24

Company Report Industry: Oil & Gas Avishek Datta ([email protected]) +91-22-66322254 Reliance Industries At the cusp of transformation

Company Report Industry: Oil & Gas

Avishek Datta ([email protected]) +91-22-66322254

Reliance Industries At the cusp of transformation

May 12, 2016 2

Reliance Industries

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Contents Page No.

Investment Argument ................................................................................................. 4

New projects to drive operating profit at 16% CAGR over FY16-18E ................................................ 4

Earnings momentum is back ............................................................................................................. 4

Core business in fine fettle - Refining margins remain healthy ......................................................... 6

Strong demand drives refining margins higher ............................................................................ 6

Demand momentum remain healthy .......................................................................................... 6

Refining capacity addition trails demand .................................................................................... 8

RIL’s GRM outperformance- Multiple factors at play ........................................................................ 9

Meanwhile, weak gasoil margins remain a concern ....................................................................... 10

However, rising discounts from Middle East oil producers is a positive ......................................... 11

Petcoke gasification project to give fillip to margins ....................................................................... 12

Asian integrated crackers benefit from low naphtha prices ........................................................... 13

Sensitivity and Risks .................................................................................................. 17

Financial Analysis ...................................................................................................... 20

Valuation and View ................................................................................................... 21

Reliance Industries

Company Report May 12, 2016

Rating Accumulate

Price Rs975

Target Price Rs1,034

Implied Upside 6.1%

Sensex 25,597

Nifty 7,849

(Prices as on May 11, 2016)

Trading data

Market Cap. (Rs bn) 3,159.0

Shares o/s (m) 3,240.0

3M Avg. Daily value (Rs m) 4,312.7

Major shareholders

Promoters 46.53%

Foreign 7.39%

Domestic Inst. 25.84%

Public & Other 20.24%

Stock Performance

(%) 1M 6M 12M

Absolute (6.2) 5.1 8.9

Relative (8.5) 6.1 15.8

How we differ from Consensus

EPS (Rs) PL Cons. % Diff.

2017 83.1 88.5 -6.1

2018 103.5 103.8 -0.3

Price Performance (RIC: RELI.BO, BB: RIL IN)

Source: Bloomberg

0

200

400

600

800

1,000

1,200

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

(Rs)

Stepping on the accelerator: RIL is at the cusp of a major transformation led by

commissioning of the US$18.5bn petrochemical projects in H2FY17E. While the

commissioning of the PTA and PET capacities (part of petrochemicals

expansion), along with higher refining profits, supported 21% YoY earnings

growth in FY16, minimal capacity addition/stabilisation in FY17E, along with

plateauing refining margins, are likely to push earnings growth to FY18E.

Project value accretion to improve with crude prices: RIL’s transformational

petrochemicals project is likely to generate incremental EBITDA of ~Rs155bn

(US$2.3bn) in FY18E. Project economics are likely to improve with higher

commodity prices. Among the projects, ethane substitution along with refinery

offgas cracker project, designed to use refinery offgas for petrochemicals

remain attractive. However, sharp drop in spot LNG prices would impact returns

on petcoke gassification.;We calculate GRM benefit of US$1.3/bbl in FY18E.

Core earnings in fine fettle: RIL’s core business continues to remain healthy as

product demand revival in US, China and India along with trailing capacity

addition support refining margins (GRMs). Though drop in gasoil spreads is a

concern, benefits like rising discounts from the Middle East producers and lower

operating cost is to aid refining margins. Also, sharp drop in naphtha prices will

benefit the Asian integrated naphtha crackers, as cracker margins are supported

by delays in new US and Chinese supplies, given crude price correction.

Initiate with an ‘Accumulate’: We initiate with an ‘Accumulate’ on RIL at a PT of

Rs1,034 based on SOTP. We expect RIL’s earnings (excl. telecom) to grow at

~11% CAGR over FY16-18E, ROE to expand 120bps over FY16-18E on the back of

improved fundamentals. However, the continued uncertainty on Reliance Jio’s

(RJio’s) launch date and rising capex (US$23bn) remains an overhang.

Key financials (Y/e March) 2015 2016 2017E 2018E

Revenues (Rs m) 3,287,720 2,331,580 2,938,657 3,115,302

Growth (%) (15.7) (29.1) 26.0 6.0

EBITDA (Rs m) 316,710 401,390 427,776 537,708

PAT (Rs m) 227,190 274,170 269,254 335,419

EPS (Rs) 70.2 84.6 83.1 103.5

Growth (%) 3.2 20.5 (1.8) 24.6

Net DPS (Rs) 13.0 14.0 15.0 16.0

Profitability & Valuation 2015 2016 2017E 2018E

EBITDA margin (%) 9.6 17.2 14.6 17.3

RoE (%) 11.0 12.0 11.0 13.2

RoCE (%) 8.0 8.7 8.3 9.8

EV / sales (x) 1.2 1.8 1.4 1.3

EV / EBITDA (x) 12.7 10.2 9.7 7.7

PE (x) 13.9 11.5 11.7 9.4

P / BV (x) 1.5 1.3 1.3 1.2

Net dividend yield (%) 1.3 1.4 1.5 1.6

Source: Company Data; PL Research

Reliance Industries

May 12, 2016 4

Investment Argument

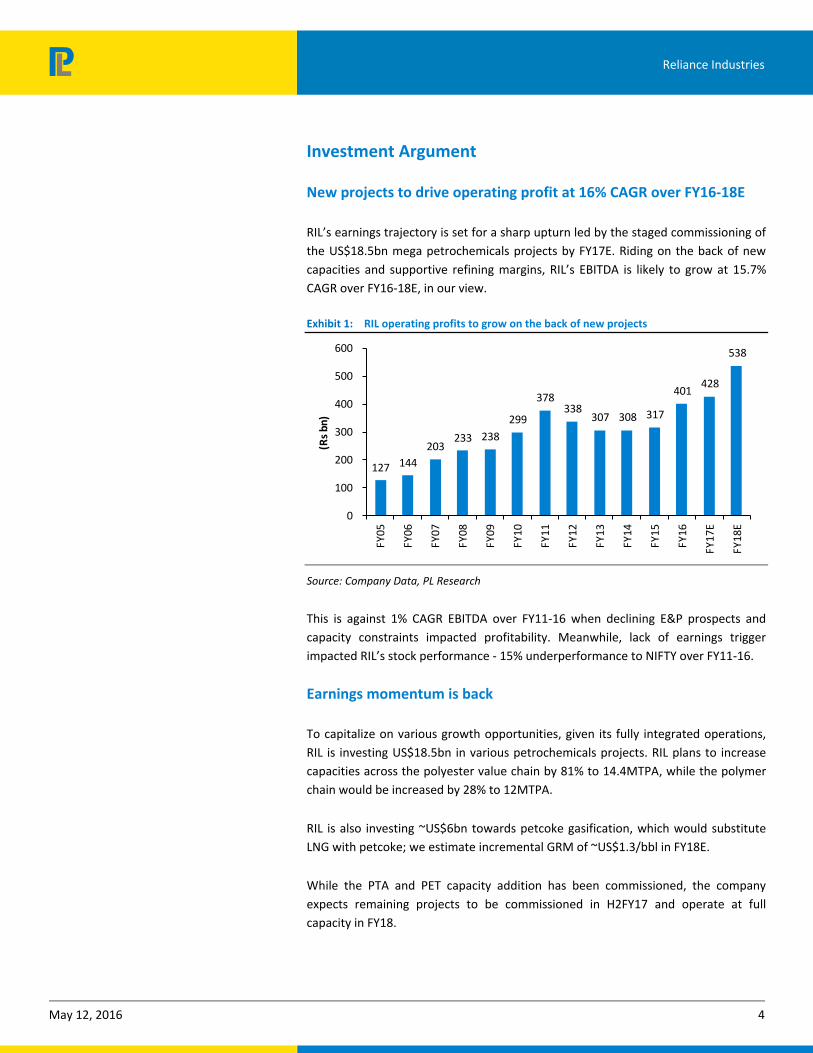

New projects to drive operating profit at 16% CAGR over FY16-18E

RIL’s earnings trajectory is set for a sharp upturn led by the staged commissioning of

the US$18.5bn mega petrochemicals projects by FY17E. Riding on the back of new

capacities and supportive refining margins, RIL’s EBITDA is likely to grow at 15.7%

CAGR over FY16-18E, in our view.

Exhibit 1: RIL operating profits to grow on the back of new projects

127 144

203 233 238

299

378 338

307 308 317

401 428

538

0

100

200

300

400

500

600

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

E

FY

18

E

(Rs

bn

)

Source: Company Data, PL Research

This is against 1% CAGR EBITDA over FY11-16 when declining E&P prospects and

capacity constraints impacted profitability. Meanwhile, lack of earnings trigger

impacted RIL’s stock performance - 15% underperformance to NIFTY over FY11-16.

Earnings momentum is back

To capitalize on various growth opportunities, given its fully integrated operations,

RIL is investing US$18.5bn in various petrochemicals projects. RIL plans to increase

capacities across the polyester value chain by 81% to 14.4MTPA, while the polymer

chain would be increased by 28% to 12MTPA.

RIL is also investing ~US$6bn towards petcoke gasification, which would substitute

LNG with petcoke; we estimate incremental GRM of ~US$1.3/bbl in FY18E.

While the PTA and PET capacity addition has been commissioned, the company

expects remaining projects to be commissioned in H2FY17 and operate at full

capacity in FY18.

Reliance Industries

May 12, 2016 5

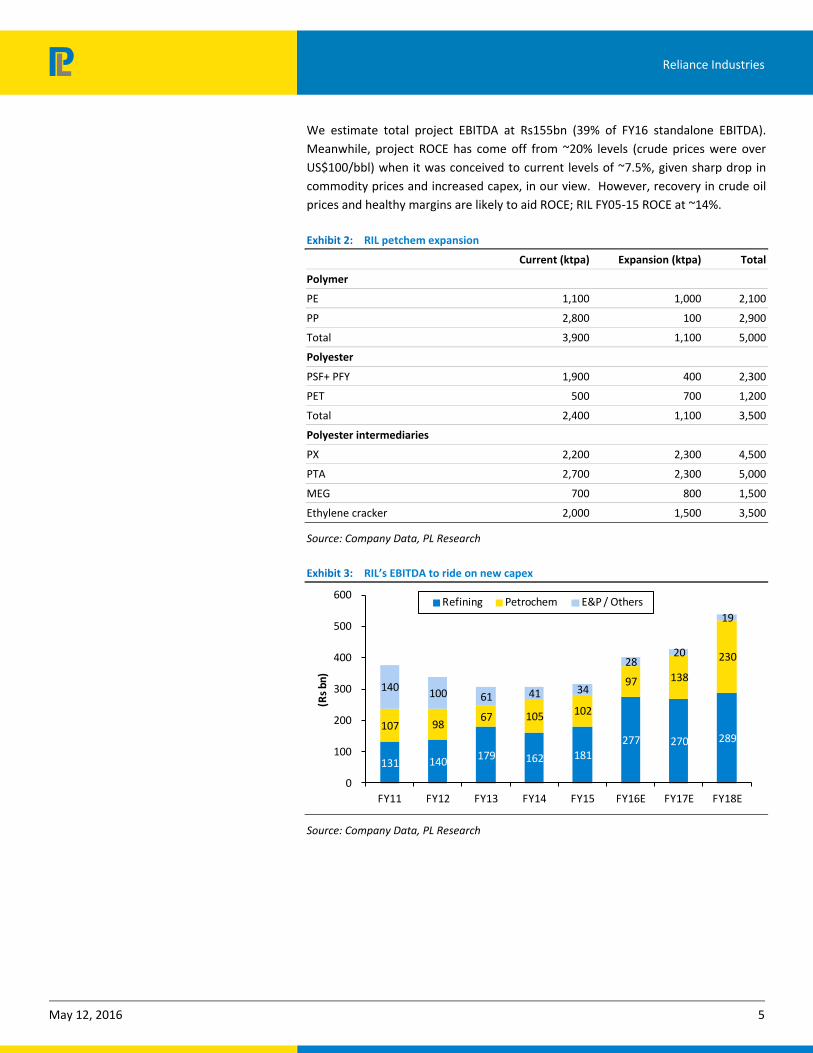

We estimate total project EBITDA at Rs155bn (39% of FY16 standalone EBITDA).

Meanwhile, project ROCE has come off from ~20% levels (crude prices were over

US$100/bbl) when it was conceived to current levels of ~7.5%, given sharp drop in

commodity prices and increased capex, in our view. However, recovery in crude oil

prices and healthy margins are likely to aid ROCE; RIL FY05-15 ROCE at ~14%.

Exhibit 2: RIL petchem expansion

Current (ktpa) Expansion (ktpa) Total

Polymer

PE 1,100 1,000 2,100

PP 2,800 100 2,900

Total 3,900 1,100 5,000

Polyester

PSF+ PFY 1,900 400 2,300

PET 500 700 1,200

Total 2,400 1,100 3,500

Polyester intermediaries

PX 2,200 2,300 4,500

PTA 2,700 2,300 5,000

MEG 700 800 1,500

Ethylene cracker 2,000 1,500 3,500

Source: Company Data, PL Research

Exhibit 3: RIL’s EBITDA to ride on new capex

131 140 179 162 181

277 270 289 107 98

67 105 102

97 138

230

140 100 61 41 34

28 20

19

0

100

200

300

400

500

600

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(Rs

bn)

Refining Petrochem E&P / Others

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 6

Core business in fine fettle - Refining margins remain healthy

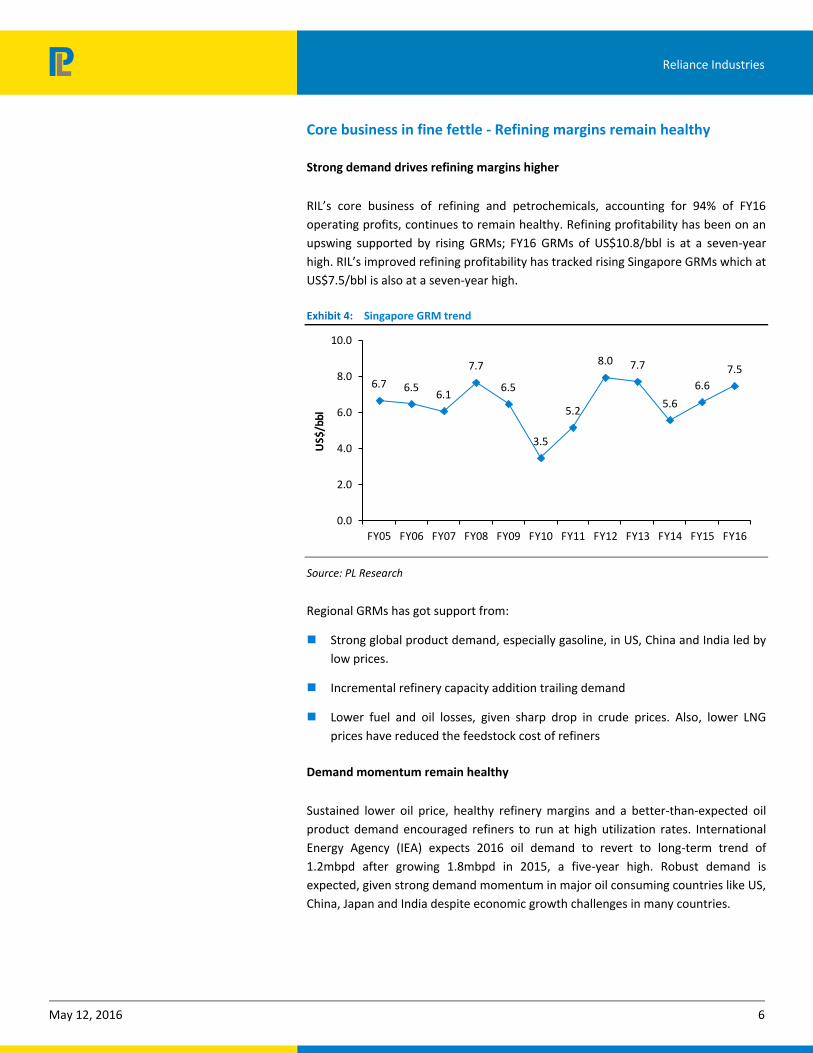

Strong demand drives refining margins higher

RIL’s core business of refining and petrochemicals, accounting for 94% of FY16

operating profits, continues to remain healthy. Refining profitability has been on an

upswing supported by rising GRMs; FY16 GRMs of US$10.8/bbl is at a seven-year

high. RIL’s improved refining profitability has tracked rising Singapore GRMs which at

US$7.5/bbl is also at a seven-year high.

Exhibit 4: Singapore GRM trend

6.7 6.56.1

7.7

6.5

3.5

5.2

8.0 7.7

5.6

6.6

7.5

0.0

2.0

4.0

6.0

8.0

10.0

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

US$

/bbl

Source: PL Research

Regional GRMs has got support from:

Strong global product demand, especially gasoline, in US, China and India led by

low prices.

Incremental refinery capacity addition trailing demand

Lower fuel and oil losses, given sharp drop in crude prices. Also, lower LNG

prices have reduced the feedstock cost of refiners

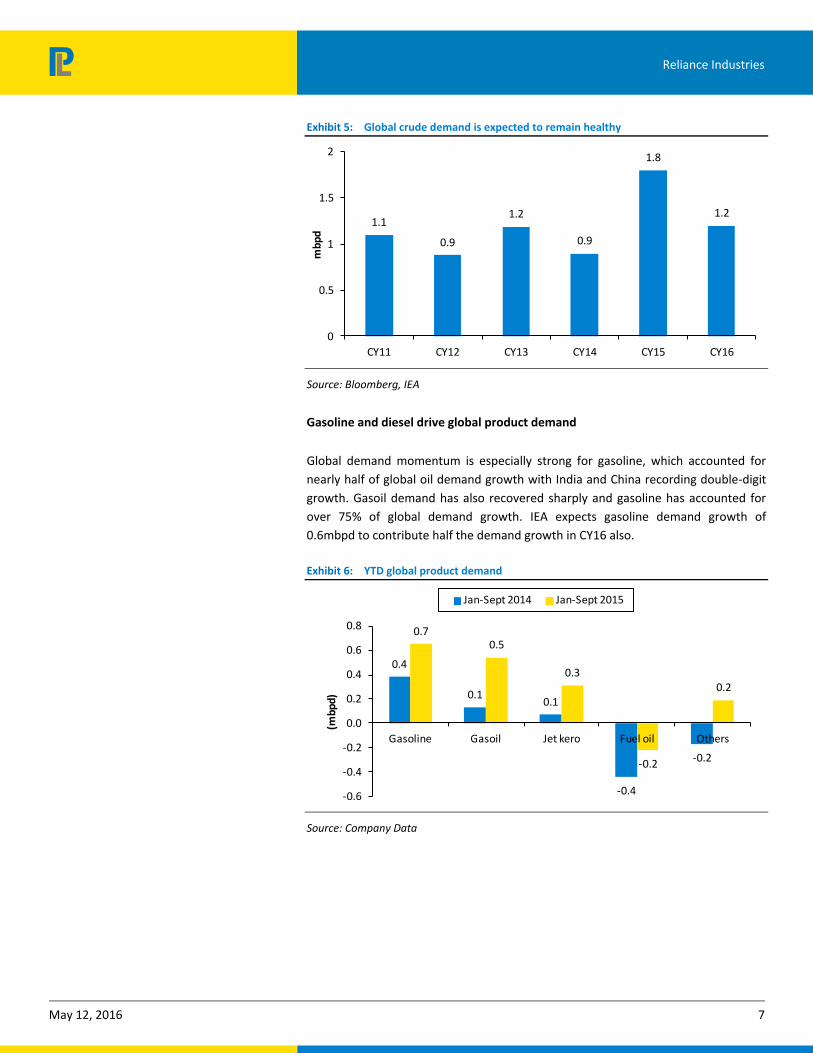

Demand momentum remain healthy

Sustained lower oil price, healthy refinery margins and a better-than-expected oil

product demand encouraged refiners to run at high utilization rates. International

Energy Agency (IEA) expects 2016 oil demand to revert to long-term trend of

1.2mbpd after growing 1.8mbpd in 2015, a five-year high. Robust demand is

expected, given strong demand momentum in major oil consuming countries like US,

China, Japan and India despite economic growth challenges in many countries.

Reliance Industries

May 12, 2016 7

Exhibit 5: Global crude demand is expected to remain healthy

1.1

0.9

1.2

0.9

1.8

1.2

0

0.5

1

1.5

2

CY11 CY12 CY13 CY14 CY15 CY16

mbp

d

Source: Bloomberg, IEA

Gasoline and diesel drive global product demand

Global demand momentum is especially strong for gasoline, which accounted for

nearly half of global oil demand growth with India and China recording double-digit

growth. Gasoil demand has also recovered sharply and gasoline has accounted for

over 75% of global demand growth. IEA expects gasoline demand growth of

0.6mbpd to contribute half the demand growth in CY16 also.

Exhibit 6: YTD global product demand

0.4

0.10.1

-0.4

-0.2

0.70.5

0.3

-0.2

0.2

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Gasoline Gasoil Jet kero Fuel oil Others

(mbp

d)

Jan-Sept 2014 Jan-Sept 2015

Source: Company Data

Reliance Industries

May 12, 2016 8

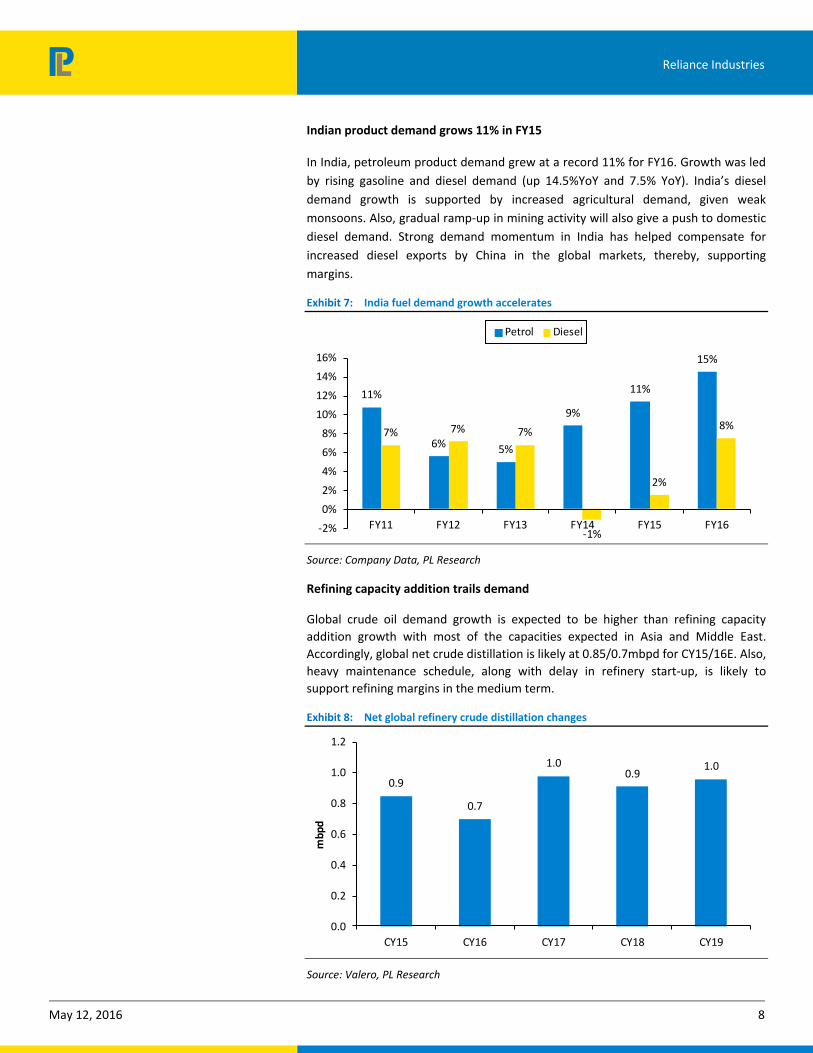

Indian product demand grows 11% in FY15

In India, petroleum product demand grew at a record 11% for FY16. Growth was led

by rising gasoline and diesel demand (up 14.5%YoY and 7.5% YoY). India’s diesel

demand growth is supported by increased agricultural demand, given weak

monsoons. Also, gradual ramp-up in mining activity will also give a push to domestic

diesel demand. Strong demand momentum in India has helped compensate for

increased diesel exports by China in the global markets, thereby, supporting

margins.

Exhibit 7: India fuel demand growth accelerates

11%

6% 5%

9%

11%

15%

7% 7% 7%

-1%

2%

8%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

FY11 FY12 FY13 FY14 FY15 FY16

Petrol Diesel

Source: Company Data, PL Research

Refining capacity addition trails demand

Global crude oil demand growth is expected to be higher than refining capacity

addition growth with most of the capacities expected in Asia and Middle East.

Accordingly, global net crude distillation is likely at 0.85/0.7mbpd for CY15/16E. Also,

heavy maintenance schedule, along with delay in refinery start-up, is likely to

support refining margins in the medium term.

Exhibit 8: Net global refinery crude distillation changes

0.9

0.7

1.00.9

1.0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

CY15 CY16 CY17 CY18 CY19

mbp

d

Source: Valero, PL Research

Reliance Industries

May 12, 2016 9

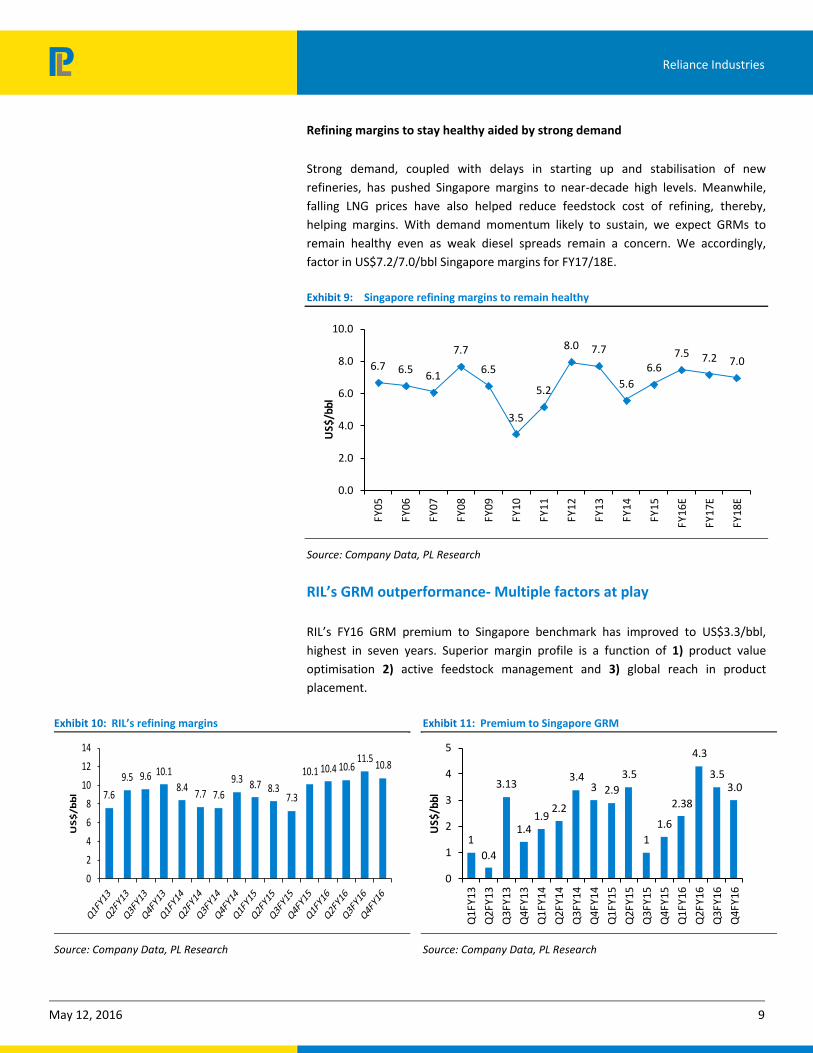

Refining margins to stay healthy aided by strong demand

Strong demand, coupled with delays in starting up and stabilisation of new

refineries, has pushed Singapore margins to near-decade high levels. Meanwhile,

falling LNG prices have also helped reduce feedstock cost of refining, thereby,

helping margins. With demand momentum likely to sustain, we expect GRMs to

remain healthy even as weak diesel spreads remain a concern. We accordingly,

factor in US$7.2/7.0/bbl Singapore margins for FY17/18E.

Exhibit 9: Singapore refining margins to remain healthy

6.7 6.56.1

7.7

6.5

3.5

5.2

8.0 7.7

5.6

6.67.5 7.2 7.0

0.0

2.0

4.0

6.0

8.0

10.0

FY05

FY06

FY07

FY

08

FY

09

FY10

FY11

FY12

FY13

FY14

FY

15

FY

16

E

FY17

E

FY18

E

US$

/bbl

Source: Company Data, PL Research

RIL’s GRM outperformance- Multiple factors at play

RIL’s FY16 GRM premium to Singapore benchmark has improved to US$3.3/bbl,

highest in seven years. Superior margin profile is a function of 1) product value

optimisation 2) active feedstock management and 3) global reach in product

placement.

Exhibit 10: RIL’s refining margins

7.6

9.5 9.6 10.1

8.47.7 7.6

9.3 8.7 8.37.3

10.1 10.4 10.611.5

10.8

0

2

4

6

8

10

12

14

US

$/b

bl

Source: Company Data, PL Research

Exhibit 11: Premium to Singapore GRM

1

0.4

3.13

1.41.9

2.2

3.43 2.9

3.5

1

1.6

2.38

4.3

3.53.0

0

1

2

3

4

5

Q1

FY

13

Q2

FY

13

Q3

FY

13

Q4

FY

13

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

US

$/b

bl

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 10

Product value optimisation: RIL has increased production of light distillates,

primarily petrol, to capitalise on gasoline margin strength. In FY16, RIL has increased

production of higher margin gasoline and alkylates to 15.2MMT. Also, RIL’s inherent

capability to swing production trend to match highest value product drives margin

outperformance.

Feedstock management: RIL’s superior refining configuration provides flexibility to

switch grades and process a wide range of crude - 149 different crude varieties till

date. The company is the first refiner to process cheaper Basra Heavy crude from

Iraq. Also, the company is also tying up with Iranian crude oil to optimise margins.

Product placement strategy: RIL has a global presence when it comes to product

placement. For the middle distillates, RIL places bulk of the products in the Middle

East, Europe and Africa. However, for gasoline, the company places majority of

products in the Middle East, Americas, South East Asia and Africa.

Exhibit 12: RIL middle distillate placement by region

Middle East25%

Africa19%

Latin America

13%

SE Asia7%

Australia1%

Europe

35%

Source: PL Research

Exhibit 13: RIL gasoline placement by region

Middle East

47%

Africa

15%

Americas

19%

SE Asia

18%

Australia1%

Source: PL Research

Meanwhile, weak gasoil margins remain a concern

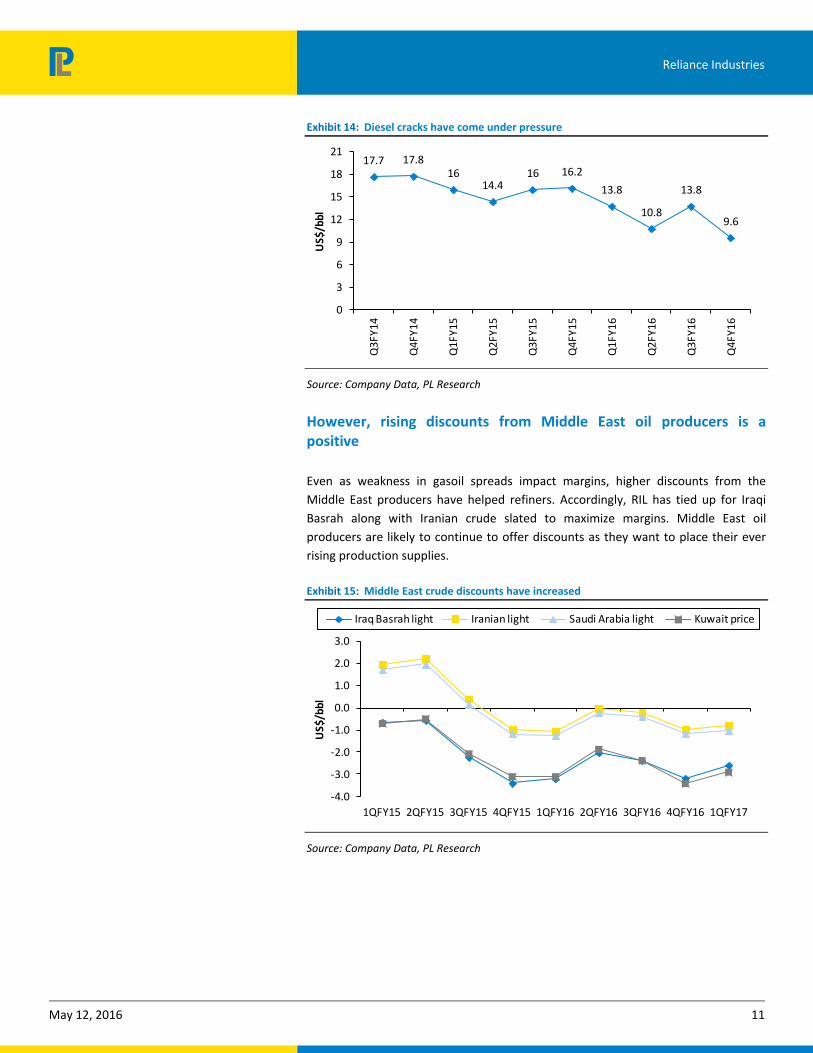

Even as the benchmark indices continue to remain healthy, weakness in gasoil cracks

is a concern. Q4FY16 gasoil spreads fell to US$9.6/bbl (-US4.2/bbl QoQ) led by

increased exports from China amidst weakening industrial demand. FY16 gasoil

spreads of US$12/bbl is lower than FY14/15 levels of ~US$17/16/bbl.

Higher diesel supplies from new capacities being commissioned in the Middle East

and Asia which have heavy diesel slate, is likely to exert pressure on cracks.

With diesel forming ~40% in RIL’s product slate against ~16% in benchmark

Singapore GRM, premiums will come under pressure, in our view. Accordingly, we

factor in US$10.75/11.25/bbl for FY16/17/18E refining margins. This includes

US$0.25/1.25/bbl benefit from petcoke gasification in FY17/18E.

Reliance Industries

May 12, 2016 11

Exhibit 14: Diesel cracks have come under pressure

17.7 17.816

14.416 16.2

13.8

10.8

13.8

9.6

0

3

6

9

12

15

18

21

Q3F

Y14

Q4

FY

14

Q1F

Y15

Q2

FY

15

Q3F

Y15

Q4F

Y15

Q1

FY

16

Q2F

Y16

Q3

FY

16

Q4F

Y16

US$

/bbl

Source: Company Data, PL Research

However, rising discounts from Middle East oil producers is a positive

Even as weakness in gasoil spreads impact margins, higher discounts from the

Middle East producers have helped refiners. Accordingly, RIL has tied up for Iraqi

Basrah along with Iranian crude slated to maximize margins. Middle East oil

producers are likely to continue to offer discounts as they want to place their ever

rising production supplies.

Exhibit 15: Middle East crude discounts have increased

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17

US$

/bbl

Iraq Basrah light Iranian light Saudi Arabia light Kuwait price

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 12

Petcoke gasification project to give fillip to margins

Even as weakness in diesel cracks put pressure on RIL’s margins, completion of the

~US$6bn petcoke gasification project scheduled for commissioning in H2FY17 is a

positive. The project is designed to convert low-value petroleum coke/coal into high

value Syngas for further use as fuels and for hydrogen and chemicals production. It

will also replace expensive LNG currently being used.

While the project is value-accretive, sharp correction in spot LNG prices (~US$5

currently from ~US$15/bbl last year) has eroded some of the value. We estimate

incremental GRMs of US$1.3/bbl post the project completion. With the project

scheduled for graded completion, we have assumed RIL’s GRMs at

US$10.75/11.3/bbl for FY17/18E.

Exhibit 16: Syngas economics

LNG delivered cost (US$/mmbtu) 8.7*

Syngas production cost (US$/mmbtu) 3.0

Benefit (US$/mmbtu) 5.7

Exchange rate (US$/Rs) 67

Avg refinery gas consumption (mmscmd) 9

EBITDA (Rs m) 43,897

EBITDA (US$/bbl) 1.3

Source: PL Research * FOB of $7 + shipping + 5% duty + inland pipeline charges

Exhibit 17: RIL GRM build-up

5.66.6 7.5 7.2 7.0

1.92

3.3 3.3 3.0

0.3 1.3

0

2

4

6

8

10

12

FY14 FY15 FY16 FY17 FY18

US$

/bbl

Singapore GRM Premium to Singapore Petcoke gassification

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 13

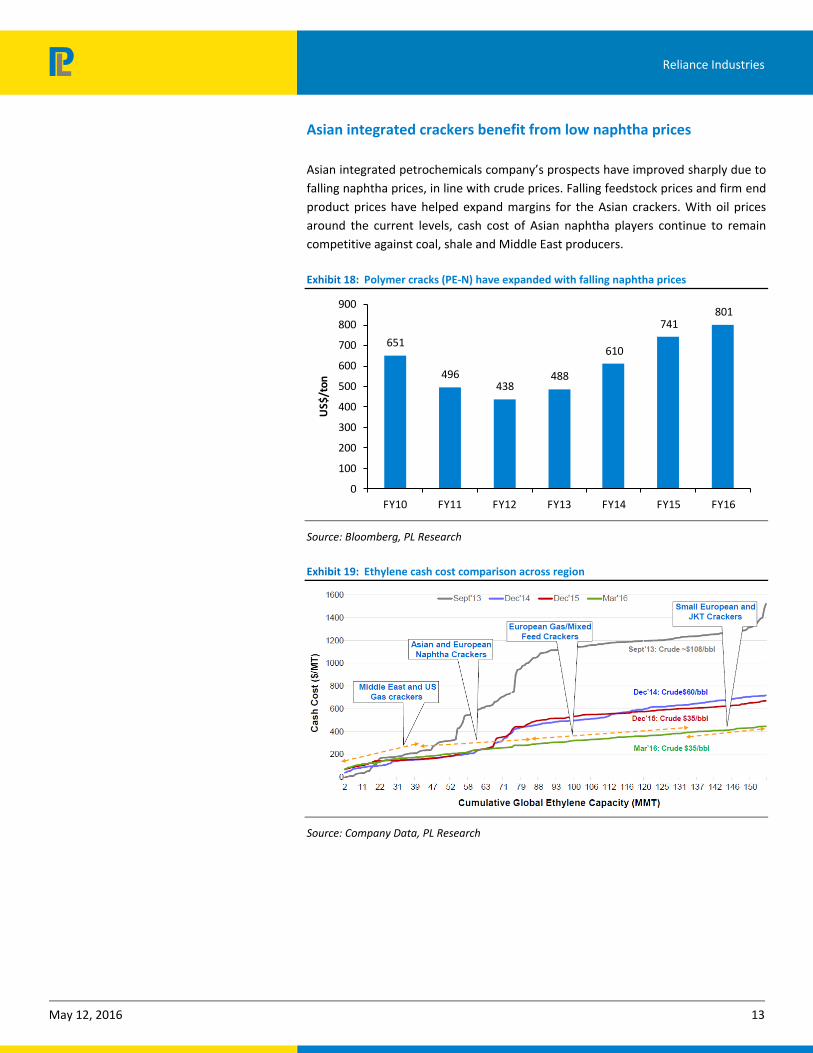

Asian integrated crackers benefit from low naphtha prices

Asian integrated petrochemicals company’s prospects have improved sharply due to

falling naphtha prices, in line with crude prices. Falling feedstock prices and firm end

product prices have helped expand margins for the Asian crackers. With oil prices

around the current levels, cash cost of Asian naphtha players continue to remain

competitive against coal, shale and Middle East producers.

Exhibit 18: Polymer cracks (PE-N) have expanded with falling naphtha prices

651

496438

488

610

741801

0

100

200

300

400

500

600

700

800

900

FY10 FY11 FY12 FY13 FY14 FY15 FY16

US$

/ton

Source: Bloomberg, PL Research

Exhibit 19: Ethylene cash cost comparison across region

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 14

End product demand remain strong

End product demand for polymers continues to remain strong. Global polymer

demand grew at ~4% CAGR over the last five years supported by healthy demand

from automotive, packaging, infrastructure sectors. Asian demand from China and

India continues to remain ahead of global averages as lower prices and increased

consumption activity supports demand. With demand momentum expected to

remain strong, China and India would account for ~80% of regional demand.

Exhibit 20: Asia polymer demand growth

0

10

20

30

40

50

60

70

80

90

China India Japan Indonesia South

Korea

Thailand Others

MM

T2015 2020

Source: Company Data, PL Research

Indian polymer demand grew 15% in FY16

Demand momentum is especially strong in India, where led by healthy demand from

end users, polymer demand grew 15% in FY16. Demand momentum was especially

strong in PP which grew ~20% YoY. PE and PVC demand also recorded healthy

demand of 14% and 11%, respectively. With increased government focus on

infrastructure creation, polymer demand is expected to maintain its healthy demand

trend.

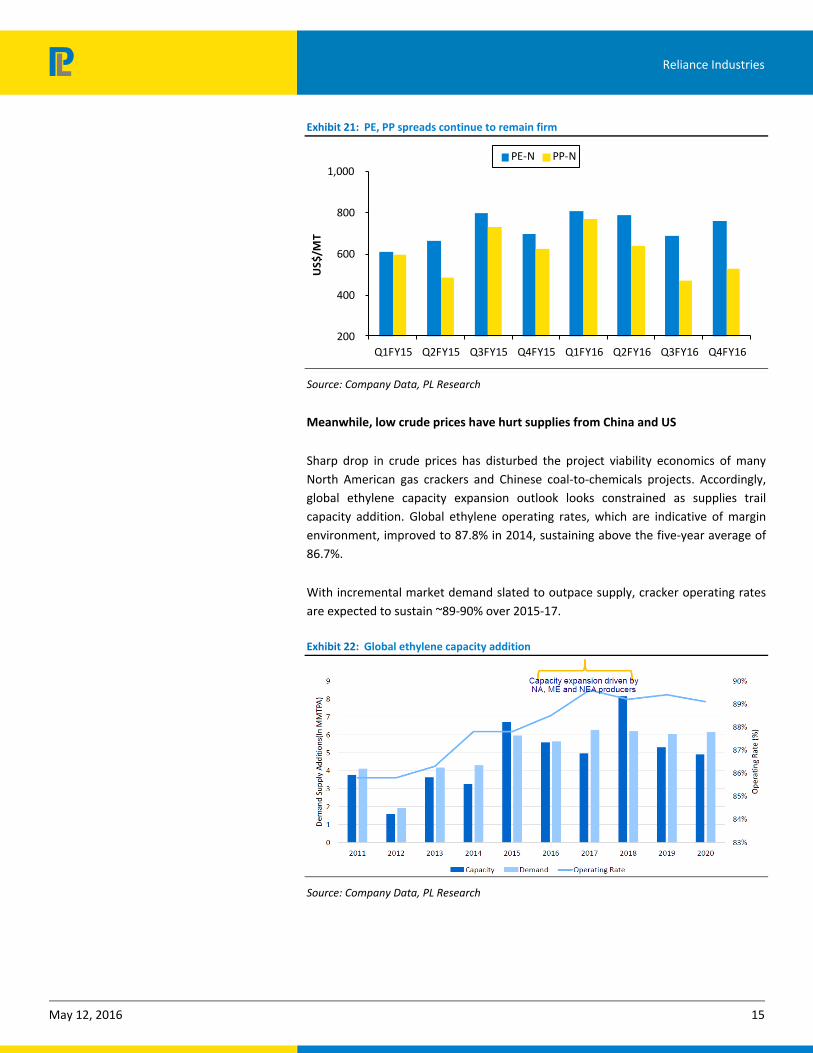

While demand momentum remains strong, product spreads also continue to remain

firm which has contributed to improved profitability for the crackers. Accordingly, PE

and PP deltas improved 11% and 12% YoY, respectively, while PVC spreads came off

3% YoY. Supported by soft raw material prices and firm end user prices, we expect

margins to remain supportive.

Reliance Industries

May 12, 2016 15

Exhibit 21: PE, PP spreads continue to remain firm

200

400

600

800

1,000

Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

US$

/MT

PE-N PP-N

Source: Company Data, PL Research

Meanwhile, low crude prices have hurt supplies from China and US

Sharp drop in crude prices has disturbed the project viability economics of many

North American gas crackers and Chinese coal-to-chemicals projects. Accordingly,

global ethylene capacity expansion outlook looks constrained as supplies trail

capacity addition. Global ethylene operating rates, which are indicative of margin

environment, improved to 87.8% in 2014, sustaining above the five-year average of

86.7%.

With incremental market demand slated to outpace supply, cracker operating rates

are expected to sustain ~89-90% over 2015-17.

Exhibit 22: Global ethylene capacity addition

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 16

Polyester margins likely to remain resilient

Polyester margins continue to remain steady supported by inventory restocking.

However, weakening Chinese demand remains a concern, partly compensated by

intermediary margin trend. India’s polyester demand grew at 5% in FY16 led by PET

which was up 7%. Integrated chain margins were also supported by healthy

intermediary spreads; PX up 3%, while MEG margins up 14% YoY.

Exhibit 23: Integrated polyester spreads have remained steady

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

1QFY

14

2QFY

14

3QFY

14

4QFY

14

1QFY

15

2QFY

15

3QFY

15

4QFY

15

1QFY

16

2QFY

16

3QFY

16

4QFY

16

Rs/

kg

Rs/

kgPOY integ PSF integ (RHS)

Source: Company Data, PL Research

Reliance Industries

May 12, 2016 17

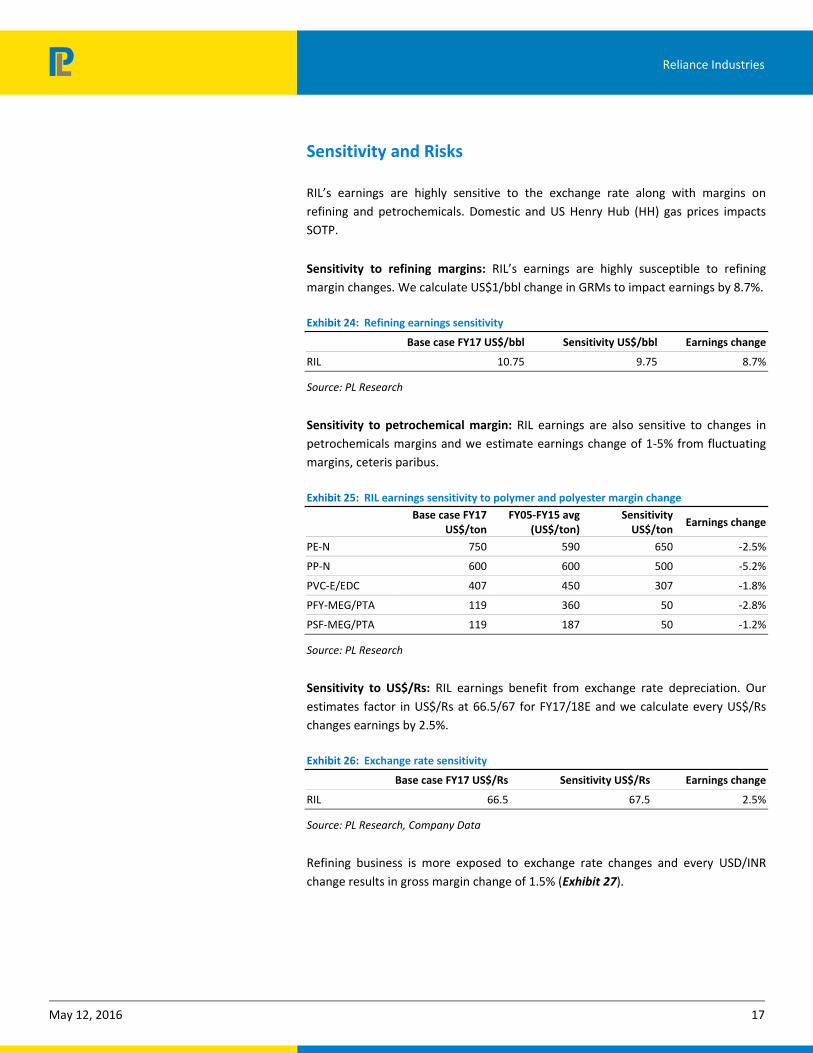

Sensitivity and Risks

RIL’s earnings are highly sensitive to the exchange rate along with margins on

refining and petrochemicals. Domestic and US Henry Hub (HH) gas prices impacts

SOTP.

Sensitivity to refining margins: RIL’s earnings are highly susceptible to refining

margin changes. We calculate US$1/bbl change in GRMs to impact earnings by 8.7%.

Exhibit 24: Refining earnings sensitivity

Base case FY17 US$/bbl Sensitivity US$/bbl Earnings change

RIL 10.75 9.75 8.7%

Source: PL Research

Sensitivity to petrochemical margin: RIL earnings are also sensitive to changes in

petrochemicals margins and we estimate earnings change of 1-5% from fluctuating

margins, ceteris paribus.

Exhibit 25: RIL earnings sensitivity to polymer and polyester margin change

Base case FY17

US$/ton FY05-FY15 avg

(US$/ton) Sensitivity

US$/ton Earnings change

PE-N 750 590 650 -2.5%

PP-N 600 600 500 -5.2%

PVC-E/EDC 407 450 307 -1.8%

PFY-MEG/PTA 119 360 50 -2.8%

PSF-MEG/PTA 119 187 50 -1.2%

Source: PL Research

Sensitivity to US$/Rs: RIL earnings benefit from exchange rate depreciation. Our

estimates factor in US$/Rs at 66.5/67 for FY17/18E and we calculate every US$/Rs

changes earnings by 2.5%.

Exhibit 26: Exchange rate sensitivity

Base case FY17 US$/Rs Sensitivity US$/Rs Earnings change

RIL 66.5 67.5 2.5%

Source: PL Research, Company Data

Refining business is more exposed to exchange rate changes and every USD/INR

change results in gross margin change of 1.5% (Exhibit 27).

Reliance Industries

May 12, 2016 18

Exhibit 27: RIL refining earnings sensitivity to USD movement

Refining capacity (MTPA) 69 69

Raw material -crude oil prices ($/bbl) 50 50

Refining margin ($/bbl) 10 10

Finished product selling price ($/bbl) 60 60

$/INR 66.5 67.5

(Rs m)

Sales 2,009,763 2,039,985

Raw material 1,674,803 1,699,988

Gross margin 334,961 339,998

$/INR sensitivity (%) 1.5%

Source: PL Research

Sensitivity to domestic gas prices: RIL’s KGD6 contribution has come off with

flagging volumes; factored in 9/8mmscmd volumes for FY17/18E. We have built-in

domestic gas prices of US$3.8/4.02mmbtu for FY17/18E. With domestic gas prices

now tied to international averages, our SOTP value of E&P come off to Rs38/sh

(Rs31/sh in base case) if the long term gas prices come off to US$3.2/mmbtu.

Sensitivity to HH prices: RIL has invested ~US$6.5bn on their shale venture, adjusted

for recent divestures. However, US HH prices have been under pressure led by rising

supplies and trailing demand trend. Accordingly, FY16 EBITDA came off to US$236m

(-65%YoY). We have factored in US$2.0/2.5/2.7/mmbtu for CY16/17/18E with

US$3/mmbtu as the long-term average. We calculate that the SOTP value of US

shale business would come off to Rs(29)/sh in the event of long-term gas prices

come off to US$2.5/mmbtu (US$3/mmbtu in base case).

RJio: RIL is in the final phase of testing the next generation mobile data services. The

company has invested Rs1.2trn till date and plans to invest Rs300bn in FY17E to

expand its network footprint to 90% from current 70% coverage area. RJio expects

to receive 800MHz spectrum from RCom in next few weeks, following which the

spectrum is likely to be integrated.

RJio have already on boarded 0.5m subscribers on a trial basis and average monthly

consumption is impressive at ~18GB per month, much higher than resent data usage

of ~700MB.

Ecosystem rapidly growing: The 4G ecosystem is expanding rapidly as over 45m LTE

smartphones are already in the market. LTE smart phone volume market share has

increased to 62% in January 2016 against 11% last year. With LTE smart phone prices

now dropping to <Rs3500, the LTE ecosystem is expected to get a major boost.

Reliance Industries

May 12, 2016 19

However, given the intensely competitive domestic telecom landscape, RJio’s

profitability is likely to be back-ended and will act as an overhang for stock

performance.

Exhibit 28: India mobile Smartphone shipment data as on January 2016

Source: GfK Nielsen India Pvt Ltd

Reliance Industries

May 12, 2016 20

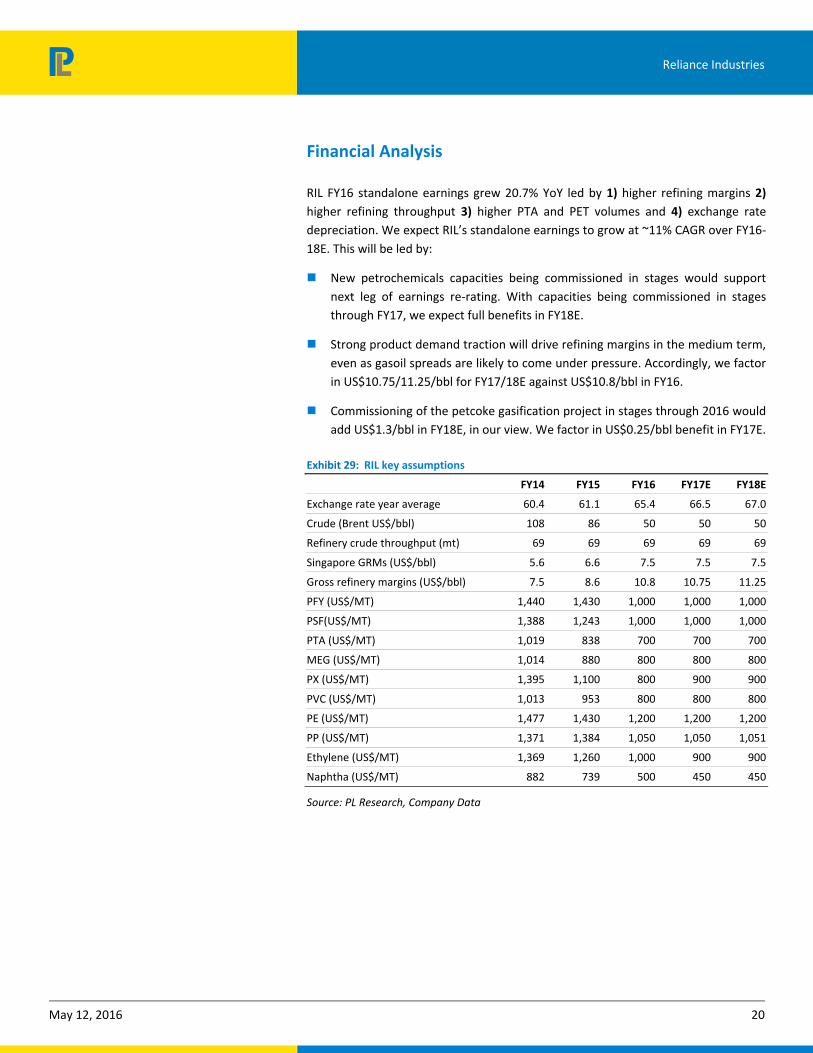

Financial Analysis

RIL FY16 standalone earnings grew 20.7% YoY led by 1) higher refining margins 2)

higher refining throughput 3) higher PTA and PET volumes and 4) exchange rate

depreciation. We expect RIL’s standalone earnings to grow at ~11% CAGR over FY16-

18E. This will be led by:

New petrochemicals capacities being commissioned in stages would support

next leg of earnings re-rating. With capacities being commissioned in stages

through FY17, we expect full benefits in FY18E.

Strong product demand traction will drive refining margins in the medium term,

even as gasoil spreads are likely to come under pressure. Accordingly, we factor

in US$10.75/11.25/bbl for FY17/18E against US$10.8/bbl in FY16.

Commissioning of the petcoke gasification project in stages through 2016 would

add US$1.3/bbl in FY18E, in our view. We factor in US$0.25/bbl benefit in FY17E.

Exhibit 29: RIL key assumptions

FY14 FY15 FY16 FY17E FY18E

Exchange rate year average 60.4 61.1 65.4 66.5 67.0

Crude (Brent US$/bbl) 108 86 50 50 50

Refinery crude throughput (mt) 69 69 69 69 69

Singapore GRMs (US$/bbl) 5.6 6.6 7.5 7.5 7.5

Gross refinery margins (US$/bbl) 7.5 8.6 10.8 10.75 11.25

PFY (US$/MT) 1,440 1,430 1,000 1,000 1,000

PSF(US$/MT) 1,388 1,243 1,000 1,000 1,000

PTA (US$/MT) 1,019 838 700 700 700

MEG (US$/MT) 1,014 880 800 800 800

PX (US$/MT) 1,395 1,100 800 900 900

PVC (US$/MT) 1,013 953 800 800 800

PE (US$/MT) 1,477 1,430 1,200 1,200 1,200

PP (US$/MT) 1,371 1,384 1,050 1,050 1,051

Ethylene (US$/MT) 1,369 1,260 1,000 900 900

Naphtha (US$/MT) 882 739 500 450 450

Source: PL Research, Company Data

Reliance Industries

May 12, 2016 21

Valuation and View

We have valued RIL based on SOTP, given the well-diversified nature of the

company. Salient highlights of the valuation matrix are:

We have valued core refining and petrochemicals at 7x FY17E EBITDA.

We have added incremental value of full blown EBITDA from new projects,

reflected in FY18E and discounted the same at 12%.

We have taken net debt based on FY17E.

We have valued domestic Exploration & Production (E&P) on DCF and assumed

long-term gas price of US$4.2/mmbtu. We have also added 10% premium to the

blocks yet to be monetized. We have assumed 9/8mmscmd gas volumes at

KGD6 volumes against ~11 mmscmd for FY16.

RJio is being valued at 8x FY18 EV/E and discounted back to FY17.

Reliance Retail is being valued based on peer valuation comparison.

Exhibit 30: RIL SOTP

(Rs bn) (Rs / share) Comments

EV of Petrochem & Refining 2,195 991 @ EV/EBITDA of 7x FY17E

Less: Net Debt 540 184 Estimated as on FY17E, net of cash and liquid investments

Add: Key investments

- E&P Assets 103 35 @10% premium to NAV of known reserves (D6, NEC, CBM)

- Organised retail & other key investments 80 27 On book value of investment in retail and Infra subs

- Infotel (BWA) -130 -44 Based on RJio's 8x FY18E EV/E discounted back

- Shale Gas NPV (Marcellus + Eagle Ford) -75 -25 NPV based on HH of US$2-2.5/mmbtu

- New projects 687 234 EV of new petchem projects @EV/EBITDA of 7x

Total value of investments & other assets 665 226

Equity value (Rs m) 3,039 1,034

Source: PL Research

Reliance Industries

May 12, 2016 22

Income Statement (Rs m)

Y/e March 2015 2016 2017E 2018E

Net Revenue 3,287,720 2,331,580 2,938,657 3,115,302

Raw Material Expenses 2,843,930 1,826,939 2,355,025 2,405,927

Gross Profit 443,790 504,641 583,632 709,375

Employee Cost — — — —

Other Expenses 127,080 103,251 155,856 171,667

EBITDA 316,710 401,390 427,776 537,708

Depr. & Amortization 84,880 95,660 107,468 129,131

Net Interest 23,670 24,540 36,902 38,239

Other Income 86,520 75,820 71,111 73,368

Profit before Tax 294,680 357,010 354,516 443,705

Total Tax 67,490 82,840 85,263 108,286

Profit after Tax 227,190 274,170 269,254 335,419

Ex-Od items / Min. Int. — — — —

Adj. PAT 227,190 274,170 269,254 335,419

Avg. Shares O/S (m) 3,236.0 3,240.0 3,240.0 3,240.0

EPS (Rs.) 70.2 84.6 83.1 103.5

Cash Flow Abstract (Rs m)

Y/e March 2015 2016 2017E 2018E

C/F from Operations 493,701 370,709 531,974 511,094

C/F from Investing (475,340) (575,390) (219,120) (26,700)

C/F from Financing (325,729) 210,616 (173,045) (419,907)

Inc. / Dec. in Cash (307,368) 5,935 139,809 64,487

Opening Cash 366,240 115,710 68,920 75,812

Closing Cash 115,710 68,920 75,812 83,393

FCFF 322,950 (695,579) 204,468 322,174

FCFE 408,239 (677,462) 252,942 354,779

Key Financial Metrics

Y/e March 2015 2016 2017E 2018E

Growth

Revenue (%) (15.7) (29.1) 26.0 6.0

EBITDA (%) 2.9 26.7 6.6 25.7

PAT (%) 3.3 20.7 (1.8) 24.6

EPS (%) 3.2 20.5 (1.8) 24.6

Profitability

EBITDA Margin (%) 9.6 17.2 14.6 17.3

PAT Margin (%) 6.9 11.8 9.2 10.8

RoCE (%) 8.0 8.7 8.3 9.8

RoE (%) 11.0 12.0 11.0 13.2

Balance Sheet

Net Debt : Equity 0.4 0.4 0.4 0.4

Net Wrkng Cap. (days) (5) (4) (20) (21)

Valuation

PER (x) 13.9 11.5 11.7 9.4

P / B (x) 1.5 1.3 1.3 1.2

EV / EBITDA (x) 12.7 10.2 9.7 7.7

EV / Sales (x) 1.2 1.8 1.4 1.3

Earnings Quality

Eff. Tax Rate 22.9 23.2 24.1 24.4

Other Inc / PBT 29.4 21.2 20.1 16.5

Eff. Depr. Rate (%) 3.6 2.8 2.9 3.4

FCFE / PAT 179.7 (247.1) 93.9 105.8

Source: Company Data, PL Research.

Balance Sheet Abstract (Rs m)

Y/e March 2015 2016 2017E 2018E

Shareholder's Funds 2,161,760 2,401,760 2,473,550 2,602,368

Total Debt 984,969 1,003,086 1,051,560 1,084,165

Other Liabilities 180,551 200,595 209,396 221,675

Total Liabilities 3,327,280 3,605,441 3,734,506 3,908,209

Net Fixed Assets 1,903,160 2,382,890 2,494,542 2,392,111

Goodwill — — — —

Investments 1,485,950 1,291,153 1,416,070 1,688,948

Net Current Assets (61,830) (68,602) (176,106) (172,849)

Cash & Equivalents 115,710 68,920 75,812 83,393

Other Current Assets 473,030 397,101 378,907 385,851

Current Liabilities 650,570 534,623 630,825 642,093

Other Assets — — — —

Total Assets 3,327,280 3,605,441 3,734,506 3,908,210

Quarterly Financials (Rs m)

Y/e March Q1FY16 Q2FY16 Q3FY16 Q4FY16

Net Revenue 658,170 608,170 565,670 499,570

EBITDA 93,070 98,330 102,720 107,270

% of revenue 14.1 16.2 18.2 21.5

Depr. & Amortization 22,650 23,720 24,050 25,240

Net Interest 5,970 6,940 6,090 5,540

Other Income 18,180 16,170 22,890 18,580

Profit before Tax 82,630 83,840 95,470 95,070

Total Tax 19,450 18,230 23,290 21,870

Profit after Tax 63,180 65,610 72,180 73,200

Adj. PAT 63,180 65,610 72,180 73,200

Key Operating Metrics

Y/e March 2015 2016 2017E 2018E

Brent (US$/bbl) 85.6 50.0 50.0 50.0

GRM(US$/bbl) 8.6 10.9 11.0 11.6

Refining thruput (MTPA) 67.9 69.6 69.0 69.0

US$/Rs 61.1 65.4 66.5 67.0

Source: Company Data, PL Research.

Reliance Industries

May 12, 2016 23

THIS PAGE IS INTENTIONALLY LEFT BLANK

Reliance Industries

May 12, 2016 24

Prabhudas Lilladher Pvt. Ltd.

3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai-400 018, India

Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209

Rating Distribution of Research Coverage PL’s Recommendation Nomenclature

44.2%40.7%

15.0%

0.0%0%

10%

20%

30%

40%

50%

BUY Accumulate Reduce Sell

% o

f To

tal C

ove

rage

BUY : Over 15% Outperformance to Sensex over 12-months

Accumulate : Outperformance to Sensex over 12-months

Reduce : Underperformance to Sensex over 12-months

Sell : Over 15% underperformance to Sensex over 12-months

Trading Buy : Over 10% absolute upside in 1-month

Trading Sell : Over 10% absolute decline in 1-month

Not Rated (NR) : No specific call on the stock

Under Review (UR) : Rating likely to change shortly

DISCLAIMER/DISCLOSURES

ANALYST CERTIFICATION

We/I, Mr. Avishek Datta (MBA), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

Prabhudas Lilladher Pvt. Ltd, Mumbai, India (hereinafter referred to as “PL”) is engaged in the business of Stock Broking, Portfolio Manager, Depository Participant and distribution for third party financial products. PL is a subsidiary of Prabhudas Lilladher Advisory Services Pvt Ltd. which has its various subsidiaries engaged in business of commodity broking, investment banking, financial services (margin funding) and distribution of third party financial/other products, details in respect of which are available at www.plindia.com

This document has been prepared by the Research Division of PL and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of PL. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security.

The information contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy or completeness of the same. Neither PL nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor.

Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication.

PL may from time to time solicit or perform investment banking or other services for any company mentioned in this document.

PL is in the process of applying for certificate of registration as Research Analyst under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

PL submits that no material disciplinary action has been taken on us by any Regulatory Authority impacting Equity Research Analysis activities.

PL or its research analysts or its associates or his relatives do not have any financial interest in the subject company.

PL or its research analysts or its associates or his relatives do not have actual/beneficial ownership of one per cent or more securities of the subject company at the end of the month immediately preceding the date of publication of the research report.

PL or its research analysts or its associates or his relatives do not have any material conflict of interest at the time of publication of the research report.

PL or its associates might have received compensation from the subject company in the past twelve months.

PL or its associates might have managed or co-managed public offering of securities for the subject company in the past twelve months or mandated by the subject company for any other assignment in the past twelve months.

PL or its associates might have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

PL or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months

PL or its associates might have received any compensation or other benefits from the subject company or third party in connection with the research report.

PL encourages independence in research report preparation and strives to minimize conflict in preparation of research report. PL or its analysts did not receive any compensation or other benefits from the subject Company or third party in connection with the preparation of the research report. PL or its Research Analysts do not have any material conflict of interest at the time of publication of this report.

It is confirmed that Mr. Avishek Datta (MBA), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

The research analysts for this report has not served as an officer, director or employee of the subject company PL or its research analysts have not engaged in market making activity for the subject company

Our sales people, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all o the foregoing, among other things, may give rise to real or potential conflicts of interest.

PL and its associates, their directors and employees may (a) from time to time, have a long or short position in, and buy or sell the securities of the subject company or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company or act as an advisor or lender/borrower to the subject company or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.

DISCLAIMER/DISCLOSURES (FOR US CLIENTS)

ANALYST CERTIFICATION

The research analysts, with respect to each issuer and its securities covered by them in this research report, certify that: All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their securities; and No part of his or her or their compensation was, is or will be directly related to the specific recommendation or views expressed in this research report

Terms & conditions and other disclosures:

This research report is a product of Prabhudas Lilladher Pvt. Ltd., which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Prabhudas Lilladher Pvt. Ltd. only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Prabhudas Lilladher Pvt. Ltd. has entered into an agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo").

Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer.