44

Reliance Infrastructure Ltd. February, 2010 Investor Presentation

Reliance Infrastructure Ltd.

February, 2010

Investor Presentation

2

Forward looking statements – Important NoteThis presentation and the discussion that follows may contain “forward looking statements”by Reliance Infrastructure that are not historical in nature. These forward looking statements, which may include statements relating to future results of operation, financial condition, business prospects, plans and objectives, are based on the current beliefs, assumptions, expectations, estimates, and projections of the directors and management of Reliance Infrastructure about the business, industry and markets in which Reliance Infrastructure operates. These statements are not guarantees of future performance, and are subject to known and unknown risks, uncertainties, and other factors, some of which are beyond Reliance Infrastructure control and difficult to predict, that could cause actual results, performance or achievements to differ materially from those in the forward looking statements. Such statements are not, and should not be construed, as a representation as to future performance or achievements of Reliance Infrastructure. In particular, such statements should not be regarded as a projection of future performance of Reliance Infrastructure. It should be noted that the actual performance or achievements of Reliance Infrastructure may vary significantly from such statements.

3

Power Business EPC Business Infrastructure Business

Business Overview

Generation

Transmission

Distribution

Trading

Airports

Real Estate/SEZ’s

Metros

RoadsPower Sector

Road Sector

4

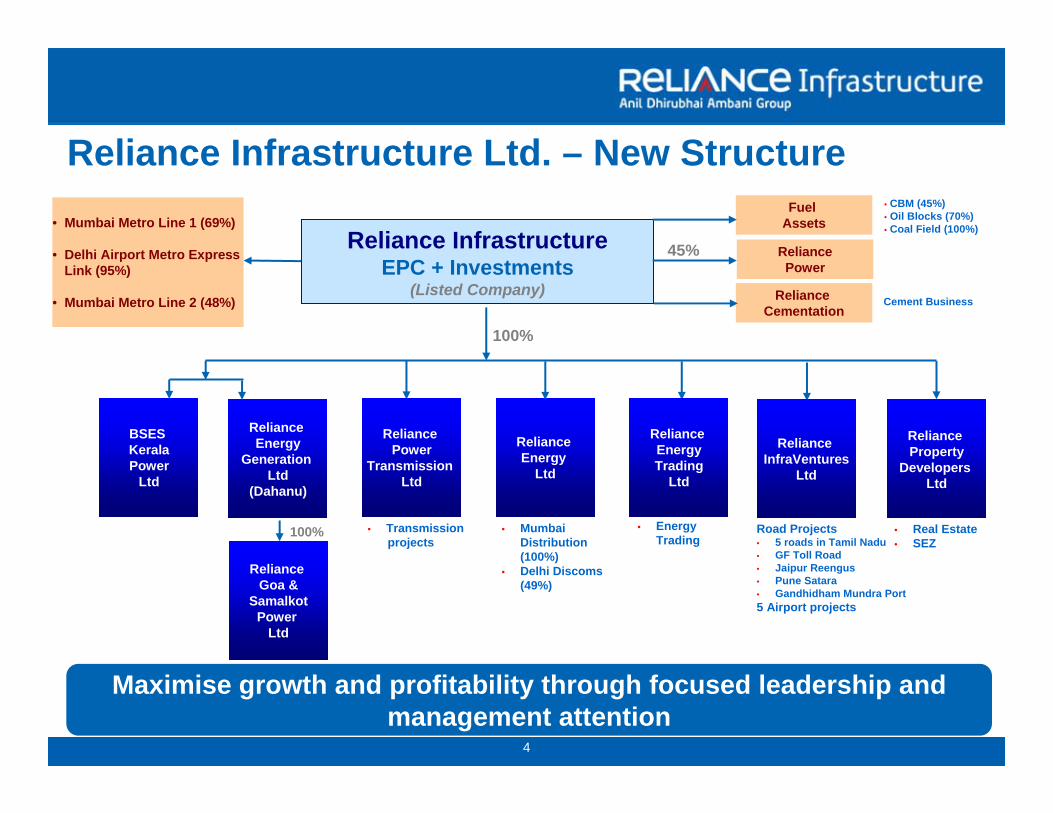

Reliance Infrastructure Ltd. – New Structure

45%

100%

• Energy Trading

• CBM (45%)• Oil Blocks (70%)• Coal Field (100%)

Road Projects• 5 roads in Tamil Nadu• GF Toll Road• Jaipur Reengus• Pune Satara• Gandhidham Mundra Port5 Airport projects

100%

Fuel Assets

• Mumbai Distribution (100%)

• Delhi Discoms (49%)

• Transmission projects

• Real Estate• SEZ

Maximise growth and profitability through focused leadership and management attention

• Mumbai Metro Line 1 (69%)

• Delhi Airport Metro Express Link (95%)

• Mumbai Metro Line 2 (48%)

Reliance InfrastructureEPC + Investments

(Listed Company)

Reliance EnergyTrading

Ltd

Reliance Energy

Ltd

Reliance InfraVentures

Ltd

Reliance Property

Developers Ltd

Reliance Power

Transmission Ltd

Reliance Energy

Generation Ltd

(Dahanu)

BSES KeralaPower

Ltd

ReliancePower

Reliance Cementation

Reliance Goa &

SamalkotPower

Ltd

Cement Business

Power Business

6

Power Generation

Operate one-of-the-most efficient thermal plants of India

Wind

Naptha

Combined Cycle

Combined Cycle

Thermal

Type

Karnataka Power Transmission Corp. Ltd

8 MWWind Farm, Karnataka

Kerela State Electricity Board165 MWKerela Power Station,

Goa Grid

Andhra Pradesh Grid

Mumbai Discom

Off-take Arrangements

48 MW

220 MW

500 MW

Capacity

Goa Power Station

Samalkot Power Station

Dahanu Power Station

Parameter

Dahanu Station running at PLF of ~100% from last 6 yrs

Samalkot Station running at PLF of ~90% since December 09

Outperformance of norms leading to high ROEs

7

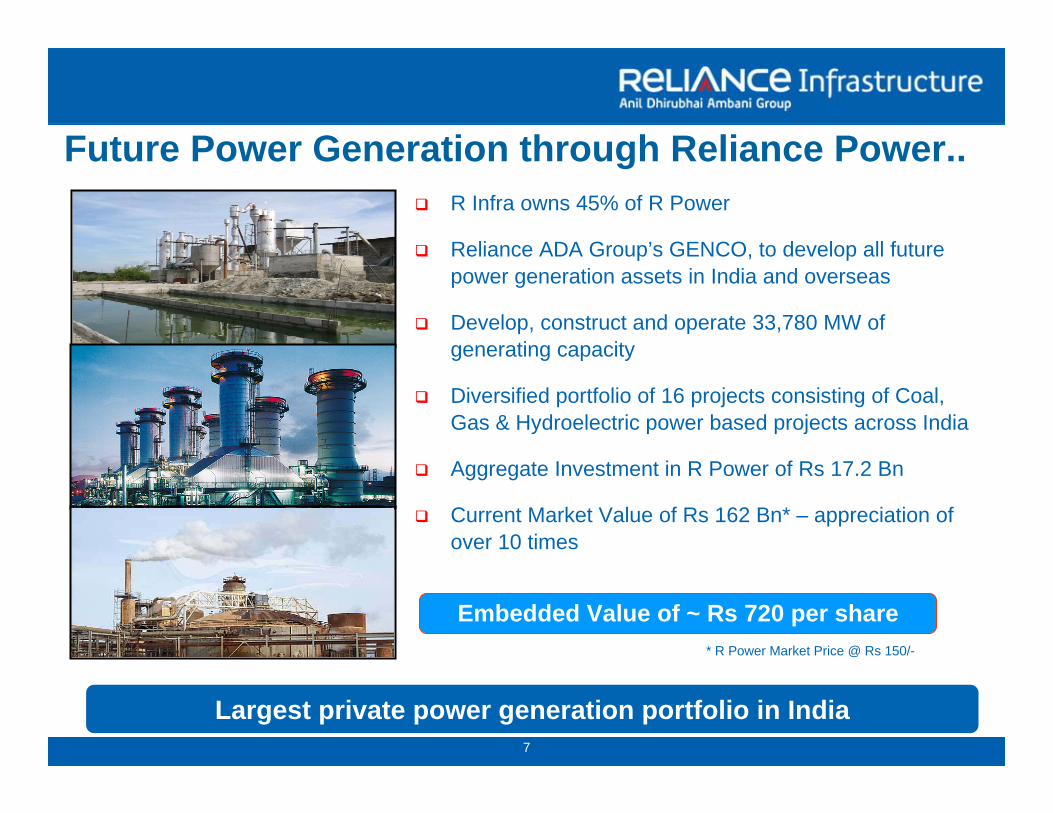

Future Power Generation through Reliance Power..

Largest private power generation portfolio in India

R Infra owns 45% of R Power

Reliance ADA Group’s GENCO, to develop all future power generation assets in India and overseas

Develop, construct and operate 33,780 MW of generating capacity

Diversified portfolio of 16 projects consisting of Coal, Gas & Hydroelectric power based projects across India

Aggregate Investment in R Power of Rs 17.2 Bn

Current Market Value of Rs 162 Bn* – appreciation of over 10 times

Embedded Value of ~ Rs 720 per share* R Power Market Price @ Rs 150/-

8

Rosa Phase I (600 MW)Rosa Phase II (600 MW)

Shahpur Coal (1,200 MW)Shahpur Gas (2,800 MW)

Sasan UMPP (3,960 MW)Chitrangi (3,960 MW)

Krishnapatnam UMPP (4,000 MW)Butibori (600 MW)

Dadri (7,480 MW)

Siyom (1,000 MW)Tato II (700 MW)

Kalai II (1,200 MWAmulin (420 MW)Emini (500 MW)

Mihundon (400 MW)

Urthing Sobla (400 MW)

4,620 MWHydroelectric

10,280 MWGas based

5,200 MWImported coal

13,680 MWDomestic coal

CapacityType

33,780 MW of power generation portfolio

Tilaiya UMPP (3,960 MW)

3,960 MWEast

4,220 MWNorth East

4,000 MWSouth

12,520 MWWest

9,080 MWNorth

CapacityRegional Grid

Reliance Power Ltd – Pan India Presence

9

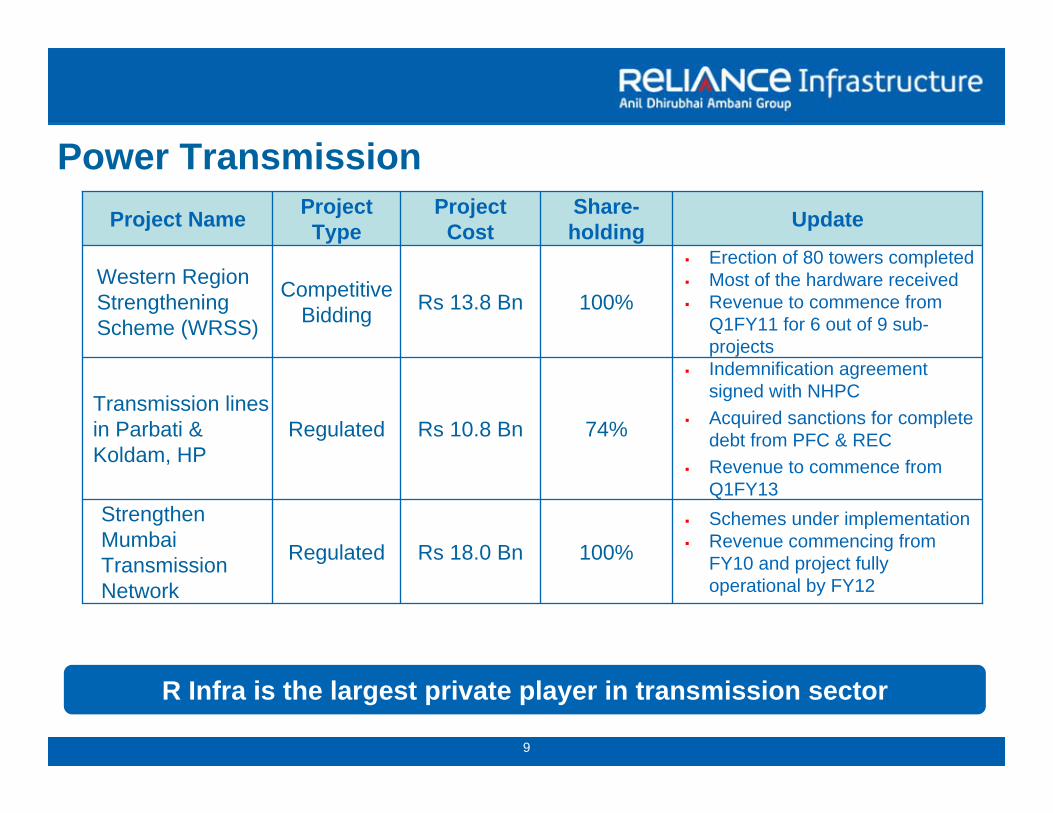

Power Transmission

Regulated

Regulated

Competitive Bidding

Project Type

Schemes under implementationRevenue commencing from FY10 and project fully operational by FY12

100%Rs 18.0 Bn

Strengthen Mumbai Transmission Network

Indemnification agreement signed with NHPCAcquired sanctions for complete debt from PFC & RECRevenue to commence from Q1FY13

74%Rs 10.8 BnTransmission lines in Parbati & Koldam, HP

Erection of 80 towers completedMost of the hardware receivedRevenue to commence from Q1FY11 for 6 out of 9 sub-projects

100%Rs 13.8 BnWestern Region Strengthening Scheme (WRSS)

UpdateShare-holding

Project CostProject Name

R Infra is the largest private player in transmission sector

10

Ultra Mega Transmission Projects

100%

100%

Share-holding

Competitive Bidding

Competitive Bidding

Project Type

Preferred Bidder, LOI awaitedRs 9 BnTalcher - II

Preferred Bidder, LOI awaitedRs 16 BnNorth

Karanpura

UpdateProject CostProject Name

Emerged preferred bidder in 2 out of 3 UMTP’s

Total transmission projects of over Rs 68 Bn

11

582Total

130Captive Projects

170Standalone State Projects

120Standalone Central Projects

1407 Projects at RFQ Stage

22Mumbai Transmission

Project Cost (Rs Bn)

Projects

Opportunities Ahead

Leadership position would play key role in emerging opportunities

12

Largest private sector distributor of power

Power Distribution

Serves 2 out 3 homes in Mumbai & DelhiServe over 5.2 million customers Distributes over 5,000 MW of power

Mumbai

13

Mumbai DistributionDistributing power to over 2.7 million customers

• 1,480 MW of peak demand• Adding 0.1 million customers every year

Among the lowest AT&C loss levels in the Country• AT&C losses of <11%• Reliability of 99.95%

Continuous upgradation and modernization undertaken

• Yearly investment of ~Rs 5 bn

Only utility without need for Invertors, Stabilizers and Generators

Technology driven organization

Awarded “Best Utility for Excellence” by IEEMA

14

Delhi Distribution

Privatised in 2002

R Infra own 49% in both discoms

Distributing power to over 2.56 million customers

2,630 MW of peak demand

AT&C loss reduction of ~35%In BRPL from 51% to 21%In BYPL from 63% to 24%

Discoms have invested Rs 34 Bn till date

Delhi Govt. saved Rs 200 Bn over last 7 years of privatization

Delhi success would lead to more private participation initiatives….

Earned Incentive of Rs 1.36 Bn in FY09 &expected to remain in incentive zone in FY10

27

23

31

21

3027

10

15

20

25

30

35

40

45

2006-07 2007-08 2008-09

AT &

C L

osse

s (%

)

BSES Rajdhani Power Limited

Incentive of

Rs 0.59 Bn

31

35

40

24

30

39

10

15

20

25

30

35

40

45

2006-07 2007-08 2008-09

AT &

C L

osse

s (%

)

BSES Yamuna Power Limited

Incentive of

Rs 0.77 Bn

Incentive of

Rs 0.58 Bn

Achieved Target

15

IT Initiative under R-APDRP* programmeEmpanelled under R-APDRP* Scheme as

IT Consultant

IT Implementation Agency

SCADA/DMS consultants

Providing IT consultancy to Karnataka State Electricity Board for 5 distribution circles

Bidding for IT implementation in following states:1. Andhra Pradesh2. Maharashtra3. Punjab4. Tamil Nadu5. Chattisgarh

* Restructured – Accelerated Power Development and Reform Programme

Total Opportunity of Rs 100 Bn

16

Opportunities Ahead - DistributionDistribution Franchisee is recognized as a way forward in power distribution business

Several states have initiated process under Franchisee model

Pursuing profitable opportunities in the space

6.02Haryana

3.53Madhya Pradesh

40.515Total

10.03Maharashtra

21.07Uttar Pradesh

Project Size (Rs Bn)

No. of CirclesStates

17

Reliance Energy Trading Ltd

Traded 2,237 MU’s till Dec 09 in FY10

Tied up with merchant and captive power plants for assured trading of 60,000 MU’s during 25 years

Integration with generation capacity of R Power & captive distribution businesses

Among the top 3 private players in trading market

1,022

1,934

2,237

FY08 FY09 YTD Dec 09

Number of units traded (in MU’s)

Achieved volume growth of over 100% in less than 2 years

EPC Business

19

EPC BusinessOrder Book of over Rs 189.7 Bn

R Power & Internal Power project: Rs 151.2 Bn• 3,960 MW Sasan UMPP• 300 MW Butibori group CPP^• Western Region Strengthening project, Maharashtra

and Gujarat

External: ~Rs 33.5 Bn• 1,200 MW Raghunathpur TPP*• 1,200 MW Rajiv Gandhi TPP* at Hisar• 500 MW Parichha TPP* BOP package

Road Project : GF Toll Road: Rs 5.0 Bn

Power projects under construction of over 7,200 MW

Dedicated manpower strength of over 1,550

* Thermal Power Project ^ Captive Power Project

20

EPC Business - Highlights

Foundation work in full swing and erection of towers initiated

WRSS Transmission Line

2,230 MT & 907 MT structure erection of Boiler Unit 1 & 2 is completed

Raghunathpur Power Plant

All sub-contract work are awarded and complete mobilization of resources is done

Gurgaon – FaridabadRoad

Boiler Foundation work nearing completionRaft work of Chimney is completed

Sasan UMPP

Shell Concrete Casting of Chimney upto 23 mtrs height is completedButibori Power Plant

Syncronized Unit 1 in December 09 –a record of 33 monthsFirst ever 600 MW unit executed in country

Hisar Power Plant

StatusEPC Projects

21

Signed MOU with Black & Veatch, USA Developing largest center for engineering excellence in India for engineering consultancy

Mentoring support to projects based on Super Critical Technology

Remote surveillance of project sites

Developing competencies in Roads, Metro Rail, Airports and Nuclear plants

Awarded first non-power project in road sector by “GF Toll Road Pvt Ltd”.

EPC Business – Major Initiatives

Recent foray in Road Sector

Infrastructure Business

23

25 years*

24 years*

18 years*

17 years*

25 - 30 years

20 years

Concession Period*

LOA received in Jan’ 1071-11.0Gandhidham Mundra Port Road

LOA received in October’ 0952-5.9Jaipur Reengus Corridor

LOA received in Jan’ 10Toll Collection to start

from Q1 FY11140-17.3Pune Satara Road

730 73.5Total

COD by Q1 FY126675:0:257.8Gurgaon Faridabad Toll Road

60:20:20

80:7:13

Funding(Debt : Grant :

Equity)

COD by Q3 FY1130424.03 Road Projects in TamilNadu (i.e TK,TD &SU)

Operational977.52 Road projects in Tamil Nadu (i.e NK & DS)

StatusLength (Km)

Project Cost

(Rs Bn)Project

Current road portfolio of Rs 73.5 Bn

Roads – Current Projects

* Including construction period

24

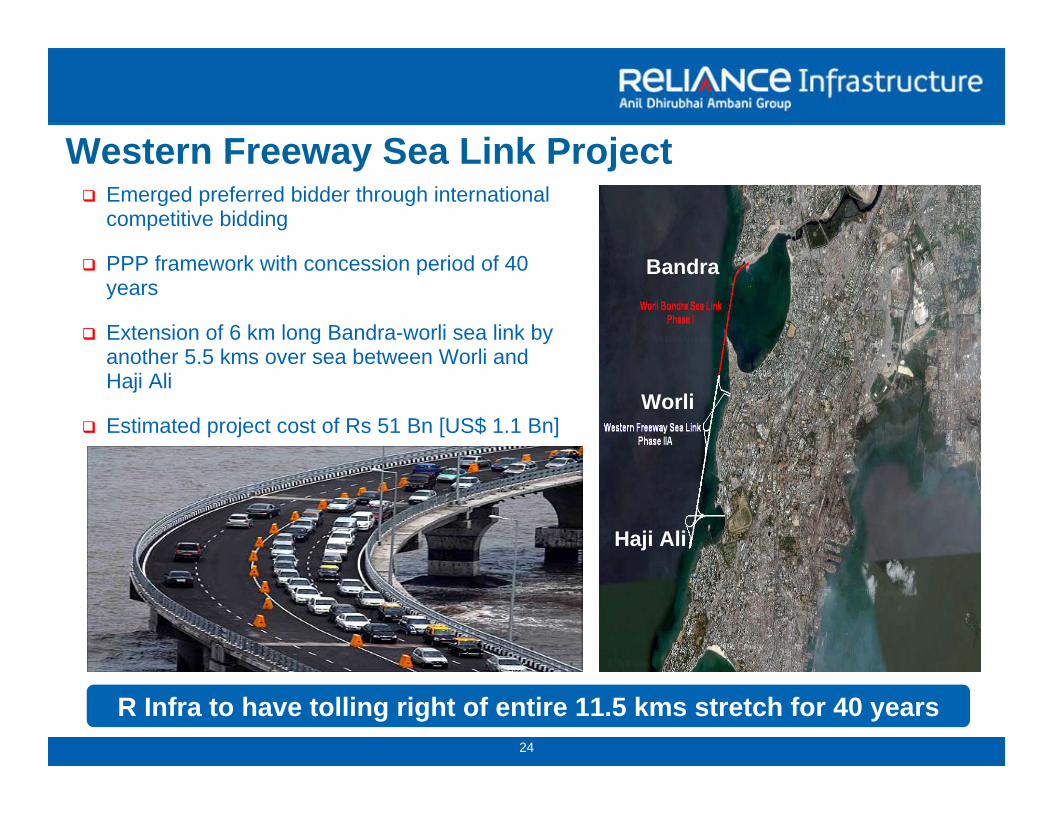

Emerged preferred bidder through international competitive bidding

PPP framework with concession period of 40 years

Extension of 6 km long Bandra-worli sea link by another 5.5 kms over sea between Worli and Haji Ali

Estimated project cost of Rs 51 Bn [US$ 1.1 Bn]

Western Freeway Sea Link Project

Haji Ali

Worli

Bandra

R Infra to have tolling right of entire 11.5 kms stretch for 40 years

Haji Ali

Worli

Bandra

25

37,554Total

18ICTT – Cochin

928SADRP

15,000Phase IV – Non NHAI

681Phase VII

1,000Phase VI

5,466Phase V

Phase IV

Phase III

Phase II

Phase I

Phase

5,000

8,459

716

6

To be awarded (Kms)

Ultra Mega Road Projects – Emerging Opportunity

Opportunity Landscape

Source: NHAI

Projects worth Rs 800 Bn would be in high traffic density

corridors

26

Total

RFQ to be submitted

RFQ submitted

RFP Stage

Stage

76

14

57

5

Number of Projects

625

130

428

67

Project Cost (Rs Bn)

9,000

1,650

6,800

550

Length (Km)

Expected to have road portfolio of Rs 200 Bn by FY12

Opportunities being pursued…

27

a) R Infra: 48%b) R Comm: 26%c) SNC Lavalin

(Canada): 26%35 Years^

Within 5 years from

financial closure

32-Rs 110.0 BnMumbai

Metro – Line II

2.33:0:1

51:27:22

Debt : Grant : Equity

a) R Infra: 95%b) CAF (Spain): 5%

a) R Infra: 69%b) MMRDA: 26% c) Veolia (France): 5%

Shareholding

30 YearsQ2 FY1123Rs 28.9 BnDelhi Airport Express Link Project

35 YearsQ2 FY1112Rs 23.5 BnMumbai Metro – Line I

Concession Period*CODLength

(Km)Project

Cost Project

R Infra is the only private player in Metro Rail

Metro Rail – Current Projects

* Including construction period ^ Could be extended for further 10 yrs

28

Mumbai Metro Line I ProjectElevated metro rail connecting Versova – Andheri – Ghatkopar

12 stations along the corridor

Capacity to move 0.6 Mn commuters per day; would reach upto 1.1 Mn in future

First metro rail project to private player

Simplex InfrastructureViaduct

Sew ConstructionStation Work

Sew InfrastructureSpecial Bridges

VNC Rail OneTrack work

ABBTraction & Power Supply

ThalesCommunication

SiemensSignaling

Consulting Engineering Services (CES)Traffic Study

CSR Nanjing Puzhen, ChinaRolling stock Supplier

Consortium of Parsons-Brinckerhoff (USA) & Systra (France)

Project Management Consultants

Business PartnersNature of work

Rs 88 km <Traffic>3 km

Rs 10 Traffic > 8 km

Rs 6 Traffic < 3 km

Fares at Base Year (2004)*Categories

* Fares to be increased @11% every 4th year

Major contractors

Fare Structure

Real Estate of 1,000 sqmtrs at each station

29

Mumbai Metro Line I – Status Update

Expected completion in Q3FY11 – 18 months ahead of contractual date

All car bodies of first train manufactured

Foundation work for Stations, Viaduct & Depot is almost completed

Foundation works for the Western Express Highway Special Bridge and the Mithi River Special Bridge is completed

Construction work at bridge over western railway track at Andheri is in full swing

Obtained viability gap funding of ~ Rs 2 Bnfrom MMRDA

30

Delhi Airport Metro Express Link Project

Metro express link connecting New Delhi Railway Station to Dwarka through IGI Airport

Traffic forecast: ~15,000 daily in initial year

Cushman & WakefieldReal Estate Potential Study

VNC Rail OneTrack work

SiemensSignaling & Traction

MVA Asia, Systra MVA ConsultingTraffic Consultant

Delhi Metro Rail Corporation (DMRC)Civil Contractor

CAF, SpainRolling stock Supplier

Mass Transit Railway Corporation (MTR), Hong Kong

Project Management Consultants

Business PartnersNature of work

Rs 30Between Dwarka Sector 21 & IGI Airport

Rs 150Between New Delhi Station & IGI Airport

Fares Categories

Major contractors

Fare Structure*

* Fares to be increased every 2 yr @ WPI

Real Estate area of 1,32,000 sqmtrs

Fastest, comfortable and economical commute to the airport

31

More than 80% of civil work has been completed

Track work on tunnels and viaducts are under progress

Factory acceptance test for major equipments of Power Supply, Tunnel ventilation, Signaling and Platform Screen Doors is completed.

Equipment delivery started at sites

Over 100 professionals from MTR (Hongkong) working along with in-house dedicated team

Loan disbursements started

Delhi Airport Metro Express Link – Status Update

Dwarka Sector 21

New Delhi

Shivaji Stadium

Dhaula Kuan

NH-8

IGI Airport

NH 8

New Delhi Station

Shivaji Stadium

Dhaula Kuan

Dwarka Sector 21

IG Airport

Expected completion in Q2FY11- Before Commonwealth Games

32

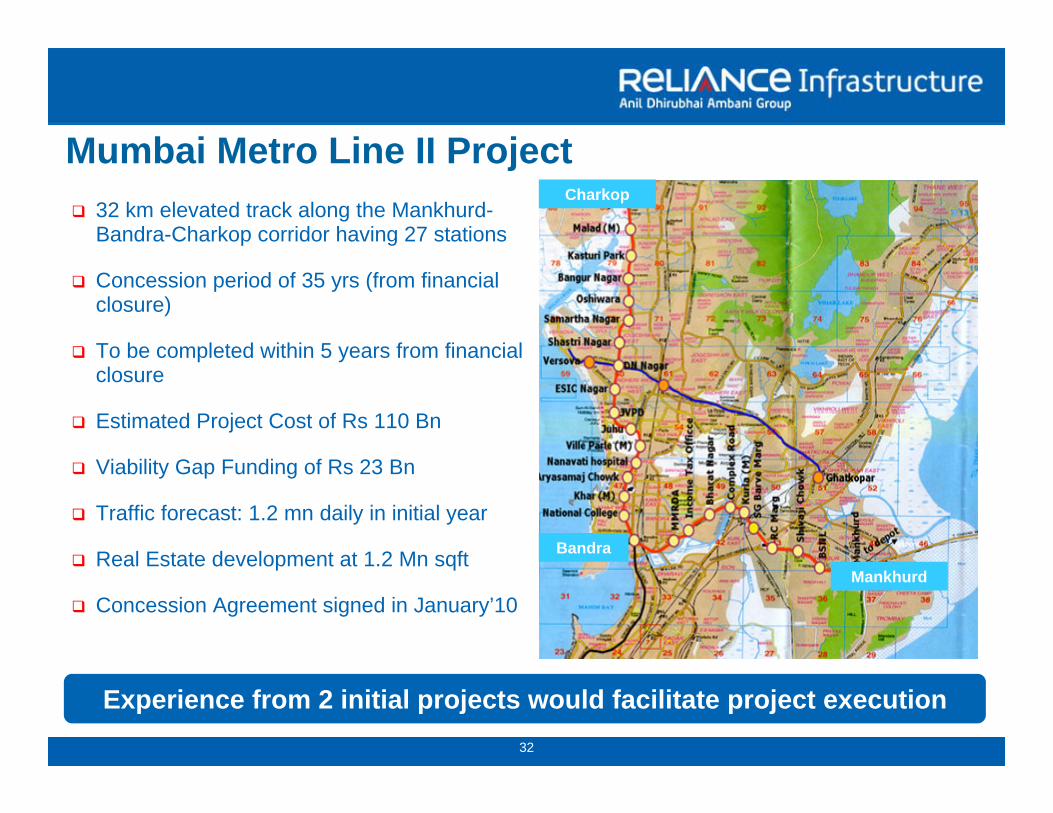

Mumbai Metro Line II Project32 km elevated track along the Mankhurd-Bandra-Charkop corridor having 27 stations

Concession period of 35 yrs (from financial closure)

To be completed within 5 years from financial closure

Estimated Project Cost of Rs 110 Bn

Viability Gap Funding of Rs 23 Bn

Traffic forecast: 1.2 mn daily in initial year

Real Estate development at 1.2 Mn sqft

Concession Agreement signed in January’10

Charkop

Bandra

Mankhurd

Experience from 2 initial projects would facilitate project execution

33

Metro Rail – Projects in Pipeline

Project cost of Rs 121 Bn72 km elevated track with 66 stations and 3 DepotsReal Estate development of 18.5 Mn sqftConcession period of 35 years extendable by 25 years

Hyderabad Metro

Bangalore High Speed Rail Link

Project cost of Rs 58 BnWill Connect the City Centre to the International Airport33 km elevated track (section within the Airport to be underground) with 4 stationsConcession period of 30 years Real Estate development at stations and Depot

Immense Opportunity to emerge….

Benefits of single and experienced player would play key role

34

Specialty Real Estate

Developing a 100 storeyed Trade Tower & Business District in Hyderabad on 80 acres of land

Unlimited FSI & no restriction on mix use

Clear titled land : APIIC in possession of the entire land

R Infra have 89% stake; 11% by APIIC

Strategic location – 6 kms from new international airport

CBD & Trade Tower SEZ

Setting-up IT/ITES SEZ at DAKC, NaviMumbai

Over 45 acres area - Initial saleable area of 4 Mn sqft

BOA approved and notification process underway

Complete land is in possession

35

AirportsAcquired developing & operating rights for 5 regional brown-field airports in Maharashtra

1. Nanded2. Latur3. Yavatmal4. Baramati5. Osmanabad

Lease period of 95 years

Lease deed executed for Nanded Airport & formally taken over

Scheduled Commercial Flights has started by Kingfisher Airlines from Nanded and LaturAirports

Signed a contract for a Training Academy at Nanded

36

Cement Business

Reliance Cementation Pvt. Ltd.

R Infra developing cement business at full swing...

To set-up 20 million tonne capacity over next 5 years with investment outlay of Rs 100 Bn

Setting up 5 million tonne integrated cement plant in Satna district, Madhya Pradesh

Setting up 5 million tonne integrated cement plant in Yavatmal, Maharashtra

Identifying other locations across India

In advance stage of achieving financial closure for Madhya Pradesh project

Financial Strengths

38

Looking Back – Standalone Financials

194.33

33.82

121.47

39.05

194.33

1.94

73.32

108.98

10.10

FY 09

183.24

52.36

90.71

40.17

183.24

1.74

44.18

125.11

12.21

9M FY 10

55.61Net Current Assets

169.24

77.26

36.37

169.24

2.49

49.89

106.68

10.19

FY 08

TOTAL

Investments

Fixed Assets

APPLICATION OF FUNDS

TOTAL

Deferred Tax Liability

Loan Funds

Reserves and Surplus

Share Capital & Warrants

SOURCES OF FUNDS

Standalone

Balance Sheet P&L A/c

11.39

11.93

3.30

17.67

10.30

98.69

FY 09

9.01

10.07

2.34

14.71

8.48

73.83

9M FY 10

10.85

11.50

3.09

16.82

7.62

64.48

FY 08

PAT

PBT

Interest

Total EBITDA

Operating EBITDA

Operating Income

Standalone

Cash & Cash Equivalent of over Rs 78 Bn as on December 31, 09

Debt free at net level

(Rs Bn)

39

Net worth of Rs 137 Bn

Capital infusion of ~Rs 40 Bn by issue of ~43 Mn warrants to promoters

Increase in Net Worth to Rs 165 Bn100.0225.3Total

12.828.7Indian Public

31.671.2Domestic Institutions-Financial Institution, Banks, Mutual Funds, LIC

17.639.8Foreign Institutional Investors

38.085.6Reliance Anil Dhirubhai Ambani Group

% HoldingNo. of Shares(In Million)

Category

Shareholding Pattern

As on December 31, 09

To sum up……

41

Partnership with Global leading players

42

Moving Ahead….Infrastructure - Expanding footprint in all high growth sectors : Fourteen Projects with aggregate outlay of Rs 315.9 Bn & growing……

Generation - Existing development pipeline of 33,780 MW in Reliance Power

• No further capital infusion required

Transmission - Implementing 3 projects with total outlay of Rs 43 Bn

Distribution - Existing distribution business to grow at 6% to 8% pa

Largest infrastructure company in the country…

43

Moving Ahead….EPC Business - Healthy EPC order book of over Rs 190 Bn

Power Trading - Among top 3 private players and business to grow steadily

Cement - Synergies with existing portfolio of businesses

Very healthy balance sheet to capitalize on growth opportunities

Growth at explosive pace……

Thank You