy to avoid being scrutinized by investors and regulators. For firms that had RPT

policies but had not disclosed their existing RPT policies before the regulation, public RPT

governance disclosure potentially enhances the monitoring as the disclosure increases the

litigation risk of responsible directors, mitigates the opportunistic behaviors of insiders, and

hence reduces agency problems arising from RPTs. To test these hypotheses, I hand-collect

4 Approximately 20% of S&P 1500 firms in my sample voluntarily disclosed RPT governance in the fiscal year 2004.

3

information regarding RPTs and RPT governance for all S&P 1500 non-financial firms from

annual proxy statements for fiscal years 2004, 2007, and 2010.5

For the first research question, I find that after the 2006 regulation, Newly-Disclosed

firms significantly reduce their RPT activities relative to Already-Disclosed firms. This result is

robust to controlling for several determinants of RPT occurrence, suggesting that (1) the

disclosure of RPT governance enhances firms’ governance on RPTs and (2) the 2006 SEC

regulation affects firms’ RPT activities. The conclusions also hold for a propensity-score

matched sample between Already-Disclosed firms and Newly-Disclosed firms.

Next, I examine whether such RPT governance disclosure effects on RPTs are

conditional on mechanisms that can reduce agency problems. Previous literature shows that

external monitoring helps reduce the opportunistic behaviors of insiders and hence reduce

agency costs (Jensen and Meckling 1976; Huddart 1993; Giroud and Mueller 2011). When

external monitoring is relatively weak, potential agency costs are high, and thus managers are

more likely to be involved in self-dealing. I expect that the RPT governance disclosure effects on

RPTs should be more pronounced when the external monitoring is less effective, because these

RPT activities are more likely to be harmful ex ante. Consistent with my expectation, I find that

the disclosure effects of RPT governance are stronger when there is lower institutional

ownership, lower analyst following, and less severe industry competition.

In the second research question, I investigate whether this mandatory disclosure alters the

implied cost of capital. Prior literature finds that RPT firms are associated with poor corporate

governance and lower accounting quality (Kohlbeck and Mayhew 2017; Gordon and Henry

2005). While not all RPTs are misused, there is a view that RPTs represent a high-risk factor for 5Following Kohlbeck and Mayhew (2017), I do not collect RPTs data in consecutive years because many RPTs are sticky transactions that either have multiple-year terms or appear every year with similar contract terms. Collecting data every three years allows for changes in RPTs and is more efficient.

4

investors to consider before investing (Cheung, Rau, and Stouraitis 2006). There is evidence that

insiders may use RPTs to directly expropriate wealth from other investors (Cheung, Qi, Rau and

Stouraitis 2009; Kohle and Shastri 2004). High information asymmetry and high expropriation

risk suggest that RPTs firms could be associated with high implied costs of capital. I argue that

this mandatory disclosure can reduce the implied costs of capital associated with RPTs.

Consistent with this expectation, my empirical analyses show that when Newly-Disclosed firms

disclose their RPT governance, investors reduce the implied cost of capital associated with RPTs

of these firms. The implied cost of capital associated with RPTs of Already-Disclosed firms, on

the other hand, does not change significantly from the pre-regulation to the post-regulation

periods.

Previous literature shows that the effects of disclosures on firms’ implied cost of capital

could be through two possible channels: an information channel or a governance channel

(Cheynel 2013; Verrecchia 2007; La Porta et al. 2000). The information channel implies that the

disclosure provides more information regarding how firms control their RPTs, reducing the

information asymmetry between firms and investors. Through the governance channel, the

disclosure improves firms’ governance on RPTs and reduces harmful RPTs, which leads to fewer

self-dealing activities and lower litigation risks. My analysis shows that, between these two

channels, the governance channel is the main contributing factor to the reduction of implied cost

of capital associated with RPTs. The empirical results show that for firms that only improved

their disclosure but that did not change their RPT behaviors in the post period, their implied cost

of capital associated with RPTs did not decrease. By contrast, for firms that reduce their RPTs in

the post period, their implied cost of capital associated with RPTs significantly reduced.

5

The SEC requires, among other disclosures, a disclosure of (1) whether the policies and

procedures are in writing, and (2) the persons or groups of persons who are responsible for the

review, approval, and ratification of RPTs. Hence I further test if these particular disclosure

requirements affect the frequency of RPTs and the implied cost of capital associated with RPTs.

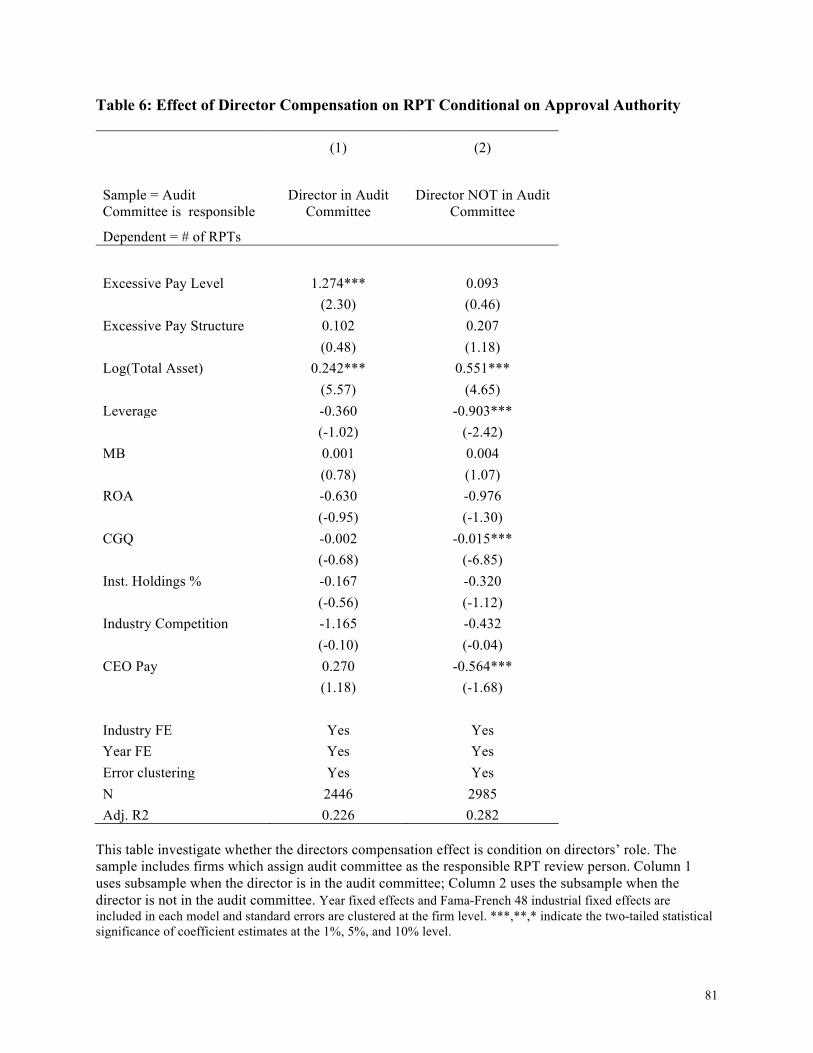

My results show that whether firms have a written policy does not affect the occurrence of RPTs

nor the implied cost of capital. The group responsible for approving RPTs, however, is

associated with outcomes of RPTs. Specifically, when an Audit Committee is responsible for

reviewing and approving RPTs, firms have fewer RPTs and lower implied cost of capital

associated with RPTs than firms that do not assign a specific committee to review RPTs.

This research contributes to the existing literature in several aspects. My study shows that

disclosure of RPT governance effectively increases firms’ monitoring of RPTs, reducing both

RPT activities and the implied cost of capital, suggesting that the disclosure of governance

enhances firms’ real governance on RPTs. Such outcomes add to literature studying real

disclosure effects (Leuz and Wysocki 2016), showing that mandatory disclosure requirements have

economic consequences on firms’ operating activities besides financial reporting.

I also find that the effects of RPT governance disclosure on RPTs are more pronounced

when industry competition is weak, when institution holding is low, and when analyst following

is low. These findings provide evidence that the effects of disclosure on governance are

contingent on potential agency costs. In addition, I find that the disclosure effects depend on the

transaction types and identities of related parties, suggesting that some types of RPTs are more

likely to be used as expropriation and that it is advisable to recognize the heterogeneity and treat

them differently.

6

This is one of the few papers investigating the economic consequences of the SEC’s 2006

regulation related to RPT governance disclosure. This mandatory requirement reflects the

continuous efforts of the SEC to encourage firms to provide more transparent disclosure about

RPTs. Studying how firms react to this new regulation and whether investors benefit from such

mandatory requirements can provide evidence on the effectiveness of the disclosure regulation

and should be relevant to future regulations.

Balsam, Gifford, and Puthenpurackal (2017) also find a change of RPTs around this 2006

SEC RPT disclosure change. My paper differs from theirs in several ways. First, this article

investigates a governance effect of a mandatory disclosure using a difference-in-differences

model around the 2006 SEC disclosure change, while their focus is on the association between

RPTs and CEO compensation. Recognizing their findings, I also control for CEO compensation

in my research design. Second, my sample includes a broader scope of companies. Specifically,

my sample consists of S&P 1500 composite firms while Balsam et al. (2017) randomly select

500 firms. Third, my paper examines more detailed RPT categories based on the identity of

related parties and transaction types. Such analysis helps to better understand the nature of RPTs

and how various types of RPTs can reflect conflict of interests differently.

Furthermore, among the several RPT disclosures required by the SEC in 2006, I provide

evidence on which particular disclosures affect investors' implied cost of capital. Such findings

can provide further guidance to regulators, and firms as well, to adopt the best practices in RPT

monitoring.

Finally, my research contributes to the limited empirical literature on RPTs in the U.S.

setting. Existing RPTs research focuses mainly on developing countries because firms are more

likely to have self-dealing problems when legal protection for investors is weak. In contrast,

7

there are few studies in more developed countries such as the U.S. My study shows that even in

the U.S., where strong minority shareholder protection is in place, RPTs can still imply risks to

investors, adding to the findings of Kohlbeck and Mayhew (2010, 2017) and Ryngaert and

Thomas (2012).

2. Hypotheses Development

2.1 Background RPT Regulations in the U.S.

RPTs represent potential “self-dealing” between the company and its executives,

directors, major shareholders, and other related parties. Such transactions usually require

additional monitoring from shareholders. In the U.S., regulators do not require shareholders’

approval of RPTs and instead rely on disclosure regulation and ex-post litigation to protect

minority shareholders.6 The FASB and the SEC set the main RPT disclosure requirements. The

FASB ASC Topic 850 requires disclosure of material RPTs in the financial statements. The SEC

regulation S-K 404(a) requires disclosure of RPTs in both 10-Ks and proxy statements. Required

disclosures by SEC include (1) the nature of the relationship, (2) a description of the transaction,

(3) the dollar amount of the transaction, and (4) the amount due to or from related parties at the

balance sheet date.

In August 2006, the SEC amended its regulations for RPT disclosure. The revised SEC

regulation includes an entirely new requirement to describe a company’s policies and procedures

for the review, approval, and ratification of RPTs. The regulation states that the description

should include: (a) the types of transactions that are covered by such policies and procedures; (b)

the standards to be applied pursuant to such policies and procedures; (c) the persons or groups of

6 Before 2002, loans to executives were prevalent RPTs in public companies. The Sarbanes-Oxley Act of 2002, however, prohibits any public company from providing loans to its executive officers and directors.

8

persons on the board of directors or otherwise who are responsible; and, (d) a statement of

whether such policies and procedures are in writing and, if not, how such policies and procedures

are evidenced.

2.2 Literature Review and Hypotheses Development

Prior literature has established two prevailing theories regarding RPTs: the conflict of

interests theory and the efficient transaction theory. The former views RPTs as a potentially

harmful form of expropriating wealth from shareholders, while the latter describes RPTs as an

efficient economic exchange.

Existing RPTs studies are more consistent with the conflict of interests theory. For

example, research finds that RPTs are associated with poorer financial reporting quality and

lower operating performance (Berkman, Cole, and Fu 2009; Ryngaert and Thomas 2012).

Research also shows that RPTs relate to weak corporate governance. Denis and Sarin (1999) and

Klein (2002) document that RPTs may undermine non-executive directors’ functions, turning

them into affiliated or gray directors who are not independent anymore, and hence are associated

with weaker corporate governance. Similarly, Kohlbeck and Mayhew (2010) and Gordon, Henry,

and Palia (2004) provide evidence that weaker corporate governance makes RPTs more likely to

occur.7 If RPTs represent the conflict of interests between investors and insiders, then effective

corporate governance should mitigate this conflict.

When studying the corporate governance effects on RPTs, prior literature uses traditional

governance proxies such as the percentage of independent directors on the board. In my study, I

7Nekhili and Cherif (2011) and Lo, Wong, and Firth (2010) find similar associations in France and China, respectively.

9

focus on a more directly relevant measure of RPTs’ governance, namely, the presence of an RPT

governance policy.

Before the 2006 SEC RPT regulation, approximately one fifth of firms voluntarily

disclosed their RPT governance policy. Following the 2006 RPT regulation, all public firms in

the U.S. are required by the SEC to disclose their RPT governance policies. I posit that this

mandatory disclosure has real effects on firms’ behavior and reduces the occurrence of RPTs.

First, under this new regulation, firms are likely to establish formal RPT governance

policies if they did not have one yet, given that the absence of formal RPT governance policies

could lead to scrutiny from investors and regulators. Another benefit for such firms to establish a

new RPT governance policy is the signaling effects. Firms with newly-created RPT policies

could signal to the market of their RPT governance, as compared to those firms that do not have

ex-ante RPT policies and choose not to establish one ex-post. Under the mandatory disclosure

requirement, these latter firms will have to disclose the fact that they do not have a formal RPT

governance policy, making them less desirable in the eyes of investors.

When firms do not have formal RPT governance policy, theoretically they could conduct

any RPTs as long as these transactions are disclosed. If the related parties are able to self-

approve their own transactions, it is likely that they benefit themselves at the cost of other

stakeholders. When a firm has an effective RPT governance policy, the policy potentially aligns

management interests with shareholders’ interests by minimizing harmful RPTs. Hence a more

transparent disclosure of governance policy may constrain the occurrence of harmful RPTs and

mitigate investor concerns regarding the self-dealing effects.

If firms had RPT governance policies but choose not to disclose them before the adoption

of the 2006 SEC regulation, this public disclosure requirement can still enhance their RPT

10

control as it decreases the monitoring cost of investors, increases the litigation risk of responsible

authorities, and therefore encourages the firm to improve the effectiveness of their RPT control,

also leading to a reduction of RPTs.

In sum, a formal RPT governance policy, no matter whether it is newly established or

already in place, could help ex-ante no-disclosure firms (i.e. Newly-Disclosed firms) to reduce

harmful RPTs when the SEC’s new mandatory disclosure requirement is in place, since it

reduces information asymmetry and aligns more with investors’ interests.

On the other hand, it is also possible that RPT governance policies are just window

dressing and do not have any practical impact on the occurrence of RPTs. For example, Enron

had set up a formal procedure to examine the fairness of transactions, yet this procedure did not

prevent Enron from its RPT wrongdoings. In such case, the disclosure of RPT governance policy

would not help firms reduce harmful RPT activities.

Taken together, I expect that, on average, the disclosure of RPT governance policy

reduces the occurrence of RPTs given the potential conflict of interests associated with RPTs.

Therefore, I construct my first hypothesis as follows (all hypotheses are stated in the alternative

form):

H1: The disclosure of RPT governance policy is associated with a lower level of RPTs.

If RPTs represent opportunistic behaviors of insiders, then RPTs are more likely to be

harmful when agency problems are more severe. As agency problems are not only constrained

by corporate governance but also affected by other factors such as industry competition,

ownership structure, and analyst following, I expect that the pressures faced by firms from these

11

external factors can also affect the nature of RPTs. Consequently, I expect the disclosure effects

to be conditional on the environment in which firms operate.

Prior research shows that ownership structure is a factor affecting firms’ behavior. With a

diffused ownership structure, there is a reduced incentive for any individual owner to monitor

corporate management, because the individual owner would bear the entire monitoring cost, yet

all shareholders benefit. As a result, only large non-controlling shareholders, such as institutional

investors, have sufficient incentives and means to monitor firms and limit agency problems

(Shleifer and Vishny 1986; Huddart 1993). Accordingly, firms with low institutional ownership

face lower monitoring pressures and are more likely to involve in harmful RPTs ex-ante.

Consequently, I expect that the ex-post reduction in RPTs is more pronounced for these firms.

H2a: The reduction of RPT occurrence following the initial disclosure of RPT governance is

more pronounced when the proportion of institutional ownership is low.

Equity analysts provide another monitoring mechanism to align insiders’ and

shareholders’ interests (Jensen and Meckling 1976). To increase their market influence and

reputation through timely and reasonable recommendations, analysts exert significant efforts in

examining firms’ strategy, governance, and activities. With scrutiny and attention from more

analysts, insiders face greater risks of negative market reactions or personal reputation damage

when involved in self-dealing transactions. Consequently, I expect that the reduction of RPTs

following disclosure of RPT governance be more pronounced when analyst following is low.

12

H2b: The reduction of RPT occurrence following the initial disclosure of RPT governance is

more pronounced when analyst following is low.

Research also shows that industry competition can put direct pressure on firms and

reduce agency costs (Giroud and Mueller 2011; Baggs and De Bettignies 2007; Jagannathan and

Srinivasan 1999). This is because firms in highly competitive industries are more likely to go

bankruptcy than other firms. This high bankruptcy risk gives managers strong incentives to work

hard to remain competitive, aligning their interests more with shareholders. With respect to RPTs,

these firms are more likely to forgo harmful RPTs and take beneficial RPTs to reduce transaction

costs and improve efficiency, mitigating expected bankruptcy costs. As a result, I expect that

reduction in RPTs following disclosure of RPT governance be more pronounced when industry

competition is weak.

H2c: The reduction of RPT occurrence following the initial disclosure of RPT governance is

more pronounced when industry competition is weak.

The conflict of interests theory suggests that RPTs firms could have higher implied costs

of equity capital for at least two reasons. First, RPTs are associated with poor accounting quality,

increasing information risks. Jian and Wong (2010) find that Chinese listed firms use abnormal

related sales to their controlling owners to prop up earnings. Chen, Cheng, and Xiao (2010) find

that controlling shareholders in China structure RPTs in the pre-IPO period to affect IPO

performance. Using a sample of 360 companies in the U.S., Gordon and Henry (2005) find that

some types of RPTs are associated with higher abnormal accruals. Kohlbeck and Mayhew (2017)

13

show that RPT firms are more likely to restate their financial reports. Similarly, Cullinan, Du,

and Wright (2006) document a significant association between executive loans and financial

misstatements. The literature shows that information risks are associated with higher cost of

equity both theoretically (Easley and O’Hara 2004; Lambert et al. 2007) and empirically (e.g.,

Francis et al. 2005).

Second, many RPTs are associated with poor corporate governance (Denis and Sarin

1999; Klein 2002; Gordon, Henry and Palia 2004). There is also evidence that insiders can use

RPTs to directly expropriate wealth from other investors. For example, Cheung, Qi, Rau, and

Stouraitis (2009) examine 254 related-party acquisitions and sales of assets in Hong Kong and

find that firms pay higher prices when purchasing from related parties and receive lower prices

when selling to related parties. Kahle and Shastri (2004) show that the loans made to executives

are usually issued at below-market interest rates. Consistent with these studies, the stock market

reacts negatively to RPTs (Cheung, Rau, and Stouraitis 2006; Ryngaert and Thomas 2012;

Kohlbeck and Mayhew 2010). This concern of expropriation could also increase the

investigation risk from SEC and litigation risk through conflict of interests lawsuits.8,9

Disclosure of RPT governance policy could mitigate the relation between RPTs and the

implied cost of capital. When firms withhold information, rational investors tend to assume the

worst scenario and increase the risk premium (Grossman 1981). Cheynel’s (2013) model

predicates that firms that voluntarily disclose their information have lower cost of equity capital

than firms that do not disclose. Lambert, Leuz, and Verrecchia’s (2007) model demonstrates that

8 For example, in October of 2015, the SEC charged Home Loan Servicing Solutions Ltd. (HLSS) with making material misstatements about its handling of related party transactions and for having inadequate internal accounting controls. HLSS agreed to pay a $1.5 million penalty to settle the SEC’s charges. 9 For example, in June 2016, Tesla Motors Inc. proposed a $2.6 billion merger with a related party, SolarCity Corp. Two individuals and two institutional shareholders of Tesla filled four lawsuits alleging board members breached their fiduciary duty.

14

disclosure can affect the cost of capital because higher quality disclosures affect the firm’s

assessed covariance with other firms’ cash flows, which is non-diversifiable. In addition, they

show that disclosure can affect a firm’s real decisions, which likely changes the firm’s ratio of

the expected future cash flows to the covariance of these cash flows with the sum of all the cash

flows in the market. Numerous empirical studies support such predictions (Botosan 1997; Lang,

Lins, and Maffett 2012).

When firms disclose their RPT governance policies, I expect that this behavior affects the

implied cost of capital through two channels: an information channel and a governance channel.

Through the information channel, a disclosure of RPT policy can provide investors with more

information regarding how firms control their RPTs, reducing the information asymmetry

premium between firms and investors. In such a case, investors are able to assess the

consequence of RPTs with less uncertainty.

Through the governance channel, a disclosure of RPT governance could improve firms’

governance and reduce harmful RPTs, mitigating the conflict of interests between insiders and

outsiders. Less risk of both expropriation and consequent litigation could also reduce the cost of

capital associated with RPTs. Therefore, my third hypothesis is:

H3: The initial disclosure of RPT governance policy is associated with lower implied costs of

capital associated with RPTs.

15

3. Data and Research Design

3.1 Related-party transaction data

I hand-collect RPT data and RPT governance data from S&P 1500 firms’ proxy

statements on the SEC’s website for 2004, 2007, and 2010. Following Kohlbeck and Mayhew

(2017), I choose every three years rather than consecutive years because this design allows for

changes in RPTs to occur, as many RPTs are sticky transactions that involve multiple years. I

start from 2004 because post-SOX period data can mitigate the SOX impact on corporate

governance and RPT disclosures. I choose 2010 as the last year of data collection, believing that

the three-year data are sufficient to study the effects of RPT policy disclosures. I focus on S&P

1500 because these firms cover approximately 90% of the U.S. market capitalization.

Out of the 1500 S&P composite firms, I exclude 430 financial firms, resulting in 3,210

firm-year observations for which proxy statements are available to identify whether or not the

firm reported RPTs. After removing firms with missing data, my final sample includes 2,850

firm-year observations.

RPTs can be measured by either the number of transactions or the amount of transactions.

In my main analyses, I adopt the number of RPTs as I consider that several small RPT

transactions likely reflect more severe agency problems than a single larger transaction if the

aggregate transaction amounts are similar. However, in additional analyses I use the transaction

amount of RPTs as an alternative measurement.

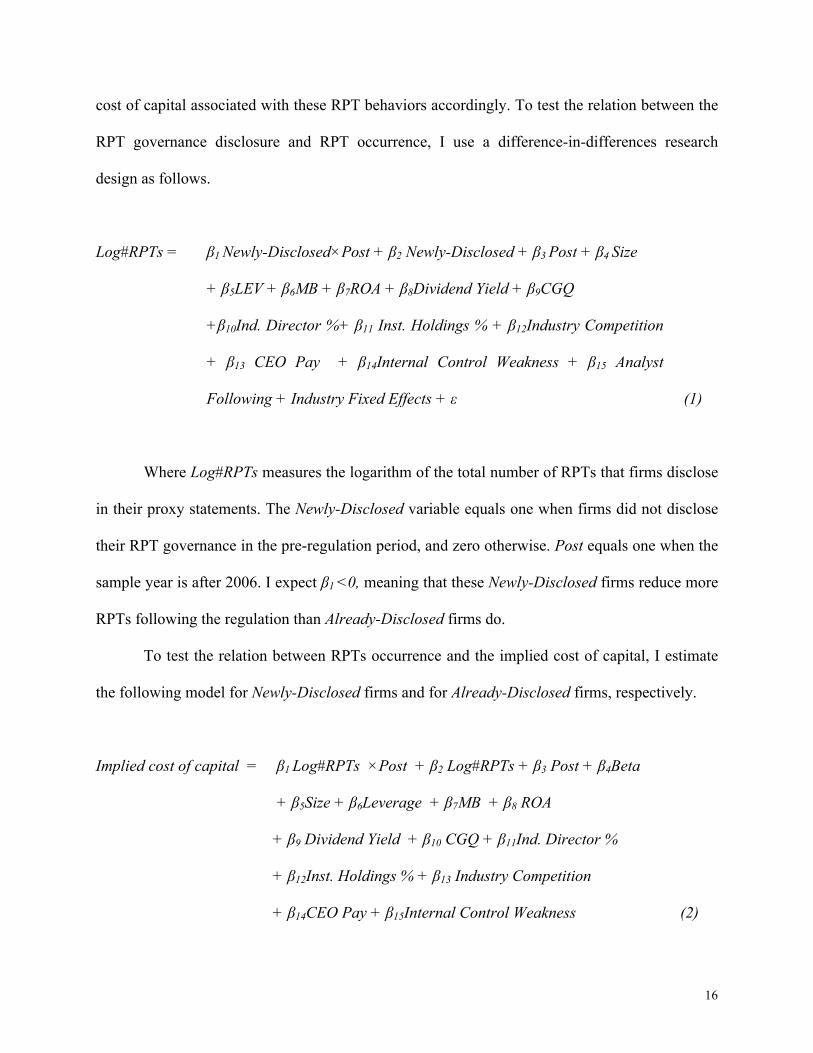

3.2 Regression model

The objective of this paper is to examine whether firms change their RPT behavior in

response to the mandated RPT governance disclosure and whether investors update the implied

16

cost of capital associated with these RPT behaviors accordingly. To test the relation between the

RPT governance disclosure and RPT occurrence, I use a difference-in-differences research

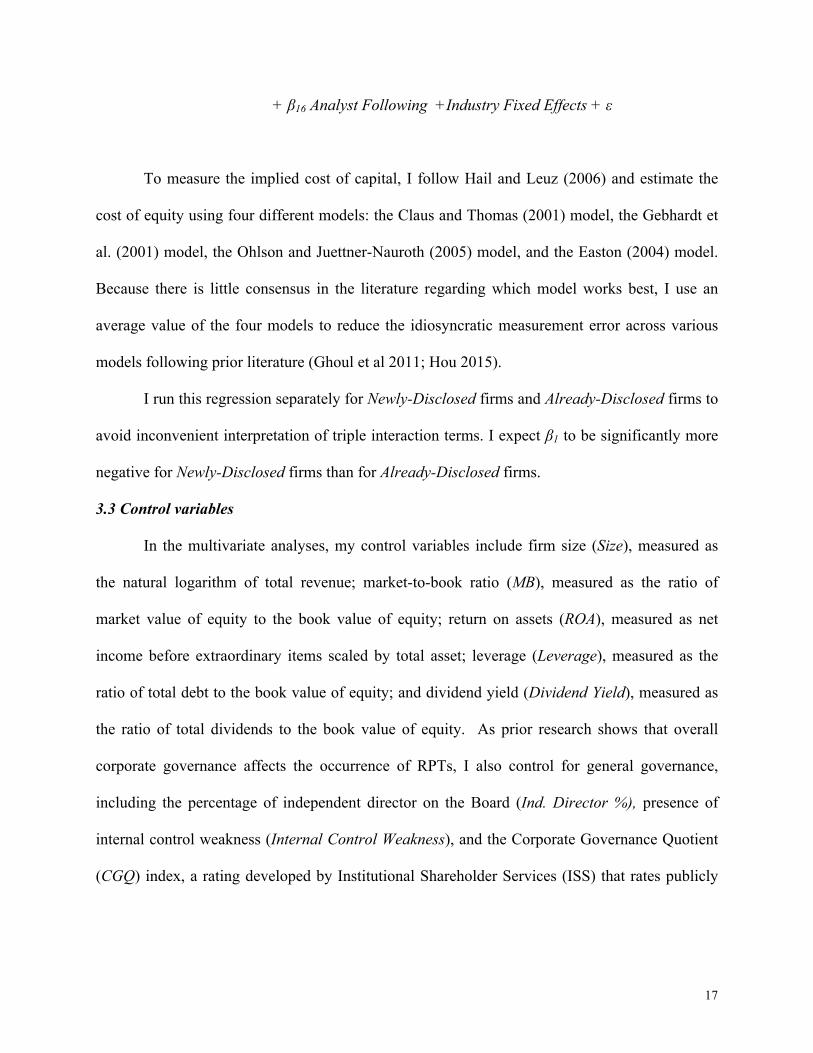

+ β16 Analyst Following +Industry Fixed Effects + ε

To measure the implied cost of capital, I follow Hail and Leuz (2006) and estimate the

cost of equity using four different models: the Claus and Thomas (2001) model, the Gebhardt et

al. (2001) model, the Ohlson and Juettner-Nauroth (2005) model, and the Easton (2004) model.

Because there is little consensus in the literature regarding which model works best, I use an

average value of the four models to reduce the idiosyncratic measurement error across various

models following prior literature (Ghoul et al 2011; Hou 2015).

I run this regression separately for Newly-Disclosed firms and Already-Disclosed firms to

avoid inconvenient interpretation of triple interaction terms. I expect β1 to be significantly more

negative for Newly-Disclosed firms than for Already-Disclosed firms.

3.3 Control variables

In the multivariate analyses, my control variables include firm size (Size), measured as

the natural logarithm of total revenue; market-to-book ratio (MB), measured as the ratio of

market value of equity to the book value of equity; return on assets (ROA), measured as net

income before extraordinary items scaled by total asset; leverage (Leverage), measured as the

ratio of total debt to the book value of equity; and dividend yield (Dividend Yield), measured as

the ratio of total dividends to the book value of equity. As prior research shows that overall

corporate governance affects the occurrence of RPTs, I also control for general governance,

including the percentage of independent director on the Board (Ind. Director %), presence of

internal control weakness (Internal Control Weakness), and the Corporate Governance Quotient

(CGQ) index, a rating developed by Institutional Shareholder Services (ISS) that rates publicly

18

traded companies in terms of the quality of their corporate governance.10 A higher CGQ implies

stronger corporate governance. To control for external monitoring factors affecting opportunistic

behaviors, I include institutional ownership (Inst. Holdings %), measured as percentage of shares

owned by institutional investors, industry competition (Industry Competition), measured as the

Herfindahl-Hirschman Index of industry market share, and analyst following (Analyst following),

measured as the number of analysts following the firm. I also control for CEO compensation

(CEO PAY), measured as the natural logarithm of total CEO annual compensation scaled by firm

size. In addition, I control for Beta in the analysis of risk associated with RPT. Finally, all

regressions include Fama-French 48 industry fixed effects to control for heterogeneity at the

industry level and error clustering at the firm level.

10 This CGQ index measures the overall corporate governance relative to a firm’s industry group. Ratings are calculated on the basis of 61 data points from eight core categories: (1) Board of directors, (2) audit, (3) charter and bylaw provision, (4) laws of the state of incorporation, (5) executive and director compensation, (6) qualitative factors, (7) ownership, and (8) director education.

19

4. Empirical Results

4.1 Descriptive statistics

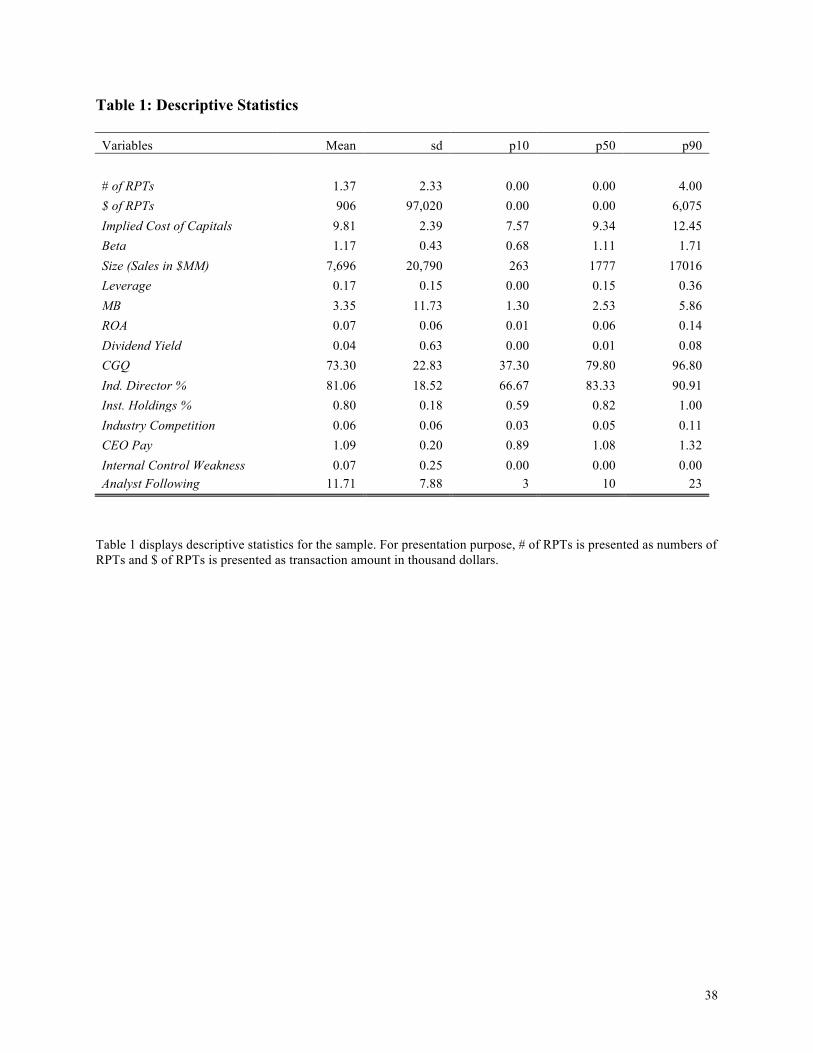

Table 1 provides descriptive statistics. On average each firm-year observation reports

1.37 related-party transactions. The mean implied cost of capital is 9.8% and the average beta is

1.17, slightly above the market average. The average revenue is $7.5 billion and the average

leverage is 0.17. The mean of the governance score (CGQ) is 73 compared to an industry

average score of 50, reflecting that my sample firms are better governed than their industry peers.

The percentage of independent directors is 81% and the percentage of average institutional

holdings is 80%, showing that both internal and external monitoring in my sample firms are

relatively strong.

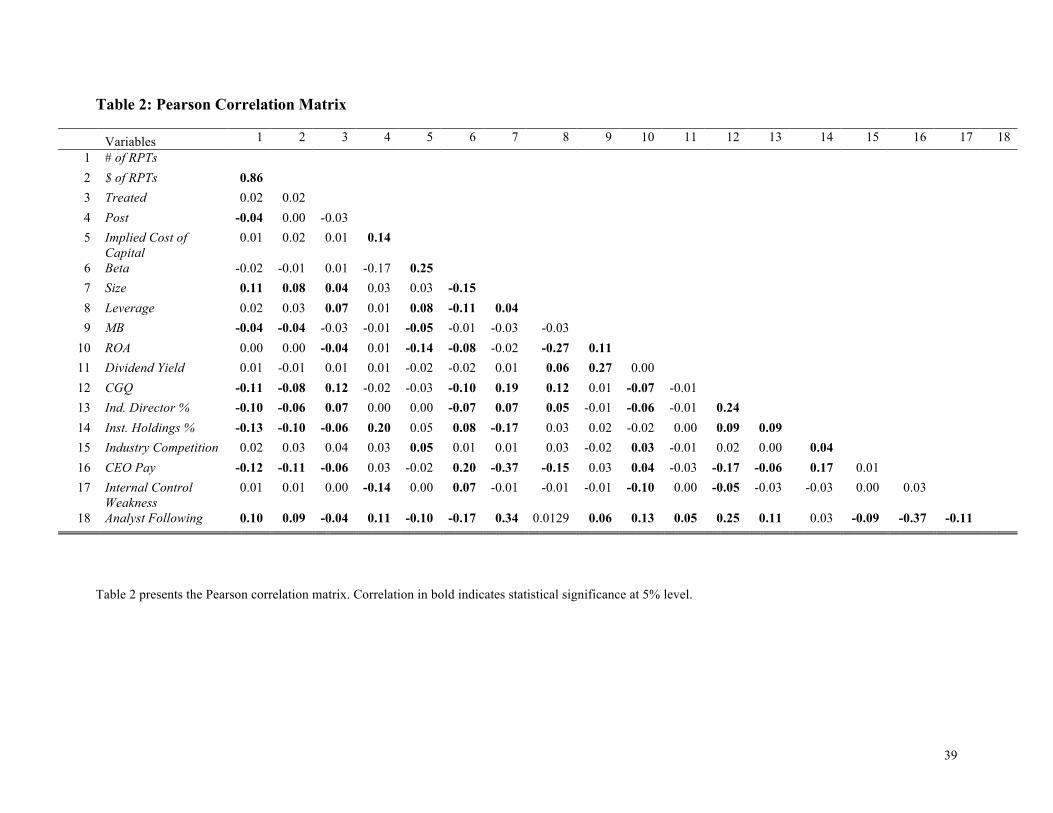

Table 2 reports the Pearson correlations and shows that firms that are larger, have higher

leverage, have lower market-to-book ratios, and are poorly governed tend to report more RPTs.

In addition, I do not find high correlations between the explanatory variables, suggesting

multicollinearity is not a serious concern in my analyses.

4.2 Primary Analyses

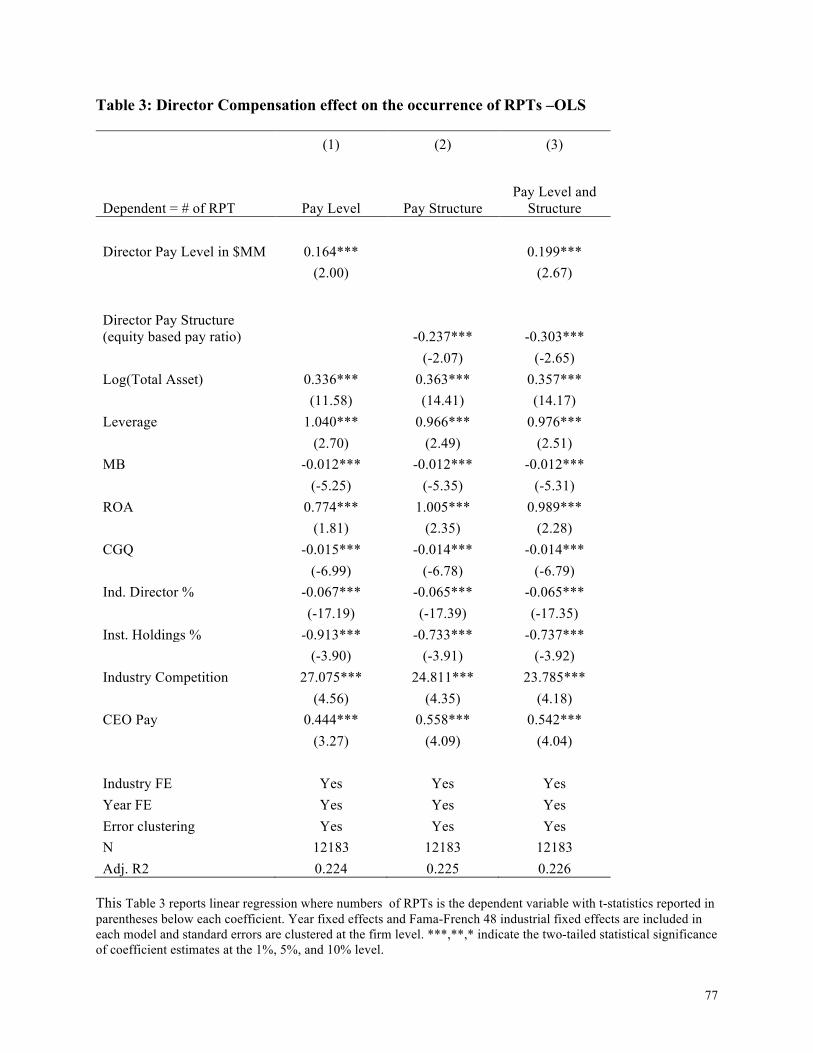

4.2.1 RPT governance disclosure and occurrence of RPTs

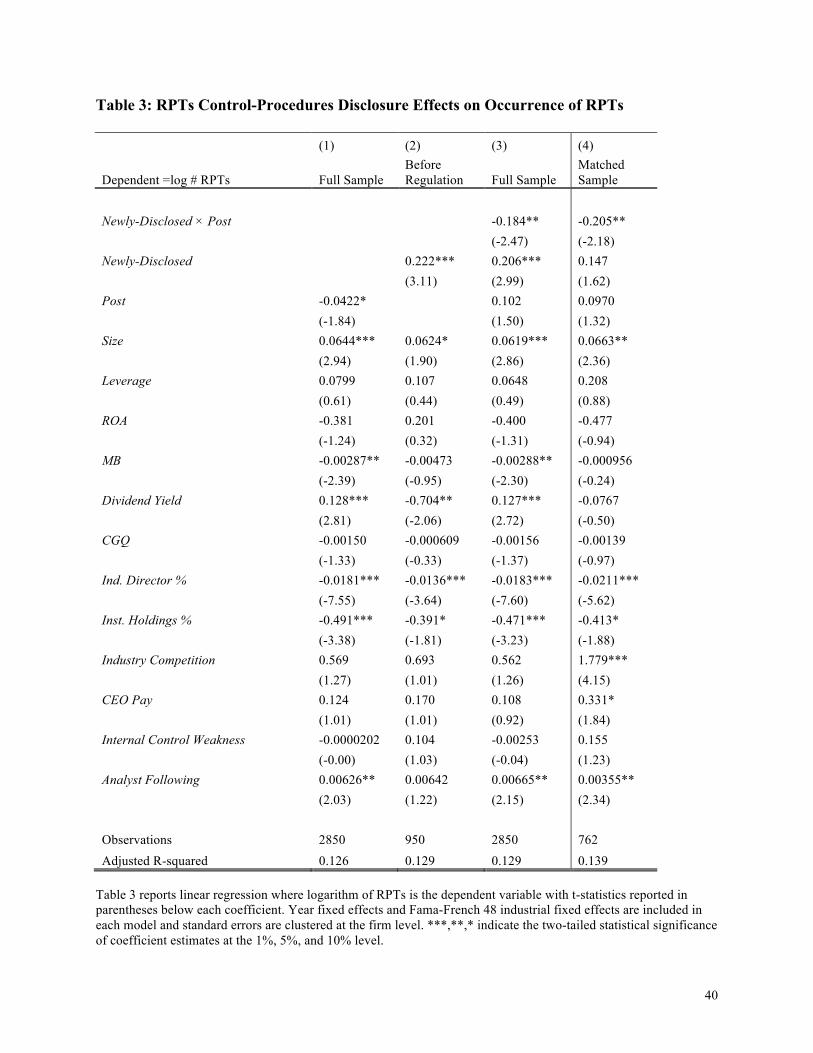

I begin my empirical analysis by examining whether disclosures of RPT governance

affect the occurrence of RPTs in Table 3. In Column 1, I regress the number of RPTs on Post

while controlling for other firm characteristics and fixed effects. The coefficient on Post is -0.04

(significant at the 10% level using a two-sided test), providing preliminary support for the 2006

SEC regulation effectively reducing the occurrence of RPTs.

20

In Column 2, I examine whether RPT governance disclosure is associated with fewer

RPTs in the pre-regulation period. The coefficient on Newly-Disclosed firms is 0.22 and is

significant at the 1% level, showing that Newly-Disclosed firms have more RPTs than Already-

Disclosed firms in the pre-regulation period. When RPT governance disclosure is voluntary, the

Newly-Disclosed firms report significantly more RPTs than Already-Disclosed firms.

In Column 3, I conduct a difference-in-differences analysis around the 2006 SEC

regulation. The interaction term of Newly-Disclosed and Post is negative and significant at the 5%

level, implying that compared with Already-Disclosed firms, the reduction of RPTs is more

salient for Newly-Disclosed firms.

The above analysis suggests that the RPT governance disclosure affects the occurrences

of RPTs, consistent with H1. One possible concern is that Already-Disclosed firms may be

fundamentally different from Newly-Disclosed firms. Including numerous firm characteristics

and fixed effects in the regression may not be sufficient to control for such pre-existing

differences. To better separate out the treatment effects, I use propensity-score matching to

match samples by firm characteristics and redo the analysis in Column 4.11 Using this balanced

panel, I continue to find that Newly-Disclosed firms reduce more RPTs than Already-Disclosed

firms in the post-regulation period, consistent with prior findings.

The signs of control variables are consistent with expectations. Larger firms tend to have

more RPTs than small firms, because larger firms tend to have more related parties and their

business is more complicated. The coefficient on MB is negative, consistent with the perception

that related-party firms are valued lower by the market. Finally, the corporate governance

measurements are negatively related to RPTs.

11 In this PSM, I first run a logistic regression of RPT governance disclosure on all control variables to obtain the propensity score. Then I match the treatment group sample (i.e. Newly-Disclosed Firms) with the control group sample (i.e. Already-Disclosed Firms) with a caliper matching set at 0.1.

21

In sum, the analyses show that the disclosure of RPT governance significantly reduces

the occurrence of RPTs even after controlling for traditional internal and external monitoring

mechanisms.

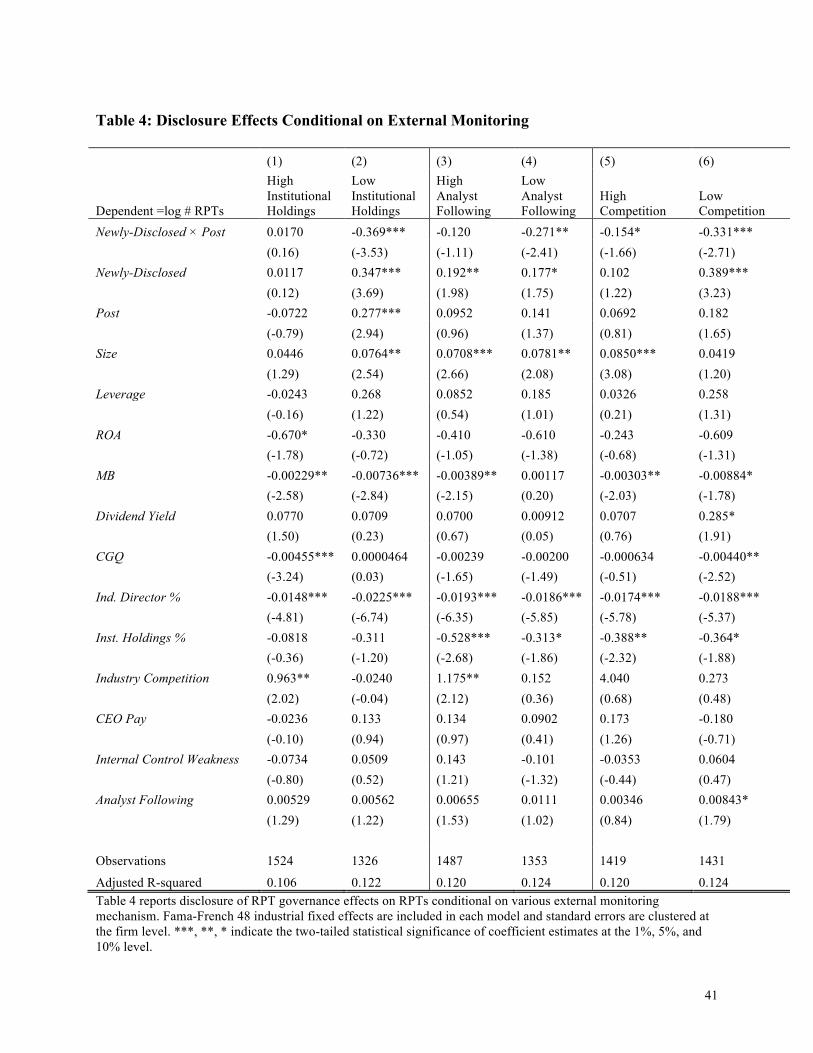

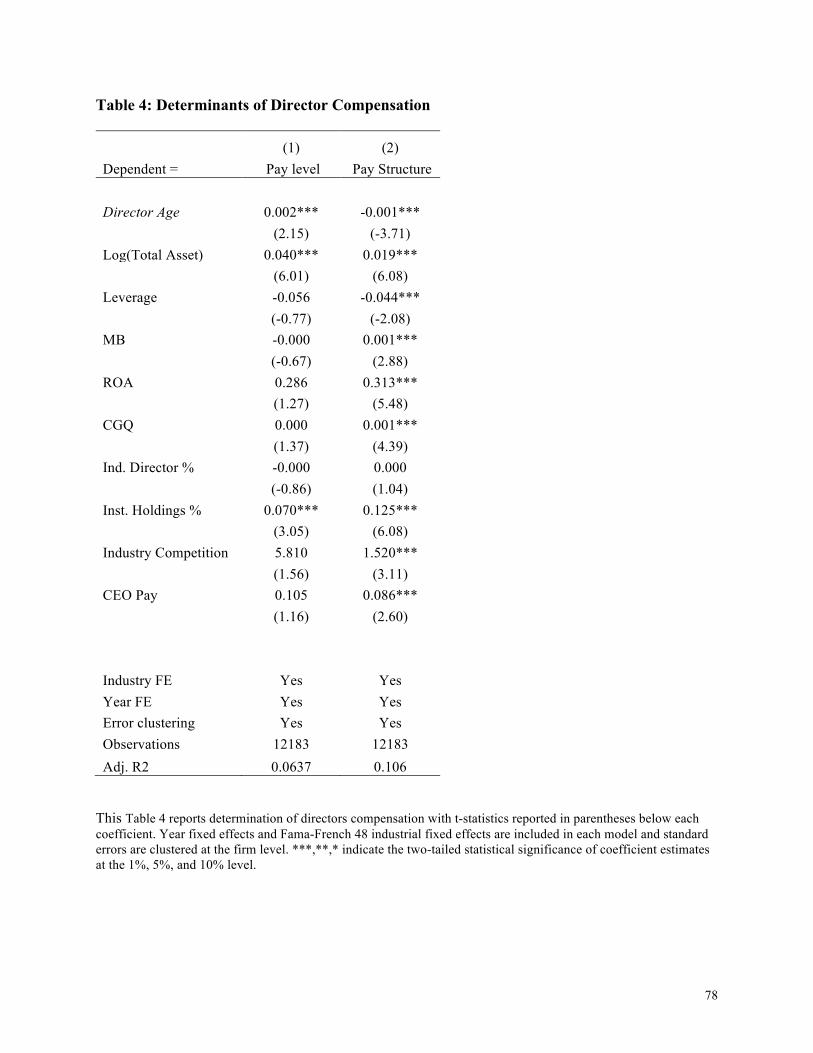

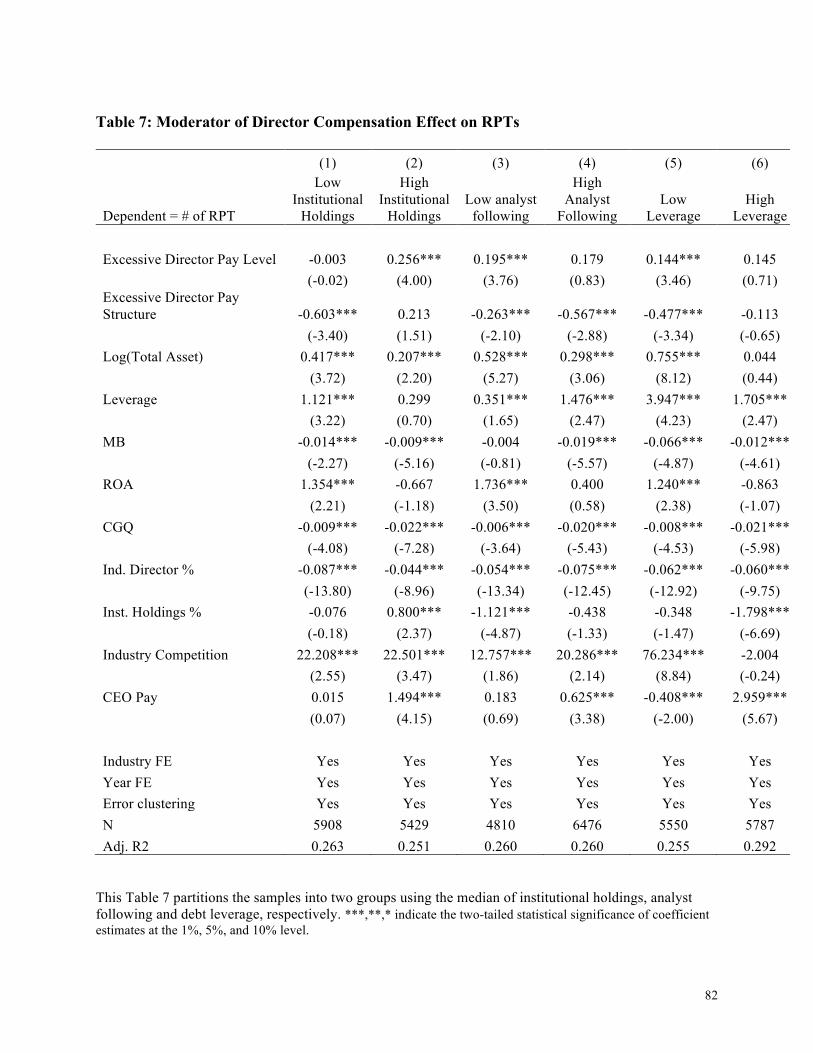

4.2.2 RPT governance disclosure effects conditional on potential agency costs

In this section, I examine under which conditions the regulation effects are more

pronounced. Because RPTs can reflect a conflict of interests, and the disclosure of RPT

governance potentially mitigates the potential risks associated with RPTs, I expect that the

effects of RPT governance disclosure are conditional on agency costs. I choose three

In Columns 1 and 2 of Table 4, I partition sample firms into high and low institutional

ownership by the median of the sample and rerun model (1) for each group. The estimated

coefficients on Newly-Disclosed and Post and the interaction of Newly-Disclosed and Post are

not significant in Column 1, suggesting that the disclosure of RPT governance has little effect on

the occurrence of RPTs when institutional holdings are high. In Column 2 where the outcomes

for low institutional ownership group is presented, I find that the coefficients on the interaction

of Newly-Disclosed and Post are significant and negative, suggesting the effects of RPT

disclosure governance concentrate on firms with low institutional ownership. The coefficient

difference between high and low institutional holding firms (using a fully-interacted model) is

significant at the 5% level.

In Columns 3 and 4 of Table 4, I partition the sample by the median of the number of

analysts following the firm. Columns 3 and 4 represent the analysis for firms with high and low

analyst following, respectively. The results show that the coefficients on the interaction of

22

Newly-Disclosed and Post are negative and significant for the low analyst following group but

not for the high analyst following group, and that the difference between the two is statistically

different. Comparing the results between the two groups, I find that when there are fewer

analysts following the firm, the mandatory disclosure of RPT governance is more likely to affect

the occurrence of RPTs.

In Columns 5 and 6, I examine whether these disclosure effects are influenced by

industry competition.12 The results show that the association between mandatory disclosure of

RPT governance and reduction of RPTs is stronger when there is less competition, consistent

with the argument that potential agency costs can alter RPT governance disclosure effects on

RPTs.

In sum, Table 4 shows the effects of RPT governance disclosure are more pronounced

when institutional holdings and analyst following are low, and when industry competition is

weak. The findings are consistent with the H2 that the disclosure effects are stronger in situations

with potentially high agency costs.

12 Industry competition is measured by the Herfindahl index using revenues in each Fama-French 48 industry.

23

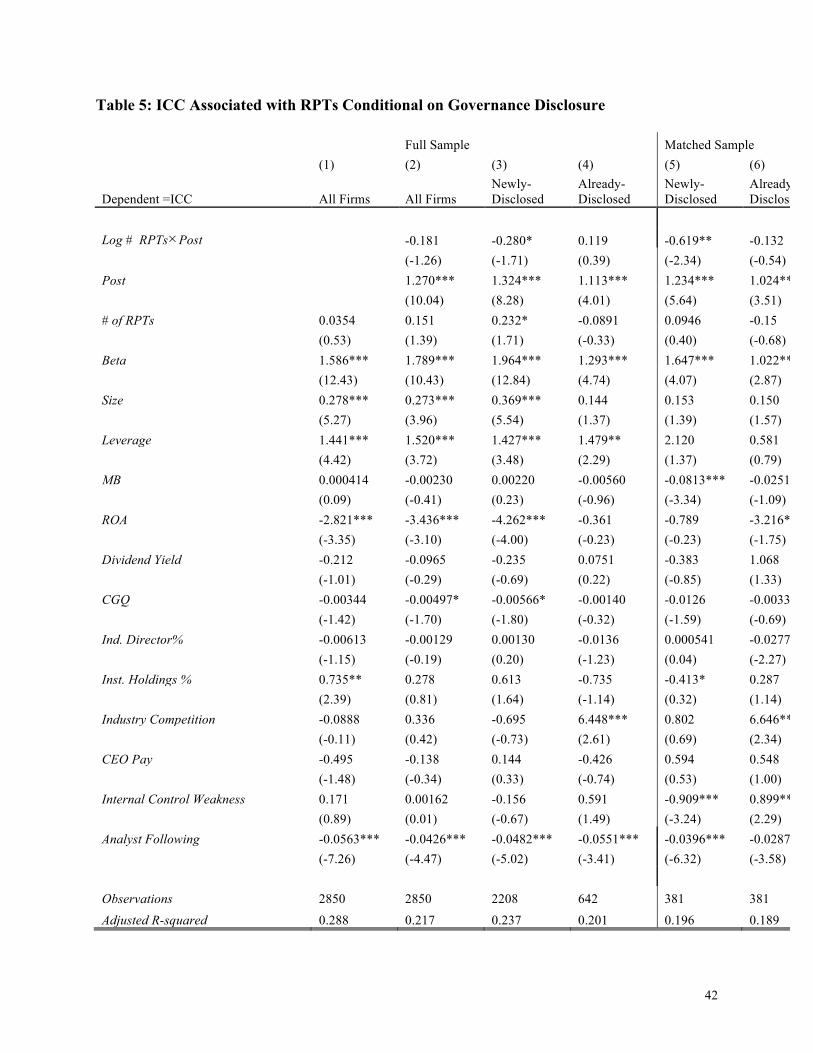

4.2.3 RPT governance disclosure and the implied cost of capital

Having shown that firms change their RPT behaviors following the 2006 regulation, I

next examine whether investors recognize this change. To examine the impact of the regulation

on the implied cost of capital associated with RPTs, I regress the average implied cost of capital

on the log number of RPTs. In Columns 1 and 2 of Table 5, I run a cross-sectional regression

using pooled data, and find that the occurrence of RPTs does not have a significant impact on

firms’ implied cost of equity capital either before or after the 2006 regulation, suggesting that on

average, the investors do not put an implied costs of capital associated with RPTs.

Investors, however, may have different RPT perceptions on Newly-Disclosed and

Already-Disclosed firms. In Columns 3 and 4, I partition the sample into Newly-Disclosed and

Already-Disclosed firms to compare the regulation effects between the two groups. In Column 3,

the coefficient on log#RPTs×Post is significantly negative, consistent with a decrease in RPT

risk premium for Newly-Disclosed firms in the post-regulation period. In Column 4, I find that

for Already-Disclosed firms, the risk premium does not significantly change in the post-

regulation period, suggesting the regulation does not have a significant impact on this group. The

results in Columns 3 and 4 are statistically different at the 10% level using two-sided tests,

supporting the argument that disclosure of RPT governance does affect the risk premium that

investors attach to RPTs. The 2006 mandatory disclosure regulation has virtually no impact on

Already-Disclosed firms, yet has a significant impact on Newly-Disclosed firms, suggesting that

investors perceive reduced risk when more risk-related information of RPTs is disclosed.

Analysis using the propensity-score matched sample in Columns 5 and 6 affirm and strengthen

the findings.

24

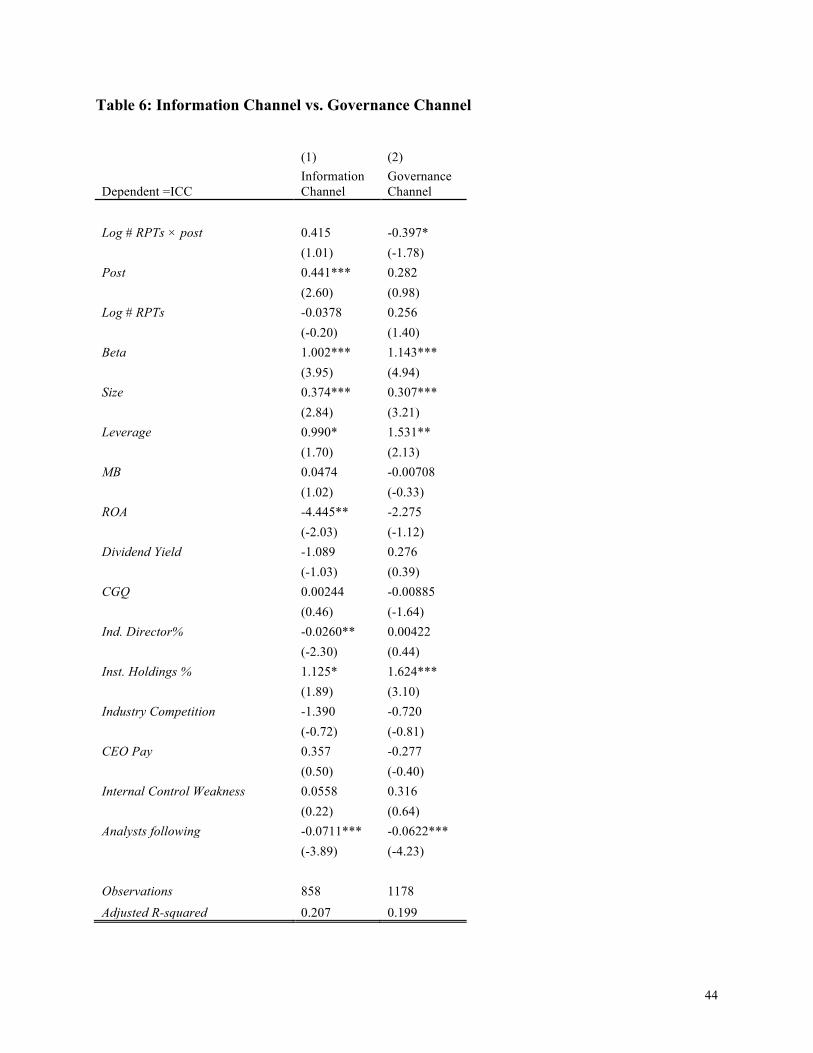

As argued in hypothesis development section, the reduction of implied cost of capital

associated with RPTs can be achieved through an information channel, that is, reducing

information asymmetry, or a governance channel, that is, reducing harmful RPTs. To distinguish

the information channel from the governance channel, I separate Newly-Disclosed firms that did

not change their RPT behaviors in 2007 from those Newly-Disclosed firms that changed their

RPT behaviors in 2007. I argue that for those Newly-Disclosed firms that did not change their

RPT behaviors, reduction in the implied cost of capital, if any, can be mainly attributed to the

effect of the information channel. For those Newly-Disclosed firms that change their RPT

behavior, reduction in the implied cost of capital can be attributed to a joint effect of the

information channel and the governance channel.

Approximately 55% of Newly-Disclosed firms changed their RPT behaviors after the

SEC regulation. For firms that do not change their RPT behavior, Column 1 in Table 6 shows

that the implied cost of capital associated with RPTs does not change, suggesting that the

information channel is likely not the main channel through which RPT policy disclosure affects

the implied cost of capital. By contrast, Column 2 shows that for firms that change their RPT

behaviors, the implied cost of capital associated with RPTs drops significantly. Thus� the

analyses in Table 6 suggest that the governance channel is likely to be the main channel leading

to a lower cost of capital associated with RPTs after the regulation.

4. 3 Robustness Tests

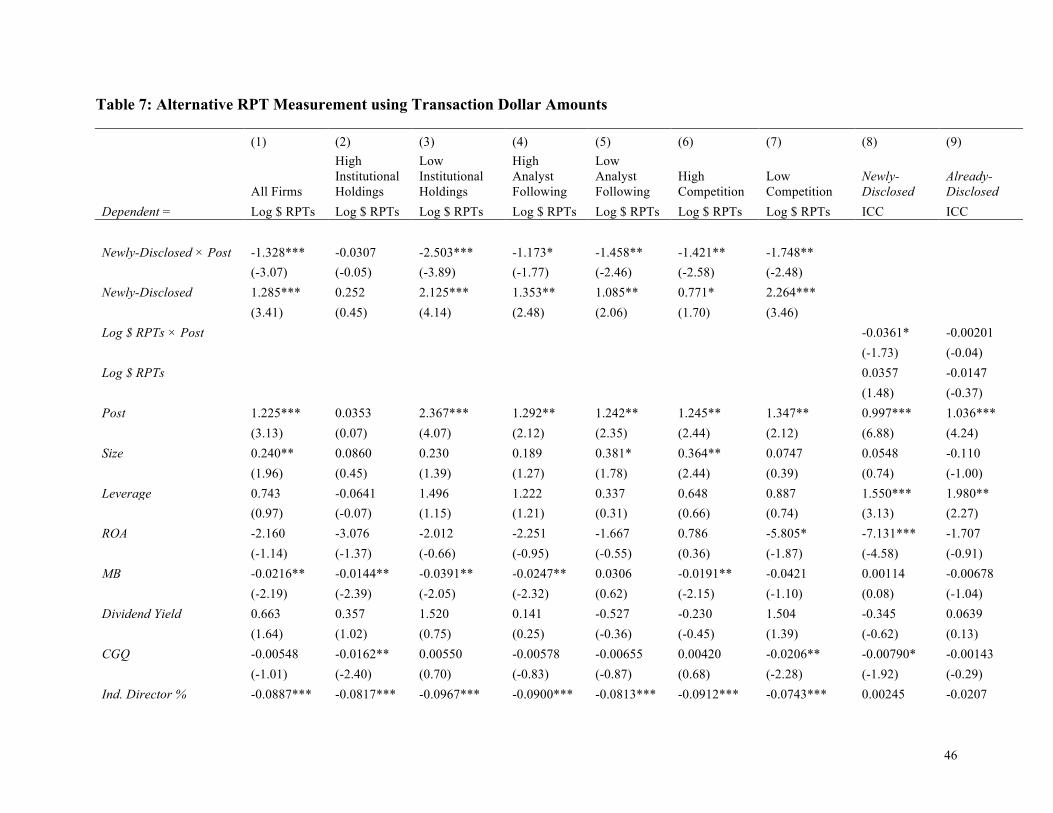

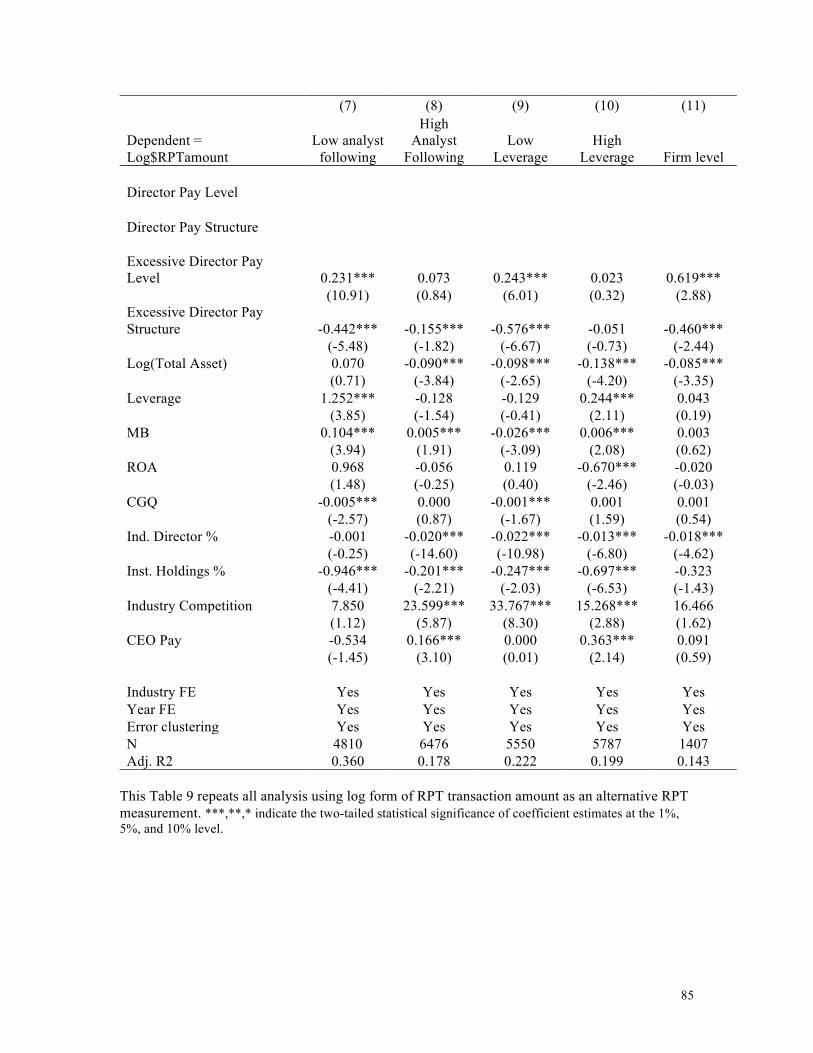

4.3.1 Alternative measure of RPTs

RPTs can alternatively be measured by transaction amount. In Table 7, I test my main

hypothesis using transaction amount. In Columns 1 to 7, the dependent variable is the logarithm

25

of the total transaction amount. The analyses show that the interaction of Newly-Disclosed and

Post is negative and significant, suggesting that this mandatory disclosure significantly reduces

Newly-Disclosed firms’ RPT transaction amount relative to Already-Disclosed firms. The results

of cross-sectional analyses are consistent with prior findings that the disclosure effects are more

pronounced when potential agency costs are high. In Columns 8 and 9, the dependent variable is

the implied cost of capital. Results indicate that Newly-Disclosed firms significantly reduce the

implied costs of capital associated with RPTs in the post-regulation period compared to Already-

Disclosed firms.

4.3.2 Regulation effects on Already-Disclosed firms

One potential concern of the difference-in-differences tests is that the 2006 regulation

could also affect the Already-Disclosed firms, disqualifying them as valid control firms. That is,

some Already-Disclosed firms may increase the disclosure level of their RPT governance

following the regulation. To mitigate this concern, I measure the disclosure level of RPT

governance based on information that firms provide in their RPT governance disclosure.

Specifically, for each RPT governance disclosure, I identify whether and how the company

discloses each of the following seven items: (1) a written RPT policy; (2) a specified RPT review

and approval committee; (3) involvement of General Counsel or legal department; (4) annual

questionnaire to Director and Officer; (5) types of transactions covered by such policy; (6)

transaction threshold submitting to approval authority; and (7) exemptions of any transactions.

Based on this information, I identify 52 Already-Disclosed firms that disclosed the same level of

RPT governance in the post period as in the pre-period, and use these 52 Already-Disclosed

firms as an alternative control sample. Table 8 reports the results. Column 1 is for the Already-

Disclosed firms that do not change their disclosure on RPT governance after the regulation.

26

Column 2 is for the Already-Disclosed firms that change their disclosure on RPT governance

following regulation. Column 3 is for the firms that initiate RPT governance disclosure following

regulation (i.e., Newly-Disclosed firms). Consistent with my main analyses in Table 3, the

coefficients on Post in Column1 and Column 2 are not significant, showing that the regulation

has little effects on RPT behavior of Already-Disclosed firms. In contrast, the coefficient in

Column 3 is negative and significant, indicating that the regulation a has a significant impact on

RPT behaviors of Newly-Disclosed firms. Additionally, the coefficients between Column 3 and

Column 1 are significantly different, suggesting that initiation of RPT governance disclosure

leads to significantly lower levels of RPTs.

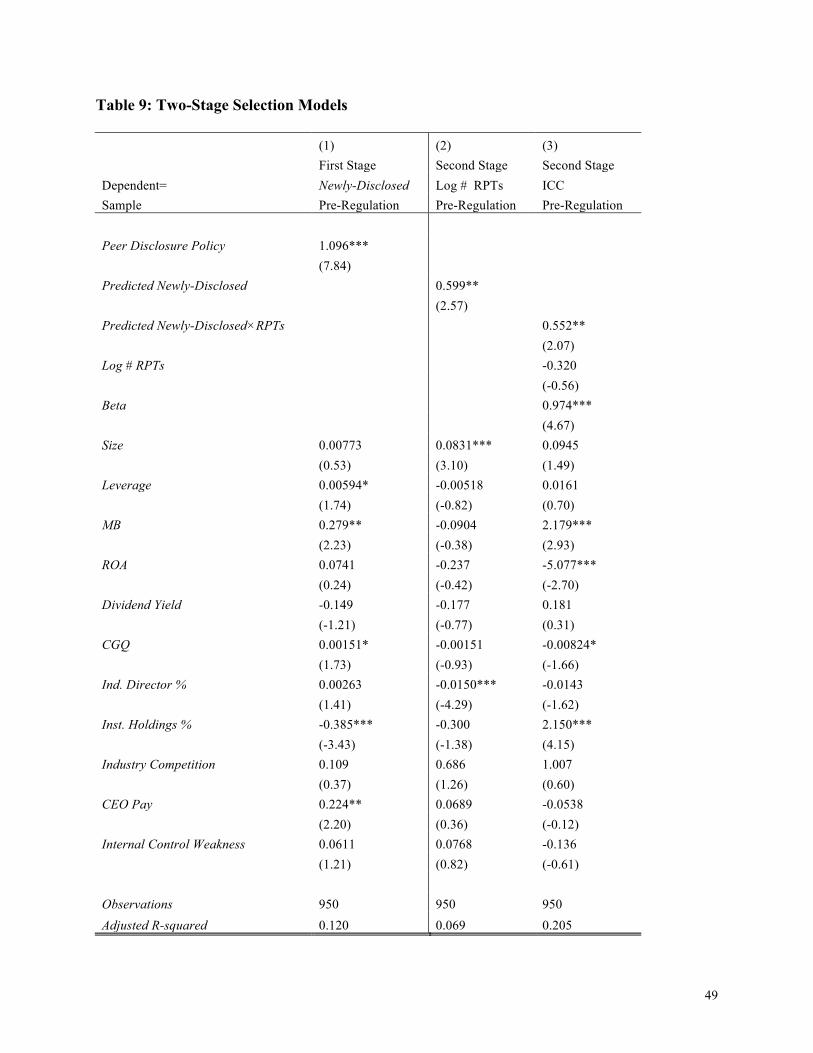

4.3.3 Two-stage selection model

In the pre-regulation period, the decision to disclose RPT governance could be

endogenous and driven by unobservable variables. As a result, the analysis in the Column 2

Table 3 could suffer from self-selection bias. To address this possibility, I use a two-stage

selection model (2SLS). The approach involves a two-stage estimation: the first stage predicts

the decision on whether to voluntarily disclose RPT governance, and the second stage explains

the disclosure of RPT governance and its economic consequences.

The validity of the selection model depends on the validity of exogenous independent

variables from the first-stage choice model that are excluded from the set of independent

variables in the second-stage regression. To effectively control a firm’s decision on whether or

not to disclose RPT governance, I identify its peers’ RPT governance disclosure decision as the

exclusion restriction.13 Specifically, I expect that whether a firm discloses its RPT governance is

partially affected by its peers’ decisions. If its peers have disclosed their RPT governance, the

13 Previous papers have also used as instruments the industry median/mean of the independent variable (Nevo 2000; Friedberg 2003; Hanlon, Rajgopal, and Shevlin 2003; Cheng, Ioannou and Serafeim 2014).

27

firm is more likely to disclose its RPT governance. The peer decisions, however, is not likely to

affect the firm’s occurrence of RPTs if the incurred RPTs are not with these peers.

To capture peer firms’ RPT governance disclosure decision, I use the industry average of

RPT governance disclosure, excluding the firm itself. Table 9 reports this 2SLS analysis before

2006. In Column 1, I regress a firm’s own RPT governance disclosure on its peers’ RPT

governance disclosure, controlling for other firm characteristics and industry fixed effects. The

analysis shows that the likelihood of a firm’s RPT governance disclosure is highly associated

with its peers’ decisions. In Columns 2 and 3, I regress the log number of RPTs and the implied

cost of capital using the predicted value of RPT governance disclosure from the selection model

(Column 1), respectively. I find a positive and significant coefficient on Newly-Disclosed firms,

suggesting an association between RPT governance disclosure and both the occurrence of RPTs

and the cost of capital associated with RPTs.

Overall, the 2SLS analysis suggests that firms voluntarily disclosing RPT governance in

the pre-regulation period report fewer RPTs and that these RPTs are associated with a lower

implied cost of capital, after controlling for self-selection bias.

28

4.3.4 News coverage effects on RPTs

Another factor that may influence the regulation effects is news coverage, as firms face

external monitoring from the media. It is possible that after the 2006 SEC regulation, the media

reports RPTs unevenly for Already-Disclosed firms and for Newly-Disclosed firms, leading to

different levels of monitoring for the two groups. To rule out this alternative explanation, I

search newspapers from 2003 to 2011 in LexisNexis and find 192 RPT news reports covering 82

firms in total�15 of which are S&P1500 composite firms. Excluding these 15 firms from my

sample, I find that no inferences are affected.

4.3.5 Measurement of CGQ on regulation effects

CGQ is a governance rating measurement developed by Institutional Shareholder

Services for public companies. Related-party transactions are one of the 61 rating factors.

Including CGQ as a control variable may affect the estimate of regulation effects on firms’ RPT

behavior. Therefore, I run my analyses excluding CGQ. Results still hold.

4.3.6 Effect of increased disclosure threshold of RPT

Besides the mandatory disclosure requirement of RPT policy and procedure, the SEC

2006 regulation also increases the reporting threshold of RPT from $60,000 to $120,000 to

reflect the inflation. Many firms, however, still report RPTs below the threshold. In 2007, for

example, approximately 18% of reported RPTs was below $120,000. To mitigate the concern

that a higher threshold leads to a drop of reported RPT, in untabulated analyses I exclude these

RPTs below $120,000 for the whole testing period (i.e. from 2004 to 2010) and redo the analyses.

Results sill hold.

29

4.4 Additional Analyses

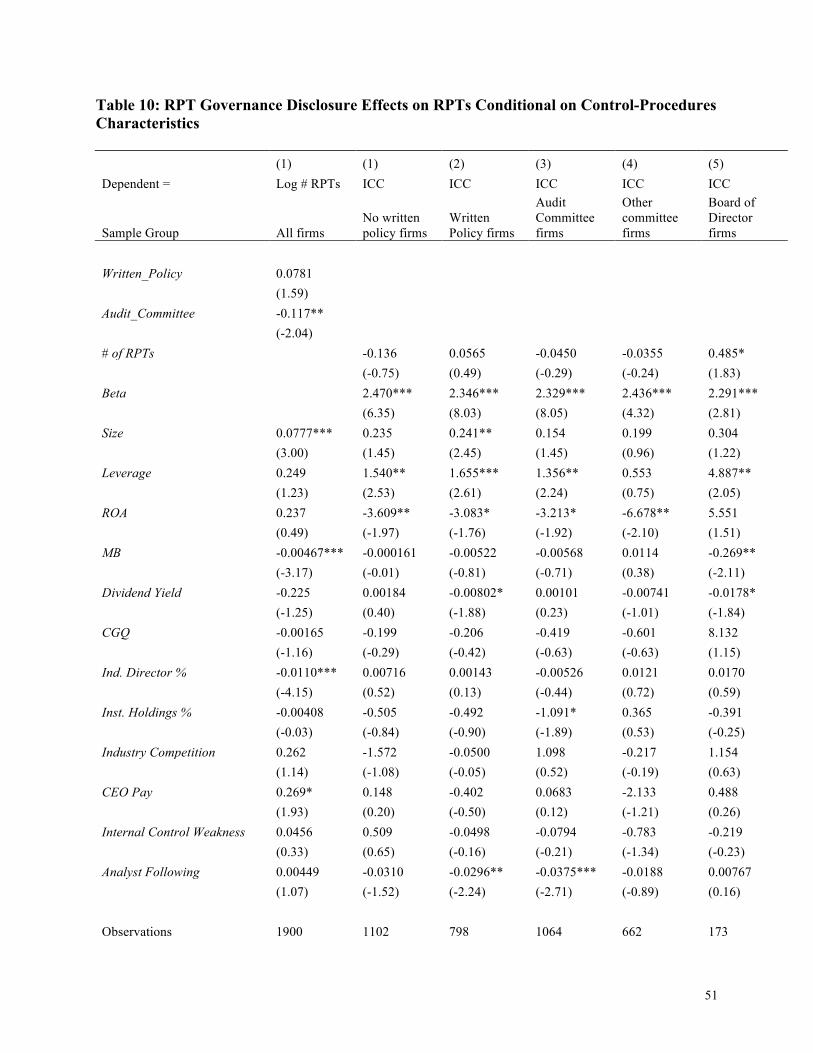

4.4.1 Policy characteristics and RPTs

RPT governance differs among companies along two main dimensions. The first is

whether firms adopt formal written RPT governance policies. In my sample, 42% of firms

explicitly state that they have adopted written policies. The second is who is responsible for the

review and approval of RPTs. In my sample, 56% of firms delegate the Audit Committee to

review and approve RPTs, 35% use other committees such as the Compensation, Governance, or

Risk Committees, and 9% simply say that the Board of Directors is responsible for reviewing

and approving RPTs.

Table 10 reports the breakdown analysis on the above two distinctive RPT governance

characteristics/dimensions. In Column 1, I regress the number of RPTs on whether the firm

adopts a formal written RPT policy and whether an audit committee is used to review and

approve RPTs. Related to the first distinction, I find that the presence of an RPT written policy

does not affect the occurrence of RPTs. A plausible explanation is that for firms without a

separate written RPT governance policy, they usually specify their RPT governance in the Code

of Conduct or in the Charter of responsible committees. Related to the second distinction,

however, I find that when the Audit Committee is responsible for the review and approval of

RPTs, firms report significantly fewer RPTs than firms in which other committees or the board

are responsible for RPT approval.

In Columns 2 to 6, I regress the implied cost of capital on these two distinctions,

respectively. Columns 2 and 3 indicate that the adoption of written RPT governance policies is

not associated with the implied cost of capital. Columns 4 to 6 show that the implied cost of

capital is higher for firms with no designated committee to review RPTs.

30

Taken together, the above findings provide certain evidence that firms benefit to have a

designated committee for RPT review and approval, but do not justify the implied cost of capital

benefit of having a separate written RPT governance policy.

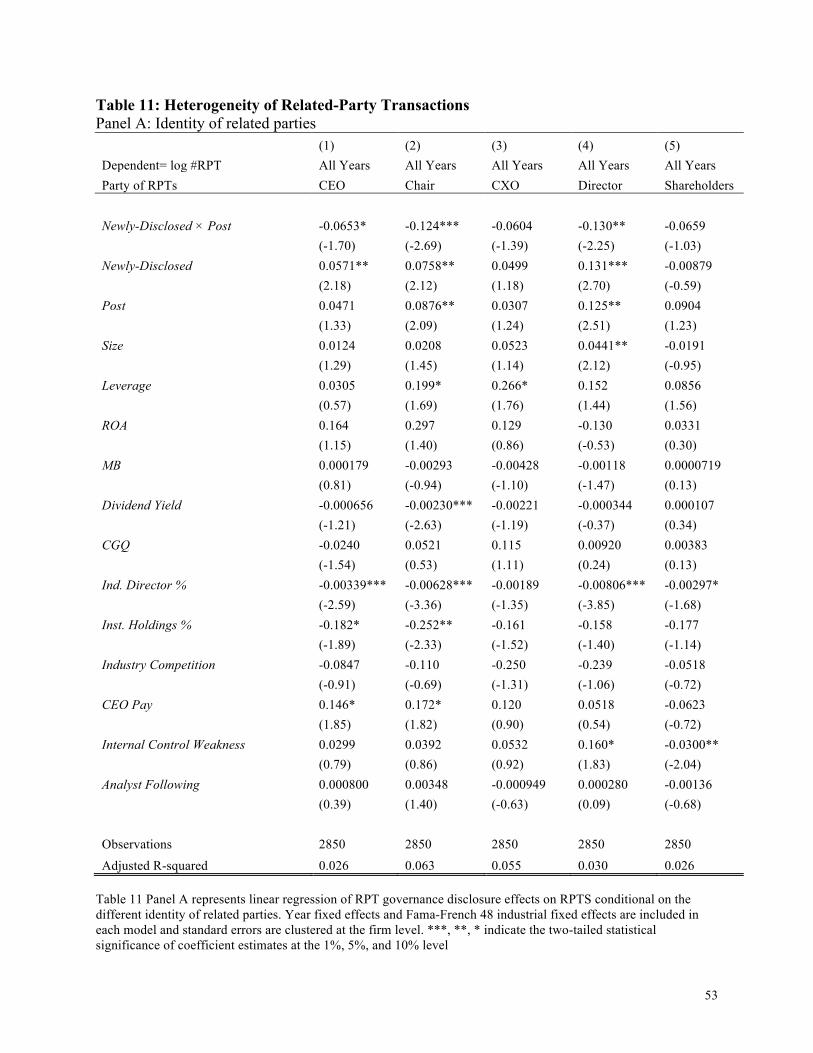

4.4.2 Heterogeneity in RPTs

RPTs differ in the identity of related parties and in the types of transactions. To better

understand whether the 2006 SEC regulation affects different types of transactions differently, I

decompose firms’ RPTs into five categories in terms of the identity of related parties, including

the CEO, other executives, the chairman of the Board, directors, and major shareholders. Panel A

of Table 11 shows that most firms reduce their RPTs in the post-regulation period for all

categories. However, the impact of RPT governance disclosure is more salient when related

parties are CEOs, Chairs of the Board, or Board directors than when related parties are other

executives or shareholders.

I also decompose RPTs based on the nature of transactions, by grouping transactions into

nine categories: buy, sell, lease, consulting, legal, hire, loan, pay, and others.14 I find in Panel B

of Table 11 that the RPT governance disclosure effects concentrate on sell, lease, and loan types

of RPTs.

The empirical evidence in Table 11 could suggest an important implication. In section

4.2.1, I posit that RPT governance disclosure has the potential to reduce harmful RPTs through

increased monitoring and control. In section 4.2.2, I find that the RPT governance disclosure

effects are more pronounced when potential agency costs are high, consistent with the perception

that the RPT governance disclosure regulation reduces these RPTs that are more likely to be used

as expropriation. Based on these arguments, the findings in Table 11 may suggest that RPTs with

CEO, Chairs, or directors are more likely to be harmful than RPTs with other executives or 14 Please refer to Appendix B for detailed RPT category definitions.

31

major shareholders. Similarly, RPTs involving sell, lease, or loans are more likely to be harmful

than RPTs involving other types of transactions.

5. Conclusion

Using the 2006 SEC’s related-party transaction governance disclosure regulation as a

quasi-experimental setting, I find that the disclosure of RPT governance has a significant impact

on the occurrence of RPTs, and that the implied cost of capital associated with RPTs is

negatively associated with the disclosure of RPT governance. Specifically, I find that both the

occurrence of RPTs and the implied costs of capital associated with RPTs decrease for these

firms that initiated RPT policy disclosure, suggesting that the initiation of RPT governance

disclosure by the 2006 SEC regulation significantly enhances the RPT governance. I also find

that the disclosure effects are contingent on external monitoring environment.

Some caveats exist. My study cannot distinguish the Newly-Disclosed firms that initiate

new RPT controls from the Newly-Disclosed firms that disclose existing controls. The mandatory

RPT governance disclosure potentially has different implications for these two types of Newly-

Disclosed firms. Another limitation is the potential confounding effect of the financial crisis

starting in 2007. The post-period in my sample, which includes 2007 and 2010, coincides with

the occurrence of the financial crisis. It is unclear whether the financial crisis has a different

influence on Newly-Disclosed firms and Already-Disclosed firms.

My paper provides empirical support for regulators’ guidance by documenting the

economic consequences of the 2006 SEC related-party transaction regulation and contributes to

the literature by showing disclosure on governance can enhance real governance. It also extends

the existing RPT literature by examining the relation between the RPT governance disclosure

32

and the implied cost of capital associated with RPTs, and by studying how this association varies

with different control procedures and different related parties.

33

References Baggs, J., and J.E. De Bettignies. 2007. “Product-market competition and agency costs.” Journal of

Industrial Economics 55 (2): 289–323. Balsam, Steven, Richard H. Gifford, and John Puthenpurackal. “Related Party Transactions, Corporate

Governance and CEO Compensation” Journal of Business Finance & Accounting 44, no. 5–6 (May 2017): 854–94.

Berkman, Henk, Rebel A. Cole, and Lawrence J. Fu. 2009. “Expropriation through Loan Guarantees to Related Parties: Evidence from China.” Journal of Banking & Finance 33 (1): 141–56.

Botosan, Christine A. 1997. “Disclosure Level and the Cost of Equity Capital.” The Accounting Review, 323–49.

Brick, Ivan E., Oded Palmon, and John K. Wald. 2006. “CEO Compensation, Director Compensation, and Firm Performance: Evidence of Cronyism?” Journal of Corporate Finance 12 (3): 403–23.

Chen, Jean Jinghan, Peng Cheng, and Xinrong Xiao. 2010. “Related Party Transactions as a Source of Earnings Management.” Applied Financial Economics 21 (3): 165–81.

Cheng, Beiting, Ioannis Ioannou, and George Serafeim. 2014. “Corporate Social Responsibility and Access to Finance.” Strategic Management Journal 35 (1): 1–23.

Cheung, Yan-Leung, Yuehua Qi, P. Raghavendra Rau, and Aris Stouraitis. 2009. “Buy High, Sell Low: How Listed Firms Price Asset Transfers in Related Party Transactions.” Journal of Banking & Finance 33 (5): 914–24.

Cheung, Yan-Leung, P. Raghavendra Rau, and Aris Stouraitis. 2006. “Tunneling, Propping, and Expropriation: Evidence from Connected Party Transactions in Hong Kong.” Journal of Financial Economics 82 (2): 343–86.

Cheynel, Edwige. 2013. “A Theory of Voluntary Disclosure and Cost of Capital.” Review of Accounting Studies 18 (4): 987–1020.

Claus, James, and Jacob Thomas. 2001. “Equity Premia as Low as Three Percent? Evidence from Analysts’ Earnings Forecasts for Domestic and International Stock Markets.” The Journal of Finance 56 (5): 1629–66.

Cullinan, Charles P., Hui Du, and Gail B. Wright. 2006. “A Test of the Loan Prohibition of the Sarbanes-Oxley Act: Are Firms That Grant Loans to Executives More Likely to Misstate Their Financial Results?” Journal of Accounting and Public Policy 25 (4): 485–97.

Denis, David J, and Atulya Sarin. 1999. “Ownership and Board Structures in Publicly Traded Corporations.” Journal of Financial Economics 52 (2): 187–223.

Easton, Peter D. 2004. “PE Ratios, PEG Ratios, and Estimating the Implied Expected Rate of Return on Equity Capital.” The Accounting Review 79 (1): 73–95.

Friedberg, L., 2003. The impact of technological change on older workers: evidence from data on computers. Industrial and Labor Relations Review, 56 (3): 511-529.

Gebhardt, William R., Charles M. C. Lee, and Bhaskaran Swaminathan. 2001. “Toward an Implied Cost of Capital.” Journal of Accounting Research 39 (1): 135–76.

Ghoul, Sadok El, Omrane Guedhami, Chuck C. Y. Kwok, and Dev R. Mishra. 2011. “Does Corporate Social Responsibility Affect the Cost of Capital?” Journal of Banking & Finance 35 (9): 2388–2406.

Giroud, X., and H. Mueller. 2011. “Corporate governance, product-market competition, and equity prices.” Journal of Finance 66 (2): 563–600.

Gode, Dan, and Partha Mohanram. 2003. “Inferring the Cost of Capital Using the Ohlson–Juettner Model.” Review of Accounting Studies 8 (4): 399–431.

Gordon, Elizabeth A., Elaine Henry, and Darius Palia. 2004. “Related party transaction and corporate governance.” In Corporate Governance, 9:1–27. Advances in Financial Economics 9. Emerald Group Publishing Limited.

Gordon, Elizabeth A., and Elaine Henry. 2005. “Related Party Transactions and Earnings Management.” SSRN Scholarly Paper ID 612234. Rochester, NY

34

Grossman, Sanford J. 1981. “The Informational Role of Warranties and Private Disclosure about Product Quality.” The Journal of Law & Economics 24 (3): 461–83.

Hail, Luzi, and Christian Leuz. 2006 "International differences in the cost of equity capital: Do legal institutions and securities regulation matter?" Journal of accounting research 44 (3) 485-531.

Hanlon, M., Rajgopal, S., and Shevlin, T., 2003. “Are executive stock options associated with future earnings?” Journal of Accounting and Economics, 36: 3-43.

Hou, Y., 2015. The role of diversification in the pricing of accruals quality. Review of Accounting Studies, 20(3), pp.1059-1092.

Huddart, Steven, 1993, “The Effect of a Large Shareholder on Corporate Value” Management Science 39 (No. 4, Aug.), 1407-1421.

Jagannathan, R., and S. B. Srinivasan. 1999. “Does product-market competition reduce agency costs?” North American Journal of Economics and Finance 10 (2): 387–400.

Jensen, M.C., and W.H. Meckling 1976. “Theory of the firm: Managerial Behavior, Agency costs, and Ownership Structure.” Journal of financial Economics 3, 305-360

Jian, Ming, and T. J. Wong. 2010. “Propping through Related Party Transactions.” Review of Accounting Studies 15 (1): 70–105.

Kahle, Kathleen M., and Kuldeep Shastri. 2004. “Executive Loans.” Journal of Financial and Quantitative Analysis 39 (04): 791–811.

Klein, April. 2002. “Audit Committee, Board of Director Characteristics, and Earnings Management.” Journal of Accounting and Economics 33 (3): 375–400.

Kohlbeck, Mark, and Brian W. Mayhew. 2010. “Valuation of Firms That Disclose Related Party Transactions.” Journal of Accounting and Public Policy 29 (2): 115–37.

Kohlbeck, Mark, and Brian W. Mayhew. “Are Related Party Transactions Red Flags?” Contemporary Accounting Research 34, no. 2 (June 1, 2017): 900–928.

La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny. “Investor Protection and Corporate Governance.” Journal of Financial Economics, Special Issue on International Corporate Governance, 58, no. 1 (January 1, 2000): 3–27.

Lambert, Richard, Christian Leuz, and Robert E. Verrecchia. 2007. “Accounting Information, Disclosure, and the Cost of Capital.” Journal of Accounting Research 45 (2): 385–420.

Lang, Mark, Karl V. Lins, and Mark Maffett. 2012. “Transparency, Liquidity, and Valuation: International Evidence on When Transparency Matters Most.” Journal of Accounting Research 50 (3): 729–74.

Leuz, Christian, and Peter D. Wysocki. “The Economics of Disclosure and Financial Reporting Regulation: Evidence and Suggestions for Future Research.” Journal of Accounting Research 54, no. 2 (May 1, 2016): 525–622.

Lo, Agnes W. Y., Raymond M. K. Wong, and Michael Firth. 2010. “Can Corporate Governance Deter Management from Manipulating Earnings? Evidence from Related-Party Sales Transactions in China.” Journal of Corporate Finance 16 (2): 225–35.

Nekhili, Mehdi, and Moêz Cherif. 2011. “Related Parties Transactions and Firm’s Market Value: The French Case.” Review of Accounting and Finance 10 (3): 291–315.

Nevo, A., 2000. “Mergers with differentiated products: the case of the ready-to-eat cereal industry.” RAND Journal of Economics, 31 (3): 395-421.

Ohlson, J.A. and Juettner-Nauroth, B.E., 2005. “Expected EPS and EPS growth as determinants of value.” Review of accounting studies, 10(2-3), pp.349-365.

Pizzo, Michele. 2013. “Related Party Transactions under a Contingency Perspective.” Journal of Management & Governance 17 (2): 309–30.

Ryngaert, Michael, and Shawn Thomas. 2012. “Not All Related Party Transactions (RPTs) Are the Same: Ex Ante versus Ex Post RPTs.” Journal of Accounting Research 50 (3): 845–82.

Shleifer, A. and R. Vishny, 1986, “Large Shareholders and Corporate Control” Journal of Political Economy 94 (No. 3, June), 461-48.

35

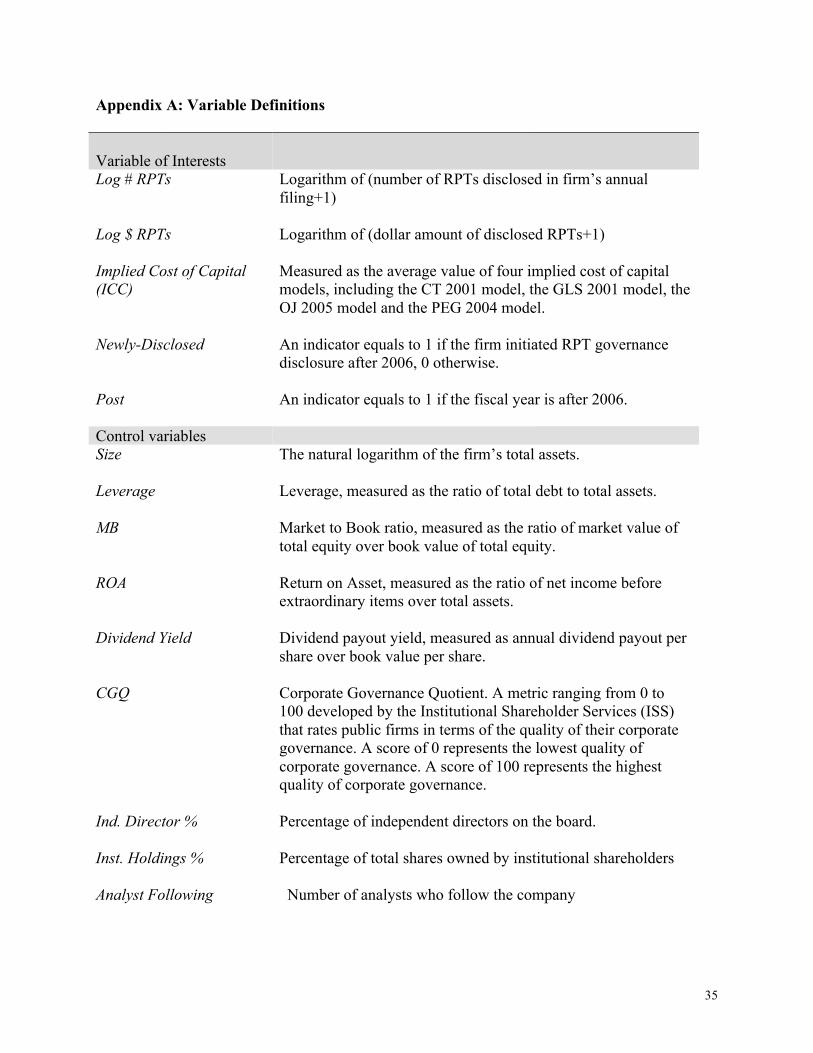

Appendix A: Variable Definitions Variable of Interests

Log # RPTs Logarithm of (number of RPTs disclosed in firm’s annual filing+1)

Log $ RPTs Logarithm of (dollar amount of disclosed RPTs+1)

Implied Cost of Capital (ICC)

Measured as the average value of four implied cost of capital models, including the CT 2001 model, the GLS 2001 model, the OJ 2005 model and the PEG 2004 model.

Newly-Disclosed An indicator equals to 1 if the firm initiated RPT governance disclosure after 2006, 0 otherwise.

Post An indicator equals to 1 if the fiscal year is after 2006. Control variables Size The natural logarithm of the firm’s total assets.

Leverage Leverage, measured as the ratio of total debt to total assets.

MB Market to Book ratio, measured as the ratio of market value of

total equity over book value of total equity.

ROA Return on Asset, measured as the ratio of net income before extraordinary items over total assets.

Dividend Yield Dividend payout yield, measured as annual dividend payout per share over book value per share.

CGQ Corporate Governance Quotient. A metric ranging from 0 to 100 developed by the Institutional Shareholder Services (ISS) that rates public firms in terms of the quality of their corporate governance. A score of 0 represents the lowest quality of corporate governance. A score of 100 represents the highest quality of corporate governance.

Ind. Director % Percentage of independent directors on the board.

Inst. Holdings % Percentage of total shares owned by institutional shareholders Analyst Following Number of analysts who follow the company

36

Industry Competition Measured as the Herfindahl index of firms market share by Fama-French 48 industries.

CEO pay CEO compensation, measured as the logarithm of total dollar amount of CEO compensation adjusted by firm size.

Internal Control Weakness

An indicator equals to 1 if the firms disclose internal control weakness under SOX 404

Beta A measure of a stock’s volatility in relation to the market,

calculated using prior 60 months daily stock price.

Predicted Newly-Disclosed

A Predicted probability of being Newly-Disclosed firm using determinant model.

Written_Policy An indicator equals to 1 if the firm has a written RPT policy, 0 otherwise.

Audit_Committee An indicator equals to 1 if the firm delegates its audit committee to review and approve RPTs, 0 otherwise.

37

Appendix B: Categories of Related-Party Transactions RPT categories in terms of transaction party CEO The related party is CEO or relatives of CEO

CXO The related party is a non-CEO executive or relatives of a non-CEO executive Chair The related party is the Chairman of Board of Director or relatives of the

Chairman Directors The related party is a director or relatives of a director Shareholders The related party is a block shareholder. Block shareholder is defined as