73

2011 - 2012 Renewable Energy Readiness Assessment Report: The GCC Countries

2011 - 2012

Renewable Energy ReadinessAssessment Report:

The GCC Countries

Organizational and Scientific Co-ordination

&

GCC Renewable Energy Readiness Report 2011 – 2012

1

Contents List of Tables ................................................................................................................................................. 3

List of Figures ................................................................................................................................................ 4

List of Acronyms ............................................................................................................................................ 5

Acknowledgements ....................................................................................................................................... 6

1 Introduction .......................................................................................................................................... 7

1.1 Motivation ..................................................................................................................................... 7

1.1 Renewable Energy Readiness ....................................................................................................... 8

1.2 Aim of this Report ......................................................................................................................... 9

1.3 Objectives...................................................................................................................................... 9

2 Energy Demand and the Deployment of Renewables ........................................................................ 10

2.1 Growing Energy Demand ............................................................................................................ 10

2.1.1 Global Energy Mix ............................................................................................................... 11

2.1.2 Future Energy Supply .......................................................................................................... 11

2.1.3 The GCC Energy Scenario .................................................................................................... 12

2.2 Deployment of Renewable Energy Technologies ....................................................................... 13

2.2.1 Drivers and Barriers to the Deployment of RETs ................................................................ 14

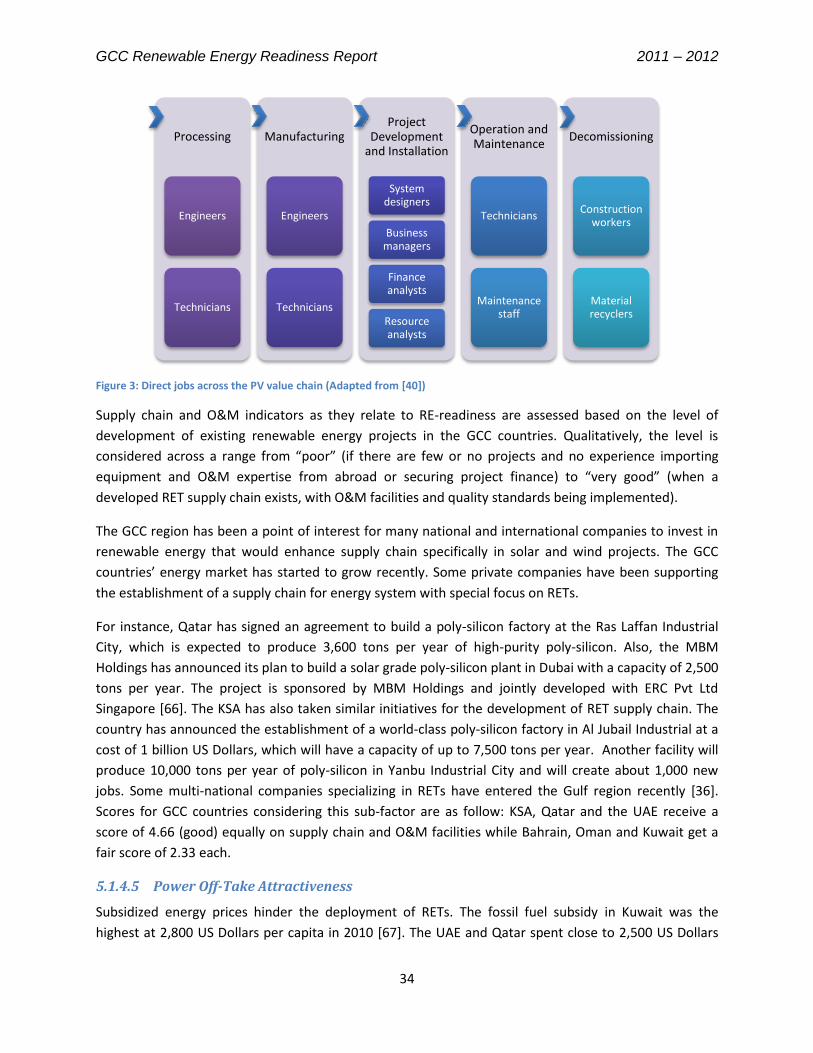

2.3 Potential Renewable Energy Jobs in the GCC Countries ............................................................. 15

3 Energy Demand and Renewable Energy Development Initiatives in the GCC Countries ................... 18

3.1 Bahrain ........................................................................................................................................ 18

3.1.1 RET Development Initiatives ............................................................................................... 18

3.2 Kingdom of Saudi Arabia ............................................................................................................. 18

3.2.1 RET Development Initiatives ............................................................................................... 19

3.2.2 Initiatives for Reducing Supply Side Energy Consumption ................................................. 19

3.2.3 Renewable Energy Program to Displace Fossil Fuels .......................................................... 19

3.3 Kuwait ......................................................................................................................................... 20

3.3.1 RET Development Initiatives ............................................................................................... 20

3.4 Oman ........................................................................................................................................... 21

3.4.1 RET Development Initiatives ............................................................................................... 21

3.5 Qatar ........................................................................................................................................... 21

3.5.1 RET Development Initiatives ............................................................................................... 21

3.5.2 National Research Funding Mechanisms ............................................................................ 23

GCC Renewable Energy Readiness Report 2011 – 2012

2

3.6 United Arab Emirates .................................................................................................................. 23

3.6.1 RET Development Initiatives ............................................................................................... 23

4 Methodology: Framework to Assess Renewable Energy Readiness .................................................. 24

5 Analysis of RE-Readiness Factors ........................................................................................................ 28

5.1 Infrastructure .............................................................................................................................. 28

5.1.1 Natural Resources ............................................................................................................... 28

5.1.2 Overall Country Infrastructure ............................................................................................ 30

5.1.3 Existing Grid Capacity .......................................................................................................... 30

5.1.4 Market Infrastructure ......................................................................................................... 30

5.1.5 Electricity Access Rate and Projected Demand................................................................... 36

5.2 Institutions .................................................................................................................................. 38

5.2.1 Public and Private Institutions Supporting RE..................................................................... 38

5.2.2 Key Policies .......................................................................................................................... 38

5.2.3 Renewable Energy Finance ................................................................................................. 42

5.2.4 Macroeconomic Environment ............................................................................................ 44

5.3 Human Capital ............................................................................................................................. 45

5.3.1 Technical and Commercial Skills ......................................................................................... 45

5.3.2 Adoption and Diffusion of New Technologies .................................................................... 48

5.3.3 Consumers, Investors and Decision Makers Awareness ..................................................... 49

6 Summary of Findings ........................................................................................................................... 51

6.1 Identified Gaps in GCC Countries ...................................................................................................... 55

6.2 SWOT Analysis ................................................................................................................................... 58

6.3 Priority Research Areas ..................................................................................................................... 59

7 Conclusions ......................................................................................................................................... 60

8 References .......................................................................................................................................... 62

9 Appendix ............................................................................................................................................. 68

GCC Renewable Energy Readiness Report 2011 – 2012

3

List of Tables Table 1: Key indicators of the GCC countries and world average (2009-2010)

Table 2: Global competitiveness scores of the GCC countries

Table 3: RE-readiness framework factors and respective weight

Table 4: The GCC countries energy reserve ranks and RE-readiness scores

Table 5: Solar and wind potential in the GCC countries

Table 6: Scoring criteria for competitive advantage of RETs

Table 7: Competitive advantages of RETs and RE-readiness scores

Table 8: Expected electricity demand growth and scores of RE-readiness

Table 9: The GCC countries RETs deployment targets and policy mechanism scores

Table 10: The GCC countries regulatory framework scores

Table 11: World ranking and financial market development scores

Table 12: RE Readiness Scores for Investment in RE Development

Table 13: Macroeconomic indicators, world ranks and competitiveness scores

Table 14: List of organizations and their R&D facilities in the GCC countries on renewable and sustainable energy

Table 15: The GCC countries RE-readiness scores and overall index

Table 16: The SWOT analysis for optimal deployment of renewables in the GCC countries

GCC Renewable Energy Readiness Report 2011 – 2012

4

List of Figures Figure 1: Average annual growth of renewable energy capacity

Figure 2: Applied methodology for this study

Figure 3: Direct jobs across the PV value chain

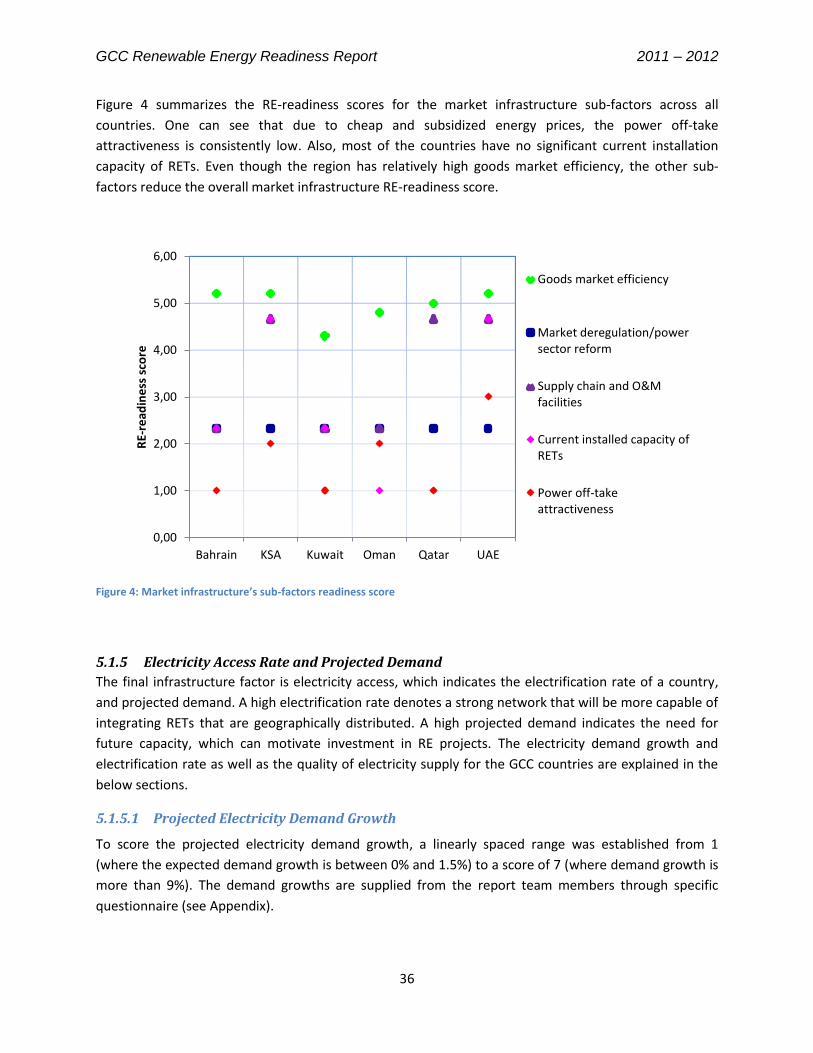

Figure 4: Market infrastructure sub-factors readiness score

Figure 5: RE-readiness for pillar 1: Infrastructure

Figure 6: RE-readiness for pillar 2: Institutions

Figure 7: RE-readiness for pillar 3: Human capital

Figure 8: GCC countries’ RE-readiness index

Figure 9: GCC countries’ attractiveness index on renewable energy development pillars

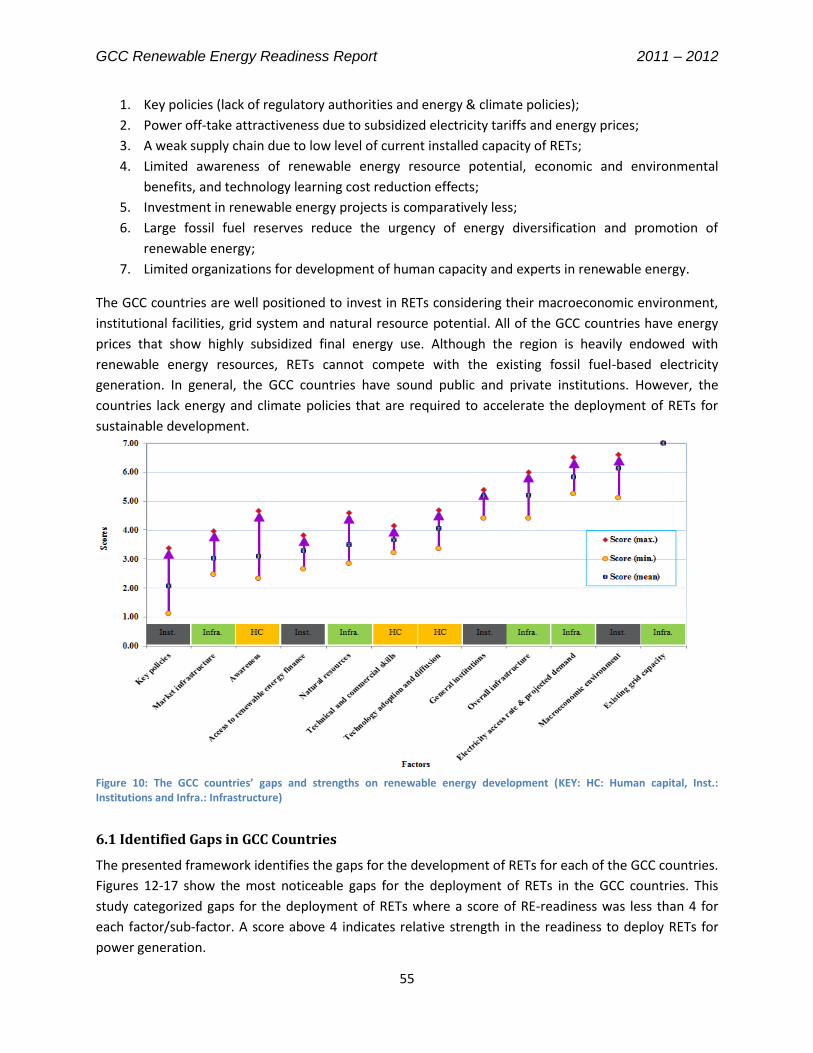

Figure 10 : GCC countries’ strengths and gaps on RE-readiness

Figure 11: RET deployment gaps in Bahrain

Figure 12: RET deployment gaps in the KSA

Figure 13: RET deployment gaps in Kuwait

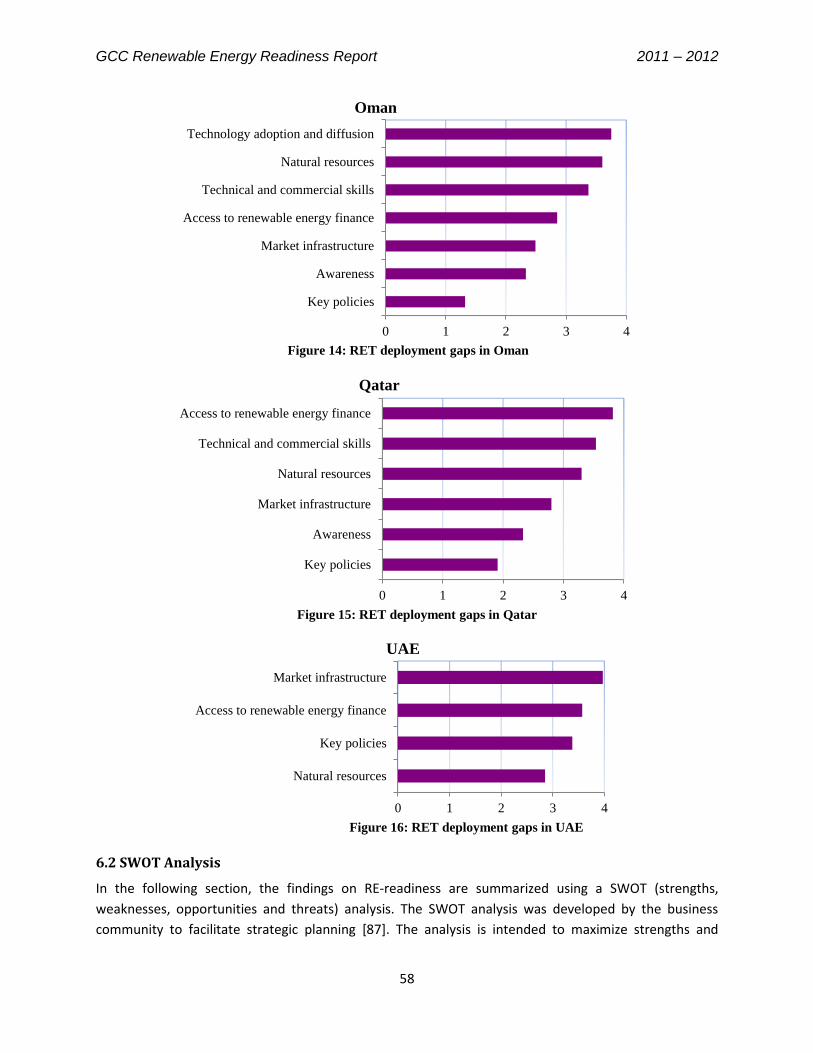

Figure 14: RET deployment gaps in Oman

Figure 15: RET deployment gaps in Qatar

Figure 16: RET deployment gaps in the UAE

GCC Renewable Energy Readiness Report 2011 – 2012

5

List of Acronyms AER: Authority for Electricity Regulation

BAPCO: Bahrain Petroleum Company

CDM: Clean Development Mechanism

COP18: 18th UNFCCC Conference of Parties

CSP: Concentrated Solar Power

DLR: German Aerospace Centre

E&Y: Ernst & Young

EWA: Electricity and Water Authority

EU: European Union

GCC: Gulf Cooperation Council

GCR: Global Competitiveness Report

GDP: Gross Domestic Product

GHG: Global Greenhouse Gas

GCI: Global Competitiveness Index

GW: Gigawatt

IAEA: International Atomic Energy Agency

IEA: International Energy Agency

IRENA: International Renewable Energy Agency

KACST: King Abdulaziz City for Science and Technology

KAUST: King Abdullah University of Science and

Technology

KA-CARE: King Abdullah City for Atomic and Renewable

Energy

KFUPM: King Fahd University of Petroleum and Minerals

KISR: Kuwait Institute for Scientific Research

KSA: Kingdom of Saudi Arabia

kW: kilowatt

kWh: kilowatt-hour

LNG: Liquefied natural gas

MCDM: Multi-criteria decision making

MEDRC: Middle East Desalination Research Centre

Mtoe: Million ton of oil equivalent

MW: Megawatt

NGO: Non-government organization

NPRP: National Priorities Research Program

NPRP-EP: NPRP-Exceptional Program

NRA: National Regulatory Authority

O&M: Operation and Maintenance

OECD: Organization for Economic Cooperation and

Development

OPEC: Organization of the Petroleum Exporting

Countries

PV: Photovoltaic

QNFSP: Qatar National Food Security Programme

QNRF: Qatar National Research Fund

QNRS: Qatar National Research Strategy

QSTP: Qatar Science and Technology Park

RE: Renewable Energy

RET: Renewable Energy Technology

RE-readiness: Renewable Energy readiness

R&D: Research and Development

SWOT: Strength, Weakness, Opportunity and Threat

SWERA: Solar and Wind Energy Resource Assessment

T&D: Transmission & Distribution

TCF: Trillion Cubic Feet

TWh: Terawatt-hour

UAE: United Arab Emirates

UN-FCCC: United Nations Framework Convention on

Climate Change

GCC Renewable Energy Readiness Report

6

Acknowledgements

This report was commissioned and financed by Masdar Institute of Science and Technology and produced in collaboration with the GCC Consortium Partners of the EU-GCC Clean Energy Network. A large share of the research for this report was conducted on a voluntary basis. Authors

Dr. Alam Mondal, Masdar Institute of Science and Technology, UAE

Diala Hawila, Masdar Institute of Science and Technology, UAE

Huden Serenat Khalil, Masdar Institute of Science and Technology, UAE

Dr. Toufic Mezher, Masdar Institute of Science and Technology, UAE

Section Authors

Dr. Rabia Ferroukhi and Arslan Khalid, Knowledge, Policy and Finance Centre, IRENA, UAE

Yousef M. Alyousef, Director, Energy Research Institute, King Abdulaziz City for Science and

Technology, Saudi Arabia

Abdul Sattar Al-Taie, Executive Director, Qatar National Research Fund (QNRF), Qatar

Foundation, Qatar

Lead Country Facilitators and Contributors

Dr. Abdullah Al-Badi, Sultan Qaboos University, Oman

Dr. Ibrahim Abdel Gelil and Maha Abdel Wahab, Arabian Gulf University, Bahrain

Dr. Rabi H. Mohtar and Dr. Mohammed Darwish, Qatar Environment and Energy Research

Institute, Qatar Foundation, Qatar

Dr. Salem F. Alhajraf, Innovative and Renewable Energy, Kuwait Institute of Scientific Research,

Kuwait

Dr. Sulaiman Al Mayman, King Abdulaziz City for Science and Technology, Saudi Arabia

Reviewers

Dr. Scott Kennedy, Masdar Institute of Science and Technology, UAE

Dr. Sgouris Sgouridis, Masdar Institute of Science and Technology, UAE

Abdulla Al Seiari, Masdar Institute of Science and Technology, UAE

Editing

Zarina Khan, Masdar Institute of Science and Technology, UAE

GCC Renewable Energy Readiness Report 2011 – 2012

7

1 Introduction

1.1 Motivation

Energy is a vital input for socio-economic development. Worldwide, the present trends of energy supply

and demand are not sustainable due to the expected gap between supply and demand in the future.

The fossil fuel reserves are limited and use of these fuels has a negative impact on the environment.

Holding energy at a secure level and global climate change at a safe level requires policies to be

connected to sustainable development strategies.

One may ask, however, why Gulf Cooperation Council (GCC) countries, endowed with substantial

reserves in oil and gas, should invest in alternative energy. There is a perceived opportunity cost of

diverting resources away from the oil and gas sector, which has high a return on investment. However,

this perception is relatively short-sighted and ignores both the near-term opportunities of economic

growth in the renewables sector as well as the long-term threats of falling behind in a transforming

energy economy.

On a purely economic basis, the GCC’s investment in the development of Renewable Energy

Technologies (RETs) provides an opportunity for a number of key benefits. First, facilitating the

diversification of the energy supply mix away from a reliance on petroleum and natural gas would

increase long-term energy security by exploiting a renewable, as opposed to finite, energy resource.

Second, reducing the domestic consumption of fossil fuels would increase oil and gas export revenue

potential and help prevent a near-term transition to the status of an energy importer for some countries

(e.g., the KSA, UAE), given current projections of rapidly increasing domestic energy demand. Third,

support for this sector would create opportunities for capital investment. Finally, the resulting economic

development can potentially create high value jobs within the region that can support the establishment

of the full renewable energy value-chain, including R&D, manufacturing, and local and international

deployment.

These benefits can only be realized through supportive policies that address the existing barriers

preventing growth in this sector. By tackling these challenges, the integration of RETs in the power

sector would not only support the sustainable development of the GCC region, but would also

contribute towards the region’s global responsibility for environmental protection.

Climate change and energy security1 [1, 2] are also important issues on the global arena which are

rapidly becoming equally important issues for the GCC. The region’s current energy situation shows a

trend of rapid energy demand growth. From 1997 to 2006, the primary energy consumption in the GCC

increased by almost 60% [3] at a rate of about 6.6% per year. Forecasts suggest that energy demand will

increase at an annual growth rate of 9.5% by 2020 [4].

1 Energy security refers to a consistent availability of sufficient supplies of primary energy. It involves the provision

of sufficient and reliable energy supplies to satisfy demand at all times and at affordable prices, while also avoiding environmental impacts [1, 2].

GCC Renewable Energy Readiness Report 2011 – 2012

8

Rapid development in the region has also resulted in a rise of CO₂ emissions of 33% to 35% between

2007 and 2008 [3]. Currently the CO₂ emissions per capita, per gross domestic product (GDP) and energy

intensities in the GCC countries are higher than the average of EU-25 and the average of the

Organization for Economic Co-operation and Development (OECD) countries [5]. Although the GCC

region represents 0.6% of the global population, it is responsible for 2.4% of the total greenhouse gas

(GHG) emissions produced globally [6].

With recent climate change modeling studies showing that the Arab region could face an increase in

surface temperature between 2 to 5.5°C by the end of the 21st century [7], all GCC countries have

responded by ratifying the Kyoto Protocol of the United Nations Framework Convention on Climate

Change (UNFCCC). In 2005, Kuwait, Oman, Qatar, the Kingdom of Saudi Arabia (KSA), and the United

Arab Emirates (UAE) all ratified the Kyoto Protocol. Bahrain was the last of the GCC countries to join the

Annex 1 party in 2006 [8].

Even with clear incentives to adopt RETs and a good potential resource base, the region’s transition

from conventional fossil dependence to widespread utilization of renewables is not an easy one.

Throughout the GCC region, domestic economies continue to enjoy significant subsidies on fossil fuels,

albeit while bearing the external costs associated with their use. Subsidies create a higher economic

barrier for adopting any alternatives, which is exacerbated by the high investment cost of RETs.

Given these barriers to RET development, GCC countries are required to provide both economic and

political interventions to support RETs. These interventions include legislation, incentives to investment,

generation targets, guidelines for energy conservation and strategies to stimulate the energy industry

[9, 10].

Assessment of renewable energy readiness (RE-readiness) is a useful approach for developing countries,

including the GCC, to find the gaps hindering deployment of RETs and to identify a country’s strengths

and weaknesses in regards to RET development. It is defined by the International Renewable Energy

Agency (IRENA) as an assessment of the key conditions for RET development and deployment in a

country, and the actions necessary to further improve these conditions of the conditions necessary for

the installation and ongoing operation of renewable energy facilities in a country [11].

1.1 Renewable Energy Readiness

IRENA defines readiness as “when actors are able to deploy renewables where they are the best option,

accounting for all economic, social and environmental criteria.” It conducts its assessments by looking at

“the current state of national readiness, across the project lifecycle, from national energy strategy and

policy, to building, operation and maintenance (O&M), with capacity-building cutting across all these

items” [11].

On a national level, RE-readiness is an indication of the country’s realization of the need for renewable

energy and its ability to introduce and support renewable energy projects. In this report, RE-readiness is

defined as the level of development of a county’s infrastructure, institutions and human capital factors

that influence the attractiveness of investing in renewable energy projects and play a role in enhancing

GCC Renewable Energy Readiness Report 2011 – 2012

9

the reliability of RETs to ensure their sustainable deployment. This report presents a RE-readiness

framework that can create a benchmark for comparison among different countries and to assess future

progress.

1.2 Aim of this Report

Prepared in partnership with GCC Consortium on Clean Energy through the European Union (EU) GCC

Clean Energy Network, this report aims to develop and disseminate an assessment framework to

evaluate GCC countries’ (RE-readiness) for deployment of (RETs).

A framework is adopted in which we apply a consistent methodology across all the GCC countries to

assess the current state of infrastructure, institutions and human capital to adopt and deploy RETs.

The framework is followed by an assessment of how conditions might be improved. The assessment will

enable countries to identify existing gaps and increase diffusion of RETs across a range of renewable

energy sources (solar and wind) resulting in improved energy security and reduced CO2 emissions.

1.3 Objectives

Through this study we hope to achieve the following objectives:

1) Foster understanding and development of RETs in GCC countries.

2) Provide a wider introduction to energy and environmental issues.

3) Develop a generic framework to assess RE-readiness of GCC countries as a case study.

4) Calculate the RE-readiness score for GCC countries and discuss the associated weaknesses and

strengths.

5) Identify priority areas for research and development related to renewable energy deployment.

Towards achieving these objectives, the report essentially serves as a benchmark to assess each

country’s RE- readiness, identifying gaps and providing recommendations to overcome the main barriers

to integrate renewable energy projects for power generation. It is useful for a first level benchmarking

of a country’s relative position against regional or global averages. However, one must recognize that

such an assessment reflects a best estimate, given currently available data, of an inherently dynamic

situation. As both the availability of data and the weight of the impact of factors behind the readiness

calculation are modified over time, the absolute scores will change and the rankings will be affected.

To meet the above mentioned objectives, this report is divided into the following sections:

Introduction: the motivation behind the study, definition of RE-readiness, aims and objectives of

this report.

Energy Demand and the Deployment of Renewables: section discusses the global and GCC

energy context, focusing on RET development, drivers and barriers to RETs. The potential of RE

jobs in the GCC as a major benefit of RET deployment in the region is also explored.

Energy Demand and Renewable Energy Development Initiatives in the GCC Countries: section

discusses the energy demand, consumption and the status of RET development initiatives in

each GCC country.

GCC Renewable Energy Readiness Report 2011 – 2012

10

Methodology: Framework to Assess RE-Readiness Factors

Analysis of RE-Readiness Factors: section discusses the factors’ and sub-factors’ scores of

infrastructure, institutions and human capital pillars.

Summary of Findings: section provides RE-readiness index and overall noticeable gaps for

development of RETs. This section also includes country-wide gaps, SWOT analysis and priority

research areas to deployment of RETs in the GCC countries.

Conclusions

2 Energy Demand and the Deployment of Renewables

This section provides an update of the current and future global energy scene: demand and supply,

diminishing fossil fuel reserves and the consequence of increasing global CO2 emissions. Within the

same context, the GCC energy scenario is discussed.

The second part of this section gives an overview of the benefits of RETs to meet growing energy

demand, growth status, drivers and barriers to deployment and deployment trends.

Lastly, the potential for renewable energy jobs in the GCC as a major benefit of RET deployment in the

region is explored.

2.1 Growing Energy Demand

The global primary energy demand in 1980 was 7,228 million ton of oil equivalent (Mtoe), the total

installed capacity of power generation was 1,945 gigawatt (GW). By 2008, global primary energy

demand had increased by 70% at 12,271 Mtoe with installed capacity increasing to 4,719 GW, of which

almost 70% was from fossil fuels [12].

In 2011, although the world primary energy consumption grew by 2.5%, roughly in line with the 10-year

average, consumption in OECD countries fell by 0.8%, the third decline in the past four years driven by

the global financial crisis. However, non-OECD consumption continued to grow by 5.3%, in line with the

10-year average. Global consumption growth decelerated in 2011 for all fuels, as did total energy

consumption for all regions [13]. This sudden shift in paradigms in recent year shows how energy plays a

vital role in the functioning of the world economy.

With improving global economic prospects, it is expected that over the next two decades, projected

electricity demand alone will require the installation of the same power generation capacity that was

installed over the entire 20th century [14].

Key factors driving this increase in energy demand can be summarized as follows:

Industrialization: particularly in emerging markets.

Increasing wealth: among rapidly developing countries, where often less efficient end-use

equipment are used.

Globalization: increasing transportation to further destinations with greater speed.

GCC Renewable Energy Readiness Report 2011 – 2012

11

Energy Security: while energy demand is typically driven by short-term considerations (e.g., GDP

growth, transport needs), long-term concerns over energy security worldwide are leading to

premiums being paid for energy assets.

2.1.1 Global Energy Mix

Conventional fossil fuels that provide energy in affordable, concentrated ready to use forms remain the

principal sources of energy worldwide. Currently, the global energy supply share of fossil fuels is about

80%. While only 20% of the worldwide total final energy demand is supplied by nuclear and renewable

energy sources [15].

Increasing global energy demand, most of which is being met by fossil fuels is causing an increase in CO₂

emissions. In 2012, a total of 35.6 billion tons of CO₂ emissions were generated worldwide, 2.6% more

than the previous year, mostly as a result of increased fossil fuel combustion. The emissions thus exceed

1990 levels (base year for the Kyoto Protocol) by almost 60% [16]. The IEA suggests that around 84% of

total CO₂ emissions are energy related [17] with 41% of emissions coming from fossil fuel-based power

generation alone [18].

A global decline in conventional coal, oil and natural gas reserves has been observed over recent

decades as these conventional fuels are not being newly formed at any significant rate, and thus their

reserves are ultimately finite. Unconventional fossil fuels, such as tar sands and shale oil and gas, have

recently seen a rapid rise in terms of their projected supply. While these unconventional sources will

likely have a major role to play in the global energy supply, they remain subject to the same drawbacks

as conventional sources: uneven distribution, finite resources, environmental impacts including GHG

emissions and other hazards.

2.1.2 Future Energy Supply

If the current rate of energy consumption is continued then conventional coal, oil and natural gas

reserves may last for 118, 46 and 58.6 years respectively [19]. On the other hand, unconventional

resources will likely last much longer [20].

The World Energy Outlook Factsheet on the evolution of global energy markets by 2035 suggests that

though renewables grow rapidly, fossil fuels remain the principal sources of energy worldwide. Demand

for oil, gas and coal grows in absolute terms through 2035, but their combined share of the global

energy mix falls from 81% to 75% during that period. The unlocking of unconventional resources

portends a very prominent future for natural gas, which nearly overtakes coal in the primary energy

supply mix by 2035 [21].

Nuclear power, in light of additional policy changes in several countries prompted by the accident at

Fukushima Daiichi has seen a downward revision from previous projections leading many to wait for a

new generation of proven nuclear reactors to minimize risks. Projections for 2035 suggest that nuclear

power will maintain a 12% share of electricity generation [21].

GCC Renewable Energy Readiness Report 2011 – 2012

12

Renewable energy deployment is driven by government incentives, falling costs, rising fossil fuel prices

and, in some cases, carbon pricing: their share of electricity generation grows from 20% in 2010 to 31%

by 2035 [21].

2.1.3 The GCC Energy Scenario

The GCC region accounts for about 45% of the world’s proven oil reserves and 25% of the world’s oil

exports. It possesses around 18% of the proven global natural gas reserves [22]. Driven by strong

economic growth, rapid industrialization and infrastructure development and investment in the energy

sector, this region’s energy consumption has increased at a tremendous rate. In 2005, total energy

consumption was 275 Mtoe which increased to 389 Mtoe in 2011 at an average growth rate of about

6.85% per year [23].

Electricity consumption in the GCC countries has also increased at a fast rate: 12.4% from 2005 to 2009

(3.15% per year). The rate is much higher than the world average of 2.2% for the same period [4].

Average per capita electricity consumption in the GCC region was 10,976 kilowatt-hour (kWh) in 2009,

which was 3.9 times more than the world average of 2,806 kWh in 2009 [24].

In 2006, the total electricity production in the GCC was about 324 TWh, which increased to 391 TWh in

2009 [24]. On this basis, it is estimated that the production growth is about 6.9% per year. Energy

demand is expected to continue increasing in line with growing industrialization in this rapidly

developing region. The present generation capacity in the GCC countries is about 80 GW [25].

Considering current trends, the region must increase its electricity capacity by an additional 60 GW to

meet the demand by 2020. Some macroeconomic, energy and environmental indicators for the GCC

countries are presented in Table 1.

Table 1: Key indicators of the GCC countries and world average (2009-10) [24]

Key indicators Bahrain Kuwait Oman Qatar KSA UAE GCC World

GDP growth (%) 4.5 3.41 4 16.6 4.6 1.43 5.7 2.71

GDP per capita (Current USD) 18,184 62,664 20,790 72,398 16,423 39,624 38,347 9,157

Electricity production (TWh) 12.05 53.21 17.82 24.78 217 90.5 415.3 20,078

Electricity consumption per capita (kWh)

9,214 17,609 5,724 14,420 7,427 11,463 10,976 2,806

Energy use per capita (kWh) 93,936 132,263 64,426 172,967 683,00 99,620 105,246 20,764

Electricity production from gas (% total)

100 28.82 82 100 44.8 98.2 75.63 21.4

Electricity production from oil (% total)

0 71.17 18 0 55.2 1.8 24.36 4.8

Electricity production from renewable (% total excluding hydro)

0 0 0 0 0 0 0 3

Access to electricity (% population)

99.4 100 98 98.7 99 100 99.18 74

CO2 emission (metric ton per capita)

21.36 30.11 17.34 49 16.56 24.98 26.55 4.76

CO2 emission from electricity

and water (% total)

54.21 68.19 56.7 52 51.4 50.8 55.55 47.5

GCC Renewable Energy Readiness Report 2011 – 2012

13

CO2 intensity2 (kg per kg oil

equivalent) 2.43 2.75 2.78 2.97 2.81 2.65 2.73 2.53

In the context of such significant need for new capacity, the GCC region has a unique opportunity to

channel future investment into the deployment of renewable energy technologies (RETs), thus

enhancing future energy security and reducing GHG emissions. The integration of RETs in the power

sector through nationwide energy planning would enhance not only the sustainable development of the

GCC region, but would also integrate the GCC’s efforts into the broader global effort to address the

challenges of climate change.

2.2 Deployment of Renewable Energy Technologies

Renewable energy plays an important role in the process of integrating the environment into energy

policies through its potential to contribute to the objectives of sustainability. Renewable energy-based

power generation generally emits no GHG’s during operation, with the notable exception of biomass-

based power plants, which are neutral over their complete life-cycle in terms of GHG emissions.

Renewable energy resources can contribute significantly to the security and diversity of a nation’s

energy supply mix by providing a secure, indigenous source of energy that is available in a variety of

forms [26].

Renewable energy benefits have created a strong motivation for pursuing RETs in both developed and

developing countries. During the global financial crises in 2009, renewable energy continued to grow to

supply 16.7% of global final energy consumption in 2010 [27]. Of this total, modern renewable energy

accounted for an estimated 8.2%, a share that has increased in recent years, while the share from

traditional biomass has declined slightly to an estimated 8.5% [28]. Global investments in RE continued

to surge, from USD 39.5 billion in 2004 to USD 244 billion in 2012 (UNEP, FSFM and BNEF, 2013).

Globally, electricity generation from renewable energy resources has been growing rapidly. During 2011,

renewables accounted for almost half of the estimated 208 gigawatts (GW) of electric capacity added in

the power sector globally. Wind and solar photovoltaics (PV) accounted for almost 40% and 30% of new

renewable capacity, respectively, followed by hydropower (nearly 25%). By the end of 2011, total

renewable power capacity worldwide exceeded 1,360 GW, up 8% over 2010; renewables comprised

more than 25% of total global power-generating capacity (estimated at 5,360 GW in 2011) and supplied

an estimated 20.3% of global electricity. Non-hydropower renewables exceeded 390 GW, a 24% capacity

increase over 2010 [28].

Solar PV grew the fastest of all renewable technologies during the period from end-2006 through 2011,

with operating capacity increasing by an average of 58% annually, followed by concentrating solar

thermal power (CSP), which increased almost 37% annually over this period from a small base, and wind

power (26%) [28]. Compared to the global 1.4% annual growth of conventional energy, worldwide

installed capacities of solar PV and wind power grew at 30% per year [29-31]. This has led to a significant

2 CO2 intensity refers to CO2 emissions per kg of oil equivalent of final energy use.

GCC Renewable Energy Readiness Report 2011 – 2012

14

reduction in the investment cost of solar PV and wind power generation. Figure 1 shows the growth of

renewable energy capacity from 2006 to 2011.

During 2011, China added 90 GW of electric capacity (70 GW of which was non-hydro) ending the year

with an estimated 282 GW, more renewable power capacity than any other nation. The top seven

countries for non-hydro renewable electric capacity—China, the United States, Germany, Spain, Italy,

India, and Japan—accounted for about 70% of total capacity worldwide. The ranking was quite different

on a per capita basis, with Germany in the lead followed by Spain, Italy, the United States, Japan, China,

and India [28].

Figure 1: Average annual growth of renewable energy capacity, 2006-2011, adopted from [28]

2.2.1 Drivers and Barriers to the Deployment of RETs

National governments tend to increase the deployment of RETs for the following three interlinked

reasons [2]:

1) To improve energy security.

2) To encourage economic development with innovation and high-tech manufacturing.

3) To protect the climate and the wider environment from the impacts of fossil fuel use.

Despite the exhibited performance of RETs worldwide and their significant environmental benefits, it

has not been possible to tap their full potential. This is due to the various barriers, relating to

infrastructure, market conditions, human capital both institutional and regulatory [9, 32-36], which all

impede the diffusion and continued growth of RETs.

Renewable energy must compete with financial and regulatory systems that have evolved to promote

the development and use of fossil fuels, and often discriminate against the use of RETs. Furthermore,

0% 10% 20% 30% 40% 50% 60% 70% 80%

Solar PV

Concentrated Solar Power (CSP)

Wind power

Solar thermal

Ethanol production

Biodiesal production

Hydropower

Geothermal power

% Growth Rate

End 2006 to 2011 2011 only

GCC Renewable Energy Readiness Report 2011 – 2012

15

the one major barrier to RETs is their relative cost. Costs are closely tied to the development of markets

and technical progress.

The cost of solar PV has been falling consistently over the last three decades, exhibiting a learning curve

with a cost reduction rate of 19.3% [37] for every doubling of solar PV capacity. This is partly driven by

the increase in the efficiency of solar PV and improvements in market conditions favorable to RETs.

Availability, affordability (price volatility and price uncertainty) and sustainability of energy supply are

interlinked aspects of an overall energy system that can significantly influence deployment.

Global new investment in renewables rose 17% to a record USD 257 billion in 2011. This was more than

six times the figure for 2004 and almost twice the total investment in 2007, the last year before the

acute phase of the recent global financial crisis. This increase took place at a time when the cost of

renewable power equipment was falling rapidly and when there was uncertainty over economic growth

and policy priorities in developed countries [28].

2.3 Potential Renewable Energy Jobs in the GCC Countries3

Investment in the development of RETs in GCC countries provides an opportunity for a number of key

benefits, one of which is the potential for job creation across the full renewable energy value-chain,

including R&D, manufacturing, installation, operation and maintenance and decommissioning. Several

studies indicate that there is considerable potential for gross job creation in renewable energy and that

the number of jobs generated per dollar of investment or per unit of capacity is generally higher in

renewable energy than in fossil fuel generation. While the extent of employment effects may be

debated, most studies suggest that renewable energy deployment may also be associated with net job

creation, although the magnitude will vary by country and by sector. Similarly, the number of jobs

created in the GCC countries will depend on a range of factors, including the success of deployment,

existing industry, labor skill and availability, training and education policy, as well as the multiplier

effects of deployment on the rest of the economy.

Unemployment is a challenge in the GCC region and could potentially threaten the high standards of

living. In particular, high population growth rates, unattractive private sector opportunities and the

relative lack of required skills among the local graduates have resulted in a significant employment

problem for GCC youth4. As such, policy makers have been considering different ways to generate jobs,

as well as shift part of the workforce away from government jobs into fast-growing new industries

outside of hydrocarbons, including the renewable energy sector.

Indeed, national renewable energy targets indicate that most countries in the GCC are planning to add

significant renewable energy based capacity in the next couple of decades. Given that all countries have

ample solar resources available throughout the year, the main focus of investment is expected to be

solar energy (PV in particular). This is also reflected in the existing and planned projects in the GCC.

3 This section is contributed by Rabia Ferroukhi and Arslan Khalid, Knowledge, Policy and Finance Centre, IRENA.

4 Unemployment rates are significantly higher in the 19-25 age groups: 30% in Saudi Arabia, 24% in the UAE, 28%

in Bahrain, 23% in Oman, and 12% in Kuwait; as opposed to the overall unemployment rates of 10.5% in Saudi Arabia, 14% in the UAE, 8% in Bahrain and Oman and 6% in Kuwait.

GCC Renewable Energy Readiness Report 2011 – 2012

16

Encouragingly, studies also indicate that when comparing between renewable technologies with

different capacity factors (employment per unit of energy), PV technologies account for the highest

number of job-years per GWh over the lifetime of a facility [38].

Realization of the announced renewable energy targets in the GCC region can potentially lead to

significant job creation along the value chain in the GCC countries, which can be estimated more

precisely using different available methodologies. Based on a simple employment factors methodology,

preliminary analysis shows that the renewable energy capacity in GCC can reach 20 GW by 2020 and 60

GW by 20305 [39], generating 0.6 and 1.8 million (gross) jobs by 2020 and 2030, respectively. More than

90% of these jobs will be generated in the solar energy sector, where the dominant share of jobs

created is generally concentrated in the manufacturing and construction6 stages of the supply chain

(discussed in Section 5.1.4.4). It must be noted that the share of local jobs will eventually depend on the

degree of localization (domestic vs. foreign) of some of the key stages of the supply chain (in particular,

manufacturing). Therefore, fostering the domestic growth of these stages should be essential in the list

of priorities of GCC governments.

In order to create a market for renewable energy and facilitate the development of the local renewable

energy supply chain, regulations and policies will play a very import role. A stable, thriving and

predictable renewable energy demand is an essential factor for attracting sizeable private investment in

a local renewable energy supply chain. Therefore, deployment policies that create a significant local

renewable energy demand (public or private), are very important in generating renewable energy

related jobs. In addition, capacity building activities that develop the necessary skills and understanding

among the stakeholders7, coupled with conducive labor policies, can facilitate the shift of labor resource

towards renewable energy.

Several studies suggest that demand for PV or wind power can lead to significant job creation through

installation and maintenance activities given that appropriate capacity building initiatives are applied.

However, in order to create jobs throughout the renewable energy supply chain, GCC countries can

adopt various industrial policies that encourage the development of the domestic industry from the

demand and the supply side.

On the demand side, incentives such as local content requirement can be a key tool to establish

manufacturing facilities by generating the demand for local equipment and services. On the supply side,

governments can support the establishment of manufacturing facilities by providing guarantees and low

cost financing; promoting research and development; arranging transfer of technology; training human

capital; and if possible, providing additional demand by facilitating export of the domestic equipment

and capabilities [40]. Finally, government can further promote the establishment of the renewable

5 It is assumed that the share of the RE technologies are the following: 60% PV, 30% CSP, 5% wind and 5% waste to

energy. 6 In general this applies to fossil fuel-based technologies, feedstock production and distribution of biofuels account

for the largest share of jobs. 7 Training and skill development program for stakeholders including workers, investors, financers and politicians.

GCC Renewable Energy Readiness Report 2011 – 2012

17

energy supply chain through direct public investment in flagship projects and/or public private

partnerships.

Of particular relevance in the enabling policies that would ensure job creation from renewable energy

deployment are renewable energy education and training. Strong skills development initiatives need to

be undertaken to build a critical mass of technical skills to ensure the sustainability and long-term

success of renewable energy industries.

To achieve deployment targets and maximize job benefits, it will be necessary to facilitate increased

renewable energy education and training. It is, therefore, advisable to conduct skills mapping exercises

to identify existing skill and knowledge-related gaps in the GCC region. This should then be used to

develop appropriate training and education policies and to make sure that vocational training and

curricula are in line with industry needs.

In the development of policies to support job creation in renewable energy, the following aspects should

also be considered: the state of existing skills should be accounted for when formulating deployment

and industrial policies; services should be provided to help match jobs and workers; and job creation

should be focused in areas/demographic groups with low employment. The efforts mentioned above

will be especially needed given that the GCC relies heavily on skilled labor from overseas, without always

ensuring that skills are transferred to local people [40].

Significant efforts are already being undertaken to increase renewable energy education. The flagship

research institutes of the Masdar Institute of Science and Technology and the King Abdullah University

of Science and Technology (KAUST), for example, have become state-of-the art higher education

facilities that provide both local and foreign students with the necessary training needed to carry

forward the dream of a renewable energy future in the GCC. Among several other educational and

research initiatives in Qatar, Qatar University, along with implementing renewable energy related

teaching, has established a teaching laboratory in collaboration with the German Heliocentric Energy

Solutions company to provide practical knowledge in the fields of solar and wind energy generation

systems and storage. The Qatar Environment and Energy Research Institute (QEERI) is conducting

research on various energy and environmental issues with special focus on solar energy. The Kuwait

Institute for Scientific Research (KISR) is financing research projects on solar energy systems and their

technical feasibility in the country, in which more than 70 researchers, engineers and technicians are

trained and involved. Dhofar University in Oman has launched projects integrating renewable

technologies into academic programs and into students’ course curricula, thus providing graduates with

knowledge in renewable energy systems and design aspects of related projects.

Clearly there is significant potential for job creation along the value chain in the GCC to meet announced

renewable energy targets. However, as explained above, sustainable job creation in the GCC will require

going beyond a deployment policy to also introduce the appropriate labor, education/training, and

industrial policies required to create the overall enabling environment. Assuming there are net

employment benefits from deploying renewables, the jobs created will be most cost-efficient when

support policies are holistic, stable, consistent, and long-term.

GCC Renewable Energy Readiness Report 2011 – 2012

18

3 Energy Demand and Renewable Energy Development Initiatives in the GCC

Countries

This section discusses the energy demand, consumption and the status of RET development initiatives in

each GCC country.

3.1 Bahrain

Population and economic growth have led to a very high estimated annual energy growth rate of 10% in

Bahrain. In 2008, the total installed power generation capacity was 2,780 megawatts (MW) [25]. It is

expected that a total capacity of 6,500 MW will be required by 2030 to meet the projected demand [41].

With an installed capacity that is not always able to meet current demand, causing occasional power

outages, this small nation will need to double its natural gas supply in less than a decade to meet the

growing demand [4] or diversify its energy supply through careful consideration of alternative energy

sources.

3.1.1 RET Development Initiatives

Bahrain installed three wind turbines at its world trade center that meet 13% of the building’s energy

demand. The country has a pilot solar energy street lighting project that was implemented by the

Electricity and Water Authority (EWA).

Initiatives by the Bahrain Government to evaluate the renewable resources include the assignment of

Petro-solar an American company to assess the potential of solar energy. In July 2011, Bahrain signed a

contract with Fichtner Consulting Engineers of Germany to prepare a detailed techno-commercial

feasibility study for solar and wind energy resources [42]. The EWA of Bahrain also conducted an

assessment of solar and wind energy resources. The authority observed the possibility of using these

resources for production of electricity and desalinated water.

The following are the planned and conducted renewable energy projects in Bahrain:

1) Bahrain Petroleum Company’s (BAPCO) first zero emissions house built with a hybrid energy

system with total capacity of 7 kW (hybrid: solar, wind and fuel cell). BAPCO had formed an

administration team consisting members from universities and energy utilities, responsible for

the oversight and promotion of RET projects in Bahrain.

2) In 2009, a 5 MW capacity solar and wind project was announced to be installed. Bidding for the

project is being organized by the EWA.

3.2 Kingdom of Saudi Arabia

The KSA’s rapid economic growth is closely linked to its per capita energy consumption which has

increased by more than 30% since 2010 [43]. This significant increase in internal energy consumption

has caused a gradual decrease in oil exports. In 2008, oil met 60% of total energy consumption (about

800 million barrels of oil equivalent). Current trends show that energy consumption in the KSA is

expected to double in 2030, which will inevitably lead to diminished oil exports [43].

GCC Renewable Energy Readiness Report 2011 – 2012

19

KSA’s power generation capacity grew 11.8% reaching 51.2 GW by 2009. Population growth and

economic expansion, are projected to increase demand for electricity capacity to 77.4 GW by 2020 [44].

3.2.1 RET Development Initiatives

The KSA made the first step in the region in the 1970’s by founding the King Abdulaziz City for Science

and Technology (KACST) and funding R&D projects including renewable energy. Despite having the

largest oil reserves in the world, the Kingdom is focusing heavily on solar energy projects, with an early

emphasis on water heating and electrification in off-grid remote areas.

In 2009, the KAUST was founded to turn the country into a key energy research hub and to develop

renewable and sustainable technologies through cooperation with global scientific bodies. However, the

renewable energy sector is still somewhat immature in the KSA. No comprehensive technical or techno-

economic feasibility studies based on local conditions have been performed yet.

In May 2010, the governor of the Saudi Electricity and Cogeneration Authority announced a framework

that set out the conditions of government funding and incentives for the development of the renewable

energy sector. A feed-in tariff based is expected but has not yet been implemented.

In April 2010, the King Abdullah City for Atomic and Renewable Energy (KA-CARE) was founded by a

Royal order with a mandate to contribute towards sustainable development through implemention of

nuclear power plants and renewable energy projects to diversify energy supply and minimize CO2

emissions. It aims to exploit the country’s abundant natural resources to reach a sustainable energy

supply mix. Its intention is to strengthen Saudi Arabia's ability to meet future international oil demand

for the development of technology and human capacity. These require the establishment of an

important new economic sector focused on alternative energy.

In April 2011, the KSA announced that it would invest USD 100 billion in renewable and nuclear energy

to reduce its dependence on crude oil and to achieve 7-10% electricity generation from RETs by 2020

[44].

3.2.2 Initiatives for Reducing Supply Side Energy Consumption8

The KSA has taken the following initiatives to reduce energy consumption on the supply side [43]: 1)

modernization of existing power plants, 2) minimum efficiency standard for new power plants, 3)

minimum overall efficiency standard for co-generation desalination plants, and 4) implementation of a

renewable energy program to displace fossil fuels.

3.2.3 Renewable Energy Program to Displace Fossil Fuels

Analysis of solar resource assessment studies show that there is a great potential for solar energy in the

KSA. A solar photovoltaic area of 22–40 km2 in Saudi Arabia can produce as much electricity as a 1,000

MW oil-fired power station [43]. Studies suggest that if subsidy on oil is removed, at current oil prices

(assuming USD 80/barrel), electricity from PV in Saudi Arabia can be more competitive than electricity

from oil-fired power generation. An estimate done by this section contributor shows that in order to

8 This section is contributed by Yousef M. Alyousef, Director, Energy Research Institute, King Abdulaziz City for

Science and Technology, Riyadh, Saudi Arabia.

GCC Renewable Energy Readiness Report 2011 – 2012

20

stimulate PV in the country, an incentive equivalent to approximately USD 0.17 /kWh needs to be

introduced.

Our review of renewable energy options for the KSA also advocates a great potential for solar thermal

applications. Concentrated solar power (CSP) electricity generating systems can achieve conversion

efficiencies of 18-30%. Solar absorption cooling, where thermal energy from the sun is used for re-

generation in absorption chillers, is another possible application.

Despite its great potential, the wide scale deployment of solar energy in the KSA faces several barriers.

These include lack of incentives, high costs (considering current subsidies on oil), the need for more

public knowledge and professional training. It is assessed that 5 GW of solar PV installation has the

potential to save about 55 TWh per year in the KSA, leading to savings of about 2.8% compared to the

base case.

3.3 Kuwait

Kuwait is the fifth largest oil producer in the Organization of the Petroleum Exporting Countries (OPEC).

Oil and natural gas are the main available primary energy resources in the country. Energy consumption

is increasing at a rate of 8% annually [45].

In 1958, the first power plant was installed with a capacity of 15 MW; the total installed capacity grew to

11.6 GW by 2008. It is expected that by 2020 a total capacity of 23 GW would be needed to meet the

projected demand of electricity [44].

3.3.1 RET Development Initiatives

The country is richly endowed with solar energy. Kuwait has set an ambitious renewable energy

production target, which aims to generate 10% of its electricity from sustainable sources by 2020 [46].

Another initiative was the establishment of the renewable energy program by the Kuwait Institute for

Scientific Research (KISR). The KISR undertakes studies on feasibility of deploying renewable energy in

Kuwait. It focuses on regulations and policies that government needs to set up to promote renewable

energy development. As part of renewable energy resources assessment efforts, a study by the Japan

External Trade Organization was commissioned by the Ministry of Economy, Trade and Industry of

Kuwait in 2008. The study assessed technical, economical and operational aspects of combined cycle

power generating system using solar thermal energy.

Several pilot projects in wind, solar PV and solar thermal technologies have been completed by the KISR.

Some of these projects are: solar heating and cooking with different thermal storage configurations,

solar cooking project with 172 solar collectors covering a total area of 300 m2, thermal and electricity

application projects including Kuwait English School (Salwa) with daily electricity load of 80 kWh, 630 PV

modules and 110 batteries with electricity production capacity of 24.2 kW, KISR’s solar house with 76 PV

modules, 48 batteries and electricity production capacity of 2.6 kW, solar power plant at Sulaibia

complex with 56 power production of 125 kW. In addition, the following renewable energy projects

have been announced [4]:

GCC Renewable Energy Readiness Report 2011 – 2012

21

1) A joint project of 15 MW wind power has been proposed by KISR and Germany to install in

Kuwait. Another project of 5-10 MW solar power is to be installed.

2) The country is also working with a Japanese company in order to assess economic feasibility of

solar power plants in Kuwait.

3.4 Oman

Expansions of industrial and population growth have put a strain on Oman’s power sector infrastructure.

In 2010, total peak electricity demand in Oman was 3,856 MW, a 46.4% increase since 2005 [44]. The

peak demand is expected to grow at an annual rate of 8% and is projected to reach about 6,600 MW by

2018 [47].

3.4.1 RET Development Initiatives

The Authority for Electricity Regulation (AER) of Oman has outlined a roadmap for the Development of

Renewable Energy Projects. The AER published a report called “Study on renewable energy resources,

Oman” in 2008. The study recommends several pilot projects of RETs [48]: 1) 10 kW off-grid solar

PV/diesel hybrid system; 2) 20 kW grid-connected solar PV system; and 3) 10 MW grid connected wind

power farm. The criteria for selection of the recommended pilot projects types include:

1) Demand for these types of projects is expected in the near future.

2) The projects are expected to be economically viable in the future.

3) The projects shall contribute to the awareness of renewable energy.

4) The projects are based on well proven and reliable technology.

However, as of yet none of the recommended projects have been confirmed. Oman has recently floated

a tender for a concentrated solar power plant between 50 MW and 200 MW capacity. Special attention

has been given to look for a suitable policy framework and develop institutions to promote renewable

energy investments under clean development mechanism (CDM).

3.5 Qatar

Qatar’s economic growth is estimated to increase by 10% annually over the next 5 years, and to

continue growing at a slightly lower rate of 7% in subsequent years [49]. The economic growth is driven

by rising energy prices and higher exports of liquefied natural gas (LNG). Almost one third of the Middle-

East’s total conventional gas reserves are in Qatar, which also has a world share of about 12% [50].

Revenues generated from tapping this resource are used to develop the country's infrastructure,

education and health facilities as well as modern hydrocarbon operations.

In the year 2000, the country’s peak electricity demand was only 1,800 MW, this figure reached 8,000

MW by the year 2011. Electricity demand growth in recent years has been about 5.1% [4]. By 2030,

Qatar’s electricity generation is projected to continue growing at an annual rate of 2.9%. The country’s

primary energy demand is projected to grow at a moderate rate of 5.2% annually.

3.5.1 RET Development Initiatives

The government of Qatar is committed to diversifying its economy and to reducing its dependency on

fossil fuels. Qatar hosted the 18th United Nations Framework Convention on Climate Change (UNFCCC)

GCC Renewable Energy Readiness Report 2011 – 2012

22

Conference of Parties (COP18) in Doha from November 26 to December 7, 2012. The COP18 marks the

beginning of negotiations for a global agreement. With the international spotlight shifting to the region,

COP18 provided an unprecedented opportunity for the GCC countries to contribute their ambition and

combined experience to the world’s most complex intergovernmental efforts. The conference was

especially important given the inseparability of the global climate and energy challenges. As the first

Gulf country to host the talks, Qatar presented an opportunity to overcome differences between energy

exporters and importers and drive forward practical, mutually beneficial solutions.

Qatar announced to host a carbon neutral Football World Cup in 2022. Although, the country has no

renewable energy goals or policy mechanisms yet [36], Qatar proposed the newly built stadiums for the

event be solar powered and suggested that solar power will be connected to each of the stadiums’

electrical systems and national grid.

The Qatar National Food Security Programme (QNFSP) recently launched a solar resource assessment

project. The project is to be conducted by the German Aerospace Centre (DLR) to identify the country’s

most favorable areas for solar energy projects. Additionally, the following are the planned renewable

energy development projects in Qatar [4]:

1) On January 7, 2010, the country announced plans to invest about USD 1 billion in solar power

projects, and to install at least 100 MW of solar power in the next five years.

2) Over USD 500 million will be invested by Qatar Foundation to establish a polycrystalline silicon

plant. The Qatar Science and Technology Park will develop a new plant at Ras Laffan Industrial

City that will be one of the first operational polycrystalline silicon plants in the GCC region.

3) Chevron will test solar panels and energy-efficient lighting in Qatar.

4) The Center for Sustainable Energy Efficiency is expected to open soon. The center aims to

identify solar power, solar air-conditioning and low-energy lighting technologies for Qatar.

In 2012, Qatar published Qatar’s National Research Strategy (QNRS) and a strategic plan for

implementation. The strategy reflects input from Qatar’s researchers, leadership and other

stakeholders. The strategy addressed some important pillars for R&D such as enterprise, energy and

environment, computer science and information technology, health and social sciences. Energy and

environment pillar goals and objectives identified there-in are as follows:

1) Sustain economic prosperity through oil and gas diversification.

2) Achieve sustainable development through economic diversification, including solar energy and

alternative fuels.

3) Energy efficiency for improvement of energy use.

4) Protecting Qatar’s natural environment.

5) Environmental sustainability.

6) Addressing global climate change.

7) Cross-cutting basic research and applications.

GCC Renewable Energy Readiness Report 2011 – 2012

23

3.5.2 National Research Funding Mechanisms9

Qatar launched the Qatar National Research Fund (QNRF) to support its strategic development plans.

QNRF funds a broad range of subjects that align with the themes and objectives listed in QNRS

(discussed in the previous section) via two flagship programs namely; National Priorities Research

Program (NPRP) and NPRP-Exceptional Program (NPRP-EP).

The NPRP grant offers competitive funding with a maximum budget per proposal of USD 350,000 per

year for up to three years (total USD 1.05 million). Lead Principal investigators (PI) from outside of Qatar

may identify a co-lead PIs inside Qatar with whom they can submit joint project proposals.

The NPRP-EP, grants only proposals that carry exceptional scientific merit, with a total budget of up to

USD 5 million for projects with a duration of up to five years.

3.6 United Arab Emirates

Although, the UAE has an abundance of natural resources, possessing 9.3% of the world’s proven oil

reserves and 4.1% of the world’s proven gas reserves [51], the relatively high energy demand and

current constraints on exploiting domestic gas reserves has led the country to become a net importer of

natural gas since 2007 [44].

Power generation in the UAE is almost entirely dependent on fossil fuels, with natural gas accounting for

98% of the total installed capacity in 2009 [24]. With the cost of natural gas heavily subsidized to

produce electricity for the utilities [9], low energy costs and high economic and population growth rates

have driven the country’s energy consumption to rise tremendously in the past decades [52]. The annual

electricity demand growth in recent years has been about 9% [53, 54].

3.6.1 RET Development Initiatives

Despite the UAE’s natural gas and oil reserves, the country has made significant commitments to

alternative energy development. The UAE is among the first major oil-producing countries to ratify the

Kyoto Protocol of the UNFCCC in 2005 with other GCC countries excluding Bahrain which ratified in

2006.

The Emirate of Abu Dhabi has established one of the world’s most comprehensive clean energy

initiatives through the Masdar Initiative. It has set target of 7% of electricity generating capacity from

renewable energy by 2020. The Abu Dhabi Climate Change Policy Plan proposes that Abu Dhabi will

generate electricity by 10% from renewable energy by 2030 [51]. IRENA’s headquarter were established

in Abu Dhabi after the emirate won the bid to host the international body. Abu Dhabi also hosts the

World Future Energy Summit every year. The Summit brings together some of the world's most

influential stakeholders across the renewable energy sector and encourages the development of RE

related human capital for the region. This initiative showcases Abu Dhabi’s commitments to the

deployment of renewable energy.

9 This section is contributed by Abdul Sattar Al-Taie, Executive Director, Qatar National Research Fund (QNRF),

Qatar Foundation, Qatar

GCC Renewable Energy Readiness Report 2011 – 2012

24

Dubai has set a target of 5% renewable energy generating capacity by 2030 (1000 MW). Both emirate

level governments are creating policies and incentive frameworks to deliver their targets.

The UAE Solar Atlas has been commissioned to provide valuable technical data for setting up solar

energy projects in the country. The UAE Solar Atlas is the outcome of the agreement signed between

Masdar Institute and IRENA. The agreement announced at the World Future Energy Summit 2012 in Abu

Dhabi also covers exchange of information; joint implementation of project activities, analyses and

research studies; as well as defining technical compatibility and methodological harmonization and data

transparency protocols for solar and wind data.

Existing RET projects in the UAE include a 10 MW PV plant in Masdar City, Abu Dhabi and the recent

Shams 1 project, a 100 MW CSP plant in the western region of Abu Dhabi. Other planned RET projects in

the country include:

100 MW PV plant

28.8 MW wind plant

100 MW waste-to-energy plant

The Dubai Supreme Council of Energy launched the Emirates Energy Award in 2012-13. It is an

international prize that will be awarded every two years to encourage rational use of energy and energy

resources. The award aims to reward best practices and leading initiatives in pursuit of alternative

energy, energy efficiency, sustainability and environmental protection.

Another notable effort on part of the UAE, is the annual Zayed Future Energy Prize to honor

outstanding, innovative achievements and governance or leadership in the global search for a

sustainable energy future.

4 Methodology: Framework to Assess Renewable Energy Readiness

The RE-readiness assessment framework has been developed by identifying the dominant barriers and

supporting mechanisms for the deployment of RETs and then proposing ways to quantify and rate those

factors. The framework defines the factors along the pillars of infrastructure, institutions, and human

capital. Each factor is assigned a weight and a score between 1 and 7, with 1 being the lowest and 7 the

highest score.

The scoring criteria for some factors and sub-factors can be initially assessed from a qualitative range of

“poor” to “very good” and then translated into a score from 1 for “poor” to 4 for “very good”. These are

then normalized into a score between 1 and 7. The scores are: 1 (poor), 2 (fair), 3 (good) and 4 (very

good), corresponding to 1, 2.33, 4.66 and 7, respectively. For other factors and sub-factors that are

related to quantitative data, this study applied different quantitative techniques to get an RE-readiness

score from 1 to 7. These techniques or assessment methods are explained in the following sections of

analysis of renewable energy readiness factors.

GCC Renewable Energy Readiness Report 2011 – 2012

25

The factors and sub-factors data relating to the deployment of RETs was provided by the team members

of this report from their respective GCC countries. A questionnaire (given in appendix 1) was supplied to

the report team members to collect data related to the deployment of RETs. After gathering all

quantitative and qualitative data, this study applied different scoring techniques to obtain an RE-

readiness score for each factor and sub-factor.

This scale range is adopted to align with the scale of the Global Competitiveness Report (GCR)

developed by the World Economic Forum [55]. Table 2 provides an example of global competitiveness

scores for some factors of the GCC countries. The GCR measures countries’ competitiveness levels by

assessing their competitiveness factors and giving them a score between 1 and 7. Some of the factors of

the GCR, such as countries’ overall infrastructure, institutions, financial market development,

macroeconomic environment, higher education and training, were taken directly from the report, as

these factors are also relevant to the countries’ level of readiness to adopt renewable energy projects.

Other factors and sub-factors, such as access to renewable energy finance, power off-take

attractiveness, renewable generation target and current installed capacity, are taken from the Ernst &

Young (E&Y) renewable energy country attractiveness indices report [56]. However, this study applies its

own technique to finding the selected factors and sub-factor scores as discussed, based on the GCC

countries’ available data. The E&Y report provides long-term indices that are forward looking and take a

long-term view. The report is published quarterly and provides scores out of 100 for national renewable

energy markets and infrastructures and their suitability for RETs. Some additional factors and sub-

factors are also incorporated that are related to the development of RETs in this framework (Table 3).

Table 2: Global competitiveness scores* of the GCC countries [55, 57]

Global Competitiveness Index (GCI)-pillars

Bahrain Kuwait Oman Qatar KSA UAE

GCI 2011-2012 4.5 4.6 4.6 5.2 5.2 4.9 Basic requirements 5.4 5.2 5.6 5.8 5.7 5.8 Institution 5.3 4.4 5.3 5.4 5.5 5.2 Infrastructure 5.1 4.4 5.2 5.2 5.3 6.0 Macroeconomic environment 5.1 6.6 6.5 6.4 6.1 6.1 Higher education and training 5.0 3.8 4.2 4.6 4.8 4.8 Goods market efficiency 5.2 4.3 4.8 5 5.2 5.2 Financial market development 5.1 4.2 4.7 5 5.1 4.6 Technology readiness 4.5 3.7 4.1 4.7 4.3 4.9 Innovation 3.2 3.0 3.4 4.7 4.2 4.0 * The score is out of 7. The higher the score, better the competitiveness of the country.

To determine the weights of different sub-factors that make up a given factor, or the factors that make

up a given pillar, the commonly utilized equal weights method [58] was applied, which weighs all

variables within one category equally. A list of the pillars, factors and sub-factors and related weights

are given in Table 3.

After determining weights, a multi-criteria decision making (MCDM) technique was applied to calculate

the final RE-readiness index for each country. The MCDM technique provides solutions to problems

GCC Renewable Energy Readiness Report 2011 – 2012

26

involving multiple conflicting objectives [59]. The MCDM is a general class of operations research models

that deals with problems involving a number of decision criteria. In this report, the weighted sum

method is applied [58] to obtain a final RE-readiness index.

This study combines the various methodologies to determine a final RE-readiness index (Figure 2). This

study also applies a SWOT analysis to find the strengths, opportunities, weaknesses and threats for the

diffusion of RETs in the GCC countries. Finally it recommends some priority areas for research and

development in this region towards sustainable development for the longer term.

Table 3: RE-readiness framework factors and respective weight

Pillars, Factors and sub-factors Weight (within immediate parent category)

Pillar 1: Infrastructure 33.34%

1.1 Natural resources 20% 1.1.1 Conventional resources 50% 1.1.2 Renewable energy potential 50% 1.2 Country overall infrastructure 20% 1.3 Existing grid capacity 20% 1.4 Market infrastructure 20% 1.4.1 Goods market efficiency 20% 1.4.2 Market deregulation/power sector reform 20% 1.4.3 Current installed capacity of RETs 20% 1.4.4 RE supply chain and operation & maintenance facilities 20% 1.4.5 Power off-take attractiveness 20% 1.5 Electricity access rate and projected demand 20% 1.5.1 Projected electricity demand growth 50% 1.5.2 Electrification rate 50% Pillar 2: Institutions 33.33%

2.1 Public and private institutions related on renewable energy 25% 2.2 Key policies 25% 2.2.1 Identified targets and policy mechanisms 34% 2.2.2 Institutional/electricity market regulatory framework 33% 2.2.3 Climate or CO2 emission reduction policy 33% 2.3 Access to renewable energy finance 25% 2.3.1 Financial market development 50% 2.3.2 Investment in renewable energy 50% 2.4 Macroeconomic environment 25% Pillar 3: Human capital 33.33%

3.1 Technical and commercial skills 34% 3.1.1 Higher education and training 25% 3.1.2 Capacity building 25% 3.1.3 Availability of renewable energy scientists and engineers 25% 3.1.4 Labor market efficiency 25% 3.2 Technology adoption and diffusion 33% 3.2.1 Technological adaption readiness 50% 3.2.2 Innovation and research & development 50% 3.3 Awareness among consumers, investors and decision makers 33% 3.3.1 Resource availability awareness 50% 3.3.2 Consumer and social awareness 50%

GCC Renewable Energy Readiness Report 2011 – 2012

27